Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

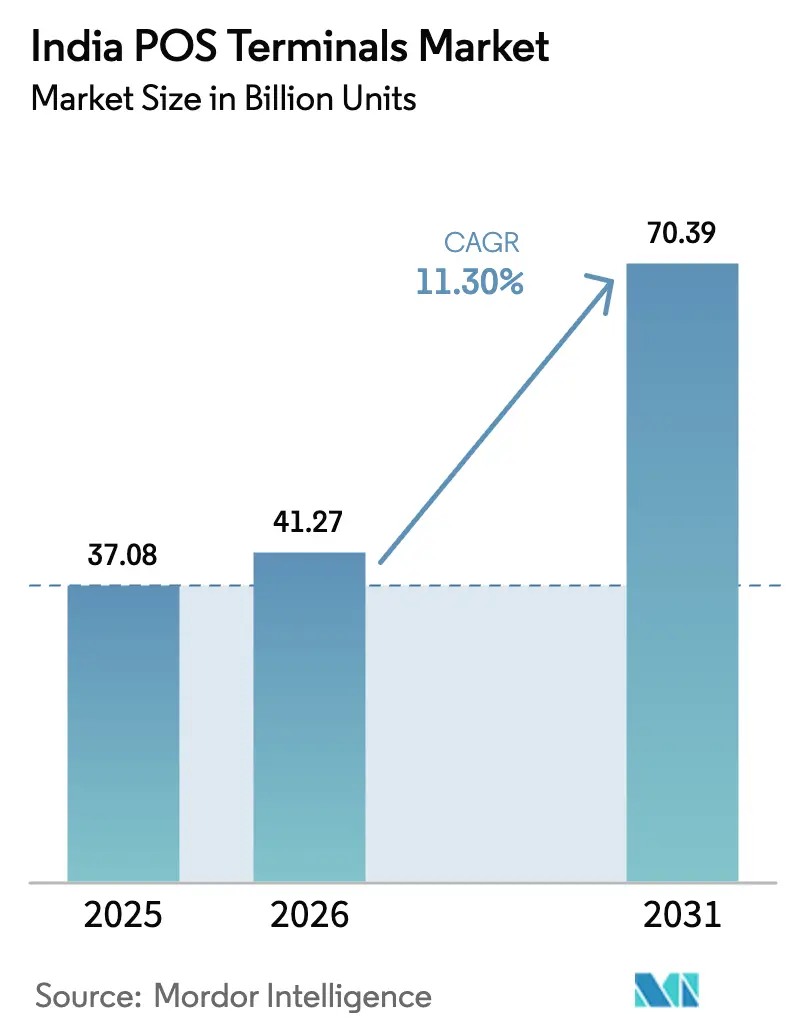

| Base Year Market Size (2025) | 37.08 Billion units |

| Market Volume (2026) | 41.27 Billion units |

| Market Volume (2031) | 70.39 Billion units |

| Growth Rate (2026 - 2031) | 11.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India POS Terminals Market Analysis by Mordor Intelligence

The India POS Terminals market size is expected to grow from 37.08 Billion units in 2025 to 41.27 Billion units in 2026 and is forecast to reach 70.39 Billion units by 2031 at 11.30% CAGR over 2026-2031. The growth pace reflected simultaneous tailwinds from government digitization mandates, a deepening credit infrastructure, and merchant demand for unified acceptance of cards, UPI, and emerging buy-now-pay-later options. Policy instruments such as Production Linked Incentive and Payments Infrastructure Development Fund subsidies cut onboarding costs for acquirers expanding into smaller cities, while GST e-invoice rules forced businesses above the INR 5 crore (USD 0.56 million) threshold to link real-time tax reporting with payment capture. At the same time the surging base of more than 100 million credit cards raised ticket sizes, improving the business case for card-capable terminals. Merchant economics nevertheless tightened once zero-MDR rules on UPI transactions came into force, pushing providers to roll out Android devices that process cards and UPI on the same hardware, and that allow instant app-based upgrades instead of forklift replacements. Competition therefore intensified between fintech specialists such as Pine Labs and Paytm and bank-led acquirers like HDFC, ICICI, and SBI that leverage existing branch footprints for distribution.

Key Report Takeaways

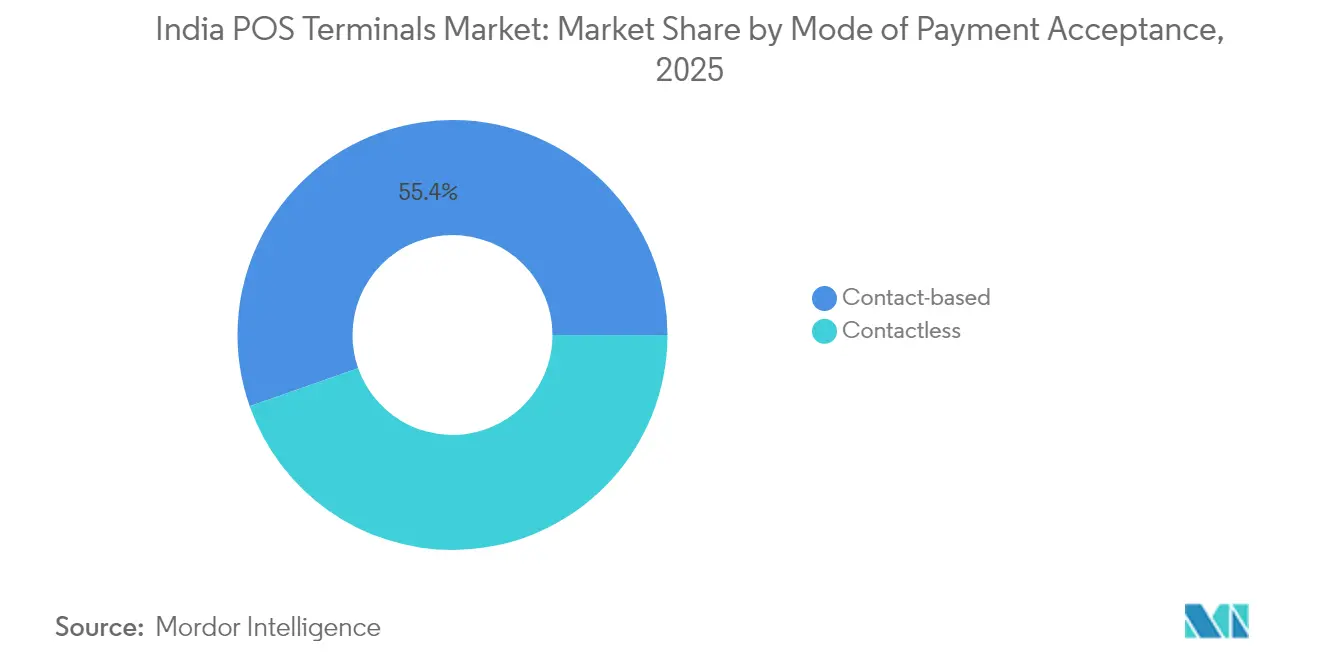

- By mode of payment acceptance, contact-based systems led with 55.38% of the India POS Terminals market share in 2025, while contactless solutions are forecast to post a 12.38% CAGR to 2031.

- By POS type, mobile and portable units accounted for 62.15% of the India POS Terminals market size in 2025 and are on track to expand at a 12.63% CAGR through 2031.

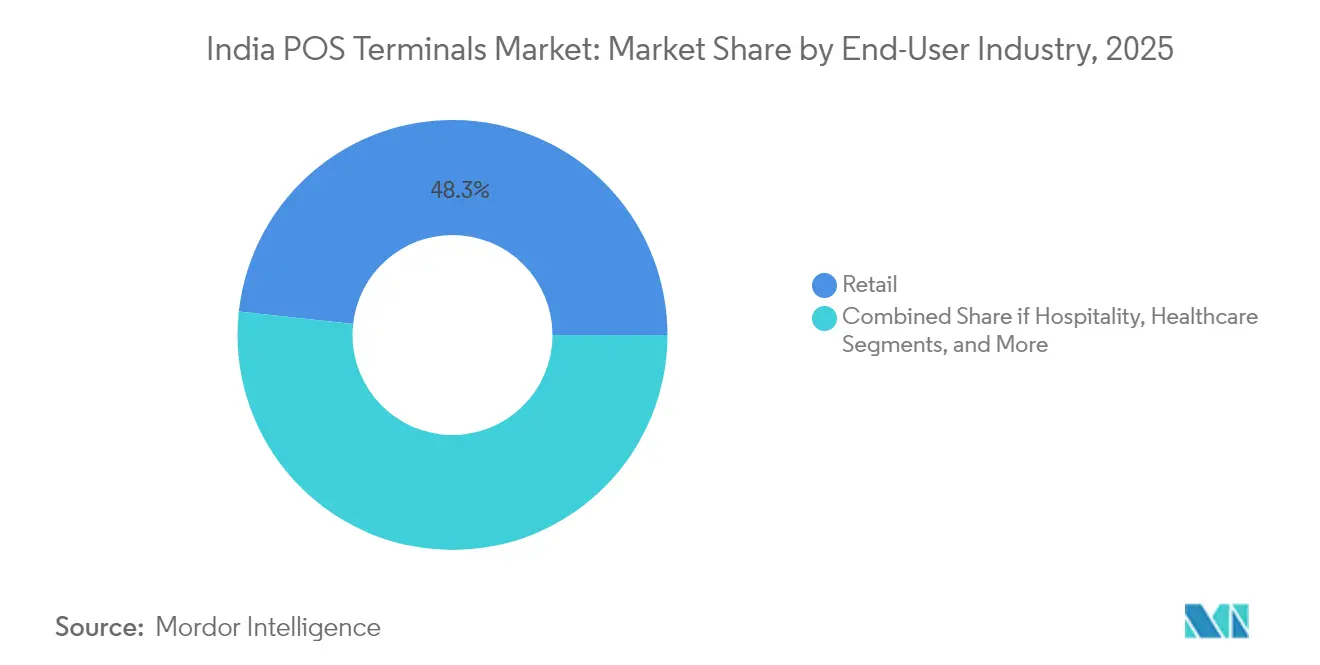

- By end-user industry, retail held 48.25% revenue share in 2025, whereas healthcare is advancing at a 13.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India POS Terminals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PIDF subsidies accelerating Tier-3-Tier-6 roll-outs | +1.8% | Tier-3 to Tier-6 cities, rural and semi-urban markets | Medium term (2-4 years) |

| Surging credit-card base (>100 mn) lifts card-swipe volumes | +1.2% | National, with concentration in metros and tier-1 cities | Short term (≤ 2 years) |

| Omni-payment Android POS (cards + UPI + BNPL in one device) | +1.6% | National, early adoption in urban retail and hospitality | Medium term (2-4 years) |

| GST e-invoice compliance driving real-time POS upgrades | +2.1% | National, businesses >Rs 5 crore turnover | Short term (≤ 2 years) |

| Smart-mall boom in Tier-2/3 cities raises fixed-POS demand | + 0.8% | Tier-2 and Tier-3 cities, retail expansion corridors | Long term (≥ 4 years) |

| Advanced analytics/AI add-ons boosting retailer ROI | +0.5% | Urban retail chains, organized retail sector | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PIDF subsidies accelerating Tier-3 – Tier-6 roll-outs

Government incentive pools such as the Payments Infrastructure Development Fund earmarked Rs 1,500 crore for terminals that process low-value UPI transactions. These incentives reduced acquirer risk and allowed providers to seed devices in towns where POS density had remained low. The subsidy design required adherence to RBI security standards, so deployments in smaller cities arrived with certified encryption and remote key injection, ensuring long-term operability.

Surging credit-card base lifts card-swipe volumes

India had issued 86 million credit cards by early 2025, and average monthly spend reached Rs 15,388, a 15% year-over-year climb.[1] Business Standard, “Credit Card Spending Crosses Rs 15,000 per Month,” business-standard.com Merchants noticed that card shoppers posted larger basket sizes than UPI users, so they upgraded to chip-and-PIN terminals that support contactless tap-to-pay. Banks and NBFCs widened card distribution, creating a virtuous loop for POS adoption even as UPI remained fee-free for small tickets.

Omni-payment Android POS adoption

Providers introduced Android-based smart terminals that accept EMV, NFC, UPI QR, and BNPL on a single screen. Pine Labs’ Hub device integrated more than 100 payment modes and offered inventory and analytics apps through over-the-air updates.[2]Pine Labs, “POS Hub: All-in-One Terminal,” pinelabs.com Merchants liked the reduced counter clutter and the ability to add new payment schemes without replacing hardware, which shortened upgrade cycles and raised lifetime value for acquirers.

GST e-invoice compliance driving real-time POS upgrades

Mandatory electronic invoicing for businesses crossing Rs 5 crore turnover forced about 2.1 million companies to generate invoices through a government portal at the moment of sale. Non-compliant legacy terminals could not push data in real time, so acquirers and software vendors bundled GST-ready POS packages with cloud connectivity, tax engine, and audit trail storage. This compliance push created a wave of refresh demand in both retail and B2B channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zero-MDR UPI erodes small-merchant economics | -1.5% | National, particularly affecting micro and small merchants | Short term (≤ 2 years) |

| QR-code ubiquity dampens new POS demand | -1.0% | National, urban and semi-urban markets | Medium term (2-4 years) |

| High total-cost-of-ownership for micro-merchants | -0.8% | Tier-3 to Tier-6 cities, micro retail segment | Long term (≥ 4 years) |

| Draft RBI PA-Offline rules raise compliance cost | -0.3% | National, affecting payment aggregators and POS providers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Zero-MDR UPI erodes small-merchant economics

The government removed merchant discount rates on UPI. Acquirers lost subsidy revenue that once offset device rentals, so many paused deployments to very small merchants. While policy makers later proposed a 0.2% fee for large chains, the near-term absence of interchange kept micro-merchant POS penetration low.

QR-code ubiquity dampens new POS demand

By February 2025 merchants had installed 352 million UPI QR codes compared with only 8.9 million POS terminals.[3]Economic Times, “QR Code Deployment Outpaces POS,” economictimes.indiatimes.com QR stickers cost little and carry no rental charges, so price-sensitive kirana stores favored them over dedicated hardware. Providers responded by embedding dynamic QR in Android POS screens, but the cost gap still slowed first-time terminal adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment Acceptance: Contactless adoption rises on NFC enablement

Contact-based methods retained 55.38% of the India POS Terminals market share in 2025 on durable chip-and-PIN infrastructure. Yet contactless payments posted a 12.38% CAGR, fueled by NFC upgrades in bank-issued cards and consumer comfort with tap-to-pay hygiene. Contactless also gained visibility through public transit pilots where fare gates promoted faster flows. The segment’s expansion indicates that, although cards remain important, the underlying interface continues to shift toward touch-free experiences.

Merchants looked beyond retail. State transport firms layered contactless validators onto buses and metros, and municipal utilities accepted tap cards for bill payment. Device makers explored biometric authentication to secure higher value taps without PIN entry. These innovations are expected to keep contactless momentum intact even once pandemic safety fades from public memory.

By POS Type: Mobile models dominate on flexibility

Portable and mobile devices controlled 62.15% of the India POS Terminals market size in 2025 and grew the fastest at 12.63% CAGR. Small retailers valued the ability to accept payments at the aisle, on delivery runs, or during pop-up events. Battery-backed mini POS units connected over 4G and paired with smartphones for receipt printing, which cut upfront costs. Fixed countertop stations retained relevance in hypermarkets and multiplex cinemas where conveyor belts and integrated scales mattered.

The mobile wave overlapped with Android deployments. Providers embedded inventory, loyalty, and billing apps, transforming the terminal into a miniature point-of-sale and back-office console. That app layer unlocked subscription income and deepened the moat against low-margin QR competitors.

By End-User Industry: Healthcare races ahead

Retail still commanded 48.25% revenue share in 2025 due to large store counts and high ticket churn. Healthcare, however, displayed the top CAGR at 13.02% as hospitals digitalized billing and insurance claims. Clinics implemented terminals that merge patient scheduling, e-prescriptions, and payment in one workflow. Diagnostics chains also outfitted technicians with portable units for at-home sample collection, thus broadening use cases for the segment.

Hospitality remained another growth pocket. Hotels integrated POS with property management software to centralize room charges and food-and-beverage bills. Restaurants upgraded to terminals that interface with kitchen display systems so that chefs receive tickets the moment servers close the order, which improved table turns.

Geography Analysis

Western and southern metros formed the first wave of POS adoption due to higher consumption and early digital payment penetration. Mumbai, Bengaluru, and Hyderabad together housed a major share of banked consumers and enterprise retailers. Northern states nevertheless recorded the largest pipeline of new organized retail projects, with 44% of mall supply scheduled in Delhi NCR, Punjab, and Uttar Pradesh. Those developments created multi-lane checkout counters that specified EMV and NFC hardware at the fit-out stage.

Tier-2 and tier-3 cities such as Jaipur, Lucknow, Indore, and Patna accelerated, benefiting from retail franchises and food chains seeking growth outside saturated metros. From 2024 to 2025, floor space across these cities increased by 25 million square feet, and food and beverage outlets rose nearly 26%, each store now embedding at least one POS to manage table orders and digital wallets. Such expansion provided a launchpad for acquirers to seed full-service Android devices coupled with financing bundles.

Rural and semi-urban clusters remained the frontier. POS deployment relied on 4G connectivity rather than fiber, hence mobile terminals with integrated SIM cards found more traction than desktop devices. Banks leveraged Jan Dhan account holder data to target micro-entrepreneurs for merchant loans paired with POS bundles. Despite these incentives, adoption timelines stretched into the outer years of the forecast because many small retailers still saw QR as enough.

Competitive Landscape

Competition in the India POS Terminals market involved fintechs, hardware vendors, and banks. No single firm held a commanding lead, keeping the field moderately fragmented and innovation driven. Pine Labs focused on mid-market retail with app-rich Android hardware, while Paytm leveraged its wallet user base to cross-sell terminals that present wallet cashbacks at checkout. Banks such as HDFC, ICICI, and SBI exploited branch reach to sign merchants in smaller towns, bundling current accounts, terminals, and working capital loans in one kit.

Product strategy converged on all-in-one acceptance. HDFC’s SmartHub Vyapar device packaged QR, card slot, NFC, and a talking soundbox speaker. Paytm and RBL Bank rolled out NFC soundboxes that announce successful card taps alongside QR transactions. Partnerships and acquisitions intensified. Zaggle bought 51% of Effiasoft to merge prepaid processing with POS software and address enterprise billing, signaling that software capability now matters as much as hardware reach. Worldline joined with Forthcode to create in-flight Android POS for airlines, highlighting niche vertical plays.

Regulation shaped the field. RBI Payment Aggregator rules increased net-worth thresholds and required security audits, which favored capitalized incumbents and nudged smaller aggregators into tie-ups. At the same time the proposed re-introduction of MDR on big-ticket UPI sales promised to rebalance profit pools and could reopen momentum for premium POS models in modern retail.

India POS Terminals Industry Leaders

Pine Labs Private Limited

One 97 Communications Limited (Paytm)

Worldline India Private Limited

Mswipe Technologies Private Limited

Innoviti Technologies Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Zaggle Prepaid Ocean Services acquired 51% of Effiasoft for Rs 41.31 crore, combining prepaid instruments with POS software to widen merchant services across India and Southeast Asia.

- March 2025: Paytm partnered with RBL Bank to deploy NFC-enabled soundbox devices and card machines that sync with the Paytm for Business dashboard, improving real-time reconciliation for merchants.

- January 2025: Pine Labs extended its 12-year alliance with SBI Payments to deepen acquiring services and seed more terminals through the bank’s network.

- December 2024: Worldline India and Forthcode launched Android POS for in-flight retail, integrating inventory and payment in a single cabin device.

India POS Terminals Market Report Scope

A point-of-sale terminal, commonly known as a POS terminal, is a hardware device utilized in retail stores to facilitate card payments. Equipped with software capable of reading both credit and debit card magnetic strips, modern POS systems are evolving to incorporate portable designs and contactless capabilities, catering to the rising trend of mobile payments.

India's POS terminals market is segmented by mode of payment acceptance (contact-based and contactless), type (fixed point-of-sale systems and mobile or portable point-of-sale systems), and end-user industry (retail, hospitality, healthcare, and other end-user industries). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

By Mode of Payment Acceptance

| Contact-based |

| Contactless |

By POS Type

| Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems |

By End-User Industry

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-user Industries |

| By Mode of Payment Acceptance | Contact-based |

| Contactless | |

| By POS Type | Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems | |

| By End-User Industry | Retail |

| Hospitality | |

| Healthcare | |

| Transportation and Logistics | |

| Other End-user Industries |

Key Questions Answered in the Report

How big is the India POS Terminals Market?

The India POS Terminals Market size is expected to grow at a CAGR of 11.30% to reach 70.39 billion units by 2031.

What is the current India POS Terminals Market size?

In 2026, the India POS Terminals Market size is expected to reach 41.27 billion units.

Who are the key players in India POS Terminals Market?

VeriFone, Inc., Worldline, Ezetap (Razorpay), MobiSwipe Technologies Private Limited and Mswipe Technologies Pvt Ltd. are the major companies operating in the India POS Terminals Market.

What years does this India POS Terminals Market cover, and what was the market size in 2025?

In 2025, the India POS Terminals Market size was estimated at 41.27 billion units. The report covers the India POS Terminals Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the India POS Terminals Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: