Natural Vanillin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

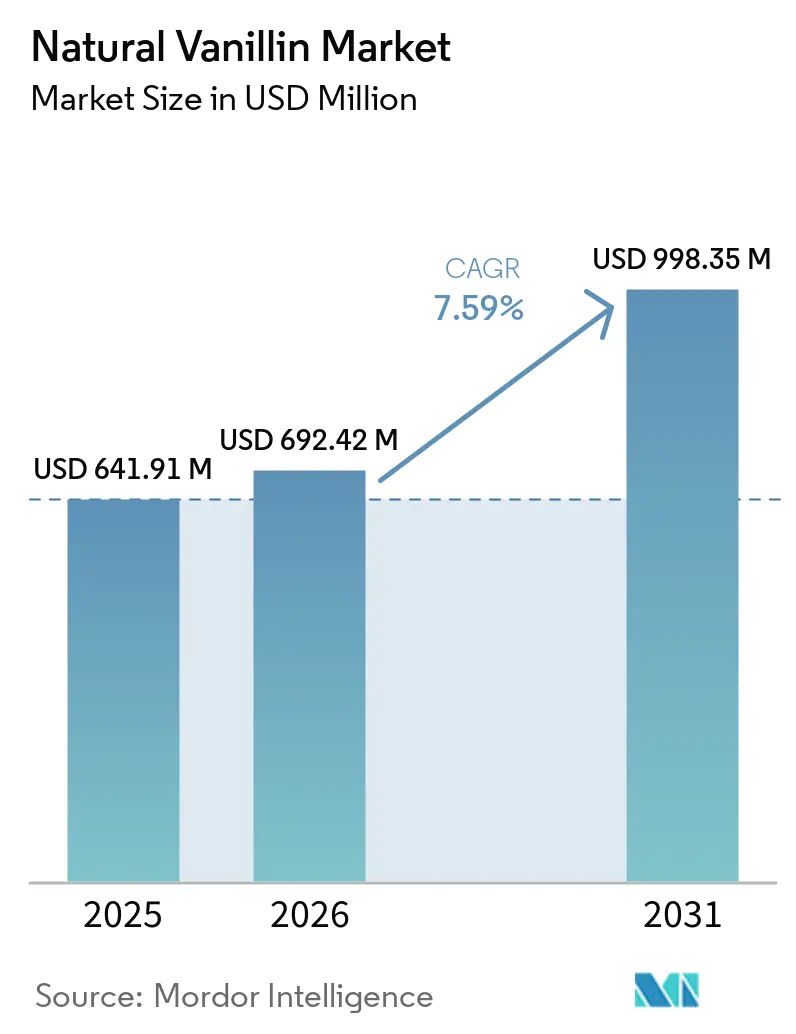

| Market Size (2026) | USD 692.42 Million |

| Market Size (2031) | USD 998.35 Million |

| Growth Rate (2026 - 2031) | 7.59% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Natural Vanillin Market Analysis by Mordor Intelligence

The natural vanillin market size is projected to expand from USD 641.9 million in 2025 and USD 692.4 million in 2026 to USD 998.4 million by 2031, registering a CAGR of 7.6% between 2026 and 2031. This market growth is bolstered by a consistent shift in food, personal care, and pharmaceutical sectors. Manufacturers are increasingly favoring natural ingredients over petrochemical ones, aligning with major regulatory systems' natural label claims. Additionally, a pivotal June 2025 decision by the European Commission imposed a hefty 131.1% anti-dumping duty on vanillin imports from China. This move not only diminished the price edge of synthetic vanillin in a key food manufacturing hub but also bolstered the market position of bio-based vanillin alternatives. As buyers prioritize consistent product launches across diverse applications, factors like fermentation purity, traceability, and supply stability have gained prominence, rivaling scale in importance. While premium confectionery, high-end fragrances, and the clean beauty sector emerge as primary revenue sources, challenges like cost pressures and raw material volatility hinder broader acceptance in mainstream products. Thus, the natural vanillin market is navigating a landscape shaped by regulatory shifts, a push for cleaner labeling, and advancements in fermentation economics, all while contending with the cost advantages of synthetic vanillin in bulk categories.

Key Report Takeaways

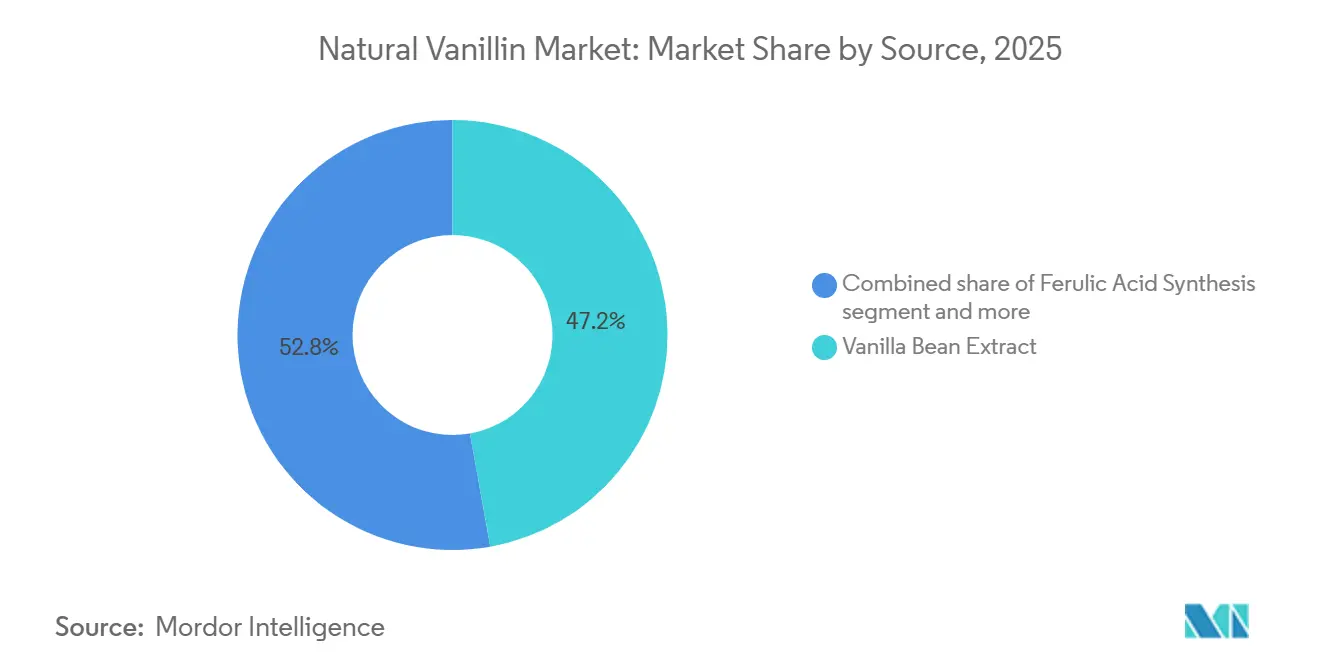

- By source, Vanilla Bean Extract accounted for the largest share of the natural vanillin market, at 46.71% in 2025, while Ferulic Acid Synthesis is projected to grow at the fastest CAGR of 9.96% during 2026-2031.

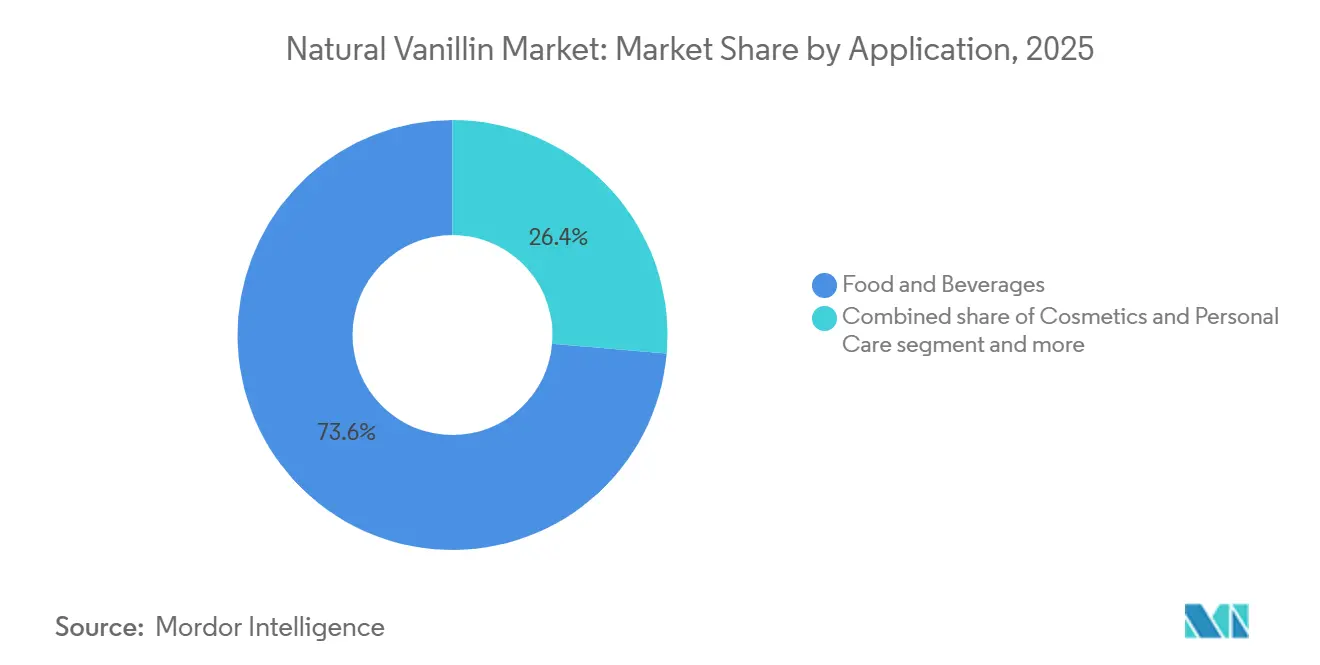

- By application, Food and Beverages accounted for the largest share of the natural vanillin market, at 73.62% in 2025, while Cosmetics and Personal Care is projected to grow at the fastest CAGR of 9.11% during 2026-2031.

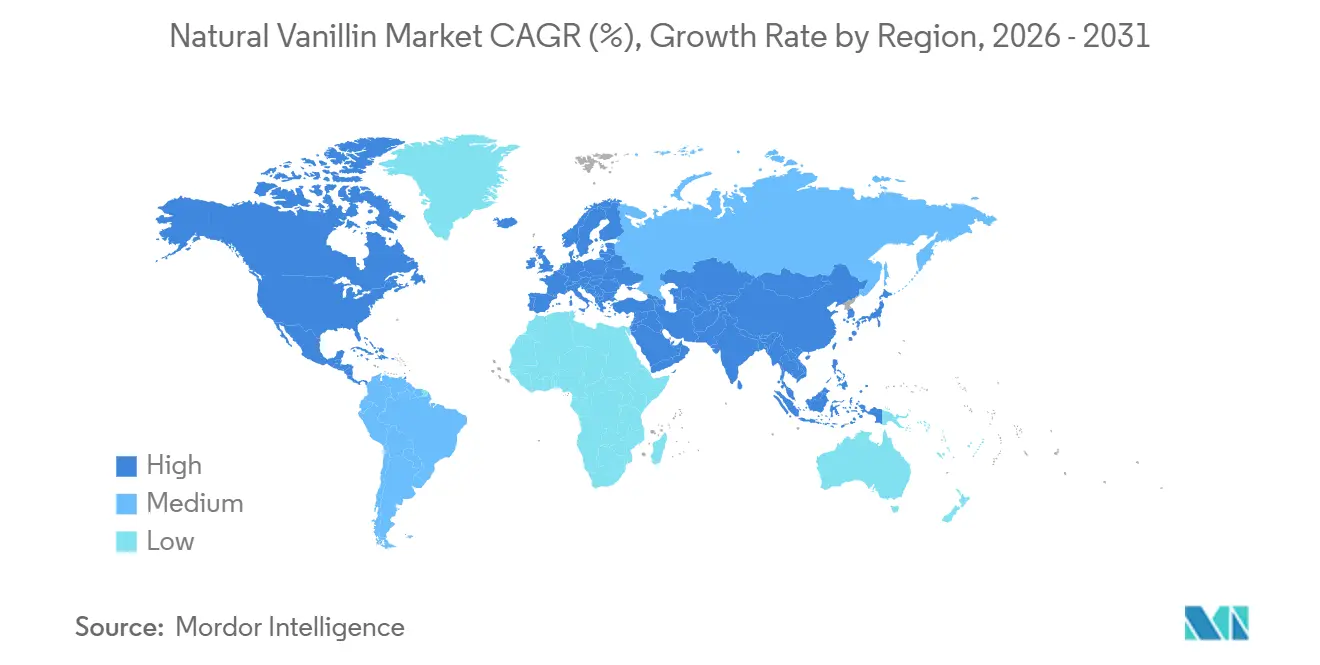

- By geography, Europe accounted for the largest share of the natural vanillin market, at 36.40% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 9.98% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Natural Vanillin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Clean-Label and Natural Ingredient Demand | +2.5% | Global | Short term (≤ 2 years) |

| Regulatory Restrictions on Artificial Ingredients | +1.2% | Europe, North America, and Asia-Pacific core | Medium term (2–4 years) |

| Growth in Premium Food, Beverage, and Fine Fragrance Formulations | +1.1% | Europe, North America | Medium term (2–4 years) |

| Sustainability Advantages of Bio-Based Vanillin Production | +0.9% | Global, early gains in Europe | Long term (≥ 4 years) |

| Advancements in Fermentation-Based Vanillin Production Technologies | +0.8% | Global | Medium term (2–4 years) |

| Increasing Adoption in Premium Confectionery and Chocolate Products | +0.7% | Europe, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising clean-label and natural ingredient demand

Leading food and personal care companies now view clean-label positioning as a standard procurement requirement, moving away from its previous status as a premium brand differentiator. Under EU Regulation (EC) No 1334/2008 and FDA 21 CFR 101.22(a)(3), vanillin, whether sourced from vanilla beans or produced through bio-fermentation, qualifies as a "natural flavoring"[1]Source: European Parliament and Council, “Regulation (EC) No 1334/2008 on Flavourings,” EUR-Lex, eur-lex.europa.eu. This classification allows for product label enhancements at a fraction of the cost of procuring full vanilla extract. In March 2026, Lallemand Bio-Ingredients highlighted a surge in global food and beverage launches featuring vanilla from 2023 to 2025[2]Source: Lallemand Bio-Ingredients, “Hevani Commercial Launch,” Lallemand, lallemand.com. This trend, evident in the bakery, dairy, confectionery, and chocolate sectors, points to a significant reformulation movement. The often-overlooked commercial insight is that shifting from synthetic to natural vanillin not only ensures label compliance but also empowers confectionery and dairy producers to command a higher retail price. This price premium helps bridge the gap in ingredient costs, presenting a compelling case for procurement teams. Furthermore, the demand for natural vanillin's clean-label appeal is gaining momentum in the cosmetics and personal care sectors. Here, younger consumers prioritize ingredient transparency, equating it with product performance in their purchasing decisions.

Regulatory restrictions on artificial ingredients

In the vanillin market, the distinction between natural and synthetic sources carries significant commercial weight. According to EU Regulation (EC) No 1334/2008, natural flavoring substances must be derived solely through physical, enzymatic, or microbiological methods from vegetable, animal, or microbiological sources. This definition effectively bars guaiacol-based synthetic vanillin from being labeled as "natural" in European markets. Further tightening the screws, on June 12, 2025, the European Commission slapped a hefty 131.1% anti-dumping duty on vanillin imports from China, citing unfair pricing practices that harmed EU producers. This move not only narrows the cost disparity between synthetic and naturally-certified vanillin in the EU's food manufacturing sector but also boosts the appeal of bio-based alternatives, especially for formulations that traditionally relied on Chinese synthetic supplies. Additionally, Asian manufacturers supplying to European food processors now grapple with heightened costs due to the duties on Chinese imports. This inflationary pressure nudges them towards sourcing naturally certified vanillin, aligning with the EU's regulatory framework.

Advancements in fermentation-based vanillin production technologies

Precision fermentation is revolutionizing bio-based vanillin production, with yeast and bacterial systems now achieving commercial purity levels of 98% or higher. Researchers from Waseda University have made strides in this field, showcasing a single-step conversion of ferulic acid to vanillin using a coenzyme-independent dioxygenase[3]Source: Waseda University, “Research on Ferulic Acid to Vanillin Conversion,” Waseda University, waseda.jp. This method offers a significant throughput advantage over the previously dominant multi-step enzymatic pathways, which had constrained industrial scalability. In a study published in Biomass Conversion and Biorefinery (February 2025), Nisar et al. highlighted the synthesis of vanillin through solid-state fermentation. They utilized corn cob biomass and Bacillus cereus PP068302, broadening the feedstock options beyond just rice bran and highlighting the potential of various agricultural byproducts as vanillin precursors. This shift has notable implications for ingredient supply chains: producers using fermentation can now operate independently of vanilla bean harvest cycles. This independence ensures a consistent year-round supply and stable costs, a feat traditional extract-dependent chains struggle to achieve. Lallemand's Hevani, crafted on Evolva's yeast fermentation platform (acquired in 2024), underscores the power of biotechnology. It showcases how new market players can rival established flavor houses, achieving natural credential equivalency without the need for traditional extraction infrastructures.

Sustainability advantages of bio-based vanillin production

Production routes for bio-based vanillin, sourced from wood pulp, rice bran, and sugar fermentation, are now being assessed using verified sustainability metrics, moving beyond mere qualitative "natural" assertions. In April 2026, Borregaard highlighted in its investor presentation that its wood-based EuroVanillin boasts a carbon footprint reduction exceeding 90% when juxtaposed with guaiacol vanillin, which is derived from crude oil. This disclosure stands out as one of the rare lifecycle carbon assessments, validated through direct company reporting in the vanillin sector. Borregaard's Sarpsborg biorefinery, utilizing 100% PEFC-certified Norway Spruce, proudly offers the market's sole PEFC-certified commercial vanillin. Meanwhile, routes producing ferulic acid vanillin, tapping into rice bran oil processing residues as feedstock, exemplify circular economy principles. By transforming low-value agricultural byproducts into premium flavor molecules, they resonate with the EU Green Deal's procurement incentives, which champion bio-based feedstock sourcing in food ingredient supply chains. Furthermore, as life cycle assessment documentation gains traction, it's becoming a staple in the supplier qualification processes of major consumer goods firms, shifting sustainability from a mere marketing narrative to a tangible procurement edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Significantly Higher Cost Compared to Synthetic Vanillin | -1.3% | Global, most pronounced in Asia-Pacific and South America | Medium term (2–4 years) |

| Volatility in the Supply of Natural Raw Materials | -0.8% | Global, primarily vanilla bean-dependent producers | Short term (≤ 2 years) |

| Stringent Regulatory Definitions for "Natural" Claims | -0.5% | Europe, North America | Medium term (2–4 years) |

| Flavor Consistency Challenges Across Natural Sources | -0.4% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Significantly higher cost compared to synthetic vanillin

Mass-market adoption of natural vanillin faces a significant hurdle: its cost compared to synthetic alternatives. According to a position paper by GDCh (Gesellschaft Deutscher Chemiker), natural vanillin sourced from vanilla beans is priced at 500 to 1,000 times more than its chemically synthesized counterparts. Furthermore, "natural" vanillin produced through fermentation commands a price that's roughly 10 times higher than the guaiacol-based synthetic versions. This pronounced cost disparity limits the use of natural vanillin to premium product tiers, such as artisanal chocolates, luxury personal care items, and high-end beverage formulations. In contrast, mainstream bakery and beverage producers predominantly opt for synthetic grades. This situation poses a structural risk: mid-market brand owners, already squeezed by inflationary pressures on various costs, are likely to postpone their clean-label reformulation efforts unless the cost gap narrows through increased production scale. Notable efforts to bridge this premium include Borregaard's ~NOK 800 million debottlenecking project in Sarpsborg and Lallemand's ramp-up in commercial fermentation. However, achieving full cost parity with synthetic production remains a distant goal rather than an immediate reality.

Volatility in the supply of natural raw materials

Manufacturers relying on vanilla bean extract for natural vanillin face formulation planning risks and price instability due to supply disruptions in vanilla bean production. With Madagascar supplying about 80% of the world's vanilla beans, the country faces heightened risks from cyclone damage, political instability, and speculative inventory behaviors by traders. Aust&Hachmann's December 2025 report projected Madagascar's 2025 vanilla crop at 2,500–3,500 metric tons. This could lead to a global oversupply, with unsold vanilla potentially surpassing 6,000 metric tons, while annual demand hovers between 2,500 and 3,000 metric tons. Such an oversupply results in pricing instability: falling bean prices shrink revenues for producers, yet a sudden policy shift or cyclone can spike prices within the same season. The Sustainable Vanilla Initiative highlighted in their 2025 booklet that newly imposed US tariffs in 2025 further exacerbated the volatility in Madagascar's already cyclical price market. In this landscape, fermentation-based producers gain a significant edge, as their detachment from agricultural cycles becomes a selling point, increasingly valued by flavor procurement teams, even at a premium cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Fermentation Economics Reshaping the Production Hierarchy

In 2025, Vanilla Bean Extract held a 46.71% share of the natural vanillin market, maintaining its status as the benchmark for flavor quality and origin. Its presence in luxury confectionery, high-end fragrances, and premium dairy products remains strong. EU and US labeling laws, which reserve terms like "vanilla flavor" and "natural vanilla flavoring" for bean-derived ingredients, create a regulatory niche that fermentation alternatives cannot replace. However, this segment faces constraints due to reliance on Madagascar for supply and a cost structure limiting its use to premium applications. Eugenol Synthesis, which converts eugenol from clove oil through oxidative microbial methods, occupies a mid-tier position. It is preferred in pharmaceuticals for its consistent high purity and in fine fragrances for its unique aromatic profiles.

Ferulic Acid Synthesis is the fastest-growing source, with a 9.96% CAGR from 2026 to 2031. This growth is driven by its scalability, agricultural feedstock availability, and recognition as a natural label under EU Regulation (EC) No 1334/2008 and FDA 21 CFR 101.22(a)(3). A 2024 review in ScienceDirect's Biochemical Engineering Journal highlighted ferulic acid's viability as a natural vanillin precursor due to its abundance in cereal crops and proven bioconversion yields. Rice bran oil processing residues, widely available in China, India, Thailand, and Indonesia, provide a cost-effective feedstock, positioning ferulic acid vanillin production within the Asia-Pacific's rice processing economies. French fermentation leader Ennolys produces Ennallin natural vanillin from rice bran oil using bioconversion fermentation, achieving over 99% purity and full EU and US natural status. Other Sources, such as lignin depolymerization and extraction from vanilla-adjacent botanicals, remain smaller but hold strategic importance in Scandinavian biorefineries, where wood-based co-production offers competitive production economics.

By Application: Premium Food Traction Masks a Faster Personal Care Expansion

In 2025, the Food and Beverages sector is set to command a dominant 73.62% share of the natural vanillin market, driven by its integration in Bakery and Confectionery, Dairy, and Beverage formulations. The Bakery and Confectionery segment leads consumption, with premium chocolate producers paying a 15–25% premium for natural vanillin due to its superior flavor complexity and clean-label appeal. Dairy and Frozen Desserts benefit from the plant-based reformulation trend, where natural flavors are standard in new launches like yogurt, oat-based ice cream, and protein beverages. The Beverage sector is expanding with vanilla-flavored ready-to-drink coffee, energy drinks, and premium protein shakes. In Pharmaceuticals, natural vanillin serves as a taste-masking agent in pediatric syrups and oral solid dosages, with its "natural" label reducing resistance from additive-sensitive patients.

Cosmetics and Personal Care is the fastest-growing sector, projected to grow at a 9.11% CAGR from 2026 to 2031. Vanillin's warm, gourmand scent and natural origin make it a key base note in clean beauty fragrances and sustainable perfumes targeting younger consumers. Lallemand's March 2026 Hevani launch highlighted its dual use in food flavors and cosmetic fragrances in the EU and US, meeting International Fragrance Association (IFRA) standards without GMO declaration. This dual regulatory advantage simplifies strategies for personal care brands operating across both markets. The Fragrances segment, distinct from personal care, remains vital in fine perfumery, where Vanilla Bean Extract commands a premium, and in household fragrances, where fermentation-derived alternatives offer natural-label appeal at competitive prices.

Geography Analysis

In 2025, Europe commanded a dominant 36.40% share of the natural vanillin market, bolstered by robust premium demand, clear regulatory frameworks, and strong local production capabilities. The EU's Regulation (EC) No 1334/2008, which bestows a clear commercial value to natural flavor status, aids producers in aligning with the region's stringent definitions of natural flavoring substances. Furthermore, an anti-dumping measure in June 2025 targeted Chinese vanillin, curbing the pricing edge of synthetic imports in Europe's food manufacturing sector. Germany, France, and the Netherlands stand out as pivotal demand hubs, thanks to their well-entrenched premium confectionery, bakery, and fragrance markets. Adding to Europe's advantage are production leaders like France's Ennolys and Norway's Borregaard, both adeptly navigating the region's regulatory and sustainability landscape.

Asia-Pacific is on a rapid ascent, with the region's natural vanillin market projected to expand at a 9.98% CAGR from 2026 to 2031, driven by a surge in premium food manufacturing and heightened awareness of ingredient transparency. China finds itself in a dual role: a significant producer of synthetic vanillin and an increasingly prominent consumer of natural vanillin, especially in its premium processed food and beverage sector. Meanwhile, India is emerging as a key player, leveraging its rice bran availability for ferulic acid production and clean-label product development. Japan's natural vanillin sales are on the rise, fueled by a robust demand for premium confectionery and a keen sensitivity to ingredient transparency. Additionally, countries like Indonesia, Thailand, and South Korea are driving secondary growth, particularly in beverages and cosmetics, further solidifying the region's foothold in the natural vanillin market.

North America plays a pivotal role, merging vast food manufacturing capabilities with a deep-rooted demand for premium flavors and fragrances. However, the region grapples with complexities in labeling, especially concerning vanilla-specific terminology in fermentation-derived products, complicating branding strategies. In South America, Brazil takes the lead, presenting the region's most promising growth avenue for the natural vanillin market, thanks to its thriving premium food processing sector. Meanwhile, the Middle East and Africa, though smaller in scale, see concentrated demand in imported premium consumer goods and select pharmaceutical applications, rather than widespread domestic formulations.

Competitive Landscape

In the natural vanillin market, competition is intensifying, particularly among companies adept at traceable sourcing, fermentation, and navigating regulatory landscapes across diverse end uses. Borregaard stands out as the sole commercial producer of wood-based vanillin. In 2025, its BioSolutions division reported an EBITDA of NOK 1,209 million, attributing part of this growth to biovanillin. Further solidifying its position, Borregaard is set to boost its capacity by 5% to 10%, backed by an NOK 800 million debottlenecking investment at its Sarpsborg facility. This move is one of the most pronounced supply-side expansions in the natural vanillin arena. Meanwhile, IFF, Givaudan, and Symrise prioritize their prowess in sourcing, refining, and seamlessly integrating natural vanillin into expansive flavor and fragrance systems, rather than merely competing on scale. This strategy ensures a competitive edge in the natural vanillin market, emphasizing the importance of formulation support and robust customer relationships alongside ingredient production.

Strategic maneuvers in 2025 and 2026 highlight the evolving competitive landscape of the natural vanillin market. In May 2026, IFF inaugurated its Vanilla Innovation Center in Madagascar, aiming to bolster origin-level research, extraction expertise, and supply resilience. This move underscores the significance of upstream control in bean sourcing. Givaudan, in its 2025 integrated report, highlighted that a commendable 87% of its naturals portfolio was sourced responsibly, underscoring the growing emphasis on procurement governance and traceability in supplier selection. In a bid to deepen its fermentation capabilities, Symrise made an equity investment in U.S. biotech Cellibre in October 2025, moving away from sole reliance on external supplies. Lallemand’s March 2026 Hevani launch demonstrated that even newer entrants can swiftly penetrate the natural vanillin market, provided they offer high purity, dual EU and U.S. natural status, and compliance with IFRA standards.

Looking ahead, the natural vanillin market's competitive focus is shifting. It's likely to emphasize cost efficiency, carbon documentation, and streamlined global product approvals, moving beyond mere availability. Conagen’s collaboration with BASF in fermentation exemplifies how synthetic biology can enhance yields, posing a challenge to traditional supply models. Additionally, an EU anti-dumping ruling on Chinese vanillin has paved the way for Europe-based bio-suppliers, alleviating pricing pressures from budget-friendly synthetic imports. As the natural vanillin market evolves, companies adept at intertwining traceable feedstocks, regulatory transparency, and consistent performance are poised to lead the pack.

Natural Vanillin Industry Leaders

Symrise AG

International Flavors and Fragrances Inc.

Solvay SA

Lesaffre International

Givaudan SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: IFF opened its Vanilla Innovation Center in Madagascar, establishing a dedicated research and extraction hub designed to optimize vanilla types, post-harvest processing variables, and flavor profiles at origin. The facility integrates into IFF's global vanilla network and is intended to generate proprietary formulation insights for IFF creation teams worldwide, strengthening the company's upstream capability in natural vanilla and its ability to support resilient vanilla supply chains at the source.

- March 2026: Lallemand Bio-Ingredients commercially launched Hevani, a natural vanillin produced via yeast-based precision fermentation, achieving 98% purity and holding natural flavoring status in both the EU and the US without requiring GMO labeling. The product is eligible for use in food, confectionery, dairy, and cosmetic applications, meets IFRA compliance standards, and is available for immediate commercial sampling and formulation across major food and beverage channels. The technology was acquired with Evolva in 2024.

- October 2025: Symrise announced a strategic equity investment in Cellibre, a US-based biotechnology company specializing in sustainable biomanufacturing. The partnership gives Symrise preferred access to Cellibre's proprietary fermentation-based technology, initially targeting taste solutions and cosmetic actives, with the stated objective of mitigating seasonal cultivation variability and building resilience in natural ingredient supply chains.

Global Natural Vanillin Market Report Scope

Natural vanillin is a primary organic flavor compound (C₈H₈O₃) responsible for the characteristic taste and aroma of vanilla. The global natural vanillin market is segmented by source, application, and geography. By source, the market is segmented into vanilla bean extract, eugenol synthesis, ferulic acid synthesis, and other sources. By application, the market is segmented into food and beverages, pharmaceuticals, cosmetics and personal care, and fragrances. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Vanilla Bean Extract |

| Eugenol Synthesis |

| Ferulic Acid Synthesis |

| Other Sources |

| Food and Beverages | Bakery and Confectionery |

| Beverages | |

| Dairy | |

| Other Food and Beverages | |

| Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Fragrances |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Source | Vanilla Bean Extract | |

| Eugenol Synthesis | ||

| Ferulic Acid Synthesis | ||

| Other Sources | ||

| Application | Food and Beverages | Bakery and Confectionery |

| Beverages | ||

| Dairy | ||

| Other Food and Beverages | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Fragrances | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which region leads sales, and which one is expanding the fastest?

Europe led with 36.40% share in 2025, while Asia-Pacific is projected to record the fastest growth at a 9.98% CAGR through 2031.

Which source type has the strongest position today?

Vanilla Bean Extract held 46.71% share in 2025, keeping its lead in premium applications that value provenance and bean-derived labeling.

Which application area offers the largest revenue base?

Food and Beverages accounted for 73.62% of the 2025 demand, supported by bakery, confectionery, dairy, and beverages.

What is driving faster growth in personal care use?

Cosmetics and Personal Care is projected to grow at a 9.11% CAGR because natural-derived fragrance ingredients fit clean beauty positioning and easier cross-category product development.

Page last updated on: