Acute Ischemic Stroke Diagnosis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

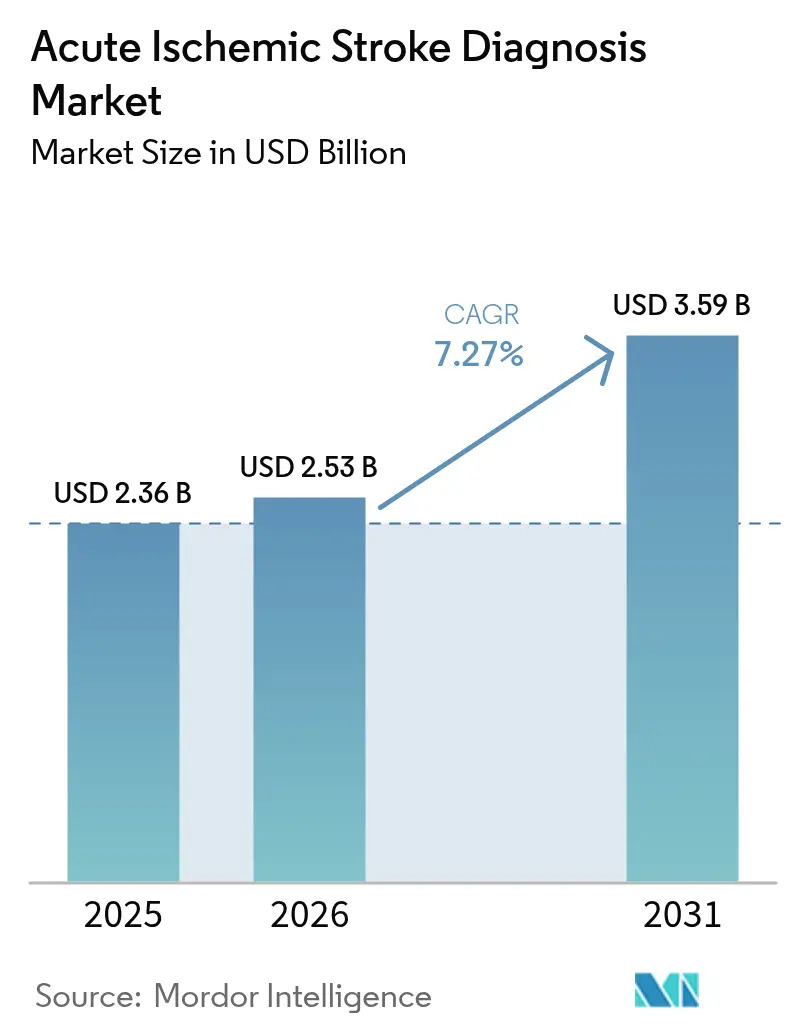

| Market Size (2026) | USD 2.53 Billion |

| Market Size (2031) | USD 3.59 Billion |

| Growth Rate (2026 - 2031) | 7.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acute Ischemic Stroke Diagnosis Market Analysis by Mordor Intelligence

The acute ischemic stroke diagnosis market size is expected to grow from USD 2.36 billion in 2025 to USD 2.53 billion in 2026 and is forecast to reach USD 3.59 billion by 2031 at 7.27% CAGR over 2026-2031. Aging populations, guideline-driven expansion of mechanical thrombectomy time windows, and the steady infusion of artificial intelligence into emergency radiology are lifting procedure volumes and driving software adoption. Computed tomography (CT) remains the dominant front-line modality, yet AI-enabled stroke triage platforms—now cleared by the U.S. Food and Drug Administration—are shifting capital budgets toward subscription software that accelerates large-vessel occlusion routing. Hospitals are prioritizing door-to-needle metrics because Medicare, European payors, and Japanese insurers attach reimbursement bonuses to imaging-guided workflow performance. North America leads revenue because of its broad network of comprehensive stroke centers, while Asia-Pacific shows the fastest growth as national stroke registries in China and India mandate multimodal imaging for suspected large-vessel occlusion.

Key Report Takeaways

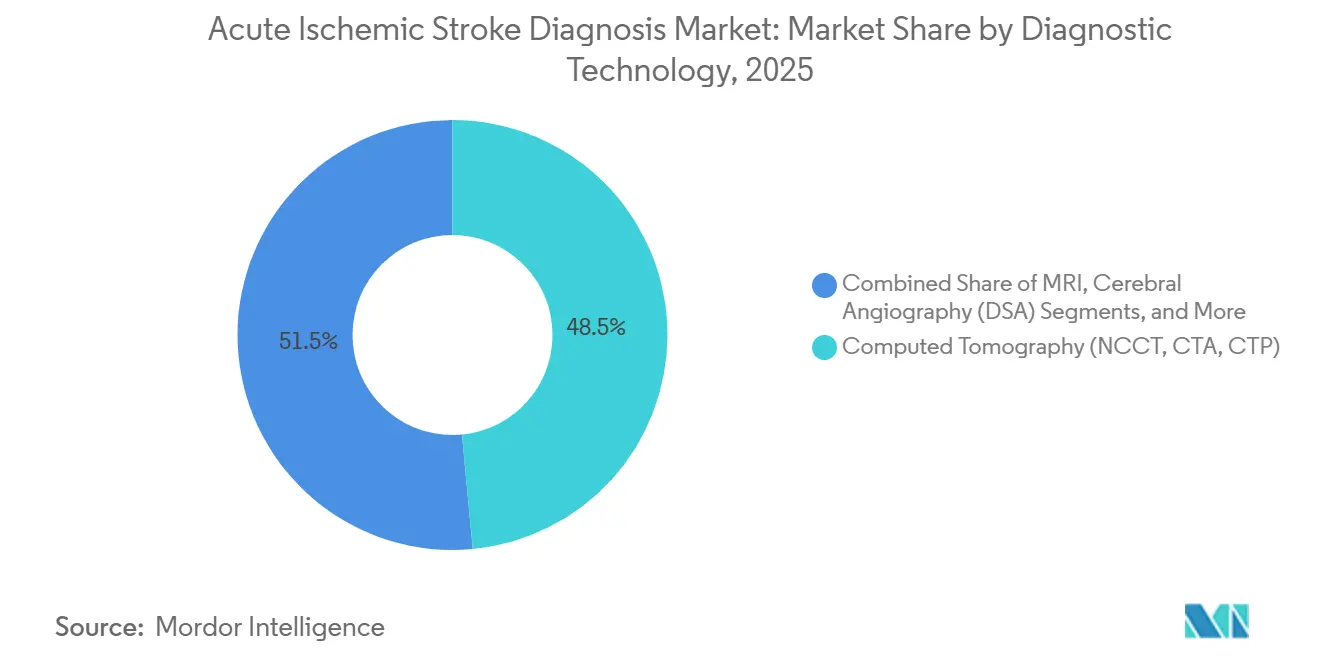

- By diagnostic technology, computed tomography captured 48.55% of 2025 revenue, while AI-enabled stroke decision-support software is projected to expand at 14.25% CAGR through 2031.

- By AI software function, large-vessel occlusion detection algorithms held 40.53% of AI software revenue in 2025; perfusion mismatch quantification tools are advancing at 16.75% CAGR through 2031.

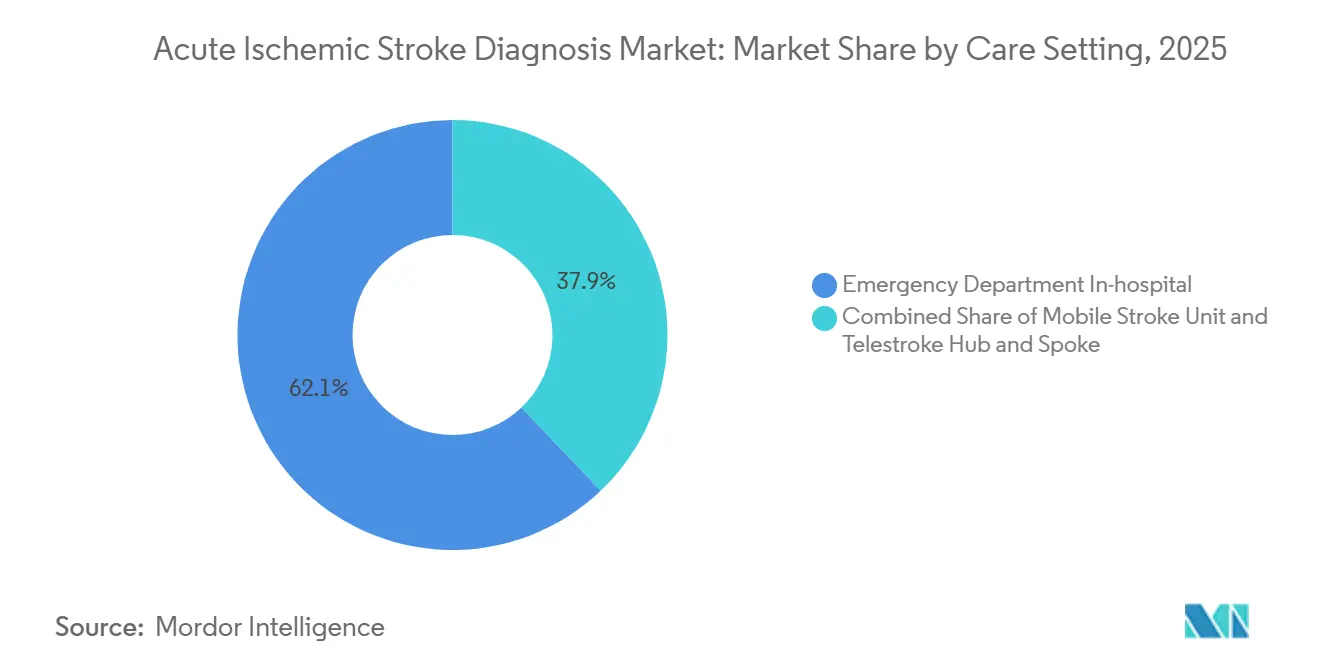

- By care setting, emergency departments generated 62.15% of 2025 care-setting revenue, yet mobile stroke units are forecast to climb at 15.82% CAGR as municipalities deploy CT-equipped ambulances.

- By end user, hospitals accounted for 74.65% of end-user revenue in 2025; ambulatory surgery and diagnostic imaging centers are growing at 12.32% as outpatient facilities add non-contrast CT for rapid hemorrhage exclusion.

- By geography, North America contributed 36.23% of global revenue in 2025, whereas Asia-Pacific is projected to expand at 11.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acute Ischemic Stroke Diagnosis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing AIS incidence in 65-plus population | +1.2% | North America, Europe, East Asia | Long term (≥ 4 years) |

| Wider adoption of multimodal CT & MR imaging | +1.5% | North America, Western Europe, urban APAC | Medium term (2-4 years) |

| Expanding endovascular-thrombectomy window | +1.8% | Global OECD stroke centers | Medium term (2-4 years) |

| Quality initiatives & reimbursement metrics | +1.3% | United States, Germany, United Kingdom, Australia, Japan | Short term (≤ 2 years) |

| Photon-counting CT & 7 T MRI adoption | +0.9% | Academic centers in North America and Europe | Long term (≥ 4 years) |

| Subscription AI bundles with teleradiology | +1.4% | North America, Western Europe, India, Brazil | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing AIS Incidence in 65-Plus Population

The share of the global population aged 65 and older will reach 16% by 2030, and stroke incidence doubles with each successive decade after 65, sustaining diagnostic demand even in regions with plateauing age-adjusted rates. Japan already mandates CT or MRI within 60 minutes of presentation for suspected stroke, a policy response to the fact that 75% of domestic cases occur in seniors. U.S. Medicare data show rising hospitalizations for mild strokes thanks to faster pre-hospital recognition and imaging, further enlarging the pool of patients routed into acute workflows. These demographic realities create a durable tailwind for every segment of the acute ischemic stroke diagnosis market.

Wider Adoption of Multimodal CT & MR Imaging Protocols

Guidelines now recommend CT angiography and CT perfusion for all patients within 24 hours of last-known-well, normalizing tissue-based triage beyond the first 6 hours[1]American Heart Association, “2024 AHA/ASA Stroke Imaging Guidelines,” ahajournals.org. U.S. comprehensive stroke centers increased multimodal CT protocol adoption by 18% in 2025, driven by evidence that perfusion mismatch predicts favorable thrombectomy outcomes. Dual-energy CT platforms compress scan time below 3 minutes and help overcrowded emergency departments meet door-to-imaging targets. Although MRI retains superior sensitivity for posterior circulation infarcts, its longer acquisition time keeps CT in the front-line role.

Expanding Endovascular-Thrombectomy 24-Hour Time-Window

Real-world registries confirm that patients with favorable perfusion profiles benefit from mechanical thrombectomy up to 24 hours after symptom onset, doubling the treatable population[2]New England Journal of Medicine, “DAWN Trial,” nejm.org. U.S. thrombectomy volumes climbed 22% per year between 2020 and 2024, with late-window cases now one-third of all procedures. AI large-vessel occlusion detection shortens door-to-groin puncture by more than 20 minutes, strengthening the ROI case for algorithm subscriptions.

National Stroke-Care Quality Initiatives & Reimbursement Incentives

Medicare bundles, German and Japanese pay-for-performance schemes, and Australia’s federally funded telestroke network all tie payment bonuses to imaging performance metrics, turning AI adoption into a revenue-protection strategy. Hospitals unable to demonstrate CT perfusion use or quick thrombolysis face reimbursement penalties, accelerating technology diffusion across mid-tier facilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance cost of scanners | -0.8% | Emerging APAC, MEA, Latin America, small U.S. hospitals | Medium term (2-4 years) |

| Neuroradiologist shortage in emerging areas | -0.6% | Sub-Saharan Africa, Southeast Asia, rural Latin America | Long term (≥ 4 years) |

| Algorithmic-bias delaying AI clearance | -0.4% | United States and European Union | Short term (≤ 2 years) |

| Xenon-CT consumable supply disruptions | -0.2% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Cost of Advanced Scanners

Photon-counting CT lists at USD 3.2 million versus USD 1.8 million for a 128-slice CT, and annual service contracts add USD 250,000, numbers that exceed the entire equipment budget of many 200-bed hospitals. District-level hospitals in India illustrate the gap: only 14% possess CT, and fewer than 2% run MRI, constraining adoption despite government subsidies.

Shortage of Neuroradiologists in Emerging Markets

Sub-Saharan Africa averages 0.03 neuroradiologists per 100,000 residents compared with 1.2 in North America, forcing general radiologists to interpret complex perfusion scans and inducing variability that dampens thrombectomy referrals. AI can triage, yet regulations still require physician over-reads, so the bottleneck persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Diagnostic Technology: CT Dominance Meets AI Disruption

Multimodal CT imaging generated 48.55% of 2025 technology revenue, underscoring its status as the workhorse of the acute ischemic stroke diagnosis market share during hyperacute triage. The acute ischemic stroke diagnosis market size attributed to AI software, though smaller today, is projected to rise fastest because subscription pricing aligns with cash-flow-constrained hospitals. MRI maintains a foothold for posterior fossa strokes and microbleed detection, but its share will erode marginally as photon-counting CT converges on MRI-like resolution with shorter scan times.

AI decision-support software is set to scale at 14.25% CAGR through 2031 because payors reward time-to-treatment performance and radiologist shortages create demand for automated pre-reads. Early adopters report sensitivity exceeding 94% for large-vessel occlusion, while false positives remain under 8%, metrics that justify per-use fees of USD 50-80. The convergence of CT hardware upgrades with cloud-deployed AI suites positions imaging OEMs and pure-play vendors to compete on workflow speed rather than pixel quality alone.

By AI Software Function: Perfusion Quantification Gains Ground

Large-vessel occlusion detection held 40.53% of 2025 AI revenue as every stroke center now prioritizes rapid occlusion identification for thrombectomy routing. Perfusion mismatch quantification tools will capture incremental share because late-window thrombectomy protocols depend on tissue viability rather than elapsed time alone. Vendors packaging occlusion detection, perfusion maps, and hemorrhage exclusion into a single dashboard win contracts by simplifying IT integration. Mobile push notifications reduce team activation times; early data show a 23-minute median reduction in door-to-groin puncture when algorithms auto-page neurointerventional teams.

By Care Setting: Mobile Units Emerge as High-Growth Niche

Hospital emergency departments retained 62.15% share in 2025 because they remain the primary entry point for stroke patients. The acute ischemic stroke diagnosis market will still find its largest installed base inside brick-and-mortar hospitals, yet mobile stroke units are scaling fastest at 15.82% CAGR. Municipalities justify capital outlays of USD 1.2-1.5 million per ambulance by demonstrating 30-50 minute time savings that translate into better functional outcomes and lower long-term disability costs.

By End User: Hospitals Retain Dominance, Outpatient Sites Expand

Hospitals controlled 74.65% of end-user revenue in 2025, reflecting their monopoly on emergency imaging and thrombectomy infrastructure. Outpatient imaging centers and ambulatory surgery centers, however, are growing at 12.32% as value-based care models push volume toward lower-cost settings. The acute ischemic stroke diagnosis industry expects outpatient sites to install non-contrast CT primarily for hemorrhage exclusion before transferring eligible patients, capturing professional fees while avoiding the complexity of full stroke care.

Geography Analysis

North America retained 36.23% global share in 2025 because comprehensive stroke centers exceed 200 and reimbursement is tightly linked to imaging-guided quality metrics. The United States Food and Drug Administration has cleared 12 AI stroke algorithms since 2024, supplying hospitals with multiple vendor options that compete on speed, cloud integration, and subscription price. Canada’s provincial telestroke networks have shortened remote transfer times, while Mexico added 18 CT scanners to regional hospitals but still struggles with a neuroradiologist deficit that slows interpretation turnaround.

The acute ischemic stroke diagnosis market in Asia-Pacific will expand fastest at 11.42% CAGR because China and India are building stroke registries that compel imaging compliance, and private hospital chains are investing heavily in advanced scanners to appeal to medical tourists. China now operates 1,200 stroke centers, a 35% jump since 2022, and ties reimbursement to imaging protocol adherence. India’s 2024-launched cardiovascular and stroke program earmarked USD 145 million for CT procurement and physician training. Japan, already imaging 92% of stroke suspects within 60 minutes, focuses on ultra-high-field MRI to improve microvascular detection in its rapidly aging society.

Europe generated a significant revenue in 2025 as Germany’s 340 certified stroke units standardized multimodal CT perfusion, and the United Kingdom added GBP 45 million worth of scanners and AI licenses to expand thrombectomy access. France issued CE-Mark approval to eight AI stroke detection platforms in 2024, triggering rapid procurement by public and private hospitals. Middle East and Africa remain nascent but attract targeted investment; the United Arab Emirates installed 14 new CT scanners in 2024, and South Africa’s handful of comprehensive stroke centers are exploring AI to amplify limited neuroradiology capacity. South America is led by Brazil’s private chains, yet public hospitals lag, with median door-to-CT times still above 90 minutes.

Regulatory Landscape

Acute ischemic stroke diagnostic offerings cover regulated imaging hardware, software as a medical device (SaMD), and evolving IVD concepts, so market access depends on the strictest applicable regime in each geography. In the United States, AI-enabled stroke triage and decision-support tools move through FDA medical-device pathways, commonly 510(k) for many imaging software functions, and FDA stroke-related study design guidance shapes the pre-clinical and clinical evidence packages that support submissions and labeling, especially around performance validation and intended-use boundaries.

In Europe, the EU Medical Device Regulation (MDR 2017/745) and Medical Device Coordination Group (MDCG) guidance on software classification and clinical evaluation increase compliance requirements for imaging AI, including expectations for technical documentation and post-market surveillance. In China, the National Medical Products Administration (NMPA) and its Center for Medical Device Evaluation (CMDE) treat AI-based ischemic stroke CT-assisted assessment software as registrable medical device software, with technical review expectations aligned to the medical device software registration guidance (2022 revision), including requirements around data governance, algorithm performance evaluation, and quality controls for labeling and dataset curation.

Competitive Landscape

The acute ischemic stroke diagnosis market is moderately concentrated. Imaging OEMs—Siemens Healthineers, GE HealthCare, Philips, and Canon Medical Systems—leverage their installed hardware bases to bundle AI modules, while pure-play vendors Viz.ai, RapidAI, and Aidoc pursue direct contracts and teleradiology partnerships. Siemens’ Syngo.via stroke module is live at more than 800 hospitals, and 62% of those customers purchase the AI add-on, paying USD 35,000-50,000 annually. GE HealthCare integrated Viz LVO into its Revolution CT, documenting door-to-groin puncture reductions of 21 minutes across 14 validation sites.

White-space innovators focus on portability: NovaSignal’s Lucid robotic ultrasound automates transcranial Doppler in ambulances, and Hyperfine’s USD 50,000 Swoop portable MRI delivers bedside diffusion-weighted images for unstable ICU patients. Patent filings highlight next-generation photon-counting calibration techniques and federated learning architectures that train AI models without centralizing patient data, a privacy-centric design favored under Europe’s AI Act.

Regulatory clearance speed is a key differentiator; vendors with both FDA 510(k) and CE Mark secure premium pricing and faster hospital uptake, while investigational tools face longer sales cycles and require institutional review board oversight.

Acute Ischemic Stroke Diagnosis Industry Leaders

Fujifilm Holdings Corporation

Koninklijke Philips NV

Siemens Healthcare

GE HealthCare

Canon Medical Systems

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are widening beyond large-vessel-occlusion alerting toward earlier infarct identification and broader front-line workflow triage on non-contrast CT, reflecting the role of CT as the dominant first test in emergency stroke pathways. A clear market signal arrived in March 2026, when Harrison.ai received FDA 510(k) clearance for acute infarct triage on non-contrast CT brain across six vascular territories, which supports procurement demand for software that covers more of the hyperacute decision tree rather than isolated point solutions.

A second area of whitespace is rapid adjunctive diagnostics that can complement imaging in time-critical settings, including mobile stroke units and telestroke hub-and-spoke networks emphasized in contemporary clinical guidance. In June 2026, TETmedical received FDA Breakthrough Device Designation for NSE-FAST, a rapid in vitro diagnostic assay intended to aid acute ischemic stroke diagnosis, reinforcing that regulatory and R&D momentum continues around faster, scalable adjunct tests that can tighten triage workflows when scanner access, specialist availability, or transfer times constrain performance.

Recent Industry Developments

- July 2026: Penumbra reported that the FDA cleared its THUNDERBOLT computer-assisted vacuum thrombectomy technology for ischemic stroke. The clearance adds another computer-assisted approach to thrombectomy workflows, reinforcing the need for rapid imaging triage and perfusion-informed patient selection at stroke centers.

- May 2026: Siemens Healthineers and Cercare Medical announced a global collaboration to integrate Cercare Medical Neurosuite with Siemens Healthineers Syngo DynaCT Multiphase, enabling cone-beam CT perfusion in the angiography suite. Bringing perfusion analytics closer to interventional point of care supports faster decision-making and tighter integration between diagnostic imaging and endovascular treatment pathways.

- March 2026: Philips introduced the Rembra CT system at ECR 2026, highlighting reconstruction speeds of up to 106 images per second for high-demand and acute imaging environments. Faster reconstruction directly supports door-to-imaging and door-to-needle performance targets that hospitals track under quality initiatives and reimbursement-linked metrics.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers revenue from tests and technologies used to confirm an acute ischemic stroke during the urgent diagnostic window, mainly in emergency and stroke-center workflows. It includes imaging-led diagnosis and supporting tests that help confirm the event and guide immediate triage.

Scope exclusions: We exclude stroke treatment products and procedures, implantable long-term monitoring devices, and post-stroke rehabilitation services from this market size.

Segmentation Overview

- By Diagnostic Technology

- Computed Tomography (NCCT, CTA, CTP)

- Magnetic Resonance Imaging (DWI, SWI, ASL)

- Carotid & Trans-cranial Ultrasound

- Cerebral Angiography (DSA)

- Blood-based Biomarker Tests

- AI-enabled Stroke Decision-Support Software

- By AI Software Function

- Early-Event Triage & Alerting

- Large-Vessel-Occlusion Detection

- Perfusion Mismatch Quantification

- Hemorrhage Exclusion

- By Care Setting

- Emergency Department In-hospital

- Mobile Stroke Unit

- Telestroke Hub & Spoke

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Surgery Centers / Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the starting demand pool and to keep assumptions realistic across regions. Public health incidence and risk-factor trends were referenced from sources such as the CDC, the World Health Organization, and the Global Burden of Disease study outputs, which helped us size the likely acute stroke arrival base over time.

We then used clinical guideline references and care pathway publications, such as those from AHA/ASA and similar neurology societies, to understand how imaging and adjunct tests are actually used within the first hours. For pricing and adoption guardrails, we reviewed sources like FDA clearances databases, peer-reviewed stroke imaging and biomarker literature, national health statistics portals, plus hospital network publications, along with company filings and investor materials when they described modality mix and utilization. Paid database subscriptions were used selectively for company financials and intelligence, and patent databases were used to sanity-check innovation intensity around stroke imaging software and biomarker assays. These examples are not exhaustive, and many other public sources were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focused on practical usage patterns and what drives real purchasing and test volumes, so we spoke with radiology and neurology stakeholders, emergency care leads, imaging administrators, and diagnostic suppliers. Since this is a global market, inputs were balanced across mature stroke systems and fast-growing settings, and then the findings were used to adjust modality mix, average selling price behavior, and realistic adoption timing for newer tools (such as software-enabled triage and biomarker tests).

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | APAC: 47% |

| Mid tier: 49% | Functional/Unit leaders: 33% | EMEA: 33% |

| Smaller Players: 21% | Managers: 54% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down, treated-cohort build where stroke incidence and emergency presentation rates are converted into an addressable acute diagnosis pool, and then mapped to expected test usage along the frontline pathway. In practice, our model relies on a small set of repeatable inputs, such as suspected stroke arrivals through emergency departments, the share routed to stroke-capable facilities, CT and MRI utilization in the acute window, uptake of CT angiography and perfusion protocols, and the run rate of ancillary testing that supports etiologic workup.

To keep totals realistic, results are corroborated with selective bottom-up checks, such as sampled modality volumes by care setting, channel feedback on system placements, and simple ASP times volume checks for key imaging suites and test categories. Pricing is handled with disciplined assumptions around ASP progression, mix shifts toward advanced protocols, and currency timing, and gaps in local data are handled by using country proxies that share similar care pathways and installed base maturity.

For the forecast, we lean on scenario analysis anchored on a steady base case, and then tuned using expert views on stroke-center expansion, protocol standardization, and adoption timing for newer diagnostic tools. Where signals diverged, we kept the assumptions tied to observable indicators and validated them again through follow-up outreach.

Data Validation & Update Cycle

Validation is done by checking whether the modeled test volumes and revenue outputs align with independent signals, such as stroke admissions trends, imaging system placement patterns, and published protocol adoption. If a country output looks off compared with these checks, the drivers are reviewed one by one, and the assumption causing the variance is corrected before sign-off.

Before publishing, the numbers go through a multi-step analyst review, where logic, units, and year-to-year movements are tested for reasonableness. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major guideline changes, regulatory clearances, or sharp pricing shifts. Right before delivery, a final pass is run so clients receive the latest updated view.

Mordor Intelligence's Acute Ischemic Stroke Diagnosis Market Size Measured Against Other Published Estimates

Published market sizes for acute ischemic stroke diagnosis can look different even when they sound like the same topic, because each estimate may count different tests, use different timing windows, and apply different pricing and currency rules. Some studies also blend diagnosis with treatment-related procedures, which can quickly change the final number.

The main gap comes from whether therapy and procedure revenue is counted alongside diagnostic workups, where Mordor Intelligence treats the market as diagnosis-only revenue tied to the acute confirmation window and excludes thrombolysis, thrombectomy, and other treatment categories. Differences also show up when some estimates roll in broad stroke workups that extend beyond the acute setting, or when they assume faster ASP expansion for advanced imaging protocols without re-checking utilization and installed base constraints.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.53 B (2026) | |

| Industry Publisher A | USD 2.41 B (2025) | Uses a different base year and mixes diagnostic categories across a longer horizon, which can shift modality weights and near-term utilization assumptions versus an acute-window definition. |

| Global Publisher B | USD 2.48 B (2025) | Broader scope language includes procedure and intervention categories in the taxonomy, and the value-chain treatment can differ (services plus bundled goods), which can move totals even when similar diagnostic labels are used. |

The spread is mainly explained by scope choices and timing, not by arithmetic. When the model sticks to a clear acute-diagnosis demand pool, applies practical utilization checks, and keeps pricing logic consistent across regions, the resulting market size stays easier to trace and repeat year after year.

Key Questions Answered in the Report

What CAGR is projected for the acute ischemic stroke diagnosis market during 2026-2031?

The market is forecast to expand at 7.27% CAGR over 2026-2031.

Which diagnostic technology currently holds the highest revenue share?

Multimodal CT imaging commanded 48.55% of 2025 revenue.

Which AI software function is growing fastest?

Perfusion mismatch quantification tools are advancing at 16.75% CAGR through 2031.

What geography is expected to grow most rapidly?

Asia-Pacific is projected to increase at 11.42% CAGR through 2031.

How fast are mobile stroke units expanding?

Mobile units are forecast to rise at 15.82% CAGR by 2031 as municipalities invest in pre-hospital imaging.

What is the key restraint hampering scanner adoption in emerging markets?

The high capital and maintenance cost of photon-counting CT and 7 T MRI systems limits uptake in resource-constrained hospitals.

Page last updated on: