Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

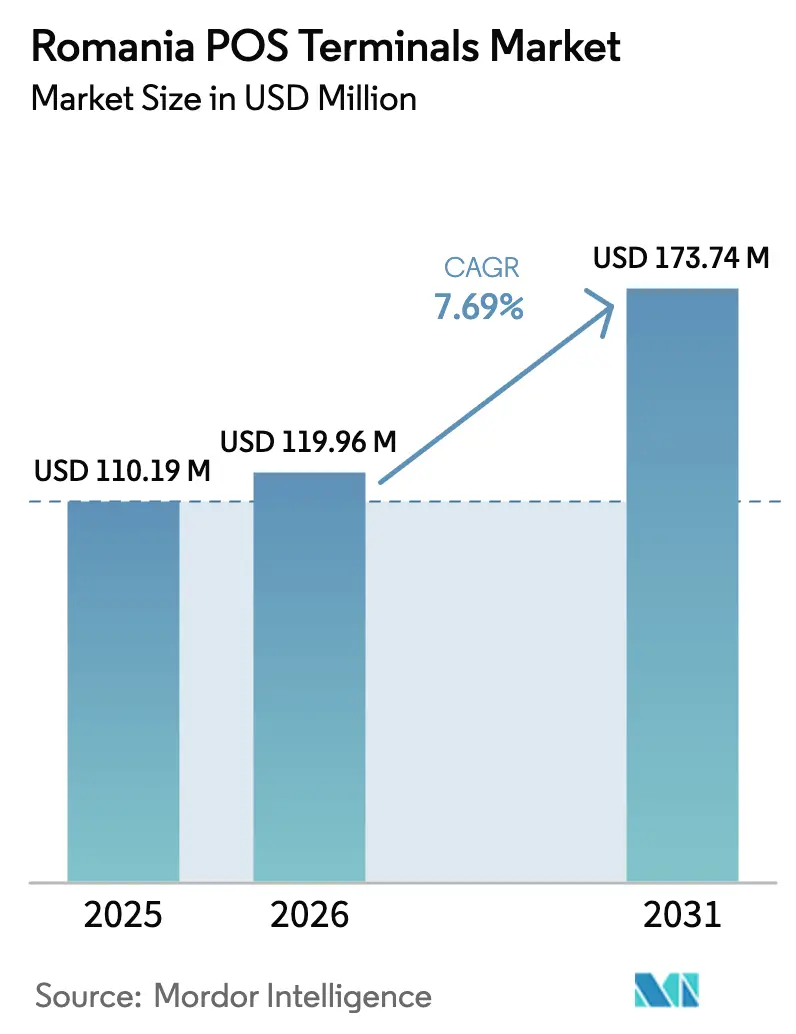

| Base Year Market Size (2025) | USD 110.19 Million |

| Market Size (2026) | USD 119.96 Million |

| Market Size (2031) | USD 173.74 Million |

| Growth Rate (2026 - 2031) | 7.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Romania POS Terminals Market Analysis by Mordor Intelligence

The Romania POS terminals market size is expected to grow from USD 110.19 million in 2025 to USD 119.96 million in 2026 and is forecast to reach USD 173.74 million by 2031 at 7.69% CAGR over 2026-2031. Legislative compulsion, banking-sector consolidation, and digital-infrastructure upgrades are jointly reshaping payment acceptance, with Law 239/2025 converting terminal deployment from a competitive choice to a legal requirement. The Banca Transilvania-OTP merger gave a single acquirer 31% of terminals, enabling aggressive pricing in rural counties. Demand for Android smart devices is rising as merchants seek value-added services, while cloud software subscriptions lower upfront costs for small businesses. Ubiquitous 4G and expanding 5G coverage are allowing outdoor merchants, transit operators, and tourism venues to maintain always-on connectivity.

Key Report Takeaways

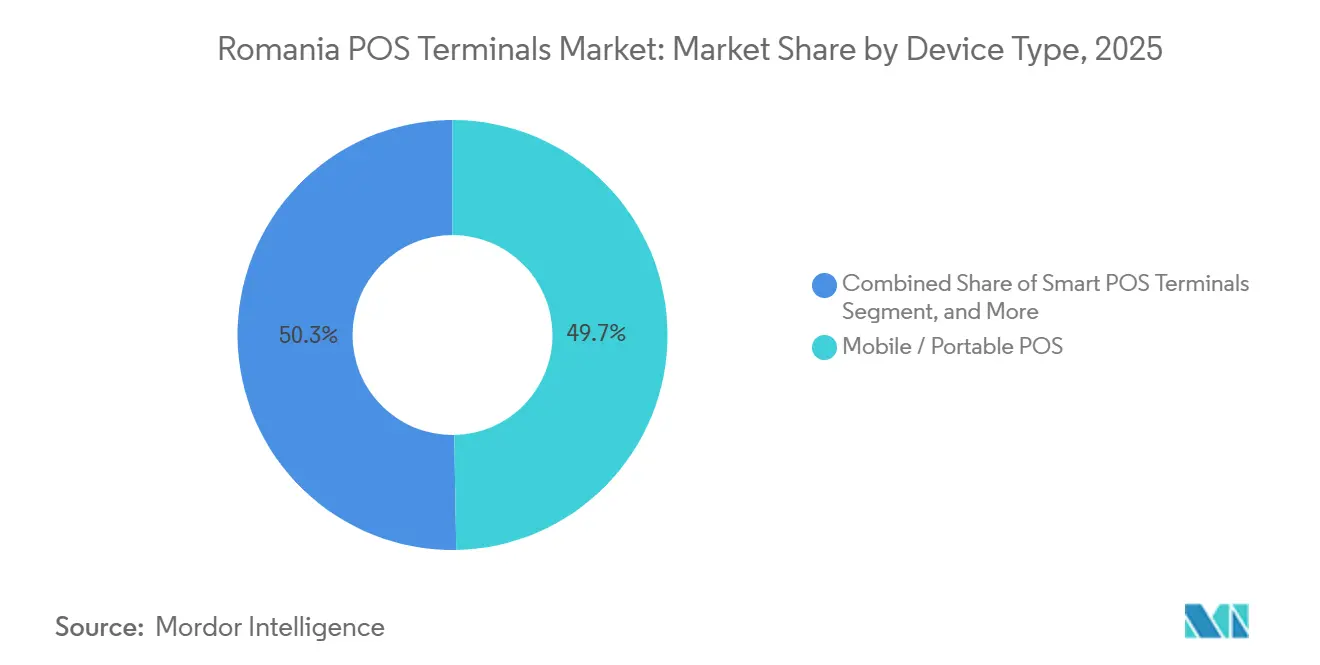

- By device type, mobile and portable terminals held 49.72% of the Romania POS terminals market share in 2025, while smart POS devices are forecast to expand at an 8.46% CAGR through 2031.

- By end-user industry, retail accounted for 38.19% of revenue in 2025, whereas transportation and logistics is projected to grow at an 8.79% CAGR to 2031.

- By component, hardware represented 63.77% of revenue in 2025; software is set to rise at an 8.23% CAGR during the forecast period.

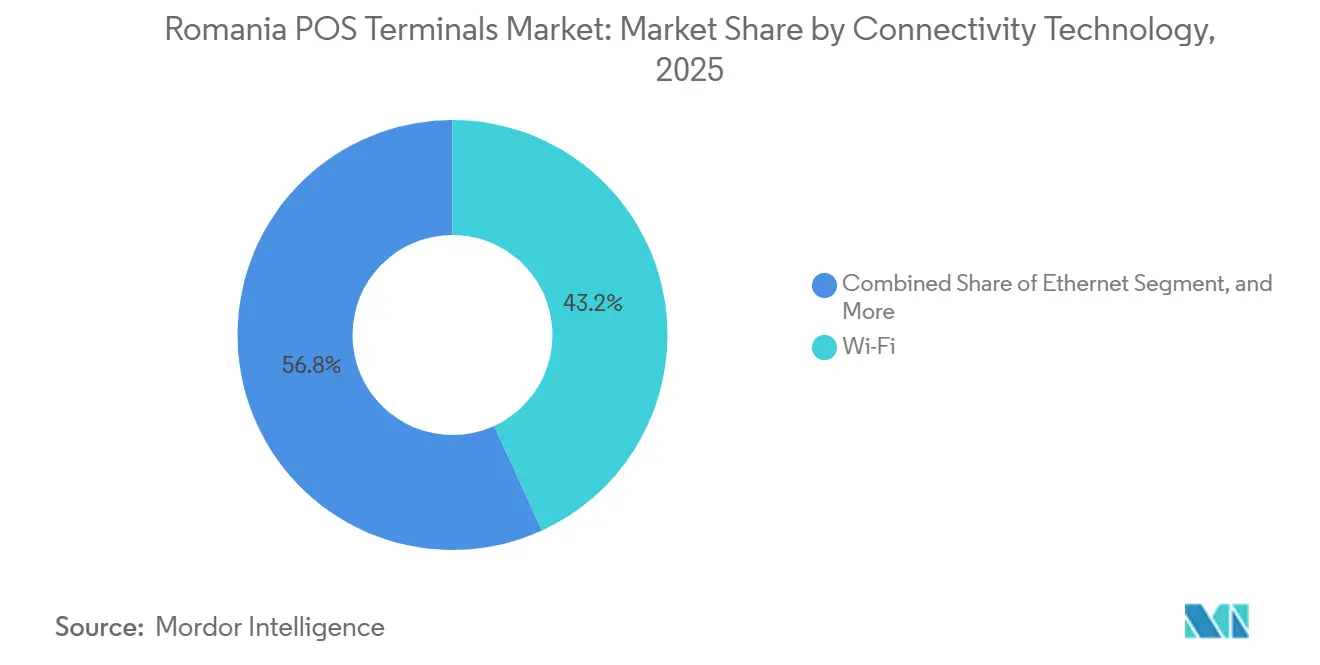

- By connectivity, Wi-Fi delivered 43.16% of 2025 installations, while cellular 4G and 5G links are advancing at an 8.41% CAGR.

- By deployment mode, cloud platforms captured 37.89% of the revenue in 2025 and are projected to progress at a 7.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Romania POS Terminals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Mobile POS Terminals | +1.2% | National, with concentration in Bucharest, Cluj-Napoca, Timișoara, and coastal tourism zones | Medium term (2-4 years) |

| Surge in Affordable Wireless Communication Technologies | +0.9% | National, accelerated by 5G rollout in urban centers and 4G densification in rural areas | Short term (≤ 2 years) |

| Rising Demand for Cashless and Contactless Payments | +1.5% | National, with higher penetration in retail and hospitality sectors | Medium term (2-4 years) |

| Government Fiscal Incentives for Electronic Fiscal Devices Adoption | +1.8% | National, enforced uniformly across all merchant categories | Short term (≤ 2 years) |

| Expansion of Romania's Tourism Industry Driving POS Deployment | +0.7% | Coastal (Constanța, Mamaia), mountain resorts (Brașov, Sinaia), and heritage cities (Sibiu, Sighișoara) | Long term (≥ 4 years) |

| EU Digital Operational Resilience Act Boosting Secure POS Upgrades | +1.0% | National, with emphasis on financial institutions and payment-service providers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Fiscal Incentives For Electronic Fiscal Devices Adoption

Law 239/2025 requires every Romanian merchant to accept electronic payments as of January 2026, eliminating previous exemptions and triggering a swift increase in new installations. Approximately 120,000 micro-enterprises are expected to acquire terminals within the first half of 2026, transforming compliance pressure into a revenue opportunity for acquirers. RO e-Factura has already digitized invoicing for 1.3 million entities, easing integration between point-of-sale systems and tax platforms. Leading banks have launched subsidized programs that waive setup fees and offer deferred payment schedules, accelerating the swap from stand-alone cash registers to integrated fiscal POS devices. This fiscal push is expected to narrow the urban-rural gap in infrastructure acceptance.[1]Romanian Parliament, “Law 239/2025 on Mandatory Electronic Payment Acceptance,” parlament.ro

Rising Demand For Cashless And Contactless Payments

Contactless taps reached 87% of card-present transactions in the first nine months of 2025 after the no-PIN ceiling rose to EUR 50 (USD 55). Mobile wallets such as BT Pay amassed 4.5 million active users, pushing digital payments into neighborhood bakeries and taxi fleets. The instant-payment scheme RoPay handled 8.2 million transfers worth RON 2.1 billion (USD 470 million) in its first six months, offering low-fee settlement outside traditional card rails.[2]National Bank of Romania, “RoPay Instant Payment System Launch,” bnr.ro Younger users favor tap-to-pay, suggesting sustained momentum as demographics evolve. Merchants are responding with terminal upgrades that support NFC and QR acceptance.

Increasing Demand For Mobile POS Terminals

Mobile devices captured nearly half of 2025 revenue, reflecting suitability for micro-merchants and service providers without fixed premises. SoftPOS technology converted about 25,000 Android phones into acceptance points by late 2024, lowering entry costs. Banks bundled SoftPOS with cloud POS software, giving restaurants the ability to manage orders, inventory, and delivery apps from a single handset. Vendors such as myPOS offer AppMarkets that add loyalty, digital receipts, and CRM tools on the device, merging payment and business management. Seasonal retailers in coastal resorts and festivals value portability and battery life over countertop features.[3]myPOS Europe, “Product Specifications and AppMarket,” mypos.com

EU Digital Operational Resilience Act Boosting Secure POS Upgrades

The Digital Operational Resilience Act, which has been enforceable since January 2025, obliges payment service providers to conduct annual penetration tests, maintain incident-response playbooks, and report ICT disruptions within four hours. Terminals must therefore support secure firmware downloads and end-to-end encryption. Larger acquirers with in-house cybersecurity teams benefit from the compliance burden, accelerating consolidation. Vendors are embedding cloud-security dashboards that enable banks to remotely patch thousands of terminals, shortening upgrade cycles and expanding demand for next-generation hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Security and Fraud Concerns | -0.8% | National, with heightened scrutiny in financial services and e-commerce sectors | Medium term (2-4 years) |

| Lack of Technical Standardization Across Legacy Infrastructure | -0.5% | National, concentrated in multi-location retail chains and franchises | Short term (≤ 2 years) |

| High Merchant Discount Rates for Small Romanian SMEs | -0.6% | National, disproportionately affecting micro-enterprises and rural merchants | Long term (≥ 4 years) |

| Supply-Chain Disruptions for Semiconductor Components | -0.3% | Global, with indirect impact on terminal availability and lead times in Romania | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Security And Fraud Concerns

Romania recorded 1,847 personal data breaches in 2024, a 19% increase from 2023, fueling merchant anxiety about networked devices. PCI DSS 4.0.1 added 53 new requirements, including mandatory multi-factor authentication, pushing acquirers to invest in compliance and recoup costs through higher service fees. Strong customer authentication reduces fraud losses, yet it lengthens checkout time, and 12% of shoppers abandoned pilot transactions that required extra steps. DORA mandates rapid incident reporting, favoring large banks that are better equipped to absorb the overhead. As a result, some small merchants delay upgrades or opt for cash-only workarounds.

High Merchant Discount Rates For Small Romanian SMEs

Card fees can exceed 3.5% for micro-merchants processing fewer than 50 transactions per month, which undermines the thin margins in groceries and kiosks. Although EU interchange caps limit scheme fees, acquirers overlay rental, gateway, and service charges, leaving cash acceptance cheaper for low-value tickets. Visa’s ePOSibil subsidies shorten the pain but have gained traction mostly for purchases above EUR 20. Flat-fee instant transfers via RoPay offer a cost alternative, yet consumer-initiated flows reduce impulse sales, constraining adoption for one-off retail encounters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Android-Based Smart Terminals Gain Traction

Smart units are expanding faster than the broader Romanian POS terminals market, growing at an 8.46% CAGR due to bundled inventory, loyalty, and analytics functions. This sub-segment is benefiting from Ingenico’s Manage 360 platform, which delivers remote updates and diagnostics, as well as from new PCI-PTS 6.x-certified models, such as the Newland N910 Pro. Smart terminals enable digital receipts and integrated loyalty, features prized by chain retailers that run multi-store promotions. However, the Romanian POS terminals market size for smart devices is constrained by upfront prices of EUR 200-400 (USD 220-440), compared with basic mobile readers priced under EUR 100 (USD 110).

Portability remains vital. Mobile and portable readers held 49.72% of the Romania POS terminals market share in 2025, allowing vendors to target farmers’ markets, events, and delivery couriers. SoftPOS extends its reach further by leveraging existing smartphones, eliminating the need for hardware expenditures. Countertop installations stay relevant in supermarkets and fuel stations where wired Ethernet and integrated scanners deliver low-latency throughput. Integrated kiosks are emerging in hospitals and transport hubs; 87 units launched by the Ministry of Transport handle self-service ticketing while meeting the security demands of public agencies.

By End-User Industry: Transportation Infrastructure Leads Growth

Transportation and logistics are projected to outpace the Romania POS terminals market at an 8.79% CAGR to 2031. Contactless validators across Bucharest metro and 15 regional bus networks shorten boarding queues and slash cash-handling costs. Oradea integrated RoPay QR codes into buses in October 2025, eliminating onboard hardware and proving the viability of mobile-initiated fare payment. Smart parking meters fitted with 4G-5G modems support dynamic pricing and remote diagnostics, reinforcing acceptance in municipal services.

Retail still leads revenue with 38.19% of the Romania POS terminals market share in 2025, yet growth is slowing as urban penetration nears saturation. Hospitality is recovering alongside tourism, spurring the adoption of tableside payments that sync with property-management systems. Healthcare digitization, backed by a EUR 150 million (USD 165 million) recovery-plan grant, is installing payment kiosks for co-pays, cafeteria meals, and parking. The remaining sectors - entertainment, professional services, education, and utilities - form a long tail that is increasingly addressed by SoftPOS solutions, which sidestep hardware costs.

By Component: Cloud Software Platforms Disrupt Traditional Hardware Models

Hardware still accounted for 63.77% of 2025 revenue, reflecting rental contracts that spread capital expenses. Yet software sales are rising at an 8.23% CAGR as merchants favor subscription models with automatic updates. Domestic SaaS vendors, such as Ebriza, charge EUR 49-179 per month for cloud POS solutions that integrate delivery apps and support offline mode. The Romania POS terminals market size for software is climbing as developers bundle ordering, loyalty, and reporting into a single dashboard.

Verifone and Ingenico now offer microservices that decouple authorization from hardware, allowing clients to add new schemes without requiring device swaps. Service installation, training, and field support remain stable, but face fee pressure as remote diagnostics shrink the need for onsite visits. Independent software vendors that provide turnkey bundles pose a competitive challenge to pure hardware suppliers that lack a developer ecosystem.

By Connectivity Technology: Cellular Networks Enable Always-On Acceptance

Wi-Fi accounted for 43.16% of installations in 2025, but cellular links are forecast to grow at an 8.41% CAGR, the fastest among connectivity options. Reliable 4G and quick 5G downloads of up to 212 Mbps enable real-time authorizations, even in open-air venues. Dual-connectivity devices meet DORA requirements for redundancy, enabling merchants to continue accepting payments during broadband outages.

Supermarkets and pharmacies, which process high volumes and prioritize latency control, continue to rely on Ethernet due to its reliability and ability to handle large data transfers efficiently. Bluetooth primarily connects peripheral scanners, such as barcode readers, to central terminals, ensuring seamless communication within the system, but it doesn't manage authorizations, which require more robust solutions. With the increasing density of the spectrum, cellular technology is poised to take the lead in seasonal locations, such as pop-up stores and temporary event spaces, as well as in burgeoning smart-city initiatives. These projects demand devices to be unattended, perpetually active, and capable of operating in diverse and dynamic environments, making cellular a more suitable option for such applications.

By Deployment Mode: Cloud Platforms Gain Share Through Subscription Economics

Cloud deployment represented 37.89% of 2025 revenue and is rising at a 7.88% CAGR as small firms adopt subscription models that replace server ownership. Omniful AI hosts data in local centers, addressing sovereignty concerns while offering auto-scaling and disaster recovery. Offline-first architectures enable merchants to queue transactions when the signal drops, syncing them later to the cloud, thereby reducing risk.

Large chains, valuing tight data control and custom integrations, dominate the on-premise systems, holding a 62.11% market share. Banks, in a strategic move, are now bundling cloud POS fees with acquiring contracts, simplifying the procurement process. However, in sectors like healthcare and finance, where regulation is stringent, concerns over recurring costs and potential data breaches are hindering the swift adoption of cloud services.

Geography Analysis

Romania had 529,520 active terminals by December 2024, equivalent to 27,771 units per million residents, which is below the European average but expanding faster as mobile adoption fills rural gaps. Bucharest, Cluj-Napoca, and Timișoara hold roughly 65% of devices due to dense retail footprints and service industries. The Banca Transilvania-OTP merger created a network of 177,000 units and the scale to push coverage into Moldavia and Wallachia, where cash still dominates.

Coastal resorts, such as Constanța and Mamaia, adopt flexible rental terms that match tourist seasonality, while mountain destinations like Brașov utilize contactless terminals for ski-lift tickets and rentals. Heritage cities, including Sibiu and Sighișoara, leverage Visa ePOSibil subsidies to equip guesthouses and craft shops that previously did not accept cards. The Ministry of Transport invested RON 450 million (USD 99 million) in 2025 to upgrade ticketing at 87 rail stations and 12 airports, aligning transit corridors with foreign travelers’ expectations.

Regional uptake remains sensitive to fees. The National Bank has resisted lower domestic interchange ceilings, preserving margins that finance rural rollouts yet slowing micro-merchant adoption. RoPay’s flat-fee transfers show promise in price-sensitive zones but lack buyer-protection features that encourage spontaneous spending. The uniform application of DORA elevates compliance costs, nudging smaller acquirers toward mergers, such as Euronet’s 2025 purchase of PayNet, which added 1,700 terminals to its portfolio.

Competitive Landscape

The Romania POS terminals market is moderately concentrated. Banca Transilvania, ING Bank, and Raiffeisen Bank together oversee about 60% of active terminals, while challengers myPOS, SumUp, and Viva Payments carve out niches in micro-merchant and hospitality segments. Banca Transilvania’s 2025 integration of OTP unlocks cross-selling potential across 4.4 million clients and underpins subsidized equipment schemes.

Hardware suppliers are evolving into software partners, reflecting a significant shift in the industry. Verifone's Bucharest center, staffed by 400 engineers, is focused on developing advanced cloud security and patch-management consoles. These solutions aim to streamline operations for acquirers by reducing overhead and enhancing system efficiency. Similarly, Ingenico's Manage 360 exemplifies this transformation by enabling remote feature deployment. This capability allows terminals to be continuously updated with new functionalities, effectively converting them from disposable units into long-term, evergreen assets that adapt to changing market needs.

White-space verticals remain. Public-hospital digitization, worth EUR 150 million (USD 165 million), is drawing integrated kiosk vendors. Municipalities deploy smart parking meters and QR fare systems, offering entry points for networking specialists. SoftPOS providers lower the barrier for sole traders, yet need to demonstrate sustainable revenue beyond per-transaction fees. DORA’s heavy compliance load favors scaled acquirers, suggesting further consolidation ahead.

Romania POS Terminals Industry Leaders

Sociedade Interbancária de Serviços, S.A.

Mellon Romania S.A.

Ingenico Group S.A.

Rapyd Financial Networks Ltd.

OTP Bank Romania S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Banca Transilvania reported a 31% acquiring share and 4.5 million BT Pay users at its Investor Day.

- November 2025: Oradea installed 30 smart parking meters with 4G-5G links, spending RON 1.45 million (USD 0.32 million).

- October 2025: Oradea became Romania’s first city to integrate RoPay QR fare payments in public buses.

- September 2025: Ingenico unveiled Manage 360, a cloud platform for remote terminal management.

Romania POS Terminals Market Report Scope

The Romania POS Terminals Market Report is Segmented by Device Type (Fixed Point-of-Sale Systems, Mobile/Portable Point-of-Sale Systems, Smart POS Terminals, Integrated POS Kiosks), End-User Industry (Retail, Hospitality, Healthcare, Transportation and Logistics, Entertainment and Recreation, Other End-User Industries), Component (Hardware, Software, Services), Connectivity Technology (Ethernet, Wi-Fi, Bluetooth, Cellular (4G / 5G)), and Deployment Mode (On-Premise, and Cloud-Based). Market Forecasts are Provided in Terms of Value (USD).

By Device Type

| Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems |

| Smart POS Terminals |

| Integrated POS Kiosks |

By End-User Industry

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Entertainment and Recreation |

| Other End-User Industries |

By Component

| Hardware |

| Software |

| Services |

By Connectivity Technology

| Ethernet |

| Wi-Fi |

| Bluetooth |

| Cellular (4G / 5G) |

By Deployment Mode

| On-Premise |

| Cloud-Based |

| By Device Type | Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems | |

| Smart POS Terminals | |

| Integrated POS Kiosks | |

| By End-User Industry | Retail |

| Hospitality | |

| Healthcare | |

| Transportation and Logistics | |

| Entertainment and Recreation | |

| Other End-User Industries | |

| By Component | Hardware |

| Software | |

| Services | |

| By Connectivity Technology | Ethernet |

| Wi-Fi | |

| Bluetooth | |

| Cellular (4G / 5G) | |

| By Deployment Mode | On-Premise |

| Cloud-Based |

Key Questions Answered in the Report

What is the current size of the Romania POS terminals market?

The Romania POS terminals market size stood at USD 119.96 million in 2026 and is projected to reach USD 173.74 million by 2031.

What CAGR is expected for point-of-sale terminals in Romania through 2031?

The market is forecast to grow at a 7.69% CAGR between 2026 and 2031.

Which device type leads adoption in Romania?

Mobile and portable terminals lead, accounting for 49.72% of 2025 revenue, due to their suitability for micro-merchants and outdoor venues.

Which end-user segment is expanding the fastest?

Transportation and logistics is the fastest-growing segment, projected to advance at an 8.79% CAGR as contactless validators and smart parking meters roll out.

How does Law 239/2025 affect merchants?

From January 2026, every merchant must accept electronic payments, forcing an estimated 120,000 micro-enterprises to deploy terminals within the first half of 2026.

Why are cellular connections gaining ground?

4G and 5G links provide always-on connectivity for merchants without fixed broadband and satisfy redundancy requirements under the Digital Operational Resilience Act.

Page last updated on: