Latin America Self Blood Glucose Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

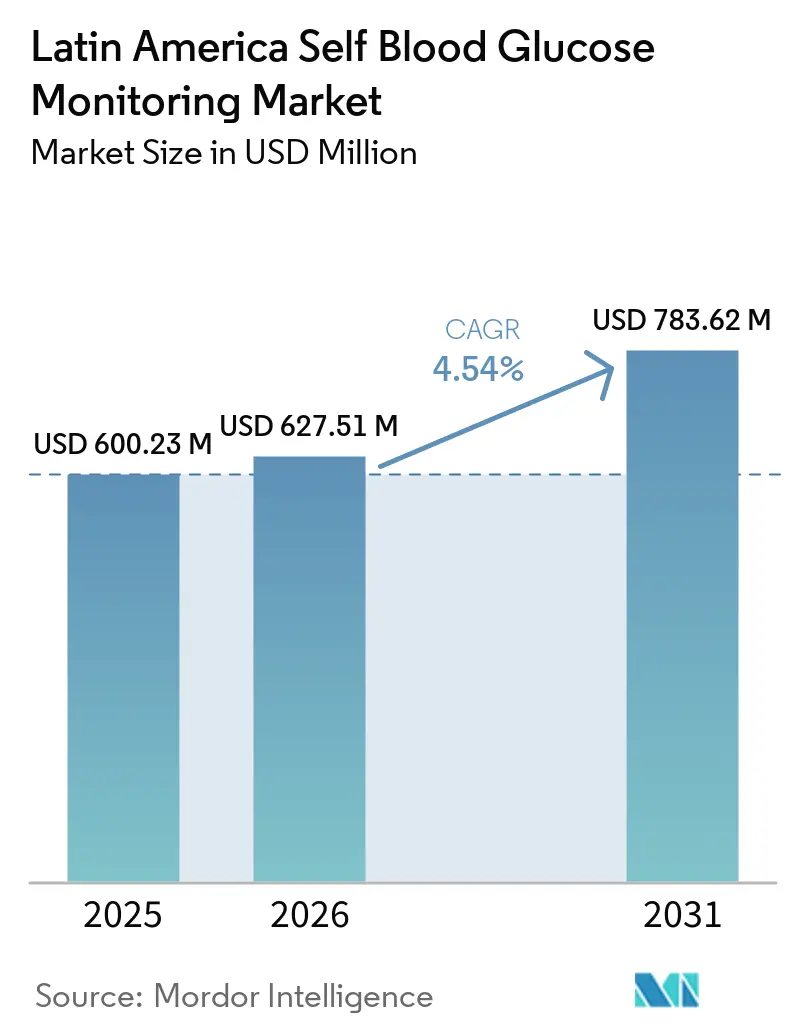

| Base Year Market Size (2025) | USD 600.23 Million |

| Market Size (2026) | USD 627.51 Million |

| Market Size (2031) | USD 783.62 Million |

| Growth Rate (2026 - 2031) | 4.54% CAGR |

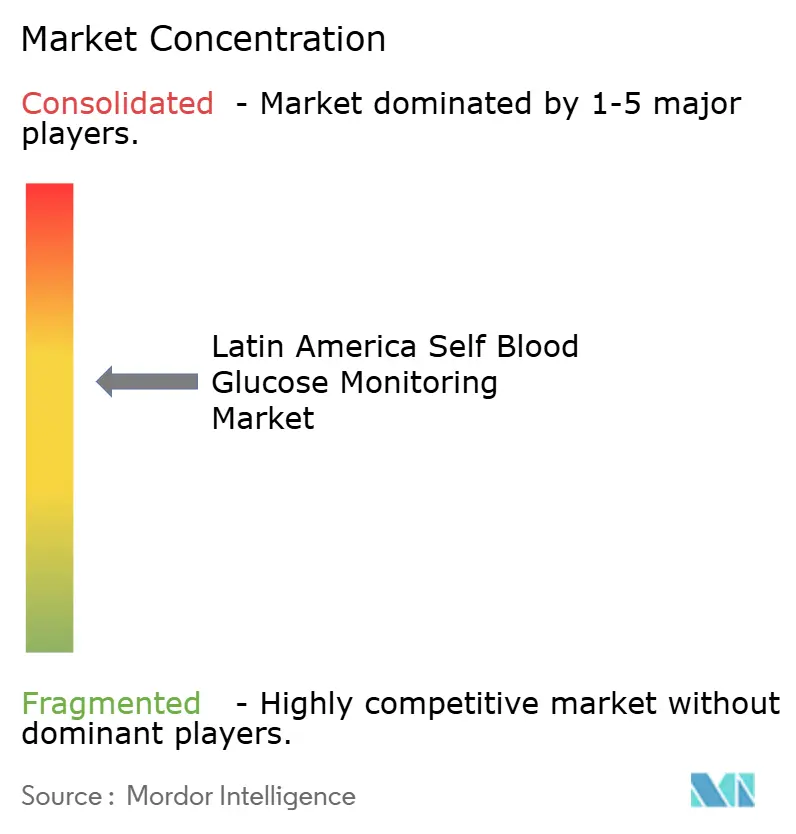

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America Self Blood Glucose Monitoring Market Analysis by Mordor Intelligence

The Latin America Self Blood Glucose Monitoring Market size was valued at USD 600.23 million in 2025 and is estimated to grow from USD 627.51 million in 2026 to reach USD 783.62 million by 2031, at a CAGR of 4.54% during the forecast period (2026-2031).

Test strips set the tone for recurring value creation through high-frequency capillary testing, while retail pharmacy reach and emerging e-pharmacy logistics shape access patterns in large urban corridors. Brazil retains the largest country-level base by value, while Mexico marks the fastest growth pace to 2031, reflecting demand concentration in high-prevalence zones and dense retail networks. Type 2 diabetes remains the principal demand pool, with gestational diabetes as the fastest-growing cohort, as prenatal protocols broaden monitoring requirements in major cities. Continuous glucose monitoring expands among insulin users in private channels, yet fingerstick self-testing continues to account for most retail volumes across non-insulin Type 2 populations. Tighter import oversight and quality enforcement[1]Agência Nacional de Vigilância Sanitária, “Dispositivos Médicos com Irregularidades São Barrados Pela Anvisa,” ANVISA, gov.br reshape tender-dependent volumes in key locales, and partnerships with large pharmacy chains support brand placement and downstream adherence programs.

Key Report Takeaways

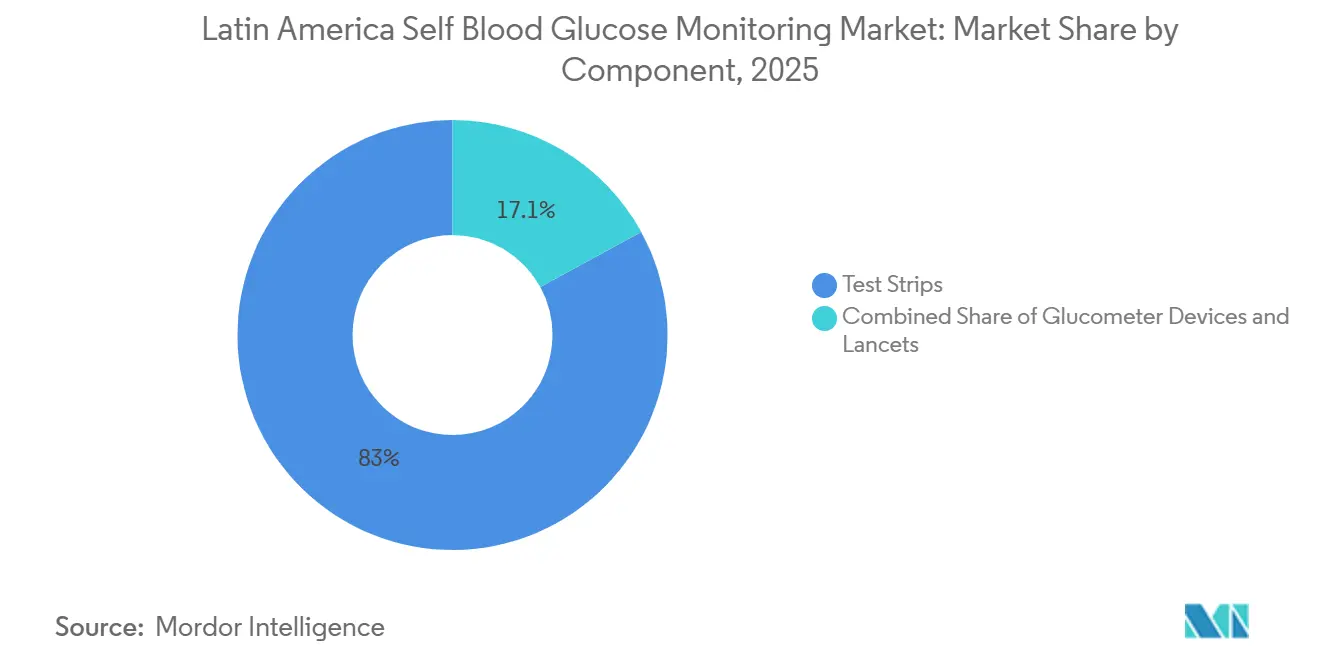

- By component, test strips led with 82.95% revenue share in 2025, and the same sub-segment is projected to grow at a 5.21% CAGR through 2031.

- By patient type, Type 2 diabetes accounted for 88.35% of 2025 revenues, while gestational diabetes is forecast to expand at a 7.46% CAGR to 2031.

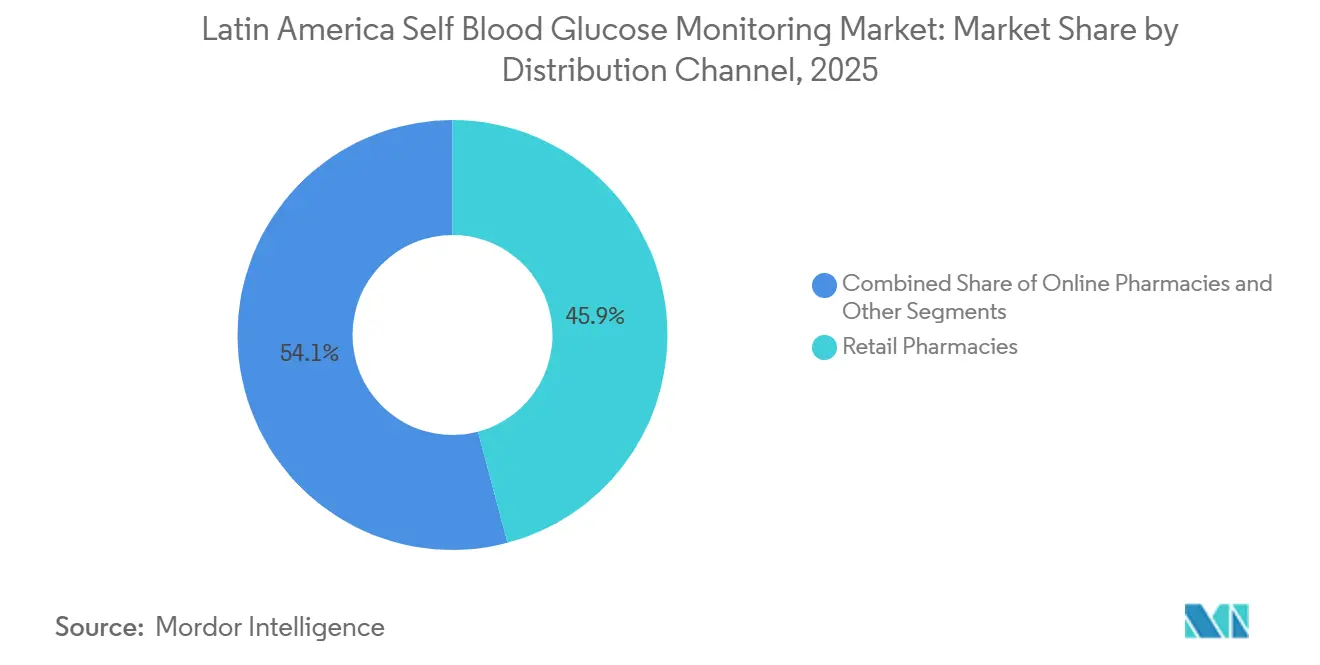

- By distribution channel, retail pharmacies accounted for a 45.89% share of the Latin America Self Blood Glucose Monitoring market size in 2025, while online pharmacies recorded the highest projected CAGR at 8.85% through 2031.

- By end-user, homecare settings held 58.09% of 2025 revenues and are projected to advance at a 5.37% CAGR over 2026-2031.

- By country, Brazil held 39.26% in 2025, while Mexico is projected to grow at a 5.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Latin America Self Blood Glucose Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diabetes Prevalence and Undiagnosed Burden | +1.8% | Brazil, Mexico, Argentina core; spillover to Chile, Colombia | Medium term (2–4 years) |

| Public Provision and Reimbursement of SMBG Supplies | +1.3% | Brazil SUS cities, Argentina PAMI, Mexico IMSS/ISSSTE zones | Long term (≥ 4 years) |

| Shift to Home-Based Self-Management and Digital Enablement | +0.9% | Urban centers—São Paulo, Mexico City, Buenos Aires | Short term (≤ 2 years) |

| Expansion of Retail and E-Pharmacy Fulfillment Improving Access | +0.6% | National, with early gains in Santiago, Valparaíso, Concepción | Medium term (2–4 years) |

| Meter–Strip Brand Lock-In Sustaining Recurring Strip Volumes | +0.5% | Global | Long term (≥ 4 years) |

| Omnichannel Pharmacy Programs Boosting Adherence | +0.4% | Brazil metropolitan areas, Mexico top-tier cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence and Undiagnosed Burden in Latin America

The rising burden of diabetes in Latin America increases routine glucose self-testing for newly identified cases and for patients intensifying therapy. Mexico exemplifies the challenge with a high adult prevalence profile[2]International Diabetes Federation, “Mexico Country Profile,” Diabetes Atlas, diabetesatlas.org, which sustains frequent monitoring across urban corridors with dense pharmacy networks. Health systems are pushing more opportunistic screening through primary care and workplace settings, which channels newly diagnosed patients into the Latin America self blood glucose monitoring market as a first step in self-management. Earlier case detection links meter adoption to behavioral coaching and diet adjustment, which stabilizes baseline strip use before any transition to advanced therapies. Primary care teams emphasize capillary testing for non-insulin patients to support medication titration and to flag complications sooner. These shifts lift recurring strip throughput as more adults formalize daily or weekly testing routines aligned to local clinical guidance.

Public Provision and Reimbursement of SMBG Supplies

Public-sector programs across the region reinforce self-monitoring by bundling meters and strips into chronic disease pathways for prioritized cohorts. City and provincial programs register eligible users and embed SMBG refills within scheduled follow-ups, which reduces missed pickups and keeps adherence steady over time. Social security and retiree plans strengthen access for older patients who require more frequent checks due to multi-morbidity and insulin use. Where public formularies exclude meters or limit strip allotments, retail purchases and employer support fill the gap. This patchwork still benefits the Latin America Self Blood Glucose Monitoring Market because multiple access routes stabilize monthly volumes as patients combine public supplies with retail top-ups. In dense urban areas, this mix of routes maintains predictable flow through pharmacy chains and distribution centers.

Shift to Home-Based Diabetes Self-Management and Digital Enablement

Structured home-based monitoring with connected meters and coaching apps is improving outcomes and lowering acute care use. In Ecuador, a controlled program using Bluetooth-enabled SMBG integrated with app support reduced mean HbA1c by 2.67 percentage points versus 1.38 points in standard care, eliminated emergency department visits that had occurred at a 16% baseline rate, and generated net monthly savings per patient, which together make a strong case for scaled implementation, according to a February 2026 article published in Frontiers in Clinical Diabetes and Healthcare[3]Frontiers Editorial, “Structured Telemonitoring With Bluetooth-Enabled SMBG Reduces HbA1c and Acute Events in Ecuador,” Frontiers in Clinical Diabetes and Healthcare, frontiersin.org. The same protocol reported annualized hospital cost avoidance when extrapolated across the enrolled population, indicating that consistent capillary testing plus digital reminders can avert destabilizing events and admissions. As programs expand, high-frequency SMBG during dose titration and behavior change supports safer transitions for insulin and oral regimens. Connected meters and app dashboards also streamline clinician review between visits, which supports targeted refills rather than blanket allocations. These gains position the Latin America self blood glucose monitoring market as a foundational layer in hybrid digital care models that blend in-person consults with data-driven follow-up.

Expansion of Retail and E-Pharmacy Fulfillment is Improving SMBG Access

Large pharmacy chains and growing e-pharmacy platforms are making SMBG supplies more accessible through delivery, click-and-collect, and subscription services. Bundled kits with starter strips reduce friction for first-time users and improve onboarding for households managing multiple diabetic members. Loyalty programs and auto-ship refills encourage continuous testing behavior, which raises strip throughput and improves stickiness for leading brands. As omnichannel options spread from major cities to secondary hubs, shopping convenience and transparent pricing shape brand choice. Peer-reviewed research from Peru has documented wide price dispersion across meters and strips, which underscores why price visibility and channel choice affect user behavior within the Latin America self blood glucose monitoring market. These channel dynamics support faster uptake in the fastest-growing country markets.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating CGM Adoption Among Insulin Users Reducing Fingerstick Frequency | -0.9% | Brazil urban hubs, Mexico City, Santiago | Medium term (2–4 years) |

| Import Dependence, FX Volatility, and Price Caps Pressure SMBG Margins | -0.7% | Argentina, Brazil (reais exposure), regional tariff zones | Short term (≤ 2 years) |

| Regulatory Suspensions/Quality Interdictions Disrupting Public Tenders | -0.3% | Brazil ANVISA jurisdiction, Mexico COFEPRIS oversight | Short term (≤ 2 years) |

| Counterfeit/Substandard Strips on Informal Channels Erode Trust | -0.2% | Border corridors, informal retail networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating CGM Adoption Among Insulin Users Reducing Fingerstick Frequency

Continuous and flash glucose sensors gain traction among insulin users in private channels, which reduces routine fingerstick frequency for patients who achieve stable wear and scanning habits. As more endocrinology clinics adopt CGM-first protocols for poor control, the highest-frequency strip users transition to sensors for daily trend visibility. This substitution affects the Latin America Self Blood Glucose Monitoring Market most in affluent metro areas where private coverage or out-of-pocket capacity is stronger. For non-insulin Type 2 cohorts, SMBG remains standard for dose titration and lifestyle management, which sustains a large base of recurring strip demand. Many clinics still recommend periodic capillary checks for CGM users to confirm readings during dose changes or when sensors signal instability, which preserves some strip volume in hybrid workflows. The net effect is a rebalancing of strip consumption away from intensive insulin users toward broader non-insulin populations and onboarding cohorts.

Import Dependence, FX Volatility, and Price Caps Pressure SMBG Margins

Import reliance for meters and strips exposes regional operators to currency swings, customs timelines, and shifting tariff classifications. In countries with administered reimbursement or price caps, sudden depreciation can compress distributor margins when price adjustments lag currency movements. Procurement fragmentation and varied mark-ups further compound retail price dispersion, which influences product rotation between premium and value tiers in the Latin America Self Blood Glucose Monitoring Market. A February 2025 article published in BMJ Public Health[4]BMJ Public Health Editorial, “Availability and Prices of Blood Glucose Monitoring Products in Peru,” BMJ Public Health, bmjpublichealth.bmj.com highlighted wide differences in the availability and retail prices of glucose testing products, which validates the impact that procurement and channel structure have on affordability and access. Companies respond with selective local assembly and tighter forecast collaboration with pharmacy chains to reduce stockouts and avoid distressed price promotions. These measures help stabilize supply, but volatility remains a planning risk for both tender and retail volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Recurring Strip Sales Anchor Profitability

Test strips captured 82.95% of 2025 revenue and are projected to grow at a 5.21% CAGR, reflecting the dominant role of consumables in the Latin America Self Blood Glucose Monitoring Market. Test strips accounted for a large share of the Latin America self blood glucose monitoring market size in 2025, while meter hardware saw thinner unit margins as placement strategies emphasized recurring strip pull-through. Subsidized or low-margin meter placements remain common to accelerate onboarding, while strip repurchases extend over long cycles due to brand and ecosystem lock-in. That lock-in strengthens because many patients prefer compatible meters and strips that match coaching materials and clinic protocols. Features that reduce waste, such as second-chance sampling and guided fill indicators, also help stretch budgets and improve perceived value for public programs and families. As more users track daily or weekly readings at home, predictable strip replacement drives steady cash-register throughput in both retail and e-pharmacy channels.

Lancets retain a smaller revenue role compared with strips but remain high in unit volumes because of single-use hygiene protocols and patient safety rules. Vendors often bundle lancets with new meters or starter kits, which simplifies initial use for newly diagnosed patients. Procurement specifications in public schemes continue to emphasize quality control for consumables, which favors established brands with strong post-market surveillance records. In urban markets where onboarding is frequent, pharmacy teams help align meter choice, lancet gauge, and strip compatibility during counseling. That support reduces returns caused by setup errors and inconsistent sampling techniques and sustains positive user experience. Taken together, strips anchor recurring revenue, hardware sustains brand placement, and lancets complete the routine at-home testing kit in the Latin America self blood glucose monitoring market.

By Patient Type: Type 2 Majority Contrasts with Gestational Surge

Type 2 diabetes represented 88.35% of the patient mix in 2025, which sets the baseline for meter placements and monthly strip consumption across the Latin America self blood glucose monitoring market. Type 2 diabetes accounted for 88.35% of the Latin America self blood glucose monitoring market share in 2025, and physicians often recommend routine SMBG during dietary changes, oral medication titration, and comorbidity management. That pattern distributes testing intensity across millions of non-insulin patients rather than concentrating volume only in insulin users. As mobile apps and connected meters become more common, many Type 2 users adopt weekly patterns that balance test frequency with coaching feedback. Clinics reinforce SMBG to flag destabilization early, which supports treatment adherence and reduces avoidable acute care. These habits underpin stable strip replacement rates across large urban centers.

Gestational diabetes is projected to grow at a 7.46% CAGR through 2031, making it the fastest-growing patient segment in the Latin America self blood glucose monitoring market. Prenatal care teams are formalizing fasting and postprandial capillary checks to manage maternal and neonatal outcomes, which expands meter and strip allocations for this cohort. Structured prenatal pathways also build SMBG familiarity that can sustain continued monitoring for women at risk of Type 2 progression after delivery. Public clinics and retail pharmacies help with onboarding by demonstrating lancing techniques and meter setup during prenatal visits and purchase encounters. The combination of expanding prenatal guidelines and patient education underpins the segment’s strong growth outlook.

By Distribution Channel: Retail Leads While Digital Accelerates

Retail pharmacies commanded 45.89% of 2025 distribution, supported by dense storefront networks and in-store counseling that improves SMBG onboarding across the Latin America Self Blood Glucose Monitoring Market. Retail pharmacies accounted for a 45.89% share of the Latin America self blood glucose monitoring market size in 2025, with store teams assisting meter setup, calibration checks, and refill timing. Loyalty programs and periodic wellness campaigns encourage regular testing and bulk purchases of strips. Retail’s presence in high-traffic neighborhoods helps newly diagnosed patients start testing quickly after prescription or counseling. As clinics refer patients to nearby pharmacies for supplies, the convenience factor supports consistent follow-through for monthly refills. This interplay of proximity, counseling, and promotions keeps retail at the center of replenishment behavior.

Online pharmacies are projected to grow at an 8.85% CAGR and are expanding coverage with same-day delivery in dense metros and fast pickup in secondary cities. Auto-ship subscriptions help stabilize strip volumes by reducing missed refills and smoothing demand between promotional peaks. For families managing multiple diabetic members, e-pharmacy baskets that bundle meters, strips, and lancets simplify purchasing and budgeting. Integration of e-prescriptions from telemedicine extends access for patients who prefer to avoid in-person pharmacy queues. Business-to-business channels maintain a steady share by serving public tenders and hospital formularies that operate under structured procurement calendars. Other channels, including employer programs and non-government clinics, add incremental volume and often pioneer alternate financing to support adherence in the Latin America self blood glucose monitoring market.

By End-User: Homecare Dominance Reflects Self-Management Imperative

Homecare settings held 58.09% of 2025 demand and are forecast to grow at a 5.37% CAGR, reflecting the central role of at-home testing in chronic disease management across the Latin America self blood glucose monitoring market. Self-testing enables dose titration, lifestyle adjustment, and early warning of destabilization without frequent clinic visits. Education on correct sampling, lancet safety, and reading interpretation improves user confidence, which supports consistent testing frequency. Retail pharmacy teams and community nurses reinforce proper technique during onboarding. Connected meters and apps further guide users on testing times and trends, which enhances adherence during the first months after diagnosis. These supports strengthen the foundation for long-term SMBG behavior.

Hospitals and clinics serve targeted roles where SMBG complements inpatient glucose control, outpatient follow-ups, and laboratory evaluations. In acute settings, capillary testing pairs with protocols for medication adjustment and decompensation management. Outpatient clinics use SMBG logs to inform treatment changes, while diagnostic centers employ capillary readings as triage before confirmatory laboratory tests. Digital care models that combine SMBG with app-based coaching have demonstrated improved outcomes and eliminated emergency department visits in controlled cohorts, which supports the case for scaling structured telemonitoring in the region. As these practices diffuse, homecare remains the anchor for daily testing while institutional sites provide escalation pathways and oversight. That mix keeps demand broad-based across the Latin America Self blood glucose monitoring market.

Geography Analysis

Brazil held 39.26% of the Latin America self blood glucose monitoring market size in 2025, which reflects its large diagnosed base and wide public distribution footprints within the Latin American market. Brazil’s municipal programs register eligible users and distribute meters and strips through local health units, which stabilizes recurring volumes within priority cohorts. Regulatory enforcement intensified in early 2026, when the national regulator barred irregular medical devices and halted imports tied to classification issues, which raised quality safeguards for public tenders and retail channels. Private channels complement public programs with counseling and convenience, which helps sustain adherence between refill cycles. As digital tools spread, data sharing from connected meters informs follow-up decisions and improves test utilization. These dynamics support a steady advance in the Brazilian portion of the Latin America Self blood glucose monitoring market.

Mexico is projected to grow at a 5.09% CAGR to 2031 and benefits from dense retail pharmacy coverage that simplifies meter onboarding and strip refills. The country records a high adult diabetes prevalence profile, which indicates a large base for SMBG among non-insulin Type 2 patients and newly diagnosed adults. Retail counseling, in-store measurement stations, and multi-pack promotions help patients start testing routines soon after diagnosis. E-pharmacy options add convenience in major metros, while click-and-collect bridges last-mile gaps for secondary cities. These channels distribute demand widely while building brand familiarity for meters and strips that patients can operate confidently at home. That combination underpins Mexico’s growth leadership in the Latin America self blood glucose monitoring market.

Elsewhere in Latin America, large urban centers in Argentina, Chile, and Colombia show steady adoption tied to primary care integration and pharmacy counseling, while pilot programs validate digital support for SMBG in settings like Ecuador. Controlled cohorts that combine Bluetooth-enabled meters with app-based coaching have demonstrated clinically meaningful HbA1c reductions and fewer acute events, which supports plans for incremental expansion in public pathways. Procurement and pricing studies in the region document meaningful dispersion in device and strip prices, which influences channel selection and timing of household purchases. Together, these factors shape adoption curves outside the two largest markets and provide a path for the Latin America self blood glucose monitoring market to broaden over the forecast window.

Competitive Landscape

The Latin America self blood glucose monitoring market features a core group of multinational leaders alongside value-focused brands and private labels. Abbott, Roche, and LifeScan lead many retail shelves through strong distribution networks, clinic relationships, and support programs that reinforce brand familiarity. Product ecosystems that link meters, test strips, coaching apps, and data dashboards increase stickiness and improve refill predictability. Pharmacy partnerships that co-develop exclusive SKUs or bundle starter kits help align brand placement with loyalty programs. These measures build recurring strip volumes and defend share against lower-priced alternatives.

Companies continue to refine meter usability to reduce sampling errors and improve first-time success for new users. Features such as guided fill, larger displays, and reminders for control tests address common pain points during onboarding. E-pharmacy integrations that offer subscription refills and rapid delivery support consistency in testing routines. In parallel, clinic education and retail counseling strengthen confidence for at-home SMBG among newly diagnosed adults and parents managing pediatric cases. These service elements raise satisfaction and reduce returns tied to perceived inaccuracy or setup issues.

Competitive strategies also include selective localization to mitigate import frictions and to qualify for tariff benefits where feasible. Data connectivity that synchronizes SMBG logs with patient portals supports clinician review and creates new value props for provider networks. Vendors that align with public procurement requirements and provide robust post-market surveillance position well for tender stability. Across these fronts, incumbents leverage distribution, education, and digital tools to reinforce recurring test strip demand within the Latin America Self blood glucose monitoring market.

Latin America Self Blood Glucose Monitoring Industry Leaders

Abbott Laboratories

Ascensia Diabetes Care

F. Hoffmann-La Roche AG

LifeScan IP Holdings, LLC

Trividia Health, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The Goiânia Municipal Health Secretariat in Brazil issued Ordinance 227/2026, updating the Municipal Program for Dispensing Supplies for Diabetes Mellitus. Key updates include increasing monthly test-strip quotas to 400 units for high-need patients, introducing Pharmaceutical Care Cards for treatment monitoring, extending glucometer access to women with gestational diabetes, and benefiting approximately 7,500 individuals across various health units.

- June 2025: Argentina's Ministry of Health issued Resolution 2091/2025, updating standards for diabetes care and introducing a new accreditation certificate valid for the chronic condition. The resolution integrates Diabetological Education Programs for Self-Management into the Mandatory Medical Benefits System with mandatory 100-percent coverage by national social security, prepaid entities, PAMI, judicial funds, armed forces, and university schemes.

- February 2025: Brazilian Deputy Renata Nicodemos introduced Bill PL 323/2025 to mandate free intermittent glucose monitoring devices for diabetics under SUS. Diabetes prevalence in Brazil rose from 9.1 percent in 2021 to 10.2 percent in 2023. Nicodemos highlighted painless, non-invasive technologies to improve disease control, prevent complications, and enhance patient quality of life.

Latin America Self Blood Glucose Monitoring Market Report Scope

As per the report's scope, self-monitoring of blood glucose is an approach used by diabetic patients/caregivers to measure blood glucose level using a glucometer, test strips, and lancets. Based on the readings, patients can adjust or check the effect of their treatment.

| Glucometer Devices |

| Test Strips |

| Lancets |

| Type-1 Diabetes |

| Type-2 Diabetes |

| Gestational Diabetes & Others |

| B2B |

| Retail Pharmacies |

| Online Pharmacies |

| Other Channels |

| Homecare Settings |

| Hospitals |

| Clinics & Diagnostic Centers |

| Mexico |

| Brazil |

| Argentina |

| Rest of Latin America |

| By Component | Glucometer Devices |

| Test Strips | |

| Lancets | |

| By Patient Type | Type-1 Diabetes |

| Type-2 Diabetes | |

| Gestational Diabetes & Others | |

| By Distribution Channel | B2B |

| Retail Pharmacies | |

| Online Pharmacies | |

| Other Channels | |

| By End-User | Homecare Settings |

| Hospitals | |

| Clinics & Diagnostic Centers | |

| By Country | Mexico |

| Brazil | |

| Argentina | |

| Rest of Latin America |

Key Questions Answered in the Report

What is the current size and growth outlook for the Latin America Self Blood Glucose Monitoring Market?

The Latin America self blood glucose monitoring market size is expected to increase from USD 600.23 million in 2025 to USD 627.51 million in 2026 and reach USD 783.62 million by 2031 at a 4.5% CAGR over 2026-2031.

Which segment holds the largest share in this market and why?

Test strips led with 82.95% in 2025 because recurring strip purchases sustain the core revenue cycle and are supported by meter–strip ecosystem lock-in that stabilizes brand adherence.

Which channels are growing the fastest for SMBG products in Latin America?

Online pharmacies are projected to grow at 8.85% CAGR through 2031 as subscriptions, delivery speed, and click-and-collect improve refill consistency and convenience for patients.

Which patient group contributes most to demand today?

Type 2 diabetes accounted for 88.35% of 2025 demand, and routine SMBG during dose titration and behavior change supports steady strip consumption in this broad cohort.

Page last updated on: