MPOS Terminals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

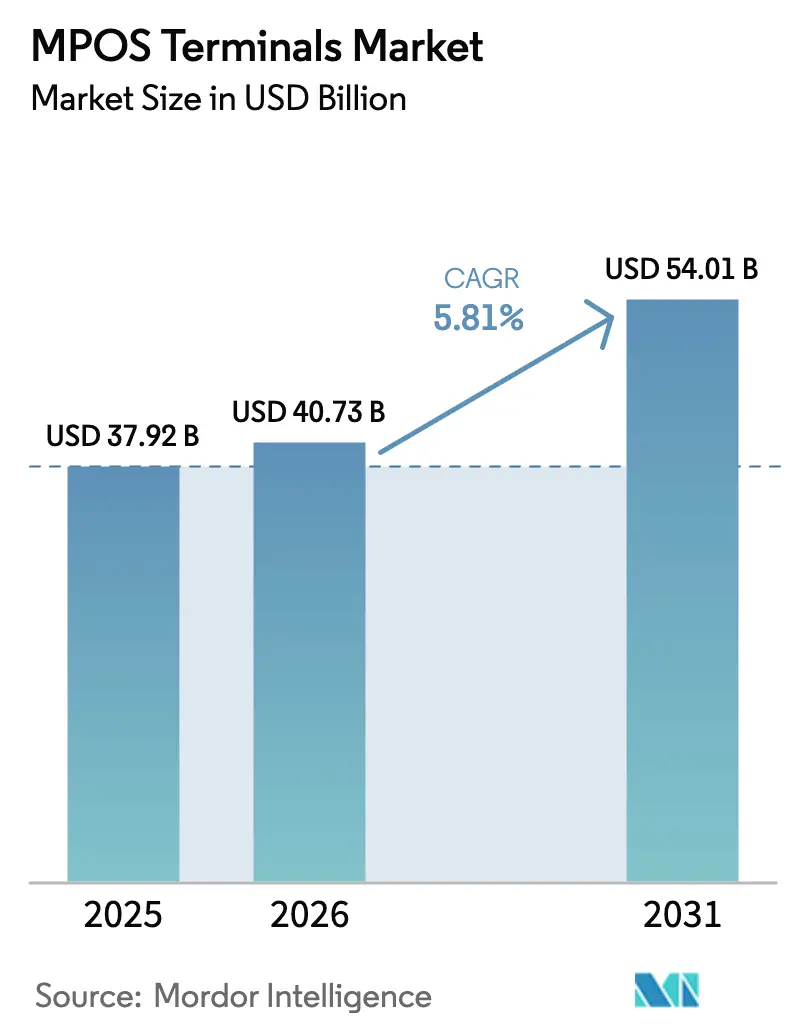

| Market Size (2026) | USD 40.73 Billion |

| Market Size (2031) | USD 54.01 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MPOS Terminals Market Analysis by Mordor Intelligence

The MPOS terminals market size is projected to expand from USD 37.92 billion in 2025 and USD 40.73 billion in 2026 to USD 54.01 billion by 2031, registering a 5.81% CAGR between 2026 to 2031. Software-only tap-to-phone certification is removing the need for dedicated entry-level hardware, while biometric Strong Customer Authentication regulations in Europe are stretching refresh cycles for premium devices. Platform players now bundle working-capital loans and data analytics with acceptance, raising merchant switching costs and compressing margins for pure-play hardware vendors. Regionally, Asia-Pacific is setting the tone with real-time payment rails and QR acceptance that speed new-merchant onboarding, whereas Europe is a compliance-driven replacement market and North America is approaching penetration limits. Cloud-based deployment keeps gaining favor because zero-capex onboarding, automated PCI DSS updates, and instant feature rollouts are more valuable to micro-merchants than local control of infrastructure.

Key Report Takeaways

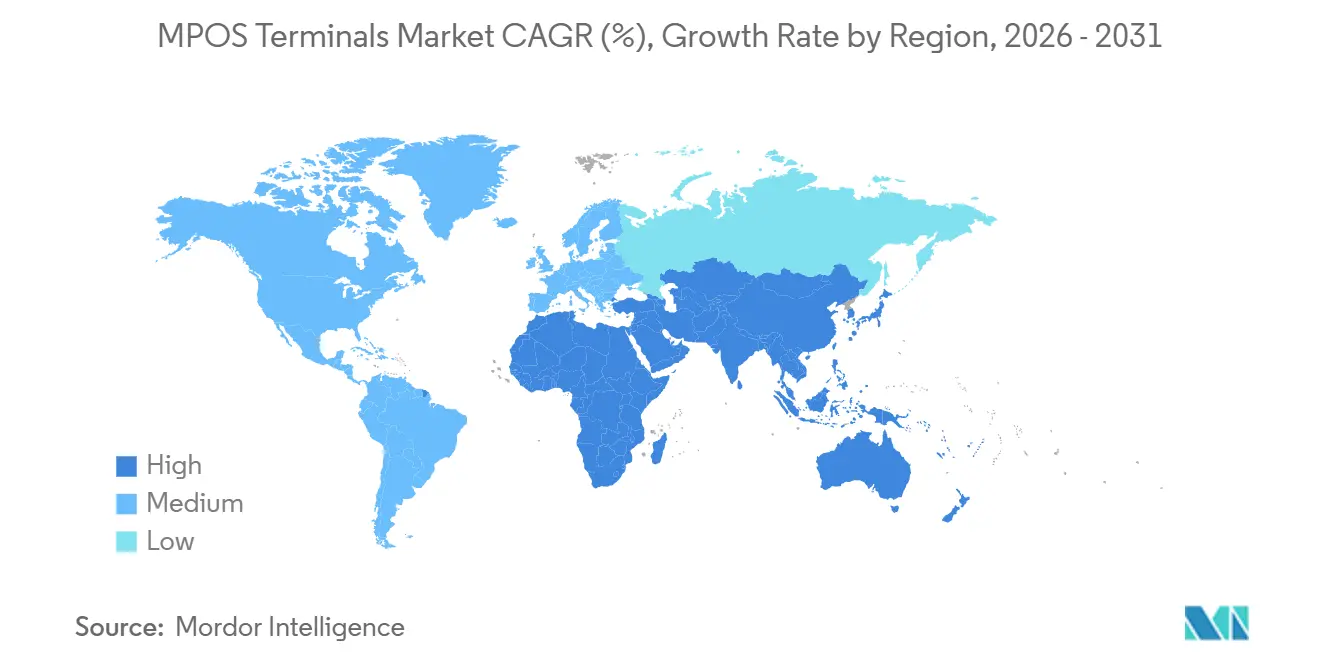

- By geography, Asia-Pacific led with 29.41% of the MPOS terminals market share in 2025; it is projected to expand at a 6.02% CAGR through 2031.

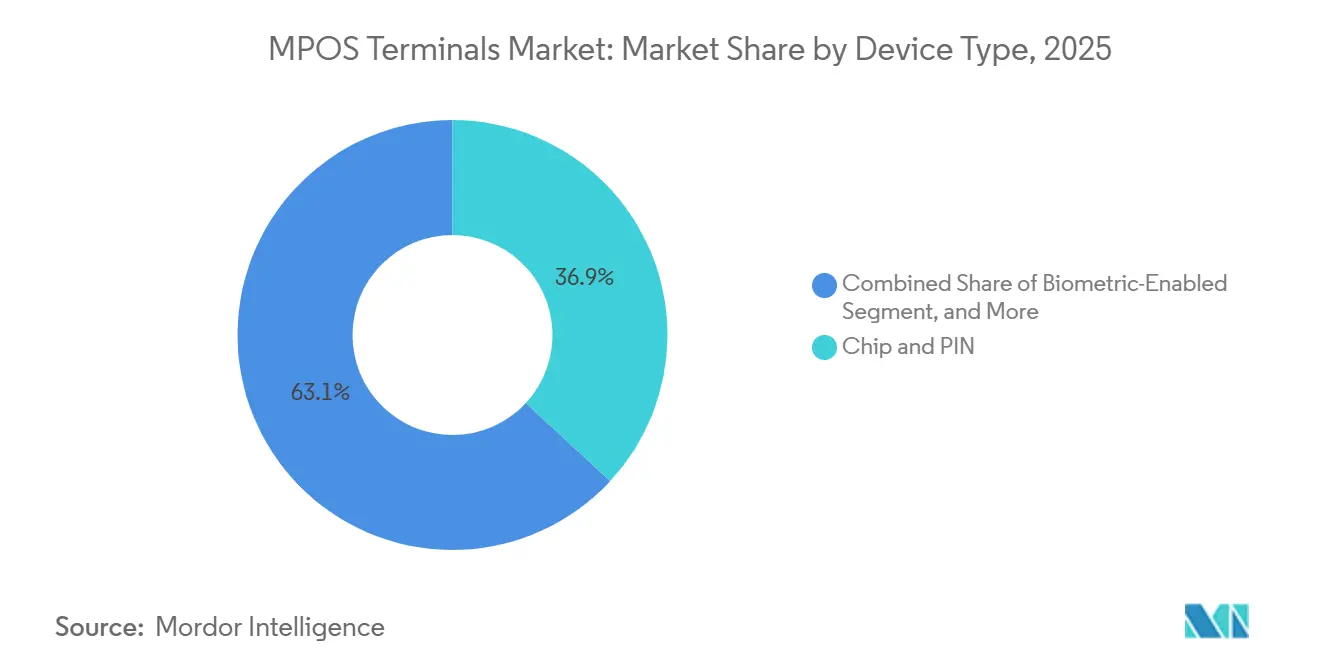

- By device type, chip-and-PIN held 36.89% of the MPOS terminals market share in 2025, while biometric-enabled devices are forecast to grow at a 9.13% CAGR through 2031.

- By mode of payment, contact-based transactions retained 76.67% share of the MPOS terminals market size in 2025, yet contactless modes are advancing at an 8.34% CAGR to 2031.

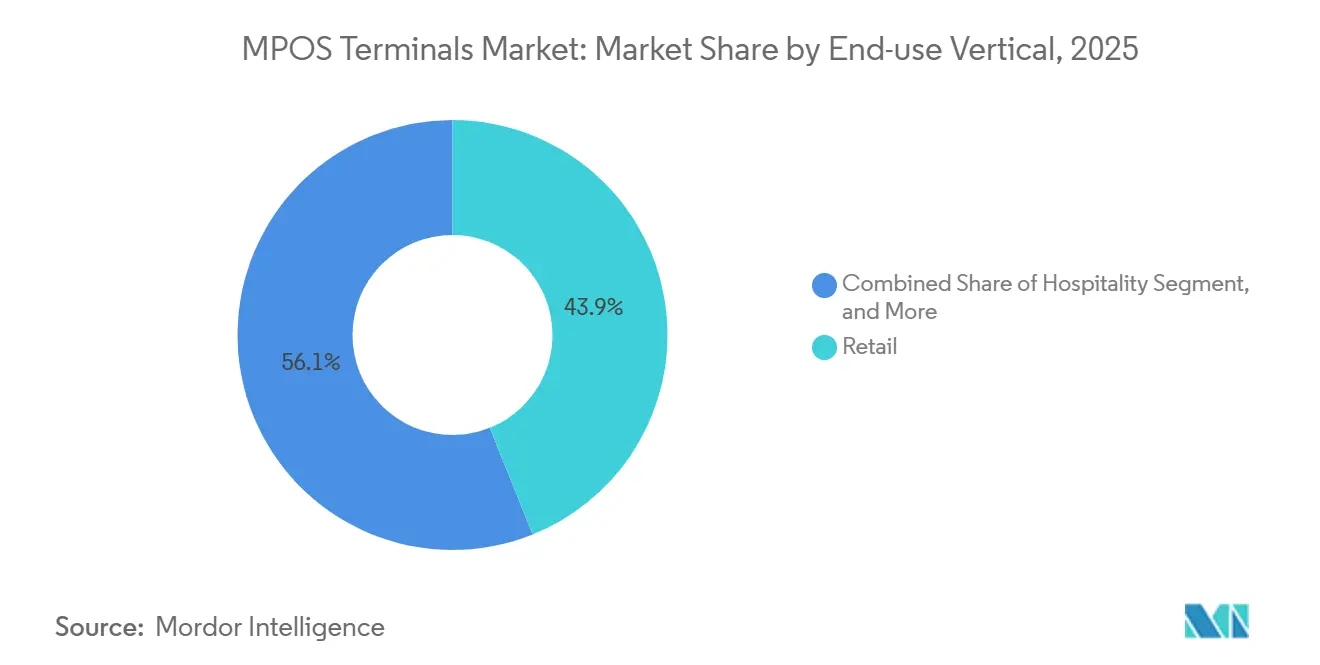

- By end-user industry, retail accounted for 43.92% share of the MPOS terminals market size in 2025, whereas hospitality is advancing at a 6.47% CAGR through 2031.

- By deployment mode, on-premise solutions commanded 70.59% share of the MPOS terminals market size in 2025, but cloud-based platforms are growing at a 7.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global MPOS Terminals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | IMPACT TIMELINE |

|---|---|---|---|

| Ubiquity of Low-Cost Card Acceptance Hardware | +1.2% | Global - highest in Asia-Pacific and South America | Short term (≤ 2 years) |

| Accelerating Consumer Shift to Contactless and E-Wallet Payments | +1.5% | Global - led by Europe and Asia-Pacific, North America catching up | Medium term (2-4 years) |

| On-Device Tap to Phone Certification Unlocking Smartphone-as-POS Solutions | +0.9% | Global - early gains in Europe, North America, urban Asia-Pacific | Medium term (2-4 years) |

| Rapid Rollout of Value-Add Analytics for Micro-Merchants | +0.7% | Global - strongest in North America and Western Europe | Medium term (2-4 years) |

| Biometric SCA Mandates Under PSD2 Boosting Hardware Refresh | +0.6% | Europe with spillover to Middle East and select Asia-Pacific | Long term (≥ 4 years) |

| In-Store BNPL Enablement Requiring MPOS Firmware Upgrades | +0.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ubiquity of Low-Cost Card Acceptance Hardware

Entry-level readers priced below USD 50 have unlocked acceptance for street vendors, pop-up retailers, and gig-economy workers that previously operated on cash alone. Square, SumUp, and PayPal Zettle all list sub-USD 50 dongles, and Asia-Pacific contract manufacturers now supply white-label units at under USD 30 ex-works, accelerating penetration into India’s tier-2 cities and Southeast Asia’s informal retail sector.[1]Block Inc., “Investor Relations,” investors.block.xyz Device commoditization is forcing vendors to pivot toward higher-margin subscriptions for analytics dashboards, loyalty integration, and embedded financing, reducing reliance on hardware gross profit. ISO 20022 messaging and EMVCo specifications guarantee interoperability, stripping away vendor lock-in and sharpening price competition.

Accelerating Consumer Shift to Contactless and E-Wallet Payments

Ireland logged mobile wallets at 58.2% of point-of-sale value during H1 2025, and 92% of U.K. card payments were tap-to-pay in 2024. For merchants, a 15-second tap replaces a 30-45-second PIN entry, shrinking queues and labor costs in quick-service restaurants. Hospitality venues report 10-15% faster table turns when tableside NFC terminals remove trips to a cashier station. The upside for MPOS vendors is an accelerated replacement wave for contactless-capable hardware, although the same consumer preference also makes SoftPOS viable, applying downward pressure on entry-level device sales.

On-Device Tap to Phone Certification Unlocking Smartphone-as-POS Solutions

PCI MPoC v1.1, released in November 2024, formalized security for software acceptance on commercial smartphones, removing the dongle requirement for many micro-merchants. Apple Tap to Pay lets small businesses download an app, pass KYC, and start accepting payments the same day, with no hardware cost beyond an NFC-enabled phone.[2]Apple Newsroom, “Apple Introduces Tap to Pay on iPhone,” apple.com Visa and Mastercard have since certified dozens of Android-based SoftPOS apps, widening availability in Europe and North America. By collapsing the total cost of acceptance to near-zero hardware and sub-2% processing, SoftPOS is poised to capture up to one-fifth of new micro-merchant onboarding in Europe by 2027.

Rapid Rollout of Value-Add Analytics for Micro-Merchants

Terminals have evolved into business-intelligence hubs that surface real-time revenue splits, peak-hour heatmaps, and inventory alerts. Square Dashboard, Toast’s restaurant analytics, Clover-QuickBooks integration, and Shopify POS each monetize premium insights at USD 20-50 per month, a margin multiple of hardware sales.[3]Shopify, “Shopify POS Features,” shopify.com/pos Micro-merchants with no dedicated finance staff can now optimize pricing, staffing, and promotion strategy, translating data into immediate profitability gains. The added stickiness drives retention and keeps payment volume on platform, counterbalancing margin erosion in hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | IMPACT TIMELINE |

|---|---|---|---|

| Emerging Tap-on-Phone SoftPOS Cannibalizing Dedicated MPOS Hardware | -0.8% | Global - most acute in Europe and North America | Short term (≤ 2 years) |

| Costly Migration to PCI MPoC and PCI v6 Compliance | -0.6% | Global - affects all hardware manufacturers | Medium term (2-4 years) |

| Patchy Broadband and Power in Rural Markets | -0.4% | Emerging Africa, South Asia, rural South America | Long term (≥ 4 years) |

| Persistent Security and Fraud Concerns | -0.3% | Global - heightened scrutiny in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Emerging Tap-on-Phone SoftPOS Cannibalizing Dedicated MPOS Hardware

Stripe’s software-only SDK, Apple Tap to Pay, and Android SoftPOS from Adyen and Worldline eliminate the USD 50-150 hardware purchase for small merchants, substituting existing smartphones for separate terminals. Micro-merchants and seasonal vendors processing fewer than 100 transactions a month are particularly drawn to zero-capex onboarding. European SoftPOS adoption could reach 15-20% of new merchant accounts by 2027, eroding entry-level device demand.[4]European Central Bank, “Payment Statistics,” ecb.europa.eu Incumbent vendors are countering by emphasizing countertop units with printers, customer displays, and biometric readers that smartphones cannot replicate, but the low-margin high-volume segment is already migrating toward software.

Costly Migration to PCI MPoC and PCI v6 Compliance

PCI PTS POI v6.0 adds secure boot, encrypted firmware, and hardware key storage, raising design complexity and lifting certification fees to USD 50,000-150,000 per model. The compliance deadline was pushed from January 2025 to June 2026, yet smaller manufacturers still face 6-12-month testing backlogs and risk stranded inventory if approvals slip. Meanwhile, PCI MPoC adds parallel compliance costs for vendors offering SoftPOS, multiplying R&D budgets. Scale players such as VeriFone, PAX Technology, and Ingenico can amortize expenses across global volume, whereas regional OEMs face margin compression or exit pressures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Biometric Authentication Drives Premium Tier Expansion

Chip-and-PIN held 36.89% of the MPOS terminals market share in 2025, underscoring its entrenchment in regulated environments. Biometric readers, however, are recording a 9.13% CAGR to 2031 after PSD2 raised authentication thresholds, fueling demand for fingerprint or facial recognition terminals across Europe. The MPOS terminals market size allocated to biometric devices therefore rises disproportionately as merchants absorb 30-40% higher unit prices to reduce chargebacks and align with data-protection rules. Low-feature magnetic-stripe and chip-only models now occupy a residual niche, mainly in countries with delayed EMV migration. Over time, device competition is shifting from interface technology toward authentication sophistication, with FIDO-certified sensors and privacy-preserving algorithms emerging as product differentiators.

The premium emphasis is attracting specialized suppliers such as Next Biometrics, which deployed fingerprint sensors in Vietnamese terminals, and PopID, which piloted facial-auth payment systems in the United Arab Emirates. Established vendors are integrating similar modules to defend share, while software platforms tie biometric readiness to value-add features like age verification and self-checkout. Cost-sensitive merchants in low-fraud environments stick with chip-and-PIN, while higher-ticket verticals migrate toward biometric-embedded models to balance security and user experience.

By Mode of Payment: Contactless Gains Accelerate Despite Contact-Based Dominance

Contact-based transactions retained 76.67% share in 2025, yet contactless volume is expanding at an 8.34% CAGR, nearly 1.5 times the overall MPOS terminals market growth. Consumer familiarity with tap-to-pay cards and mobile wallets has reached a tipping point, exemplified by Canada’s 3.4 billion mobile contactless transactions in 2024 and the United Kingdom’s 92% tap rate. To remain competitive, merchants are accelerating terminal refresh cycles toward NFC-enabled models or adopting SoftPOS that leverages the built-in antenna on smartphones.

Speed and convenience drive this migration. Contactless swipes average 15 seconds versus up to 45 seconds for PIN entry, translating into shorter queues and higher throughput in retail and hospitality. While compliance-driven verticals such as fuel or high-value ticketing will sustain contact-based methods, the growth premium for contactless is expected to keep widening as mobile wallet ecosystems expand loyalty, coupon, and digital-identity features that deepen user engagement.

By End-User Industry: Hospitality Leads Growth as Retail Holds Share

Retail bookings represented 43.92% of the MPOS terminals market size in 2025 owing to transaction volume and geographic ubiquity. Hospitality, however, is on track for a 6.47% CAGR through 2031, catalyzed by tableside payments that improve table turns by 10-15% and boost tip capture through suggested-gratuity screens. The MPOS terminals market share commanded by hospitality is therefore rising faster than its underlying transaction count, reflecting multiple terminals per venue rather than single checkout points.

Beyond restaurants, hotels are adopting handheld check-in units, and stadiums are shifting concessions to mobile kiosks. Healthcare is another growth pocket, integrating HIPAA-compliant MPOS modules into practice-management software for patient co-pay capture. Transportation fleets embed readers into driver handhelds for proof-of-delivery payment capture, while parking operations retrofit pay-on-foot machines with contactless modules. These specialized workflows highlight a pivot from generic payment acceptance toward process-specific terminal deployment that monetizes convenience and data insights.

By Deployment Mode: Cloud-Based SaaS Gains on Zero-Capex Appeal

On-premise infrastructure still held 70.59% share in 2025, but cloud adoption is accelerating at a 7.21% CAGR on the back of zero upfront capital expenditure, automated PCI updates, and rapid feature release cadences. Stripe, Adyen, and Square provision new merchants in hours, bundling payment processing, analytics, and settlement within a single subscription interface. The MPOS terminals market size linked to cloud models is enlarging faster than the headline market as micro-merchants favor pay-as-you-go economics.

Connectivity remains the constraint. Rural India, Indonesia, and sub-Saharan Africa, where broadband penetration lags 40%, still rely on on-premise or hybrid devices that buffer transactions offline. Vendors are mitigating risk with dual-SIM modules, local storage, and solar-charging docks, but those features lift device cost and complicate inventory. Over time, 5G rollout and satellite backhaul will ease the constraint, extending SaaS predominance into currently underserved regions.

Geography Analysis

Asia-Pacific contributed 29.41% of global revenue in 2025 and is forecast to post a 6.02% CAGR through 2031, the fastest of any region. Momentum stems from India’s UPI, which recorded 16.73 billion transactions in December 2024, and China’s Alipay Plus, which lets Thai, Malaysian, and Indonesian merchants accept payments from Chinese visitors via QR code without new hardware. Japan and South Korea are migrating from magnetic stripe to NFC ahead of regulatory sunsets, while Australia’s tap-and-go penetration tops 95%. Rural broadband in India and Indonesia hovers below 40%, and inconsistent electricity in Bangladesh and Vietnam limits always-on deployment.

North America ranks second in size. The region’s early EMV liability shift front-loaded hardware upgrades, so current demand revolves around replacing legacy units with contactless and biometric models. Canada’s 3.4 billion mobile contactless payments in 2024 showcase the consumer uptake, and Mexico’s fintech-driven merchant onboarding adds incremental headroom. Growth is steady but trails Asia-Pacific, reflecting market maturity and high existing penetration.

Europe’s trajectory hinges on PSD2 Strong Customer Authentication, which is driving premium hardware refresh even as SoftPOS cannibalizes entry tiers. Markets such as France and Germany are retrofitting terminals with fingerprint sensors to meet exemption thresholds, while micro-merchants adopt smartphone-based acceptance to avoid capital outlays. South America is propelled by Brazil’s Pix instant-payment system that exceeded 40 billion transfers in 2024, integrating QR acceptance directly into point-of-sale software. The Middle East benefits from smart-city investments in the United Arab Emirates and Saudi Arabia’s Vision 2030, whereas Africa remains constrained by power availability, forcing hybrid offline-first deployments despite strong mobile-money ecosystems.

Competitive Landscape

Competition is moderate in concentration but intense in platform value-added layers. Block’s Square, Fiserv’s Clover, and Toast’s restaurant-specific stack employ hardware as a gateway to recurring software revenue, including analytics, payroll, and working-capital loans that raise switching costs. Traditional device OEMs like VeriFone and PAX Technology increasingly supply white-label units to fintech aggregators, preserving scale volumes while ceding direct merchant touchpoints. Hardware gross margins have compressed from about 40% a decade ago to near 15-20% today, compelling all players to rely on subscription and processing fees over unit sales.

Strategic whitespace persists in healthcare, transportation, and rural emerging markets. Fewer than 30% of U.S. small medical practices have modern point-of-care payment capture because HIPAA compliance and legacy billing integrations raise adoption friction. Logistics operators need interoperable handheld readers for proof-of-delivery settlement, yet the segment remains splintered across proprietary solutions. Rural India, Indonesia, and sub-Saharan Africa still favor hybrid offline-first devices, creating entry points for vendors capable of pairing solar charging and offline buffering with cloud analytics.

Start-ups are leveraging pricing and settlement speed to chip at incumbents. South Africa’s Yoco offers zero-monthly-fee processing and same-day settlement to 400,000 micro-merchants, while Eastern Europe’s myPOS bundles IBAN accounts and instant payouts across the European Economic Area. Square Capital lent USD 4.1 billion to merchants in 2025, and Toast Capital expanded Working Capital loans beyond the United States, tying financing rates to payment volume. The fight is gradually shifting from device features to embedded financial-service breadth.

MPOS Terminals Industry Leaders

Block Inc. (Square)

Fiserv Inc. (Clover)

VeriFone Inc.

PAX Technology Ltd.

Newland Payment Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Central Bank of the United Arab Emirates launched a biometric payment terminal pilot with PopID, deploying facial-authentication devices across 50 Dubai retail locations to test next-generation digital-identity standards.

- January 2025: JP Morgan Payments introduced the Paypad and Pinpad terminal series for small and medium businesses, coupling integrated processing, invoicing, and real-time settlement.

- November 2024: The PCI Security Standards Council released PCI MPoC v1.1, formalizing global security requirements for software-based card acceptance on smartphones.

- October 2024: Block Inc. unveiled Square Terminal Flex, a 7-inch touchscreen portable device with integrated barcode scanning and 12-hour battery life, priced from USD 299.

Global MPOS Terminals Market Report Scope

MPOS terminals (Mobile Point-of-Sale terminals) are portable payment devices that allow businesses to accept card or digital payments using a smartphone or tablet instead of a traditional fixed checkout machine.

The MPOS Terminals Market Report is Segmented by Device Type (Chip and PIN, Chip and Signature, Contactless and NFC, Magnetic-Stripe-Only, Biometric-Enabled), Mode of Payment (Contact-based, Contactless), End-User Industry (Retail, Hospitality, Healthcare, Transportation and Logistics, Other End-User Industries), Deployment Mode (On-Premise, Cloud-Based and SaaS), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Chip and PIN |

| Chip and Signature |

| Contactless and NFC |

| Magnetic-Stripe-Only |

| Biometric-Enabled |

| Contact-based |

| Contactless |

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-User Industries |

| On-Premise |

| Cloud-Based and SaaS |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Device Type | Chip and PIN | |

| Chip and Signature | ||

| Contactless and NFC | ||

| Magnetic-Stripe-Only | ||

| Biometric-Enabled | ||

| By Mode of Payment | Contact-based | |

| Contactless | ||

| By End-User Industry | Retail | |

| Hospitality | ||

| Healthcare | ||

| Transportation and Logistics | ||

| Other End-User Industries | ||

| By Deployment Mode | On-Premise | |

| Cloud-Based and SaaS | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the MPOS terminals market in 2031?

The MPOS terminals market is forecast to reach USD 54.01 billion by 2031.

How quickly is the MPOS terminals market expected to grow between 2026 and 2031?

The market is projected to advance at a 5.81% CAGR over the 2026-2031 period.

Which region is expanding fastest in MPOS terminal adoption?

Asia-Pacific is anticipated to register the highest regional growth with a 6.02% CAGR through 2031.

Why are biometric MPOS devices gaining traction?

European Strong Customer Authentication rules and wider fraud-reduction efforts are driving a 9.13% CAGR in biometric-enabled terminal shipments.

What is SoftPOS and why does it matter?

SoftPOS software turns NFC-enabled smartphones into payment terminals, eliminating separate hardware costs and attracting micro-merchants seeking zero-capex acceptance.

How are vendors offsetting shrinking hardware margins?

Providers bundle analytics, financing, payroll, and inventory tools into subscription packages, shifting revenue toward high-margin recurring software and services.

Page last updated on: