Molecular Diagnostics For Emerging Infectious Diseases Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

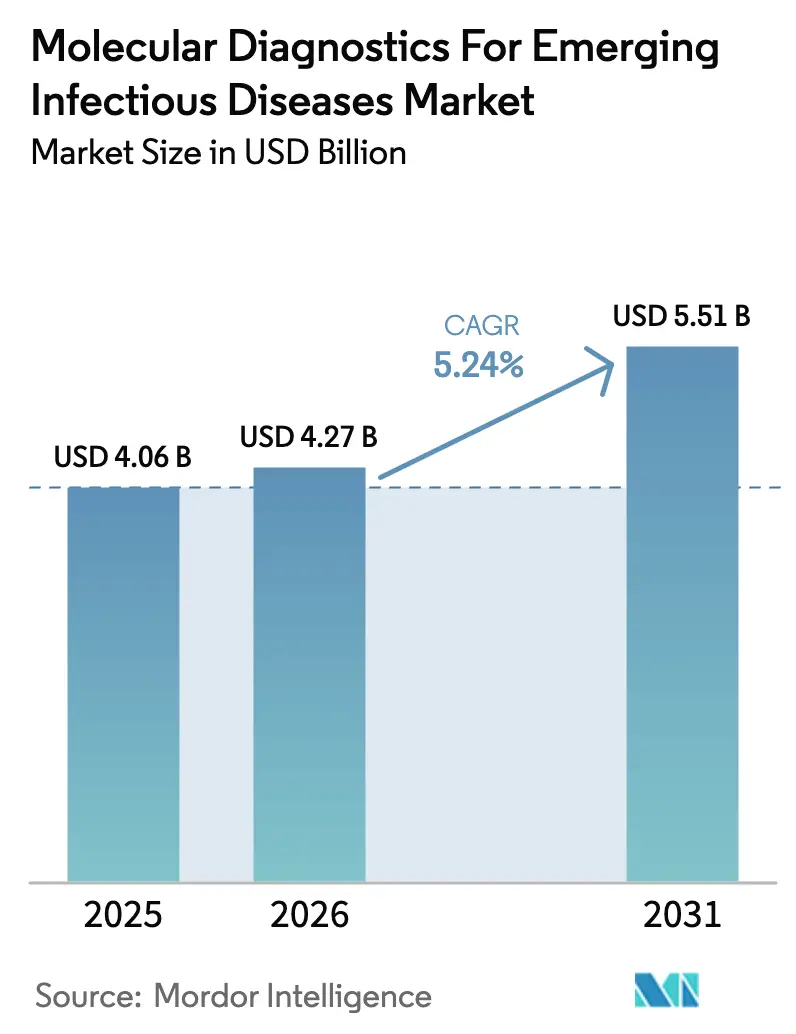

| Market Size (2026) | USD 4.27 Billion |

| Market Size (2031) | USD 5.51 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

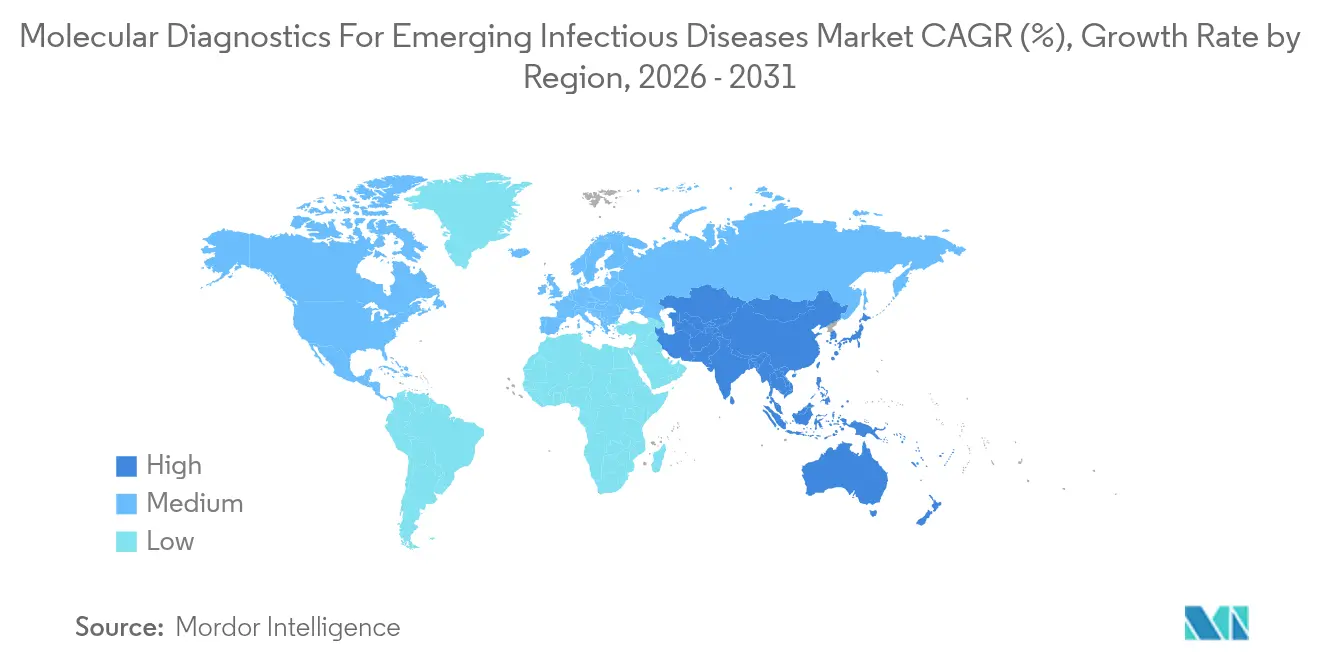

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Molecular Diagnostics For Emerging Infectious Diseases Market Analysis by Mordor Intelligence

The molecular diagnostics for emerging infectious disease market size in 2026 is estimated at USD 4.27 billion, growing from 2025 value of USD 4.06 billion with 2031 projections showing USD 5.51 billion, growing at 5.24% CAGR over 2026-2031. Sustained government spending on pandemic-preparedness programs keeps demand stable even as the COVID-19 surge recedes. Uptake of syndromic panels, non-invasive sample collection, and data-rich reporting tools pushes laboratories toward platform-integrated solutions. CRISPR-enabled assays and rapid next-generation sequencing shorten time-to-result, while wastewater surveillance broadens the testing footprint. Strong patent activity and cross-sector partnerships underscore the need for flexible systems that can pivot quickly to new threats.

Key Report Takeaways

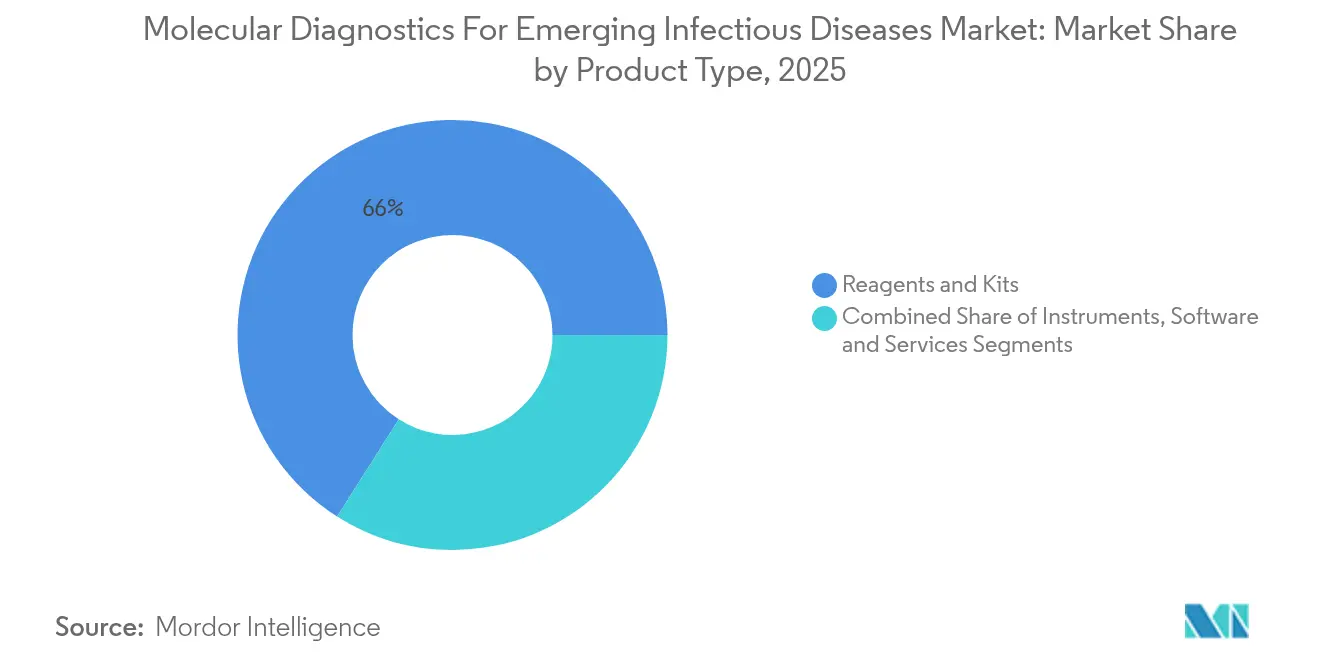

- By product type, reagents and kits held 65.98% of the molecular diagnostics for emerging infectious disease market share in 2025, whereas software and services are advancing at a 12.78% CAGR through 2031.

- By technology, PCR led with 40.12% revenue share in 2025; CRISPR-based platforms are forecast to expand at a 14.21% CAGR to 2031.

- By sample type, respiratory swabs accounted for 44.05% of the molecular diagnostics for emerging infectious disease market size in 2025, while saliva and oral fluids show a 13.22% CAGR outlook.

- By pathogen type, viral segment accounted for 63.77% share of the market size in 2025; novel / unknown pathogens are expected to climb at 17.36% CAGR through 2031.

- By end user, hospitals & clinics held 41.74% revenue share in 2025, whereas public health agencies are forecast to grow at 12.61% CAGR between 2026 and 2031.

- By application, pathogen detection led with 74.65% of the market share in 2025, while syndromic panels are projected to compound at 14.39% CAGR to 2031.

- By geography, North America captured 38.91% share in 2025; Asia-Pacific is growing fastest at a 9.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Molecular Diagnostics For Emerging Infectious Diseases Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Outbreaks Of Zoonotic & Vector-Borne Diseases | +1.2% | Global, with higher impact in APAC and Africa | Medium term (2-4 years) |

| Acceleration Of Pandemic-Preparedness Funding Pipelines | +0.8% | North America & EU, spill-over to emerging markets | Short term (≤ 2 years) |

| Rapid-Turnaround NGS & Digital PCR Platforms | +0.9% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Decentralized Point-Of-Care (POC) Deployment In Low-Resource Settings | +1.1% | APAC, Africa, Latin America | Long term (≥ 4 years) |

| Wastewater-Based Molecular Surveillance Roll-Outs | +0.7% | Global, with focus on urban centers | Medium term (2-4 years) |

| AI-Assisted Assay Design Reducing Time-To-Market | +0.6% | Global, concentrated in R&D hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in outbreaks of zoonotic & vector-borne diseases

Frequent mpox, avian influenza, and arboviral flare-ups raise the need for rapid multiplex detection across clinical and field settings. The WHO’s 2024 mpox alert spotlighted diagnostic gaps in low-resource regions, prompting investment in biosensor technologies that deliver results in 20 minutes and support proactive surveillance[1]bioMérieux Editors, “Global Response to the 2024 Mpox Outbreak: Need for Enhanced Diagnostics and Equitable Resource Distribution,” bioMerieux.com. Platforms that screen multiple zoonotic threats at once shorten response time and help prevent global spread.

Acceleration of pandemic-preparedness funding pipelines

The United States set aside USD 176 million in 2024 and another USD 211 million in 2025 to fast-track flexible test platforms, while the multilateral Pandemic Fund committed USD 500 million to expand regional manufacturing[2]U.S. Federal Register, “Validation of Certain In Vitro Diagnostic Devices for Emerging Pathogens,” federalregister.gov. These allocations favor companies able to swap assay targets quickly, reinforcing demand for modular instruments and cloud-enabled analytics.

Rapid-turnaround NGS & digital PCR platforms

Metagenomic NGS now validates at 93.6% sensitivity for respiratory pathogens, with results in hours rather than days[3]Tan J.K. et al., “Laboratory Validation of a Clinical Metagenomic NGS Assay,” medrxiv.org. Digital PCR adds precise viral-load quantification, improving treatment decisions and variant tracking. Converging workflows that blend NGS, digital PCR, and resistance profiling optimize laboratory throughput and clinical impact.

Decentralized point-of-care deployment in low-resource settings

Cartridge-based systems integrate extraction, amplification, and detection for under USD 1 per test, achieving >95% sensitivity. Real-time cloud uploads give clinicians and public-health officials rapid situational awareness. Community-level networks using these devices detect outbreak signals early, especially valuable where central labs are distant.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Per-Test Costs Of Advanced MDx | -0.9% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Complex & Evolving Regulatory Frameworks | -0.7% | Global, varying by jurisdiction | Medium term (2-4 years) |

| Enzyme/Oligonucleotide Supply-Chain Volatility | -0.5% | Global, concentrated in specialized suppliers | Short term (≤ 2 years) |

| Genomic-Data Privacy & Biosecurity Concerns | -0.4% | Global, stricter in EU and developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capital & per-test costs of advanced MDx

Reagent inflation and tight reimbursement widen the gap between test cost and payment. New U.S. fee schedules under gap-fill rules often trail real expenses, and multiplex panels can exceed USD 200 per sample. Laboratories hesitate to extend menus without clarity on cost recovery.

Complex & evolving regulatory frameworks

The FDA will phase in oversight of laboratory-developed tests over four years, introducing new premarket reviews and documentation. Lawsuits and divergent global rules demand duplicated pathways, straining smaller providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services accelerate platform integration

Reagents and kits commanded 65.98% of the molecular diagnostics for emerging infectious disease market in 2025. Software and services, though smaller, are rising at a 12.78% CAGR as laboratories prefer turnkey packages that fuse testing hardware with analytics dashboards and cyber-security layers.

Laboratories adopting the BIOFIRE FILMARRAY TORCH cut hands-on time to minutes while securing automated quality control. Vendors earn recurring revenue by bundling consumables, informatics, and remote support into subscription contracts that ease capital pressure and ensure instrument uptime.

By Technology: CRISPR transforms detection

PCR retained 40.12% share in 2025, yet CRISPR assays are scaling at 14.21% CAGR on the strength of sequence-agnostic detection and portable formats. The molecular diagnostics for emerging infectious disease market size for CRISPR solutions is forecast to expand quickly as regulatory clearances accumulate.

Isothermal methods such as LAMP bridge resource gaps, while next-generation sequencing and nanopore workflows provide full genomic snapshots for surveillance. Combined, these alternatives chip away at PCR’s dominance and encourage laboratories to diversify portfolios for speed, breadth, and resilience.

By Sample Type: Non-invasive collection gains ground

Respiratory swabs delivered 44.05% of the molecular diagnostics for emerging infectious disease market size in 2025. Saliva and oral fluids, growing at 13.22% CAGR, improve patient comfort and reduce exposure risk for healthcare staff.

Wastewater testing adds community-level insight, detecting pathogen trends before clinical case spikes. Innovations in inhibitor removal and rapid concentration shorten processing time, widening adoption in municipal monitoring programs.

By Pathogen Type: Novel threats spur broad-spectrum assays

Viral agents held 63.77% share in 2025, yet assays for unknown pathogens are advancing fastest at 17.36% CAGR as stakeholders prioritize future-proof platforms. The molecular diagnostics for emerging infectious disease market welcomes metagenomic screens that flag unexpected organisms and resistance genes in a single run.

Bacterial, fungal, and parasitic panels remain essential for targeted infections but see steadier growth. AI-guided primer design and adaptive bioinformatics help test makers stay ready for the next novel threat.

By Application: Syndromic panels reshape workflows

Pathogen detection made up 74.65% of revenue in 2025. Syndromic panels, however, are scaling at 14.39% CAGR by delivering 20-plus targets in under an hour and guiding therapy at first encounter.

Hospitals gain operational efficiency, while public-health programs benefit from real-time data streams that integrate with surveillance dashboards. Resistance testing and biothreat panels expand these gains into antimicrobial stewardship and security domains.

By End-User: Public-health demand surges

Hospitals and clinics represented 41.74% of consumption in 2025, but public-health agencies are rising at a 12.61% CAGR as governments fund regional hubs and mobile labs. The molecular diagnostics for emerging infectious disease market thus leans toward high-throughput instruments able to flex from routine workflows to surge capacity during emergencies.

Academic centers continue to drive discovery and validation, feeding novel assays into commercial channels. Diagnostic laboratories remain critical for quality assurance and large-scale testing services.

Geography Analysis

North America captured 38.91% revenue in 2025 on the back of strong reimbursement, integrated electronic records, and swift translation of R&D outputs into clinical tools. FDA rules on emergency use and LDT oversight guide quality while challenging smaller entrants. Continued public-private funding partnerships underpin steady platform upgrades.

Europe shows steady demand amid budget pressures and the implementation of IVDR. Harmonized standards lift quality, yet compliance costs favor well-capitalized suppliers. Personalized-medicine initiatives sustain high-complexity testing, and national procurement programs keep price competition tight.

Asia-Pacific posts the fastest regional CAGR of 9.74%, fueled by health-system expansion, rising awareness, and state support for biotech manufacturing. China’s investments in domestic platforms increase self-reliance, while Japan’s aging population drives sophisticated pathogen panels. India’s broad disease burden encourages hybrid models mixing centralized labs and point-of-care devices.

Competitive Landscape

The molecular diagnostics for emerging infectious disease market features moderate fragmentation. Roche, Abbott, and Thermo Fisher Scientific leverage broad menus, global channels, and regulatory depth to defend share. Service contracts and middleware analytics differentiate offers and lock in consumable revenue.

Specialists including Sherlock Biosciences and Oxford Nanopore Technologies push disruptive models such as CRISPR and portable sequencing. Larger firms respond by acquiring capabilities, exemplified by Bruker’s EUR 870 million purchase of Elitech, which widened its European footprint and infectious-disease portfolio.

Partnerships between diagnostics and pharmaceutical companies accelerate companion-diagnostic development, weaving testing into therapeutic decision paths. AI collaboration agreements shorten design cycles and tailor panels to local epidemiology, intensifying competitive dynamics without a single player dominating revenue.

Molecular Diagnostics For Emerging Infectious Diseases Industry Leaders

Thermo Fisher Scientific, Inc.

F. Hoffmann-La Roche Ltd

Abbott Laboratories

Illumina Inc.

bioMérieux SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: FDA issued draft guidance on validation requirements for in vitro diagnostic devices aimed at emerging pathogens during Section 564 emergencies, streamlining future rapid-test clearances.

- May 2024: Bruker completed its EUR 870 million acquisition of Elitech Group, adding molecular platforms and enlarging its European base.

Global Molecular Diagnostics For Emerging Infectious Diseases Market Report Scope

According to the scope, emerging infectious diseases (EIDs) are diseases caused by newly discovered pathogens or those that have notably risen in frequency or expanded their geographical distribution, such as COVID-19, antimicrobial resistant tuberculosis and malaria, among others. Molecular diagnostics for emerging infectious diseases utilize advanced technologies to detect, identify, and monitor pathogens at the molecular level, focusing on specific DNA or RNA sequences, such as single nucleotide polymorphisms (SNPs), deletions, rearrangements, insertions, and more, that are associated with various diseases.

The molecular diagnostics for emerging infectious diseases market is segmented by product type, technology, application, end-user and geography. By product type, the market is segmented into instruments, reagents and kits and other product types. By technology, the market is segmented into in-situ hybridization, chips and microarrays, mass spectrometry, sequencing, polymerase chain reaction (PCR), and other technologies. By application, the market is segmented into pathogen detection, antimicrobial resistance testing, syndromic testing and other applications. By end-user, the market is segmented into hospitals and clinics, diagnostics laboratories, research institutes and other end-user. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market size is provided in terms of USD value.

| Instruments |

| Reagents & Kits |

| Software & Services |

| PCR (Conventional, qPCR, Digital) |

| Isothermal Amplification (LAMP, INAAT) |

| Next-Generation Sequencing & Nanopore |

| CRISPR-based Diagnostics |

| Mass Spectrometry |

| Microarrays & Chips |

| Respiratory Swabs |

| Blood/Plasma |

| Saliva & Oral Fluids |

| Stool & GI Samples |

| Wastewater & Environmental |

| Viral |

| Bacterial |

| Fungal |

| Parasitic |

| Novel / Unknown Pathogens |

| Pathogen Detection |

| Antimicrobial Resistance (AMR) Testing |

| Syndromic Panels |

| Surveillance & Epidemiology |

| Multiplexed Biothreat Detection |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Public Health Agencies |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Instruments | |

| Reagents & Kits | ||

| Software & Services | ||

| By Technology | PCR (Conventional, qPCR, Digital) | |

| Isothermal Amplification (LAMP, INAAT) | ||

| Next-Generation Sequencing & Nanopore | ||

| CRISPR-based Diagnostics | ||

| Mass Spectrometry | ||

| Microarrays & Chips | ||

| By Sample Type | Respiratory Swabs | |

| Blood/Plasma | ||

| Saliva & Oral Fluids | ||

| Stool & GI Samples | ||

| Wastewater & Environmental | ||

| By Pathogen Type | Viral | |

| Bacterial | ||

| Fungal | ||

| Parasitic | ||

| Novel / Unknown Pathogens | ||

| By Application | Pathogen Detection | |

| Antimicrobial Resistance (AMR) Testing | ||

| Syndromic Panels | ||

| Surveillance & Epidemiology | ||

| Multiplexed Biothreat Detection | ||

| By End-User | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Public Health Agencies | ||

| Academic & Research Institutes | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the molecular diagnostics for emerging infectious disease market?

The market is valued at USD 4.27 billion in 2026.

How fast is the market expected to grow?

It is projected to grow at a 5.24% CAGR, reaching USD 5.51 billion by 2031.

Which product segment is expanding the quickest?

Software and services are advancing at a 12.78% CAGR as laboratories adopt integrated platforms.

Which technology is gaining ground on PCR?

CRISPR-based diagnostics are the fastest-growing technology segment at 14.21% CAGR.

Why is Asia-Pacific considered the key growth region?

Government investment in biotech manufacturing and expanding healthcare access underpin a regional CAGR of 9.74%.

What restrains wider adoption of advanced molecular tests?

High per-test costs and evolving regulatory requirements limit rapid deployment, particularly in emerging markets.

Page last updated on: