Global Healthcare Interoperability Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

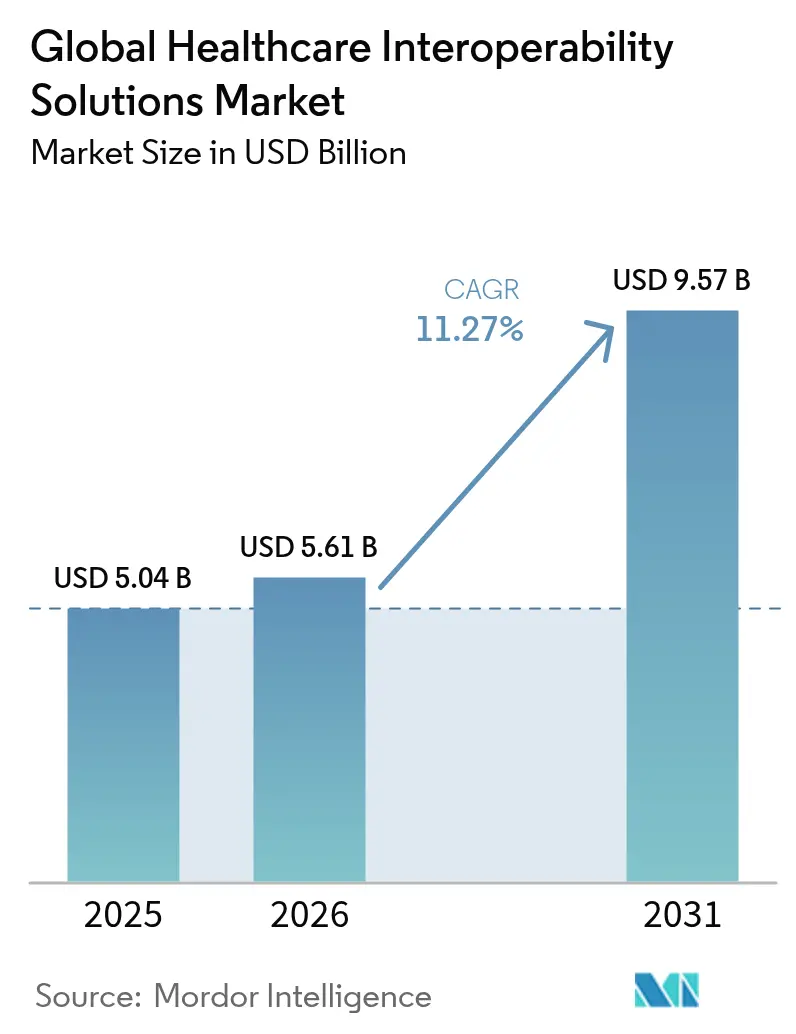

| Market Size (2026) | USD 5.61 Billion |

| Market Size (2031) | USD 9.57 Billion |

| Growth Rate (2026 - 2031) | 11.27% CAGR |

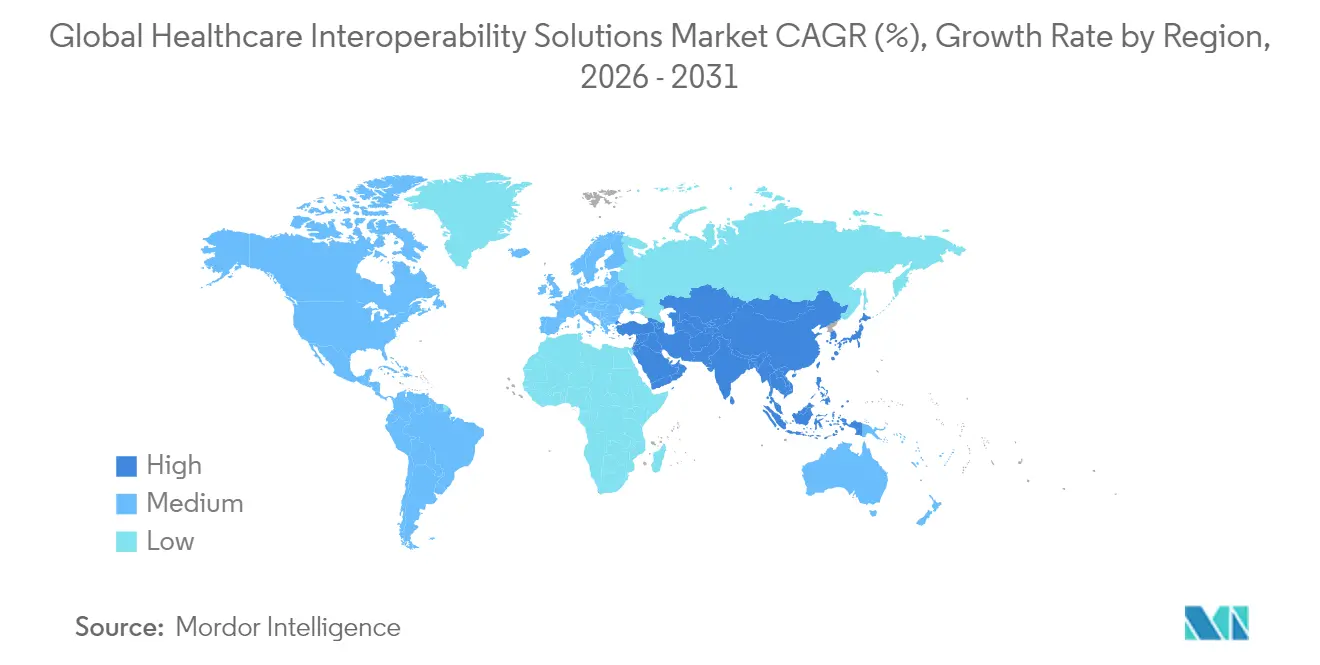

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Healthcare Interoperability Solutions Market Analysis by Mordor Intelligence

Healthcare Interoperability Solutions market size in 2026 is estimated at USD 5.61 billion, growing from 2025 value of USD 5.04 billion with 2031 projections showing USD 9.57 billion, growing at 11.27% CAGR over 2026-2031. Demand is accelerating as nationwide interoperability mandates, cloud maturation, and AI-ready data models converge to enable cross-enterprise information exchange, clinical workflow optimization, and new revenue streams. Scaling investments in TEFCA-compliant networks, FHIR-based APIs, and cyber-resilient cloud architectures are shortening implementation cycles and lowering ownership costs for providers and payers alike. Meanwhile, value-based reimbursement frameworks are shifting procurement priorities toward solutions that can measure outcomes across disparate care settings in near real time. The Healthcare Interoperability Solutions market also benefits from telehealth’s sustained popularity, which requires seamless ingestion of continuous monitoring data, and from the emergence of health-data marketplaces that monetize de-identified clinical datasets for research and life-sciences collaborations. Heightened cybersecurity spending—spurred by a record 725 U.S. breaches in 2024—adds another layer of resilience investment.

Key Report Takeaways

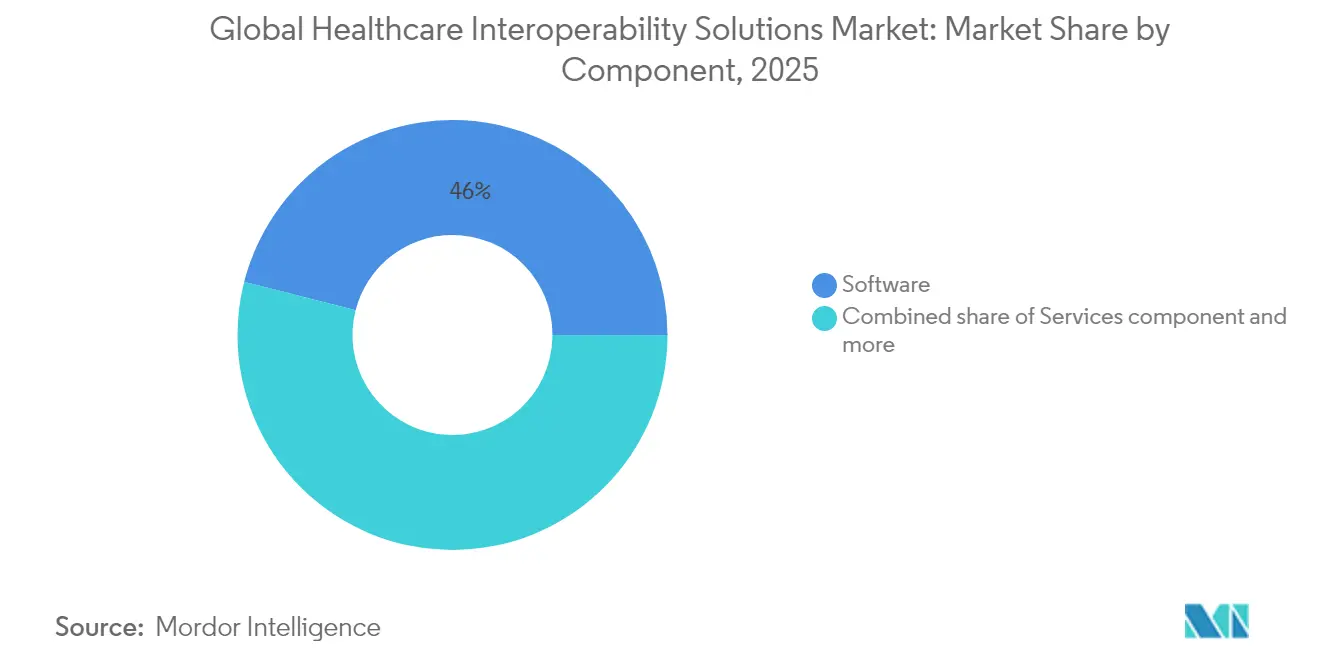

By component, software led with 46.45% revenue share in 2024, while platforms / middleware is forecast to post the fastest 11.89% CAGR through 2030.

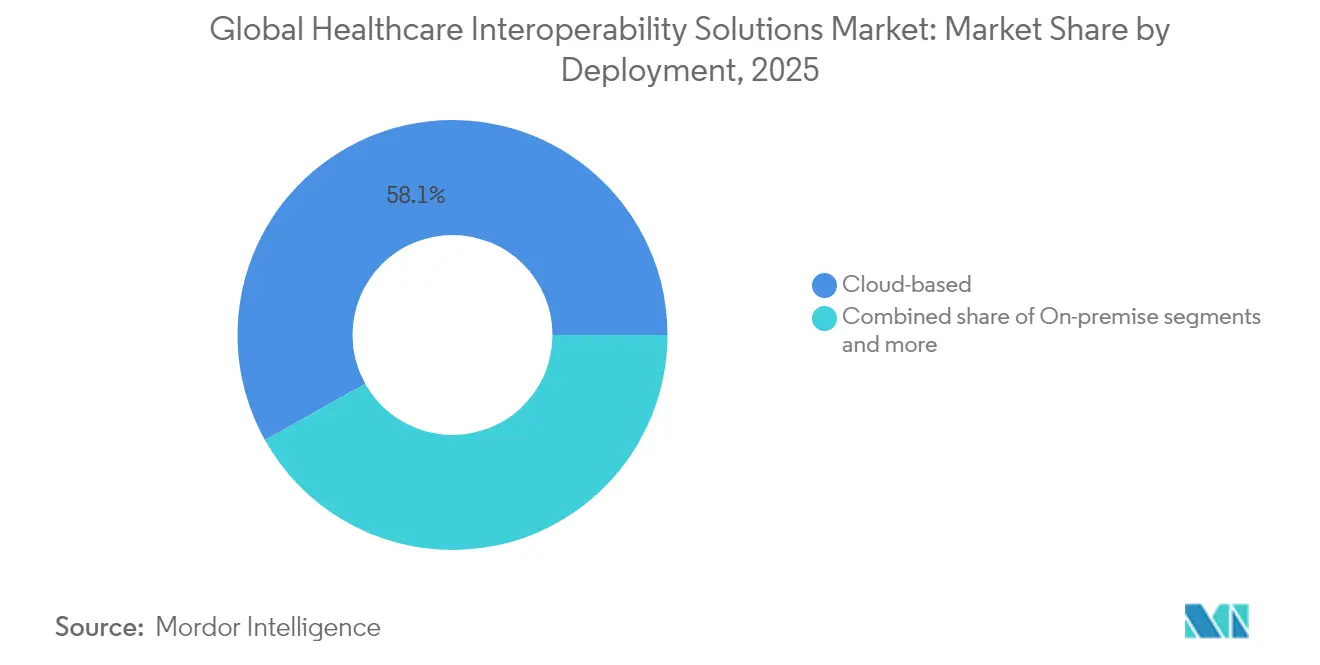

By deployment mode, cloud accounted for 58.60% of the Healthcare Interoperability Solutions market share in 2024 and is projected to grow at 12.38% during the forecast window.

By end user, hospitals & health systems generated 32.75% of the Healthcare Interoperability Solutions market size in 2024; payers represent the fastest-growing group at 12.13% CAGR.

By geography, North America contributed 42.23% revenue in 2024, whereas Asia-Pacific is expected to expand at 12.89% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Interoperability Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory mandates for EHR interoperability | +2.8% | Global, with strongest impact in North America & EU | Medium term (2-4 years) |

| Growing adoption of cloud-based healthcare IT | +1.9% | Global, led by North America, expanding to APAC | Short term (≤ 2 years) |

| Shift to value-based care requiring integrated data | +2.1% | North America primary, EU secondary adoption | Medium term (2-4 years) |

| Expansion of telehealth & remote monitoring | +1.4% | Global, accelerated post-pandemic adoption | Short term (≤ 2 years) |

| Rise of healthcare data marketplaces | +0.8% | North America & EU core markets | Long term (≥ 4 years) |

| AI-driven CDS demanding standardized data models | +0.7% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory mandates for EHR interoperability

Information-blocking penalties of up to USD 1 million per violation have turned API standardization into a board-level imperative, forcing providers to adopt HL7 FHIR R4 endpoints that comply with the 21st Century Cures Act. TEFCA went live in 2024 and quickly connected more than 625 hospitals through Qualified Health Information Networks, proving nationwide data exchange viability. Europe’s EHDS regulation mirrors this pressure by mandating cross-border data liquidity using FHIR and SNOMED CT, compelling hospitals to upgrade middleware, governance policies, and workforce skills simultaneously. These mandates collectively accelerate capital allocation toward the Healthcare Interoperability Solutions market.

Growing adoption of cloud-based healthcare IT

Microsoft Azure’s FHIR service surpassed 1 billion monthly API calls in 2024[1]Source: Microsoft, “Azure Healthcare APIs,” microsoft.com , demonstrating elastic performance at scale. NextGen migrated its Mirth interface engine to a managed cloud service, shrinking provisioning time from weeks to hours and cutting operating expenses for mid-tier hospitals. Hybrid deployment is becoming the norm, keeping sensitive archives on-premise while bursting analytics workloads to the cloud, and thereby propelling further adoption within the Healthcare Interoperability Solutions market.

Shift to value-based care requiring integrated data

CMS finalized a rule that obliges Medicare Advantage and Medicaid plans to expose prior-authorization APIs by January 2026, prompting payers to build FHIR ingestion hubs for real-time utilization review[2]Source: Centers for Medicare & Medicaid Services, “Interoperability and Prior Authorization Final Rule,” cms.gov . Accountable Care Organizations now assemble multi-source data lakes to monitor outcomes and cost trends, reinforcing the financial link between interoperability and reimbursement. Consequently, provider groups prioritize solutions capable of translating clinical, claims, and social-determinant data into unified dashboards, amplifying Healthcare Interoperability Solutions market momentum.

Expansion of telehealth & remote monitoring

Remote-patient-monitoring platforms stream continuous vitals into EHRs through HIPAA-compliant pipelines, as illustrated in Microsoft’s reference architecture for IoT health data. Bidirectional record exchange ensures virtual-visit notes sync instantly with primary-care systems, eliminating manual reconciliation and emphasizing low-latency FHIR gateways. Sustained telehealth demand therefore accelerates procurement within the Healthcare Interoperability Solutions market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of integration projects | -1.2% | Global, with acute impact on smaller healthcare organizations | Short term (≤ 2 years) |

| Data privacy & security concerns | -0.9% | Global, with varying regulatory intensity by region | Medium term (2-4 years) |

| Vendor reluctance to open proprietary APIs | -0.7% | Global, with strongest impact in markets with dominant EHR vendors | Medium term (2-4 years) |

| Fragmented consent‐management frameworks | -0.5% | EU & North America primary, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of integration projects

Complex multi-facility deployments can exceed eight figures once customization, migration, and staff training are tallied. Smaller hospitals lack the scale to dilute these capital outlays across large patient volumes, forcing phased rollouts that slow Healthcare Interoperability Solutions market penetration. CFOs must also fund cybersecurity, cloud licensing, and AI pilots concurrently, stretching budgets and elongating deal cycles.

Data privacy & security concerns

A record 725 U.S. breaches in 2024 underscored the heightened risk of wider attack surfaces created by open data networks. GDPR imposes strict consent mechanisms and cross-border transfer restrictions, adding compliance overhead to every new FHIR feed. Providers therefore demand immutable audit logs, field-level encryption, and zero-trust frameworks, which can delay procurement decisions within the Healthcare Interoperability Solutions market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Platform Innovation

Software contributed 46.02% revenue in 2025 because integrated suites bundle EHR connectivity, FHIR translation, and analytics in a single contract, easing vendor management and accelerating time to value. Platforms / middleware is forecast to grow 11.67% CAGR, driven by hospitals that use low-code API hubs to connect legacy HL7 v2 feeds with cloud FHIR stores. Services remain indispensable for configuration, governance design, and lifecycle support, often absorbing one-third of total budgets.

Pricing models have shifted from perpetual licenses to transaction-based subscriptions, lowering entry barriers for community hospitals. Middleware suppliers now wrap SaaS portals around established engines, providing turnkey TEFCA readiness and automated compliance reporting. Epic’s platform approach illustrates how incumbents defend share by embedding interoperability deep in their clinical workflows, whereas API-first vendors such as Redox win greenfield deployments where buyers want vendor neutrality. The Healthcare Interoperability Solutions market therefore rewards suppliers that combine rapid-mapping tools with pre-built regulatory templates.

By Interoperability Level: Semantic Standards Drive Market Evolution

Structural interoperability held 41.52% share in 2025 as organizations first focused on message routing and document exchange. Semantic interoperability is projected to expand at 12.41% CAGR because AI-driven analytics and population-health dashboards require codified data across sites of care. HL7 FHIR R5 advances semantic maturity by tightening value-set bindings and adding richer codeable-concept support.

Foundational and organizational layers remain essential for secure transport and governance but will capture less incremental growth. Hospitals are investing in terminology servers, patient-master-indexes, and data-quality engines to unify disparate vocabularies, positioning semantic capabilities as the ultimate goal. As a result, semantic toolkits are now embedded in five-year digital-health roadmaps across the Healthcare Interoperability Solutions market.

By Deployment Mode: Cloud Migration Accelerates Market Growth

Cloud deployments held 58.12% revenue in 2025 and are forecast to rise at a 12.16% CAGR as providers pivot to consumption-based economics, automatic patching, and zone-redundant failover. Microsoft Azure’s FHIR service passing 1 billion monthly calls in 2024 validated hyperscale performance for high-throughput clinical messaging. On-premise estates persist for latency-sensitive imaging and data-sovereignty use cases, yet many CIOs now orchestrate hybrid topologies that keep PHI on local clusters while bursting analytics to regional clouds. Subscription dashboards that forecast egress charges and security-drift alerts have become differentiators, nudging laggard systems into the Healthcare Interoperability Solutions market.

Cloud momentum reduces capital barriers for community hospitals while enabling pay-per-use scaling during public-health surges. Disaster-recovery metrics also improve because multi-region replication is bundled into most SaaS tiers. Resistance still surfaces around vendor lock-in, so containerized middleware that can move between hyperscalers is gaining attention. As hybrid blueprints mature, procurement teams increasingly mandate blueprint conformity to TEFCA, EHDS, and GDPR in a single contract, further standardizing purchasing criteria across the Healthcare Interoperability Solutions market.

By End User: Payers Drive Market Transformation

Hospitals & health systems generated 32.41% of 2025 spend, reflecting their need to route high-volume messages across inpatient, outpatient, and ancillary settings. Payers, however, are on course for the fastest 11.92% CAGR as CMS rules require FHIR-based prior-authorization and patient-access APIs by January 2026. Ambulatory and specialty clinics adopt low-cost SaaS interface engines to secure referrals and share visit summaries, while laboratories and pharmacies strengthen medication-reconciliation through LOINC-coded order exchange.

Health Information Exchanges are evolving into regional utilities that monetize consent brokering and public-health surveillance, attracting private-equity funding and increasing transaction volumes. For all users, semantic-interoperability layers now top wish lists because AI-driven population-health dashboards rely on normalized codes. These dynamics widen the buyer base and deepen wallet share inside the Healthcare Interoperability Solutions market.

Geography Analysis

North America retained 41.85% share in 2025 thanks to clear ONC mandates, robust broadband, and early TEFCA onboarding. Asia-Pacific is projected to log a 12.67% CAGR as Japan’s national medical DX program standardizes electronic records and Australia’s Interoperability Plan funds FHIR roll-outs;. Europe’s EHDS regulation boosts demand despite GDPR-driven implementation complexity, while South America and the Middle East & Africa are early-stage but increasingly target cloud-hosted HIEs to bypass capital constraints.

Emerging-market ministries often adopt managed-service pricing to convert CapEx into OpEx, opening white-space for vendors willing to provide multilingual support and sovereign-cloud options. Cross-border telehealth in the Gulf Cooperation Council and ASEAN blocs is another catalyst, pushing regional players into the Healthcare Interoperability Solutions market for standards-based identity federations.

Competitive Landscape

Epic Systems and Oracle Cerner anchor the field by bundling native interfaces, analytics, and revenue-cycle modules into enterprise agreements, capturing economies of scope that dissuade large-scale rip-and-replace decisions. Yet API-first disruptors such as 1upHealth, Health Gorilla, and Redox win greenfield projects where buyer priorities center on agility and vendor neutrality. InterSystems leverages a multimodal data-platform pedigree, embedding generative-AI summarization to differentiate on latency and context preservation.

Strategic alliances intensify: hyperscalers pair with terminology-server specialists, while telecom carriers embed FHIR gateways at 5G edges to support low-latency tele-ICU services. M&A activity is brisk—Cotiviti’s purchase of Edifecs for USD 1.2 billion extends payer-side compliance toolkits, and HEALWELL’s acquisition of Orion Health spreads platform reach across Europe and APAC. Venture capital likewise favors firms with TEFCA and EHDS storylines, foreseeing high switching costs inside the Healthcare Interoperability Solutions market.

Economic moats increasingly depend on semantically rich data-models and pre-certified compliance accelerators. Vendors unable to expose open APIs or guarantee sub-second response times risk relegation to niche interface support roles. Consequently, product roadmaps converge on low-code mapping, SaaS cost-governance dashboards, and AI-ready data fabrics.

Global Healthcare Interoperability Solutions Industry Leaders

Koninklijke Philips NV

EPIC Systems Corporation

NextGen Healthcare, Inc.

Oracle Corporation (Cerner Corporation)

Koch Software Investments (Infor, Inc)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: HEALWELL AI finalized the acquisition of Orion Health’s global business

- October 2024: Netsmart, Epic, and MedAllies released 360X closed-loop referral workflows

Global Healthcare Interoperability Solutions Market Report Scope

As per the scope of this report, interoperability in healthcare facilitates timely and established access, integration, and application of electronic health data to enhance and optimize health outcomes for patients. The healthcare interoperability solutions market is segmented by deployment (cloud-based and on-premise), level (foundational, structural, and semantic), type (solutions and services), end user (healthcare providers, healthcare payers, and pharmacies), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in USD million for the above segments.

| Software |

| Services |

| Platforms / Middleware |

| Foundational |

| Structural |

| Semantic |

| Organizational |

| On-premise |

| Cloud-based |

| Hybrid |

| Hospitals & Health Systems |

| Ambulatory & Specialty Clinics |

| Laboratories |

| Pharmacies |

| Payers |

| Health Information Exchanges (HIEs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Component | Software | |

| Services | ||

| Platforms / Middleware | ||

| By Interoperability Level | Foundational | |

| Structural | ||

| Semantic | ||

| Organizational | ||

| By Deployment Mode | On-premise | |

| Cloud-based | ||

| Hybrid | ||

| By End User | Hospitals & Health Systems | |

| Ambulatory & Specialty Clinics | ||

| Laboratories | ||

| Pharmacies | ||

| Payers | ||

| Health Information Exchanges (HIEs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Healthcare Interoperability Solutions market?

The market is valued at USD 5.61 billion in 2026.

What CAGR is forecast for Healthcare Interoperability Solutions to 2031?

Analysts project an 11.27% CAGR through 2031.

Which region contributes the largest share of spending?

North America leads with 41.85% revenue in 2025.

Who are the major solution providers?

Epic Systems, Oracle Cerner, InterSystems, 1upHealth, and Redox dominate current deployments.

Why are payers investing so heavily in interoperability?

CMS rules require FHIR-based APIs for prior-authorization and patient-access by 2026, pushing payers to modernize data platforms.

How does TEFCA influence buying decisions?

TEFCA sets national exchange standards in the U.S., so buyers insist that new solutions are QHIN-ready to future-proof investments.

Page last updated on: