Nitrile Medical Gloves Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

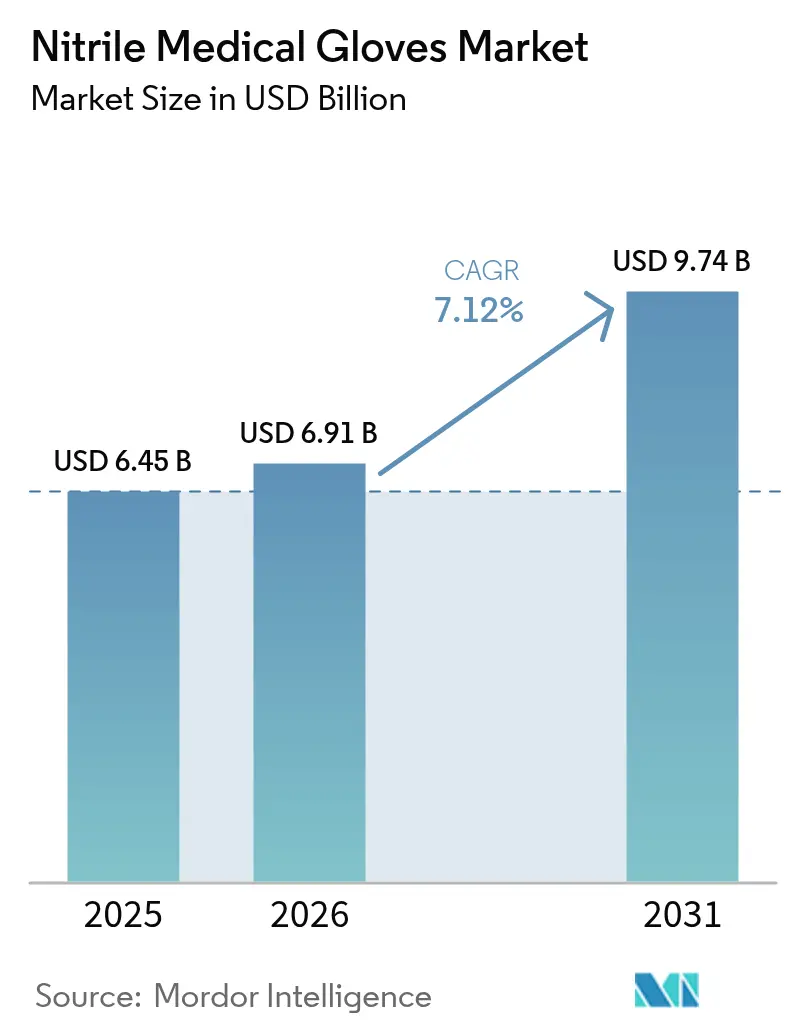

| Market Size (2026) | USD 6.91 Billion |

| Market Size (2031) | USD 9.74 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nitrile Medical Gloves Market Analysis by Mordor Intelligence

The nitrile medical gloves market size in 2026 is estimated at USD 6.91 billion, growing from 2025 value of USD 6.45 billion with 2031 projections showing USD 9.74 billion, growing at 7.12% CAGR over 2026-2031. Growth flows from stricter infection-control mandates, accelerating migration away from latex, and the elevated role of disposable barrier protection within OSHA’s bloodborne pathogen framework [1]Source: ScienceDirect, “Natural Rubber – Increasing Diversity of an Irreplaceable Renewable Resource,” sciencedirect.com. Price pressure eased as procurement teams prioritize verified performance, supply-chain traceability, and waste-reduction credentials. At the same time, US tariff escalation on Chinese gloves is realigning trade lanes, steering volume toward Malaysian and Thai producers. Automation, vertical NBR integration, and early moves into biodegradable offerings create the most visible competitive differentiators across the nitrile medical gloves market.

Key Report Takeaways

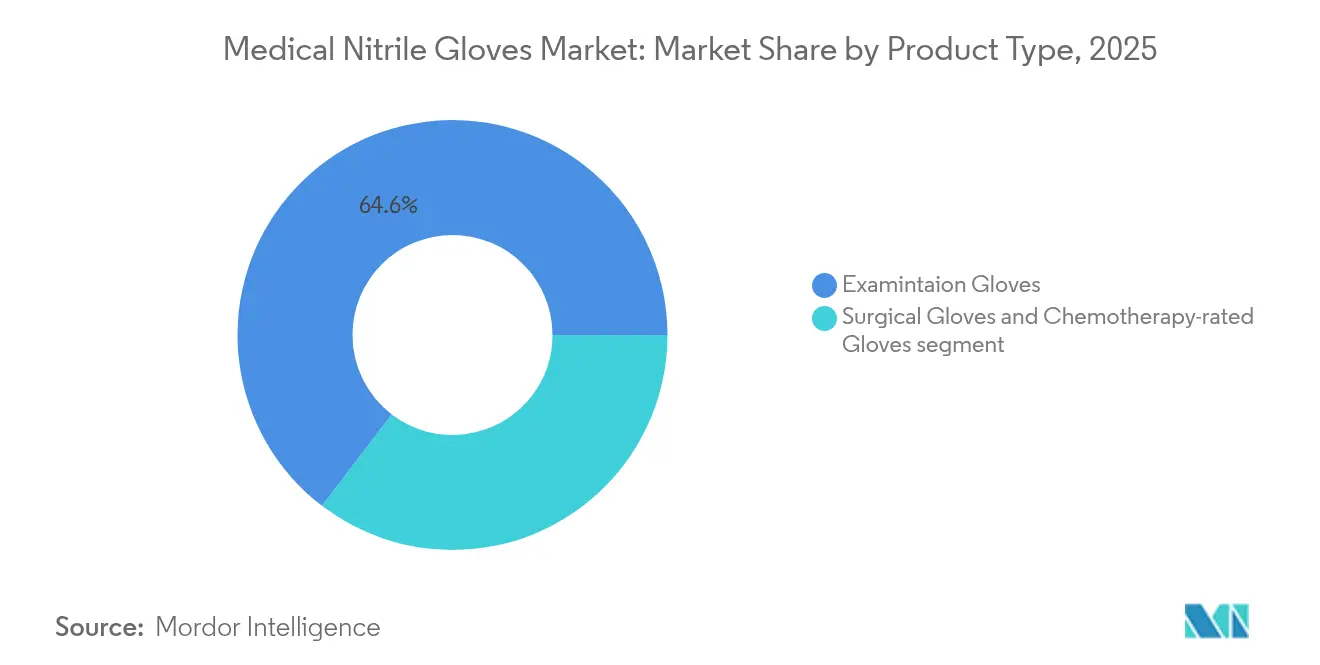

- By product type, examination gloves held 64.62% of nitrile medical gloves market share in 2025 while surgical gloves are projected to expand at a 6.31% CAGR through 2031.

- By form, powder-free variants commanded 87.05% of the nitrile medical gloves market size in 2025 and continue growing at 6.88% CAGR.

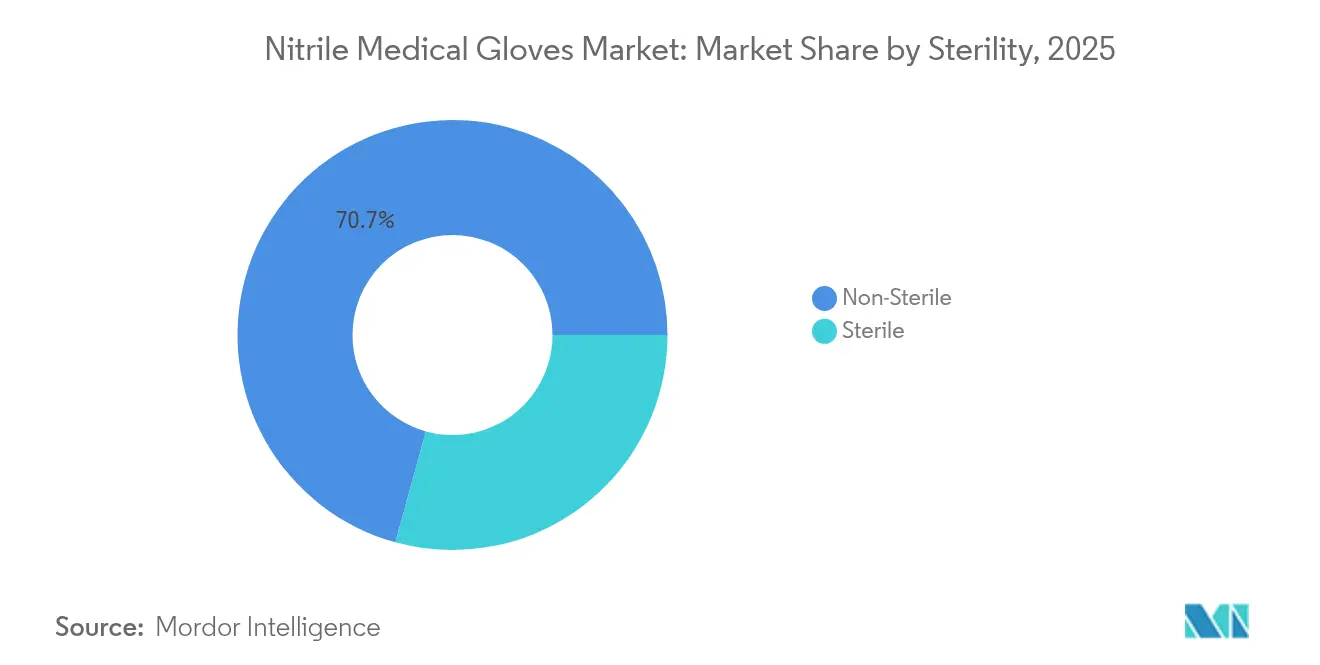

- By sterility, non-sterile gloves captured 70.72% of nitrile medical gloves market size in 2025; sterile demand is rising at 6.9% CAGR.

- By end user, hospitals and clinics contributed 57.10% revenue in 2025, whereas home-healthcare segment is advancing at a 6.11% CAGR.

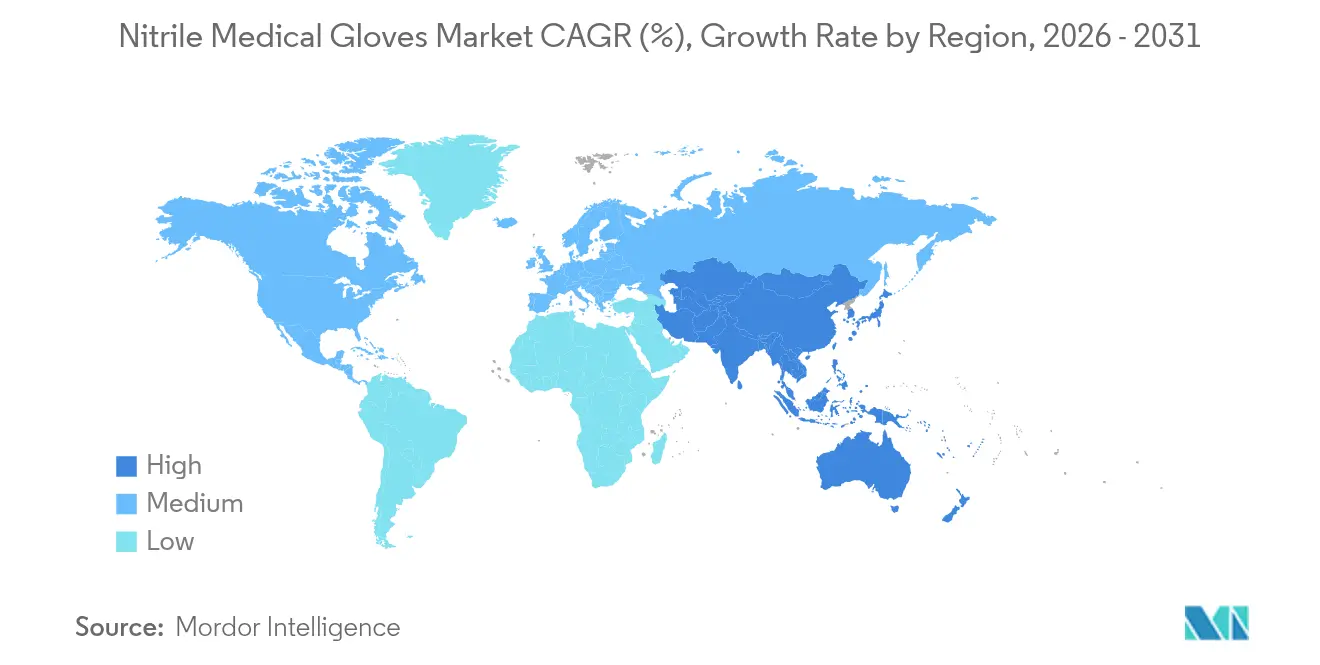

- By geography, North America led with 37.20% revenue share in 2025, while Asia-Pacific delivers the fastest 7.16% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nitrile Medical Gloves Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical procedure volumes worldwide | +1.20% | Global, led by North America & Europe | Medium term (2-4 years) |

| Stringent infection-control regulations & OSHA compliance | +0.80% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Shift from latex to nitrile due to allergy concerns | +0.60% | Global, led by developed markets | Long term (≥ 4 years) |

| Capacity investments in NBR latex plants in ASEAN | +0.40% | ASEAN core, global spill-over | Medium term (2-4 years) |

| AI-enabled glove defect-detection lines | +0.30% | Global, early adoption in Malaysia & Thailand | Long term (≥ 4 years) |

| Surge in tele-health home-testing kits requiring disposable exam gloves | +0.25% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Procedure Volumes Worldwide

Outpatient centers now perform a larger share of minimally invasive surgeries, each consuming 15-20 glove pairs across peri-operative phases. Aging demographics and chronic illness prevalence keep procedure counts on an upward trend, directly scaling glove demand. Powder-free nitrile products are preferred for surgical tasks because they combine puncture resistance with low allergenic risk. As cardiovascular, orthopedic, and cancer interventions climb, the nitrile medical gloves market absorbs steady incremental volume.

Stringent Infection-Control Regulations & OSHA Compliance

OSHA’s 2024 update expanded inspection scope and documentation requirements, repositioning gloves as strategic safety assets rather than commodities. Hospitals weigh documented pin-hole rates, tensile strength data, and traceability records before awarding contracts. Similar requirements under the EU Medical Device Regulation harmonize performance baselines, raising the entry bar for low-cost producers. As compliance costs of healthcare-associated infections reach USD 28-45 billion per year in the United States, buyers increasingly select premium nitrile options to reduce liability.

Shift from Latex to Nitrile Due to Allergy Concerns

Workplace latex allergies affect 8-12% of healthcare professionals, exposing providers to litigation risk. System-wide latex-free policies have become standard across many hospital groups, locking-in multiyear nitrile purchase commitments. With superior chemical resistance, nitrile also covers chemotherapy preparation and extended procedures, reinforcing adoption across allied departments.

AI-Enabled Glove Defect-Detection Lines Improving Yield

Machine-vision systems now catch 99.5% of defects, versus 95% under manual inspection, shrinking rejection rates by up to 40% and lifting effective capacity [2]Source: ScienceDirect, “Natural Rubber – Increasing Diversity of an Irreplaceable Renewable Resource,” sciencedirect.com . Hartalega’s 85% automation shows how data-driven efficiency supports premium pricing and regulatory documentation.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile NBR raw-material prices linked to butadiene supply | -0.90% | Global, acute in ASEAN | Short term (≤ 2 years) |

| Rising environmental scrutiny over non-biodegradable nitrile waste | -0.70% | EU & North America, expanding globally | Long term (≥ 4 years) |

| Over-capacity risk as pandemic-driven demand normalizes | -0.65% | Asia (e.g., Malaysia, Thailand, China) and North America | Short term (≤ 2 years) |

| Trade protectionism & anti-dumping duties on Asian glove exports | -0.85% | North America, Europe, and Asian Countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile NBR Raw-Material Prices Linked to Butadiene Supply

Butadiene shortages stemming from refinery outages and a looming natural-rubber gap place immediate margin pressure on manufacturers that spend 40-50% of cost on latex inputs. With limited medical-grade substitutes, glove plants hedge feedstock futures and diversify suppliers to manage swings.

Rising Environmental Scrutiny Over Non-Biodegradable Nitrile Waste

Traditional nitrile takes decades to break down, prompting EU discussions on extended-producer responsibility. Ansell confirms the polymer’s inert structure resists microbial attack. Early biodegradable launches, such as Top Glove’s BioGreen line, indicate future standards, but scale and cost parity have yet to materialize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Examination Dominance Drives Volume Growth

Examination gloves held 64.62% of nitrile medical gloves market share in 2025, underpinned by routine patient contact across all healthcare settings. OSHA’s broad definition of exposure risk keeps examination demand resilient as every blood draw, transport, or specimen handling task requires disposable protection. As a result, the nitrile medical gloves market size allocated to examination lines surpasses USD 4.17 billion, giving manufacturers predictable high-throughput volumes.

Surgical gloves are gaining at a 6.31% CAGR through 2031 as procedure counts rise and surgeons demand tighter pin-hole specifications. Although accounting for a smaller piece of nitrile medical gloves market size today, the segment secures premium pricing because of sterility validation, exact sizing, and extended cuff lengths. Chemotherapy-rated gloves form a niche but high-margin pocket as oncology units require thicker materials for cytotoxic resistance, demonstrating how value migrates toward application-specific performance rather than price alone.

By Form: Powder-Free Preference Reflects Safety Evolution

Powder-free variants represented 87.05% of nitrile medical gloves market size in 2025, fueled by the US FDA ban on surgical glove powder and cornstarch contamination concerns. Polymer-coated interiors replicate easy donning, enabling swift hospital conversion with minimal workflow disruption.

Powdered gloves now cater mainly to lower-risk industrial or low-income healthcare settings, holding a thin residual share. As modern high-speed formers and polymer coatings narrow cost gaps to under 5%, even cost-sensitive buyers adopt powder-free lines, raising the baseline quality level across the nitrile medical gloves market.

By Sterility: Non-Sterile Applications Drive Market Volume

Non-sterile products covered 70.72% of nitrile medical gloves market size in 2025 because outpatient clinics, emergency rooms, and home-care programs consume gloves for each patient encounter. Bulk pack formats and streamlined sizing simplify logistics and keep per-pair pricing competitive.

Sterile gloves, expanding at 6.9% CAGR, respond to higher surgical throughput and sterile pharmacy compounding rules. Hospitals deploy risk-based purchasing protocols that limit sterile use to procedures demanding validated asepsis, balancing cost and safety while sustaining predictable growth for premium grades.

By End User: Hospital Consolidation Drives Procurement Efficiency

Hospitals and clinics contributed 57.10% of 2025 revenue, leveraging group-purchasing contracts that stipulate ASTM performance and lot-traceability clauses. Consolidated health systems favor multiyear supply deals with audited plants, shutting smaller unverified suppliers out of large bids.

Home-healthcare shows the fastest 6.11% CAGR as aging demographics push care into houses, drawing sustained glove demand for wound care and chronic-disease management. Ambulatory surgery centers and labs seek premium specialty lines such as extra-thin tactile gloves or chemo-resistant variants, reinforcing the nitrile medical gloves market’s shift to differentiated SKUs.

Geography Analysis

North America commanded 37.20% of 2025 revenue, reflecting OSHA enforcement intensity, high per-capita surgical rates, and the preference for supply chains viewed as geopolitically secure. With US tariffs on Chinese gloves slated for 25% by 2026, buyers redirect orders to Mexico and Canada, reinforcing near-shoring trajectories. The nitrile medical gloves market sees new North American lines financed to capture that regional premium.

Asia-Pacific records the fastest 7.16% CAGR to 2031 as public-hospital construction, health-insurance expansion, and greater infection-control awareness accelerate glove penetration. Malaysian and Thai producers capitalize on regional NBR proximity and automation investment to supply export markets, gaining share as tariffs constrain Chinese competitors. Domestic demand in Indonesia, Vietnam, and the Philippines climbs as universal healthcare schemes widen access.

Europe is a compliance-driven market where extended-producer responsibility for medical waste is shaping procurement toward lifecycle data. Hospitals pilot biodegradable nitrile options and require environmental product declarations, nudging suppliers to disclose carbon footprints. Meanwhile, Middle East, Africa, and South America represent smaller but double-digit growth adjacencies, where rising surgical volumes intersect with price sensitivity, encouraging mid-tier nitrile offerings.

Competitive Landscape

The nitrile medical gloves market centers on Malaysia, where Top Glove, Hartalega, and Kossan own a significant percentage of installed capacity. Scale, automation, and NBR integration allow these firms to sustain margins despite post-pandemic price normalization. Top Glove’s January 2025 results showed 80% revenue growth and a 325% profit rebound as US customers shifted orders away from China.

Technology investment remains the key differentiator. Hartalega targets 2.7 billion-piece output on 85% automated lines by FY2025, expecting lower unit cost and consistent defect levels. Chinese firms such as INTCO Medical respond by planning offshore plants to bypass tariffs, but capital intensity and regulatory documentation hurdles slow execution.

Sustainability is the next battleground. Top Glove’s BioGreen nitrile and Unigloves’ BioTouch line underscore an industry pivot toward waste mitigation. Early adopters win pilots with EU hospitals seeking circular procurement. Nonetheless, cost parity and certification remain barriers, suggesting incremental rather than disruptive transition over the forecast horizon.

Nitrile Medical Gloves Industry Leaders

Dynarex Corporation

Halyard

Superior Gloves

Shield Scientific

Ansell LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The United States imposed a 10% tariff on Chinese rubber gloves, amplifying earlier duties on medical gloves and creating route-to-market opportunities for Malaysian and Thai suppliers.

- August 2024: Grainger released biodegradability guidance directing healthcare buyers to full lifecycle assessments when choosing nitrile gloves.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study calls the nitrile medical gloves market the total annual revenues generated from single-use, non-latex, nitrile butadiene rubber gloves that carry medical or examination grade listings and are intended for patient care, diagnostics, surgery, or home-health kits. The value base is manufacturer-level sales converted to constant 2025 USD.

Scope exclusion: Gloves sold primarily for industrial safety, food handling, or clean-room electronics are not counted.

Segmentation Overview

- By Product Type

- Examination Gloves

- Surgical Gloves

- Chemotherapy-rated Gloves

- By Form

- Powder-Free

- Powdered

- By Sterility

- Non-Sterile

- Sterile

- By End User

- Hospitals & Clinics

- Ambulatory Surgery Centers

- Diagnostic Laboratories

- Home Healthcare & Tele-medicine Kits

- Dental & Veterinary Practices

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts hold structured calls with distributors, infection-control nurses, procurement managers, and materials scientists across North America, Europe, ASEAN, and the Gulf. These conversations validate usage rates, average selling prices, tariff pass-through, and latex-allergy driven conversion trends that secondary sources only hint at.

Desk Research

We start by combing trusted open data such as US FDA 510(k) device clearances, EU MDR notified-body listings, UN Comtrade HS-4015 export flows, and monthly Malaysian Rubber Board production bulletins. Hospital procedure volumes from OECD Health Stats, CDC National Health Care Safety Network infection data, and WHO surgical safety guidelines supply demand fingerprints. Premium datasets, including D&B Hoovers financials and Dow Jones Factiva news archives, help us map revenues and capacity shifts at leading producers. This list is illustrative; dozens of additional public and proprietary sources inform the final model.

Market-Sizing & Forecasting

A top-down build begins with national procedure counts, patient-encounter ratios, and glove-per-encounter benchmarks. Import-export reconciliations reconstruct unreported domestic output, which is then tested against sampled supplier roll-ups for bottom-up sanity. Key variables like surgical volume growth, healthcare expenditure per capita, NBR feedstock price index, regulatory recall events, and hospital bed additions feed a multivariate regression that generates the 2025-2030 curve. Where bottom-up gaps appear (e.g. in smaller LATAM markets), region-level ASP×volume proxies bridge the void.

Data Validation & Update Cycle

Outputs pass variance checks against historical trade elasticities and peer ratios, followed by a two-layer analyst review before sign-off. We refresh the dataset every twelve months, and extraordinary events such as pandemic outbreaks or tariff shocks trigger an interim update so clients always receive the latest view.

Why Mordor's Nitrile Medical Gloves Baseline Commands Confidence

Published numbers often diverge because firms pick unequal scopes, inconsistent base years, or untested price assumptions, which can mislead planners. By limiting scope strictly to medical-grade units and aligning every currency and tariff to 2025 realities, we reduce hidden distortions.

Key gap drivers include: some publishers merging industrial and food-service demand with healthcare volumes; others anchoring to pandemic-era spot prices without normalizing post-COVID corrections; a few using static exchange rates or three-year-old import data. Our annual refresh and dual-path (top-down plus selective bottom-up) cross-checks keep Mordor's baseline balanced and traceable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.45 B (2025) | Mordor Intelligence | - |

| USD 4.60 B (2025) | Regional Consultancy A | Excludes home-health and veterinary demand; relies on limited ASP panels |

| USD 3.46 B (2024) | Global Consultancy B | Earlier base year and no currency rebasing to 2025 dollars |

| USD 34.00 B (2025) | Industry Journal C | Combines industrial, food, and medical grades into one pool |

In short, our disciplined scope setting, variable selection, and yearly refresh cycle give decision-makers a dependable, middle-path baseline that is neither inflated by non-medical volumes nor narrowed by data gaps.

Key Questions Answered in the Report

What is the current size of the nitrile medical gloves market?

The nitrile medical gloves market stands at USD 6.91 billion in 2026 and is projected to reach USD 9.74 billion by 2031.

Which product segment dominates the market?

Examination gloves dominate with 64.62% of market share in 2025, owing to their routine use across healthcare settings.

Why are powder-free gloves preferred in hospitals?

Powder-free variants eliminate particulate contamination risks and now account for 87.05% of market size, backed by FDA and OSHA guidance.

How will US tariffs influence global supply chains?

Tariffs rising to 25% on Chinese gloves by 2026 are redirecting US demand to Malaysian, Thai, Mexican, and Canadian manufacturers.

Are biodegradable nitrile gloves commercially viable?

Early launches like Top Glove’s BioGreen and Unigloves’ BioTouch show promise, but cost parity and certification hurdles limit large-scale adoption in the near term.

Page last updated on: