Thermoset Molding Compound Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

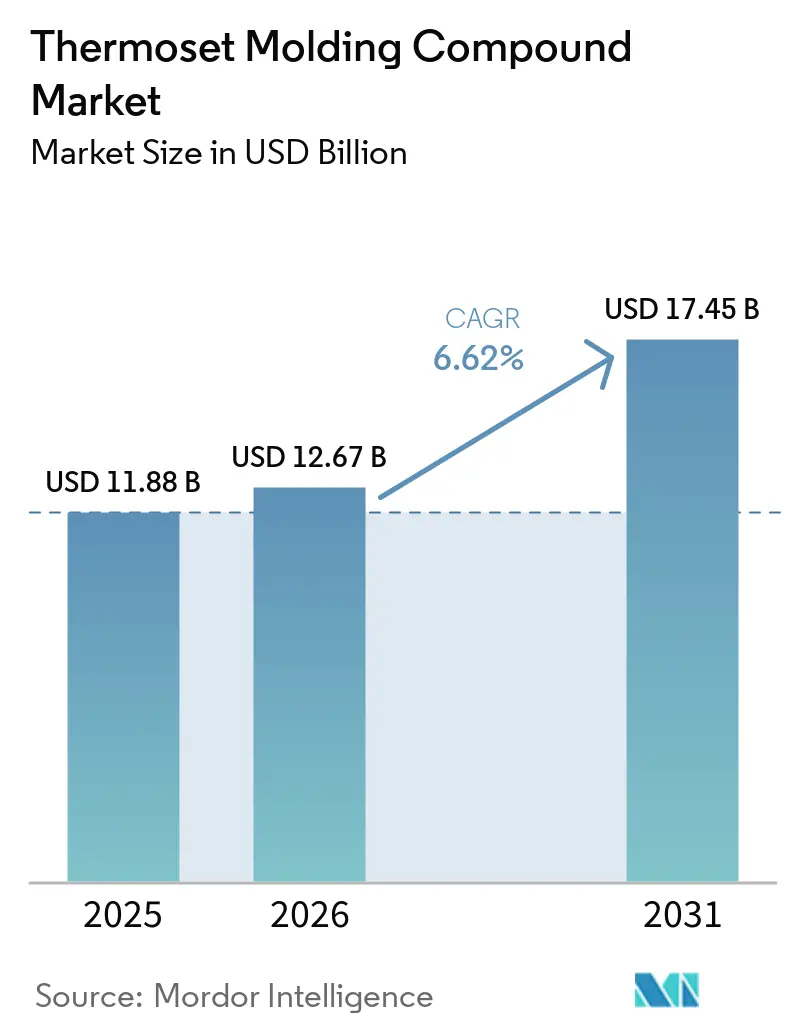

| Market Size (2026) | USD 12.67 Billion |

| Market Size (2031) | USD 17.45 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermoset Molding Compound Market Analysis by Mordor Intelligence

The Thermoset Molding Compound Market size is projected to be USD 11.88 billion in 2025, USD 12.67 billion in 2026, and reach USD 17.45 billion by 2031, growing at a CAGR of 6.62% from 2026 to 2031. Rising demand for miniaturized 5G electronics, electric-vehicle (EV) lightweighting, and offshore wind-turbine blades is steering formulators toward high-performance epoxy and low-emission phenolic chemistries. Rapid-cure prepregs that trim autoclave cycles by 40%, hybrid fillers that lift thermal conductivity above 0.80 W/m/K, and bio-carbon content exceeding 15% are redefining value propositions for sustainability-minded OEMs (Original Equipment Manufacturers). Trade barriers on Chinese epoxy and formaldehyde exposure limits under the EPA (Environmental Protection Agency) TSCA (Toxic Substances Control Act) are simultaneously tightening supply and catalyzing regional resin investments in India, Mexico, and Southeast Asia. Venture funding for dynamic-covalent vitrimer networks, although embryonic, signals that recyclability breakthroughs could materially alter disposal economics after 2030.

Key Report Takeaways

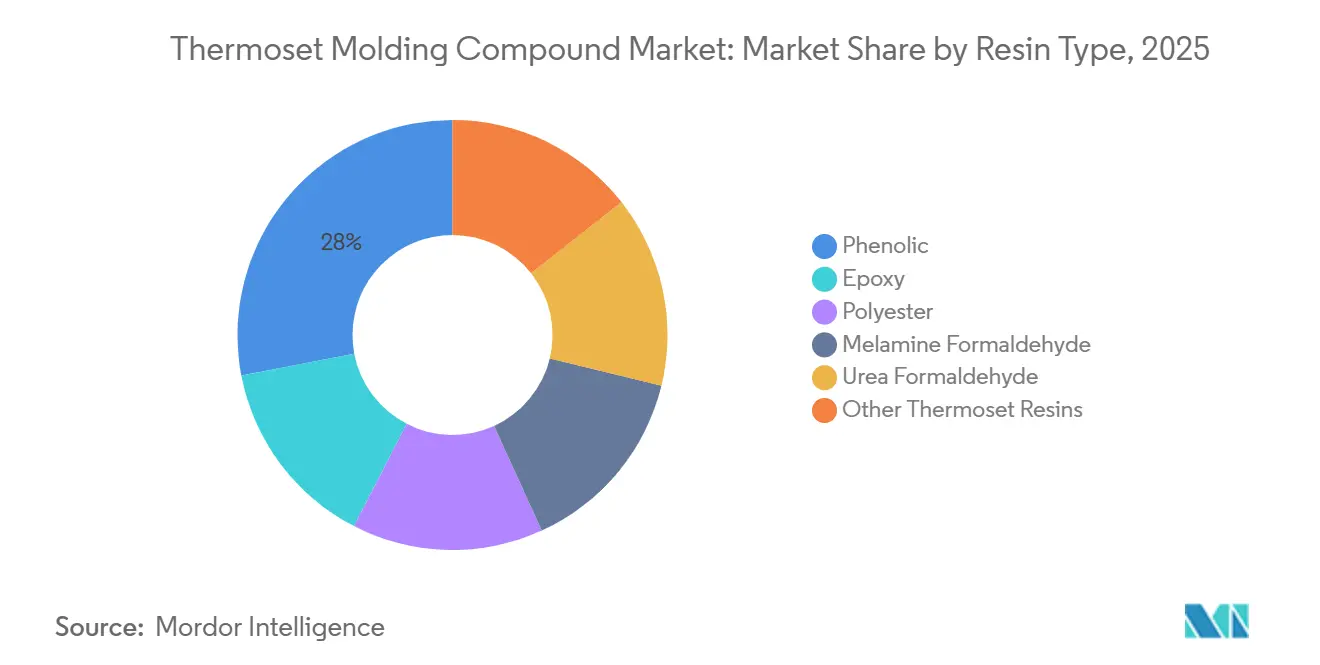

- By resin type, phenolic resins commanded 28.02% share of the Thermoset Molding Compound market size in 2025, while epoxy compounds are advancing at a 7.02% CAGR through 2031.

- By fiber reinforcement, glass fiber accounted for 63.63% of the Thermoset Molding Compound market size in 2025; carbon fiber reinforcement is expanding at a 7.34% CAGR over the forecast period (2026-2031).

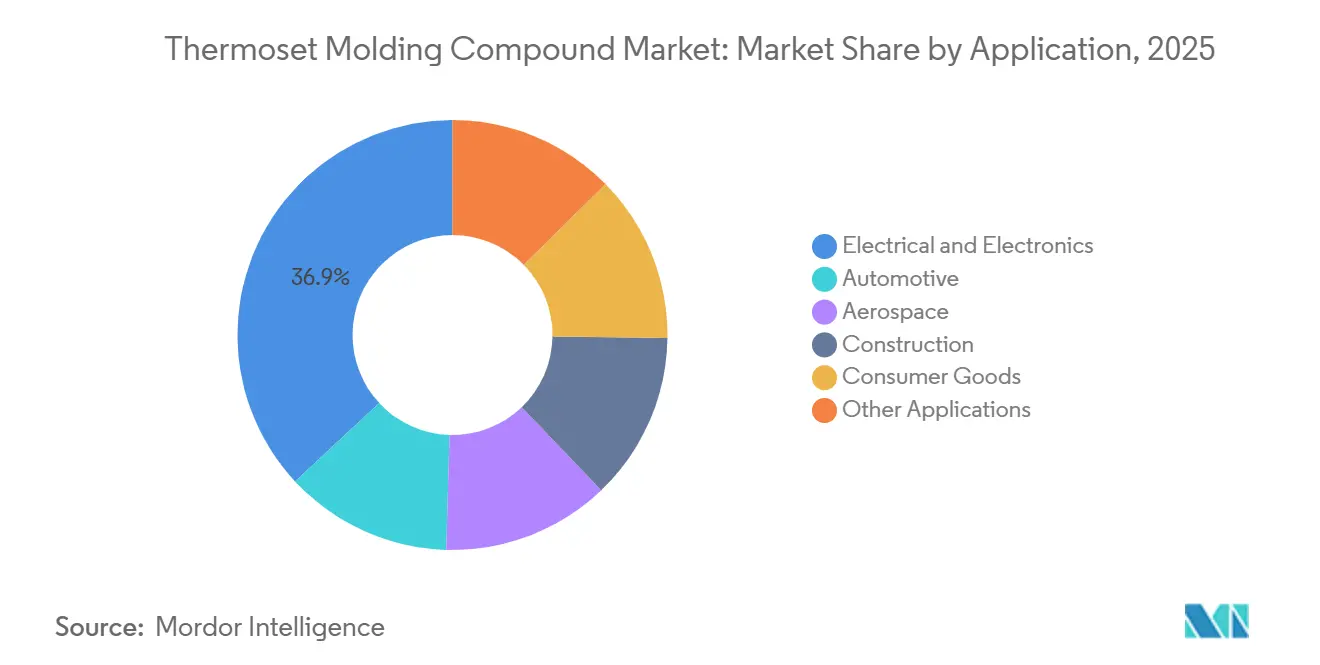

- By application, electrical and electronics held 36.92% of the Thermoset Molding Compound market share in 2025; automotive is forecast to post the fastest 7.77% CAGR through 2031.

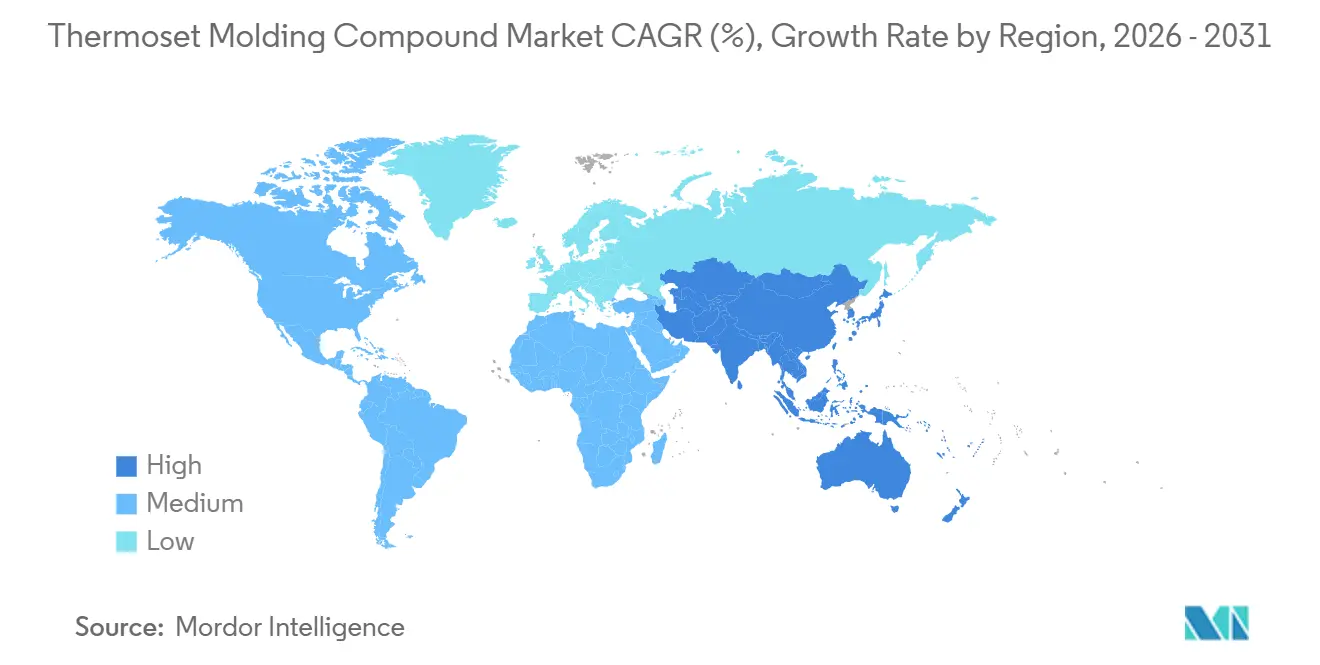

- By geography, Asia-Pacific controlled 45.72% revenue in 2025 and is growing at a 7.43% CAGR during the forecast period (2026-2031), the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thermoset Molding Compound Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing use in electrical and electronics | +1.2% | Global, with concentration in APAC (China, Korea, Taiwan) and North America | Medium term (2-4 years) |

| Automotive and aerospace lightweighting push | +1.5% | North America, Europe, APAC (Japan, Korea) | Long term (≥ 4 years) |

| Renewable-energy composite demand surge | +0.9% | Global, led by China, Europe (offshore wind), North America | Long term (≥ 4 years) |

| Infrastructure prefabs adopting high-durability compounds | +0.7% | APAC (China, India, ASEAN), Middle East | Medium term (2-4 years) |

| Regional epoxy capacity build-up post anti-dumping duties | +0.8% | India, Southeast Asia, North America (Mexico) | Short term (≤ 2 years) |

| Dynamic-covalent/vitrimer technologies enabling recyclability | +0.5% | Europe, North America (early R&D adoption) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Use in Electrical and Electronics

Thermal-management requirements for 800-volt EV inverters and 5G base stations are driving epoxy specifications toward thermal conductivities above 0.80 W/m/K and dielectric constants below 4.0[1]Institute of Electrical and Electronics Engineers, “High Thermal Conductivity Epoxy Molding Compounds,” ieee.org. Hybrid hBN-AlN filler systems now deliver UL 94 V-0 flame ratings without halogens, supporting data-center power supplies that must pass 105°C continuous-use tests. China’s printed-circuit-board output is forecast to hit USD 54.6 billion by 2026, sustaining epoxy demand for FR-4 and high-frequency laminates. Semiconductor packaging for AI accelerators increasingly favors cycloaliphatic epoxies with glass-transition temperatures above 150°C, eroding phenolic share. Shorter qualification cycles, now under 12 months, reward suppliers offering digital simulation and in-house rapid prototyping capabilities.

Automotive and Aerospace Lightweighting Push

European fleet CO₂ ceilings of 95 g/km are compelling OEMs to shift brackets, crossbeams, and battery enclosures from steel to glass-fiber phenolic and carbon-fiber epoxy, trimming vehicle mass by up to 50%[2]BASF SE, “Spray Transfer Molding for EV Components,” basf.com. BASF’s spray transfer molding process enables Class-A body panels in 3-minute cycles, eliminating paint-bake ovens and cutting energy usage 40%. In aerospace, HexPly M51 prepreg cures in 40 minutes at 180°C, reducing autoclave energy 30% and unlocking single-shift throughput. Korea’s supply chain is piloting glass-mat thermoplastic bumper beams that threaten phenolic sheet-molding compounds in non-structural zones. Across mobility platforms, lightweighting ties directly to regulatory credits and extended battery range, enhancing the thermoset molding compound market value proposition.

Renewable Energy Composite Demand Surge

Offshore wind blades longer than 100 m require epoxy matrices with glass-transition temperatures above 80°C and moisture uptake below 1.5% to secure 25-year durability in marine climates. China’s cumulative wind capacity surpassed 441 GW in 2023, and epoxy is displacing polyester in 15-MW turbine blades for fatigue resistance. Hexcel’s bio-based M949 prepreg incorporates 15% renewable carbon, aligning with EU Directive 2018/851 that mandates 70% material recovery by 2030. Arkema’s Kentucky plant started in 2025 to supply low-GWP (Global Warming Potential) blowing agent Forane 1233zd, facilitating closed-loop polyurethane foam cores. Integrated blade recyclability pilots involving vitrimers underscore a long-term pivot to circular composites.

Infrastructure Prefabs Adopting High Durability Compounds

Prefabricated data-center modules and modular hospitals specify phenolic and melamine compounds that meet ASTM E84 Class A flame performance and resist fungal growth per ASTM G21. India’s USD 1.4 trillion National Infrastructure Pipeline is spurring Atul and Hindusthan Speciality Chemicals to expand epoxy capacity following anti-dumping duties on imports. Middle Eastern water-treatment projects prefer corrosion-resistant polyester BMC (Bulk Molding Compound) over glass-reinforced polyamide, despite a 15% price premium. Southeast Asian prefab bathroom pods use urea-formaldehyde compounds releasing under 0.05 ppm (parts per million) formaldehyde to achieve E1 indoor-air grades. Rapid urbanization keeps thermoset demand buoyant across panels, ducts, and fire-safe enclosures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Poor recyclability/end-of-life costs | -0.8% | Europe (stringent circular-economy mandates), North America | Medium term (2-4 years) |

| Formaldehyde-based compound HSE risks | -0.6% | Global, with acute pressure in EU (REACH) and North America (EPA TSCA) | Short term (≤ 2 years) |

| Protectionist trade barriers disrupting supply chains | -0.5% | Global, concentrated in US-China-India trade corridors | Short term (≤ 2 years) |

| Emergent thermoplastic composites cannibalising low-temperature uses | -0.4% | Automotive (Europe, Korea, Japan), consumer goods | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Poor Recyclability and End of Life Costs

Irreversible cross-linking confines most thermoset scrap to landfill or costly pyrolysis, where gate fees run USD 200-400 per tonne, double virgin material value. EU Directive 2018/851 targets 70% composite recovery by 2030, yet mechanical grinding downgrades materials to low-value fillers. A single 3-MW wind turbine yields 20 tonnes of blade waste, and Europe expects 14,000 blade retirements, straining landfill space in Germany and Denmark. Design-for-disassembly adds USD 50-100 per vehicle in labor, discouraging OEM adoption unless extended producer responsibility regimes expand. Vitrimer plants require USD 50 million investment, affordable only for integrated resin majors, slowing near-term penetration.

Formaldehyde Based Compound HSE Risks

EPA TSCA rules finalized in 2024 cap workplace formaldehyde at 0.75 ppm and consumer emissions at 0.1 ppm, pushing phenolic and melamine producers toward low-emission catalysts or exit. REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) Annex XVII mirrors the 0.1 ppm threshold for molded furniture, shrinking urea-formaldehyde addressable volumes. Sumitomo Bakelite’s novolac resins emit below 0.05 ppm but cost 15-20% more, acceptable only in regulated segments. Real-time plant monitoring shows mold-opening peaks beyond 2 ppm, forcing USD 500,000 ventilation retrofits per press line. Epoxy substitution removes formaldehyde yet raises part cost 30% and flammability challenges, leaving formulators to juggle safety, performance, and economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Phenolic Dominance Meets Epoxy Momentum

Phenolic resins delivered 28.02% of the Thermoset Molding Compound market share in 2025 on the back of friction materials and EV motor housings. The Thermoset Molding Compound market size for phenolics is projected to advance modestly as emission-controlled variants secure appliance interiors. Epoxy is pacing ahead at a 7.02% CAGR through 2031 on demand for AI semiconductor packaging and 15-MW wind-blade skins. Polyester BMC trails in cost-sensitive sanitary ware, while melamine and urea derivatives fade under emission scrutiny.

Epoxy formulators are commercializing cycloaliphatic grades with Tg above 150°C and 1% moisture uptake, aligning with AI accelerator packages. China’s phenolic output surpassed 1.60 million tons in 2024, led by Shandong Shengquan with 25% share, underscoring Asia’s cost edge. Niche systems such as vinyl-ester and diallyl phthalate occupy corrosion-resistant and high-voltage insulation segments, respectively, at 2-5× price premiums, which the thermoset molding compound industry absorbs where failure is not an option.

By Fiber Reinforcement: Carbon Fiber Ascends

Glass fiber retained 63.63% share in 2025, owing to USD 2-4 per kg pricing and global supply from Owens Corning and Jushi. Carbon fiber is expanding at a 7.34% CAGR for the forecast period (2026-2031), driving the thermoset molding compound market size for aerospace and luxury EV parts.

Rapid-cure carbon prepregs like HexPly M51 cut autoclave cycles to 40 minutes at 180°C, shrinking the glass-fiber cost gap. Korean suppliers are piloting RTM driveshafts that lower mass 60% versus steel, paving the way for annual volumes above 10,000 units. Hybrid programs such as Hexcel’s Hy-Bor fuse boron and carbon fibers at 200 GPa stiffness for space applications. Meanwhile, aramid and natural fibers fill protective and bio-content niches, respectively, within the broader thermoset molding compound market.

By Application: Automotive Outpaces Electrical

Electrical and electronics applications commanded 36.92% revenue in 2025, driven by 5G heat sinks and power-module substrates that require 0.80 W/m/K thermal conductivity. The thermoset molding compound market size for automotive is forecast to balloon fastest at a 7.77% CAGR through 2031 as fleet emission targets spur metal substitution.

Phenolic PM-5820 compounds endure 200°C continuous exposure for EV motor housings, while BASF’s STM process molds Class-A panels in 3 minutes, lifting line productivity 25%. Aerospace remains thermoset-dominated thanks to 180°C service demands, with HexPly M51 securing positions on Airbus A350 and Boeing 787 fuselages. Construction, consumer goods, and corrosion-resistant tanks round out the remaining outlets, though thermoplastic competition is intensifying in luggage shells and appliance skins.

Geography Analysis

Asia-Pacific anchored 45.72% of the Thermoset Molding Compound market revenue in 2025 and is projected to rise at a 7.43% CAGR to 2031, propelled by China’s 4.0 million-ton epoxy capacity and surging offshore wind installations. Indian anti-dumping duties are catalyzing domestic resin projects linked to a USD 1.4 trillion infrastructure pipeline. Japanese OEMs are adopting PM-5700 phenolic compounds in EV gears, targeting USD 13 million sales by 2030. Korean programs around long-fiber thermoplastics signal emerging substitution threats, yet the thermoset molding compound market in the region remains resilient on mandated flame performance.

North America faces supply tightness after U.S. anti-dumping margins on Chinese epoxy, shifting procurement to Mexico and Canada, while domestic capacity lags 40% below prior import volumes. Hexcel’s USD 1.89 billion sales in 2025 underscore aerospace pull, and Arkema’s Kentucky Forane 1233zd plant backs domestic wind-blade recyclability initiatives.

Europe balances 0.1 ppm (parts per million) formaldehyde thresholds with 70% composite recycling mandates, pressuring phenolic incumbents to innovate or exit. Germany and Denmark confront blade-waste surges, accelerating vitrimer research collaborations. South America and Middle East-Africa remain smaller but growth-oriented, emphasizing corrosion-resistant vinyl-ester systems for petrochemical and water infrastructure.

Competitive Landscape

The Thermoset Molding Compound market is moderately fragmented. Backward integration is accelerating as Hexcel and Toray enlarge epoxy synthesis to hedge against trade volatility, a capital-intensive moat small molders cannot cross. Patent filings for recyclable thermosets rose 35% between 2024 and 2025, highlighting a scramble to comply with future circularity mandates.

Thermoset Molding Compound Industry Leaders

Hexion Inc.

BASF

Sumitomo Bakelite Co., Ltd.

Owens Corning

Toray Advanced Composites

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Sumitomo Bakelite Co., Ltd. announced plans to acquire all shares of a new company being established by Kyocera Corporation, which will inherit part of Kyocera's Chemical Business. This move aims to enhance Sumitomo Bakelite's position in the ICT sector, focusing on epoxy-resin molding compounds, bonding pastes, and industrial-use resins.

- December 2024: McClarin Composites signed a joint development deal with ExxonMobil’s Proxxima division. This partnership seeks to fast-track the expansion of high-speed, closed-mold composites manufacturing. The collaboration follows McClarin's strategic move, which acquired and relocated specific polyolefin thermoset molding facilities from ExxonMobil affiliate, Materia Inc.

Global Thermoset Molding Compound Market Report Scope

Thermoset molding compounds are polymer resins that undergo an irreversible chemical cross-linking process under heat and pressure to form rigid, high-strength, and heat-resistant parts.

The Thermoset Molding Compound market is segmented by resin type, fiber reinforcement, application, and geography. By resin type, the market is segmented into epoxy, phenolic, polyester, melamine formaldehyde, urea formaldehyde, and other thermoset resins. By fiber reinforcement, the market is segmented into glass fiber, carbon fiber, and other reinforcements. By application, the market is segmented into electrical and electronics, automotive, aerospace, construction, consumer goods, and other applications. The report also covers the market size and forecasts for thermoset molding compounds in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Epoxy |

| Phenolic |

| Polyester |

| Melamine Formaldehyde |

| Urea Formaldehyde |

| Other Thermoset Resins |

| Glass Fiber |

| Carbon Fiber |

| Other Reinforcements |

| Electrical and Electronics |

| Automotive |

| Aerospace |

| Construction |

| Consumer Goods |

| Other Applications |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Resin Type | Epoxy | |

| Phenolic | ||

| Polyester | ||

| Melamine Formaldehyde | ||

| Urea Formaldehyde | ||

| Other Thermoset Resins | ||

| By Fiber Reinforcement | Glass Fiber | |

| Carbon Fiber | ||

| Other Reinforcements | ||

| By Application | Electrical and Electronics | |

| Automotive | ||

| Aerospace | ||

| Construction | ||

| Consumer Goods | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected revenue for the thermoset molding compound market in 2031?

The Thermoset Molding Compound Market size is projected to be USD 11.88 billion in 2025, USD 12.67 billion in 2026, and reach USD 17.45 billion by 2031, growing at a CAGR of 6.62% from 2026 to 2031.

Which resin type is growing fastest?

Epoxy formulations are expanding at a 7.02% CAGR thanks to semiconductor packaging and wind-turbine blade demand.

Why is Asia-Pacific the leading region?

The region houses 4.0 million tonnes of Chinese epoxy capacity and robust wind-energy build-outs that yielded a 45.72% share in 2025.

How are trade barriers affecting supply?

U.S. and Indian anti-dumping duties have redirected buyers to Mexico and domestic sources, tightening North American supply by 40%.

Page last updated on: