Model-based Enterprise Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

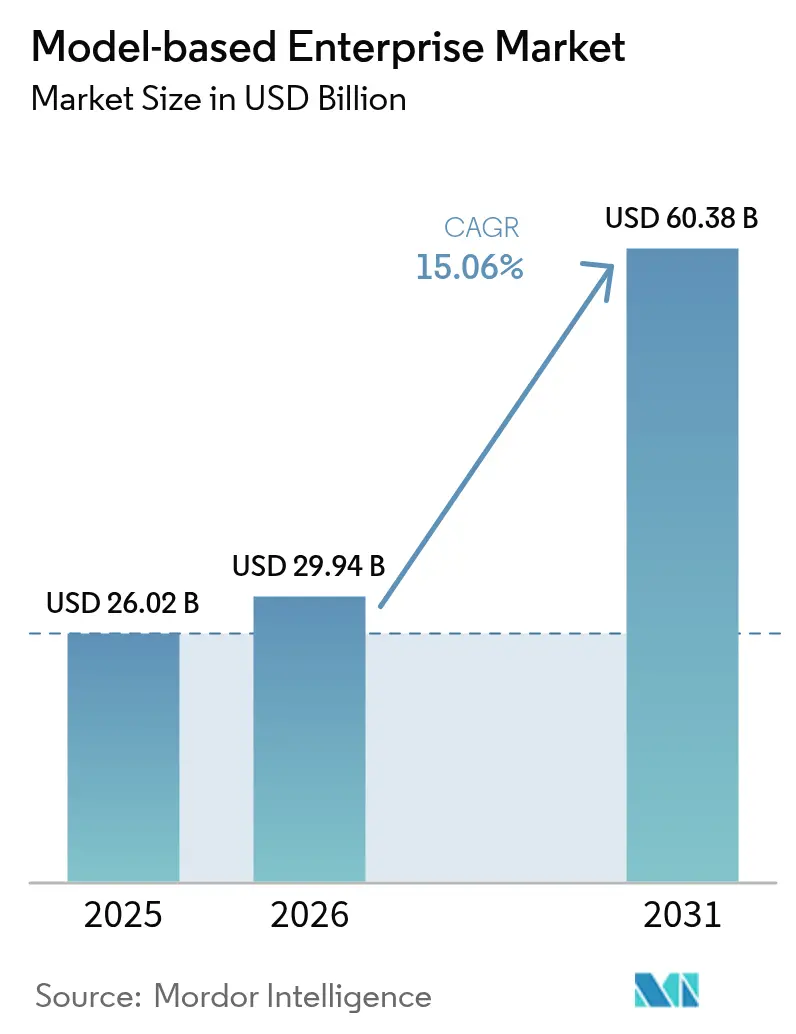

| Market Size (2026) | USD 29.94 Billion |

| Market Size (2031) | USD 60.38 Billion |

| Growth Rate (2026 - 2031) | 15.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Model-based Enterprise Market Analysis by Mordor Intelligence

The model-based enterprise market size is expected to grow from USD 26.02 billion in 2025 to USD 29.94 billion in 2026 and is forecast to reach USD 60.38 billion by 2031 at 15.06% CAGR over 2026-2031. This momentum is anchored in the shift from document-centric workflows to coherent digital threads that connect design, engineering, manufacturing, and service functions. The United States Department of Defense requirement that digital models act as the single authoritative data source is spurring swift uptake among aerospace and defense contractors. Automotive manufacturers are adopting similar practices to compress electric-vehicle development timelines, while cloud-native product-lifecycle-management suites are lowering barriers for small and medium manufacturers in Asia-Pacific. Vendors are investing in AI-driven simulation, additive-manufacturing quality loops, and integrated digital twins to deliver faster ROI, yet many users still grapple with workforce reskilling costs and data-interoperability gaps.

Key Report Takeaways

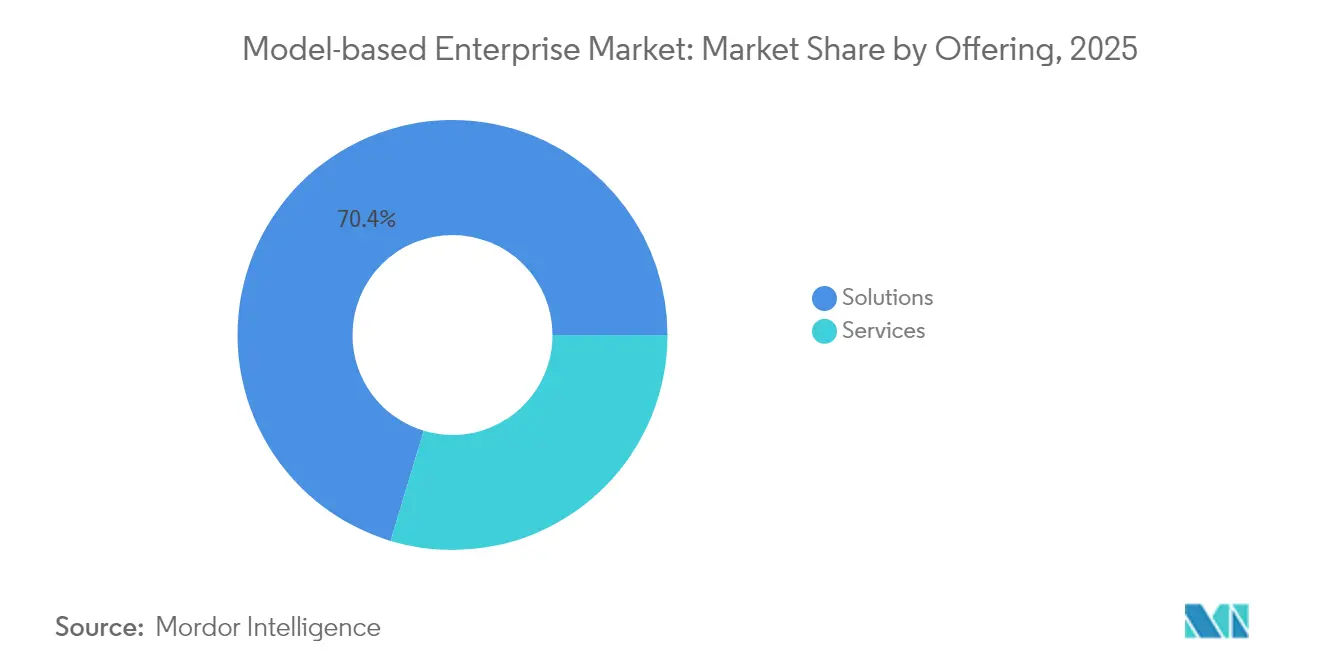

- By offering, Solutions held 70.35% of 2025 revenue, whereas Services are projected to post the fastest 17.46% CAGR through 2031.

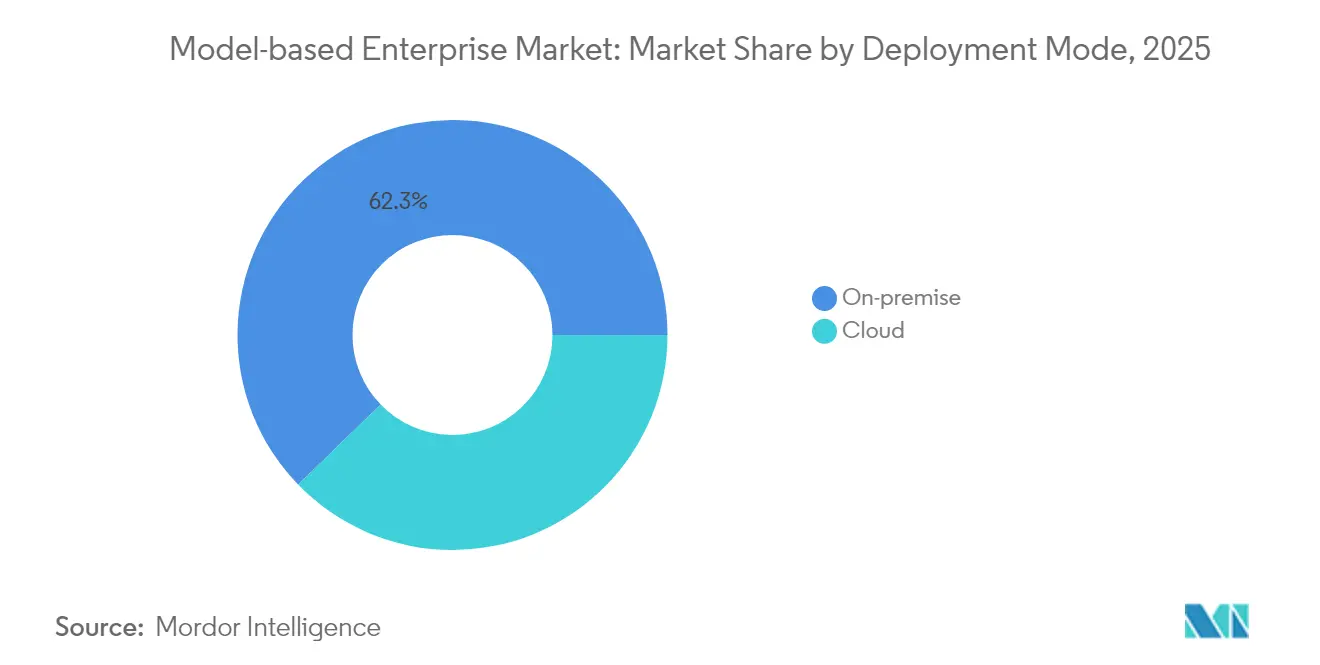

- By deployment mode, on-premise installations commanded 62.25% share of the model-based enterprise market size in 2025; cloud deployments are growing at an 17.96% CAGR.

- By end-user industry, aerospace & defense accounted for 32.55% share of the model-based enterprise market size in 2025, and automotive is advancing at a 15.86% CAGR.

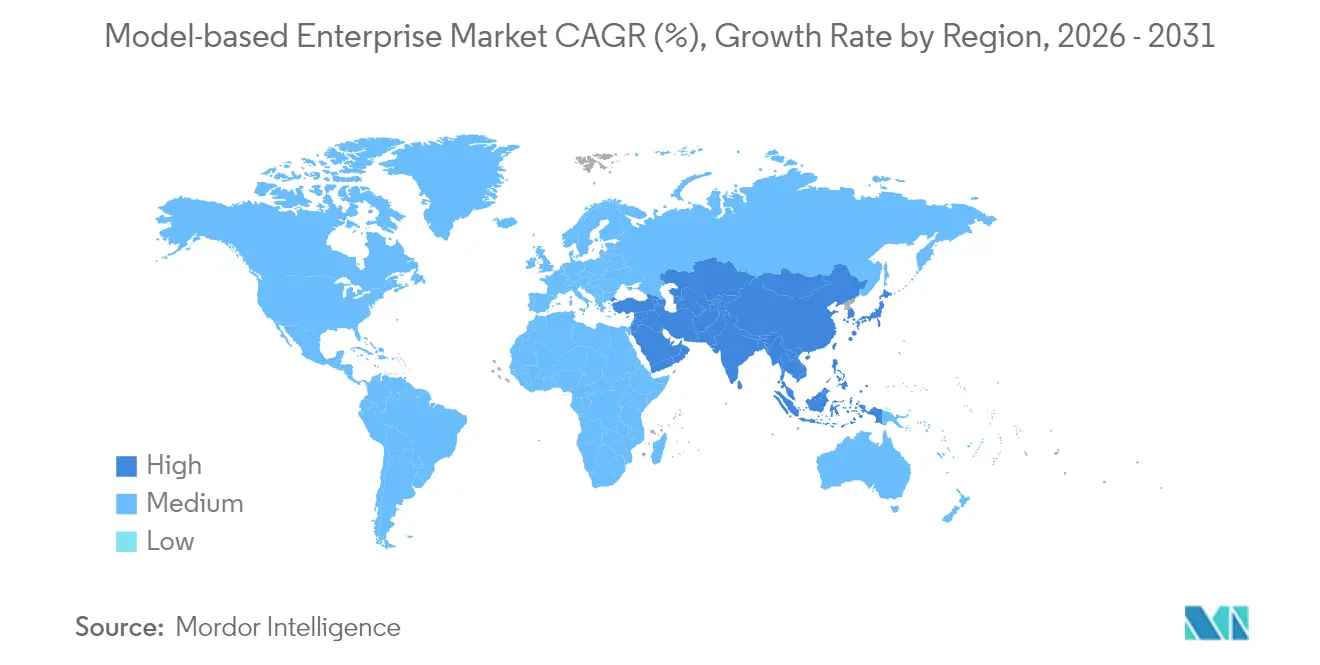

- By geography, North America led with 37.62% of model-based enterprise market share in 2025, while Asia-Pacific is set to expand at an 18.34% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Model-based Enterprise Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DoD Digital Engineering Mandates | +3.8% | North America with spillover to Europe & Asia-Pacific | Medium term (2-4 years) |

| Automotive OEM Shift to Full-3D Digital Thread | +3.4% | Europe, North America, China | Medium term (2-4 years) |

| Surge in Cloud-Native PLM Suites for SMBs | +2.8% | Asia-Pacific (Japan, South Korea, India) | Short term (≤ 2 years) |

| ROI From Aerospace MRO Turn-Around-Time Reduction | +2.3% | North America & Europe | Medium term (2-4 years) |

| Integrating MBD With Additive-Manufacturing Quality | +1.8% | North America, Europe, advanced Asia hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

DoD Digital Engineering Mandates Accelerating Adoption in North America

Defense contractors must now treat 3D models as the single source of truth for design, analysis, sourcing, and sustainment decisions. Close to 300,000 suppliers have started updating processes, software stacks, and cybersecurity safeguards to stay eligible for future contracts. Uptake is spilling over to commercial aerospace as shared subcontractors align with mandate-compliant workflows. Tool vendors are responding with packaged compliance templates and automated model-based definition (MBD) checkers that cut documentation time and enhance traceability.

Automotive OEM Shift to Full-3D Digital Thread for EV Platforms

Battery-electric programs rely on concurrent design of mechanical, electrical, and thermal systems. Deploying a unified 3D digital thread has allowed leading automakers to shrink platform cycles from 72 months to 36 months while improving traceability.[1]PTC Inc., “How the Digital Thread Transforms Automotive Manufacturing Processes,” ptc.com The integration of digital twins with model-based systems engineering lets teams simulate energy flow, crash behavior, and battery degradation early, curbing late redesigns and warranty risk. These gains drive widespread rollouts across Europe, North America, and China.

Surge in Cloud-Native PLM Suites Enabling SMB Access in Asia-Pacific

Cloud deployment removes the need for heavy servers and specialized IT staff. Typical migrations complete in 45–90 days, enabling manufacturers across Japan, South Korea, and India to deploy advanced PLM and MBD with limited capital outlay.[2]CIMdata Inc., “PLM Industry Summary,” cimdata.com Pay-as-you-go pricing and automated updates lower lifetime ownership costs, making enterprise-grade digital-thread capabilities accessible to the region’s vast SMB base. Rapid onboarding fuels the region’s position as the fastest-growing adopter.

ROI From Aerospace MRO Turn-Around-Time Reduction

Digital twins embedded with predictive-maintenance algorithms cut unscheduled maintenance and improve fleet availability by 15%, with similar savings in direct costs.[3]Aerospace Testing International, “How Digital Twins Are Transforming Aerospace Development and Testing,” aerospacetestinginternational.com Airlines and MRO providers now pull configuration-managed 3D models to forecast part life and optimize spares provisioning. Improved data fidelity raises maintenance-record accuracy to roughly 97%, supporting air-worthiness audits and cutting penalty risks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Interoperability Gaps Between Legacy CAD and New MBD Standards | -2.3% | Global, stronger in mature manufacturing regions | Medium term (2-4 years) |

| High Up-Front Workforce Reskilling Costs | -1.8% | Global, acute where skill shortages persist | Short term (≤2 years) |

| Cyber-Security Concerns Over IP in Cloud Deployments | -1.5% | Global, especially defense, aerospace, automotive | Medium term (2-4 years) |

| Multi-Tier Supply-Chain Compliance Complexity | -1.2% | North America, Europe, Asia-Pacific export hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Interoperability Challenges Hinder Seamless Integration

Roughly 65% of engineering projects still encounter delays when transforming historical CAD files into feature-rich, MBD-ready models.[4]CAD Interop, “Expert Solutions for CAD Migration,” cadinterop.com Geometry translation alone is not enough; teams must also preserve features, constraints, and linked drawings built over decades. Specialized conversion tools are improving, yet enterprise-wide migrations remain resource intensive and carry risk of data loss that can stall digital-thread initiatives.

Workforce Reskilling Creates Implementation Hurdle

Moving from document-centric to model-centric workflows changes every daily task, from design review to shop-floor inspection. Firms must fund extensive training programs, refresh standard operating procedures, and realign performance metrics. Resistance to change is common, especially in organizations where experienced staff have honed 2D practices for decades. Comprehensive change-management plans and incremental rollouts are proving essential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Outpace Solutions Growth

The Solutions segment generated 70.35% of 2025 revenue, underscoring its role as the backbone of most deployments. Service engagements, however, are registering a 17.46% CAGR as enterprises confront the complexity of rolling out model-based practices at scale. Service providers are embedding AI to automate data migration and validation, shortening time-to-value and boosting confidence in model accuracy. Training and certification packages focused on digital-thread skills are rising in demand, highlighting the persistent talent gap. The influx of specialized service firms is broadening options for mid-market manufacturers seeking guidance without the expense of large consulting teams.

Rising subscription models are shifting revenue from perpetual software toward continuous service relationships tied to performance metrics and outcome-based contracts. Predictive analytics applied within maintenance and support agreements can flag integration glitches before they disrupt production. These capabilities reinforce client reliance on trusted partners, sustaining the upward trajectory of the Services share within the model-based enterprise market.

By Solution Type: Digital-Twin & Simulation Gaining Momentum

Product-lifecycle-management platforms remain the foundation of most implementations, but the Digital-Twin & Simulation segment is gaining prominence as organizations seek closed-loop feedback between design and operation. Real-time sensor data feeding high-fidelity models creates self-updating digital twins that guide maintenance, optimize performance, and extend asset life. The convergence of simulation and systems engineering reduces rework by validating requirements early, a benefit that is especially acute in regulated domains such as aerospace and medical devices.

Visualization and collaboration tools are adding AR/VR overlays to facilitate immersive design reviews. Engineers, suppliers, and even field technicians can inspect the same model in real time, shrinking the decision window. CAD/CAM/CAE suites now embed product-manufacturing information directly in 3D geometry. This allows downstream software, including inspection planning and shop-floor metrology platforms, to consume a single data set, trimming translation steps and minimizing revision errors.

By Service Type: Integration & Implementation Addresses Complexity

Integration & Implementation services account for the largest slice of service revenue because aligning new PLM, simulation, and analytics layers with legacy ERP and MES systems is rarely straightforward. High-quality models that span the concept, design, production, and sustainment phases are essential to prevent data silos. As a result, service teams frequently deploy connectors, configure application-programming interfaces, and test digital-thread continuity across domains.

Consulting & Training engagements are expanding fastest as enterprises request road-maps, maturity assessments, and workforce enablement programs. Structured curricula covering model-based definition, systems engineering, and additive-manufacturing workflows help firms overcome cultural inertia. Support & Maintenance contracts are shifting toward proactive analytics, where service desks monitor usage metrics and flag anomalies before they escalate into downtime. Vendors that can blend all three service types-integration, consulting, and proactive support-are solidifying long-term client relationships.

By Deployment Mode: Cloud Adoption Accelerates Flexibility

On-premise deployments retained a 62.25% revenue share in 2025 because many firms already own significant data-center assets and must adhere to strict security controls. Even so, cloud solutions are growing at an 17.96% CAGR as software-as-a-service models show that updates, scalability, and cost predictability can outweigh perceived risks. Hybrid approaches let organizations keep sensitive data on-premise while using cloud compute for bursty simulation or real-time collaboration.

The arrival of containerized PLM and simulation micro-services enables consistent performance across private and public environments. In Asia-Pacific, small and mid-size enterprises increasingly adopt full cloud stacks because they lack legacy data centers. North-American and European multinationals often choose phased migrations, starting with supplier collaboration portals or engineering-change workflows before moving mission-critical CAD data to secure cloud vaults.

By End-User Industry: Aerospace & Defense Leads Implementation

Aerospace and Defense held 32.55% of 2025 revenue, reflecting strict regulatory requirements and the complexity of multi-year programs where digital continuity cuts risk. Budget commitments and the DoD mandate ensure stable demand for hardened, traceable, model-centric toolchains. Predictive simulation linked to digital twins accelerates test cycles, allowing contractors to meet performance targets while managing cost caps.

Automotive posted the fastest 15.86% CAGR as electrification and software-defined vehicles require cross-disciplinary collaboration. Unified 3D threads enable engineers to align battery thermal models with crash-worthiness targets and manufacturing constraints. Electronics & Hi-Tech, Construction & Infrastructure, and Power & Energy segments are also increasing their investments because digital twins promise shorter project schedules, lower rework, and better lifecycle management.

Geography Analysis

North America contributed 37.62% of 2025 revenue, supported by defense spending, a mature aerospace supply chain, and automakers seeking to accelerate electric-vehicle launches. Federal policies that enforce digital models as the official technical baseline are nudging even conservative contractors to modernize. Canada and Mexico participate through integrated supply chains that must also prove compliance, driving widespread adoption across the continent.

Asia-Pacific is the fastest-growing region with an 18.34% CAGR over 2026-2031. Cloud-hosted PLM lowers entry barriers for Japan’s precision manufacturers, South Korea’s electronics champions, and India’s engineering-services providers. China’s investment in digital factories fuels demand for digital-thread solutions that can scale across vast production networks. Local governments promote smart-manufacturing grants, accelerating SMB participation.

Europe maintains robust adoption driven by Germany’s Industrie 4.0 initiatives and France’s advanced aerospace programs. A United Kingdom digital-twin center in Belfast demonstrates national commitment to remain competitive in next-generation aircraft development. Sustainability regulations further encourage model-centric design to track carbon footprints and optimize resource use. Regional standards bodies collaborate on interoperability frameworks, smoothing cross-border collaboration.

Competitive Landscape

Long-standing PLM providers-Siemens, Dassault Systèmes, and PTC-retain dominant positions by bundling CAD, PLM, simulation, and IoT analytics in unified suites. They are augmenting portfolios with AI-powered physics engines and cloud micro-services to improve scalability and accuracy. Challenger vendors such as Aras employ open architectures that ease integration with heterogeneous toolchains, appealing to enterprises wrestling with legacy data.

White-space opportunities lie in mid-market offerings that deliver robust digital-thread functions without enterprise-level complexity. Specialist firms focus on additive-manufacturing quality or model-based systems engineering templates, enabling faster domain-specific deployments. Customers increasingly judge vendors on their ability to supply outcome-oriented service bundles, training, and rapid pilot-to-production pathways, rather than on software features alone.

Manufacturers are both customers and innovators. Rolls-Royce’s connected-enterprise program uses model-based systems engineering to streamline design and service analytics. Partnerships such as Siemens and PhysicsX illustrate how incumbents embrace external AI expertise to refine simulation speed and accuracy. As cloud adoption rises, joint ventures between PLM vendors and hyperscale cloud providers are expected to intensify.

Model-based Enterprise Industry Leaders

Siemens AG

General Electric Company

PTC Inc.

Dassault Systèmes SE

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Siemens updated NX with expanded model-based definition and the NX Inspector tool for streamlined inspection workflows.

- April 2025: Ansys broadened its model-based systems-engineering suite, adding automation, embedded-software, and safety-analysis modules.

- March 2025: Thinaer introduced real-time asset-visibility technology to aid defense suppliers in meeting DoD mandate 5000.97.

- February 2025: The United Kingdom inaugurated a Digital Twin Centre in Belfast to bolster aerospace competitiveness.

- January 2025: Autodesk released Fusion Manage, a cloud PLM platform aimed at collaborative product development

Global Model-based Enterprise Market Report Scope

Model-based enterprise (MBE) is an engineering strategy that primarily aims to clarify the design intent during the manufacturing process by using a 3D model-based definition that includes all the product and manufacturing process information associated with the product's manufacturing.

The model-based enterprise market is segmented by offering (solutions and services), deployment mode (on-premise and cloud), end user (aerospace and defense, automotive, construction, power and energy, retail, and other end users), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market size and forecasts are provided in terms of value in USD for all the above segments.

| Solutions |

| Services |

| PLM Software |

| CAD/CAM/CAE |

| Digital-Twin and Simulation |

| Visualization and Collaboration |

| Integration and Implementation |

| Consulting and Training |

| Support and Maintenance |

| On-premise | |

| Cloud | Public Cloud |

| Private Cloud | |

| Hybrid Cloud |

| Aerospace and Defense |

| Automotive |

| Construction and Infrastructure |

| Power and Energy |

| Retail and CPG |

| Electronics and Hi-Tech |

| Marine and Offshore |

| Other Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Offering | Solutions | |

| Services | ||

| By Solution Type | PLM Software | |

| CAD/CAM/CAE | ||

| Digital-Twin and Simulation | ||

| Visualization and Collaboration | ||

| By Service Type | Integration and Implementation | |

| Consulting and Training | ||

| Support and Maintenance | ||

| By Deployment Mode | On-premise | |

| Cloud | Public Cloud | |

| Private Cloud | ||

| Hybrid Cloud | ||

| By End User Industry | Aerospace and Defense | |

| Automotive | ||

| Construction and Infrastructure | ||

| Power and Energy | ||

| Retail and CPG | ||

| Electronics and Hi-Tech | ||

| Marine and Offshore | ||

| Other Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What are the top regulatory forces shaping model-based enterprise adoption?

The U.S. Department of Defense digital-engineering mandate and similar aerospace regulations compel suppliers to maintain model-centric workflows, accelerating investment across the supply chain.

Why is cloud deployment gaining traction despite security concerns?

Cloud PLM offers rapid onboarding, elastic compute for simulation, and subscription pricing; hybrid architectures retain sensitive data on-premise to address intellectual-property risk.

How do digital twins improve maintenance, repair, and overhaul operations?

Real-time sensor data synchronizes with high-fidelity models, enabling predictive scheduling that has cut aircraft maintenance costs and turnaround times by roughly 15%.

Which industries demonstrate the fastest uptake after aerospace and defense?

Electric-vehicle programs in automotive manufacturing adopt full 3D digital threads to meet compressed launch schedules and integrate software-defined functionality.

What is the greatest technical hurdle to enterprise-wide rollouts?

Converting decades of legacy CAD into fully annotated, parametric models without losing design intent remains the dominant technical barrier and often delays projects.

Which industry currently invests the most?

Aerospace and Defense stands out, contributing 32.55% of 2025 revenue due to mandated digital-engineering policies and the complexity of long-lifecycle programs that benefit from full digital continuity.

Page last updated on: