AI In Clinical Knowledge Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.20 Billion |

| Market Size (2031) | USD 8.90 Billion |

| Growth Rate (2026 - 2031) | 22.79% CAGR |

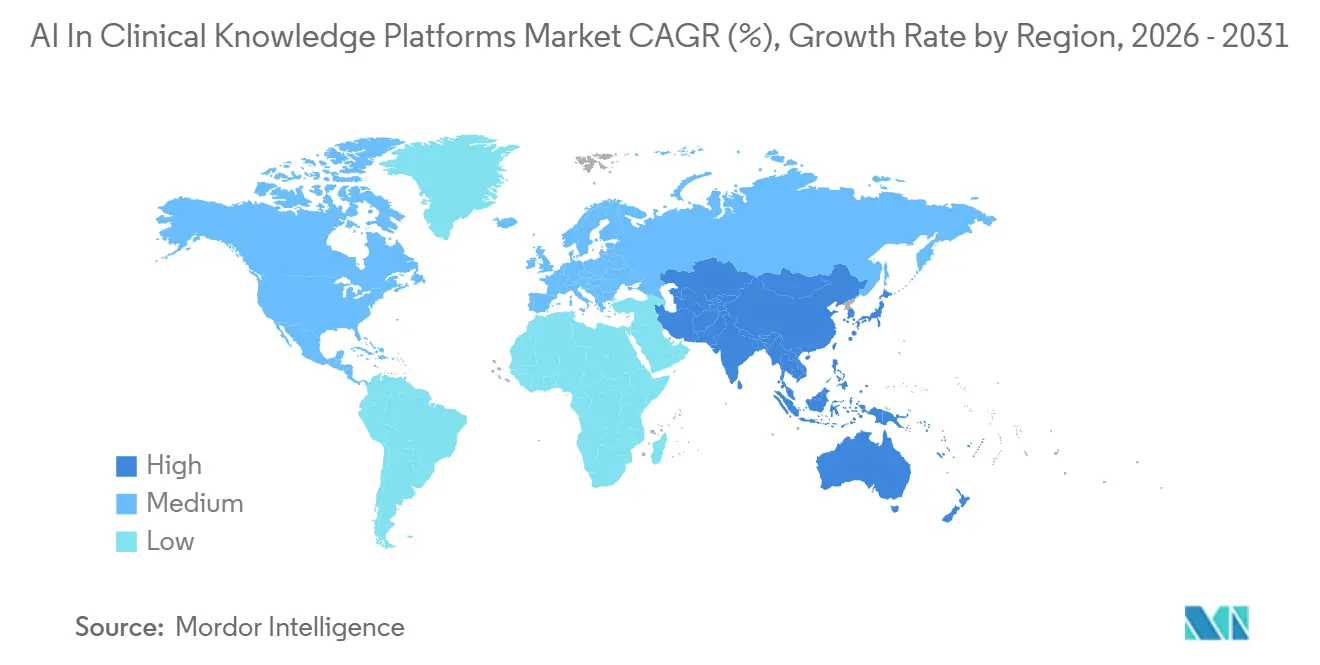

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

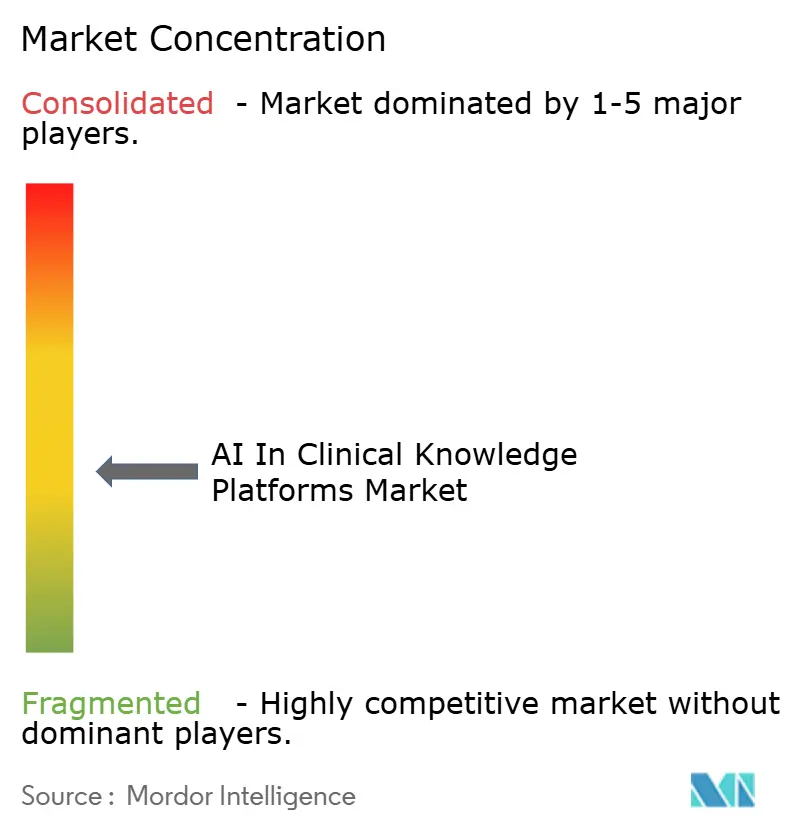

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Clinical Knowledge Platforms Market Analysis by Mordor Intelligence

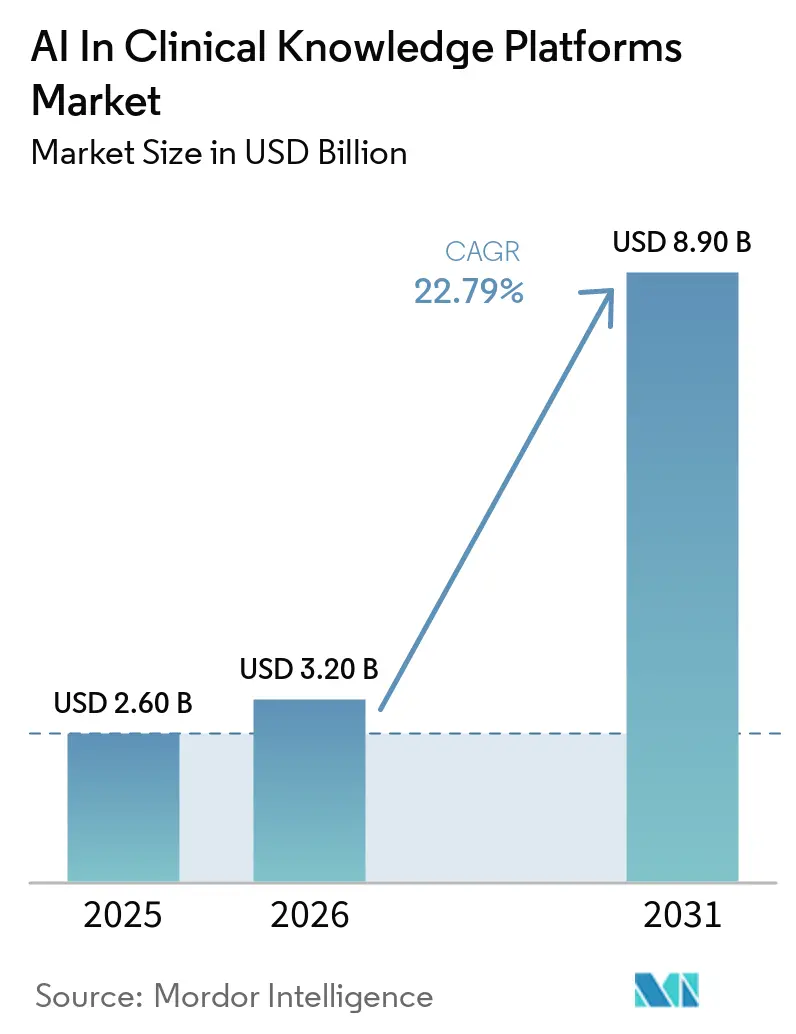

The AI In Clinical Knowledge Platforms Market size is expected to increase from USD 2.60 billion in 2025 to USD 3.20 billion in 2026 and reach USD 8.90 billion by 2031, growing at a CAGR of 22.79% over 2026-2031.

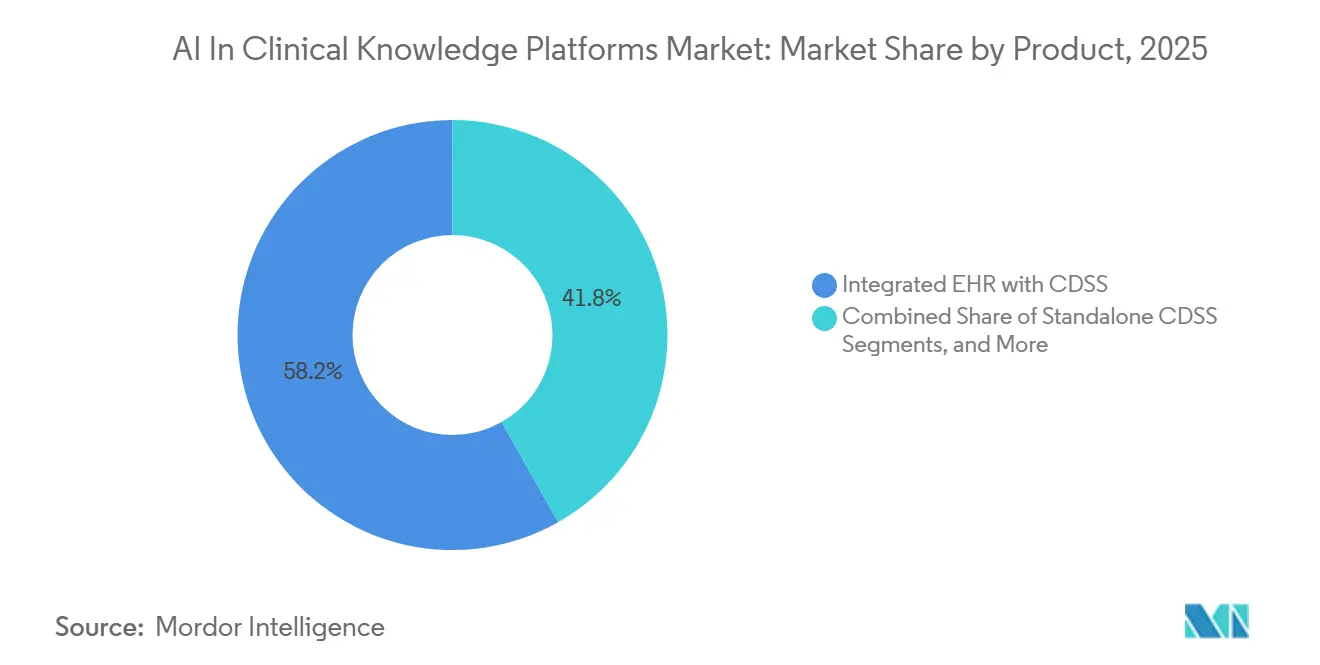

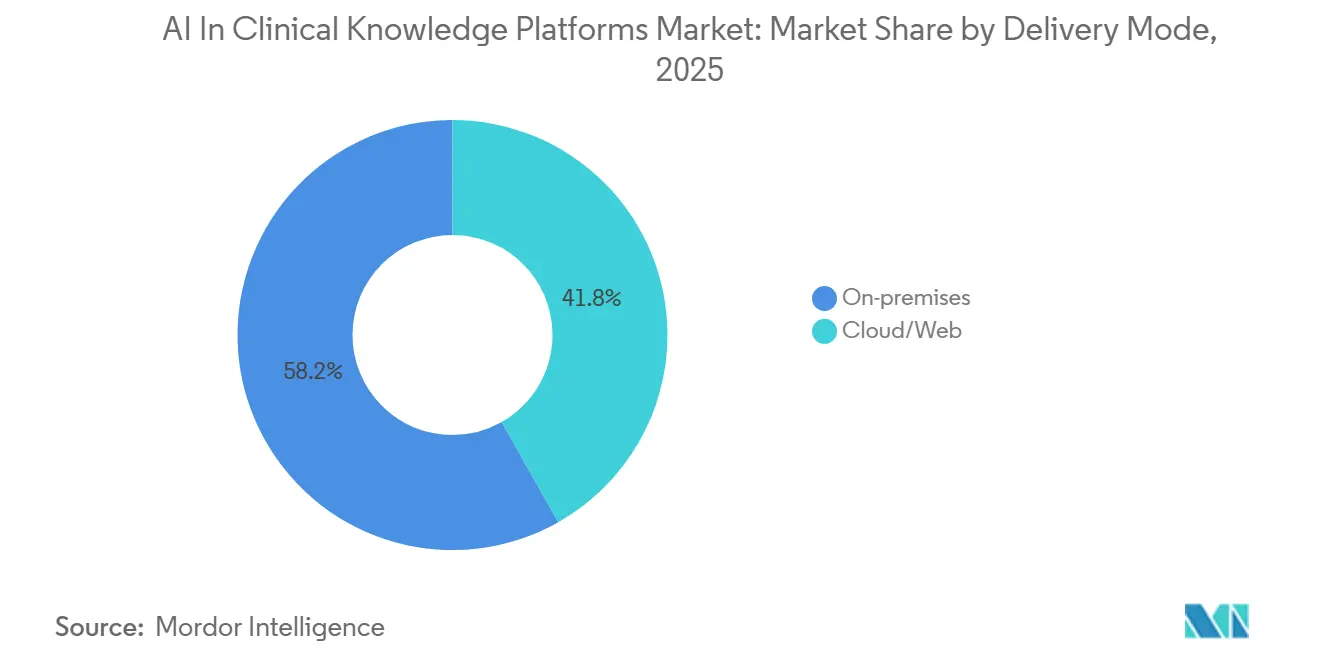

Hospitals are increasingly addressing clinician burnout and the need for modernized medication safety by adopting evidence-based solutions within the electronic health record (EHR) workflow. By 2025, integrated EHR configurations are expected to contribute 58.18% of revenue due to their ability to eliminate context-switching. Cloud-hosted tools are experiencing the fastest growth as vendors provide HIPAA-compliant, regionally hosted instances that ensure data residency and streamline upgrade cycles. Furthermore, non-knowledge-based models powered by large language models (LLMs) are gaining market share by proving their effectiveness in summarizing patient histories and developing guideline-aligned care plans.

Key Report Takeaways

- By product category, integrated EHR with clinical decision support systems (CDSS) captured 58.18% of 2025 revenue; standalone CDSS solutions are projected to expand at a 24.16% CAGR through 2031.

- By model type, knowledge-based systems commanded 65.13% of the AI in Clinical Knowledge Platforms market share in 2025, while non-knowledge-based AI/ML models are projected to grow at a 25.16% CAGR through 2031.

- By deployment, on-premises installations represented 58.19% of 2025 demand, whereas cloud/web delivery is projected to grow at a 26.13% CAGR.

- By care setting, inpatient deployments held 64.18% of 2025 revenue, and ambulatory/outpatient use cases are projected to grow at a 25.27% CAGR through 2031.

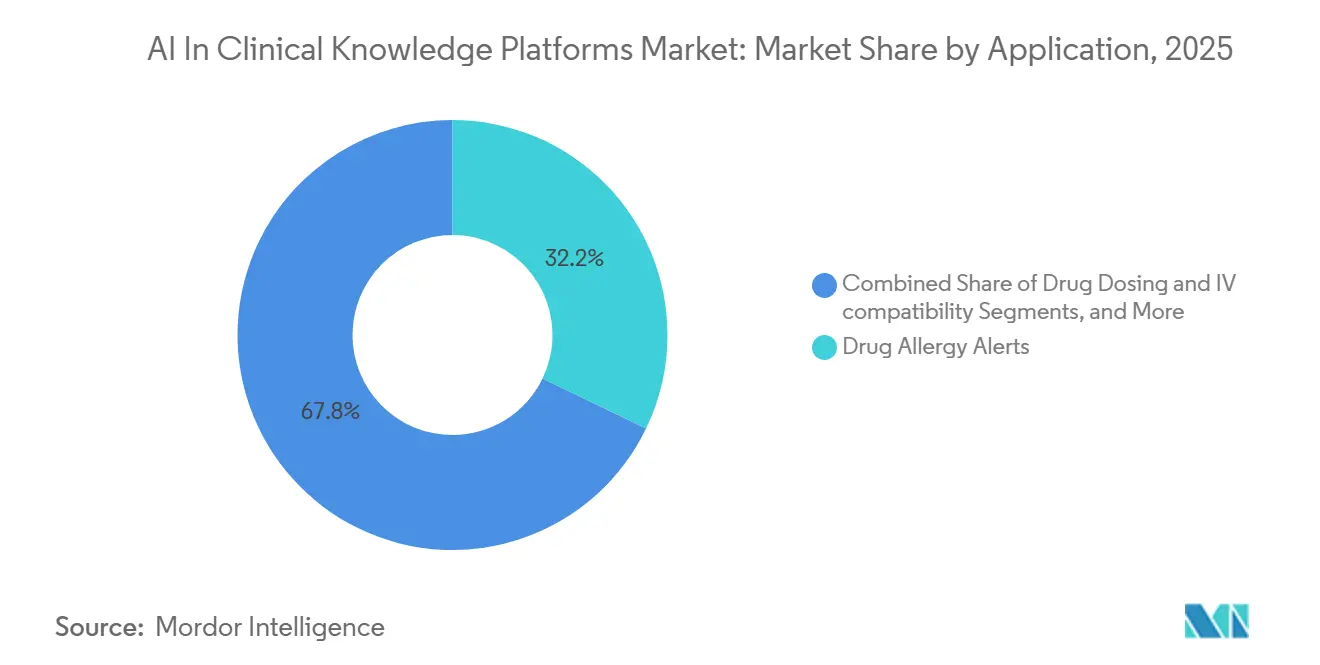

- By application, drug-allergy alerts led with 32.16% of 2025 revenue; diagnostic decision support is projected to grow at a 26.08% CAGR through 2031.

- By geography, North America led with 42.18% of 2025 revenue; Asia-Pacific iis projected to grow at a 26.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Clinical Knowledge Platforms Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| EHR-integrated, evidence-based answers | +6.2% | Global, early uptake in North America and Western Europe | Medium term (2-4 years) |

| Clinician productivity pressure driving AI | +5.8% | Global, most acute in North America, UK, Australia | Short term (≤ 2 years) |

| Medication safety & pharmacy CDS modernization | +4.1% | Global, regulatory push in North America and EU | Medium term (2-4 years) |

| Licensed, publisher-owned GenAI copilots | +3.9% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| National-scale licensing | +2.3% | UK, Nordics, Australia, emerging Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EHR-Integrated, Evidence-Based Answers at Point of Care

Clinicians currently spend approximately two hours per shift navigating reference websites, guideline portals, and drug databases. Embedded decision support is addressing this inefficiency by providing context-specific answers directly within electronic health records (EHR). Epic’s AI Charting, implemented in multiple U.S. systems since 2025, streamlines workflows by summarizing visits and identifying guideline deviations, reducing documentation time by up to 15 minutes per patient encounter.[1]Elsevier, “Elsevier expands ClinicalKey AI with unrivaled full-text knowledge base,” elsevier.com In 2026, Wolters Kluwer partnered with Microsoft to integrate UpToDate’s extensive database into Microsoft DAX Copilot, enabling users to access evidence without leaving the EHR.[2]Wolters Kluwer, “Wolters Kluwer unveils plans for Medi-Span Expert AI to advance Medication Intelligence for digital health,” wolterskluwer.com Hospitals are increasingly prioritizing single-sign-on capabilities and FHIR APIs that maintain audit trails, pressuring standalone vendors to adopt open connectors or risk losing market presence. This shift reflects a broader industry trend toward embedding intelligence directly into workflows, securing longer-term contracts for vendors that meet interoperability standards.

Clinician Productivity Pressure Driving AI Copilots

Physician burnout exceeded 50% in 2025, with charting and inbox management identified as primary contributors. This has driven demand for AI copilots that automate note creation and streamline administrative tasks. By mid-2025, Microsoft’s DAX Copilot had been adopted by over 200 health systems, saving an average of 5-7 minutes per office visit. EBSCO’s Dyna AI Mode, introduced in 2026, integrates conversational answers within DynaMed, recording each interaction with timestamps and enabling clinicians to incorporate evidence directly into their notes. These productivity gains are particularly significant in primary-care settings, where patient panel sizes have increased by 30% without corresponding changes in visit durations. Importantly, these tools are designed with human oversight to ensure compliance with emerging FDA guidelines, which emphasize clinician accountability for algorithmic outputs.

Medication Safety and Pharmacy CDS Modernization

Adverse drug events, many of which are preventable, cost U.S. hospitals an estimated USD 42 billion annually. Wolters Kluwer’s Medi-Span Expert AI, launched in 2026, introduces a context-aware protocol server that evaluates factors such as renal function, allergies, and genomics before finalizing prescriptions.[3]Premier, “Premier, Inc. Expands Clinical Decision Support (CDS) Capabilities with Acquisition of IllumiCare,” premierinc.com Premier’s acquisition of IllumiCare in 2025 enhanced real-time cost attribution and formulary adherence, delivering return-on-investment ratios as high as 10:1 by reducing the use of low-value medications. These advancements are transforming pharmacy clinical decision support (CDS) systems from static rule-based tools to dynamic, data-driven solutions that enhance medication safety.

Licensed, Publisher-Owned GenAI Copilots Build Trust

In 2025, only 40% of physicians expressed trust in AI-generated recommendations, citing concerns about inaccuracies and lack of transparency. Publishers are addressing these issues by training large language models (LLMs) exclusively on peer-reviewed content. Elsevier’s ClinicalKey AI, expanded in 2026, now provides access to full-text content from thousands of journals and practice guidelines, with updates occurring every 24 hours and each answer linked to its original source. Similarly, EBSCO’s Dyna AI framework employs a retrieval-augmented model to ensure the provenance of its answers. This approach not only builds trust among clinicians but also drives increased departmental spending on these tools, surpassing traditional library budgets.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| GenAI accuracy & safety concerns | -3.7% | Global, heightened in North America and EU | Short term (≤ 2 years) |

| Workflow & EHR integration backlogs | -2.9% | Global, acute where legacy EHR customizations dominate | Medium term (2-4 years) |

| Tighter CDS/AI regulatory obligations | -2.1% | North America, EU, emerging Brazil & Australia | Medium term (2-4 years) |

| Provenance/IP constraints on training data | -1.6% | Global, legal precedents in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GenAI Accuracy and Safety Concerns in Clinical Use

Benchmark studies have shown that general LLMs, when addressing clinical queries, can exhibit hallucination rates of up to 15%. These inaccuracies have occasionally resulted in the citation of non-existent sources or unsafe dosing recommendations. In response, the FDA introduced clinical decision support guidelines in January 2026, requiring provenance documentation, model update protocols, and rigorous post-market surveillance for higher-risk tools. These measures have narrowed previously broad exemptions. Similarly, Brazil's CFM Resolution in August 2026 mandated validation audits and prohibited the exclusive reliance on AI for critical communications. Specialties such as obstetrics and oncology, which face higher malpractice risks, remain cautious and are awaiting improvements in AI explainability.

Workflow/EHR Integration and IT Backlog Constraints

Hospitals manage over 50 legacy applications, creating significant challenges for integrating new Clinical Decision Support Systems (CDSS) within a complex network of proprietary APIs and custom templates. A 2025 survey of U.S. CIOs revealed that 68% identified EHR integration backlogs as the primary barrier to adoption. Major vendors like Epic, Oracle Health, and Meditech require separate connectors, increasing vendor maintenance costs. While SMART-on-FHIR applications offer a more lightweight solution, many health systems remain hesitant to share protected health information with external clouds, even with assurances of regional hosting and business associate agreements, resulting in slower implementation timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: EHR-Integrated, Evidence-Based Answers at Point of Care

In 2025, integrated EHR deployments dominated the AI in Clinical Knowledge Platforms market, capturing 58.18% of the revenue. Hospitals are increasingly opting for single-vendor solutions to ensure accountability, provide a seamless user experience, and maintain unified audit trails. Companies like Epic and Oracle Health embed features such as guideline checking, note summarization, and ambient documentation directly into core workflows. This integration reduces the need for clinicians to switch between applications and minimizes training requirements. While standalone CDSS is projected to grow at a robust 24.16% CAGR, it must either deepen its specialty focus or ensure cross-EHR interoperability to remain competitive. The market share for standalone tools in the AI in Clinical Knowledge Platforms space is expanding in ambulatory networks, particularly where diverse EHR systems dominate and modular tools outperform traditional monolithic stacks.

By Model: AI/ML Algorithms on the Rise

Knowledge-based platforms accounted for 65.13% of the 2025 revenue, driven by their transparent, human-edited rules that align with regulatory preferences for explainability. Platforms like UpToDate, DynaMed, and BMJ Best Practice rely on physician editors to curate recommendations and disclose conflicts of interest, fostering clinician trust. However, non-knowledge-based AI/ML algorithms are scaling at a 25.16% CAGR, leveraging retrieval-augmented generation to contextualize recommendations with the latest research. This development is expanding the AI in Clinical Knowledge Platforms market by introducing adaptive models that learn from institutional data patterns without requiring manual rule set updates.

By Delivery Mode: Cloud Solutions Surge

In 2025, on-premises deployments accounted for 58.19% of installations, driven by data-sovereignty mandates from HIPAA, GDPR, and China's Cybersecurity Law. Large academic institutions with robust IT teams prioritize control over customizations and research data. However, cloud vendors offering regionally hosted, SOC-2-certified environments are delivering monthly feature updates that on-premises systems cannot match. This advantage is driving a 26.13% CAGR in web-based solutions, particularly among community hospitals that lack the capital for server upgrades. As cybersecurity frameworks evolve and insurers push for zero-trust architectures, CIOs are reassessing total ownership costs, accelerating hybrid migrations.

By Setting: Ambulatory Practices Embrace AI

In 2025, inpatient settings captured 64.18% of the demand, driven by the need for real-time alerts in high-acuity scenarios, such as complex drug regimens and rapid sepsis detection. The AI in Clinical Knowledge Platforms market remains strong in this segment, as multidisciplinary teams rely on structured pathways integrated within EHR order sets. Premier’s Stanson Health, with its real-time cost attribution, highlights the shift in expectations from safety to value-based stewardship.

Ambulatory practices are projected to grow at a robust 25.27% CAGR. AI tools are assisting primary-care clinicians by preparing charts, drafting letters, and managing inboxes. With payer contracts increasingly emphasizing chronic-care quality metrics, clinics are adopting lightweight cloud solutions. These tools integrate seamlessly with platforms like athenahealth or eClinicalWorks, requiring minimal IT intervention and creating new opportunities for vendors.

By Application: Diagnostics and Guidelines Lead the Way

Drug-allergy alerts accounted for 32.16% of the 2025 revenue but are nearing saturation and facing rising override rates. Hospitals are refining these alerts to combat fatigue, reserving critical triggers for severe reactions like anaphylaxis. Despite this, drug-allergy alerts remain a fundamental safety feature in every EHR.

Diagnostic decision support, on the other hand, is forecast to grow at a 26.08% CAGR. Advanced AI models are integrating data from imaging, labs, genomics, and clinical notes to produce ranked differentials. This approach directly addresses diagnostic errors, a leading cause of malpractice in the U.S. Initial trials indicate improved accuracy in challenging cases, such as rare diseases and atypical oncology, driving significant interest from tertiary medical centers.

Geography Analysis

In 2025, North America led the AI in Clinical Knowledge Platforms market, contributing 42.18% of the revenue. This leadership is primarily due to Epic and Oracle Health, which collectively dominate over 70% of the electronic health record (EHR) market in U.S. hospitals. Additionally, clear FDA guidelines have exempted certain low-risk clinical decision support (CDS) tools from stringent regulations. The region faces significant burnout rates among healthcare professionals but continues to attract substantial venture capital funding, as demonstrated by Hippocratic AI's USD 126 million Series C funding round in April 2026. Combined with pressures from value-based payment models, these factors have created a market environment where stakeholders are willing to invest at a premium. Canada, while slightly behind the U.S., benefits from nationwide interoperability initiatives that effectively reduce integration costs.

Europe has maintained steady growth in the mid-teens range. The region's single-payer systems, such as NHS England, have utilized blanket licenses, as evidenced by their 2025 diagnostic AI registry, to ensure consistent access to AI tools for 1.5 million clinicians. However, the EU AI Act presents challenges by classifying most decision support tools as "high-risk," necessitating strict conformance audits and transparency requirements. This has resulted in longer procurement cycles. Despite these hurdles, the region demonstrates adaptability, with Germany's leading radiology firms and France's AP-HP projects serving as early compliance models.

Asia-Pacific is projected to achieve a strong 26.55% CAGR through 2031, driven by government mandates and minimal legacy IT constraints. In China, major technology companies like Alibaba Cloud and Tencent are driving the development of extensive telehealth platforms that extend to tier-2 cities. In India, the Ayushman Bharat Digital Mission is advancing FHIR-based personal health records, opening opportunities for third-party CDS applications. Japan is also making strides with its national electronic medication record system, which enhances pharmacy safety and encourages local vendors to integrate AI for polypharmacy management.

Competitive Landscape

The market remains moderately fragmented. Legacy content publishers such as Elsevier, Wolters Kluwer, and EBSCO combine extensive editorial teams with proprietary libraries, strengthening their network advantages among academic hospitals. EHR giants Epic and Oracle Health integrate third-party APIs to avoid the high costs of duplicating editorial workflows, allowing them to focus on platform orchestration. Niche players like Isabel Healthcare, VisualDx, and PEPID specialize in diagnostic solutions, often using SMART-on-FHIR wrappers for seamless deployment within any EHR.

M&A activity reflects a strategic push toward real-time cost and evidence synthesis. In June 2025, Premier acquired IllumiCare to incorporate cost transparency into Stanson Health alerts, enhancing differentiation from standard dosage-checking tools. Similarly, Doximity's USD 63 million acquisition of Pathway Medical in July 2025 aims to support free reference tools for its network of two million physicians while driving revenue through adjacent telehealth services.

Competitive priorities now focus on integration depth, citation transparency, and regulatory compliance. Publishers are investing in GenAI agents with full-text traceability, cloud-native companies emphasize rapid innovation, and established EHR providers leverage their existing customer bases to promote embedded intelligence. Price competition remains limited due to the high switching costs associated with integrating decision rules into clinical governance frameworks.

AI In Clinical Knowledge Platforms Industry Leaders

Wolters Kluwer Health

Merative

Elsevier Health

Zynx Health

WebMD/Medscape

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Artera.io launched an AI Services Model that pairs human and agent intelligence to craft bespoke solutions for specialty clinics and federal agencies.

- February 2026: Elsevier today announced major content and technology enhancements to ClinicalKey AI, its flagship clinical decision support tool, responding to clinicians’ growing demands for transparency, security and quality assurance in medical AI tools.

- September 2025: Wolters Kluwer Health introduced UpToDate Expert AI, an advanced generative AI-powered clinical decision support (CDS) solution developed to meet the requirements of healthcare professionals and systems effectively.

Global AI In Clinical Knowledge Platforms Market Report Scope

As per the scope of the report, AI in Clinical Knowledge Platforms refers to the integration of artificial intelligence, specifically machine learning (ML), natural language processing (NLP), and deep learning into digital systems that store, manage, and analyze medical information to support healthcare decision-making.

The AI in Clinical Knowledge Platforms Market is segmented by product, model, delivery mode, setting, application, and geography. By product, the market includes standalone clinical decision support systems (CDSS), integrated computerized physician order entry (CPOE) with CDSS, and integrated electronic health records (EHR) with CDSS. By model, the market is segmented into knowledge-based models and non-knowledge-based models (AI/ML). By delivery mode, the market is categorized into on-premises solutions and cloud/web solutions. By setting, the market is segmented into inpatient settings and ambulatory/outpatient settings. By application, the market includes drug allergy alerts, drug dosing & IV compatibility, clinical guidelines & pathways, point-of-care clinical answers, diagnostic decision support, and other applications. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Standalone CDSS |

| Integrated CPOE with CDSS |

| Integrated EHR with CDSS |

| Knowledge-based |

| Non-knowledge-based (AI/ML) |

| On-premises |

| Cloud/Web |

| Inpatient settings |

| Ambulatory/Outpatient settings |

| Drug allergy alerts |

| Drug dosing & IV compatibility |

| Clinical guidelines & pathways |

| Point-of-care clinical answers |

| Diagnostic decision support |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Standalone CDSS | |

| Integrated CPOE with CDSS | ||

| Integrated EHR with CDSS | ||

| By Model | Knowledge-based | |

| Non-knowledge-based (AI/ML) | ||

| By Delivery Mode | On-premises | |

| Cloud/Web | ||

| By Setting | Inpatient settings | |

| Ambulatory/Outpatient settings | ||

| By Application | Drug allergy alerts | |

| Drug dosing & IV compatibility | ||

| Clinical guidelines & pathways | ||

| Point-of-care clinical answers | ||

| Diagnostic decision support | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the AI in Clinical Knowledge Platforms market be by 2031?

The AI in Clinical Knowledge Platforms market size is projected to reach USD 8.9 billion by 2031, reflecting a 22.79% CAGR over 2026-2031.

Which segment is growing fastest within these platforms?

Standalone CDSS solutions show the highest growth, advancing at a 24.16% CAGR as ambulatory networks adopt cloud-first, EHR-agnostic tools.

Why are publishers launching their own GenAI copilots?

Clinicians demand transparent sourcing; publisher-owned models trained on proprietary peer-reviewed libraries build greater trust and meet emerging regulatory provenance requirements.

What geographic region offers the strongest growth outlook?

Asia-Pacific is forecast to post a 26.55% CAGR thanks to national digital-health mandates and lighter legacy IT, despite North America currently holding the largest revenue share.

How are hospitals addressing medication-safety gaps?

Systems deploy context-aware APIs like Medi-Span Expert AI that factor renal function, genomics, and real-time labs before finalizing orders, reducing costly adverse drug events.

What drives adoption in ambulatory care?

Primary-care clinicians facing rising panel sizes use AI copilots to auto-draft notes and manage inboxes, accelerating uptake in outpatient settings at a 25.27% CAGR.

Page last updated on: