Network Point-of-Care Glucose Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.55 Billion |

| Market Size (2031) | USD 1.93 Billion |

| Growth Rate (2026 - 2031) | 4.50% CAGR |

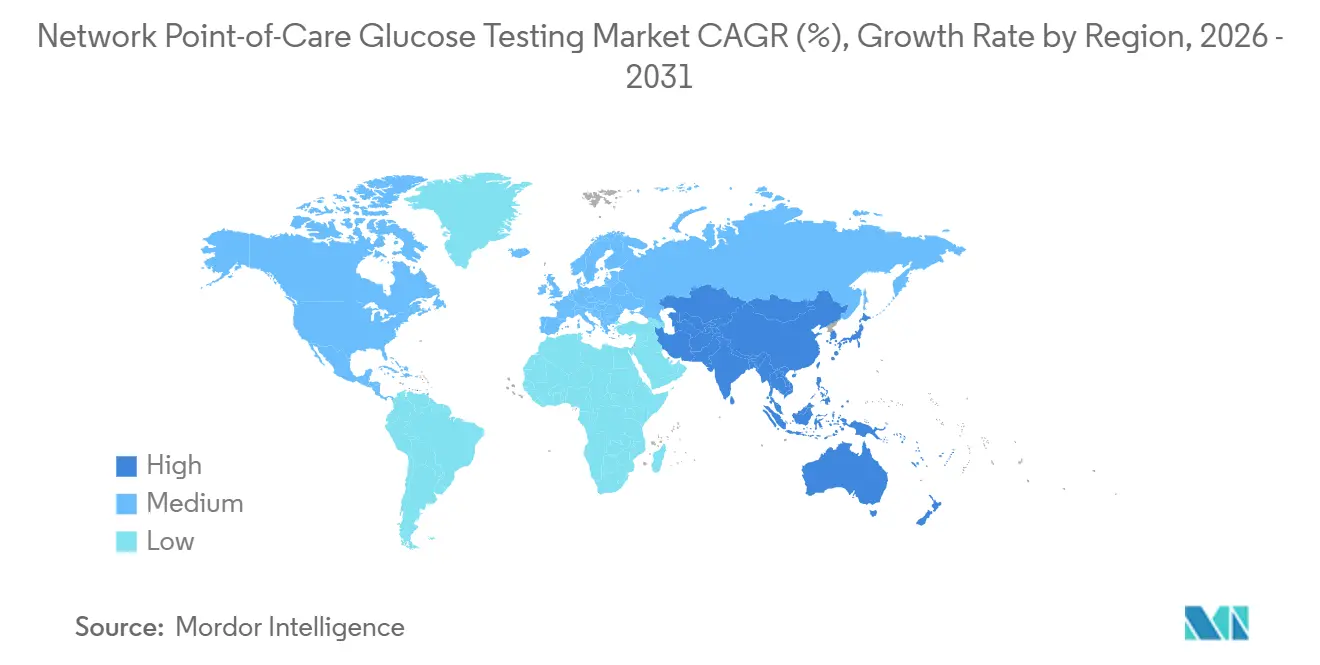

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

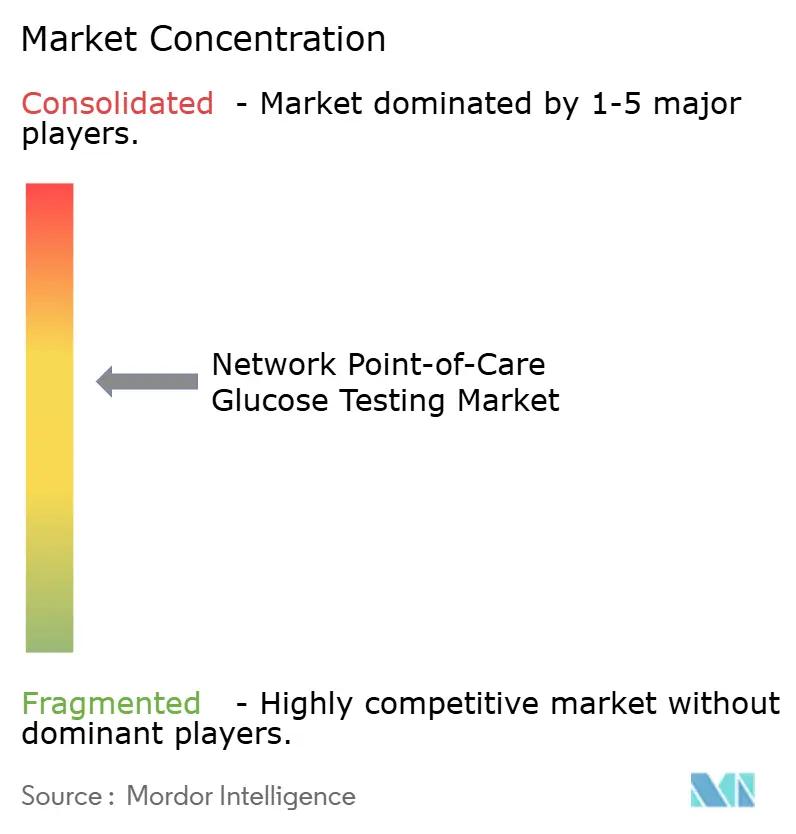

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Network Point-of-Care Glucose Testing Market Analysis by Mordor Intelligence

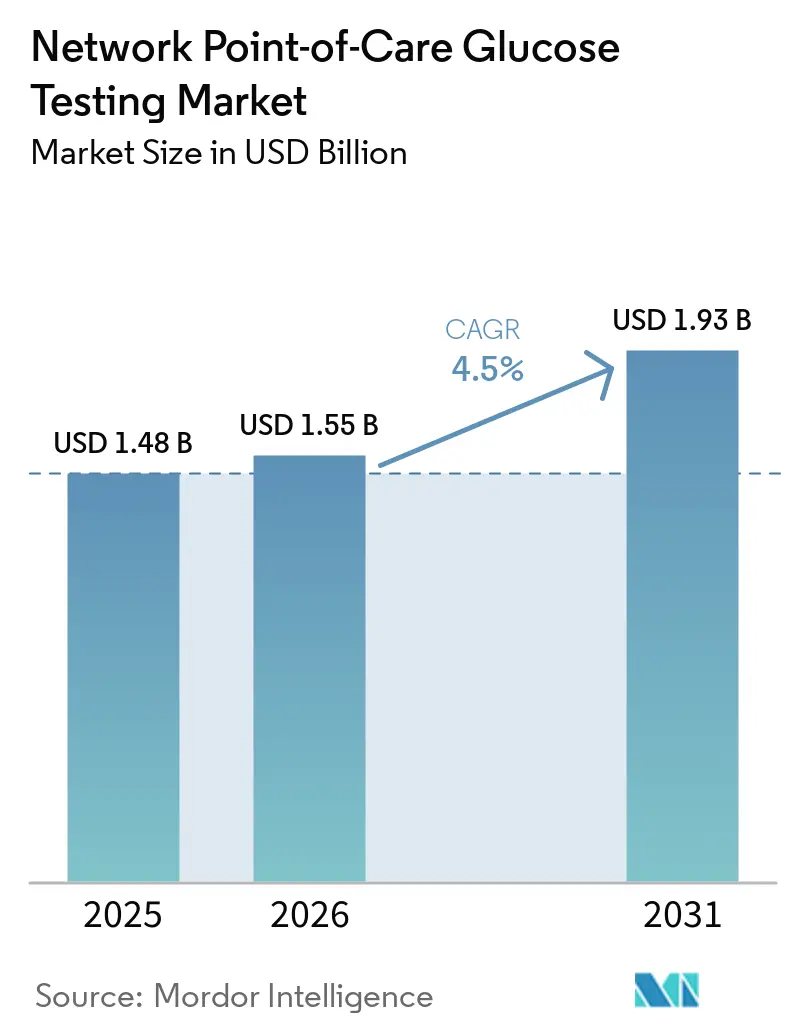

The Network Point-of-Care Glucose Testing Market size is expected to grow from USD 1.48 billion in 2025 to USD 1.55 billion in 2026 and is forecast to reach USD 1.93 billion by 2031 at 4.5% CAGR over 2026-2031.

Hospitals are increasingly adopting networked systems that directly transmit glucose readings into electronic health records, moving away from disconnected bedside meters and manual transcription. This shift emphasizes the importance of IT modernization and device connectivity, which are now as critical as meter accuracy during system evaluations. Procurement decisions remain tied to quality and workflow standards, particularly in markets where funding prioritizes connected point-of-care platforms that integrate with existing digital infrastructure. The network point-of-care glucose testing market is also growing due to rising interest in remote monitoring, cloud-based insulin dosing tools, and wearable glucose devices that enhance inpatient care. However, stricter cybersecurity requirements and budget constraints in underfunded hospital systems are slowing replacement cycles, favoring larger vendors with stronger regulatory and software capabilities.

Key Report Takeaways

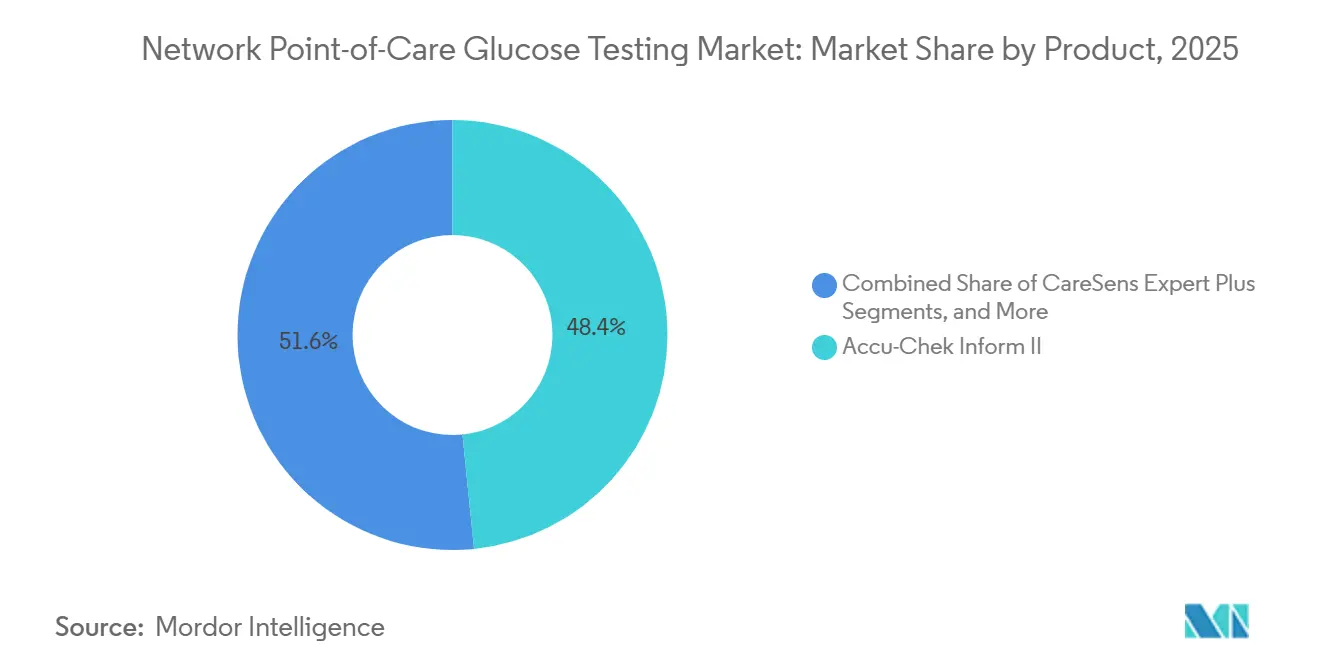

- By product type, Accu-Chek Inform II held 48.40% of revenue in 2025, while CareSens Expert Plus is projected to expand at a 7.80% CAGR through 2031.

- By modality, handheld and portable devices accounted for 42.87% of revenue in 2025, while wearable devices are expected to grow at an 8.25% CAGR through 2031.

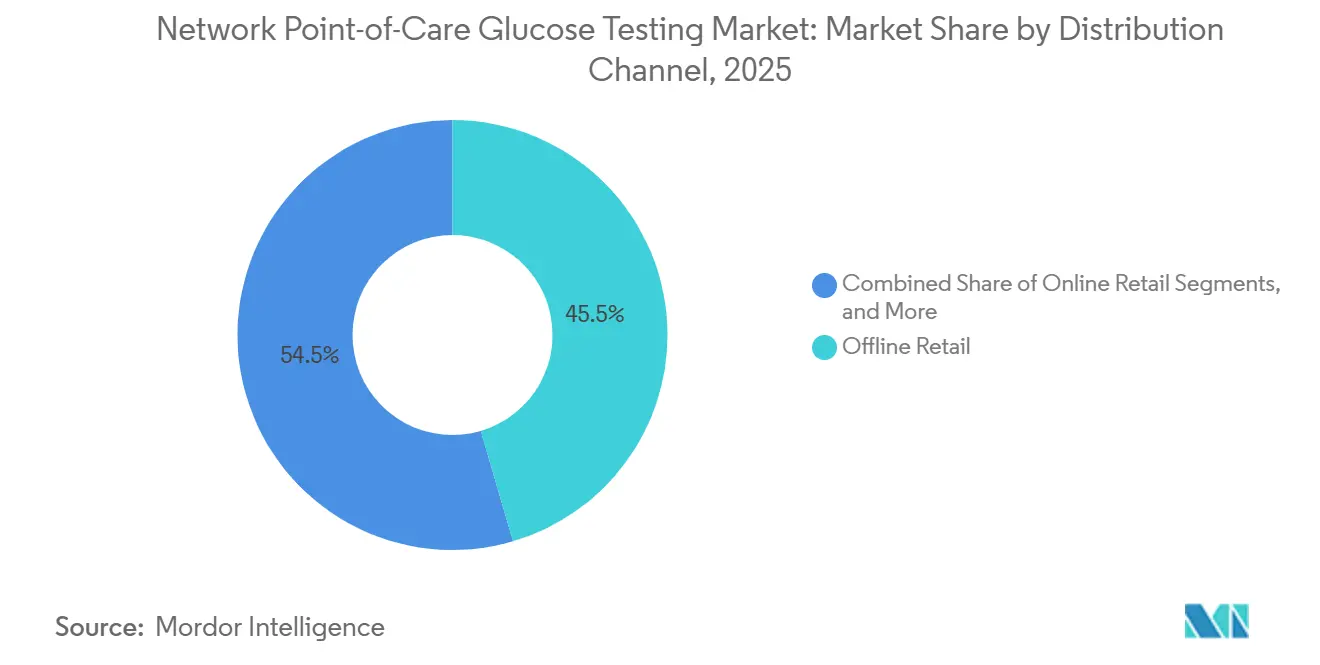

- By distribution channel, offline retail held 45.45% of revenue in 2025, while online retail is projected to advance at a 6.69% CAGR through 2031.

- By geography, North America held 40.27% of revenue in 2025, while Asia-Pacific is projected to grow at a 7.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Network Point-of-Care Glucose Testing Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Hospital network integration and centralization of real-time glucose data into EHR systems | +1.5% | Global, with primary uptake in North America and Germany | Short term (≤ 2 years) |

| Remote monitoring demand in high-risk diabetic and critically ill patient populations | +1.0% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Strong procurement preference for workflow-integrated, GPO-aligned devices | +0.8% | North America & EU | Short term (≤ 2 years) |

| Wider use of interoperable connected devices across hospital care settings | +0.7% | Global | Medium term (2-4 years) |

| Expansion of digital diabetes ecosystems linking device data to insulin dosing platforms | +0.6% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Reimbursement support for connected glucose monitoring in inpatient and remote settings | +0.5% | North America, EU, select APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hospital Network Integration: From Isolated Meters to Glycemic Command Centers

Hospitals are transitioning from standalone bedside testing to integrated glucose systems that directly input results into enterprise records. In April 2025, Abbott integrated FreeStyle Libre data into Epic via the Aura software platform. This move granted over 575,000 U.S. healthcare providers, catering to 280 million patients, seamless access to glucose data within their routine workflow. Once glucose data integrates with nursing documentation, billing, and treatment protocols, hospitals become reluctant to switch devices, even if competitors offer similar performance. Roche announced 24,000 new cobas pulse placements across EMEA by its 2026 Diagnostics Day, with a live U.S. launch in 2026, underscoring buyers' preference for systems that align with broader hospital software environments. Germany's KHZG funding program bolsters this trend, spotlighting connected point-of-care systems that resonate with hospital digitalization goals, catching the eye of procurement teams.

Remote Monitoring in High-Risk Diabetic Patients: Expanding Bedside Testing Beyond the Bedside

Remote glucose monitoring is evolving from a temporary solution to a sustainable care model for high-risk inpatients. In May 2026, Glooko secured FDA 510(k) clearance for EndoTool IV Cloud, marking it as the first cloud-based inpatient insulin dosing platform approved for hospital use. This innovation eliminates the need for on-premise infrastructure, enabling centralized management across facilities. A multicenter study in Diabetes Care highlighted that real-time continuous glucose monitoring, paired with remote nursing oversight, curbed hypoglycemia in insulin-dependent inpatients without adverse effects. This allows hospitals to extend specialist supervision without overburdening bedside staff and emphasizes the growing importance of software platforms in procurement discussions.

Expansion of Digital Diabetes Ecosystems: Devices as Entry Points, Not Endpoints

Connected glucose devices are increasingly recognized for their role in feeding data into expansive diabetes workflows, rather than just displaying readings at the bedside. Glooko advanced this approach in June 2026 by launching an insulin pump settings EHR integration, which incorporates basal schedules, insulin-to-carbohydrate ratios, and closed-loop status into EHR flowsheets. This integration allows clinicians to monitor glucose trends and insulin settings in a unified platform, minimizing the need to navigate multiple device portals. Hospitals now prioritize open integration over closed data models, reshaping supplier evaluations. Vendors supporting broad interoperability are advancing faster in hospital purchasing processes, solidifying the network point-of-care glucose testing market's connection to the development of digital diabetes ecosystems in hospitals and outpatient settings.

Reimbursement Support for Connected Glucose Monitoring: Unlocking Volume in Outpatient Transition Zones

Reimbursement backing is amplifying the value of connected glucose data, extending its significance beyond the initial inpatient stay. In the U.S., the rise in remote patient monitoring billing has increased interest in glucose systems capable of transmitting data post-discharge. This capability allows providers to integrate monitoring into documented follow-up workflows, ensuring a smooth transition for insulin-dependent patients returning to home management. In December 2025, Findex and Abbott Japan signed a data-linkage agreement connecting FreeStyle Libre 2 CGM data with the Medical Avenue patient guidance app and Claio medical data management system, enhancing continuity between hospital care and outpatient follow-up.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Cybersecurity review burden for premarket submission of connected glucose devices | -0.5% | Global | Short term (≤ 2 years) |

| Interoperability friction across heterogeneous hospital IT architectures and medical devices | -0.4% | Global | Medium term (2-4 years) |

| Test strip and meter quality variability affecting clinical confidence in connected results | -0.3% | Global | Short term (≤ 2 years) |

| Budget pressure on healthcare facilities constraining medical technology refresh cycles | -0.2% | MEA, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity Review Burden: Compliance as a Market Entry Barrier

Connected glucose meters now face stricter compliance requirements before regulatory approval. The FDA’s final cybersecurity guidance, issued on June 27, 2025, updated Section 524B expectations, requiring software bills of materials, vulnerability disclosure plans, and detailed cybersecurity risk assessments in premarket submissions. These measures are critical as connectivity failures can erode trust in clinical outcomes. In December 2024, the FDA announced a Class I software correction for Nova Biomedical’s StatStrip glucose and glucose/ketone meters due to a software error that risked transmitting incorrect results during simultaneous wireless events. Smaller vendors often struggle with the time and costs needed to meet these demands, making market entry more challenging and favoring larger companies with stronger regulatory capabilities.

Interoperability Friction: The Hidden Cost of Multi-Vendor Hospital Environments

Many hospitals operate mixed-vendor point-of-care systems, creating integration challenges that exceed product claims. While a glucose meter may support connectivity, it often requires custom middleware setups and local validation to ensure smooth data transfer into laboratory or hospital information systems. A multicenter study on the cobas pulse system revealed that achieving reliable data flow across diverse IT environments required significant configuration and compliance validation during deployment.[1]National Center for Biotechnology Information, “Remote Glucose Monitoring Feasibility Study in Inpatients,” Diabetes Care via PMC, pmc.ncbi.nlm.nih.gov These additional efforts increase time, costs, and coordination, prompting procurement teams to assess devices based on total implementation effort rather than just features or performance. Consequently, the network point-of-care glucose testing market heavily depends on hospitals’ IT readiness and integration capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Accu-Chek Dominance Tested by Connectivity-First Challengers

Accu-Chek's Inform II, supported by Roche's navify POC Operations software, dominated the network point-of-care glucose testing market with a 48.40% share in 2025. This stronghold, particularly in European and North American hospitals, is reinforced by Roche's software, which supports over 100 device types and streamlines data management. Buyers now prioritize workflow platforms alongside testing devices, reflecting the industry's shift towards data management and compliance reporting. CareSens Expert Plus, featuring Wi-Fi, Ethernet, USB, and NFC connectivity, is the fastest-growing product, projected to expand at a 7.80% CAGR through 2031.

StatStrip, the only FDA-cleared meter for all critically ill patient sample types, continues to play a pivotal clinical role. Nova Biomedical strengthened this position in March 2025 with its next-generation platform, offering a Linux OS, RFID data entry, and a wider hematocrit range. HemoCue's Glucose 201+ maintains a steady presence in decentralized care, reporting 20 million tests in 2024 across 11,000 U.S. practices. Abbott's i-STAT 1 system remains critical in emergency settings, with FDA-cleared updates in August 2025 ensuring its relevance in multi-analyte testing. The market's leading systems integrate clinical functionality with hospital operations seamlessly.

By Modality: Handheld Devices Lead, But Wearables Are Rewriting the Clinical Logic

Handheld devices accounted for 42.87% of the network point-of-care glucose testing market in 2025, remaining the preferred choice for inpatient protocols due to their established presence and ease of integration into nursing routines. However, wearables are projected to grow at an 8.25% CAGR through 2031, driven by expanding clinical applications. A 2025 review highlighted the feasibility of real-time CGM with EHR integration in reducing fingerstick checks, though confirmatory testing remains standard in many settings.

Wearables are gaining traction as their clinical use cases expand. Abbott's CE Mark approval in May 2026 for its dual glucose-ketone biowearables highlights this trend. Benchtop devices, while the smallest modality, cater to lab-adjacent settings prioritizing throughput over portability. Japan's 2024 reimbursement pathway for inpatient real-time CGM signals faster wearable adoption. The competition is shifting from device form factors to the value of continuous, connected data in care decisions.

By Distribution Channel: Offline Retail Holds Share, But Digital Procurement Is Restructuring Hospital Purchasing

Offline retail held 45.45% of the network point-of-care glucose testing market in 2025, as hospitals relied on established distributor networks and direct contracts for regulated glucose systems. These purchases often involve validation, service agreements, and staff training, favoring distributors capable of long-term support. Online retail is projected to grow at a 6.69% CAGR through 2031, as facilities increasingly use digital tools for recurring supplies like strips and lancets. The market is split, with capital equipment moving through traditional channels and consumables finding easier access online.

Direct sales remain crucial for premium accounts, allowing major suppliers to bundle devices with software and support. Roche, Abbott, and Nova Biomedical excel in this model, as hospitals prefer comprehensive packages covering implementation and training. Smaller manufacturers face challenges in matching the extensive service structures of larger vendors. In emerging markets, digital procurement improves access to consumables, even as hospitals rely on traditional processes for initial system decisions. This dynamic shapes channel competition, balancing complex device adoption with swift supply fulfillment.

Geography Analysis

In 2025, North America accounted for 40.27% of the network point-of-care glucose testing market, making it the largest regional contributor. The region benefits from strong tertiary care infrastructure, high EHR adoption, and reimbursement systems that support connected monitoring. U.S. hospital networks often integrate glucose systems into broader IT and pharmacy workflows, favoring vendors with advanced integration tools. Roche’s 2026 launch of cobas pulse in the U.S. highlights the region's significant replacement and upgrade potential. Europe remains the second-largest market, with Germany leading due to KHZG funding, which drives adoption of connected point-of-care systems aligned with hospital digitalization strategies.

Asia-Pacific is projected to grow at a 7.45% CAGR through 2031, the fastest among all regions. Growth is driven by expanding hospital infrastructure, increasing diabetes care needs, and rising interest in connected monitoring in countries like China, India, Japan, and South Korea. Hospitals are increasingly adopting systems that support bedside testing and digital data integration. In 2025, Findex and Abbott Japan linked FreeStyle Libre 2 CGM data with patient guidance and medical data management systems in Japan, showcasing advancements in data connectivity across care settings.

The Middle East, Africa, and South America exhibit uneven growth due to budget constraints, fragmented IT systems, and slower device refresh cycles. However, urban hospital networks in Brazil and well-funded Gulf health systems present opportunities for connected glucose platforms. Multinational vendors play a key role in these regions, as hospitals often require significant implementation support. Market growth in these areas depends heavily on funding stability and digital readiness.

Competitive Landscape

Roche, Abbott, and Nova Biomedical dominate the network point-of-care glucose testing market, particularly in hospital settings. These industry leaders have shifted their competitive focus beyond mere device accuracy and strip economics. Today, software capabilities, interoperability, and seamless workflow integration play pivotal roles in contract negotiations. Roche solidified its market stance by merging its established meters with navify POC Operations and broadening the reach of cobas pulse across various hospital systems. Similarly, Abbott integrated its Libre data into Epic in April 2025, ensuring glucose data remains within the familiar clinical workflows of healthcare providers. Glooko intensifies the competition with its cloud-based inpatient dosing platform and EHR integration tools, emphasizing the significance of software orchestration alongside hardware connectivity.

These strategic maneuvers indicate a shift in competition, extending from mere bedside testing to encompassing broader glucose management functions. In May 2026, Abbott secured a CE Mark for its Libre Duo, introducing dual glucose-ketone sensing to wearables. This advancement elevates standards for connected monitoring, especially in high-risk diabetes management. Medtronic, too, is deepening its foray into integrated glycemic control. In November 2025, the FDA granted 510(k) clearance for Medtronic's SmartGuard Technology Predictive Low Glucose, categorizing it under interoperable automated glycemic controllers.

Switching costs have emerged as a significant competitive factor. Once hospitals establish validated interfaces, train their staff, and synchronize glucose data with nursing and pharmacy records, transitioning to a new system proves more disruptive than the device's price might indicate. This challenge is magnified by cybersecurity demands, as larger suppliers possess a distinct advantage in maintaining documentation, rolling out software updates, and ensuring audit readiness over time. Consequently, while the network point-of-care glucose testing market remains open to new entrants, the most substantial gains are poised for those adept at simultaneously addressing workflow and compliance challenges.

Network Point-of-Care Glucose Testing Industry Leaders

Abbott Laboratories

Ascensia Diabetes Care Holdings AG

F. Hoffmann-La Roche Ltd.

Nova Biomedical Corporation

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Glooko introduced the first Insulin Pump Settings EHR Integration, enabling device-agnostic visualization of insulin pump data, including basal schedules and insulin-to-carbohydrate ratios, directly in EHR flowsheets.

- May 2026: Abbott received CE Mark approval for Libre Duo and Libre Duo 10 Day, the first dual glucose-ketone biowearables for continuous monitoring of both analytes from a single sensor.

- May 2026: Glooko obtained FDA 510(k) clearance for EndoTool IV Cloud, the first cloud-based insulin dosing platform designed for hospital use.

- February 2026: Trividia Health issued a Class I recall for all TRUE METRIX Blood Glucose Monitoring Systems across multiple regions due to an E-5 error code labeling issue.

- January 2026: Ascensia Diabetes Care signed an agreement to transfer Eversense CGM commercialization to Senseonics, with the U.S. transition completed in January 2026 and Europe expected by June 2026.

Global Network Point-of-Care Glucose Testing Market Report Scope

As per the scope of the report, network Point-Of-Care (POC) Glucose Testing refers to blood sugar monitoring systems where portable, bedside testing devices (like glucometers) are digitally connected to a hospital or clinic's Electronic Health Records (EHR) and laboratory information systems.

The network point-of-care glucose testing market is segmented by product type, modality, distribution channel, and geography. By product type, the market includes Accu-Chek Inform II, StatStrip, HemoCue, BAROzen H Expert Plus, i-STAT, and CareSens Expert Plus. By modality, the market is segmented into handheld/portable devices, wearable devices, and benchtop devices. By distribution channel, the market is categorized into online retail, offline retail, and direct sales. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Accu-Chek Inform II |

| StatStrip |

| HemoCue |

| BAROzen H Expert Plus |

| i-STAT |

| CareSens Expert Plus |

| Handheld/Portable Devices |

| Wearable Devices |

| Benchtop Devices |

| Online Retail |

| Offline Retail |

| Direct Sales |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Accu-Chek Inform II | |

| StatStrip | ||

| HemoCue | ||

| BAROzen H Expert Plus | ||

| i-STAT | ||

| CareSens Expert Plus | ||

| By Modality | Handheld/Portable Devices | |

| Wearable Devices | ||

| Benchtop Devices | ||

| By Distribution Channel | Online Retail | |

| Offline Retail | ||

| Direct Sales | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of network point-of-care glucose testing by 2031?

The sector is projected to reach USD 1.93 billion by 2031, up from USD 1.55 billion in 2026, at a 4.50% CAGR over 2026-2031.

Which product leads hospital adoption today?

Accu-Chek Inform II led in 2025 with 48.40% revenue share, supported by its long hospital presence and Roche's connected workflow tools.

Which modality is expanding the fastest through 2031?

Wearable devices are forecast to grow the fastest at an 8.25% CAGR as hospitals become more comfortable with connected continuous monitoring.

Why does North America hold the largest regional share?

North America held 40.27% in 2025 because of strong hospital IT adoption, dense tertiary care networks, and better support for connected clinical workflows.

What is the main factor slowing adoption of connected glucose systems?

Cybersecurity and integration demands are the main barriers, because connected devices now need stronger regulatory documentation and more hospital IT validation.

How are hospitals changing the way they buy these systems?

Hospitals still rely on offline and direct channels for validated system purchases, but online procurement is growing faster at 6.69% CAGR for recurring supplies and consumables.

Page last updated on: