Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

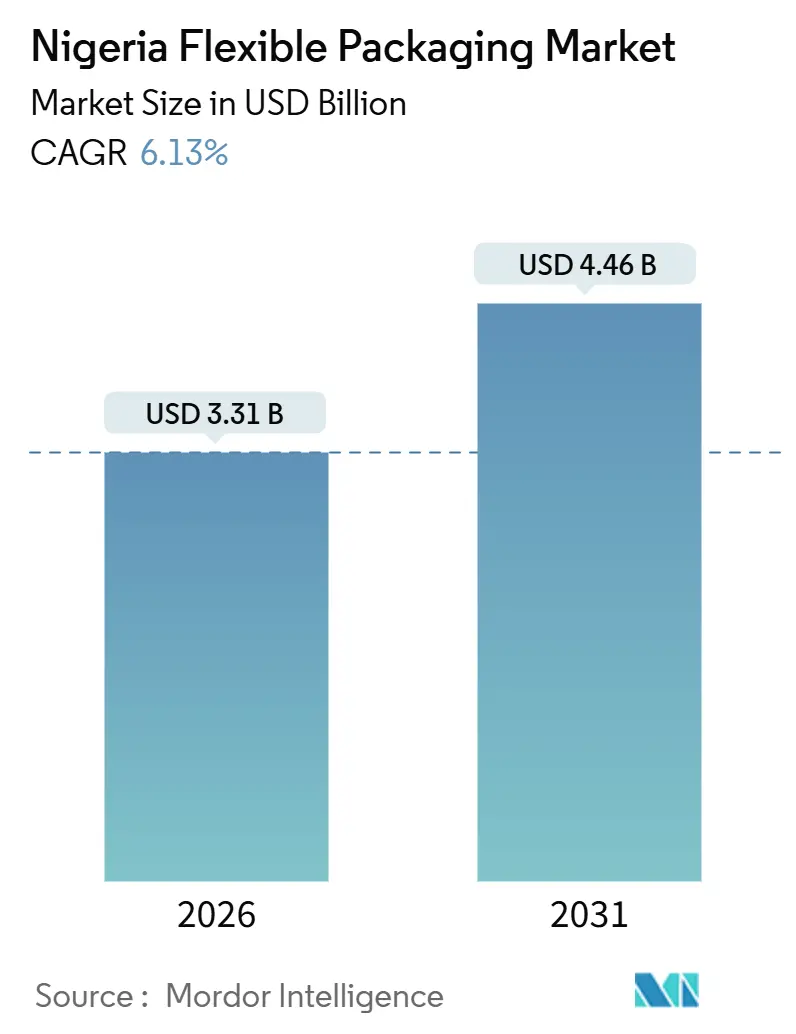

| Market Size (2026) | USD 3.31 Billion |

| Market Size (2031) | USD 4.46 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

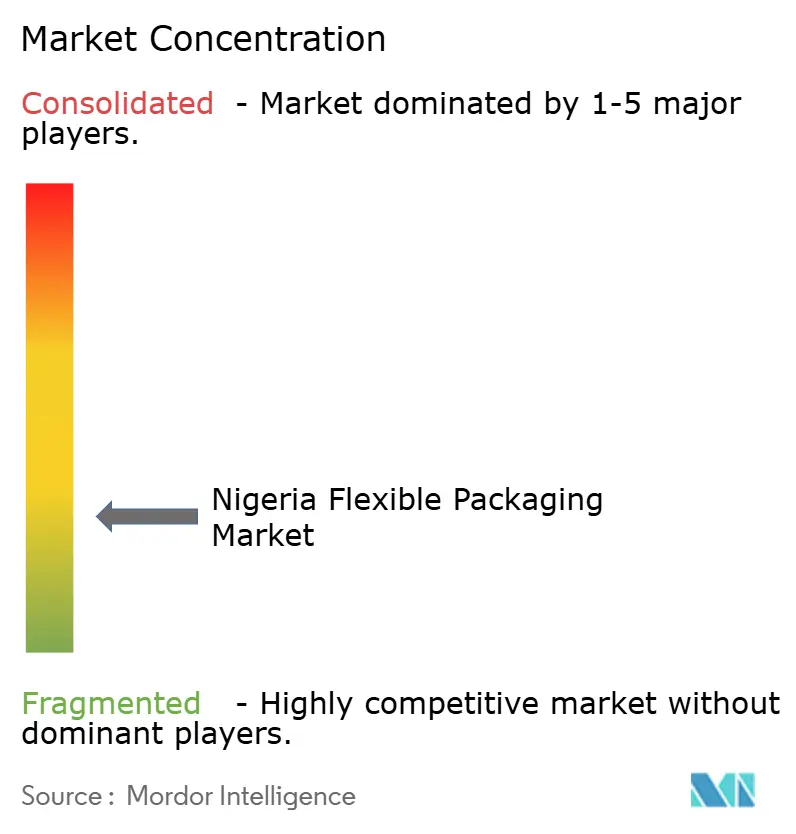

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Flexible Packaging Market Analysis by Mordor Intelligence

The Nigeria flexible packaging market size stood at USD 3.31 billion in 2026 and is projected to reach USD 4.46 billion in 2031, reflecting a 6.13% CAGR over the forecast period. The upward trajectory is underpinned by rapid urbanization, rising disposable incomes, and an accelerating shift from rigid to lightweight packaging that lowers freight costs and extends shelf life in humid conditions. Robust e-commerce adoption, which accounted for 15% of retail transactions in 2025, continues to elevate demand for tamper-evident pouches that protect items during multi-stage delivery. Growth is further amplified by tax incentives that reward converters sourcing 60% of resin from Dangote Petrochemical’s domestic lines, reducing landed film costs by 12%. Multinational FMCG players expanding local capacity in Lagos, Ogun, and Rivers states stabilize contract volumes for converters, while micro-distribution sachet models keep flexible formats indispensable for low-income households. Sustained investment in food processing, 8.2% year-on-year output growth in 2025, reinforces the pull for high-barrier laminates that lengthen shelf life without a cold chain.

Key Report Takeaways

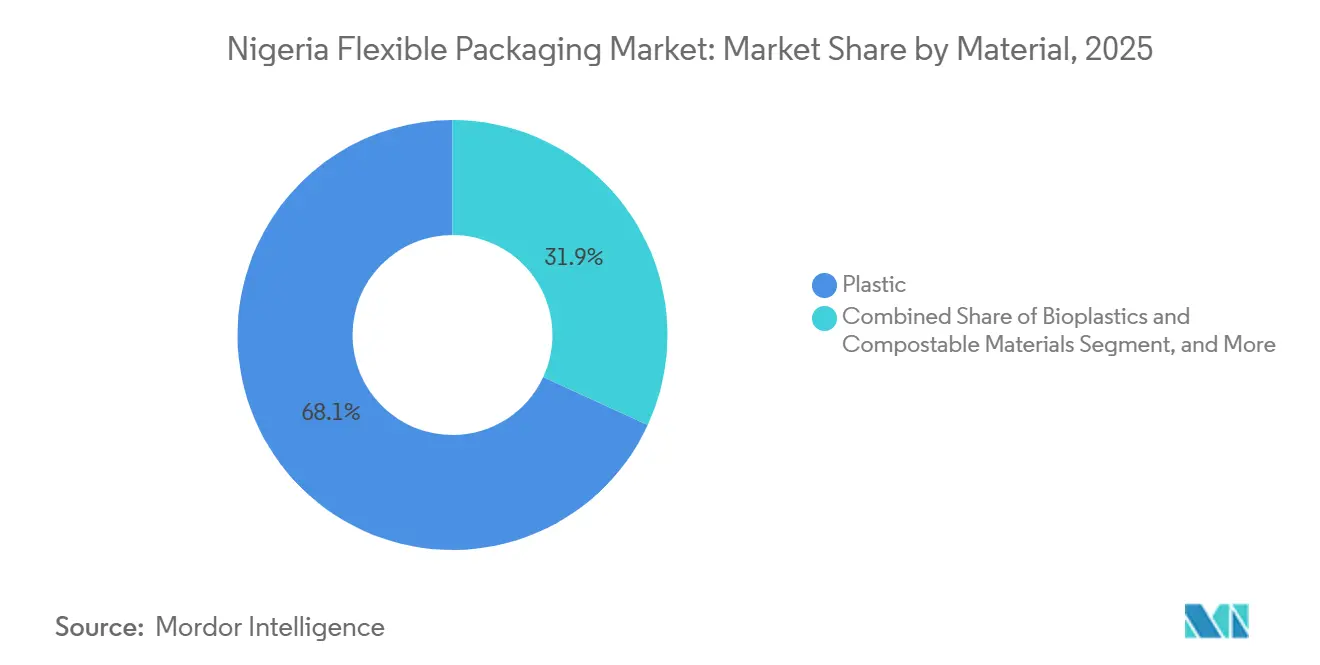

- By material, plastics led with 68.12% of Nigeria flexible packaging market share in 2025; bioplastics are forecast to grow at a 7.52% CAGR through 2031.

- By product type, bags and pouches accounted for 47.63% of the revenue in 2025, while sachets and stick packs are expected to expand at a 7.32% CAGR to 2031.

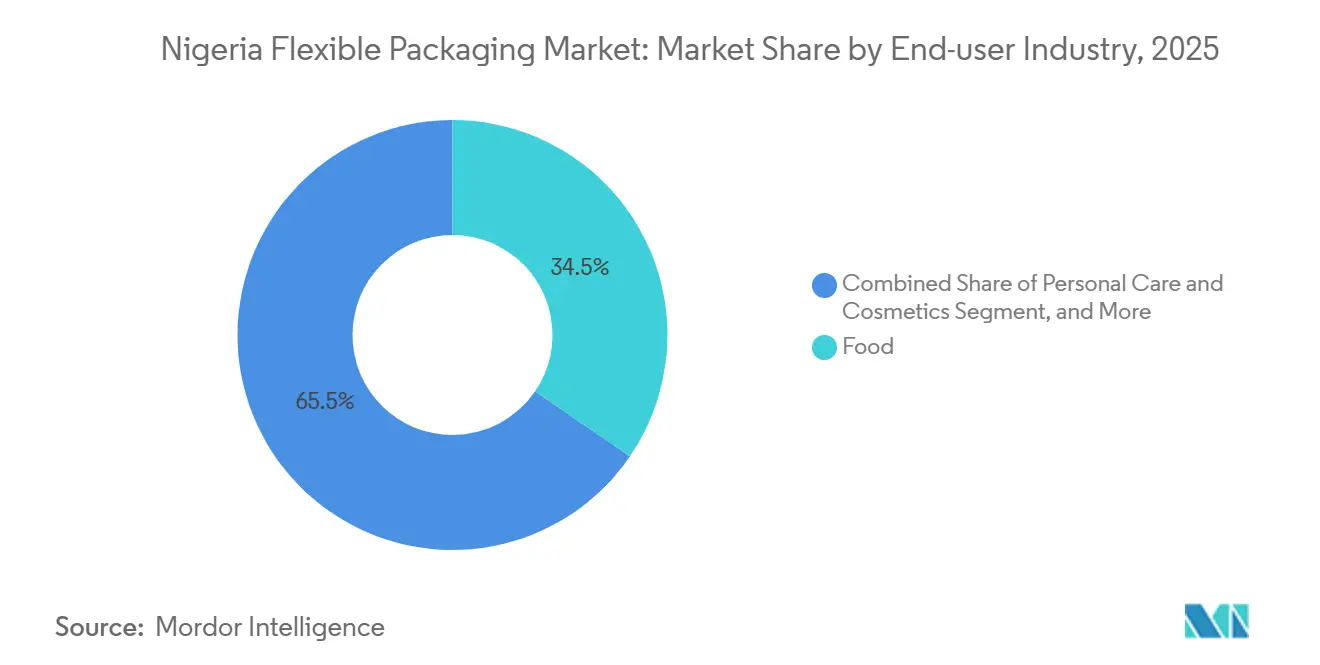

- By end-user industry, food captured 34.53% of Nigeria flexible packaging market size in 2025 and personal care is advancing at a 7.73% CAGR through 2031.

- By printing technology, flexography held 45.72% share of Nigeria flexible packaging market size in 2025; digital printing is projected to grow at an 8.43% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nigeria Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of Nigeria's E-commerce Sector | +1.2% | National, with early concentration in Lagos, Abuja, and Port Harcourt | Short term (≤ 2 years) |

| Expanding Processed Food Manufacturing Capacity | +1.4% | National, with clusters in Ogun, Lagos, and Kano states | Medium term (2-4 years) |

| Shift From Rigid to Flexible Formats Reducing Logistics Costs | +0.9% | National, particularly last-mile distribution networks | Medium term (2-4 years) |

| Rising Investments by FMCG Brand Owners in Local Converting | +1.1% | National, anchored in Lagos-Ogun industrial corridor | Short term (≤ 2 years) |

| Federal Tax Incentives for Polymer Backward Integration (2026 onward) | +0.8% | National, with spillover to West African export markets | Long term (≥ 4 years) |

| Growth of Refill-on-the-Go Micro-distribution Models | +0.7% | National, strongest in peri-urban and rural markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth Of Nigeria's E-Commerce Sector

Nigeria’s online retail penetration increased from 8% in 2022 to 15% in 2025, creating new requirements for lightweight, flexible packs that can withstand up to nine handling points before final delivery. Marketplaces such as Jumia and Konga reported a combined 22 million monthly active users in 2025, 60% of whose orders are for food and personal-care items that require moisture barriers. [1]International Trade Administration, “Nigeria E-Commerce Overview,” trade.gov Demand for stand-up pouches and pillow packs that reduce parcel weight by up to 60% enables couriers to meet 48-hour delivery promises in congested Lagos corridors, where average speeds are only 12 km per hour. Converters that embed QR codes and NFC tags provide authentication and brand-engagement features that e-commerce sellers value for loyalty campaigns. These attributes have cemented the Nigeria flexible packaging market as a pivotal enabler of direct-to-consumer strategies.

Expanding Processed Food Manufacturing Capacity

Food processors increased installed capacity by 8.2% in 2025, drawing flexible laminates with oxygen and grease barriers into noodle, pasta, and confectionery lines. [2]USDA Foreign Agricultural Service, “Food Processing Industry Report 2025,” fas.usda.gov Nestlé’s USD 30 million Ogun plant, inaugurated in September 2025, alone requires 500 million BOPP pouches each year. Cluster incentives within Kaduna and Kano agro-processing zones reduce transport distances, enabling converters to deliver within 72 hours rather than several weeks. ISO 22000 compliance is now a de facto entry ticket for suppliers, and converters unable to certify lose access to multinational tenders. This manufacturing boom anchors the Nigeria flexible packaging market, linking film demand tightly to local value-added production in grains, dairy, and snacks.

Shift From Rigid To Flexible Formats Reducing Logistics Costs

Brand owners can achieve savings of up to 40% on freight by replacing HDPE bottles with PE pouches, a critical lever in a country where diesel averages USD 1.65 per liter. Last-mile shippers fit 20% more flexible units per delivery van, trimming trips and emissions. Sachet formats also lower unit prices to NGN 50 (USD 0.06) for low-income households, enhancing affordability and market reach. These efficiencies accelerate the Nigeria flexible packaging market, particularly in rural zones where transport infrastructure is underdeveloped. Rigid formats persist in niche premium segments, yet overall momentum favors lighter, collapsible packs.

Rising Investments By FMCG Brand Owners In Local Converting

Multinationals invested USD 420 million in Nigerian capacity expansions between 2024 and 2025, often adding captive printing and lamination lines that internalize a third of their packaging needs. Unilever’s 2025 rotogravure hall in Agbara prints 500 million sachets annually, while Coca-Cola HBC’s Port Harcourt hub integrates shrink-sleeve production. These moves stabilize baseline volumes for resin suppliers and drive higher technical standards across the Nigeria flexible packaging market. Converters with ISO 9001 and HACCP certifications secure multi-year contracts but commit to annual price re-openers tied to naira volatility, which squeezes margins and incentivizes investments in energy-efficient presses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Polymer Resin Prices Linked to Crude Oil | -0.9% | National, with acute exposure for import-dependent converters | Short term (≤ 2 years) |

| Emerging Single-Use Plastic Restrictions | -0.6% | National, with pilot enforcement in Lagos and Abuja | Medium term (2-4 years) |

| Chronic Electricity Shortages Raising Operating Costs | -0.7% | National, most severe in northern states | Long term (≥ 4 years) |

| Surge in Counterfeit Flexible Packs Undermining Brand Trust | -0.5% | National, concentrated in pharmaceutical and sachet water segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Polymer Resin Prices Linked To Crude Oil

Polyethylene and polypropylene traded between USD 1,100 and USD 1,650 per metric ton during 2024-2025, mirroring Brent swings and naira depreciation. Unhedged converters absorbed 8%-12% margin erosion on fixed-price contracts, prompting quarterly repricing that strained buyer relationships. The naira lost 28% against the U.S. dollar in 2025, magnifying import pain and choking working capital for smaller operators. Dangote’s domestic PP output, online since December 2025, promises lead-time relief yet remains tied to crude feedstock dynamics. Until price stability sets in, resin volatility will temper Nigeria flexible packaging market expansion.

Emerging Single-Use Plastic Restrictions

Lagos State banned non-biodegradable beverage sachets in March 2024, giving the industry until December 2027 to transition to certified compostable films. [3]Lagos State Environmental Protection Agency, “Single-Use Plastic Ban,” lasepa.gov.ng Draft federal EPR rules issued in June 2025 add a 2%-4% recyclate-funding surcharge to converter revenues. Retrofitting a single PE line for PLA costs USD 500,000-2 million, creating entry barriers for thinly capitalized firms. NESREA levied NGN 85 million (USD 105,000) in fines during 2025, signaling stepped-up enforcement. Compliance uncertainty moderates enthusiasm in the Nigeria flexible packaging market, though early movers in bioplastics secure premium contracts from sustainability-minded brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Polyethylene Anchors Volume, Bioplastics Capture Premium Tier

Plastics contributed 68.12% to Nigeria flexible packaging market share in 2025, with PE films dominating inexpensive sachet water, detergents, and snack packs due to moisture resistance and low sealing temperatures. BOPP laminated with CPP serves confectionery and pharmaceutical blister packs where gloss and heat-seal integrity are critical. Bioplastics, while holding below 3% in 2025, are forecast to grow at 7.52% through 2031 as Lagos restrictions spur demand for compostable alternatives that degrade within 180 days under industrial conditions. Importing PLA and PHA from Europe and Southeast Asia at premiums of 40% over PE challenges price-sensitive SKUs, yet Unilever’s pledge to source 25% renewable content by 2030 signals steady upscale demand. Paper laminates carve a niche in artisanal dry-food brands targeting eco-conscious consumers, despite absorbing 15% more moisture than PE in tropical climates.

Converters with ASTM D6400 accreditation and collection partnerships secure higher-margin orders, while smaller operators remain entrenched in commodity PE. Dangote’s PP output reduces import reliance, shrinking lead times to two weeks and improving Nigeria flexible packaging market competitiveness. Aluminum foil laminates stay concentrated in premium dairy and pharmaceutical oxygen-barrier uses because average unit costs run 60%-80% above BOPP. The material mix will thus evolve slowly, with PE anchoring mass-volume demand and bioplastics gaining calculated share in regulated segments.

By Product Type: Sachets Proliferate In Informal Retail

Bags and pouches held 47.63% of revenue in 2025, spanning stand-up, pillow, and flat variants that service juice, yogurt, and detergent brands across modern and traditional trade. Sachets and stick packs are projected for a 7.32% CAGR to 2031, sustained by kiosks handling 65% of FMCG sales and catering to households spending NGN 50-200 (USD 0.06-0.25) per purchase. Maggi seasoning, Omo detergent, and Always sanitary pads exemplify this micro-pack model, ensuring broad rural reach. Films and wraps for fresh produce and bakery track cold-chain and supermarket growth yet remain capped by a modern-retail penetration of only 12% of grocery sales.

Converters operating 500-unit-per-minute sachet lines with holographic strips deter counterfeiting in pharmaceutical applications, adding value beyond basic commodity supply. Resealable zipper and spout pouches gain ground in juice and liquid soap thanks to portion control and reduced spill risk, although unit costs remain higher than single-use sachets. As disposable incomes rise and sustainability pressure mounts, a gradual trade-up from one-time sachets to reclosable pouches may lift average selling prices within the Nigeria flexible packaging market.

By End-User Industry: Food Dominates, Personal Care Accelerates

Food captured 34.53% of Nigeria flexible packaging market size in 2025, fueled by demand spikes in noodles, snacks, baked goods, and pet food as urban routines tighten. Multilayer laminates with oxygen scavengers extend shelf life to 12 months without refrigeration, critical amid erratic power supply. Personal-care packages, forecast for a 7.73% CAGR to 2031, ride a 25 million-household middle class that favors branded skincare, soaps, and deodorants. Sachet formats retain appeal for cost-sensitive consumers, but reclosable pouches offer premium upsell potential.

Pharmaceutical packs comply with NAFDAC serialization mandates requiring track-and-trace codes on each unit, upping technical barriers and margins. Beverage formats confront Lagos single-use bans yet grow in jurisdictions without enforcement. Fertilizer and seed bags under the Agricultural Transformation Agenda add volume to woven PP sacks with PE liners, underscoring agriculture’s linkage to the Nigeria flexible packaging market. Industrial chemicals and lubricants adopt stand-up pouches and FIBCs to cut return-logistics costs, further diversifying end-user demand.

By Printing Technology: Digital Gains On Short Runs

Flexography generated 45.72% of revenue in 2025, excelling in runs above 500,000 units where plate amortization pushes per-pack graphics below USD 0.02. Digital printing is poised for an 8.43% CAGR to 2031, driven by artisanal foods, subscription boxes, and e-commerce brands that refresh SKUs monthly and value variable data. Xeikon and HP Indigo units installed in 2024-2025 enable same-day proofs, eliminating the need for four-week plate-making cycles. Rotogravure retains its prestige in the chocolate and pharmaceutical industries, where color fidelity is crucial, yet the high costs of cylinder plates, ranging from USD 2,000 to USD 5,000 per design, deter brands with fluid portfolios.

Converters integrating digital presses with cloud portals can accept orders as small as 5,000 packs, widening service reach. Energy-efficient LED UV inks also cut curing costs by 30% compared with solvent-based flexo, partially offsetting Nigeria’s high electricity tariffs. The technology mix reinforces the Nigeria flexible packaging market’s twin priorities of high-volume efficiency and short-run agility.

Geography Analysis

Lagos and Ogun states host around 60% of the nation’s converting lines, leveraging deepwater port access at Apapa and Tin Can Island for resin imports and West African exports. Ogun’s lower land costs and enterprise zones drew Nestlé, Unilever, and P&G to cluster plants that ensure steady contract loads for adjacent converters. Kano, Nigeria’s northern commercial hub with a population of 15 million, supplies the flour, dairy, and pharmaceutical industries across Kaduna, Katsina, and Sokoto, anchoring a second flexible-packaging cluster. Port Harcourt in Rivers State meets the film demand for industrial chemicals serving the oil and gas sector, thereby reinforcing regional diversity.

Emergent urban nodes around Abuja, Nasarawa, and Niger are growing on the back of 3.8% annual urban population gains, which concentrate disposable income. Converters deploying satellite warehouses near these hubs cut lead times and win market share from Lagos-centric rivals. Poor road infrastructure and security risks on northern highways inflate insurance premiums and transit budgets, pressuring operating margins.

Nevertheless, ECOWAS protocols allow Nigerian converters to ship films to Ghana, Benin, and Togo under reduced tariffs, with cross-border volume up 12% in 2025. Dangote’s resin availability curtails imports, freeing port capacity and enabling quicker turnaround for finished goods exports, a boon for Nigeria flexible packaging market competitiveness across West Africa.

Competitive Landscape

The Nigeria flexible packaging market is highly fragmented, with more than 20 converters each holding less than an 8% share, ensuring fierce price competition and abundant innovation. PrimePak Industries, Quantum Plastic Nigeria, and Flexipack Plastics benefit from Lagos' proximity and agile scheduling that accommodate rapid SKU changes. Multinational captive lines within Coca-Cola, Unilever, and Nestlé plants secure high-volume SKUs, but outsource specialty runs to independent converters equipped with digital presses and holographic capabilities. Annual cost-reduction negotiations of 3%-5% against naira depreciation sharpen operational discipline and speed capital-equipment upgrades.

Energy accounts for up to 25% of total production cost because the grid supply averaged 4,500 MW against 30,000 MW of latent demand in 2025. Converters investing in solar-diesel hybrid systems report 12-15% savings, which helps cushion margin volatility. Dangote Pack’s vertical integration, from polypropylene monomer to printed laminates, exemplifies a model that neutralizes resin price shocks and secures a steady feedstock. The Standards Organisation of Nigeria conducted 800 factory audits in 2025, suspending 15 licenses for hygiene and traceability lapses, signaling a tightening of regulatory standards that favors certified players.

Counterfeit packs account for 12% of sachet water and pharma wrapping, prompting branded manufacturers to demand serialization and tamper features that smaller shops cannot afford, driving gradual consolidation. White-space prospects appear in bioplastics extrusion, pharmaceutical ISO 15378 compliant lines, and e-commerce fulfillment pouches that require on-pack digital triggers. As competition intensifies, market leaders deploy Industry 4.0 analytics for predictive maintenance, reducing unscheduled downtime by 18% and safeguarding contract SLAs. These performance gaps shape the Nigeria flexible packaging market where technological agility and quality certifications delineate competitive advantage.

Nigeria Flexible Packaging Industry Leaders

Victor Oscar Company

Flexipack Plastics Ltd

PrimePak Industries Nigeria Ltd

Quantum Plastic Nigeria Ltd

Tempo Paper Pulp & Packaging Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Dangote Petrochemical commenced polypropylene production at Lekki, supplying 75,000 metric tons per month to local converters.

- November 2025: Unilever Nigeria installed a USD 25 million rotogravure line in Agbara, adding capacity for 500 million sachets per year.

- September 2025: Nestlé Nigeria opened a USD 30 million noodle plant in Ogun State, partnering with PrimePak Industries for oxygen-barrier pouches.

- August 2025: Standards Organisation of Nigeria mandated 90% degradation within 180 days for certified biodegradable films.

Nigeria Flexible Packaging Market Report Scope

Flexible packaging encompasses materials or packages that readily adapt their shape upon being filled or sealed. Typically crafted from non-rigid materials such as plastics, films, foils, or paper, these packaging products include bags, pouches, liners, wraps, and sachets. The study on the Nigerian flexible packaging market tracks the demand for material types such as plastic, paper, and metal. It also examines the market size in terms of revenue for the respective end-user industry verticals in the country, covering the listed product types.

The Nigeria Flexible Packaging Market Report is Segmented by Material (Plastics, Paper, Metal Foil, and Bioplastics and Compostable Materials), Product Type (Bags and Pouches, Films and Wraps, Sachets and Stick Packs, and Other Product Types), End-user Industry (Food, Beverage, Healthcare and Pharmaceutical, Personal Care and Cosmetics, Agriculture and Horticulture, and Other End-User Industries), Printing Technology (Flexography, Rotogravure, Digital Printing, and Other Printing Technologies). The Market Forecasts are Provided in Terms of Value (USD).

By Material

| Plastics | Polyethylene (PE) |

| Biaxially Oriented Polypropylene (BOPP) | |

| Cast Polypropylene (CPP) | |

| Other Plastics | |

| Paper | |

| Metal Foil | |

| Bioplastics and Compostable Materials |

By Product Type

| Bags and Pouches |

| Films and Wraps |

| Sachets and Stick Packs |

| Other Product Types |

By End-user Industry

| Food | Baked Goods |

| Snacks | |

| Meat, Poultry and Seafood | |

| Confectionery | |

| Pet Food | |

| Other Food Products | |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Agriculture and Horticulture | |

| Other End-User Industries |

By Printing Technology

| Flexography |

| Rotogravure |

| Digital Printing |

| Other Printing Technologies |

| By Material | Plastics | Polyethylene (PE) |

| Biaxially Oriented Polypropylene (BOPP) | ||

| Cast Polypropylene (CPP) | ||

| Other Plastics | ||

| Paper | ||

| Metal Foil | ||

| Bioplastics and Compostable Materials | ||

| By Product Type | Bags and Pouches | |

| Films and Wraps | ||

| Sachets and Stick Packs | ||

| Other Product Types | ||

| By End-user Industry | Food | Baked Goods |

| Snacks | ||

| Meat, Poultry and Seafood | ||

| Confectionery | ||

| Pet Food | ||

| Other Food Products | ||

| Beverage | ||

| Healthcare and Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Agriculture and Horticulture | ||

| Other End-User Industries | ||

| By Printing Technology | Flexography | |

| Rotogravure | ||

| Digital Printing | ||

| Other Printing Technologies | ||

Key Questions Answered in the Report

What is the current value of the Nigeria flexible packaging market?

The market was valued at USD 3.31 billion in 2026 and is projected to hit USD 4.46 billion by 2031.

Which segment shows the fastest growth within Nigeria’s flexible packaging landscape?

Sachets and stick packs are expected to grow at a 7.32% CAGR through 2031 due to micro-distribution demand.

How are tax incentives influencing local converting capacity?

Five-year pioneer status for converters sourcing 60% domestic resin cuts corporate taxes and import duties, encouraging new lines and lowering film costs by about 12%.

What role does e-commerce play in flexible packaging demand?

Online retail penetration of 15% demands tamper-evident, lightweight packs that withstand multi-stage logistics, boosting flexible film uptake.

How are single-use plastic bans affecting material choices?

Lagos and draft federal rules push converters toward certified compostable films, accelerating 7.52% CAGR growth in bioplastics through 2031.

Why is digital printing gaining share?

Artisanal brands and e-commerce sellers need short-run, variable-data packs; digital presses deliver same-day proofs and avoid plate costs, fueling an 8.43% CAGR.

Page last updated on: