Bio Vanillin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

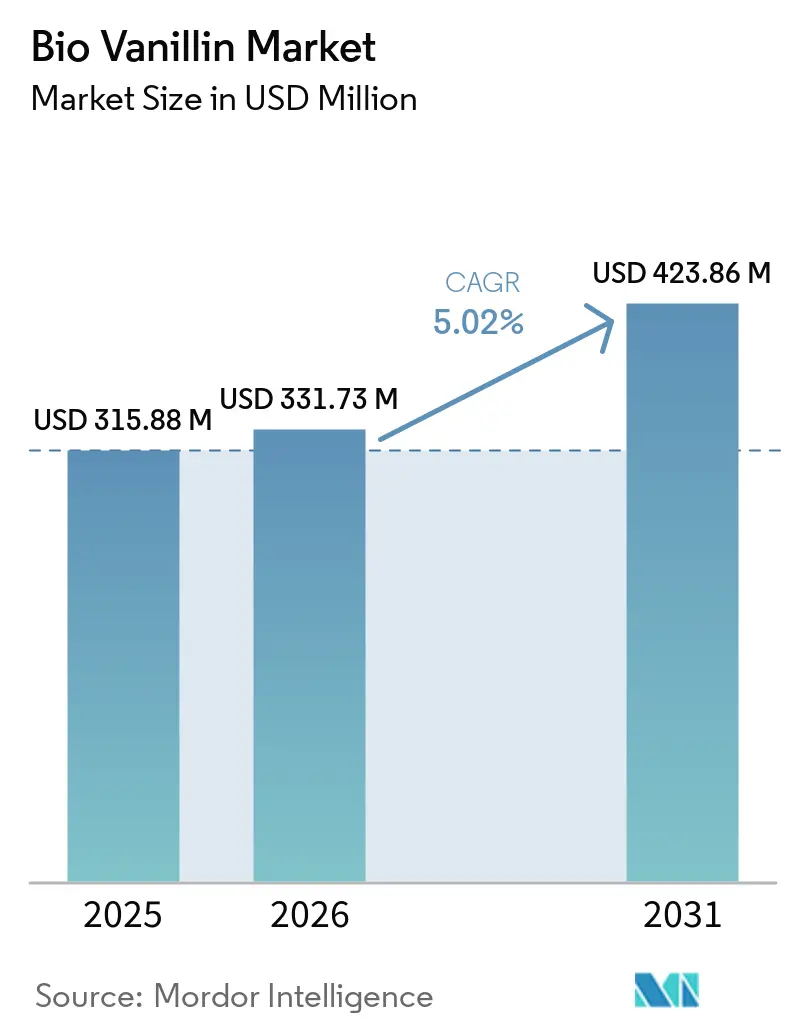

| Market Size (2026) | USD 331.73 Million |

| Market Size (2031) | USD 423.86 Million |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bio Vanillin Market Analysis by Mordor Intelligence

The bio vanillin market size is expected to grow from USD 315.88 million in 2025 to USD 331.73 million in 2026 and is forecast to reach USD 423.86 million by 2031 at 5.02% CAGR over 2026-2031. This growth trajectory reflects the market's resilience despite significant regulatory headwinds, particularly the U.S. Department of Commerce's [1]Source: U.S. Department of Commerce, "weighted-average dumping margin", www.federalregister.govfinal affirmative determination imposing antidumping duties of 190.20% on Chinese vanillin imports, which includes bio-sourced synthetic vanillin. Companies are achieving breakthrough yields in biotechnological production, with systems based on Corynebacterium glutamicum now producing 22 grams of vanillin per liter. This achievement significantly surpasses previous benchmarks in microbial production. As global demand for vanillin nears 20,000 tons annually, and natural sources fall short at under 2,000 tons, the market stands at a pivotal juncture. Biotechnological methods are uniquely poised to bridge this substantial supply gap. Furthermore, the food and beverage sector's embrace of sustainability-driven procurement policies, coupled with regulatory backing for natural labeling claims, creates a conducive atmosphere for the expansion of the bio vanillin market. This growth occurs even in the face of challenges like production costs and varying regional awareness.

Key Report Takeaways

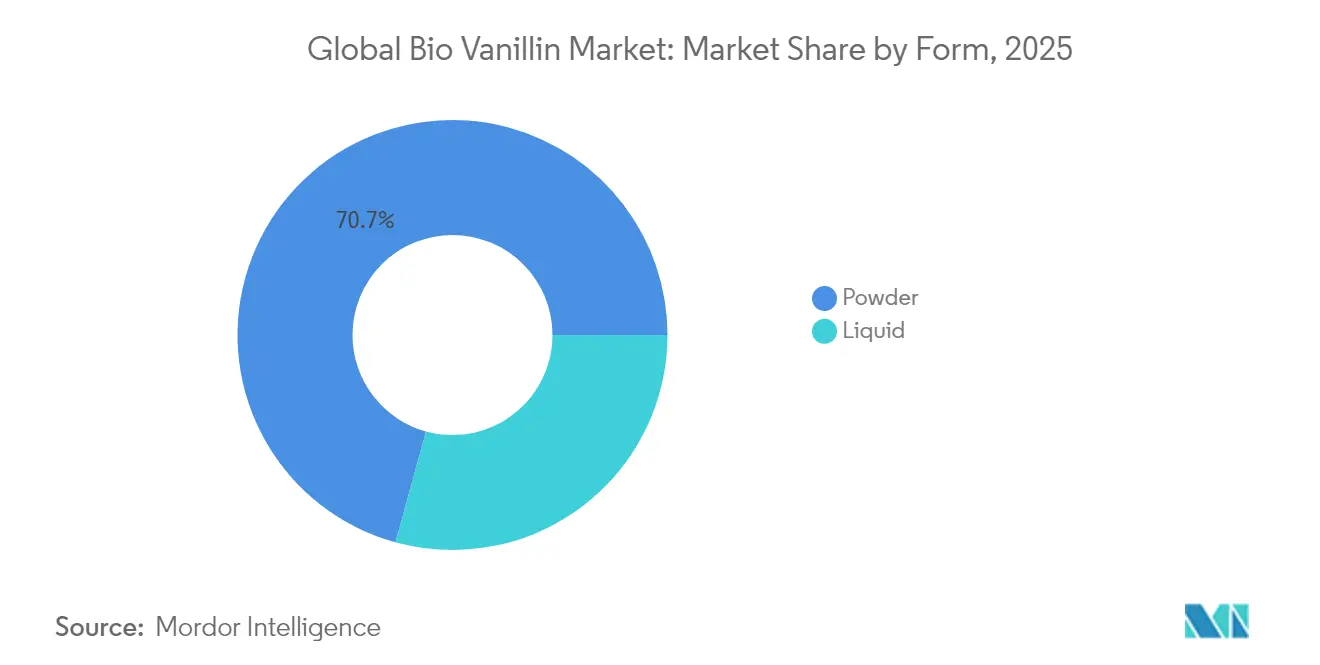

- By form, powder accounted for 70.73% of the bio vanillin market share in 2025, while the liquid segment is projected to grow at an 8.58% CAGR through 2031.

- By purity grade, food-grade products captured 63.62% share of the bio vanillin market size in 2025; fragrance-grade is forecast to expand at a 6.93% CAGR to 2031.

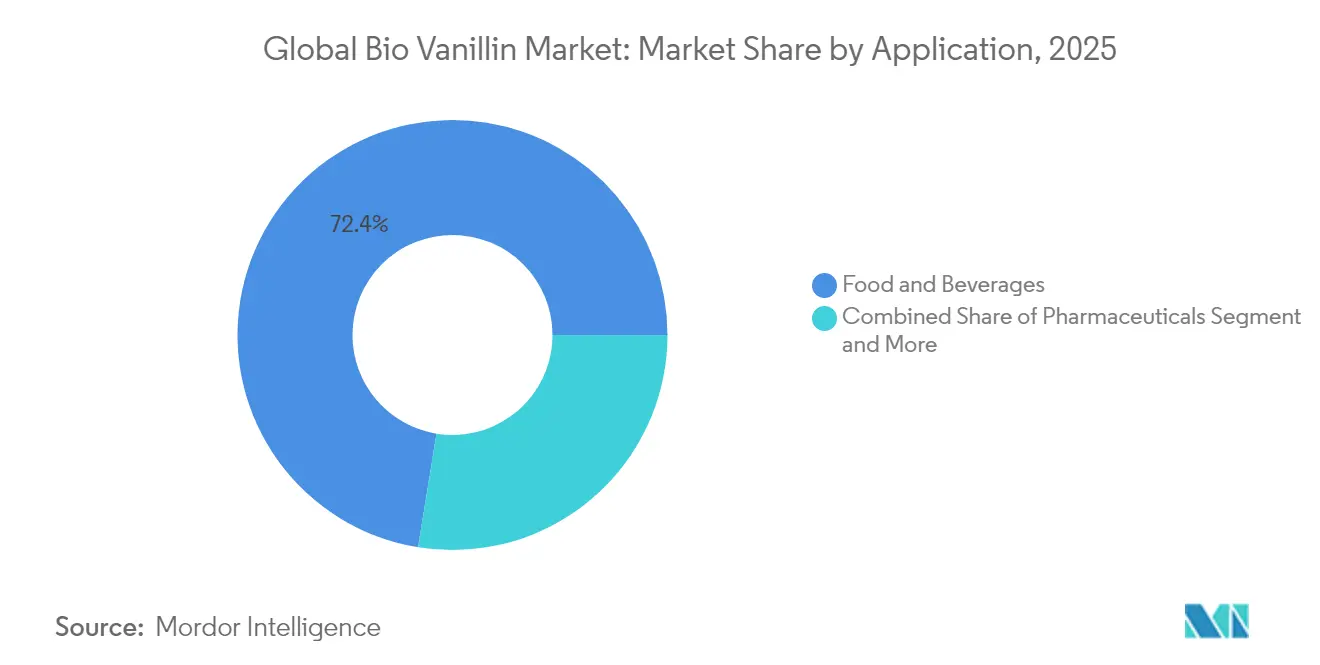

- By application, food and beverage held 72.44% revenue share in 2025, whereas pharmaceutical uses are advancing at an 7.86% CAGR to 2031.

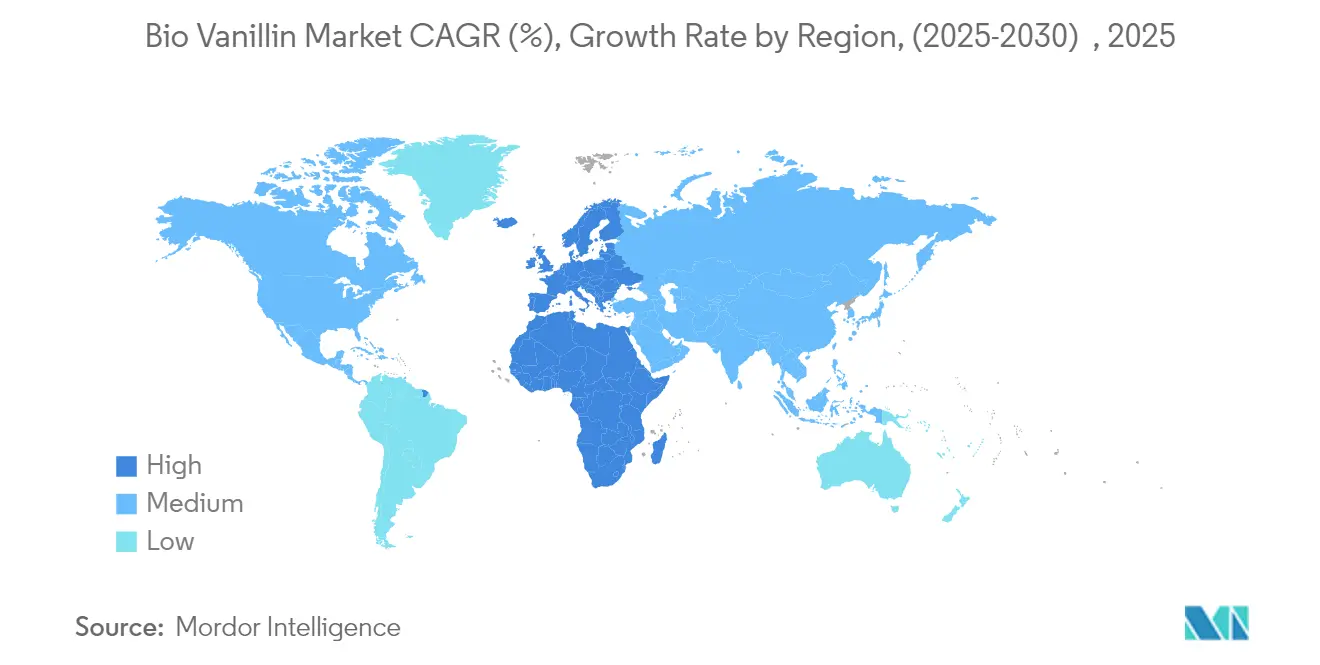

- By geography, Europe led with 32.33% share of the bio vanillin market size in 2025; the Middle East and Africa region is on track for a 7.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bio Vanillin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-driven demand from the food and beverage sector | +1.2% | North America and Europe, spreading globally | Medium term (2-4 years) |

| Regulatory support for “natural” label claims | +0.9% | North America and Europe, rising in Asia-Pacific | Long term (≥ 4 years) |

| Growing consumer preference for plant-based and vegan products | +0.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Technological advancements in biotechnological production | +0.7% | Global, with research and development clusters in Europe, North America, Asia | Long term (≥ 4 years) |

| Rising demand for clean-label and non-genetically modified organism (GMO) ingredients | +0.6% | Global, with strong traction in North America, Europe, and emerging in Asia | Medium term (2–4 years) |

| Expansion of bio vanillin applications in cosmetics and personal care | +0.5% | Global, led by Europe and Asia-Pacific | Medium to long term (3–5 years) |

| Source: Mordor Intelligence | |||

Sustainability-Driven Demand from the Food and Beverage Sector

The food and beverage industry's commitment to sustainability is fundamentally reshaping vanillin procurement strategies, with major manufacturers increasingly prioritizing bio-based alternatives that demonstrate measurable environmental benefits. Borregaard's wood-based vanillin production from Norway Spruce achieves a 90% reduction in CO2 emissions compared to oil-based vanillin, establishing a compelling sustainability benchmark that resonates with corporate environmental commitments. The sustainability imperative extends beyond carbon footprint considerations to encompass water usage, waste generation, and renewable resource utilization, positioning bio vanillin as a strategic ingredient for companies pursuing comprehensive environmental stewardship.

Regulatory Support for "Natural" Label Claims

Regulatory frameworks across major markets are creating distinct competitive advantages for biotechnologically produced vanillin through precise definitions of "natural" that exclude petroleum-derived synthetic alternatives. The U.S. Alcohol and Tobacco Tax and Trade Bureau explicitly recognizes vanillin derived from specific biotechnological processes as natural vanillin, allowing companies like Advanced Biotech and Apple Flavors to market their products with natural labeling claims that command premium pricing. FDA (Food and Drug Administration) [2]Source: FDA (Food and Drug Administration), " Generally Recognized as Safe (GRAS), www.ecfr.gov regulations under 21 CFR 172.510 provide clear pathways for natural flavoring substances, including bio vanillin, to achieve Generally Recognized as Safe (GRAS) status when produced through approved biotechnological methods. The regulatory environment is evolving toward greater transparency and traceability requirements, creating additional barriers for synthetic alternatives while providing clear competitive advantages for biotechnologically produced vanillin that can demonstrate natural sourcing and sustainable production methods.

Growing Consumer Preference for Plant-Based and Vegan Products

Consumer demand for plant-based and vegan products is driving fundamental changes in ingredient sourcing strategies, with bio vanillin positioned as a key enabler of natural flavor profiles in plant-based food formulations. The clean label movement reflects deeper consumer awareness of ingredient origins, with biotechnologically produced vanillin meeting consumer expectations for natural, plant-derived ingredients while avoiding the sustainability concerns associated with vanilla bean cultivation. Plant-based product manufacturers face unique formulation challenges in achieving authentic flavor profiles without traditional dairy or animal-derived ingredients, creating opportunities for bio vanillin to enhance taste experiences in vegan ice cream, plant-based baked goods, and alternative protein products. The intersection of plant-based trends with clean label preferences creates a compounding effect, as consumers increasingly scrutinize ingredient lists for both plant-based credentials and natural sourcing, positioning bio vanillin as a strategic ingredient that satisfies multiple consumer preferences simultaneously.

Technological Advancements in Biotechnological Production

Breakthrough innovations in biotechnological production are dramatically improving the economic viability of bio vanillin through enhanced yields, reduced production costs, and simplified processing requirements. Tokyo University of Science researchers developed a genetically engineered enzyme that converts ferulic acid from agricultural waste into natural vanillin in a single-step process, eliminating the need for cofactors and operating under mild conditions that significantly reduce energy requirements. Advanced microbial engineering approaches utilizing Corynebacterium glutamicum have achieved vanillin production levels of 22 grams per liter, representing a substantial improvement over previous biotechnological methods and approaching commercially viable production scales according to the Biotechnology for Biofuels and Bioproducts. These technological advances are converging to create production systems that combine high yields, low costs, and environmental sustainability, positioning biotechnological vanillin production for large-scale commercial implementation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost | –1.8% | Global, with sharper impact in emerging markets | Medium term (2-4 years) |

| Lack of awareness in developing countries | –0.7% | Asia-Pacific, Middle East and Africa, Latin America | Long term (≥ 4 years) |

| Regulatory and labeling compliance costs | –0.5% | Highly regulated markets worldwide | Short term (≤ 2 years) |

| Competition from alternative natural flavorings | –0.3% | Premium segments worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production Cost

The substantial cost differential between biotechnologically produced vanillin and synthetic alternatives represents the most significant barrier to market expansion, with production economics requiring careful optimization to achieve commercial viability. Current biotechnological production methods face inherent cost challenges related to fermentation infrastructure, substrate costs, downstream processing, and quality control requirements that synthetic production avoids through established petrochemical pathways. The price gap between natural vanillin at USD 700 per kilogram and synthetic vanillin at USD 15 per kilogram creates a 46-fold cost differential that limits market penetration to premium applications where natural labeling commands sufficient price premiums. The cost challenge is compounded by the need for specialized equipment, skilled personnel, and regulatory compliance infrastructure that synthetic production facilities do not require, creating additional barriers to entry for new market participants.

Lack of Awareness in Developing Countries

Limited awareness of bio vanillin benefits and applications in developing markets constrains market expansion opportunities, particularly in regions where food processing industries are experiencing rapid growth but lack familiarity with biotechnologically produced ingredients. Educational gaps regarding the distinction between biotechnologically produced vanillin and synthetic alternatives create market confusion that favors established synthetic products with lower price points and simpler supply chains.Consumer awareness of natural ingredient benefits remains limited in price-sensitive markets where purchasing decisions prioritize cost over ingredient sourcing, reducing demand for premium-priced bio vanillin products. The awareness challenge is exacerbated by limited marketing and educational resources dedicated to developing market penetration, as bio vanillin producers typically focus on established markets with existing demand for natural ingredients and regulatory frameworks that support premium pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Dominance Drives Market Stability

Powder form bio vanillin commands 70.73% market share in 2025, reflecting its superior stability characteristics, extended shelf life, and compatibility with diverse food processing applications that require precise dosing and consistent flavor delivery. The powder segment's dominance stems from its reduced susceptibility to oxidation and moisture absorption compared to liquid alternatives, making it the preferred choice for manufacturers requiring long-term storage capabilities and consistent product performance across varying environmental conditions.

Liquid bio vanillin, despite representing a smaller market share, is projected to achieve the fastest growth at 8.58% CAGR through 2031, driven by increasing demand from beverage manufacturers and liquid food applications where immediate solubility and homogeneous distribution are critical performance factors. Liquid formulations are gaining traction in applications requiring rapid flavor release and enhanced bioavailability, particularly in pharmaceutical and nutraceutical products where vanillin's antioxidant properties provide functional benefits beyond flavoring.

By Purity Grade: Food Applications Lead Market Development

Food grade bio vanillin represents 63.62% market share in 2025, reflecting the segment's maturity and established regulatory pathways that facilitate market access and consumer acceptance across diverse food and beverage applications. The food grade segment benefits from well-defined quality standards, established supply chains, and consumer familiarity that support stable demand growth and predictable market dynamics.

Fragrance grade bio vanillin emerges as the fastest-growing segment at 6.93% CAGR through 2031, driven by increasing demand from perfume and personal care manufacturers seeking natural alternatives that align with clean beauty trends and sustainability commitments.Pharmaceutical grade bio vanillin represents a specialized market segment with stringent quality requirements and regulatory oversight that create barriers to entry but support premium pricing for qualified suppliers. The pharmaceutical applications leverage vanillin's antioxidant and anti-inflammatory properties, with research demonstrating stronger antioxidant activity than synthetic alternatives and potential therapeutic benefits in various drug formulations.

By Application: Food Sector Dominance Amid Pharmaceutical Emergence

Food and beverage applications command 72.44% market share in 2025, establishing bio vanillin as a critical ingredient across ice cream, baked goods, beverages, and chocolate confectionery categories where natural labeling provides competitive advantages and consumer appeal. The food and beverage segment's dominance reflects established supply chains, regulatory approval pathways, and consumer acceptance that support stable market growth and predictable demand patterns.

Pharmaceutical applications represent the fastest-growing segment at 7.86% CAGR through 2031, driven by research demonstrating vanillin's therapeutic properties and increasing pharmaceutical industry interest in natural-derived active ingredients. The pharmaceutical segment's growth trajectory reflects vanillin's emerging role as a functional ingredient with antioxidant, anti-inflammatory, and anti-mutagenic properties that extend beyond traditional flavoring applications according to U.S Department of Health and Human Service .

Geography Analysis

Europe maintains market leadership with 32.33% share in 2025, supported by stringent natural flavoring regulations, established biotechnology infrastructure, and consumer preferences for premium natural ingredients that create favorable market conditions for bio vanillin adoption. The Middle East and Africa region is positioned for the fastest growth at 7.51% CAGR through 2031, driven by expanding food processing industries, increasing consumer awareness of natural ingredients, and growing disposable income that supports premium product adoption.

North American markets benefit from established biotechnology companies, supportive regulatory frameworks, and consumer demand for clean label products that drive bio vanillin adoption across food, pharmaceutical, and personal care applications. The region's market development is supported by companies like Borregaard, which has invested approximately USD 15 million to expand vanillin production capacity, and emerging players like Spero Renewables developing cost-competitive production methods from agricultural waste.

Asia-Pacific markets present significant growth opportunities despite current market share limitations, with increasing food processing activity, growing middle-class populations, and evolving consumer preferences for natural ingredients creating favorable long-term market dynamics. The geographic diversification reflects varying regulatory environments, consumer preferences, and industrial development levels that influence bio vanillin market penetration and growth strategies across different regions.

Note: Segment shares of all Individual segments will be available upon report purchase

Competitive Landscape

The bio vanillin market exhibits moderately concentrated conditions, reflecting a competitive environment where established chemical companies compete alongside emerging biotechnology firms through differentiated production technologies and market positioning strategies. Industry leaders like Kerry Group plc, Givaudan SA, Symrise AG, Archer-Daniels-Midland Company, and Solvay S.A. leverage established customer relationships, global distribution networks, and financial resources to maintain market positions while investing in biotechnological production capabilities that align with sustainability trends and regulatory requirements.

The competitive dynamics are increasingly shaped by technological differentiation, with companies pursuing distinct production pathways, including wood-based extraction, microbial fermentation, and enzymatic conversion that create unique value propositions and cost structures. Patent activity reflects intense innovation competition, with Evolva and International Flavors & Fragrances collaborating on biosynthesis methods for vanillin production using recombinant microorganisms, demonstrating the strategic importance of intellectual property in maintaining competitive advantages.

The competitive landscape is evolving toward sustainability-focused positioning, with companies emphasizing carbon footprint reduction, renewable resource utilization, and circular economy principles that resonate with environmentally conscious customers and regulatory trends. Strategic partnerships and joint ventures are becoming increasingly important for market access and technology development, as companies seek to combine biotechnology expertise with established distribution channels and customer relationships to accelerate market penetration and scale production capabilities.

Bio Vanillin Industry Leaders

-

Kerry Group plc

-

Givaudan SA

-

Solvay S.A.

-

Symrise AG

-

Archer-Daniels-Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The United States Department of Commerce issued final affirmative determinations on antidumping and countervailing duty investigations for vanillin imports from China, establishing dumping margins of 190.20% for most Chinese producers and 379.87% for the China-wide entity, significantly impacting global vanillin trade dynamics and creating opportunities for domestic and alternative source producers.

- November 2024: Research published in MDPI demonstrated biotechnological advances in vanillin production using metabolic engineering platforms, highlighting microalgae as promising production systems with ability to utilize CO2 and produce high-value compounds sustainably.

- May 2024: Tokyo University of Science researchers announced breakthrough development of a genetically engineered enzyme that converts ferulic acid from agricultural waste into natural vanillin in a single-step process, operating under mild conditions without cofactor requirements and utilizing abundant raw materials like rice and wheat bran for industrial-scale production.

Global Bio Vanillin Market Report Scope

The global bio vanillin market is segmented by application and geography. On the basis of application, the market is segmented into food, beverage, pharmaceutical, and fragrance. The food segment is further classified into ice cream, baked goods, chocolate, and other foods. On the basis of geography, the study provides an analysis of the bio vanillin market in the emerging and established markets across the world, including North America, Europe, Asia-Pacific, South America, and Middle-East & Africa.

| Powder |

| Liquid |

| Food Grade |

| Pharma Grade |

| Fragrance Grade |

| Food and Beverages | Ice Cream |

| Baked Goods | |

| Beverages | |

| Chocolate & Confectionery | |

| Other Food and Beverage Applications | |

| Pharmaceutical | |

| Fragrance and Personal Care |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Powder | |

| Liquid | ||

| By Purity Grade | Food Grade | |

| Pharma Grade | ||

| Fragrance Grade | ||

| By Application | Food and Beverages | Ice Cream |

| Baked Goods | ||

| Beverages | ||

| Chocolate & Confectionery | ||

| Other Food and Beverage Applications | ||

| Pharmaceutical | ||

| Fragrance and Personal Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What drives current growth in the bio vanillin market?

Demand for natural-labeled flavors, widening sustainability commitments by food companies, and antidumping duties on synthetic imports are the primary growth enablers.

How large is the bio vanillin market today?

The bio vanillin market size stands at USD 331.73 million in 2026 and is on course to reach USD 423.86 million by 2031 at a 5.02% CAGR.

Which segment grows the fastest?

Liquid formulations register the quickest expansion, projecting an 8.58% CAGR through 2031 as beverage makers seek rapid dissolution and clean labels.

Which companies are prominent in the competitive landscape?

The major comapnies in bio vanillin market are Kerry Group plc, Givaudan SA, Solvay S.A., Symrise AG, and Archer-Daniels-Midland Company.

Page last updated on: