Mobile Stroke Unit Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

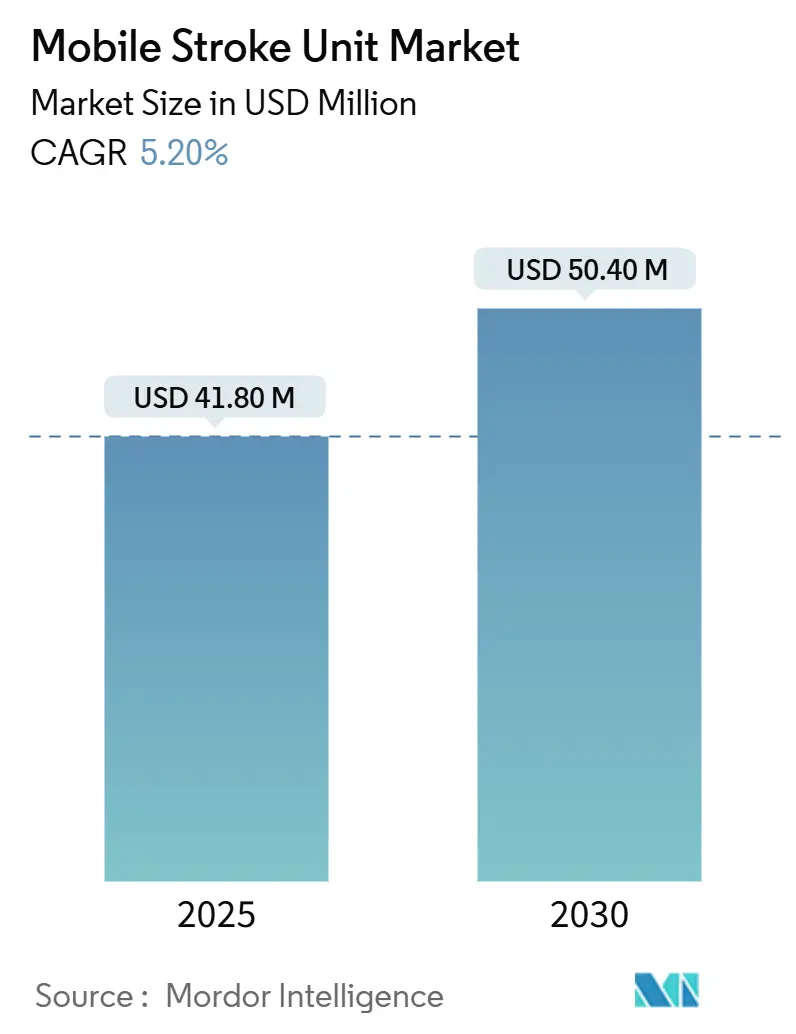

| Market Size (2025) | USD 41.80 Million |

| Market Size (2030) | USD 50.40 Million |

| Growth Rate (2025 - 2030) | 5.20% CAGR |

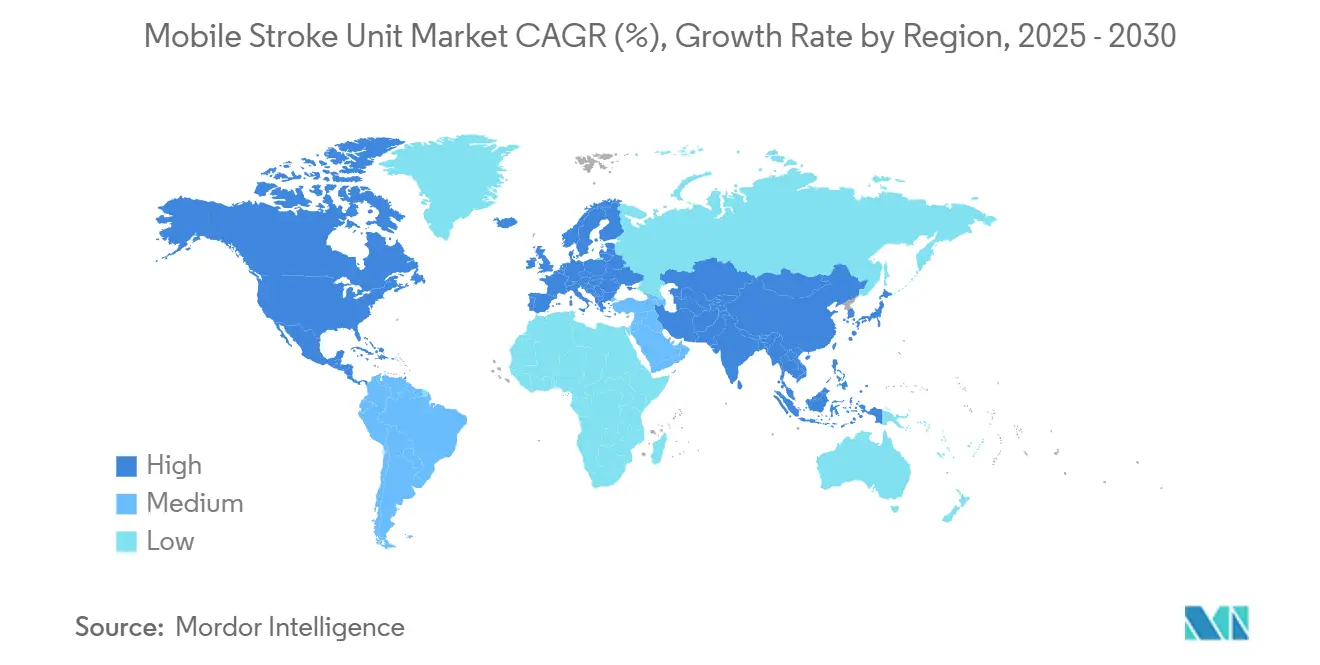

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Stroke Unit Market Analysis by Mordor Intelligence

The mobile stroke unit market size stands at USD 41.8 million in 2025 and is forecast to reach USD 50.4 million by 2030, reflecting a 5.2% CAGR over the period. Growing stroke incidence, rapid technology advances in portable CT imaging, and evolving reimbursement frameworks are the primary forces propelling the expansion of the Mobile stroke unit market. Health-system chief financial officers increasingly view pre-hospital stroke treatment as a route to lower long-term disability costs. At the same time, hospital networks use partnership models to spread the heavy capital load of each unit. Leading imaging vendors are introducing photon-counting CT and AI-based triage tools that shorten diagnostic cycles and elevate clinical confidence in field decisions. On the demand side, aging populations in North America, Europe, Japan, and Australia guarantee a steadily rising caseload, assuring steady utilization rates that underpin investment returns.

Key Report Takeaways

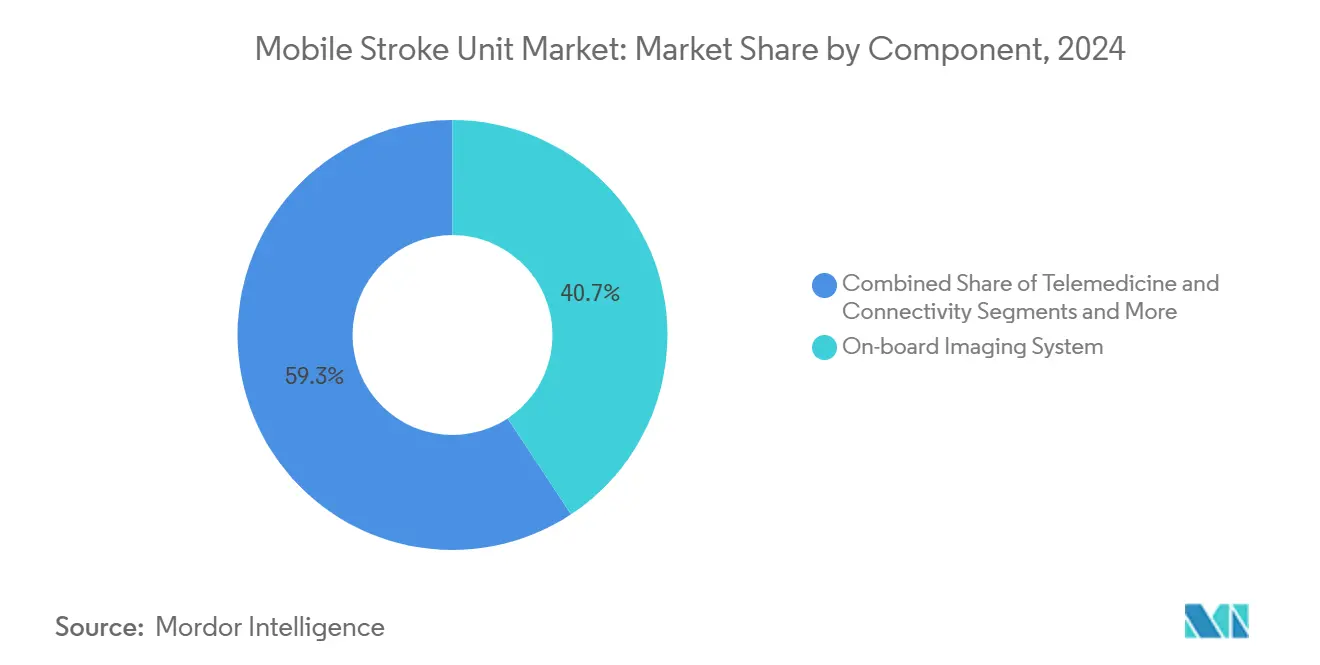

- By component, onboard imaging systems held 40.7% of the mobile stroke unit market share in 2024, while telemedicine and connectivity are projected to expand at a 17.4% CAGR through 2030.

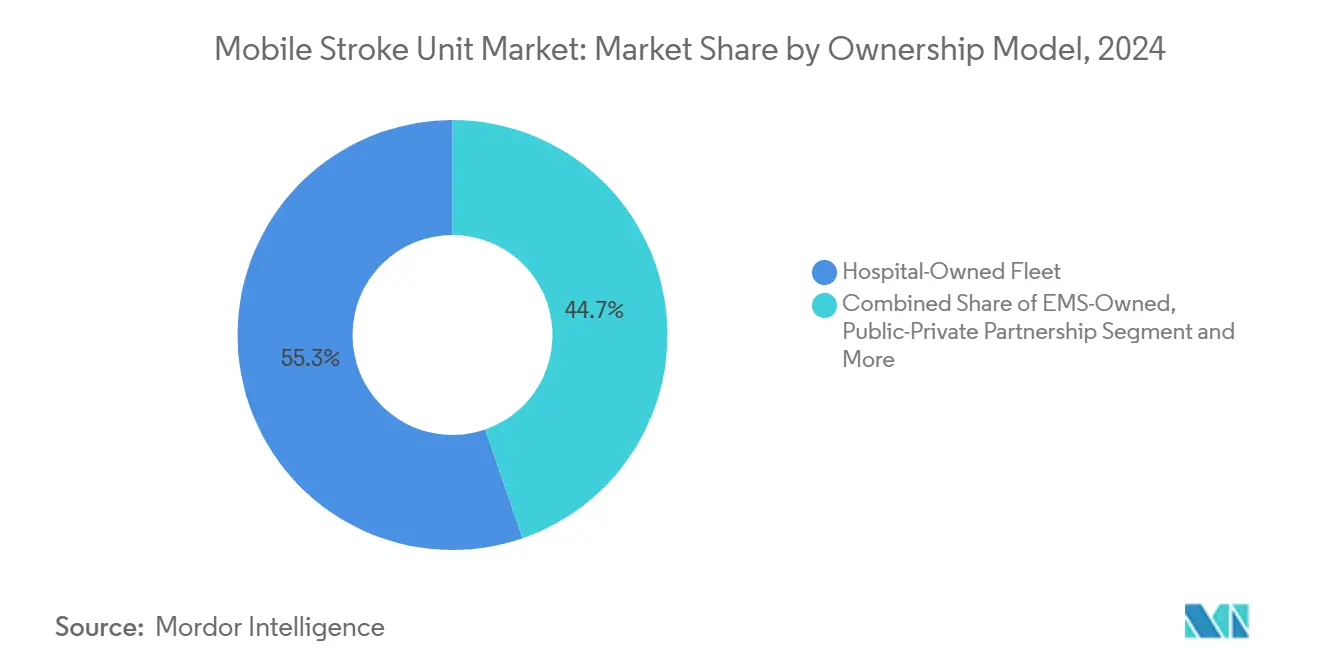

- By ownership model, hospital-owned fleets accounted for 55.3% of the mobile stroke unit market size in 2024; public-private partnership fleets are poised to grow at a 16.5% CAGR to 2030.

- By geography, North America led with 46.2% revenue in 2024, but Asia Pacific is set to post the fastest 12.6% CAGR to 2030

Global Mobile Stroke Unit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Stroke Incidence & Ageing Population | +1.80% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Clinical Evidence Of Improved Door-To-Needle Time | +1.20% | Global, particularly urban centers in developed markets | Medium term (2-4 years) |

| Rising Healthcare Expenditure & Pre-Hospital Care Adoption | +0.90% | North America, Western Europe, Asia Pacific developed markets | Medium term (2-4 years) |

| Portable CT & POC Diagnostics Breakthroughs | +0.70% | Global, with technology leadership from North America & Europe | Short term (≤ 2 years) |

| Medicaid & Payer Reimbursement Revisions (US) | +0.40% | United States primarily, with spillover to Canada | Short term (≤ 2 years) |

| Military/Disaster-Response MSU Pilots | +0.20% | Global, focused on disaster-prone regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Stroke Incidence & Aging Population

Global stroke burden keeps climbing, with 11.9 million incident strokes recorded in 2021.[1]Valery L. Feigin et al., “Global, Regional, and National Burden of Stroke and Its Risk Factors, 1990–2021,” The Lancet Neurology, thelancet.com Forecasts point to stroke prevalence doubling by 2050, largely concentrated in adults over 60. France’s Dijon registry predicts cerebrovascular events will rise 35% by 2035 and 56% by 2050, primarily because of aging demographics.[2]Jessalyn K. Holodinsky et al., “In What Scenarios Does a Mobile stroke unit Predict Better Patient Outcomes?” Stroke, ahajournals.org Mobile stroke units treat patients inside the critical 60-minute therapeutic window at rates ten times higher than conventional EMS, reinforcing their role in future stroke infrastructure. Urbanization intensifies demand by concentrating older patients in metropolitan areas where rapid response is feasible. Together, demographic pressure and city clustering sustain a resilient growth base for the mobile Stroke Unit market.

Clinical Evidence of Improved Door-to-Needle Time

Randomized and observational studies confirm superior outcomes when thrombolysis begins inside MSUs, with time savings of 29–48 minutes versus standard transport. The BEST-MSU multicenter trial showed statistically significant utility-weighted disability benefits at 90 days in MSU-treated cohorts. Door-to-needle times under 30 minutes correlate with 22.7% lower hospitalization costs and markedly better functional recovery.[3]Jia Dong James Wang et al., “Improved Functional Outcomes and Cost Benefits of Door-to-Needle Time Under 30 min,” Frontiers in Stroke, frontiersin.org Tissue-defined averted strokes rose to 18% with MSUs compared with 11% in standard care, strengthening the economic rationale for providers. These clinical validations translate directly into increased hospital C-suite support for Mobile stroke unit market deployments.

Rising Healthcare Expenditure & Pre-Hospital Care Adoption

U.S. emergency department treatment costs climbed from USD 54 billion in 2012 to USD 88 billion in 2019. Medicare ambulance transports rose 15% from 2007-2018, with rural cost growth 38% higher than urban. Health-economics modelling in Norway finds MSU care yields an incremental 0.065 QALY gain per patient and meets willingness-to-pay thresholds at annual volumes above 260 patients. U.S. ET3 reimbursement pilots project cumulative savings of USD 69.8 million if widely adopted. These data underpin payer enthusiasm, boosting capital access and accelerating the mobile stroke unit market uptake.

Portable CT & Point-of-Care Diagnostics Breakthroughs

NeuroLogica’s OmniTom Elite photon-counting CT secured 510(k) clearance in 2024, offering 0.141 mm resolution with a 30 cm field-of-view. Compact cone-beam CT with antiscatter grids improves image fidelity yet shrinks footprint for easier chassis integration. GFAP + D-dimer biomarker panels achieve 93% specificity and 81% sensitivity for large-vessel-occlusion stroke screening. These advances shrink the technology gap between hospital and roadside care, allowing OEMs to pitch lighter, less power-hungry MSU platforms and sustaining growth momentum in the Mobile stroke unit market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Operating Cost Of MSUs | -1.40% | Global, particularly pronounced in emerging markets | Medium term (2-4 years) |

| Shortage Of Neuro-Radiology Staff | -0.80% | Global, with acute shortages in rural and developing regions | Long term (≥ 4 years) |

| Regulatory Ambiguity For Mobile Radiation Use | -0.60% | Global, with varying regulatory frameworks across jurisdictions | Medium term (2-4 years) |

| Patchy 5G/Tele-Connectivity In Rural Areas | -0.40% | Rural regions globally, particularly in developing markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Operating Cost of MSUs

A single fully equipped unit costs more than CAD 1 million plus specialized staffing outlays. Houston’s program required USD 1.5 million initial funding and ongoing maintenance, driving CFO caution in low-volume catchments. Cost-effectiveness models show viability only above certain patient thresholds, limiting rural deployments. Supply chain shocks, such as the 2022 contrast-media shortage that cut CT perfusion scans 26%, expose further cost risk. As inflation lifts component prices, smaller providers defer purchase, tempering near-term growth in the Mobile stroke unit market.

Shortage of Neuro-Radiology Staff

Hospital audits in the UK report one-quarter of consultant stroke physician posts unfilled. Saudi Arabia calculates a need for 97 additional stroke specialists to meet guideline ratios. Credentialing barriers further slow pipeline expansion, as seen in the UK mechanical thrombectomy program. Remote MR scanning and tele-radiology mitigate gaps but depend on reliable broadband. Workforce scarcity, therefore, caps the operational hours MSUs can sustain, limiting mobile Stroke Unit market penetration in underserved regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Imaging Technology Drives Market Leadership

On-board imaging systems generated the most significant revenue slice, securing 40.7% of the mobile stroke unit market size in 2024. Persistent clinical proof that field CT shortens decision-to-treatment intervals underpins demand for premium scanners. Siemens Healthineers’ SOMATOM On.site telescopic gantry achieves full-body head imaging without moving patients, enhancing workflow. Competition intensified after NeuroLogica’s OmniTom Elite photon-counting CT won 2024 clearance, nudging image resolution into sub-millimeter territory. Telemedicine & connectivity ranks as the fastest-growing component, racing at 17.4% CAGR on the back of 5G rollouts and AI triage platforms from Brainomix and Methinks. Point-of-care laboratory systems expand as GFAP-D-dimer assays prove field utility. Vehicle chassis makers, Frazer and Demers, co-develop low-vibration mounts that shield delicate detectors, locking in OEM partnerships and lifting the Mobile stroke unit market share of integrated system suppliers.

Technological miniaturization is shrinking generator footprints and slashing power consumption, opening doors for electric or hybrid ambulance bases. Meanwhile, regulatory authorities such as the FDA’s Office of Supply Chain Resilience publicly list at-risk imaging components, helping purchasers avoid procurement shocks. Collective progress elevates imaging performance to hospital equivalency, supporting wider adoption of Mobile stroke unit market offerings across metropolitan and secondary cities.

By Ownership Model: Partnership Models Accelerate Growth

Hospital-owned fleets dominated 2024 revenue with a 55.3% slice of the Mobile stroke unit market share, leveraging in-house neurology staffing and 24/7 command centers. Yet public-private partnership fleets post the highest growth at 16.5% CAGR. The Australian Stroke Alliance’s AUD 40 million grant exemplifies government injections that de-risk first deployments. Alberta Health Services operates Canada’s research-backed MSU in a hybrid model linking university stroke fellows with provincial EMS. Private EMS operators eye ET3 incentives to offset staffing expenses, while insurers gain from avoided downstream rehabilitation costs. These aligned interests are catalyzing innovative lease-back or subscription structures, widening the Mobile stroke unit market.

EMS-owned fleets lag because they must add imaging specialists atop paramedic crews, inflating payroll. Nonetheless, pilot programs in Texas and North Carolina test AI-guided CT workflows that could cut on-board staffing requirements. Over the forecast horizon, flexible financing and cloud-based teleradiology promise to level capital and personnel hurdles, keeping partnership models at the forefront of Mobile stroke unit market expansion.

Geography Analysis

North America remains the anchor for global deployments. The Houston mobile stroke unit program documents 40-minute faster treatment and 20% more patients receiving thrombolysis than standard EMS, shaping U.S. best practice. Medicare’s G0 modifier and ET3 flexibilities shorten return-on-investment horizons, magnetizing private equity into service contracts. Canada’s prairie provinces use MSUs to bridge distances exceeding 300 kilometers between tertiary centers, proving the platform’s value in sparsely populated geographies. Collectively, payer alignment and strong evidence lock in a stable growth lane for the Mobile stroke unit market in North America.

Europe represents the most mature clinical research arena. Germany’s STEMO initiative built the foundational cost-effectiveness dataset, and the EUR 26.9 million UMBRELLA project unites 20+ partners to integrate AI decision support across fleets. France’s thrombectomy gap, with only 7,500 cases treated versus a 20,500 potential, demonstrates latent demand that MSUs could address. Harmonized CE-IVDR rules ease multi-country rollouts, positioning Europe as the second-largest Mobile stroke unit market by 2030.

Asia-Pacific is the fastest-growing geography, albeit from a small base. Japan’s Kanazawa Mobile Embolectomy Team achieved 80% revascularization success in early cohorts. India’s first MSU in Coimbatore cut door-to-needle to 55 minutes but still battles limited public awareness. China’s deployments shaved call-to-needle averages from 89 to 59.5 minutes, although scale-up hinges on provincial funding. Australia, with strong federal grants, is piloting ruggedized MSUs for bush settings, marking the region as a testbed for next-generation designs. These advances point toward a rising Mobile stroke unit market footprint across Asia-Pacific by the decade’s end.

Competitive Landscape

The mobile stroke unit market exhibits moderate fragmentation. Siemens Healthineers leverages its SOMATOM On.site platform and leads the UMBRELLA consortium that funnels real-world data into algorithmic stroke triage. GE HealthCare collaborates with Stanford Medicine on photon-counting CT, seeking leadership in ultra-high-resolution imaging. Medtronic partners with Brainomix and Methinks to layer AI onto fleet operations, differentiating its proposition through software ecosystems.

Vehicle integrators Frazer, Demers, and U.S. upstart Excellance compete on chassis customization, vibration damping, and power management. Supply-chain resilience becomes a deciding factor; Medtronic’s 2024 restructuring cut its supplier roster and consolidated distribution centers to manage geopolitical disruptions. OEMs compliant with FDA Section 506J disruption reporting gain a reputation boost among hospital buyers wary of shortages. Over the forecast window, AI enablement, service packages, and financing creativity will determine who captures the rising Mobile stroke unit market share.

White-space lies in rural zones of the United States, Latin America, and Africa where stroke mortality remains high yet fleet economics are challenging. Manufacturers are experimenting with modular CT pods that slide into existing ambulances, lowering entry price. Companies able to demonstrate interoperable, cloud-native, and low-maintenance solutions stand to consolidate an otherwise fragmented market, nudging the Mobile stroke unit market toward a moderately concentrated structure by 2030.

Mobile Stroke Unit Industry Leaders

Frazer, Ltd.

Siemens Healthineers

GE HealthCare

Koninklijke Philips N.V.

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Medtronic formed partnerships with Brainomix and Methinks AI to co-develop AI-enhanced stroke detection and care coordination solutions.

- January 2025: DocGo expanded its partnership with SHL Telemedicine to embed SmartHeart portable ECG devices into mobile health units.

- October 2024: Siemens Healthineers and the World Stroke Organization launched a two-year collaboration to widen global stroke-care access.

Global Mobile Stroke Unit Market Report Scope

| Vehicle/Chassis |

| On-board Imaging System |

| Telemedicine & Connectivity |

| Point-of-Care Laboratory |

| Pharmaceuticals & Consumables |

| Hospital-Owned Fleet |

| EMS-Owned Fleet |

| Public-Private Partnership Fleet |

| Government / Public Health Agency Fleet |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Vehicle/Chassis | |

| On-board Imaging System | ||

| Telemedicine & Connectivity | ||

| Point-of-Care Laboratory | ||

| Pharmaceuticals & Consumables | ||

| By Ownership Model | Hospital-Owned Fleet | |

| EMS-Owned Fleet | ||

| Public-Private Partnership Fleet | ||

| Government / Public Health Agency Fleet | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the global Mobile stroke unit market size in 2025?

The Mobile stroke unit market size is USD 41.8 million in 2025 and is projected to climb steadily through 2030.

How fast is the Mobile stroke unit market expected to grow?

The market is forecast to register a 5.2% CAGR from 2025-2030, driven by rising stroke incidence and technology advances.

Which component holds the largest revenue share?

On-board imaging systems lead with 40.7% share, reflecting their central role in rapid diagnosis.

Which ownership model is growing the fastest?

Public-private partnership fleets are expanding at a 16.5% CAGR as innovative financing spreads capital risk.

Why are Mobile stroke units considered cost-effective?

Studies show MSUs cut door-to-needle by up to 48 minutes and reduce long-term disability, yielding favorable cost per QALY outcomes in high-volume regions.

What technological breakthrough is most influential right now?

Photon-counting CT and AI-aided triage, which raise image resolution and decision accuracy while fitting inside ambulance constraints.

Page last updated on: