Biomedical Textile Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

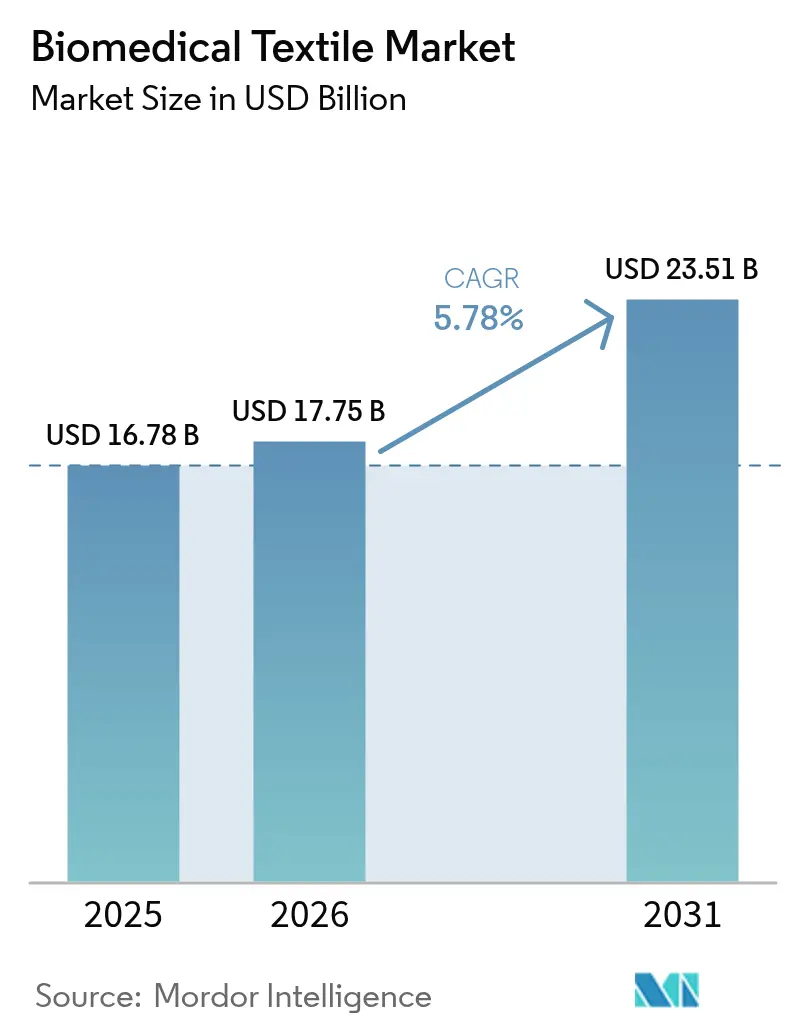

| Market Size (2026) | USD 17.75 Billion |

| Market Size (2031) | USD 23.51 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

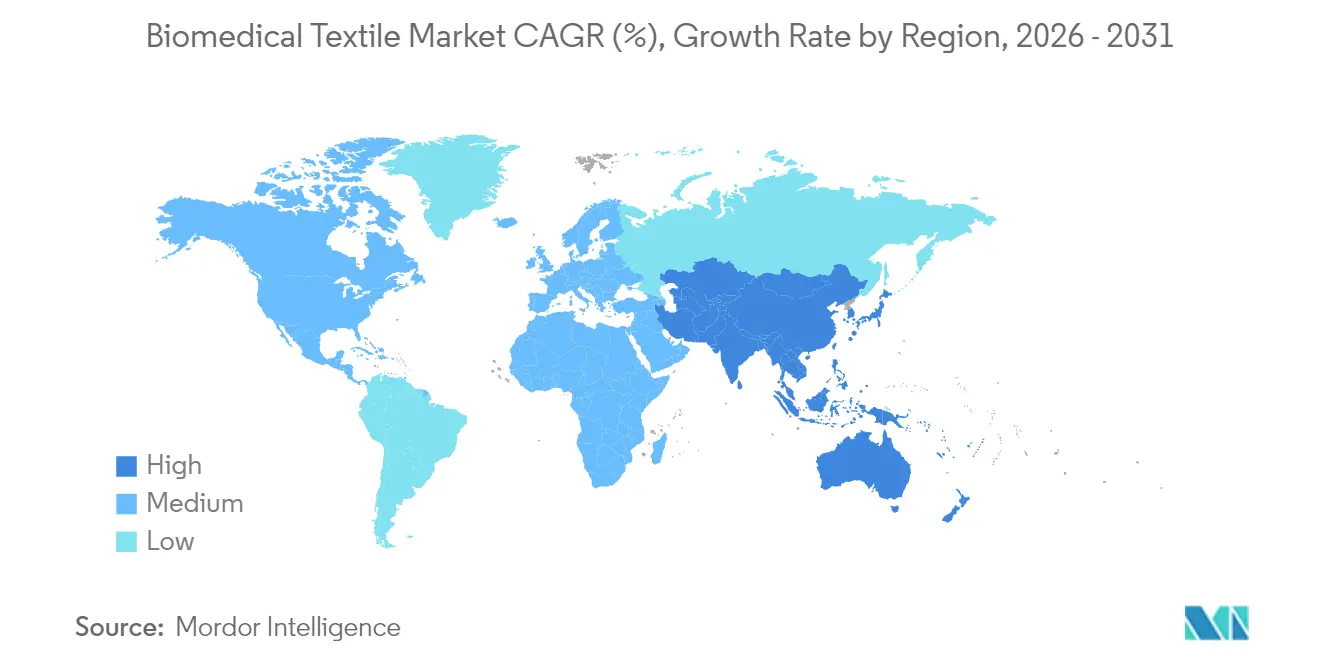

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biomedical Textile Market Analysis by Mordor Intelligence

The Biomedical Textile Market size was valued at USD 16.78 billion in 2025 and estimated to grow from USD 17.75 billion in 2026 to reach USD 23.51 billion by 2031, at a CAGR of 5.78% during the forecast period (2026-2031). This growth rests on the expanding surgical workload created by older populations, the commercialization of minimally-invasive implantable fabrics, and steady public-sector funding that migrates defense textile research into civilian care. Demand also rises as care settings shift toward home health and ambulatory clinics that rely on portable, sensor-ready dressings. Sustained regulatory clarity from the FDA on biocompatibility testing shortens approval cycles, while Europe’s single-use plastics rules accelerate the switch to compostable fibers and bioresorbable scaffolds. Mergers such as Freudenberg’s acquisition of Heytex concentrate know-how in nonwovens, strengthening supply resilience and shortening innovation timelines. Simultaneously, retail channels now stock electro-spun nanofiber dressings, signaling mainstream acceptance of advanced wound products and opening recurring revenue streams for consumer-facing variants of clinical lines.

Key Report Takeaways

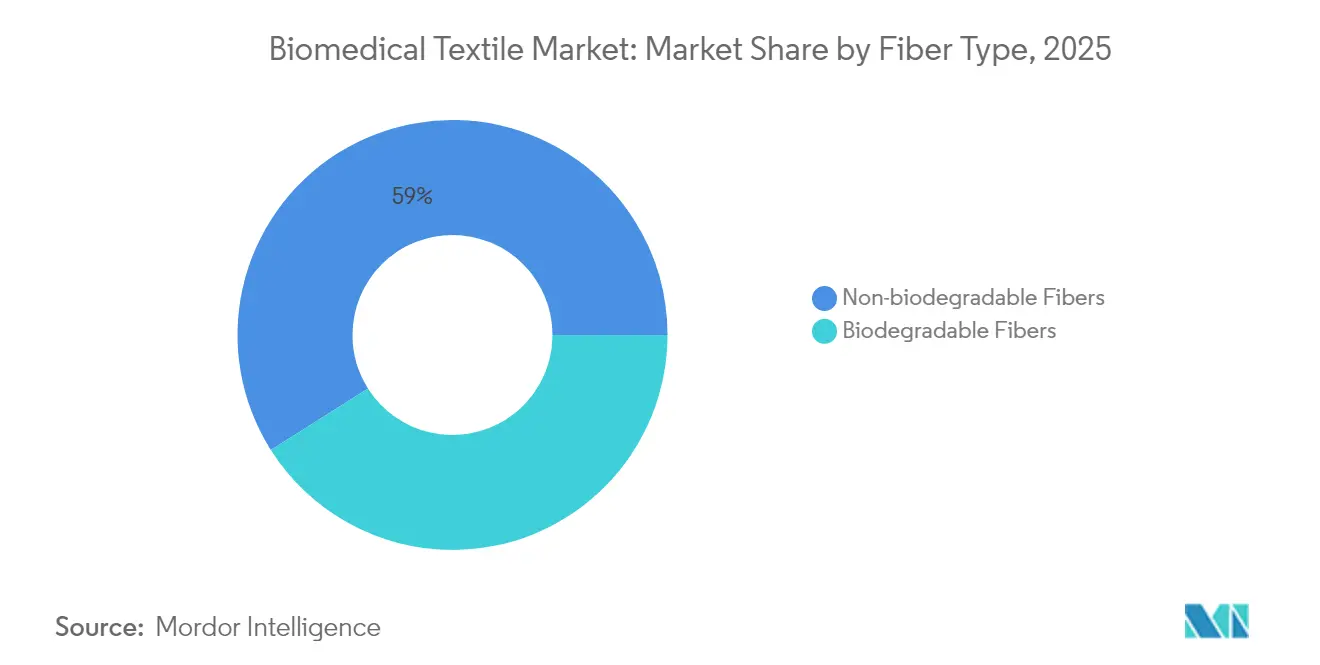

- By fiber type, non-biodegradable fibers held 58.98% of the biomedical textile market share in 2025, while biodegradable fibers are projected to expand at an 7.68% CAGR through 2031.

- By fabric form, non-woven textiles captured 61.85% revenue share in 2025; the segment is forecast to grow 8.14% annually to 2031.

- By application, non-implantable products accounted for 53.92% of the biomedical textile market size in 2025, whereas implantables are set to advance at a 6.79% CAGR between 2026-2031.

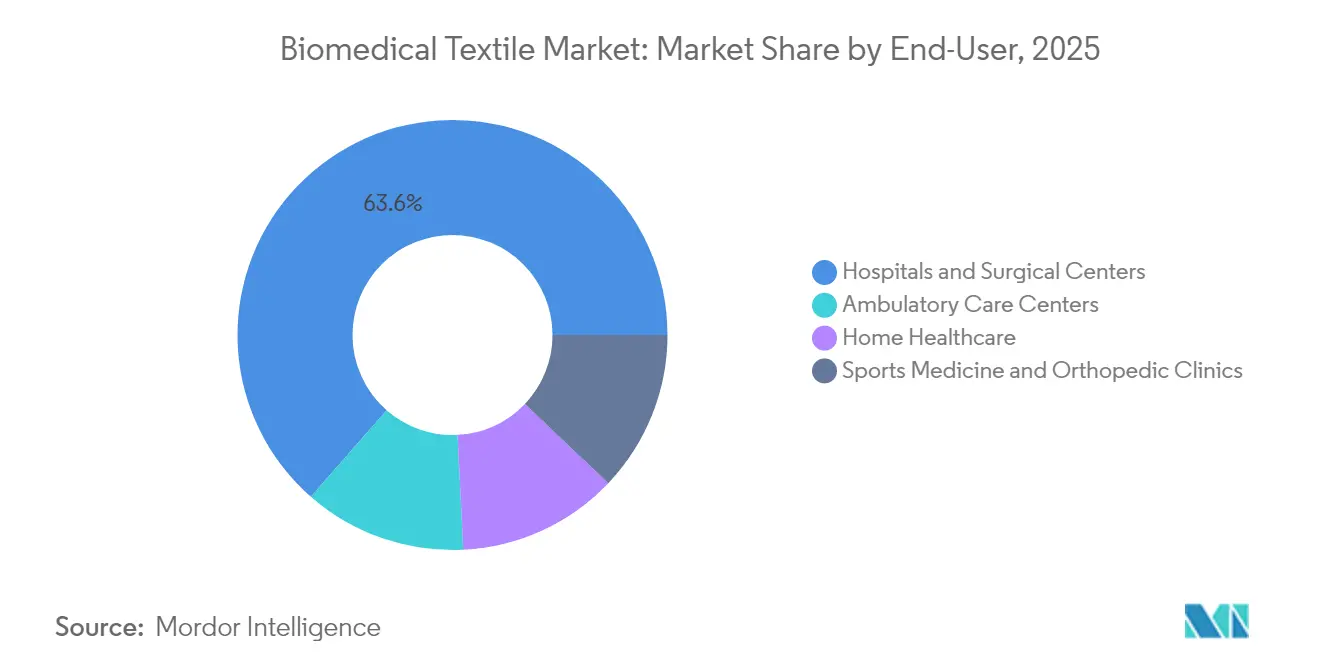

- By end-user, hospitals and surgical centers commanded 63.55% share of the biomedical textile market in 2025 and are growing at a 7.35% CAGR to 2031.

- By geography, North America led with 37.72% of the biomedical textile market share in 2025; Asia-Pacific registers the fastest regional CAGR at 7.06% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biomedical Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising number of surgeries | +1.80% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growing need for high-quality wound‐care textiles | +1.50% | Asia-Pacific emerging markets, global hospital systems | Short term (≤ 2 years) |

| Rapid ageing population in key economies | +1.20% | North America, Europe, Japan | Long term (≥ 4 years) |

| Advances in minimally-invasive implantable textiles | +0.90% | North America, EU, spillover to Asia-Pacific | Medium term (2-4 years) |

| Bioresorbable electro-spun nanofiber dressings entering retail channels | +0.60% | Developed markets | Short term (≤ 2 years) |

| Defense-funded sensor fabrics accelerating med-smart textile crossover | +0.40% | North America with global diffusion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Number of Surgeries

Global surgical procedures continue to climb as median ages rise and elective interventions become more accessible. The U.S. Department of Defense’s nanofabric programs, originally aimed at battlefield care, generate antimicrobial yarns and lightweight vascular grafts that transfer into civilian operating rooms[1]U.S. Department of Defense, “Advanced Functional Fabrics of America Award,” defense.gov . Hospitals integrate programmable fibers that record temperature and pH at incision sites, letting surgeons detect infection risk without removing dressings. Asia-Pacific hospitals accelerate adoption because improved insurance coverage brings larger middle-class cohorts into surgical theaters, amplifying textile consumption per case.

Growing Need for High-Quality Wound Care Textiles

Advanced dressings shorten recovery, lower readmissions, and reduce nursing time. Electro-spun nanofiber products, such as Spincare, achieved 46.6% epithelialization without rehospitalization versus conventional gauze in clinical trials. Chinese factories boost output for export while also meeting domestic demand for multifunctional silver-ion mats that limit bacterial growth. Wearable biosensors now embed graphene traces into spun-bond substrates, allowing home-care nurses to remotely read wound moisture on mobile dashboards[2]Nature Research, “Self-Powered Biosensors for Wound Monitoring,” nature.com . These capabilities align with payer pressure to shift chronic-wound treatment from inpatient wards to outpatient and home settings.

Rapid Aging Population

Life expectancy improvements in Japan, Germany, and the United States enlarge cohorts that need orthopedic repairs, vascular grafts, and decubitus ulcer dressings. Biomimetic scaffolds woven from collagen-coated polylactic acid replicate extracellular matrices and accelerate granulation in elderly skin. Long-term care facilities deploy smart bedding that tracks shear forces, warning staff before pressure injuries form. These developments lock in durable demand for patient-specific textile interventions.

Advances in Minimally-Invasive Implantable Textiles

Surgeons favor micro-braided stents and small-diameter knitted grafts that pass through 6-F catheters yet expand to full luminal size once in place. Electrospinning marries polyurethane elasticity with polyglycolic acid resorption, yielding graft walls that support endothelialization and then vanish within 12 months. The FDA’s latest 2025 guidance clarifies cytotoxicity and hemocompatibility test thresholds, accelerating 510(k) clearances for textile implants. Adding fiber-optic filaments permits post-implant strain monitoring, enabling earlier intervention if dilatation occurs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of vascular grafts & artificial skin | -0.80% | Emerging markets, global price-sensitive payers | Medium term (2-4 years) |

| Electronic-textile integration complexity | -0.60% | Developed markets | Short term (≤ 2 years) |

| Absent shelf-life standards for antimicrobial biotextiles | -0.40% | Global | Long term (≥ 4 years) |

| Regulatory backlash on single-use medical nonwovens waste | -0.30% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Vascular Grafts & Artificial Skin

Tissue-engineered grafts require sterile cleanrooms, multi-week cell seeding, and precision weaving, driving prices beyond reimbursement caps in many health systems. Insurance guidelines in the United States still classify numerous bioengineered dressings as investigational, limiting coverage and slowing scale economies. Without volume, unit costs remain high, deterring procurement by hospitals in Latin America and parts of Southeast Asia.

Electronic-Textile Integration Complexity

Clinical laundry exposes e-textiles to detergents and 80 °C sterilization that corrode silver and copper coatings. Tests at Ghent University showed resistance in silver-plated yarns more than doubled after 25 wash cycles, compromising signal fidelity. Certification bodies lack harmonized protocols, which forces device makers to self-define reliability metrics, prolonging market adoption. Encapsulation films and thermoplastic coatings extend life but increase weight and inhibit breathability, forcing trade-offs that slow specification in critical-care garments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Type: Biodegradable Innovation Drives Future Growth

Biodegradable threads account for 41.02% of 2025 revenue, yet are pacing the biomedical textile market at an 7.68% CAGR through 2031. FDA recognition of poly-lactic acid and poly-caprolactone resorption profiles opens regulatory doors, and surgeons value scaffolds that dissolve, eliminating follow-up retrieval. Start-ups now coat polylactic acid microfibers with honey-derived antimicrobials to meet infection control goals without systemic antibiotics.

Non-biodegradable fibers such as polyethylene terephthalate retain dominance where permanent load-bearing is vital, including ligament repairs and hernia meshes. They hold 58.98% of the biomedical textile market share, supported by decades of clinical data. Producers invest in low-shedding yarn treatments that reduce particle release during long implants. Together, these dual fiber classes widen supplier portfolios and let procurement teams match materials to procedure complexity, reinforcing the resilience of the biomedical textile market.

By Fabric Form: Non-woven Dominance Across Metrics

Non-woven lines posted 61.85% 2025 revenue and deliver the sector’s highest 8.14% CAGR due to melt-blown versatility and inline lamination that embeds hydrogel layers for moisture balance. Production scale allows Freudenberg to recycle 7 million PET bottles daily into single-use drapes that meet ISO 13432 compostability thresholds. Hospitals favor these drapes for reduced lint and rapid barrier deployment.

Woven and knitted formats serve niche implantables that demand precise tensile strength and controlled porosity. Engineers now weave 3D bifurcated tubes that mimic natural blood-vessel branches, expanding indications for textile-based endovascular grafts. Hybrid constructions that laminate a melt-blown antimicrobial core between warp-knit covers converge benefits of both worlds, a trend that helps sustain broad-based growth in the biomedical textile market.

By Application: Implantable Growth Outpaces Non-implantable Volume

Non-implantables, covering surgical masks, gowns, and wound pads, secured 53.92% of 2025 revenue. Volume surged during pandemic-driven inventory overhauls, and institutional stock policies keep baseline demand high. However, implantables expand 6.79% annually as scaffolded tissue engineering shifts from experimental to reimbursable therapy. Knitted polyester-urethane heart patches seeded with autologous cells now show 12-month retention with no calcification in early clinical cohorts.

Extracorporeal textiles, while smaller, post steady orders for dialysis and oxygenation membranes. Smart sensors embedded in implantable meshes transmit real-time strain data to surgeons, allowing remote monitoring and proactive revision. This digital layer raises implant value, reinforcing premium pricing and bolstering revenue diversity within the biomedical textile market size figures for 2026-2031.

By End-user: Hospital Centricity Sustains Share and Growth

Hospitals and surgical centers consumed 63.55% of biomedical textiles in 2025 and are growing fastest at 7.35% because sterile protocols and high case volumes require continuous replenishment. Many facilities upgrade to antimicrobial curtains and bedding that cut pathogens by 95% within 15 minutes of contact, aligning with infection-control mandates. Operating-room managers also specify RFID-tagged drapes to automate inventory counts, streamlining cost coding.

Ambulatory surgery centers and home-health providers adopt lightweight wraps with integrated biosensors for wound moisture and temperature, fueling emerging demand. Sports clinics request elastic compression socks that house accelerometers to track rehabilitation kinetics. Such diversification embeds biomedical textile market products along an extended care continuum, supporting resilience against procedure-mix shifts.

Geography Analysis

North America commands 37.72% 2025 revenue, driven by broad insurance coverage and rapid translation of federally funded textile research into commercial supply chains. The Department of Defense’s USD 75 million smart-fabric program delivered sensor yarns now appearing in civilian negative-pressure wound dressings. FDA biocompatibility guidance released in 2025 streamlines approvals, letting local firms secure early-mover contracts. Capital investment from device majors such as Smith & Nephew anchors regional manufacturing clusters in Massachusetts and Minnesota.

Asia-Pacific posts a 7.06% CAGR to 2031 as governments expand universal health insurance and stimulate domestic medtech output. China aggressively scales nanofiber lines to meet both export orders and home demand, while Japan funds geriatric remote-care pilots that rely on sensor-integrated gauze. Regulatory harmonization through ASEAN Medical Device Directives gradually lowers entry barriers, supporting multinational and regional vendors alike.

Europe blends advanced regulation with sustainability imperatives. The EU Single-Use Plastics Directive bans certain fossil-based disposables, prompting hospitals to trial Lenzing’s cellulosic stent covers and bio-based nonwoven pads. Freudenberg leverages the Heytex acquisition to supply polyurethane-coated substrates for negative-pressure therapy devices. Nonetheless, waste-reduction rules raise compliance costs; suppliers succeed by certifying compostability and closed-loop recycling audits.

South America and the Middle East & Africa trail on value but show accelerating unit growth as tertiary hospitals open and governments subsidize trauma networks. Cost-optimized spun-bond wound pads made from locally recycled PET balance price sensitives with adequate barrier function. International NGOs aid procurement training, helping clinicians choose evidence-backed textile solutions and broadening the biomedical textile market footprint.

Competitive Landscape

The biomedical textile market remains fragmented. B. Braun SE, Cardinal Health, dsm-firmenich, Freudenberg Performance Materials, and Medline Industries LP collectively hold roughly 30% share, anchoring a field of more than 200 specialist weavers and converters. Scale players deepen defensible niches through M&A: Freudenberg’s EUR 100 million Heytex deal adds coated technical fabrics that complement its wound-care nonwovens, while Lenzing’s stake in TreeToTextile secures access to low-carbon cellulosic feedstock.

Smaller innovators target white-space in sensor integration and biodegradable elastomers. U.S. start-up SynTiss integrates micro-LEDs into braided sutures for intraoperative illumination, and India-based BioWeave optimizes banana-fiber vascular patches for price-sensitive markets. Continuous capital inflow from strategic venture arms accelerates pilot-to-clinic timelines. Competitive intensity centers on intellectual property around electrospinning nozzles, antimicrobial coatings, and wash-durable circuitry.

Regulatory expertise is a key differentiator. Firms with ISO 13485 plants and in-house toxicology labs navigate faster toward FDA and EU MDR approvals, shortening customer lead times. Environmental audits further filter vendors, as hospitals increasingly demand verified recycling or composting pathways for disposable gowns. Those able to pair clinical efficacy with eco-credentials secure multi-year supply contracts, reinforcing margins despite commodity polymer volatility.

Biomedical Textile Industry Leaders

B. Braun SE

Cardinal Health

dsm-firmenich

Freudenberg Performance Materials

Medline Industries LP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cortland Biomedical has achieved FDA registration, officially broadening its capabilities to include full-service biomedical-textile contract manufacturing in the United States. This milestone is projected to positively impact the biomedical textile market by increasing domestic production capacity and advancing the industry.

- October 2024: Lenzing Group has acquired a minority stake in TreeToTextile AB, partnering with H&M Group and Inter IKEA Group to drive advancements in sustainable cellulose fiber production for medical and textile applications. This collaboration is poised to boost the biomedical textile market through eco-friendly and innovative materials.

Global Biomedical Textile Market Report Scope

The biomedical textiles market report includes:

| Non-biodegradable Fibers |

| Biodegradable Fibers |

| Non-woven |

| Woven |

| Other Fabric Types (Knitted, Braided) |

| Non-implantable |

| Implantable |

| Other Implantable (Extracorporeal, etc.) |

| Hospitals and Surgical Centers |

| Ambulatory Care Centers |

| Home Healthcare |

| Sports Medicine and Orthopedic Clinics |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Fiber Type | Non-biodegradable Fibers | |

| Biodegradable Fibers | ||

| By Fabric Form | Non-woven | |

| Woven | ||

| Other Fabric Types (Knitted, Braided) | ||

| By Application | Non-implantable | |

| Implantable | ||

| Other Implantable (Extracorporeal, etc.) | ||

| By End-user | Hospitals and Surgical Centers | |

| Ambulatory Care Centers | ||

| Home Healthcare | ||

| Sports Medicine and Orthopedic Clinics | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the biomedical textile market size in 2026?

The biomedical textile market size stands at USD 17.75 billion in 2026.

Which fabric form leads the biomedical textile market?

Non-woven textiles lead, holding 61.85% of 2025 revenue and expanding at an 8.14% CAGR to 2031.

Which region is growing fastest in the biomedical textile market?

Asia-Pacific is the fastest-growing region, projected to rise at a 7.06% CAGR through 2031.

Why are biodegradable fibers gaining popularity in the biomedical textile industry?

They eliminate secondary removal surgeries, address sustainability mandates, and now follow clearer FDA biocompatibility guidance.

How does electronic-textile integration affect market growth?

Integration challenges around wash durability and reliability currently subtract 0.6 percentage points from forecast CAGR, but breakthroughs in encapsulation are narrowing this gap.

What share of the biomedical textile market do hospitals hold?

Hospitals and surgical centers account for 63.55% of 2025 revenue and are expanding at 7.35% annually.

Page last updated on: