Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

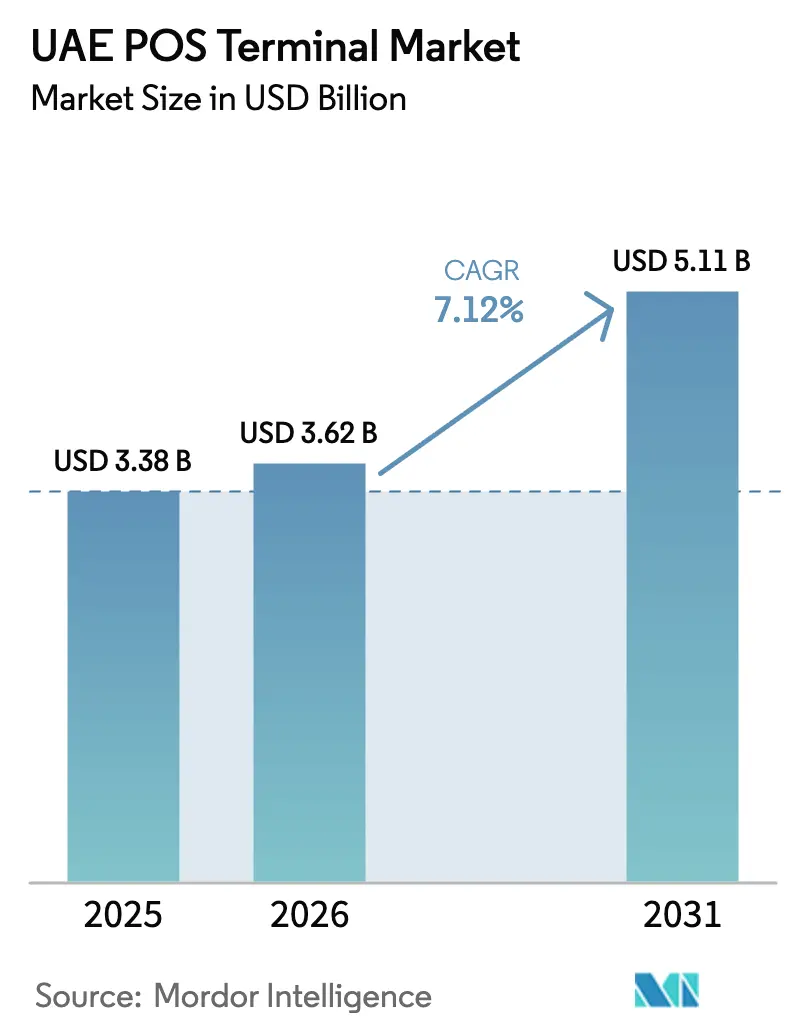

| Base Year Market Size (2025) | USD 3.38 Billion |

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 5.11 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

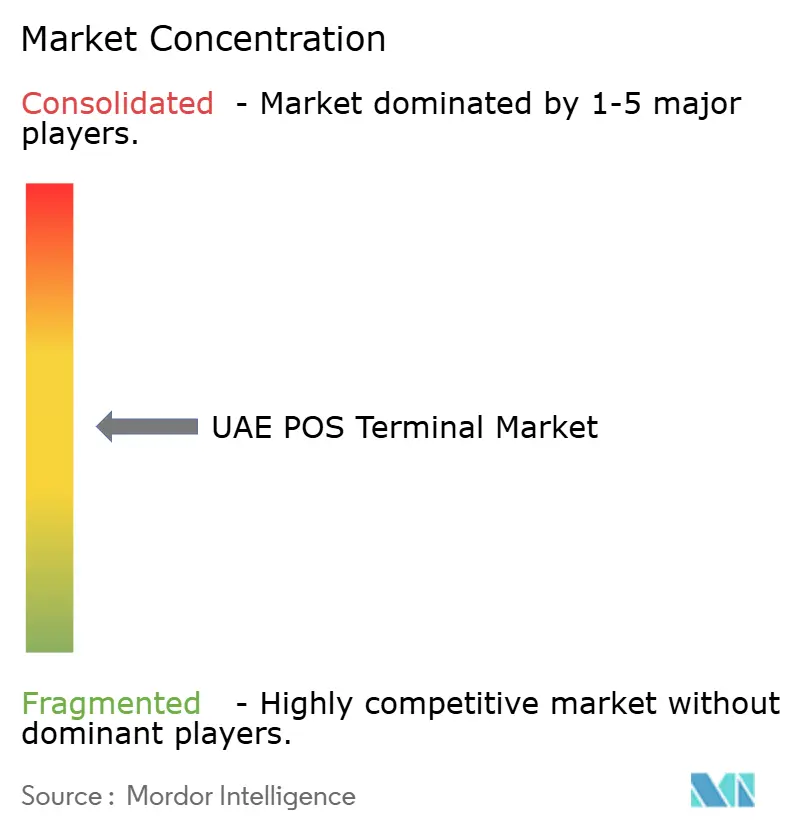

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE POS Terminal Market Analysis by Mordor Intelligence

The UAE POS Terminal market size was valued at USD 3.38 billion in 2025 and estimated to grow from USD 3.62 billion in 2026 to reach USD 5.11 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031). Rapid gains arise from Vision 2031’s cash-lite roadmap, the Central Bank’s Digital Dirham pilot, and steep shifts in consumer habits that pushed contactless penetration above 80% of all in-store transactions by 2024.[1]Central Bank of the UAE, “Digital Dirham Pilot Program Launch,” Central Bank of the UAE, centralbank.ae Government incentives, including VAT e-invoicing mandates and import-tariff relief for retail technology, stimulate merchant investments in next-generation terminals equipped with NFC, QR, and biometric authentication. Renewed tourism inflows and the return of global events bolster hospitality upgrades, while the rise of unattended retail from smart vending to autonomous convenience stores broadens the addressable base. Competitive dynamics pivot around Android-based form factors and cloud software that blend payments with inventory, analytics, and loyalty functions, positioning integrated solutions as the primary route to differentiation.

Key Report Takeaways

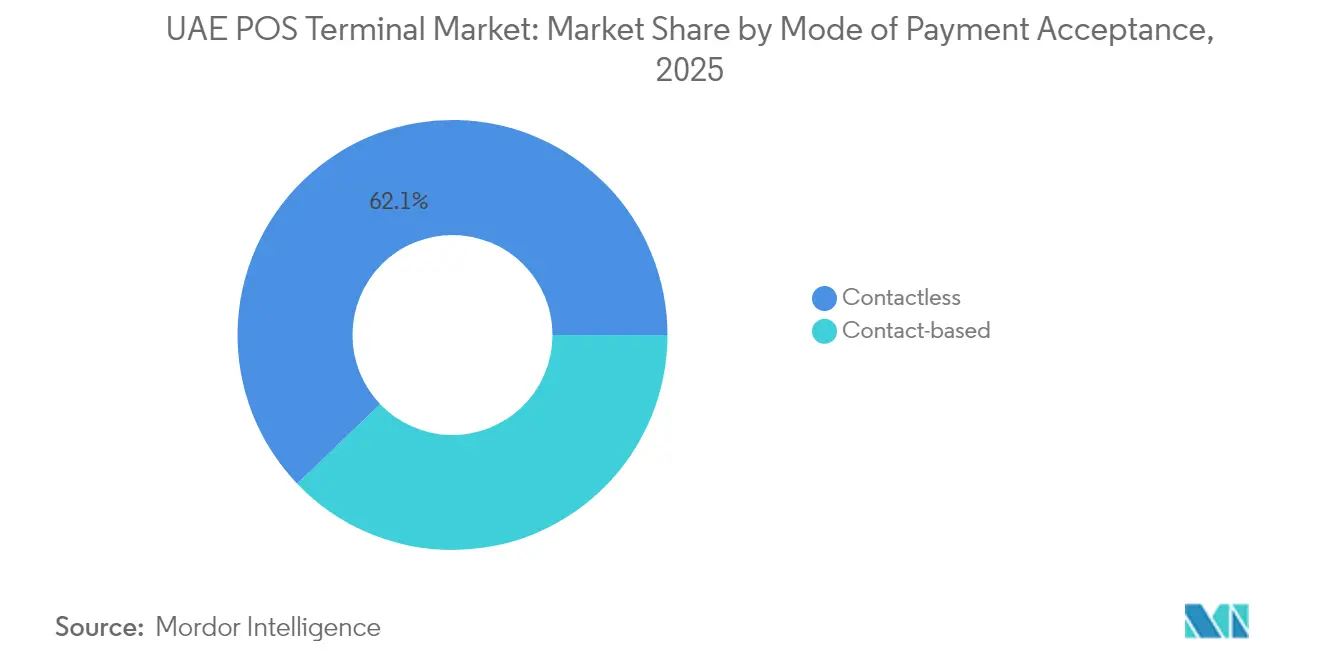

- By mode of payment acceptance, contactless systems held 62.15% of UAE POS Terminal market share in 2025, whereas mobile and portable solutions are projected to expand at 8.31% CAGR to 2031.

- By POS type, fixed terminals commanded 59.38% share of the UAE POS Terminal market size in 2025, while SoftPOS and other mobile variants deliver the fastest 8.33% CAGR between 2026-2031.

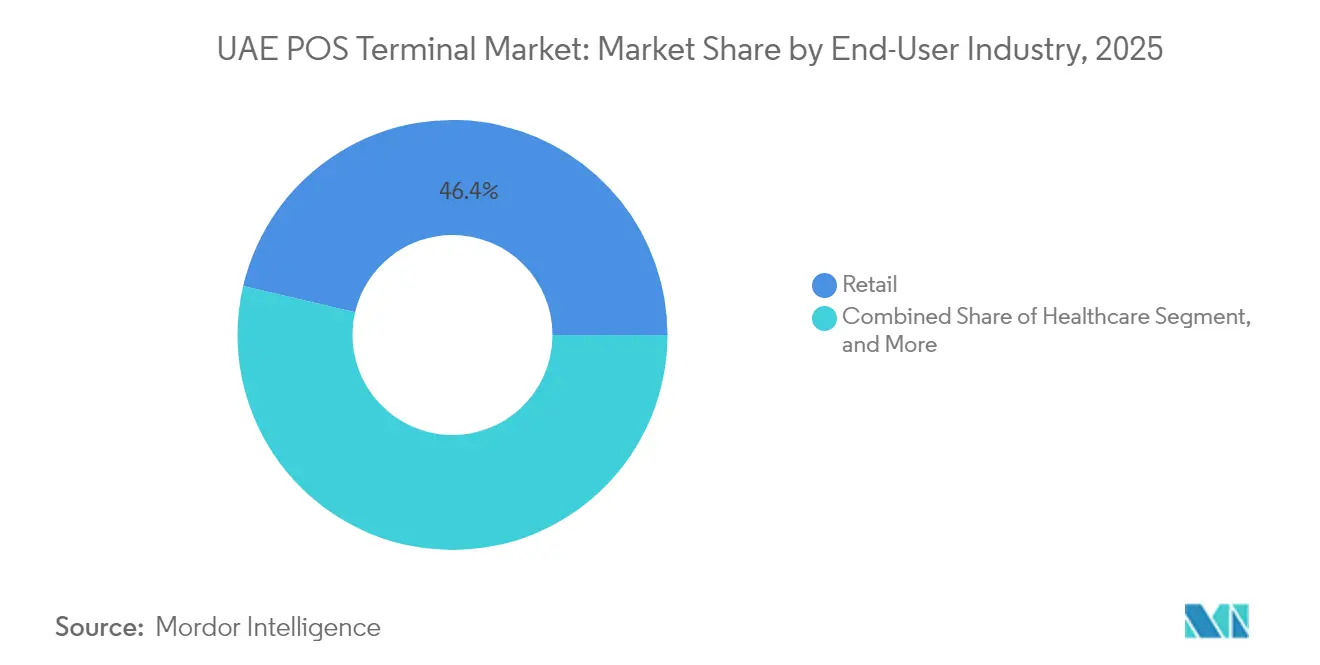

- By end-user industry, retail led with 46.35% revenue share in 2025 of the UAE POS Terminal market ; healthcare is advancing at the highest 8.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE POS Terminal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government cash-lite push (Vision 2031, CBUAE initiatives) | +1.8% | UAE-wide, strongest in Dubai and Abu Dhabi | Long term (≥ 4 years) |

| Contactless and mobile wallet boom post-COVID-19 | +2.1% | UAE-wide with spillover to broader GCC | Medium term (2-4 years) |

| Tourism rebound revitalising retail and hospitality POS demand | +1.4% | Dubai, Abu Dhabi, Northern Emirates tourism zones | Short term (≤ 2 years) |

| VAT e-invoicing mandates driving POS upgrades | +0.9% | UAE-wide, particularly affecting SMEs | Medium term (2-4 years) |

| Rise of unattended retail (smart vending, autonomous stores) | +0.6% | Dubai, Abu Dhabi urban centers | Long term (≥ 4 years) |

| Dubai retail-tech sandbox import-tariff incentives | +0.4% | Dubai with expansion to other Emirates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Cash-Lite Push Accelerates Infrastructure Modernization

The Vision 2031 agenda positions digital payments as a national backbone. More than 2.8 billion government transactions were completed electronically in 2024, a 340% jump over pre-pandemic volumes. Each new commercial license in Dubai now requires a POS terminal that supports NFC and QR, effectively locking in future demand. Abu Dhabi and Sharjah embed payment modules inside smart-city utilities, so transport, energy, and public-service kiosks adopt merchant-grade terminals rather than mechanical meters. This state-directed overhaul widens margins for suppliers qualifying early under UAE Switch and EMVCo rules. Vendors able to localize Arabic interfaces and integrate the Digital Dirham API secure priority access to tenders that will roll out over the coming decade.

Contactless Payment Surge Reshapes Terminal Specifications

Contactless transaction counts spiked from 1.2 billion in 2020 to 4.7 billion in 2024. NFC capability, therefore, shifted from optional to mandatory, while dual-antenna designs that serve both card tap and QR code scanning became the default. Mobile wallet usage reached 78% among residents, and PayBy alone processed USD 12 billion in 2024.[2]PayBy, “Annual Transaction Report 2024,” PayBy, payby.com As a result, merchants replace legacy units in favor of devices that bundle Apple Pay, Samsung Pay, and region-specific wallets under one SDK. The upgrade cycle also tilts pricing upward because enhanced encryption and PCI PTS 6.x certification add hardware cost yet remain non-negotiable for acquirers. Demand extends into B2B contexts, fuel depots, clinics, and government counters, where badge-based tap solutions streamline user verification.

Tourism Recovery Fuels Hospitality POS Modernization

International arrivals recovered to 17.15 million in 2024, revitalizing duty-free, luxury retail, and hotel F&B outlets. Visitors expect frictionless payments in home currencies, so hotels deploy multi-currency dynamic conversion plus Alipay and UnionPay acceptance. Operators cut queuing by rolling out portable POS tablets for tableside check-out, upselling spa or excursion bookings in a single tap. Mall anchors invest in customer-relationship management modules baked into terminals, enabling in-store staff to access loyalty history during payment. Expo City legacies and new leisure projects in Ras Al Khaimah widen geographic demand, increasing shipment volumes for water-resistant and outdoor-rated units suitable for beach clubs, golf courses, and marinas.

VAT E-Invoicing Compliance Mandates System Upgrades

Real-time e-invoicing became compulsory in 2024, obliging every taxable entity to transmit transaction data to the Federal Tax Authority. Small merchants rush to replace cash registers with cloud POS terminals that issue digital receipts and file VAT concurrently. Compliance spending ranges from AED 15,000 (USD 4,080) to AED 50,000 (USD 13,600), depending on site complexity. Suppliers answer with subscription bundles that wrap hardware, e-invoicing software, and 24-hour support, smoothing cash flow for micro-retailers. Payment gateways leverage the regulation to upsell value-added modules such as digital bookkeeping and inventory sync, raising average revenue per merchant and locking in multi-year contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and data-privacy vulnerabilities | -1.2% | UAE-wide, heightened in financial districts | Medium term (2-4 years) |

| High upfront device and service costs for micro-merchants | -0.8% | UAE-wide, particularly affecting SMEs | Short term (≤ 2 years) |

| Fragmented EMVCo / UAESWITCH certification process | -0.7% | UAE-wide, affecting all POS deployments | Medium term (2-4 years) |

| Semiconductor shortages extending POS lead-times | -0.5% | Global impact with UAE market effects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Vulnerabilities Constrain Market Expansion

The National Cybersecurity Strategy 2031 enforces stringent PCI DSS and tokenization rules, raising deployment cost by 15-25%. Smaller hotels and neighborhood grocers hesitate to migrate because quarterly penetration testing and mandatory log retention inflate operating overhead. High-profile breaches in regional acquirers during 2024 fueled risk aversion, pushing some merchants to keep offline ECRs for fallback. Compliance varies across emirates, so multi-branch chains must reconcile Abu Dhabi’s Data Management Standards with Dubai’s Smart City protocols, driving demand for centralized security orchestration, an expense that compresses margin unless scale offsets exist.

Cost Barriers Limit Micro-Merchant Participation

Entry-level POS bundles price between AED 2,000 (USD 544) and AED 5,000 (USD 1,360), a steep outlay for kiosks turning under AED 50,000 monthly revenue.[3]Dubai SME, “Small Business Development Report 2024,” Dubai SME, dubaisme.gov.aeTransaction fees of 1.5-3.5% plus AED 120 rental further erode thin margins. Most micro-merchants lack collateral for bank leasing, and fintech financiers charge risk premiums that neutralize any savings. Confusing tiered pricing across acquirers prolongs decision cycles past 90 days, delaying fleet expansion. Without scale, suppliers struggle to stock inventory, making it harder to drive the UAE POS Terminal market deeper into informal retail.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment Acceptance: Contactless Dominance Accelerates

Contactless systems captured 62.15% UAE POS Terminal market share in 2025 and are projected to grow at 9.08% CAGR, underscoring a decisive consumer tilt toward tap-and-go convenience. Government decrees obligate new merchants to adopt NFC and QR capability, consolidating demand for hybrid terminals that read multiple tags in sub-400 ms. The UAE POS Terminal market size derived from contactless hardware alone is set to surpass USD 3.07 billion by 2031 as portable kiosks, parking meters, and event ticket scanners all converge on uniform acceptance stacks. Demand also stems from high-value retail, where biometric-secured taps ease fraud concerns without compromising shopping ambience. Import-tariff exemptions granted under Dubai’s sandbox shorten payback cycles, encouraging retailers to refresh fleets every three years rather than five. As wearable payments spread, terminal makers embed BLE beacons to auto-detect smartwatches, nudging incremental hardware revenues.

In contrast, chip-and-pin remains relevant for luxury automotive, fine jewelry, and B2B transfers that exceed soft limits. These niches demand encrypted PIN pads and rear-facing customer screens, adding complexity but maintaining ASPs. Dual-interface cards enable fallback, so manufacturers supply all-in-one devices that auto-switch between contact and contactless modes. Over the forecast horizon, the UAE POS Terminal market will see contactless attach rates inside fixed terminals jump from 87% to near-universal coverage, leaving mag-stripe support only for tourist-heavy outlets.

By POS Type: Mobile Solutions Gain Momentum

Fixed setups retained 59.38% of UAE POS Terminal market size in 2025 on the back of large-footprint retailers and hotels that demand integrated CRM, inventory, and analytics dashboards. Yet shipment growth flattens as omni-channel operators pivot to curbside pick-up, click-and-collect, and delivery orchestration. Portable devices therefore post the quickest 8.33% CAGR, with SoftPOS allowing any Android 8.0+ handset to double as a payment reader. This software-only model slashes hardware outlay for seasonal merchants, juice bars, and independent couriers, unlocking fresh pockets of volume previously boxed out by cost hurdles.

Cloud POS vendors capitalize by bundling inventory sync, staff scheduling, and AI-driven demand forecasting, pushing average software ARPU to USD 35 monthly. The UAE POS Terminal market now witnesses hybrid rollouts where high-traffic cashiers rely on countertop workstations, while roaming sales associates check out shoppers via pocket-POS devices at busy times. Battery life, cellular redundancy, and tamper detection emerge as critical spec lines, steering R&D budgets into power-efficient chipsets and rugged casings that survive desert heat.

By End-User Industry: Healthcare Leads Growth Velocity

Retail accounted for 46.35% of overall shipments in 2025, thanks to Dubai’s dominant mall ecosystem and Abu Dhabi’s duty-free corridors. Chains integrate endless-aisle and digital signage controls into their POS stacks, capturing shopper data across touchpoints. Hospitality follows closely; hotels deploy multi-language interfaces and PMS integration to unify room, restaurant, and spa charges under a single folio. However, healthcare is projected to log the sharpest 8.21% CAGR through 2031, buoyed by the Ministry of Health mandates that every public clinic accept electronic payments. Hospitals seek terminals that pair with electronic medical records, insurance portals, and biometric patient IDs to cut administrative friction.

The UAE POS Terminal market share within healthcare is rising off a small base but gains momentum as private networks replicate public-sector digitization. Pharmacies introduce drive-thru lanes equipped with outdoor-rated readers, while telehealth providers integrate pay-by-link to sync co-pays automatically. Secondary verticals transport, education, and public utilities adopt sector-specific add-ons such as NFC season pass renewal and tuition installment tracking, broadening consumption beyond core retail.

Geography Analysis

Dubai and Abu Dhabi together contributed roughly three-quarters of UAE POS Terminal market value in 2025, reflecting their dense merchant footprints and proactive digitization policies. Dubai’s tourist hotspots demand high-end terminals supporting multi-currency settlement, UnionPay, and Alipay, while its fashion flagships adopt CRM-ready readers that surface customer profiles in real time. Abu Dhabi channels hydrocarbon surpluses into smart-city grids; utility counters accept Digital Dirham, and municipal parking meters feature solar-powered NFC pads, lifting institutional demand.

In the Northern Emirates, Sharjah harnesses its manufacturing base to deploy industrial POS nodes across factory canteens and logistics hubs, whereas Ras Al Khaimah’s resort pipeline fuels hospitality demand. Ajman and Umm Al Quwain modernize traditional souks with shared SoftPOS schemes backed by micro-finance, broadening penetration but at lower avg. selling prices. Free-zone frameworks such as DIFC and ADGM introduce bespoke compliance layers that favor vendors with ready cross-border certification.

Blockchain-enabled identity initiatives under Dubai’s Paperless Strategy prompt a forthcoming wave of terminals featuring secure element chips for decentralized ID verification. These pilots position the UAE POS Terminal market as a live laboratory for next-gen payment stacks, attracting global fintechs keen on GCC expansion.

Competitive Landscape

Global majors Ingenico, Verifone, and PAX Technology collectively command the upper end of the UAE POS Terminal market, leveraging mature logistics, local repair hubs, and bilingual firmware. Regional champions Magnati and PayBy exploit domestic settlement rails to undercut international interchange rates, winning share among mid-sized retailers and government agencies. Fragmentation intensifies in cloud software, where at least 30 vendors compete on vertical specificity, margin management, and local language UX.

Hardware rivalry converges on Android OS adoption, letting suppliers tap larger developer ecosystems and roll out app stores dedicated to loyalty, analytics, and workforce optimization. Biometrics fingerprint, facial, and palm vein, feature prominently in jewelry, health, and high-risk retail, offering elevated ASPs and service revenue. Entry of SoftPOS disrupts hardware refresh cycles, so incumbents pivot into SaaS, offering estate management and security subscriptions that offset unit erosion.

Certification speed acts as a moat: early EMVCo L3 and UAESWITCH approvals shorten time-to-market, while in-country service centers remain pivotal given desert operating conditions. Vendors differentiating on cybersecurity, localized reporting, and voice-enabled checkout stand to capture incremental UAE POS Terminal market share as omni-channel commerce deepens.

UAE POS Terminal Industry Leaders

Ingenico Group SA

Verifone Systems Inc.

PAX Technology Limited

Diebold Nixdorf Incorporated

BBPOS Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: PayBy launched QR-enabled POS terminals with instant payment links, cutting checkout time by 40% and targeting SME rollouts across Dubai and Abu Dhabi.

- September 2024: Magnati partnered with Sheikh Shakhbout Medical City to equip 200 biometric-ready terminals integrated with insurance claim workflows.

- August 2024: The Central Bank commenced Digital Dirham pilots, requiring participating merchants to deploy CBDC-capable POS readers in 50 locations.

- July 2024: Network International installed 500 unattended POS units across Dubai Metro stations and malls, supporting smart vending and autonomous stores.

UAE POS Terminal Market Report Scope

The POS Terminals market captures revenues accumulated from hardware, software, and services that manages the transaction during the sale of a product or a service. It helps to store, capture, share, and report data related to the sales transaction.

It eases the shopping experience and helps to expedite the checkout process, resulting in customer satisfaction. Inventory management, stock in hand, availability of a product, and pricing information are primary data that are acquired from the systems.

The various end-user industries considered in the scope include entertainment, retail, healthcare, hospitality, among others. The impact of COVID-19 on the market and affected segments is also covered under the scope of the study.

By Mode of Payment Acceptance

| Contact-based |

| Contactless |

By POS Type

| Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems |

By End-User Industry

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-User Industries |

| By Mode of Payment Acceptance | Contact-based |

| Contactless | |

| By POS Type | Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems | |

| By End-User Industry | Retail |

| Hospitality | |

| Healthcare | |

| Transportation and Logistics | |

| Other End-User Industries |

Key Questions Answered in the Report

How large is the UAE POS Terminal market in 2026?

The UAE POS Terminal market size reaches USD 3.62 billion in 2026 and is on track for USD 5.11 billion by 2031.

What CAGR is predicted for UAE POS terminals to 2031?

Shipments and revenue are forecast to rise at a steady 7.12% CAGR through 2031.

Which acceptance mode leads UAE shipments?

Contactless systems dominate with 62.15% share in 2025 and remain the chief growth engine.

Why is healthcare the fastest-growing end-user?

Ministry-mandated electronic payments and integration with patient records drive an 8.21% CAGR for healthcare terminals.

How does SoftPOS impact micro-merchant adoption?

By turning standard smartphones into certified readers, SoftPOS reduces hardware costs to near zero, easing entry barriers for small retailers.

What cybersecurity rules affect POS deployments?

The National Cybersecurity Strategy 2031 and PCI DSS audits impose stricter encryption, monitoring, and tokenization across all terminals.

Page last updated on: