AI In Clinical Documentation Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 3.05 Billion |

| Growth Rate (2026 - 2031) | 21.46% CAGR |

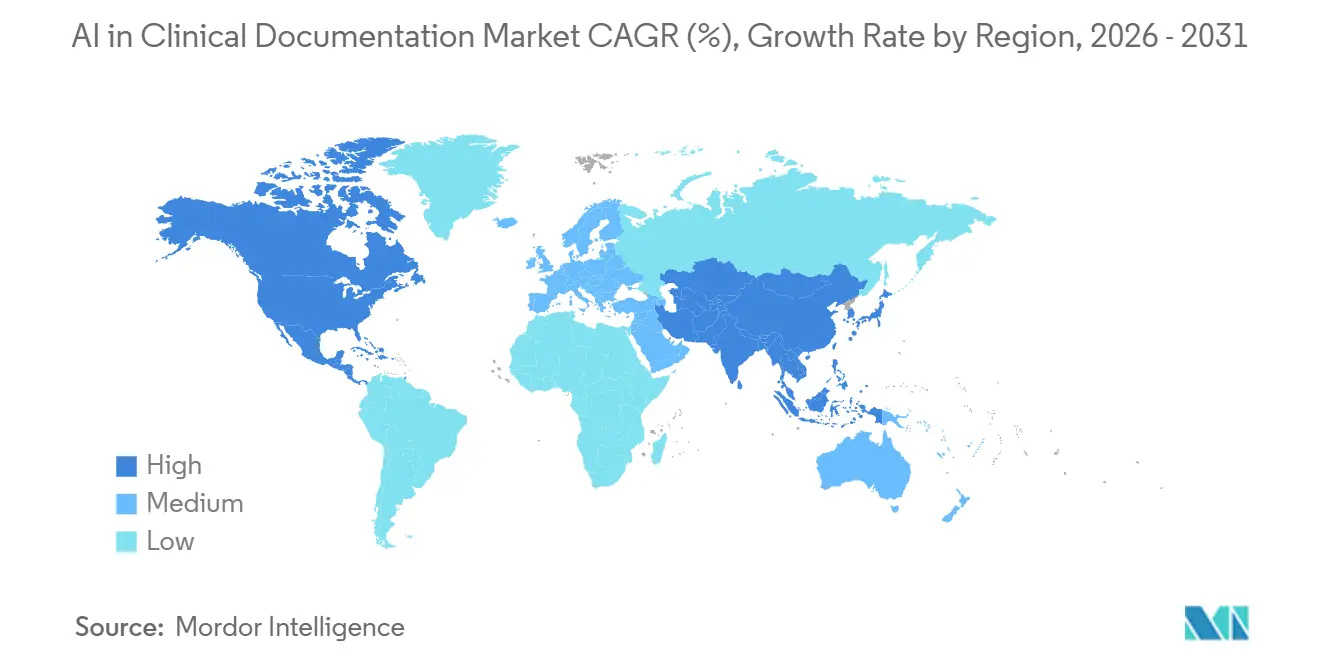

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Clinical Documentation Market Analysis by Mordor Intelligence

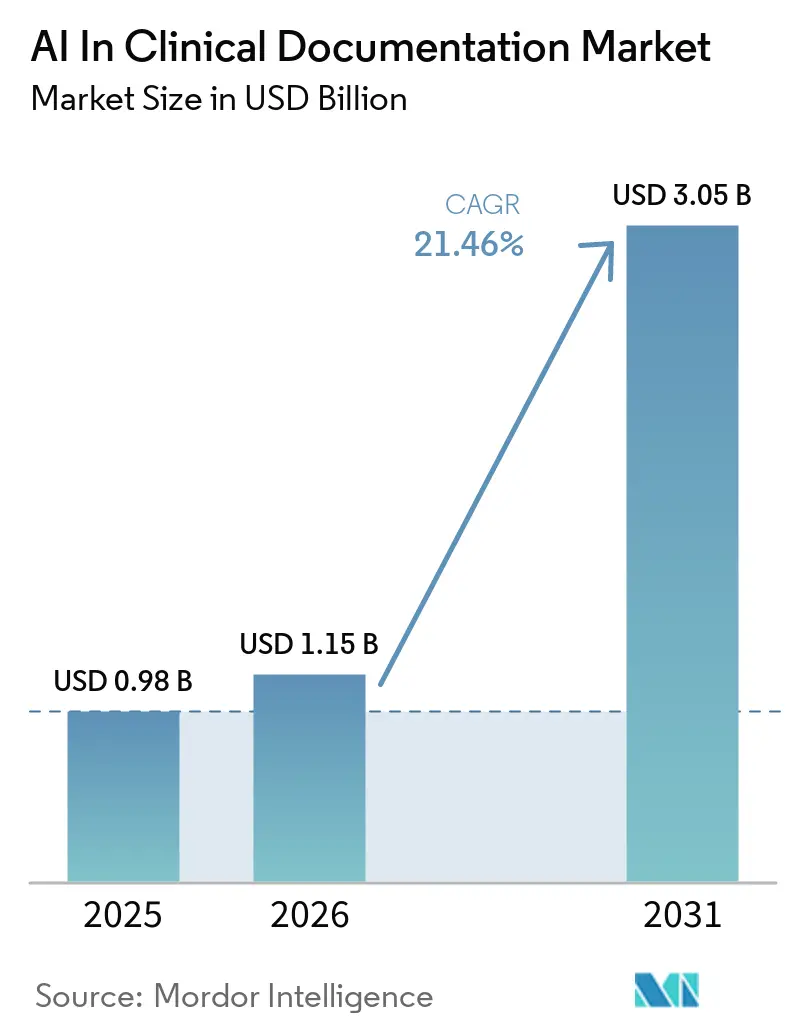

The AI in clinical documentation market size is expected to grow from USD 0.98 billion in 2025 to USD 1.15 billion in 2026 and is forecast to reach USD 3.05 billion by 2031 at 21.46% CAGR over 2026-2031. The growth profile reflects a structural shift from proof-of-concept pilots to enterprise-scale adoption that prioritizes EHR-native experiences, evidence-linked outputs, and unit-economics discipline around inference costs. Health systems are moving from basic dictation to ambient scribing and documentation integrity workflows that connect note quality to measurable revenue outcomes and shortened revenue cycles. Vendors are competing less on raw transcription accuracy and more on how automated notes integrate with order sets, coding specificity, and prior authorization readiness at the point of care. Regulatory momentum in 2026 around interoperability, transparency, and safety is reinforcing standards-based integrations and explainability features that make audit trails and clinician verification faster and easier. With enterprise buyers focusing on value capture and operating leverage, the AI in clinical documentation market is expected to favor platforms that compress token usage per note while maintaining clinical fidelity and traceability across diverse specialties and languages.

Key Report Takeaways

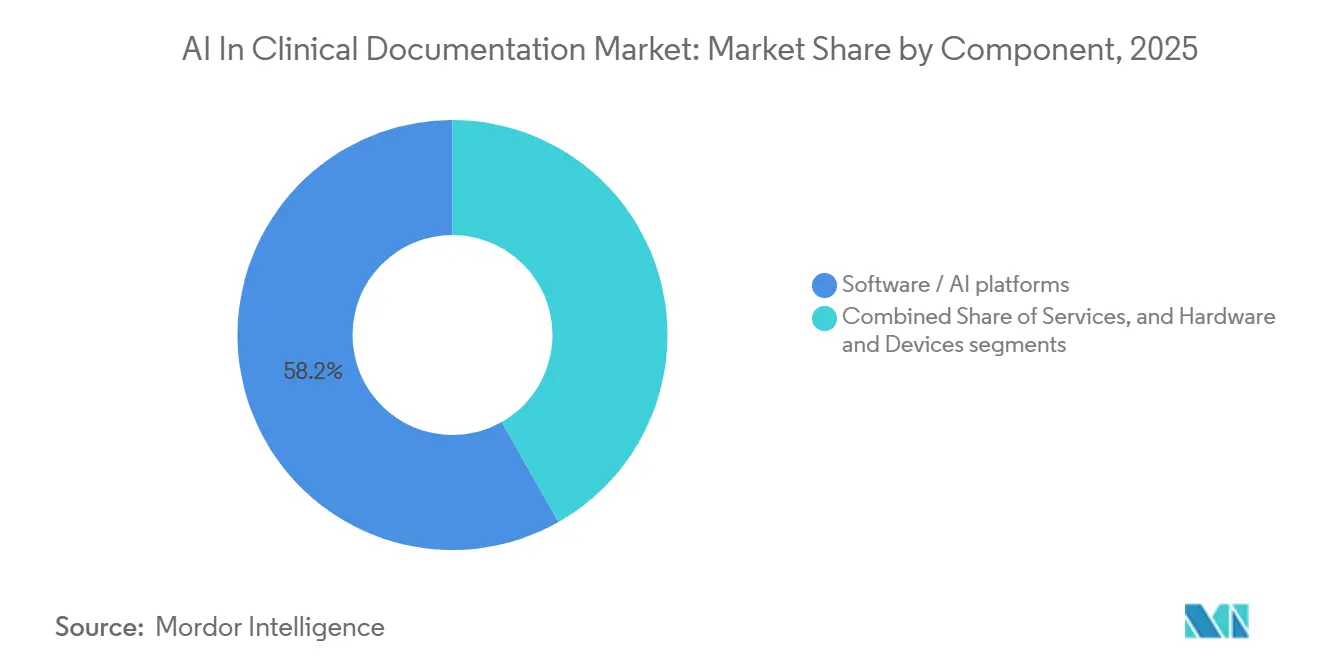

- By component, software/AI platforms led with 58.24% revenue share in 2025 and are projected to expand at a 23.44% CAGR through 2031.

- By deployment, Cloud/SaaS commanded 51.35% share in 2025 and recorded the fastest projected CAGR at 23.82% to 2031.

- By application, ambient clinical scribing accounted for 53.34% of the 2025 value, and CDI or CAPD is forecast to grow at a 23.41% CAGR through 2031.

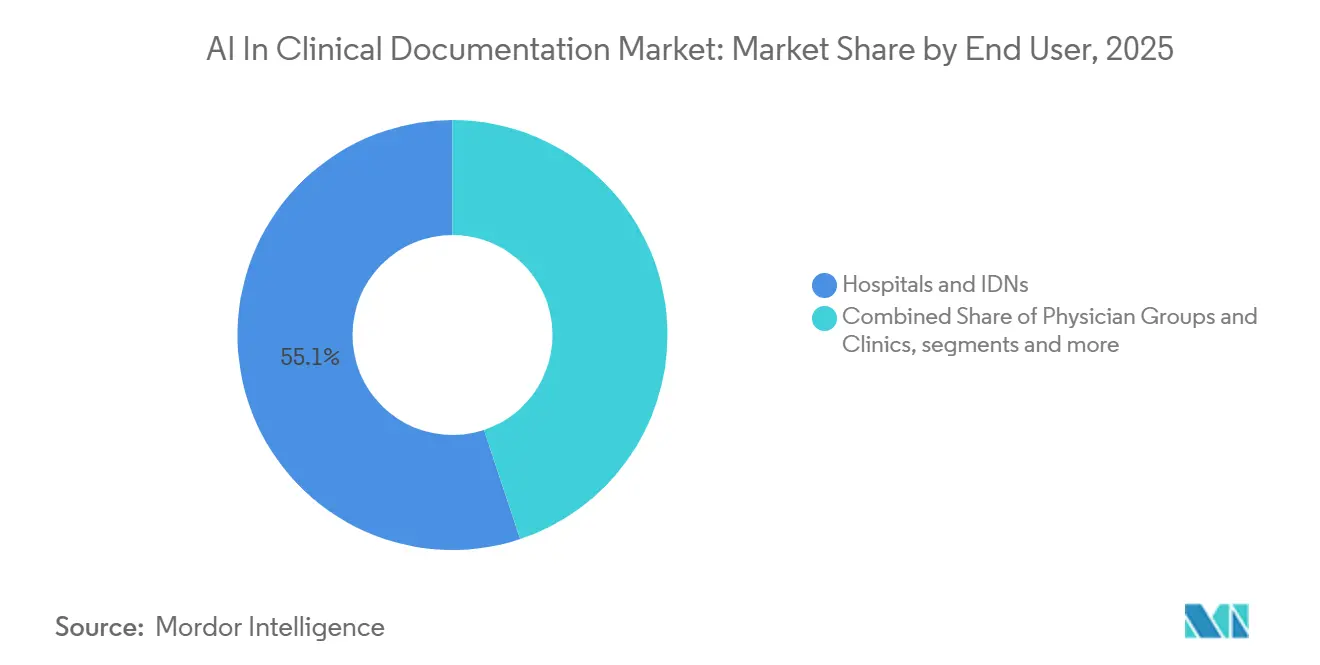

- By end user, hospitals and IDNs represented 55.13% of 2025 spending, and healthcare payers are the fastest-growing at 22.62% CAGR through 2031.

- By clinical setting, inpatient commanded 61.55% share in 2025, and outpatient is the fastest-growing at 22.31% CAGR through 2031.

- By geography, North America held 50.16% share in 2025, and Asia-Pacific is the fastest-growing region at 23.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Clinical Documentation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ambient Scribing And CDI/CAPD Reduce Documentation Burden and Increase Throughput | +5.2% | Global, with acute uptake in North America and Western Europe | Short term (≤ 2 years) |

| Deep EHR-Native Integrations Drive In-Workflow Adoption at Enterprise Scale | +4.8% | North America core, expanding to APAC (Epic or Oracle installs) | Medium term (2-4 years) |

| Accuracy Gains in Medical Speech Recognition and LLMs Elevate Note Quality and Speed | +3.7% | Global, with language-specific performance variance | Medium term (2-4 years) |

| Revenue Integrity and Audit Pressure Expand AI-Supported CDI/CAPD and Coding | +4.1% | North America and EU pilots | Short term (≤ 2 years) |

| Multilingual, Specialty-Tuned Models Open ED, Inpatient, and Complex Specialty Use | +2.9% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Enterprise AI Platforms and GPU Access Enable Bundled, Scaled Deployments | +3.6% | Global data-center hubs in North America, EU, and select APAC metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ambient Scribing and CDI or CAPD Reduce Documentation Burden and Increase

Throughput Ambient scribing moved into the clinical mainstream as organizations prioritized reduced after-hours charting and improved visit flow without adding staff. Evidence from ambulatory settings shows that AI-generated notes can reduce documentation time and improve perceived efficiency, which supports a shift toward higher daily visit volumes when clinicians absorb time savings into added patient slots rather than shorter workdays. Providers are pairing front-end ambient scribing with back-end CDI or CAPD reviews so that narrative notes are transformed into specific, auditable statements that support better coding and fewer downstream queries. Vendors report measurable uplifts in coded complexity and revenue integrity where AI suggests needed qualifiers and maps to ICD-10 and HCC codes with supporting rationales, reducing amended encounters and tightening cash cycles.[1]Suki Team, “Suki Supercharges Revenue Cycle with Next-Gen AI Coding,” Suki, suki.ai As prior authorization and interoperability rules emphasize timeliness and transparency in 2026, payers expect clinical submissions that are concise, structured, and traceable, making combined scribing and integrity checks a strategic lever at the point of care. The AI in clinical documentation market is therefore aligning product roadmaps around throughput, coding specificity, and explainability, which together reduce denial risk and create clearer financial returns for health systems and payers.

Deep EHR-Native Integrations Drive In-Workflow Adoption at Enterprise Scale

Adoption scales fastest when documentation support is embedded directly inside EHR workflows so clinicians do not toggle between external windows or re-enter data. Health systems are reporting smoother rollouts and higher sustained use where AI-generated notes, orders, and coding suggestions write back to the EHR with minimal clicks and clear evidence links, reinforcing trust and auditability. EHR-native or tightly integrated approaches also reduce IT lift because deployment, permissions, and clinical content are managed within existing governance and security frameworks. Integration depth matters more than marginal accuracy gains when frontline users seek fewer steps and fewer screen changes during time-pressed encounters, especially in specialties with complex templates. Environments that couple ambient capture with structured write-back can surface payer requirements earlier and reduce avoidable friction at discharge, referral, or prior authorization checkpoints. The AI in clinical documentation market continues to converge around standards-aligned integrations that keep the clinician in flow and convert audio and text into orders, codes, and patient instructions within the native system of record.

Accuracy Gains in Medical Speech Recognition and LLMs Elevate Note Quality and Speed

Medical speech recognition advanced with domain-tuned models that reduce word error rates and improve recall for clinical terms, providing a better substrate for downstream language models. A medical ASR model released in 2025 reported 93% transcription accuracy with fewer errors on terminology and strong keyword recall, a level that stabilizes the input for summarization and structuring tasks.[2] Speechmatics Team, “Speechmatics Launches Medical Model for AI Medical Speech Recognition,” Speechmatics, speechmatics.com Quality comparisons between AI-generated notes and clinician-authored notes show broadly comparable overall ratings in controlled studies, though AI outputs can include unsupported inferences that require a fast verification step before sign-off.[3]Erin Palm et al., “Assessing the Quality of AI-Generated Clinical Notes,” Frontiers in Artificial Intelligence, frontiersin.orgProduct design has shifted toward rapid evidence linkage so clinicians can check the origin of each sentence and edit with confidence, which is increasingly expected by safety teams and regulators. The FDA’s guidance on AI-enabled device software functions emphasizes transparency in how models are developed, validated, updated, and labeled, reinforcing the need to show performance metrics and human-in-the-loop instructions at the point of use. As these safeguards standardize across vendors, the AI in clinical documentation market benefits from faster trust formation and more resilient workflows that preserve speed while managing error risk.

Revenue Integrity and Audit Pressure Expand AI-Supported CDI or CAPD and Coding

Healthcare payer scrutiny of documentation specificity has tightened since risk-adjustment updates reshaped coding expectations and audits. AI-supported CDI and coding modules now propose detailed qualifiers, justify code selections, and generate supporting rationales that reduce amended encounters and improve first-pass claim acceptance. New transparency and burden-reduction initiatives at the federal level in 2026 are pushing organizations to provide clearer, structured submissions and to monitor turnaround for decisions, both of which benefit from documentation that is complete at the source encounter.[4]U.S. Department of Health and Human Services, “TEFCA, America’s National Interoperability Network, Reaches Nearly 500 Million Health Records Exchanged as HHS Leverages Technology and AI to Lower Costs and Reduce Burden,” HHS Press Office, hhs.govHealth systems are prioritizing tools that connect physician notes to coding support that aligns with policy updates and evolving coverage criteria while creating audit trails for downstream review. Where ambient scribing accelerates note generation, CDI or CAPD overlays convert narrative content into high-integrity data elements, which raises the financial yield on each encounter. These dynamics channel investment toward platforms that couple scribing with coding integrity, creating an adoption flywheel for the AI in clinical documentation market in high-volume service lines where specificity drives payment accuracy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patient Consent and Privacy Constraints on Ambient Audio Capture and Storage | -2.8% | EU privacy-centric jurisdictions and select U.S. states | Short term (≤ 2 years) |

| Clinical Risk/Liability Necessitating Human Review and Strong Governance | -3.1% | Global with heightened sensitivity in U.S. litigation environments | Medium term (2-4 years) |

| Unit Economics Sensitivity to LLM or ASR Inference Cost and Latency | -2.3% | Global data-center hubs and GPU-constrained markets | Medium term (2-4 years) |

| Accent or Language Performance Gaps Limiting Equitable Global Rollout | -1.9% | APAC, MEA, and Latin America where non-English languages are primary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patient Consent and Privacy Constraints on Ambient Audio Capture and Storage

Consent dynamics remain a gating factor for always-on audio in some settings, especially when patients receive detailed disclosures about model usage, data handling, and vendor access. Survey research in ambulatory care shows that consent rates can drop when patients are given more granular information on AI features and data flows, and a notable share of respondents prefer that encounter data is not shared with vendors at all. Patients also report they may self-censor on sensitive topics if they know audio capture tools are in use, which introduces selection bias that can erode the clinical completeness of generated notes for higher-risk populations. These patterns shape deployment design, making opt-out options and clear in-visit consent flows central to patient experience. Some organizations are prioritizing approaches that limit the movement of raw audio and emphasize rapid deletion or on-device processing to address comfort and privacy concerns, supported by transparent user interfaces and visible recording controls. As consent processes mature and documentation tools foreground privacy by design, the AI in clinical documentation market can balance efficiency with patient trust and regulatory expectations across care settings.

Clinical Risk or Liability Necessitating Human Review and Strong Governance

Clinician verification remains essential because language models can introduce unsupported statements or omit critical details, which creates liability exposure if not caught before sign-off. Comparative studies show that AI-generated notes can match overall quality ratings but exhibit higher rates of unsupported inferences, which validates policies that require human review with clear evidence links. Regulators expect transparency around performance, training data characteristics, update policies, and labeling that clarifies the human-AI workflow so clinicians can calibrate trust and responsibilities during use. Health systems are responding with monitoring tools, audit logs, and subgroup performance checks that detect drift and highlight fairness issues as part of routine model governance. These safeguards shape vendor roadmaps by rewarding explainability, provenance mapping, and safe fallback behaviors for ambiguous content. Over time, stronger governance reduces risk while preserving speed, which supports durable adoption in the AI in clinical documentation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software or AI Platforms Command Majority Share, Yet Services Layer Accelerates with Enterprise Rollouts

Software and AI Platforms captured 58.24% of market value in 2025 and are projected to grow at 23.44% through 2031, reflecting a shift from perpetual licenses to flexible SaaS aligned to encounter volume. The pricing evolution links fees to realized outcomes rather than fixed seats, which improves economic alignment in large deployments and reduces idle cost during low-volume periods. Enterprise buyers value the ability to scale users seasonally and to bundle ambient scribing with integrity overlays as a single experience, which increases stickiness at the platform level. Vendor announcements highlight growing enterprise adoption where multimodal capture, structured write-back, and coding support run as one workflow at scale across many specialties. This configuration supports standardized governance, faster onboarding, and more consistent results across inpatient and ambulatory settings. The AI in clinical documentation market continues to reward platforms that minimize clicks, compress token usage, and deliver traceable outputs that are simple to audit.

Hardware and devices play a smaller role in total spend today but remain relevant where organizations seek more control over capture environments or want to minimize movement of raw audio. Edge capture paired with centralized language models can address consent sensitivities and provide a backup when connectivity is variable. As hospitals extend documentation support to nursing and allied health workflows, demand for peripherals, ambient microphones, and room setup services can rise with bed capacity. Professional services also expand as deployments move from single-specialty pilots to complex rollouts that involve admissions, daily progress notes, discharge summaries, and care transitions. Cloud providers and EHR vendors are investing in health-specific solution architectures to reduce time to value, which narrows gaps between software capabilities and operational change management. As a result, the AI in clinical documentation industry is building around software-first platforms while reinforcing services that accelerate adoption and reduce friction in complex environments.

By Deployment: Cloud/SaaS Leads Share and Growth, Yet Hybrid Architectures Emerge for Latency-Sensitive Workflows

Cloud/SaaS deployment held 51.35% of market value in 2025 and is expanding at the fastest 23.82% CAGR, since centralizing models allows rapid updates to clinical vocabularies, safety guardrails, and prompt strategies without local maintenance. Health systems benefit from synchronized improvements that roll out across sites and specialties at once, which shortens the time from pilot to measurable returns. Providers also favor centralized monitoring of model performance and fairness, which is simpler to run when inference paths are standardized. Cloud-based configuration aligns with existing enterprise governance practices and allows rapid policy changes if model behaviors need updates. As model quality rises, the risk of inconsistent local versions decreases, which improves trust and reduces training overhead for frontline staff. Many organizations will continue to prefer cloud-centric models in the AI in clinical documentation market because the total cost of ownership is lower when both software and oversight scale together.

Hybrid patterns are gaining traction in privacy-centric and latency-sensitive workflows. In these designs, audio capture and primary transcription occur locally while de-identified text is sent to cloud-hosted models for summarization and coding support, which balances consent concerns with scalability. This approach reduces exposure of raw audio outside the care setting while preserving centralized improvements in prompt engineering and safety rails. Hybrid designs also align with the needs of multilingual clinics that want low-latency capture while leveraging stronger cloud models for structuring content. Inpatient areas with variable network conditions use hybrid set-ups to copy data to the EHR reliably, especially during high-acuity periods. As regulatory requirements evolve, this architecture gives health systems flexibility to shift processing across the edge or cloud with minimal workflow change. The AI in clinical documentation market will likely sustain both approaches, with cloud as the default and hybrid for specific regulatory or operational needs.

By Application: Ambient Clinical Scribing Dominates Current Spend, While CDI or CAPD Surges on Revenue-Cycle Urgency

Ambient Clinical Scribing accounted for 53.34% of application value in 2025 as organizations prioritized immediate relief from clerical burden. Fast time-to-value in ambulatory settings made scribing the early entry point, which then expanded into inpatient service lines as templates matured and governance improved. As scribing platforms integrate with ordering and task management, they are increasingly positioned as encounter orchestration layers rather than standalone dictation replacements. Clinical integrity overlays are expanding because payers require precise supporting statements and consistent qualifiers for risk scoring and coverage decisions. Vendors that connect scribing outputs to high-precision coding suggestions at the same time of note generation deliver clearer returns for revenue integrity. In segments where health systems measure results by reduced denials or shorter days in accounts receivable, the AI in clinical documentation market size linked to CDI or CAPD is projected to become a larger share of future growth.

CDI or CAPD is the fastest-growing application at 23.41% CAGR through 2031 and complements scribing by elevating specificity and audit readiness. Coding modules propose ICD-10, HCC, and related code sets with supporting rationales and then align mapped CPT or E&M decisions to the clinical narrative, which reduces amended encounters and clarifies documentation at submission. Organizations can use these overlays to reduce repetitive post-discharge queries while strengthening the integrity of data sent to payers. This dual-path approach results in fewer gaps between what clinicians say, what the note records, and what the claim requires. As payer transparency expands in 2026 and beyond, demand rises for outputs that reflect documented medical necessity and provide clear provenance for each statement. The AI in clinical documentation market supports this shift by embedding integrity checks into the same flow that generates the clinical note, which accelerates review without adding new steps.

By End User: Hospitals and IDNs Anchor Spending, Yet Healthcare Payers’ AI Adoption Signals a Strategic Pivot

Hospitals and IDNs represented 55.13% of spending in 2025 as systems scaled from primary care pilots to multi-specialty rollouts across inpatient and ambulatory networks. Expansion into nursing, imaging, and procedure documentation increased the share of hospital-based use cases that require deeper integration and services support. Large systems have prioritized evidence-linked outputs and standardized templates across departments so notes stay consistent in tone and structure while preserving specialty nuance. Providers also look for ambient tools that convert narrative to orders and care instructions inside the EHR to accelerate discharge and referral workflows. As governance requirements grow, health systems emphasize safety monitoring and audit logs that track model outputs and edits across teams. Within this context, the AI in clinical documentation market continues to track hospital-scale needs for reliability, traceability, and operating leverage.

Healthcare payers are the fastest-growing end-user segment at 22.62% CAGR as they invest in workflows that score medical necessity, assess coverage rules, and surface documentation gaps for providers to address at the source encounter. Documentation generated with explainable elements, code rationales, and clear provenance can reduce the time to decision and minimize back-and-forth after submission. Payers seeking continuity across prior authorization and claims review advocate for structured narrative elements that speak to policy criteria. As transparency efforts progress in 2026, there is increased emphasis on reporting turnaround times and decision patterns, which elevates the importance of clear, structured inputs with traceable evidence. These conditions support closer alignment between payer-side review tools and provider-side documentation engines. The AI in clinical documentation industry is adapting to this alignment by designing outputs that serve both clinical readability and administrative determinism.

By Clinical Setting: Inpatient Volumes Dominate, Yet Outpatient Velocity and ED Complexity Shape Product Roadmaps

Inpatient settings captured 61.55% of clinical-setting value in 2025 due to the complexity and frequency of notes that span admissions, daily progress, handoffs, and discharges. Enterprise buyers emphasize note standardization and governance so that each specialty can use templates with predictable structures and explainable evidence links. Inpatient deployments require coordination across multidisciplinary teams, which raises the importance of integration with order sets, task queues, and care transitions. As hospitals extend these tools into nursing documentation, ambient capture can generate shift handoffs and care-transition summaries that reduce duplication and improve continuity. These workflows also highlight the need for consistent provenance so that each element of a note points to audio or structured data that supports it. The AI in clinical documentation market keeps prioritizing inpatient reliability because the margin for error is lower when more clinicians touch the same chart.

Outpatient settings are the fastest accelerants of new deployments by user count because time savings create more visit capacity and shorter backlogs. High-volume specialties and primary care view scribing as a way to handle seasonal surges and persistent staffing gaps. Ambient notes that assemble problem lists, medications, and plan elements with accurate attribution reduce after-hours charting and improve patient communication. Outpatient groups also benefit from embedded preventive care prompts and condition management reminders that surface during the note, which improves quality measures and closes care gaps. Payers’ expectations for clarity at the point of authorization drive interest in generating visit summaries that align to policy criteria on the first attempt. With this feedback loop, the AI in clinical documentation market is tailoring outpatient features toward speed, accuracy, and actions that reduce downstream administrative touchpoints.

Geography Analysis

North America accounted for 50.16% of global value in 2025 due to large-scale EHR installations and sustained clinical IT spending that prioritizes clinician experience and administrative efficiency. Interoperability initiatives and network-level data exchange that expanded by 2026 are enabling faster movement of structured clinical information, which supports documentation that is both readable and machine-actionable. U.S. hospitals and physician groups are scaling ambient scribing across multiple service lines while building CDI overlays and coding support that align with coverage criteria and risk adjustment needs. Clinical governance is central to adoption, so organizations emphasize evidence-linked outputs and rapid verification inside the EHR. The American Hospital Association has profiled early deployments that show how provider systems are standardizing workflows and monitoring quality as ambient tools expand into enterprise use. With privacy and safety expectations rising, the AI in clinical documentation market in North America rewards designs that surface the source evidence for each claim and provide consistent edit trails across teams.

Europe shows measured uptake because reimbursement models vary and direct revenue gains from saved minutes are less pronounced in many systems. Hospitals and clinics in privacy-centric jurisdictions often prefer hybrid designs that limit the movement of raw audio, with quick deletion policies and on-device capture paired with cloud summarization. Buyers emphasize explainability and consistency, especially in multilingual environments where small errors can create administrative friction. Provider and payer organizations focus on clear human review steps and audit logs that preserve clinical accountability for final notes. Within these priorities, ambient scribing often enters through specialties where documentation burden is acute and then expands with integrity overlays as governance matures. As models adapt to local languages and clinical conventions, the AI in clinical documentation market in Europe is expected to grow through designs that minimize data exposure and maximize traceability.

Asia-Pacific is the fastest-growing region at 23.24% CAGR as national digital-health strategies and public-sector programs accelerate standardization and interoperability goals. Health systems in cities and academic centers are piloting generative tools that support multilingual patient populations in clinical settings, often through collaborations that test medical language models in real-world workflows. Providers are also exploring hybrid deployments that match language and latency needs with data protection expectations across jurisdictions. Public and private hospitals that serve dense urban populations see clear benefits in throughput and note standardization, which strengthens adoption in ambulatory and emergency settings. Buyers look for tools that can handle code sets and clinical conventions across countries so documentation outputs are locally compliant. As capabilities improve across English and non-English languages, the AI in clinical documentation market in Asia-Pacific is expected to sustain its momentum through language support and interoperable designs.

Competitive Landscape

Competition centers on three archetypes that converge at the point of care. First, cloud platforms integrate AI services that handle speech recognition, summarization, and entity extraction to deliver ambient scribing and coding support at scale. Second, vertical specialists focus on clinical documentation with deep prompts, specialty templates, and explainability features tuned for frontline users. Third, EHR-native approaches embed ambient documentation and integrity checks into existing workflows to reduce toggling and training. Hospitals prioritize reliability and traceability, so vendors that show evidence links for every sentence and maintain audit logs for edits earn stronger trust with safety teams. Integration with the system of record remains the decisive feature where buyers care about click counts and in-flow verification more than marginal accuracy gains.

Strategic moves signal a pivot toward productization around workflow actions and revenue integrity. Launches of medical ASR models with domain-optimized performance highlight vendor emphasis on clinical terminology and keyword recall as the base for summarization and coding. Major technology firms are publishing healthcare updates that extend large language models into clinical settings, with pilots aimed at multilingual support and physician workflows. Health systems are spotlighting embedded experiences that keep clinicians inside the EHR while ambient tools generate structured notes and allow rapid, evidence-linked edits. As interoperability frameworks progress, providers want documentation tools that exchange structured content reliably and align to payer expectations in a traceable way.

Regulatory guidance has become a core differentiator because it shapes how vendors manage updates and communicate performance. The FDA’s guidance on AI-enabled device software functions emphasizes transparency across development, labeling, and human factors that determine safe deployment, which raises the bar for documentation tools that operate within or adjacent to regulated workflows. Associations and provider coalitions are also highlighting operational lessons that support enterprise expansion with governance, fairness monitoring, and continuous improvement practices. As procurement teams assess platforms, they weigh explainability, integration simplicity, and operating leverage in hybrid or cloud designs. These criteria favor solutions that compress inference costs while maintaining note quality and that present clear provenance so busy clinicians can verify content in seconds. Within these dynamics, the AI in clinical documentation market continues to evolve toward integrated, evidence-linked experiences that align clinical, operational, and financial outcomes.

AI In Clinical Documentation Industry Leaders

Microsoft

Solventum

Abridge

eClinicalWorks

Suki

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Ambience Healthcare unveiled a multi-year platform roadmap to "rebuild healthcare with AI," introducing performance incentive-based contracts that link vendor compensation directly to measurable financial outcomes for health systems, including reduced claim denials and accelerated revenue cycles, a commercial model few AI vendors have adopted and one that shifts downside risk onto the technology supplier.

- March 2026: Zoom announced Epic EHR integrations and launched its "Clinical Note" ambient AI feature at the HIMSS26 conference, enabling automatic structured documentation from patient conversations with integration into Epic Mobile Haiku and Hyperspace. PocketRN, an early adopter, reported a 60% reduction in documentation time, $27,000 in monthly savings, and a 30% drop in ER visits and readmissions, positioning Zoom as a new competitor in the ambient scribe market.

- March 2026: University Hospitals of Leicester and University Hospitals of Northamptonshire awarded Accurx a £1.9 million contract to deploy Ambient Voice Technology to clinical and non-clinical staff across multiple hospital sites, with an initial three-year term and potential 12-month extension, following pilots that saved eight minutes per patient on post-clinic documentation and an average of one hour of admin time per day.

- February 2026: Epic Systems launched AI Charting, a native ambient scribe integrated directly into its EHR platform with real-time order queuing capabilities. Group Health Cooperative of South Central Wisconsin, an early co-development partner, reported savings of up to 60 minutes per day per clinician, prompting health systems to reassess third-party scribe contracts and intensifying competitive pressure on standalone AI vendors.

Global AI In Clinical Documentation Market Report Scope

As per the scope of the report, AI in clinical documentation refers to the use of machine‑learning, natural‑language processing, and automation tools to capture, structure, and generate clinical notes from physician-patient interactions. It reduces manual data entry, improves accuracy and completeness of records, and streamlines workflows through ambient listening, real‑time transcription, coding support, and automated summarization, ultimately enhancing clinician efficiency and documentation quality.

The AI clinical documentation market is segmented into component, deployment, application, end user, clinical setting, and geography. By component, the market is segmented into software / AI platforms, services, and hardware & devices. By deployment model, the market is segmented into cloud / SaaS and on-premises. By application, the market is segmented into ambient clinical scribing, medical speech recognition, clinical documentation integrity (CDI) / CAPD, automated medical transcription and note summarization, and others. By end user, the market is segmented into hospitals and IDNs, physician groups and clinics, diagnostic imaging centers, healthcare payers, and others. By clinical setting, the market is segmented into inpatient, outpatient, and emergency and urgent care. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software / AI platforms |

| Services |

| Hardware and Devices |

| Cloud / SaaS |

| On-Premises |

| Ambient Clinical Scribing |

| Medical Speech Recognition |

| Clinical Documentation Integrity (CDI) / CAPD |

| Automated Medical Transcription and Note Summarization |

| Others |

| Hospitals and IDNs |

| Physician Groups and Clinics |

| Diagnostic Imaging Centers |

| Healthcare Payers |

| Others |

| Inpatient |

| Outpatient |

| Emergency and Urgent Care |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software / AI platforms | |

| Services | ||

| Hardware and Devices | ||

| By Deployment | Cloud / SaaS | |

| On-Premises | ||

| By Application | Ambient Clinical Scribing | |

| Medical Speech Recognition | ||

| Clinical Documentation Integrity (CDI) / CAPD | ||

| Automated Medical Transcription and Note Summarization | ||

| Others | ||

| By End User | Hospitals and IDNs | |

| Physician Groups and Clinics | ||

| Diagnostic Imaging Centers | ||

| Healthcare Payers | ||

| Others | ||

| By Clinical Setting | Inpatient | |

| Outpatient | ||

| Emergency and Urgent Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for AI in the clinical documentation market?

The AI in clinical documentation market size is USD 1.15 billion in 2026 and is forecast to reach USD 3.05 billion by 2031 at 21.46% CAGR over 2026-2031.

Which applications are leading and which are growing fastest in AI-powered documentation?

Ambient Clinical Scribing leads with 53.34% of 2025 value, while CDI or CAPD posts the fastest growth with a 23.41% CAGR through 2031 as organizations target revenue integrity and audit readiness.

What deployment models are preferred for AI in clinical documentation and why?

Cloud /SaaS lead with 51.35% share in 2025 and the fastest 23.82% CAGR because centralized models speed updates and enable easier monitoring, while hybrid designs address privacy and latency needs in specific workflows.

Which end users are adopting AI documentation the fastest?

Hospitals and IDNs account for 55.13% of 2025 spending, while healthcare payers are the fastest-growing end users at 22.62% CAGR as they expand prior authorization and claims review workflows that prefer structured, explainable notes.

Page last updated on: