Green Hydrogen Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

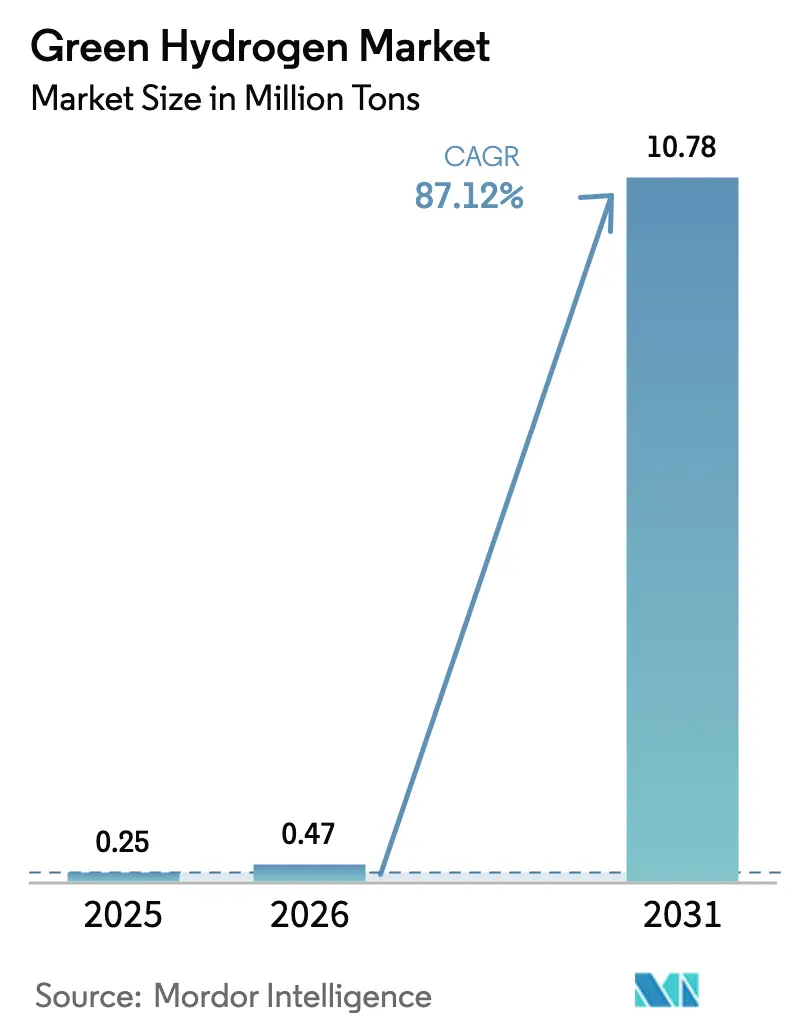

| Market Volume (2026) | 0.47 Million tons |

| Market Volume (2031) | 10.78 Million tons |

| Growth Rate (2026 - 2031) | 87.12% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Green Hydrogen Market Analysis by Mordor Intelligence

The Green Hydrogen Market size is projected to expand from 0.25 million tons in 2025 and 0.47 million tons in 2026 to 10.78 million tons by 2031, registering a CAGR of 87.12% between 2026 to 2031. This outlook translates into a sizable jump in market size and confirms that large‐scale industrial decarbonization is replacing gray hydrogen rather than supplementing it. Persistent drops in renewable power costs, supportive government incentives, and early-stage infrastructure build-outs are the primary catalysts. Capacity additions concentrate in regions with high solar irradiance or strong wind resources, while emerging carbon border fees in Europe and more stringent fuel rules in shipping extend demand to new use cases. Cost curves for electrolyzers keep bending downward as gigafactories ramp up, and merchant PPAs for curtailed electricity now let many projects lock in near-zero input prices. Competitive intensity is moderate because five manufacturers still handle most orders, yet Chinese suppliers are cutting into margins with lower-priced alkaline units and may reset price expectations once export volumes rise.

Key Report Takeaways

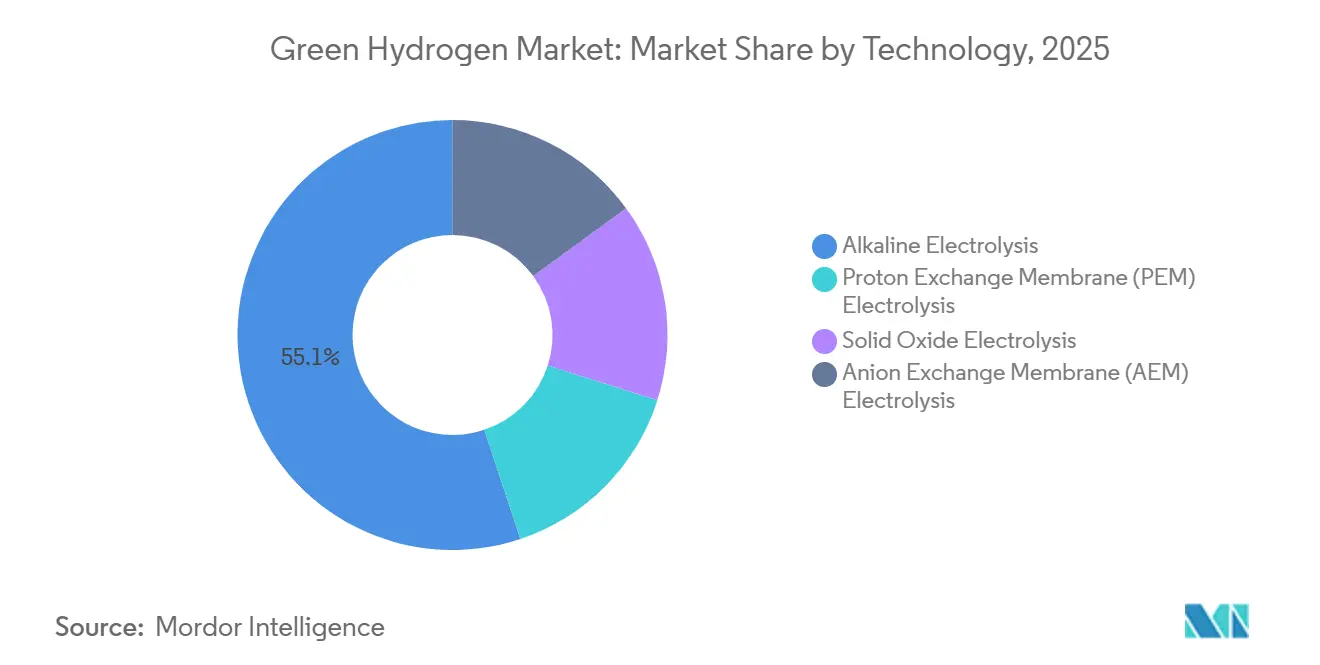

- By technology, alkaline electrolysis captured 55.13% of the 2025 volume, while PEM is forecast to post a 92.35% CAGR through 2031.

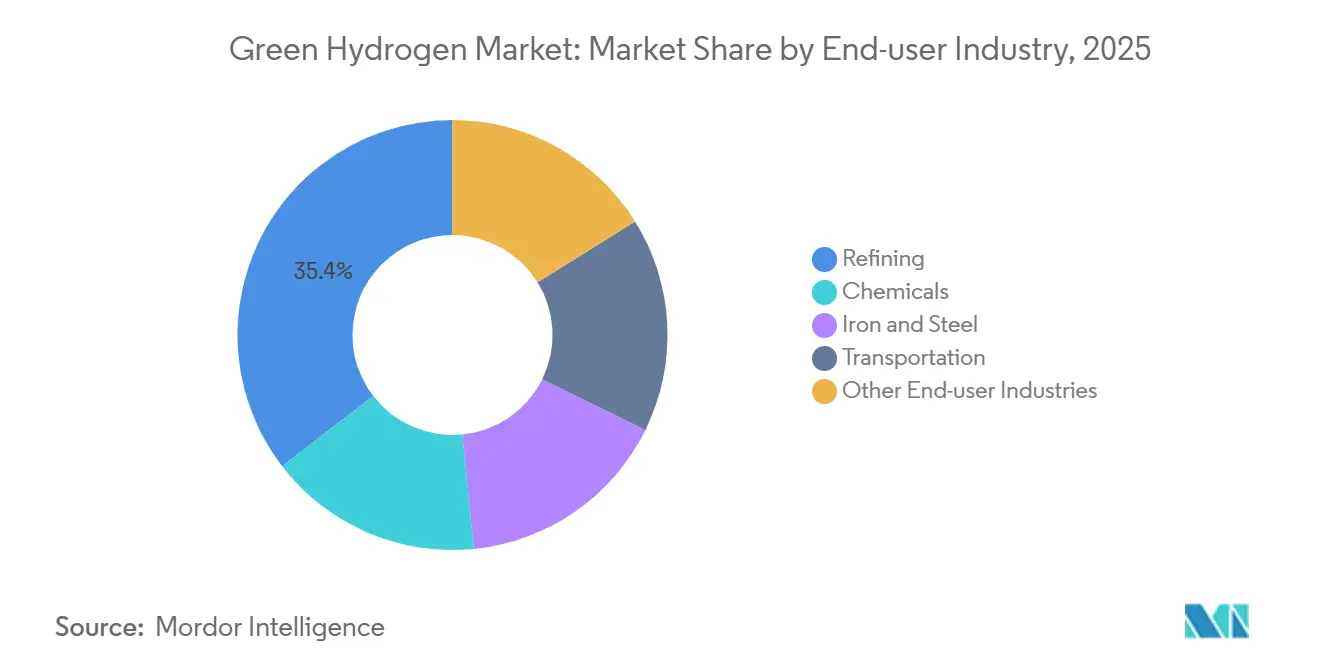

- By end-user industry, refining held 35.45% of the green hydrogen market share in 2025, but chemicals are projected to expand at a 97.22% CAGR to 2031.

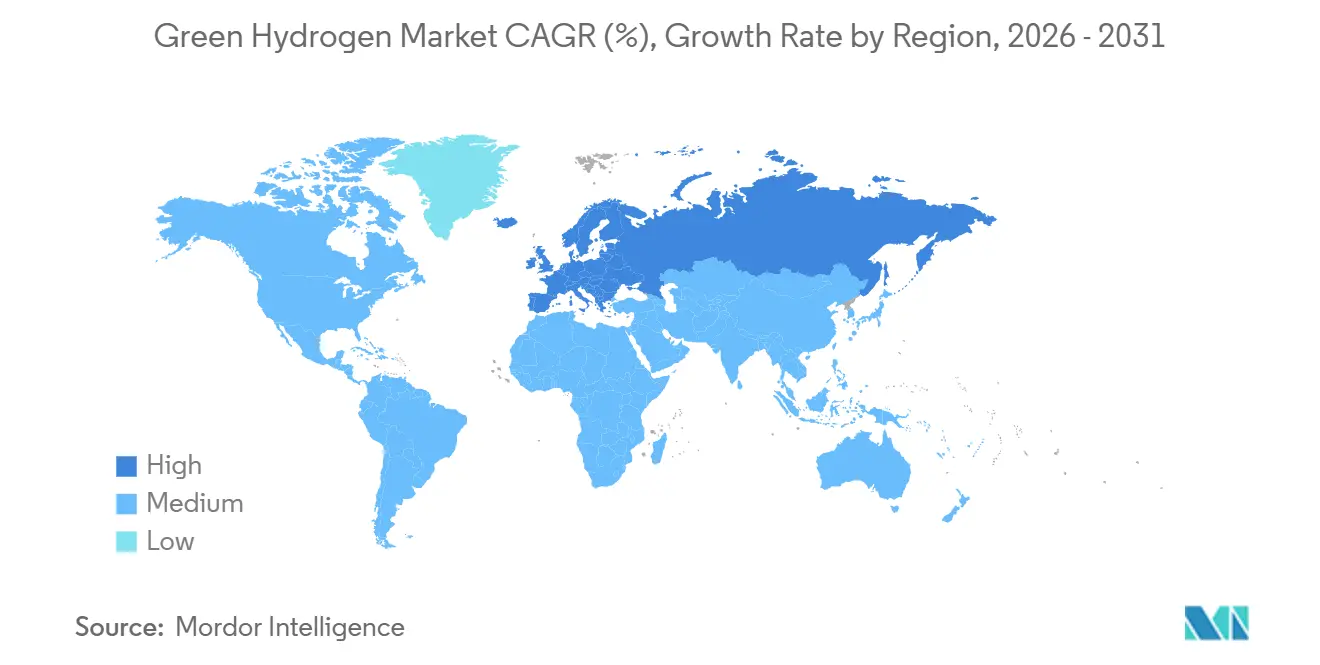

- By geography, Asia-Pacific accounted for 48.23% of the 2025 volume, yet Europe is expected to advance at a 94.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Green Hydrogen Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining LCOE of renewables in high-irradiance regions | +18.5% | Middle East, North Africa, Australia, Chile | Medium term (2-4 years) |

| EU industrial decarbonization mandates (steel, fertilizer) | +17.2% | Europe, spillover to Turkey and North Africa | Short term (≤ 2 years) |

| Maritime fuel rules spurring green-ammonia bunkering demand | +16.1% | Global, early adoption in Europe and Singapore | Medium term (2-4 years) |

| Electrolyzer-gigafactory economies of scale | +15.8% | Global, concentrated in China, Germany, India, United States | Short term (≤ 2 years) |

| Surplus curtailed wind/solar PPAs enabling negative-price H₂ | +14.3% | North America, Europe, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining LCOE of Renewables in High-Irradiance Regions

In 2025, solar and onshore wind projects in Saudi Arabia, Chile, and Australia achieved low generation costs. This pricing enables electrolytic hydrogen to compete with steam methane reforming, provided natural gas prices remain favorable. The NEOM complex enjoys a competitive blended LCOE, allowing it to operate without subsidies. Meanwhile, Chile’s Magallanes wind cluster aims to export green ammonia by 2030. By co-locating electrolyzers with resource sites, projects can significantly reduce transmission costs. A case in point is Fortescue’s system in Pilbara, which showcases how iron-ore producers are integrating hydrogen into their operations [1]Fortescue Metals Group, “FFI Commissions 50 MW Electrolyzer in Pilbara,” fmgl.com.au . Collectively, these initiatives have narrowed the green premium over time.

EU Industrial Decarbonization Mandates (Steel, Fertilizer)

Under the 2026-2030 ETS, a carbon price floor renders blast-furnace steel unviable unless carbon capture or hydrogen-based DRI is employed. This is underscored by ArcelorMittal’s trials in Hamburg, where a shift to hydrogen achieved a significant reduction in Scope 1 emissions. Germany allocated funds to help fertilizer producers mitigate the green premium, facilitating the offtake of green ammonia. The Carbon Border Adjustment Mechanism amplifies these challenges beyond the EU, leading Turkish and Ukrainian mills to either explore electrolytic methods or brace for tariffs on their product's value.

Maritime Fuel Rules Spurring Green-Ammonia Bunkering Demand

By 2030, the IMO mandates a reduction in well-to-wake emissions, positioning ammonia as a prime alternative fuel. In a strategic move, Maersk placed orders for vessels primed for ammonia use, but with a caveat: the establishment of bunkering hubs in Rotterdam, Singapore, and Los Angeles. Demonstrating the fuel's potential, MAN Energy unveiled a prototype ammonia engine boasting high thermal efficiency. Further solidifying ammonia's foothold, Rotterdam inaugurated a substantial storage terminal in November 2025. While ammonia storage demands more space than diesel, shipowners find value in sidestepping sulfur scrubbers and intricate carbon capture systems, streamlining compliance for their long-haul fleets.

Electrolyzer-Gigafactory Economies of Scale

At thyssenkrupp Nucera’s Delfzijl plant, alkaline stack costs have been reduced, while at Reliance Industries’ Jamnagar factory, PEM stack costs have also decreased. In China, Ningxia Baofeng has achieved a milestone, producing alkaline units at a competitive rate. Thanks to automated assembly and standardized balance-of-plant packages, engineering expenses have been reduced. This efficiency allows the green hydrogen market to profitably support projects operating at low utilization levels.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Iridium and platinum supply bottlenecks for PEM stacks | -3.2% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Limited grid-hosting capacity for greater than 100 MW electrolysis clusters | -2.4% | Asia Pacific, North America, emerging markets | Medium term (2-4 years) |

| High cost of cryogenic LH₂ shipping over 7,000 km routes | -1.8% | Intercontinental trade routes (Middle East to Asia, Australia to Europe) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Iridium and Platinum Supply Bottlenecks for PEM Stacks

Global iridium output was significant in 2025, yet PEM demand may increase substantially in 2028 if loading rates stay constant. Spot iridium prices rose sharply in December 2025, adding to PEM costs. Recycling provides only a limited amount annually, and mixed-oxide substitutes lag in durability[2]NREL, “PEM Catalyst Research,” nrel.gov. Suppliers aim to cut loadings by 2027, but supply concentration in South Africa and labor strikes heighten price volatility.

Limited Grid-Hosting Capacity for Large Electrolyzers

Clusters require reactive-power compensation and frequently require the construction of new high-voltage lines. Reliance Industries undertook the construction of a dedicated 400 kV substation and a 60 MVAR static-VAR unit in Jamnagar, resulting in a project delay. California’s Path 15 corridor faces a limitation, unable to accommodate additional electrolysis load without transmission enhancements, consequently deferring certain projects. Germany and Australia encountered analogous challenges, leading to moratoria or the implementation of distributed siting regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PEM Gains Despite Alkaline Dominance

Alkaline systems controlled 55.13% of 2025 volume, thanks to capital costs and lifetimes aligning perfectly with the demands of refiners and chemical plants operating at near-maximum efficiency. Meanwhile, PEM systems are set to climb at a 92.35% CAGR, bolstered by their rapid ramp rates, making them ideal for harnessing intermittent power. As strategies for renewable integration mature, the market size for PEM projects in the green hydrogen sector is set for a pronounced uptick. On the other hand, high-temperature SOEC pilots, boasting impressive electrical efficiency, face a hurdle: their stack life, falling short of 20,000 hours, curtails immediate adoption. AEM units, while successfully sidestepping the use of platinum group metals, grapple with a challenge of membrane durability, also under the 20,000-hour mark, before they can hit the commercial stage.

Recent orders highlight this industry shift. In 2025, refiners in the Asia-Pacific region secured a significant amount of alkaline equipment, prioritizing lower capital expenditures. Conversely, Europe, leaning towards PEM, captured a dominant share of those orders, justifying the premium with potential grid-service revenue. Solid oxide systems, though holding a smaller share of the 2025 volume, are on track for robust growth, driven by iron and steel plants merging electrolysis with their waste heat streams. This trend underscores a pivotal shift: the choice of technology is increasingly dictated by plant-specific economics rather than a blanket preference for one technology over another.

By End-User Industry: Chemicals Overtake Refining Growth

Refining commanded 35.45% of 2025 demand, a testament to the entrenched hydrogen networks in hydrocracking and desulfurization units. Chemicals will be the fastest-growing segment at a 97.22% CAGR. This surge is largely fueled by fertilizer and methanol producers striving to align with increasingly stringent life-cycle carbon thresholds. Yara's electrolyzer is making waves, displacing natural-gas feedstock annually. Meanwhile, BASF has ambitious plans, eyeing PEM capacity that promises an annual yield of green methanol. Although transportation currently accounts for a modest share of the 2025 volume, the landscape could shift as heavy-duty fuel cell trucks edge closer to diesel's cost competitiveness. Notably, the green hydrogen market for the chemicals segment is on track to outpace refining within the forecast period.

Iron and steel are set for significant expansion, driven by the viability of DRI retrofits in the wake of rising carbon pricing. While major plants grapple with substantial capex, the direct-reduction technology offers a silver lining, slashing output CO₂ emissions. This reduction is especially crucial for European mills contending with CBAM levies. The remaining sectors, including glass, power generation, and smaller industrials, collectively account for a smaller share of the 2025 demand.

Geography Analysis

Asia-Pacific’s 48.23% share in 2025, driven by the rapid expansion of electrolyzer capacity in China and India, even as coal-dominated grids pose challenges to carbon intensity improvements. China Three Gorges operates a large electrolyzer, harnessing cost-effective off-peak wind power. With limited domestic renewable resources, Japan emerges as the top prospective importer, securing long-term agreements. South Korea, bolstered by substantial subsidies, is retrofitting the Ulsan and Incheon clusters, targeting a complete transition to green supply by 2029. Meanwhile, India’s National Mission has rallied commitments, but to address reactive power and harmonic constraints in Rajasthan, an investment is needed for grid enhancements.

Europe records the highest growth rate at a projected 94.19% CAGR. The CBAM policy compels upstream suppliers to pivot to green hydrogen or incur tariffs. Concurrently, Germany is channeling significant funding into a pipeline initiative, connecting offshore wind resources to plants in the Ruhr Valley. Highlighting the region's potential, Iberdrola's ambitious project in Castilla-La Mancha demonstrates that competitively priced solar energy can yield hydrogen at a low cost. The UK is making strides too, with a long-term guarantee of a strike price, facilitating the development of new capacity. Not to be outdone, France's TotalEnergies has augmented its La Mède facility, aiming for a substantial reduction in renewable diesel emissions.

North America, buoyed by the U.S. 45V tax credit, is witnessing robust growth. Air Products is making a significant move with a large complex in Louisiana, integrating electrolysis with renewable energy, targeting substantial annual output for export. In Quebec, Canada, a plant is capitalizing on hydro energy, translating to a low production cost. Mexico is also in the fray, with Tula refinery's retrofit set to substitute gray hydrogen, leading to significant annual CO₂ savings.

By 2030, the Middle East and Africa, spearheaded by NEOM and Masdar, are poised to export a large volume of green ammonia. Meanwhile, South America's Chilean wind corridor is attracting substantial investment for projects aimed at exports.

Competitive Landscape

The green hydrogen market is moderately consolidated. Chinese firms priced alkaline stacks competitively, capturing a significant share of bookings in the Asia-Pacific region and exerting pressure on Western margins. Patent activity centers on iridium-free PEM catalysts and low-resistance plate coatings; thyssenkrupp nucera secured patents for titanium-nitride layers, achieving a notable reduction in contact resistance. Growth opportunities lie in distributed off-grid packages, SOEC systems for process-heat integration, and electrolyzer-as-a-service contracts.

Green Hydrogen Industry Leaders

Air Liquide

Linde PLC

China Petroleum & Chemical Corporation (Sinopec)

Plug Power Inc.

Nel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ABB and Charbone Hydrogen agreed to develop up to 15 modular production facilities across North America, with the first unit in Québec slated for mid-2025 grid connection.

- February 2025: Air Liquide launched two electrolyzer projects in Rotterdam and Zeeland, totalling 450 MW and EUR 1 billion (~USD 1.14 billion) in investment, aiming to avoid 500,000 tonnes of CO₂-equivalent emissions annually.

- January 2025: Lhyfe signed an MoU with Masdar targeting 1 million tons of annual green hydrogen output by 2030 through a 100 GW renewable portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the green hydrogen market as all hydrogen generated through water electrolysis powered solely by renewable electricity, then delivered for industrial feedstock, mobility, power generation, or long-duration energy storage. Capacity is included once commercial offtake begins.

Scope Exclusions: Hydrogen derived from fossil fuels or from grid electricity that breaches accepted carbon-intensity thresholds is not part of this assessment.

Segmentation Overview

- By Technology

- Alkaline Electrolysis

- Proton Exchange Membrane (PEM) Electrolysis

- Solid Oxide Electrolysis

- Anion Exchange Membrane (AEM) Electrolysis

- By End-user Industry

- Refining

- Chemicals

- Iron and Steel

- Transportation

- Other End-user Industries (Power Generation, Glass, Semiconductors)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Desk Research

Open-source evidence anchors our work: IEA renewable statistics, Eurostat HS 2804 trade data, US DOE H2Hub filings, and Hydrogen Council dashboards show real volumes and projects. Company 10-Ks, project press releases, and news archived in Dow Jones Factiva and D&B Hoovers flesh out costs, start-up dates, and supply deals. These references are illustrative; many other public and paid sources guided data checks.

Primary Research

Mordor analysts spoke with electrolyzer manufacturers, renewable IPPs, industrial gas offtakers, and policy officers across Asia-Pacific, Europe, North America, and the Middle East. The conversations validated utilization rates, average selling prices, subsidy timing, and project commissioning schedules that desk work could not fully capture.

Market-Sizing & Forecasting

We begin with a top-down reconstruction. Renewable electricity earmarked for dedicated electrolysis is multiplied by typical capacity factors and conversion efficiencies to yield hydrogen output by country. Bottom-up roll-ups of announced plants (nameplate × realistic ramp-up) and sampled ASP benchmarks adjust totals where gaps appear. Key inputs include renewable PPA prices, electrolyzer capex per kW, policy incentive dollars per kg, industrial substitution targets, and learning-rate effects. A multivariate regression, stress-tested through scenario analysis, produces the five-year outlook.

Data Validation & Update Cycle

Analysts compare model outputs with trade flows, spot price series, and publicly announced offtake contracts. Anomalies trigger peer review before sign-off. Reports refresh annually, with interim updates issued after material market events.

Why Our Green Hydrogen Baseline Commands Reliability

Published estimates often vary because firms mix value and volume, count pipeline capacity differently, or refresh at unequal intervals.

Key gap drivers include scope breadth, whether equipment spend is booked as 'market value,' and how under-construction plants are treated.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 0.45 million tons (2025) | Mordor Intelligence | |

| USD 1.1 billion (2023) | Global Consultancy A | Blends blue projects and values revenue, not physical output |

| USD 11.86 billion (2025) | Global Consultancy B | Counts under-construction capacity and electrolyzer sales as market |

| USD 1.19 billion (2024) | Industry Journal C | Focuses on transport demand only and excludes Asian supply |

The comparison shows that Mordor's disciplined scope, transparent variables, and yearly refresh provide decision-makers with a balanced, repeatable baseline they can trust.

Key Questions Answered in the Report

What volume does the green hydrogen market reach by 2031?

The market is forecast to hit 10.78 million tons by 2031, up from 0.47 million tons in 2026, registering a CAGR of 87.12%.

Which technology grows fastest through 2031?

PEM electrolysis posts the highest forecast growth at a 92.35% CAGR because its fast ramp rates blend well with variable renewable generation.

Why is Europe showing the highest growth rate?

Binding carbon-border fees, an updated ETS, and well-funded infrastructure programs are driving a projected 94.19% CAGR for European demand.

Which end-use segment will overtake refining?

The chemicals segment is projected to expand at a 97.22% CAGR and surpass refining demand before 2031, mainly through ammonia and methanol synthesis.

Page last updated on: