Fuel Cell Electric Bus Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

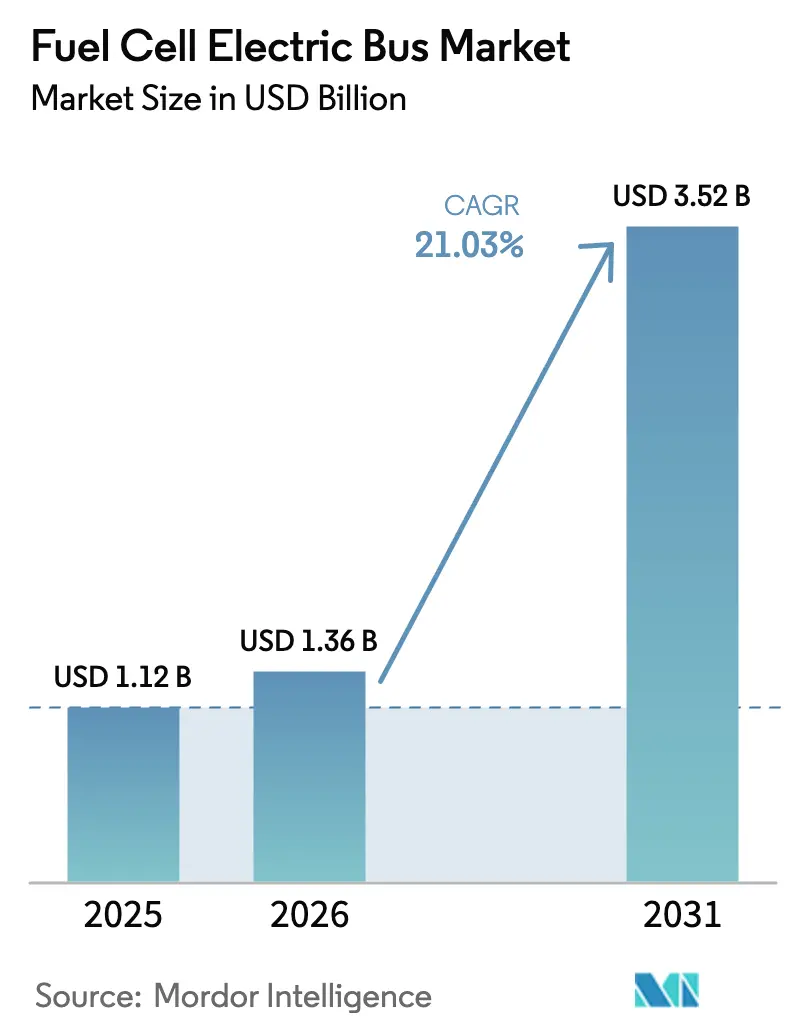

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 3.52 Billion |

| Growth Rate (2026 - 2031) | 21.03% CAGR |

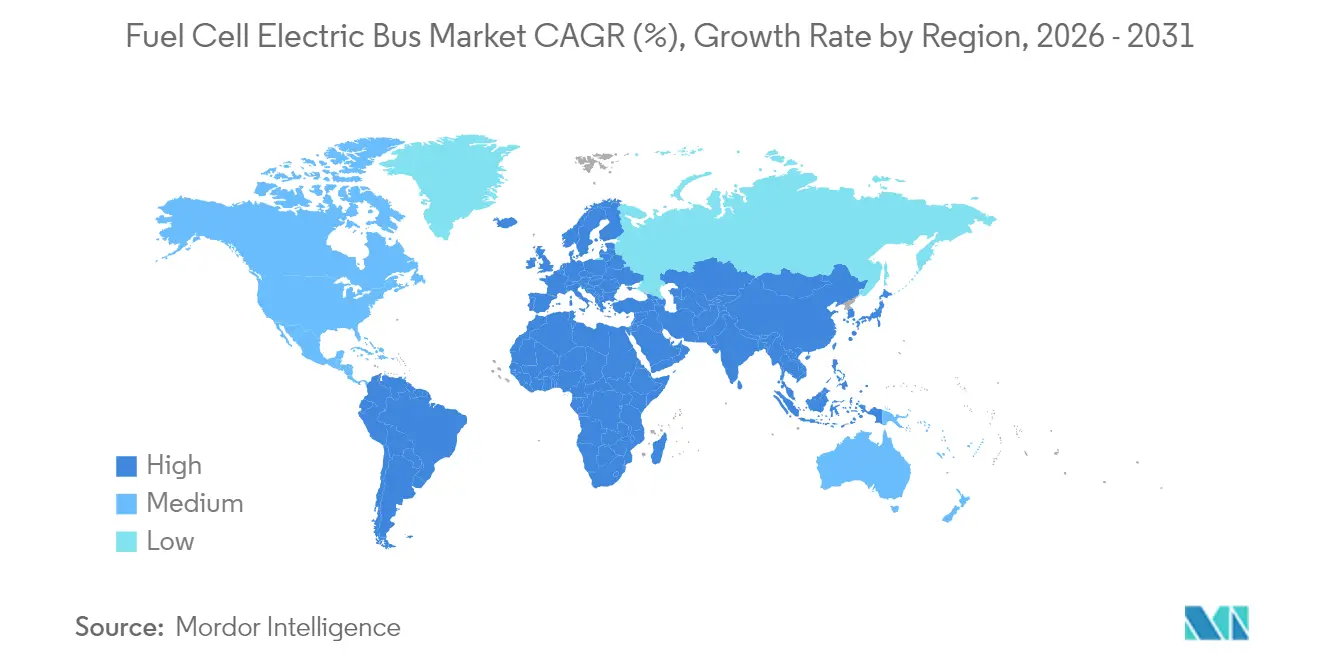

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fuel Cell Electric Bus Market Analysis by Mordor Intelligence

The fuel cell electric bus market size was valued at USD 1.12 billion in 2025 and estimated to grow from USD 1.36 billion in 2026 to reach USD 3.52 billion by 2031, at a CAGR of 21.03% during the forecast period (2026-2031). Policy mandates, falling green-hydrogen costs, and purpose-built bus platforms are converging to create dependable multi-year order books for OEMs. Transit agencies value the long-range, rapid refueling, and cold-weather resilience of hydrogen buses, especially on duty cycles where battery-electric alternatives would require mid-shift charging.

Asia-Pacific leads current volumes on the back of China’s build-out of 1,200 hydrogen stations by 2025, while federal grant programs are accelerating early deployments in North America. At the same time, the Middle East is emerging as the fastest-growing region, supported by national diversification agendas that frame hydrogen mobility as a strategic industry. Competitive intensity is rising as fuel-cell specialists, vertically integrated vehicle makers, and retrofit kit suppliers vie for municipal tenders, each betting on scale to compress unit costs.

Key Report Takeaways

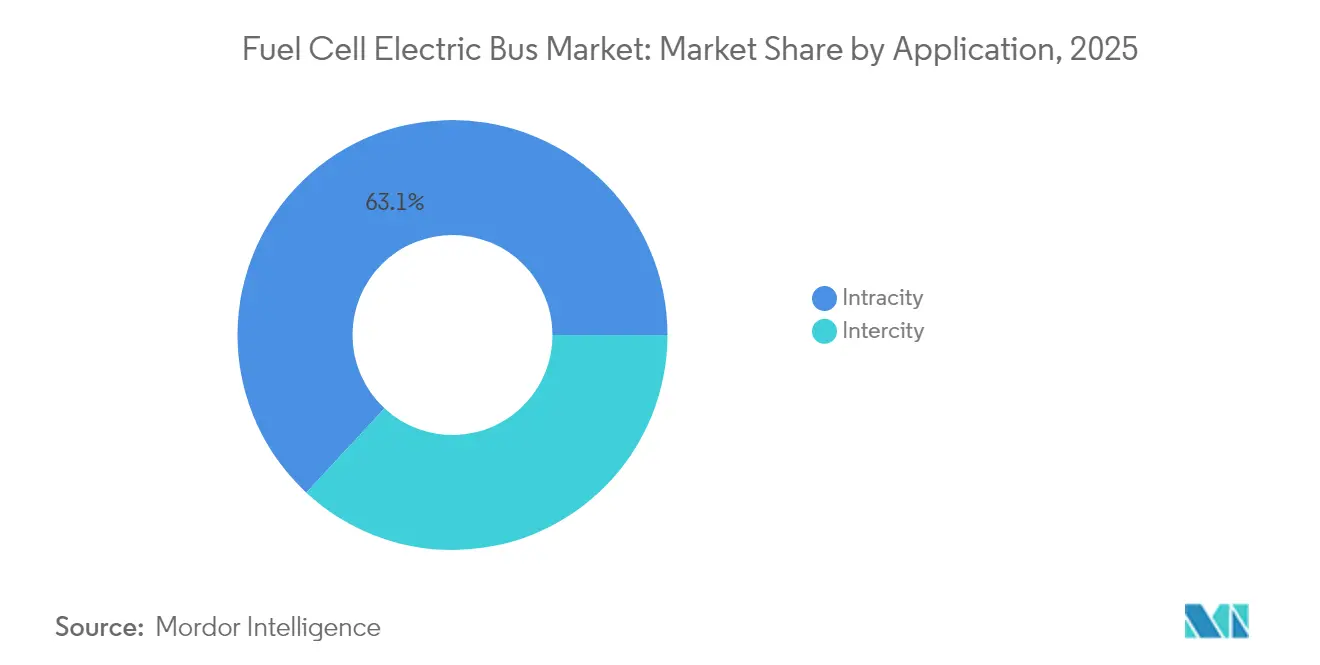

- By application, intracity buses held the largest share at 63.10% in 2025, whereas intercity buses are the fastest-growing segment with a CAGR of 24.74% from 2026 to 2031.

- By bus type, new hydrogen buses dominated with a 71.10% share in 2025, while retrofitted hydrogen buses are expected to grow the fastest at a CAGR of 31.97% during 2026-2031.

- By fuel-cell type, PEMFC led the market with an 83.95% share in 2025, whereas SOFC is the fastest-growing type with a CAGR of 28.95% from 2026 to 2031.

- By power rating, the 150–250 kW category accounted for the largest share at 47.10% in 2025, while the above 250 kW segment is growing fastest at a 28.92% CAGR.

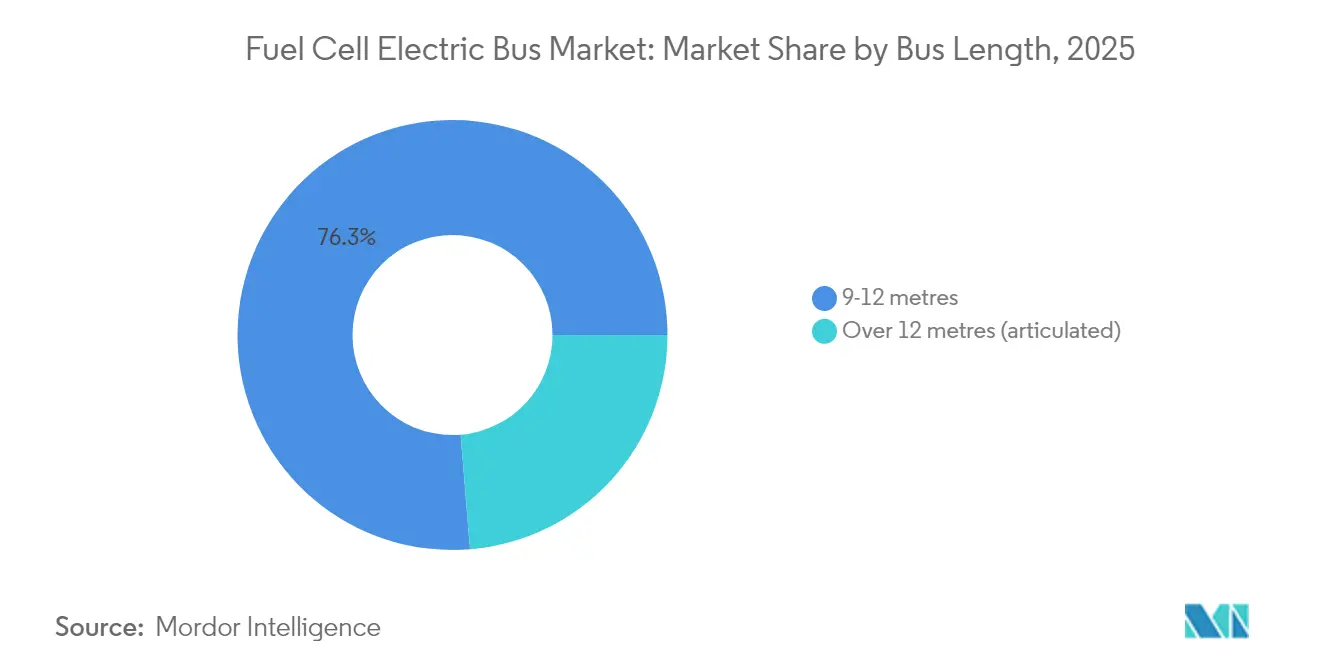

- By bus length, buses sized 9–12 metres had the largest share at 76.30% in 2025, whereas over 12 metres is the fastest-growing length segment with a CAGR of 27.93%.

- By driving range, the 300–500 km range dominated with a 56.15% share in 2025, while buses with above 500 km range are growing fastest at a CAGR of 30.86%.

- By geography, Asia-Pacific led the market with a 43.26% share in 2025, whereas the Middle East and Africa is the fastest-growing region with a CAGR of 30.64% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fuel Cell Electric Bus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zero-Emission Mandates for Transit Fleets | +4.2% | Global, with strongest impact in North America & EU | Medium term (2-4 years) |

| Green Hydrogen Price Drop Post-2025 | +3.8% | Global, with early gains in Asia-Pacific & Europe | Long term (≥ 4 years) |

| Government Bulk Procurement Support | +3.5% | Asia-Pacific core, expanding to North America & EU | Short term (≤ 2 years) |

| Liquid Hydrogen Corridor Expansion | +2.9% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| OEM Platform Standardisation Reduces TCO | +2.1% | Global | Short term (≤ 2 years) |

| FCEBs Chosen for Autonomous Shuttle Pilots | +1.2% | North America & EU, pilot programs in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Zero-Emission Mandates for Public Transit Fleets

Many transit agencies now face statutory deadlines to eliminate diesel, prompting multi-year framework agreements for hydrogen buses. California requires full zero-emission fleets by 2040, triggering near-term orders under its Innovative Clean Transit rule. European Union’s Clean Vehicles Directive pushed zero-emission buses to 49% of new deliveries in 2024, with fuel-cell models already taking 3% of the total. Emerging markets follow a similar path—Abu Dhabi targets a 20% green fleet share by 2030, providing clear procurement visibility for OEMs. Binding mandates, therefore, underpin the long-term demand curve of the fuel cell electric bus market.

Sharp Decline in Green Hydrogen Prices Post-2025

Electrolyzer scale-up and cheaper renewables are expected to cut average production costs to EUR 2.7 per kg by 2050, with Asia projected to hit EUR 1.8 per kg, altering the operating-cost parity versus diesel. China’s hydrogen sector nearly doubled revenue to CNY 3.93 billion in 2023, demonstrating the deflationary trajectory of equipment and supply chains. Newly funded hubs such as the Pacific Northwest Hydrogen Hub in the United States add regional cost advantages that lower fuel bills for transit fleets.

Government-Backed Bulk Procurement Programmes

Large, centrally funded orders compress up-front prices by offering manufacturers predictable volumes. Hyundai’s deal to supply 1,000 hydrogen buses to Seoul by 2027 typifies how city-level commitments de-risk capacity investments for OEMs. China couples similar purchase guarantees with toll waivers and accelerated station rollouts, accelerating the fuel cell electric bus market adoption curve.

Rapid Expansion of Liquid-Hydrogen Refuelling Corridors

Investors are moving beyond single stations toward high-throughput corridors that support intercity operations. Canada’s Infrastructure Bank committed USD 337 million to Western corridors, while Germany’s North Rhine-Westphalia region plans hubs to serve 3,800 buses by 2030. The US intends nationwide coverage from 2027, enabling long-haul routes to switch away from diesel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition From Fast-Charging BE Buses | -4.1% | Urban markets globally, strongest in Europe & North America | Short term (≤ 2 years) |

| Grey Hydrogen Remains Cheaper | -3.2% | Global, particularly in regions without renewable energy subsidies | Short term (≤ 2 years) |

| Shortage of Trained Maintenance Staff | -2.8% | Global, most acute in emerging markets | Medium term (2-4 years) |

| High Cost of Cryogenic Storage Systems | -2.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition From Fast-Charging Battery-Electric Buses

Battery-electric buses outsold diesel in EU city segments for the first time in 2024, buoyed by falling battery costs and abundant depot chargers. The International Energy Agency counted over 70,000 new e-buses worldwide in 2024, a 30% jump from the year[1]“Trends in Heavy-Duty Electric Vehicles – Global EV Outlook 2025,” International Energy Agency, iea.org. On routes below 200 km daily, TCO modelling still favors batteries, forcing hydrogen proponents to emphasise longer-range and high-utilisation niches.

Grey-Hydrogen Supply Still Cheaper Than Green

Absent carbon pricing, grey hydrogen from natural-gas reforming remains meaningfully cheaper, constraining fleet operators in price-sensitive jurisdictions. Until renewable-powered electrolysis achieves parity, agencies rely on subsidies or contractual green-fuel guarantees to meet sustainability pledges. Cost disparities are widest in markets lacking large-scale offshore wind or solar resources, limiting near-term uptake and tempering the growth rate of the fuel cell electric bus market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Intracity Dominance Drives Current Volumes

Intracity services generated 63.10% of 2025 revenue, equal to USD 0.71 billion of fuel cell electric bus market size, because city routes favour centralized refueling and predictable duty cycles. Intercity lines, while nascent, promise the steepest 24.74% CAGR as operators exploit hydrogen’s 300-500 km sweet spot to avoid en-route charging. The fuel cell electric bus market benefits when depot footprints are tight and grid upgrades for megawatt-scale chargers prove costly. Demonstrations such as Chile’s 600 km-range fleet underscore hydrogen’s suitability for long-haul corridors.

Urban agencies also appreciate 10-minute refueling that keeps schedule recovery buffers thin. Intercity networks look to hydrogen to power overnight express links where battery packs would erode passenger capacity. Autonomous shuttle pilots increasingly specify fuel cells to support 20-hour daily duty without downtime, sharpening the performance edge for the fuel cell electric bus market.

By Bus Type: New Deployments Lead Market Transformation

New bus models represented 71.10% of 2025 deliveries, reflecting OEM focus on optimized chassis that integrate tanks within the roofline and free floor space. Retrofits, although smaller, are sprinting at a 31.97% CAGR as kit providers enable agencies to convert younger diesel stock instead of scrapping it early. Transit authorities with capped capital budgets view conversions as a bridge to 2030 emission targets, especially where policy offers purchase vouchers.

Still, builders like Solaris and Hyundai embed stacks, inverters, and cooling loops directly into new frames, delivering lower curb weight and simpler maintenance. As economies of scale sharpen, the fuel cell electric bus market is expected to pivot toward fresh builds because total lifecycle cost favors factory-integrated systems beyond year five of operation.

By Fuel-Cell Type: PEMFC Dominance Faces SOFC Challenge

PEMFC units held 83.95% revenue share in 2025, supplying most intracity fleets thanks to rapid start and low operating temperature. SOFC products, however, are logging a 28.95% CAGR, appealing to operators that need continuous power and the option to run on reformed gas during hydrogen outages. NA Clean Energy notes the higher efficiency of SOFC stacks, lowering hydrogen consumption per kilometre.

PEMFC costs have dropped as Ballard engines pass 35,000 service hours in field trials. Still, resilience to fuel purity swings and hotter climates positions SOFC as a credible second technology pillar, injecting fresh competition into the fuel cell electric bus market.

By Power Rating: Mid-Range Systems Dominate Current Deployments

Units rated 150-250 kW supplied 47.10% of buses in 2025, a band that balances acceleration with stack cost. Orders for 300 kW plus configurations are accelerating at 28.92% CAGR as agencies adopt articulated 18-metre vehicles such as Solaris Urbino 18 Hydrogen, Bus of the Year 2025. These higher outputs allow longer routes and hill climbs without sacrificing heating loads in winter.

Conversely, sub-150 kW systems power shuttles and paratransit services where lighter frameworks reduce operating expense. As refueling corridors mature, the demand mix will tilt toward high-power setups that extend range beyond 500 km and widen the addressable scope of the fuel cell electric bus market.

By Bus Length: Standard Configurations Lead Market Adoption

The 9-12 m bracket dominated with 76.30% of 2025 deployments as agencies standardize on one-route-fits-all vehicles that fit existing depot bays. Articulated formats above 12 m post a 27.93% CAGR outlook, lifted by BRT corridors that prize passenger throughput over maneuverability. Brighton & Hove’s 34 double-deck hydrogen units exhibit a local appetite for specialised configurations when municipal density demands high capacity.

Standard-length models will remain the bedrock of the fuel cell electric bus market because of their flexible duty conversions and easier maintenance access. That said, articulated growth signals a widening application envelope as the cost per seat falls with larger vehicles.

By Driving Range: Extended-Range Capabilities Drive Premium Segment Growth

Buses offering 300-500 km covered 56.15% of the 2025 turnover, providing enough autonomy for two intracity shifts without refueling. Units exceeding 500 km are forecast to grow 30.86% CAGR, carving out the premium long-distance niche. Agencies adopting country-wide intercity routes prefer these models to avoid building multiple truck-stop-style stations.

Short-range (Less than 300 km) buses suit feeder loops that return to the depot frequently, but large compressed-hydrogen tanks penalise curb weight. As liquid-storage technology advances, the extended-range segment will deepen its lead, solidifying hydrogen’s distinctive value proposition within the fuel cell electric bus market.

Geography Analysis

Asia-Pacific commanded 43.26% of global revenue in 2025, equal to USD 0.48 billion of fuel cell electric bus market size, owing to China’s infrastructure blitz and Korean bulk orders. The region’s 30.12% CAGR to 2031 rests on 1,200 new hydrogen stations, national toll exemptions, and integrated industrial strategies that align energy, vehicle, and component value chains. North America follows, expanding at a 27.26% CAGR on the strength of USD 623 million federal funding and state mandates that force fleet turnovers by 2035. Projects like the Pacific Northwest Hydrogen Hub bring USD 1 billion into the upstream supply, lowering delivered fuel prices for agencies along Interstate corridors. Canada’s Zero Emission Transit Fund also kick-starts municipal pilots, evidenced by Mississauga’s first hydrogen fleet. Europe shows a 23.42% CAGR outlook, powered by the Clean Vehicles Directive and local manufacturing dominance. Germany alone targets 3,800 fuel-cell buses by 2030 with heavy co-investment in stations. The Middle East & Africa represents the fastest-growing territory at 30.64% CAGR, even if it starts from a lower base, spurred by UAE and Saudi sustainability programs that reposition hydrocarbons majors into hydrogen mobility. Pilot deployments in Abu Dhabi and Riyadh validate climatic performance and seed local supply chains, broadening the geographic reach of the fuel cell electric bus market.

Competitive Landscape

Ballard Power Systems led 2024 shipments, leveraging its engine-only model to supply multiple OEMs under long-term frameworks that anchor revenue visibility. New Flyer followed, blending in-house bus engineering with external stacks, while Hyundai scaled vertically from cells to complete vehicles, underpinned by a forthcoming Ulsan fuel-cell plant. commands Europe via its Urbino family, and Yutong capitalizes on domestic incentives in China.

Strategic alliances dominate. Hexagon Purus struck a long-term tank agreement with GILLIG to harmonize US designs. Karsan teamed with Toyota to integrate Mirai stacks into midibus platforms, shortening validation cycles. Retrofit specialists also carve niches, offering conversion packages that undercut new-bus capex by 35%.

Technology roadmaps focus on higher stack durability, modular tank layouts, and digital twins that predict degradation, lowering lifetime cost. Safety recalls, such as Hyundai’s 2025 action covering 1,269 domestic units, underline maturing quality processes vital for trust in the fuel cell electric bus market. Over the mid-term, platform standardisation and cross-industry supply pacts are expected to narrow cost gaps with diesel and electric peers, sustaining the momentum of the fuel cell electric bus industry.

Fuel Cell Electric Bus Industry Leaders

Ballard Power Systems

New Flyer Industries

Hyundai Motor Company

Toyota Motor Corporation

Van Hool NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ballard Power Systems secured a 5 MW fuel-cell engine order for bus applications, reinforcing its OEM partnerships.

- February 2025: Orange County Transportation Authority awarded New Flyer a 40-unit hydrogen bus contract under FTA funding.

- February 2025: Brighton & Hove placed 34 double-deck hydrogen buses into service, making it one of the UK’s largest deployments.

- September 2024: Abu Dhabi launched a green-bus service mixing hydrogen and electric models within its 2030 mobility roadmap.

Global Fuel Cell Electric Bus Market Report Scope

Fuel cell-powered buses are buses that utilize fuel cell technology. Hydrogen and oxygen are combined in a fuel cell to generate heat, electricity, and water. The bus's electric motor is powered by the generated electricity thus propelling the bus.

The Fuel Cell Electric Bus Market is segmented based on Application, Bus Type, and Geography.

Based on Application, the market is segmented as Intercity and Intracity.

By Bus Type, the market is segmented as New Hydrogen Buses and Retrofitted Hydrogen Buses.

By Geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the world.

The report also provides market sizing and forecast for all the above-mentioned segments.

| Intercity |

| Intracity |

| New Hydrogen Buses |

| Retrofitted Hydrogen Buses |

| Proton-Exchange Membrane (PEMFC) |

| Phosphoric-Acid (PAFC) |

| Solid-Oxide (SOFC) |

| Others |

| Less than 150 kW |

| 150 - 250 kW |

| Above 250 kW |

| 9 - 12 metres |

| Over 12 metres (articulated) |

| Less than 300 km |

| 300 - 500 km |

| Above 500 km |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East & Africa |

| By Application | Intercity | |

| Intracity | ||

| By Bus Type | New Hydrogen Buses | |

| Retrofitted Hydrogen Buses | ||

| By Fuel-cell Type | Proton-Exchange Membrane (PEMFC) | |

| Phosphoric-Acid (PAFC) | ||

| Solid-Oxide (SOFC) | ||

| Others | ||

| By Power Rating | Less than 150 kW | |

| 150 - 250 kW | ||

| Above 250 kW | ||

| By Bus Length | 9 - 12 metres | |

| Over 12 metres (articulated) | ||

| By Driving Range | Less than 300 km | |

| 300 - 500 km | ||

| Above 500 km | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size of the fuel cell electric bus market?

It was valued at USD 1.36 billion in 2026 and is forecast to reach USD 3.52 billion by 2031, reflecting a 21.03% CAGR.

Which region leads fuel cell electric bus adoption?

Asia-Pacific holds 43.26% of global revenue, driven by China’s station build-out and Korea’s bulk orders.

How do hydrogen buses compare with battery-electric buses on cost?

Battery models remain cheaper on sub-200 km urban loops, but hydrogen becomes competitive on ranges above 300 km, particularly as green-hydrogen prices fall.

What is the main growth driver for hydrogen buses?

Mandatory zero-emission fleet regulations in North America, Europe, and parts of Asia create assured demand pipelines that de-risk OEM investments.

How quickly can a fuel cell electric bus refuel?

Typical depot systems deliver a full 350-bar fill in 10-20 minutes, enabling continuous multi-shift operation without long dwell times.

Page last updated on: