Natural Language Understanding Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

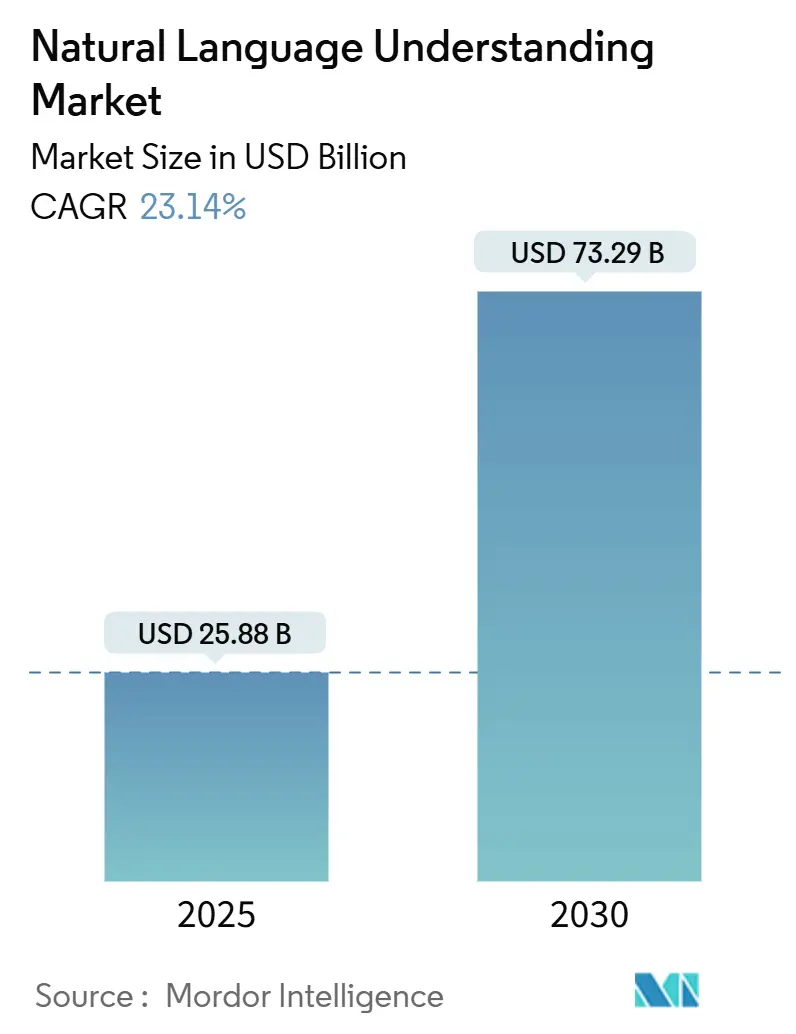

| Market Size (2025) | USD 25.88 Billion |

| Market Size (2030) | USD 73.29 Billion |

| Growth Rate (2025 - 2030) | 23.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Natural Language Understanding Market Analysis by Mordor Intelligence

The Natural Language Understanding market size is valued at USD 25.88 billion in 2025 and is forecast to reach USD 73.29 billion by 2030, advancing at a 23.14% CAGR. Intensifying investment in conversational AI, rapid progress in domain-specific large language models, and wider deployment of privacy-preserving Edge AI solutions underpin this expansion. Enterprises are shifting from rule-based language tooling to contextual understanding platforms that capture nuanced intent, drive hyper-personalized engagement, and eliminate repetitive knowledge work. Strategic partnerships between hyperscale cloud vendors and specialist AI firms accelerate time-to-value, while government incentives for sovereign AI spur multilingual R&D across Asia-Pacific and Europe. Heightened regulatory focus on data privacy complements demand for on-premises and hybrid deployments that secure sensitive workloads without sacrificing scale.

Key Report Takeaways

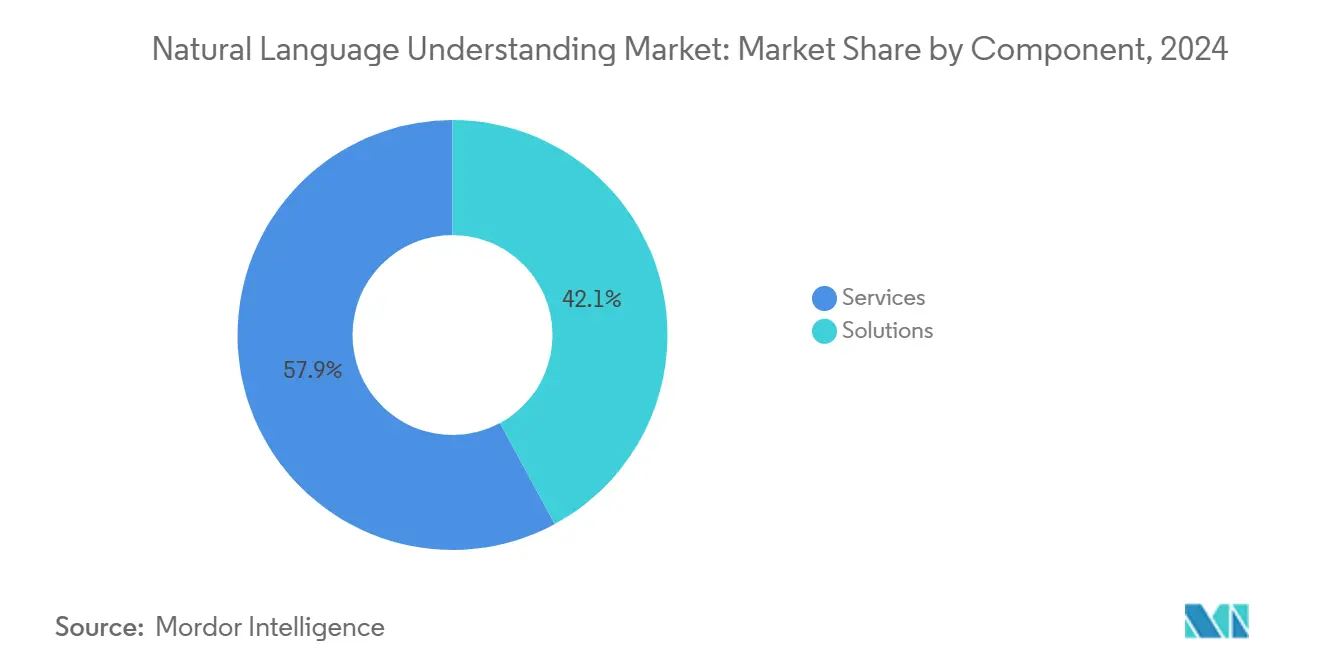

- By component, services led with a 57.89% share of the Natural Language Understanding market in 2024; solutions are projected to expand at a 23.63% CAGR through 2030.

- By deployment mode, cloud retained a 63.42% share of the Natural Language Understanding market size in 2024 and is projected to advance at a 23.74% CAGR through 2030.

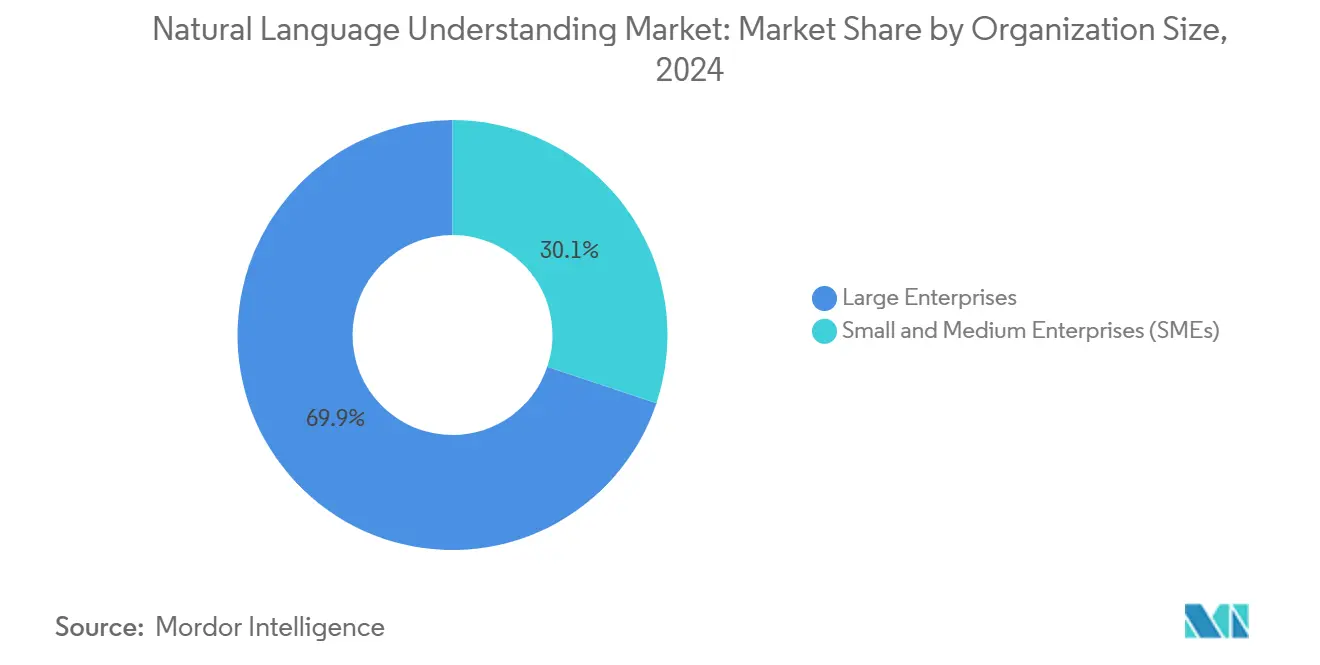

- By organization size, large enterprises accounted for 69.86% revenue share in 2024, whereas small and medium enterprises recorded the highest projected CAGR at 23.69% through 2030.

- By industry vertical, banking, financial services, and insurance held 25.91% of the Natural Language Understanding market share in 2024, while healthcare and life sciences are poised to register the fastest growth, at a 24.76% CAGR, over the same horizon.

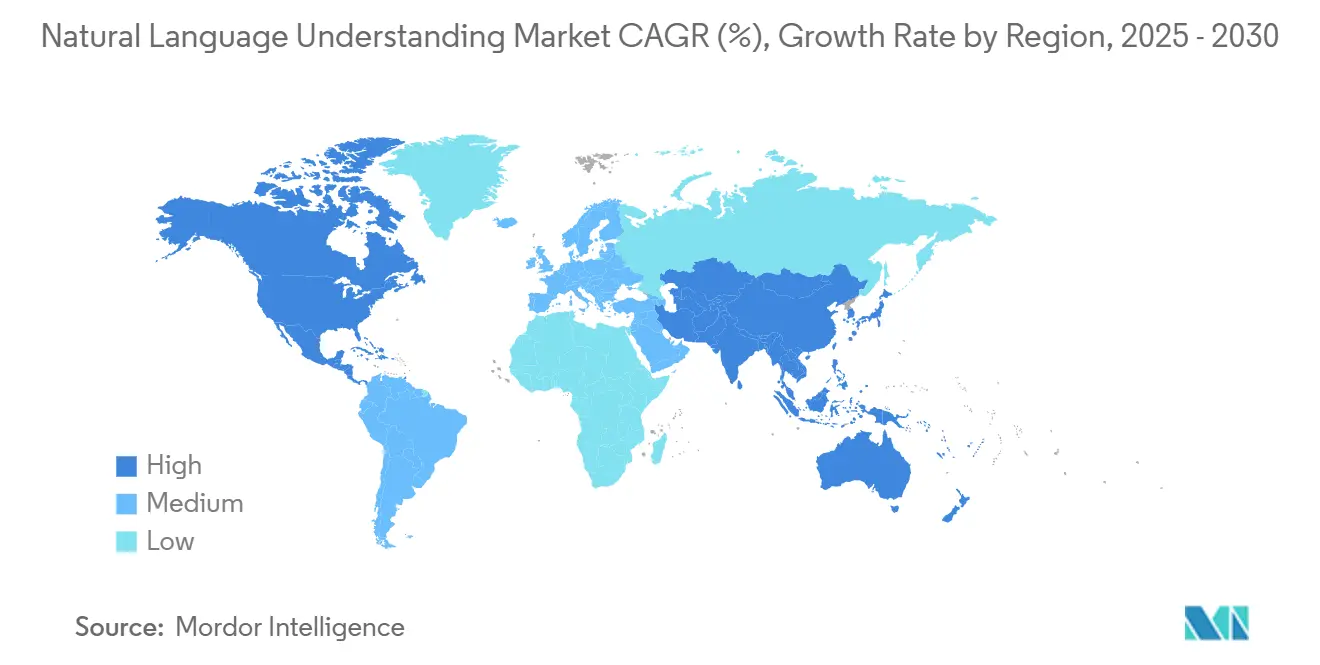

- By geography, North America accounted for 36.73% revenue share in 2024, whereas Asia Pacific recorded the highest projected CAGR at 24.11% through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Natural Language Understanding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Voice-Enabled Applications | +4.2% | Global, strong in North America and Asia-Pacific | Medium term (2-4 years) |

| Expansion of Multilingual Digital Customer Support | +3.8% | Global, prominent across Europe, Middle East and Asia-Pacific | Short term (≤ 2 years) |

| Integration of NLU in Edge AI Devices | +3.5% | North America and Europe, extending into Asia-Pacific | Long term (≥ 4 years) |

| Accelerating Investments in Conversational Commerce | +3.1% | Global, led by North America and China | Medium term (2-4 years) |

| Domain-Specific Large Language Models Gain Traction | +2.9% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Privacy-Preserving Federated Learning Techniques | +2.4% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Voice-Enabled Applications

Enterprises are increasingly embedding voice interfaces within manufacturing, healthcare, and field-service workflows to free up hands and speed up task execution. Context-aware Natural Language Understanding market deployments enable fine-grained instructions, adapt to domain-specific terminology, and reduce documentation time for clinicians by multiple hours per shift. Amazon reported a 340% jump in enterprise voice workloads on Alexa for Business during 2024.[1]Amazon Web Services, "Alexa for Business - Enterprise Voice Solutions," aws.amazon.com Manufacturers add voice-guided quality checks, while hospitals embrace ambient clinical documentation that listens, understands, and files encounter notes in compliant formats.

Expansion of Multilingual Digital Customer Support

Global brands must serve customers who switch among languages and dialects across channels. Real-time language detection, contextual translation, and cultural nuance handling are now table-stakes. Transcosmos achieved a 60% improvement in deployment success rates after training models on domain-specific support corpora for more than 200 clients in 2024.[2]Transcosmos, "Global Multilingual Customer Support Solutions," transcosmos.co.jp Financial institutions utilize multilingual fraud-alert bots that can parse both slang and formal speech, thereby boosting trust in underserved regions and accelerating cross-border growth.

Integration of NLU in Edge AI Devices

Latency-sensitive and privacy-critical use cases drive inference toward local compute. Siemens activated edge-resident Natural Language Understanding market solutions across shop floors in 2024, enabling predictive-maintenance alerts even when networks drop.[3]Siemens, "Manufacturing AI and Industrial Automation Stories," siemens.com Automakers embed on-board interpreters for navigation and diagnostics, while medical device makers ensure that protected health information never leaves the facility. Hybrid designs combine cloud-scale training with on-device reasoning, reducing bandwidth costs and meeting stringent compliance requirements.

Accelerating Investments in Conversational Commerce

Retailers now rely on dialog-driven storefronts that infer implicit needs and orchestrate complex orders. Walmart’s conversational grocery experience, launched in mid-2024, has increased customer satisfaction by 45% compared to form-based ordering. Natural Language Understanding market engines parse dietary, gifting, or subscription intents, upsell relevant bundles, and fill carts in fewer exchanges. The resulting lift in conversion and basket size cements conversational buying as a mainstream revenue lever.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Context-Rich Training Data | -2.8% | Global, acute in specialized domains | Short term (≤ 2 years) |

| Data Privacy and Sovereignty Regulations | -2.4% | Europe, North America, and Asia-Pacific jurisdictions with strict rules | Long term (≥ 4 years) |

| High Cost of Annotation and Model Maintenance | -2.1% | Global, higher in cost-sensitive markets | Medium term (2-4 years) |

| Algorithmic Bias and Explainability Concerns | -1.8% | Global, with heightened scrutiny in regulated industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Context-Rich Training Data

Sophisticated systems demand corpora that capture regulatory jargon, clinical narratives, or financial discourse in context. Healthcare projects must balance completeness against HIPAA constraints, which limit the data that developers can pool. Finance teams confront similar confidentiality barriers, slowing the rollout of risk-language parsers that could streamline compliance filings. The resulting data bottleneck curbs accuracy gains and lengthens development cycles.

High Cost of Annotation and Model Maintenance

Expert tagging of niche terminology costs USD 50-150 per hour, pushing early budgets beyond forecasts, especially for regulatory content that requires multiple reviewer sign-offs. After launch, models demand a steady refresh to reflect new laws or evolving idioms. Healthcare providers report spending up to 40% of their AI operating budgets on ongoing updates. The financial burden can delay expansion into additional languages or business lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Dominate, Platforms Accelerate

Services captured a 57.89% market share in Natural Language Understanding in 2024, as enterprises leaned on consulting, customization, and managed support to navigate complex deployments. Solutions, however, are scaling at a 23.63% CAGR, reflecting the emergence of pre-trained domain models that significantly reduce build times. The Natural Language Understanding market size for services remains anchored in specialist data-preparation engagements and continuous optimization contracts. Meanwhile, low-code tools democratize experimentation, allowing citizen developers to spin up bots without the need for full engineering teams.

Managed service uptake is rising as CIOs offload model tuning and monitoring. Microsoft logged a 180% surge in Azure Cognitive Services managed agreements with healthcare and finance clients during 2024. Solution vendors now bundle pipeline visualization, bias detection, and governance modules, creating integrated environments that shorten feedback loops and enforce compliance.

By Deployment Mode: Cloud Scale Meets Emerging Edge Needs

Cloud installations held a 63.42% share of the Natural Language Understanding market size in 2024 and are poised for a 23.74% CAGR through 2030, driven by elastic capacity and pay-as-you-go economics. Tight latency service-level agreements and data-sovereignty mandates sustain on-premises clusters in banking and public agencies. Hybrid paradigms are gaining ground: models are trained centrally and then export compressed weights for field inference. GE Vernova demonstrated this pattern in 2024 across industrial turbines, running fault-detection interpreters locally while aggregating insights to the cloud for fleet-wide analytics.

Cloud providers now market confidential-compute nodes, regional replication, and “train-in-place” tools to persuade regulated customers. Edge hardware vendors add AI accelerators that parse voice or text offline yet sync updates when connectivity resumes. The interplay of cloud reach and edge autonomy will define next-generation architectures.

By Organization Size: SMEs Democratize Advanced Capabilities

Large enterprises commanded a 69.86% market share in the Natural Language Understanding market in 2024, due to their deep data pools and integration talent. Small and medium-sized enterprises are expanding at the fastest rate, clocking a 23.69% CAGR as subscription pricing, API-first tools, and marketplace plug-ins lower the entry thresholds. The Natural Language Understanding market size within SMEs benefits from starter packages that bundle intent libraries and regulatory presets, allowing support teams to launch 24/7 multilingual agents within weeks.

Enterprise buyers continue to scale cross-domain rollouts, automating claims processing, contract review, and workforce knowledge mining. ISO 27001 certification remains a decisive factor for vendor selection across both segments. Start-ups gravitate to cloud instances with embedded governance, while global banks still favor on-premises federated clusters for fraud analysis.

By Industry Vertical: Healthcare Surges Past BFSI Growth

Banking, financial services, and insurance retained a 25.91% market share in the Natural Language Understanding market in 2024 by leveraging document parsing for compliance and conversational authentication. The segment also utilizes real-time trade surveillance, which flags risky phrases across various channels. The healthcare and life sciences sector is forecasted to grow at a 24.76% CAGR to 2030, thereby elevating the Natural Language Understanding market size for clinical voice capture, multilingual triage chat, and automated research summarization.

Retail and eCommerce brands adopt dialog-first shopping journeys that drive higher conversion. Target’s 2024 rollout of AI agents cut call center volume by 40% and raised satisfaction scores. Telecom carriers use intent analytics to predict churn, while governments pilot citizen-service bots despite lengthy procurement cycles. Manufacturing plants embed textual sensor logs into predictive models to preempt downtime.

Geography Analysis

North America led the Natural Language Understanding market with a 36.73% market share in 2024, driven by deep venture capital investments, research hubs, and clear AI guidance, such as the NIST AI Risk Management Framework. Federal health programs and sector-specific rules encourage responsible adoption without stalling innovation. Canada directs CAD 443 million (USD 327 million) into multilingual NLP centers that serve public services and private firms. Mexico’s fintech boom catalyzes Spanish-language understanding engines for customer onboarding and anti-fraud screening.

The Asia-Pacific region records the fastest 24.11% CAGR, driven by sovereign AI agendas, booming e-commerce, and vast linguistic diversity. China’s provincial governments fund domain-specific models for smart-city services, while Japan subsidizes eldercare robots with the ability to comprehend contextual speech. India’s trilingual commerce apps require simultaneous parsing of English, Hindi, and regional languages, broadening the Natural Language Understanding market. Singapore channels SGD 500 million (USD 370 million) into responsible AI and has issued model-audit sandboxes to accelerate commercial pilots.

Europe balances innovation with stringent privacy norms embodied in the EU AI Act. Enterprises tend to favor on-premises or private-cloud deployments to protect citizen data. Germany’s Industrie 4.0 program sponsors plant-floor chatbots, and the United Kingdom’s regulators promote explainable compliance bots in finance. In the Middle East and Africa, the UAE aims to achieve 25% of AI-enabled public transactions by 2031, thereby spurring Arabic language understanding initiatives. South America, led by Brazil and Argentina, scales Portuguese and Spanish models to support cross-border retail and digital banking.

Competitive Landscape

The Natural Language Understanding market exhibits moderate concentration, with hyperscale platforms dominating infrastructure, while specialist vendors carve out vertical niches. Incumbent software firms embed native comprehension features to defend their portfolios, thereby lowering the differentiation of standalone tools. Strategic alliances shape go-to-market strategies, as exemplified by Microsoft and OpenAI extending co-engineering to embed large language models into productivity suites.

Pure-play AI start-ups focus on healthcare dictation, legal contract review, or multilingual call-center analytics, leveraging curated corpora to surpass the accuracy of generalist systems. Certification around data handling, bias controls, and audit logging becomes a key tender requirement, favoring well-capitalized vendors who can invest in compliance. Pricing shifts from license fees to consumption-based, outcome-linked structures tied to accuracy or handle-time reductions.

Investment activity remains vigorous. OpenAI’s USD 6.6 billion Series C funding round in October 2025 establishes a USD 157 billion valuation to support specialized enterprise offerings. Anthropic’s USD 4 billion raise in June 2025 underscores the appetite for safer conversational AI. Cloud giants layer custom-model services, letting clients fine-tune proprietary data without exposing it outside tenant boundaries. Competition now hinges on speed to customization, regulatory assurances, and demonstrable ROI for line-of-business users.

Natural Language Understanding Industry Leaders

-

Amazon Web Services Inc.

-

Google LLC

-

Microsoft Corporation

-

International Business Machines Corporation

-

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: OpenAI completed a USD 6.6 billion Series C funding round, valuing the company at USD 157 billion and allocating the proceeds to expand enterprise-grade domain-specific language models.

- September 2025: Microsoft added advanced natural language understanding to Microsoft 365 Copilot, enabling automated content generation and document analysis across Word, Excel, and PowerPoint for enterprise clients.

- August 2025: Amazon Web Services introduced Amazon Bedrock Custom Models, allowing organizations to fine-tune foundation models with proprietary data while maintaining full privacy and security controls.

- July 2025: Google Cloud broadened Vertex AI with healthcare, finance, and retail-focused natural language models that include built-in regulatory compliance features.

Global Natural Language Understanding Market Report Scope

The Natural Language Understanding Market Report is Segmented by Component (Solutions, and Services), Deployment Mode (On-Premises, and Cloud), Organization Size (Small and Medium Enterprises, and Large Enterprises), Industry Vertical (Banking, Financial Services, and Insurance (BFSI), Retail and eCommerce, Healthcare and Life Sciences, Telecom and IT, Media and Entertainment, Government and Public Sector, Manufacturing and Other Industry Vertical), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Software Tools |

| Platforms | |

| Services | Professional Services |

| Managed Services |

| On-Premises |

| Cloud |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Banking, Financial Services, and Insurance (BFSI) |

| Retail and eCommerce |

| Healthcare and Life Sciences |

| Telecom and IT |

| Media and Entertainment |

| Government and Public Sector |

| Manufacturing and Other Industry Vertical |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Solutions | Software Tools | |

| Platforms | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment Mode | On-Premises | ||

| Cloud | |||

| By Organization Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) | ||

| Retail and eCommerce | |||

| Healthcare and Life Sciences | |||

| Telecom and IT | |||

| Media and Entertainment | |||

| Government and Public Sector | |||

| Manufacturing and Other Industry Vertical | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is driving the rapid growth in the Natural Language Understanding market?

The market is growing at 23.14% CAGR primarily due to voice application adoption (contributing +4.2% to CAGR), multilingual customer support expansion (+3.8%), edge AI integration (+3.5%), and conversational commerce investments (+3.1%). These drivers collectively address enterprise needs for automation, personalization, and global customer engagement.

How are small businesses adopting NLU technology?

Small and medium enterprises are adopting NLU at a 23.69% CAGR through 2030, leveraging cloud-based subscription models, pre-configured solutions, and low-code platforms that eliminate large upfront investments. These businesses primarily implement customer service automation and domain-specific applications that provide immediate ROI without extensive customization.

Which industries benefit most from Natural Language Understanding?

Banking and financial services currently lead with 25.91% market share, using NLU for compliance automation and fraud detection. Healthcare is growing fastest at 24.76% CAGR, implementing clinical documentation automation and patient engagement systems. Retail, telecom, and manufacturing also see significant benefits through conversational commerce and operational efficiency applications.

What challenges do organizations face when implementing NLU systems?

The primary challenges include scarcity of context-rich training data (-2.8% impact on CAGR), especially in specialized domains with privacy restrictions, and high costs for expert annotation and model maintenance (-2.1% impact). Organizations also struggle with integration complexity, which explains why services account for 57.89% of the market as businesses seek implementation expertise.

How is edge computing changing the Natural Language Understanding landscape?

Edge computing enables real-time language processing without cloud connectivity, addressing latency and privacy concerns for mission-critical applications. Organizations like GE Vernova and Siemens have implemented edge-based NLU for industrial applications, while automotive manufacturers integrate voice capabilities directly into vehicles. This hybrid approach combines cloud-scale training with local inference for optimal performance.

What recent developments are shaping the future of NLU technology?

Recent developments include major funding rounds (OpenAI's USD 6.6 billion Series C, Anthropic's USD 4 billion raise), enterprise integration (Microsoft 365 Copilot), custom model platforms (Amazon Bedrock), industry-specific solutions (Google's Vertex AI vertical models), and specialized applications for healthcare (Nuance's Dragon Medical One) and legal services (Expert.ai's Cogito platform). These advancements are making NLU more accessible, customizable, and industry-relevant.

Page last updated on: