Neoprene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

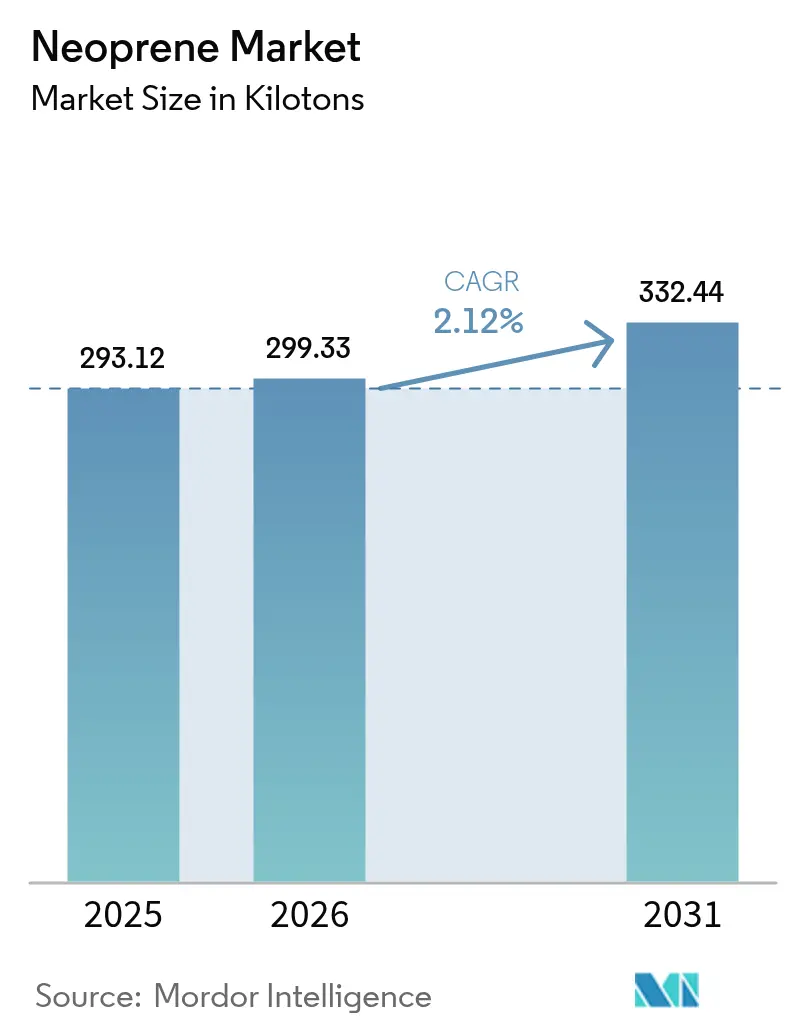

| Market Volume (2026) | 299.33 kilotons |

| Market Volume (2031) | 332.44 kilotons |

| Growth Rate (2026 - 2031) | 2.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neoprene Market Analysis by Mordor Intelligence

The Neoprene Market size is projected to expand from 293.12 kilotons in 2025 and 299.33 kilotons in 2026 to 332.44 kilotons by 2031, registering a CAGR of 2.12% between 2026 to 2031. This trajectory illustrates a maturing synthetic-elastomer segment where capacity discipline outweighs volume ambition. The neoprene market is anchored by Asia-Pacific’s wire-harness and gasket demand, but producers in Japan and China are pivoting toward specialty grades that command margin premiums over commodity polychloroprene, especially in heat-aging and flame-retardant applications.Rising electrification, infrastructure spending, and increasingly stringent VOC and carcinogenic-exposure regulations continue to shape product development, capital allocations, and geographic sourcing strategies in the neoprene market. Competitive intensity has sharpened as incumbents restructure capacity, while niche players exploit white space in water-borne latexes and precrosslinked grades that bypass on-site vulcanization constraints. Headline risks include crude-oil and acetylene volatility inflating chloroprene-monomer costs, plus EU Carc.1B reclassification that may accelerate polymerization offshoring and tighten supply chains in the neoprene market.

Key Report Takeaways

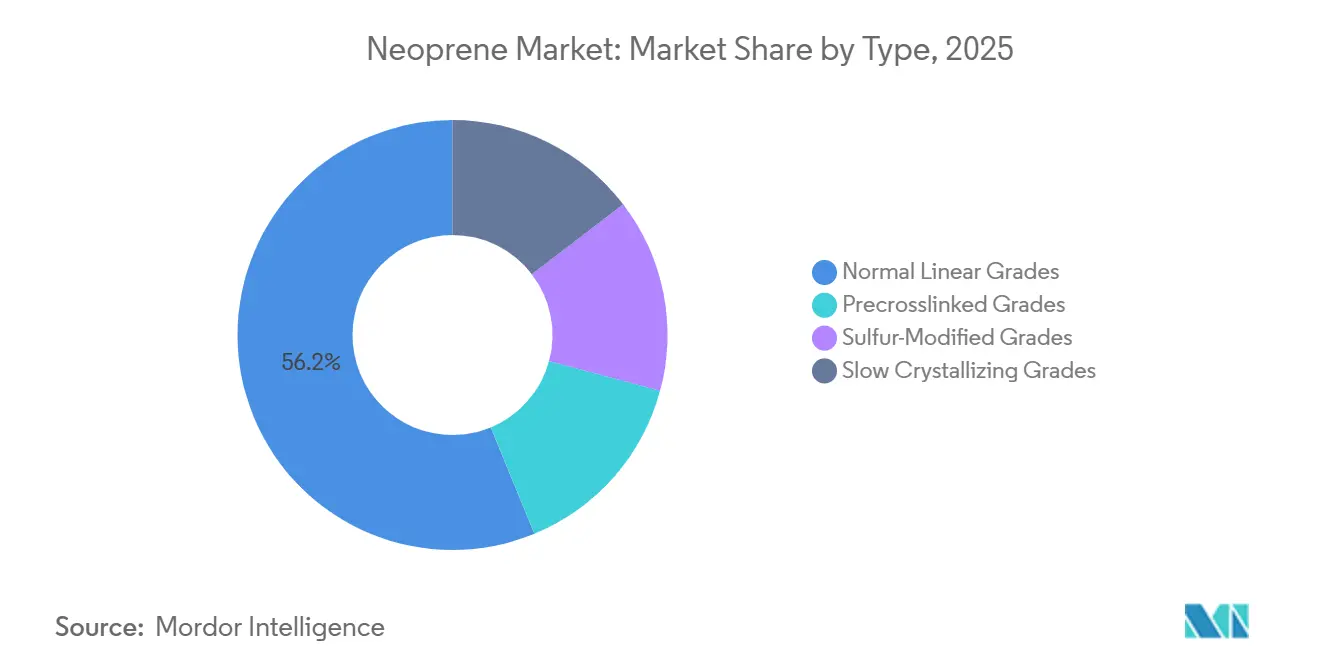

- By type, normal linear grades led with 56.22% of 2025 volume, while sulfur-modified grades are forecast to expand at a 2.64% CAGR through 2031.

- By application, elastomers captured 59.48% of the 2025 volume; adhesives, however, are expected to grow at a 2.44% CAGR to 2031.

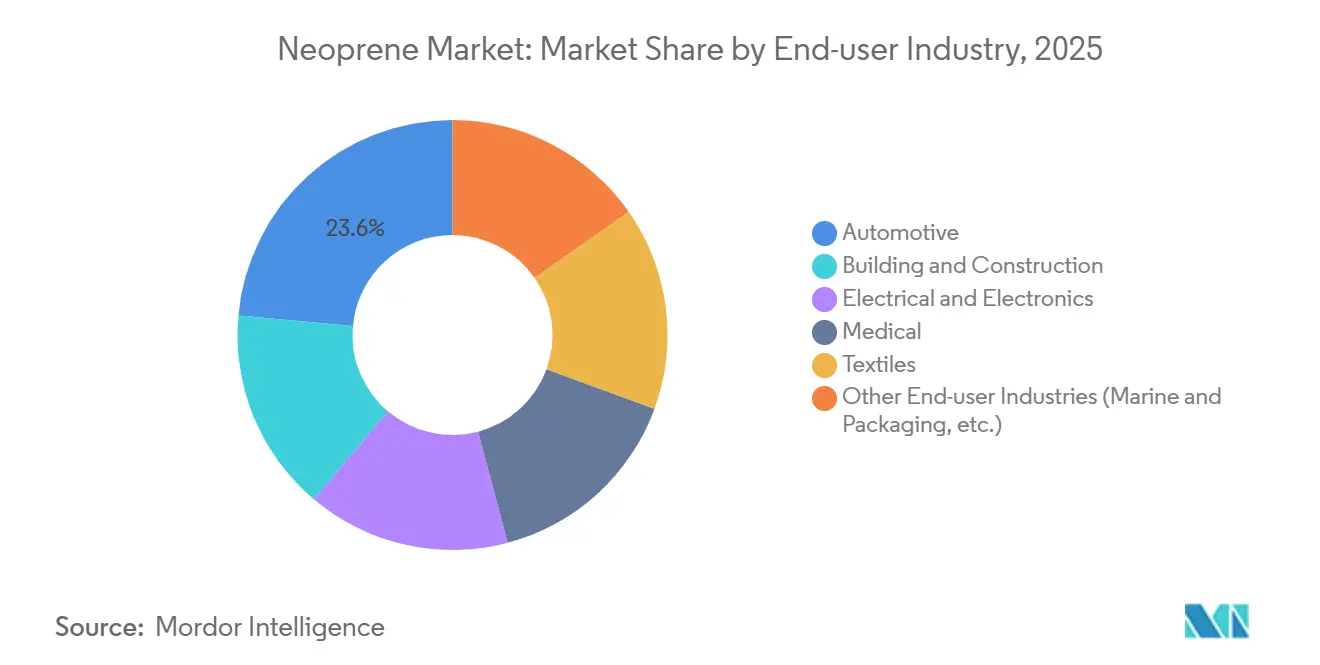

- By end-user industry, automotive captured 23.56% of 2025 volume, while electrical and electronics is expected to grow at a 2.46% CAGR to 2031.

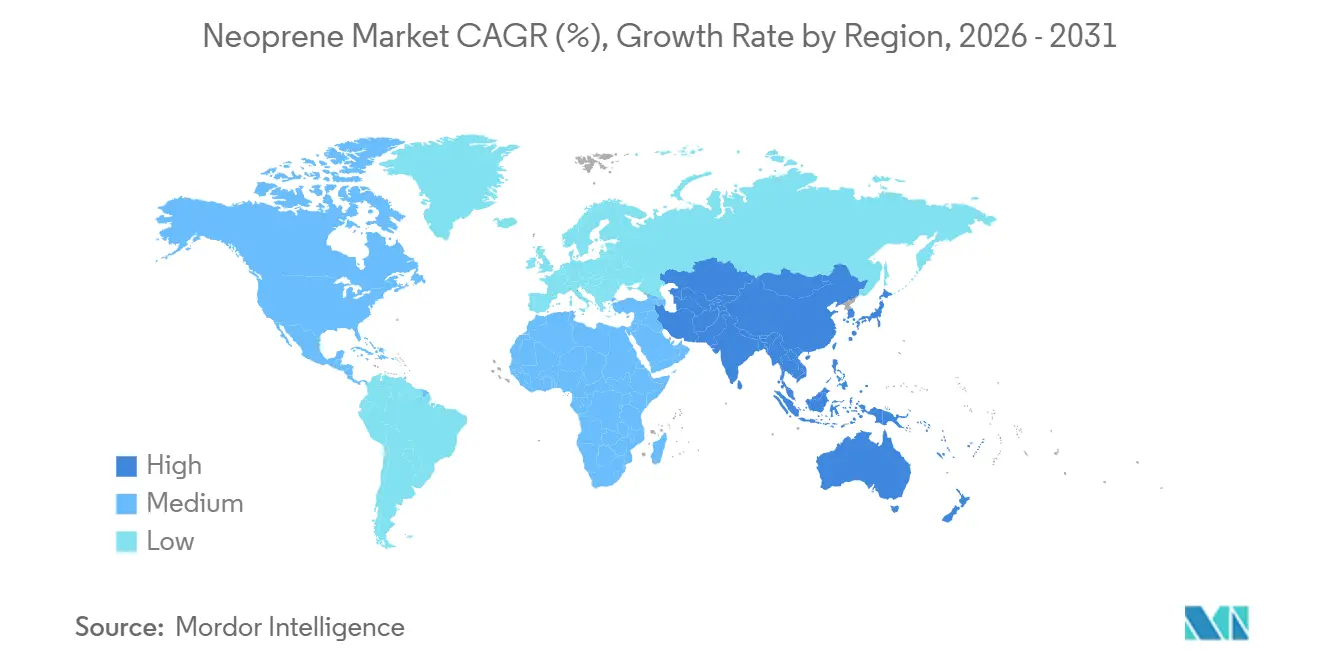

- By geography, Asia-Pacific held 61.57% of the 2025 demand and is advancing at a 2.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neoprene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-led construction boom in Asia-Pacific | +0.5% | Asia-Pacific core, spill-over to Middle-East | Medium term (2-4 years) |

| Electrification drives heat-resistant wire and cable sheathing | +0.4% | Global, with concentration in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Sports, medical and dive-wear adoption surge | +0.3% | North America, Europe, APAC coastal markets | Short term (≤ 2 years) |

| EV battery-pack flame-barrier gaskets demand | +0.3% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Shift toward solvent-free water-borne neoprene dispersion | +0.2% | North America and EU (regulatory-driven), Asia-Pacific adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Led Construction Boom in Asia-Pacific

Government-funded metro-rail and bridge programs in China, India, and ASEAN specify neoprene bearings that absorb seismic and thermal loads, underpinning a sustained demand baseline in the neoprene market[1]Ministry of Finance India, “National Infrastructure Pipeline Update,” mof.gov.in . China’s Belt and Road Initiative extends that pull into Central Asia, while precrosslinked grades that cure at ambient temperature reduce field labor and project delays. Seismic building codes in Indonesia and the Philippines are an under-reported catalyst because they mandate elastomeric isolation systems that favor neoprene’s ozone resistance. Capacity expansions, such as Tosoh’s 22,000 tpa project slated for 2030, are timed to capture these long-cycle infrastructure orders.

Electrification Drives Heat-Resistant Wire and Cable Sheathing

Renewable-energy interconnects and data-center expansions require cable jackets that retain flexibility at –65 °C and withstand 90 °C-plus service, keeping neoprene entrenched in low-voltage control cables despite cross-linked polyethylene’s rise in high-voltage lines. Offshore wind farms adopt neoprene-sheathed cables for salt-spray resistance, while IEC 60502 and UL 44 standards cement its position by mandating flame-propagation limits that commodity PVC cannot meet. Military-grade heat-shrink tubing specifications cascade into commercial installations, driving incremental premium demand in the neoprene market.

Sports, Medical and Dive-Wear Adoption Surge

Recreational diving and triathlon participation sustain foam-grade consumption because 5 mm neoprene wetsuits maintain core temperature 2.5 °C higher than TPE counterparts after one hour in 15 °C water, a measurable performance gap valued by athletes. Hospitals specify hypoallergenic neoprene braces that survive 50 kGy gamma sterilization, widening the medical footprint of the neoprene market. Smooth-skin silicone-coated neoprene fetches 30%–50% premiums, signaling a pivot toward differentiated consumer gear that supports margin expansion.

EV Battery-Pack Flame-Barrier Gaskets Demand

Thermal-runaway mitigation drives OEMs to specify UL94-V0 gaskets with compression-set ≤25% at 100 °C; sulfur-modified grades deliver this profile at cost points acceptable for sub-USD 30,000 EV segments. Competing silicone foams boast higher continuous-use temperatures (≥120 °C), but neoprene holds share where price sensitivity prevails, keeping the neoprene market relevant across diverse EV tiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil and acetylene price volatility inflating monomer cost | -0.3% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Stricter VOC limits on solvent-borne neoprene adhesives | -0.2% | North America and EU (regulatory-driven) | Medium term (2-4 years) |

| EU reclassification of chloroprene as Carc.1B limiting workplace exposure | -0.2% | Europe, potential spill-over to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil and Acetylene Price Volatility Inflating Monomer Cost

Japan spot chloroprene prices climbed to USD 7,000–7,200 / t in June 2025 after energy-policy shifts constrained Chinese calcium-carbide output, squeezing converters already operating on thin margins. Sustained volatility incentivizes backward integration among large compounders, yet small toll mixers risk exit, tightening liquidity in the neoprene market.

Stricter VOC Limits on Solvent-Borne Neoprene Adhesives

Water-borne neoprene latex requires stainless-steel mixing equipment costing USD 50,000–150,000 per line, a capital burden that threatens smaller converters, potentially pruning downstream demand in the neoprene market size[2]Maryland Department of the Environment, “2024 Architectural Coatings Rule,” mde.maryland.gov .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Sulfur-Modified Grades Gain Heat-Aging Edge

Normal linear grades commanded 56.22% of 2025 volume in the neoprene market share, driven by their 14 MPa tensile strength and 600%-plus elongation that satisfy general-purpose belts and gaskets. Sulfur-modified grades are projected to post a 2.64% CAGR, supported by Denka’s US9475895B2 polymer that retains 58%–67% elongation after 500 h at 100 °C.

Performance metrics rather than viscosity now drive type selection. ISO 37 tensile and ASTM D395 compression-set results are procurement gatekeepers, favoring producers with lab capabilities to tailor sulfur and accelerator packages to rising thermal profiles in EVs and renewables-sector cabling.

By Application: Adhesives Outpace Elastomers on VOC Compliance

Elastomers held 59.48% of 2025 volume; however, adhesives will outgrow at 2.44% CAGR, reflecting regulatory-driven migration to low-VOC systems. Water-borne latexes reach 60% solids and achieve green strength in 10 minutes at 23 °C, matching solvent tack but requiring longer open times that necessitate process re-engineering on high-speed laminating lines. Hybrid neoprene-acrylic dispersions now dominate automotive interior lamination, demonstrating how compliance can yield price premiums.

Latex foam cores for wetsuits and carpet underlay retain demand yet face competition from nitrile and natural rubber in cost-sensitive gloves. The neoprene market continues to diversify by blending with acrylics or polyurethanes to improve wet tack and freeze-thaw stability, a key purchasing criterion for Tier-1 automotive suppliers.

By End-user Industry: Electrical and Electronics Lead Growth

Automotive consumed 23.56% of 2025 demand, but lightweighting and TPE substitution temper growth. Electrical and Electronics will register a 2.46% CAGR through 2031, buoyed by renewable-energy interconnects and data-center cable harnesses that require UL94-V0 jackets and -65 °C flexibility. Building and Construction application of neoprene in expansion joints enjoys steady uptake across India’s USD 1.4 trillion infrastructure pipeline. Medical, textiles, and miscellaneous industrial uses round out demand, collectively benefiting from neoprene’s radiation tolerance and thermal insulation.

Geography Analysis

Asia-Pacific leads the neoprene market with 61.57% of 2025 volume and a forecast 2.12% CAGR to 2031. China’s listing of chloroprene as “Restricted” may slow new capacity, but domestic demand remains strong in wire harnesses and gaskets despite competitive pressure from EPDM. Japan’s TOSOH investment targets electrification-driven demand for heat-resistant grades, while India’s metro-rail and highway build-out escalates elastomeric bearing usage.

In North America, grid upgrades and data-center proliferation spur control-cable consumption, sustaining market growth despite flat vehicle output. EPA carcinogenicity classification raises compliance costs, nudging some polymerization offshore while lifting imports of finished polymer from Asia. Canada and Mexico contribute through automotive supply chains and oil-field requirements.

Europe’s share remains constrained as ECHA’s Carc. 1B path prompts compounders to source pre-polymerized grades, potentially elongating lead times and elevating costs. Wind-farm cabling and automotive sealing sustain baseline demand, but near-zero growth is forecast as silicone and EPDM capture incremental applications.

South America, and Middle-East and Africa collectively command single-digit volume shares. Brazil eyes backward integration via butadiene chlorination, while Saudi petrochemical diversification supports neoprene gaskets for energy infrastructure. However, import dependence and price sensitivity temper rapid expansion in these regions of the neoprene market.

Value Chain Analysis

Neoprene (polychloroprene) value creation starts upstream with petrochemical and carbide chains that shape chloroprene monomer economics, including acetylene/calcium-carbide routes and petroleum-derived streams (linked to naphtha cracking and 1,3-butadiene availability). Chloroprene monomer and polymerization capacity is concentrated among a small set of integrated producers, which increases supply-risk sensitivity to feedstock volatility and compliance-driven operating costs. The June 2025 spike in Japan spot chloroprene prices to about USD 7,000-7,200 per ton shows how upstream constraints can flow quickly into converter margins.

Midstream producers (including Denka, ARLANXEO, Tosoh, China National Bluestar, and Sundow) supply neoprene in multiple grades to compounders and formulators that tailor properties such as heat aging, flame retardancy, and compression set for elastomer parts and adhesives. Downstream, the chain runs through compounders, adhesive formulators (including water-borne dispersion lines requiring stainless-steel mixing), and fabricators/OEM-ODM manufacturers serving sports and industrial goods. Vertically integrated converters such as Sheico Group combine neoprene sheet making with finished-product fabrication, which reduces exposure to resin lead times. Distribution is handled via direct contracts and regional distributors to end users in automotive and electrical and electronics (wire and cable), construction (bearings and expansion joints), and consumer/medical products, where dual-sourcing and inventory buffers have gained importance after production footprint disruptions such as Denka Performance Elastomer operational suspension in the United States.

Competitive Landscape

ARLANXEO, Denka, Tosoh, China National Bluestar, and Sundow collectively control about 72% of global capacity, signaling moderate concentration in the neoprene market. Zeon’s plan to shutter 60% of Tokuyama capacity between 2026-2028 reflects margin pressure in commodity grades. ARLANXEO’s 5,000 tpa HNBR plant commissioning in 2026 reveals a strategic pivot toward higher-value nitrile-based elastomers. Denka leverages patent US9475895B2 to protect sulfur-modified products aimed at EV battery seals and high-temperature wire insulation.

Niche players such as Pidilite Industries and SEDO Chemicals capture regional adhesive shares through tailored water-borne dispersions, while advanced-materials firms like W. L. Gore introduce non-fluorinated composites that compete directly with neoprene in EV modules. Integrated producers with in-house monomer synthesis and closed-loop solvent recovery best withstand VOC regulations and feedstock spikes, preserving margins and share in the neoprene market.

Neoprene Industry Leaders

Denka Company Limited

ARLANXEO

Tosoh Corporation

China National Bluestar (Group) Co. Ltd.

Sundow Polymers Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Supply restructuring and compliance-driven product migration are creating defined pockets of whitespace across grades and applications. Denka's indefinite suspension of chloroprene rubber production at its U.S. subsidiary has already shifted shipments toward its Omi Plant in Japan, and Denka reported profitability improvement in its elastomers business for the fiscal year ended March 31, 2026 after removing higher-cost U.S. output. This supports converters that can qualify alternate supply and upgrade compounding and logistics to manage longer lead times, while also improving room for producers with resilient monomer access and efficient polymerization assets.

On the demand side, opportunities cluster in higher-specification elastomer and adhesive systems tied to electrification and VOC compliance. Water-borne neoprene dispersions are attracting attention as VOC limits tighten, although downstream retrofits such as stainless-steel mixing lines raise the entry bar for smaller adhesive makers, supporting consolidation and premiumization among capable formulators. In materials positioning, sustainability credentials are increasingly appearing in procurement conversations: ARLANXEO stated that its chloroprene rubber portfolio uses ISCC PLUS-certified chlorine (sourced from Covestro) as of January 2026, offering a pathway for differentiated offerings where customers screen for lower-footprint inputs. Capacity planning also points to where suppliers are placing long-cycle bets; Tosoh's announced investment of about 75 billion yen for a 22,000 tpa chloroprene rubber expansion at its Nanyo Complex (targeted for 2030 commercial operation) aligns with specialty-grade pull from wire and cable, industrial sealing, and infrastructure bearings that require consistent heat-aging and flame performance.

Recent Industry Developments

- June 2026: ARLANXEO announced that its chloroprene rubber production portfolio uses ISCC PLUS-certified chlorine sourced from Covestro, in effect for the full portfolio as of January 2026. The shift supports customer decarbonization and traceability requirements and raises the bar for comparable sustainability claims in neoprene supply chains.

- June 2025: Tosoh Corporation announced an approximately 75 billion yen investment to build additional chloroprene rubber capacity at its Nanyo Complex, targeting 22,000 metric tons per year and commercial operation in 2030. This expansion concentrates incremental supply at a high-efficiency Japanese site, reinforcing Asia-Pacific as the strategic production hub for neoprene grades used in cables, gaskets, and infrastructure bearings.

- May 2025: Denka Company Limited announced it would not restart chloroprene rubber production at its Denka Performance Elastomer facility in LaPlace, Louisiana for an indefinite period, citing rising costs, staffing challenges, and declining volumes. The decision tightened North America-local supply options and increased reliance on imports and alternative sourcing from producers with operating capacity outside the United States.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the neoprene market is defined as the commercial demand and supply of neoprene (polychloroprene) in primary forms that are sold for downstream use across industrial and consumer applications, counted as market revenue in USD.

Scope exclusions: We exclude finished products made from neoprene (such as wetsuits, gloves, belts, and gaskets) and count only the neoprene material sold into those value chains.

Segmentation Overview

- By Type

- Normal Linear Grades

- Precrosslinked Grades

- Sulfur-Modified Grades

- Slow Crystallizing Grades

- By Application

- Elastomers

- Latex

- Adhesives

- By End-user Industry

- Automotive

- Building and Construction

- Electrical and Electronics

- Medical

- Textiles

- Other End-user Industries (Marine and Packaging, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDIC Countries

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public data that helps anchor realistic demand pools, supply capacity, and trade movements for chloroprene based elastomers. We used sources such as UN Comtrade for trade flows, USITC DataWeb for import and tariff context, the USGS for broader chemical and materials indicators, and U.S. EPA resources for regulatory signals that can affect plant operations and product substitution.

To connect market demand to end use realities, we also reviewed public company annual reports and presentations, trade association publications for rubber and polymers, and peer reviewed chemistry and materials journals that discuss neoprene performance and formulation trends. In parallel, we referenced paid subscriptions that support company financials and intelligence, patent landscaping, and shipment level trade checks, which helped us avoid over relying on any one public series. The desk research sources listed here are illustrative only, and many other public references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test the desk assumptions on what gets counted as neoprene revenue, how pricing is negotiated, and how quickly demand shifts by application when regulations or feedstock costs change. We spoke with a mix of producers, distributors, compounders, and large buyers, with coverage intended to reflect key consuming regions and resulting differences in product grade mix and import dependence. Where secondary data was thin, these inputs were used to triangulate utilization, trade reliance, and typical price bands before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 52% |

| Mid tier: 48% | Functional/Unit leaders: 43% | EMEA: 30% |

| Smaller Players: 21% | Managers: 44% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach that reconstructs neoprene consumption from visible demand drivers and supply signals, and then reconciles the totals against observed trade and operating patterns. Country level demand was inferred from indicators such as downstream production trends in automotive and industrial components, rubber goods output signals, net import versus export balance for relevant codes, and observed shifts in application mix (for example, adhesive and latex uses versus solid rubber uses).

After that initial view, selective bottom-up approximations were used as reasonableness checks, including sampled supplier revenue disclosures where available, channel checks on typical contract pricing behavior, and volume times ASP calculations for a limited set of high visibility trade lanes. When gaps appeared, the residual demand was allocated to the most consistent end use buckets based on interview feedback and regional production footprints, and then validated that the implied pricing stayed within realistic bands.

For forecasting, we relied on scenario analysis supported by simple time series smoothing on the main drivers, since neoprene demand tends to move steadily unless disrupted by feedstock swings or regulatory actions. The forward view was informed by expert perspectives on capacity discipline, substitution pressure from other elastomers, and the expected pace of industrial output and vehicle production, and then it was rolled up to a single global market value.

Data Validation & Update Cycle

Model outputs were cross checked against independent signals like import dependence by region, implied capacity utilization ranges, and whether the pricing trend required to hit the total looked realistic for the year. When a country level number looked too high or too low, we rechecked the trade balance logic, the end use weights, and then reached back to experts when the variance could not be explained with public data alone.

Before sign off, the work goes through multi step reviews where assumptions are checked for consistency across regions and across years, and unusual jumps are challenged until a clear driver is documented. Reports are refreshed annually, and interim updates are made when a material event occurs, such as a major capacity change, trade disruption, or regulation affecting production. Right before delivery, the latest public updates are scanned again so clients receive a current view.

Mordor Intelligence's Neoprene Market Size Compared Against Other Published Estimates

Published market sizes for neoprene often do not match because the underlying counting rules are not the same, even when the topic name looks identical. Differences usually come from what is treated as the market product, whether finished neoprene goods are mixed in with material sales, and how pricing is converted and averaged across regions.

The biggest gaps typically show up in scope and price logic, where some estimates blend neoprene sheets and end products into one revenue pool, or they use a single global ASP that does not reflect the different grade mix and import reliance by region. Another driver is timing, since some publishers report 2024 value as a base while others quote 2025, and the currency conversion month and assumed price progression can move the total by a noticeable amount. This is why the value here stays tied to material level sales only and is refreshed using application mix and trade signals, a choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.12 B (2025) | |

| Global Consultancy A | USD 2.14 B (2024) | Uses a 2024 base and a broader application framing that can pull in higher value downstream forms, and the year shift also changes the price averaging and currency timing versus a 2025 view. |

| Regional Consultancy B | USD 2.07 B (2024) | Leans on a conservative 2024 pricing baseline and narrower captured demand signals, which can undercount regions where imports and specialty grades lift realized ASPs. |

Across the three values, most of the spread is explained by whether the estimate stays at neoprene material revenue or blends in parts of the finished goods chain, followed by base year selection and price conversion choices. By keeping the steps traceable to demand drivers, trade balance checks, and interview backed pricing behavior, the final number remains practical to reproduce and easier to update when market conditions change.

Key Questions Answered in the Report

What is the projected volume of the neoprene market in 2031?

The neoprene market is forecast to reach 332.44 kilotons by 2031.

Which grade is expected to grow fastest to 2031?

Sulfur-Modified Grades, driven by EV heat-aging requirements, are set to expand at 2.64% CAGR.

How will VOC regulations influence neoprene-based adhesives?

Limits such as Maryland’s 750 g/L cap are accelerating a shift to water-borne dispersions, lifting adhesive demand at 2.44% CAGR through 2031.

Why does Asia-Pacific dominate global neoprene demand?

The region hosts automotive, cable, and construction hubs that together accounted for 61.57% of 2025 volume.

Page last updated on: