Mixed Martial Arts Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

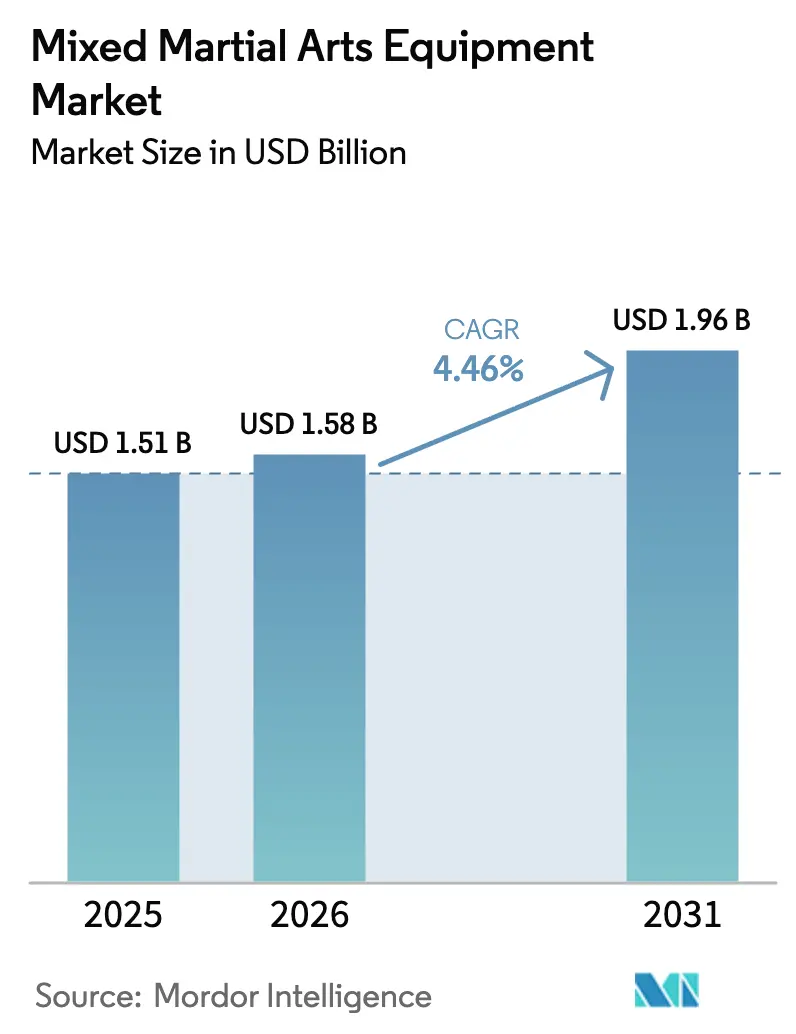

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 1.96 Billion |

| Growth Rate (2026 - 2031) | 4.46% CAGR |

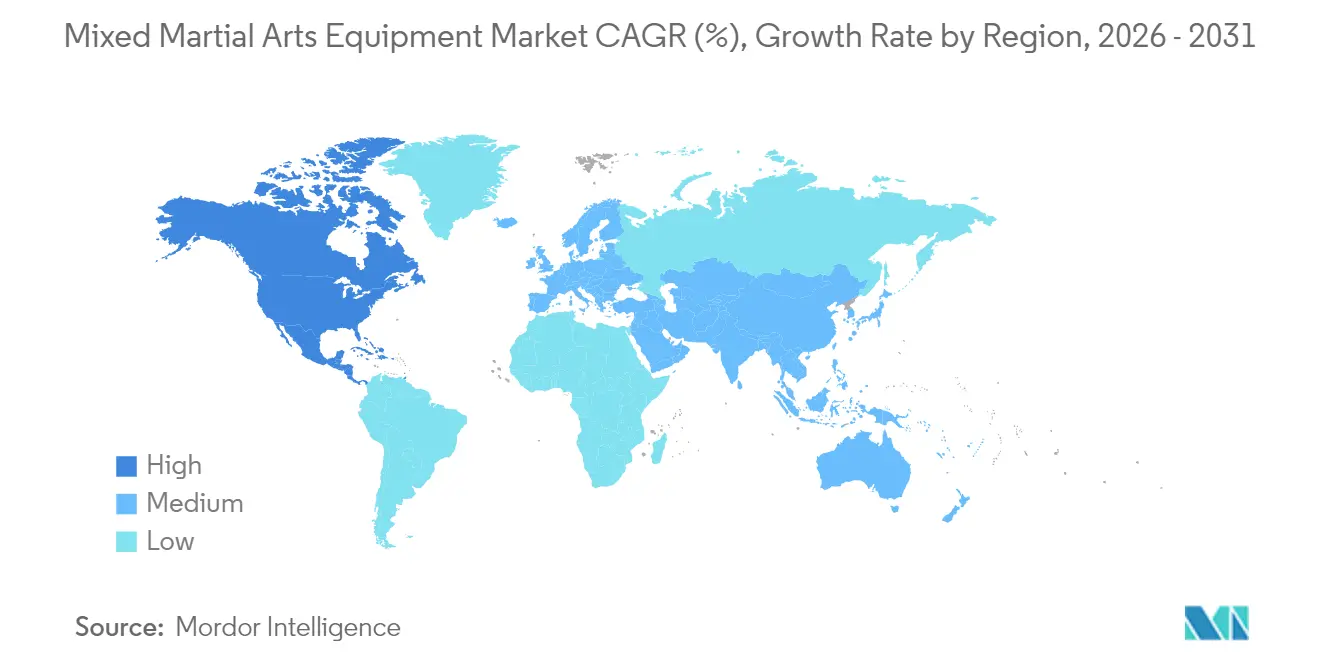

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mixed Martial Arts Equipment Market Analysis by Mordor Intelligence

The mixed martial arts market size was valued at USD 1.51 billion in 2025 and estimated to grow from USD 1.58 billion in 2026 to reach USD 1.96 billion by 2031, at a CAGR of 4.46% during the forecast period (2026-2031). The growth reflects the sport’s transition from a niche combat pursuit to a mainstream fitness option, propelled by wider gym adoption, professional-league visibility and technology-driven product upgrades. Rising female participation, stricter safety regulation and the appeal of connected fitness ecosystems are further reinforcing demand across protective equipment and smart wearables. North America remains the largest revenue base, yet Europe is gaining speed on the back of regulatory harmonization and expanding professional circuit activity. Competitive intensity is moderate; fragmentation allows agile specialists to address premium, smart and sustainably produced gear niches while established brands leverage scale and endorsements.

Key Report Takeaways

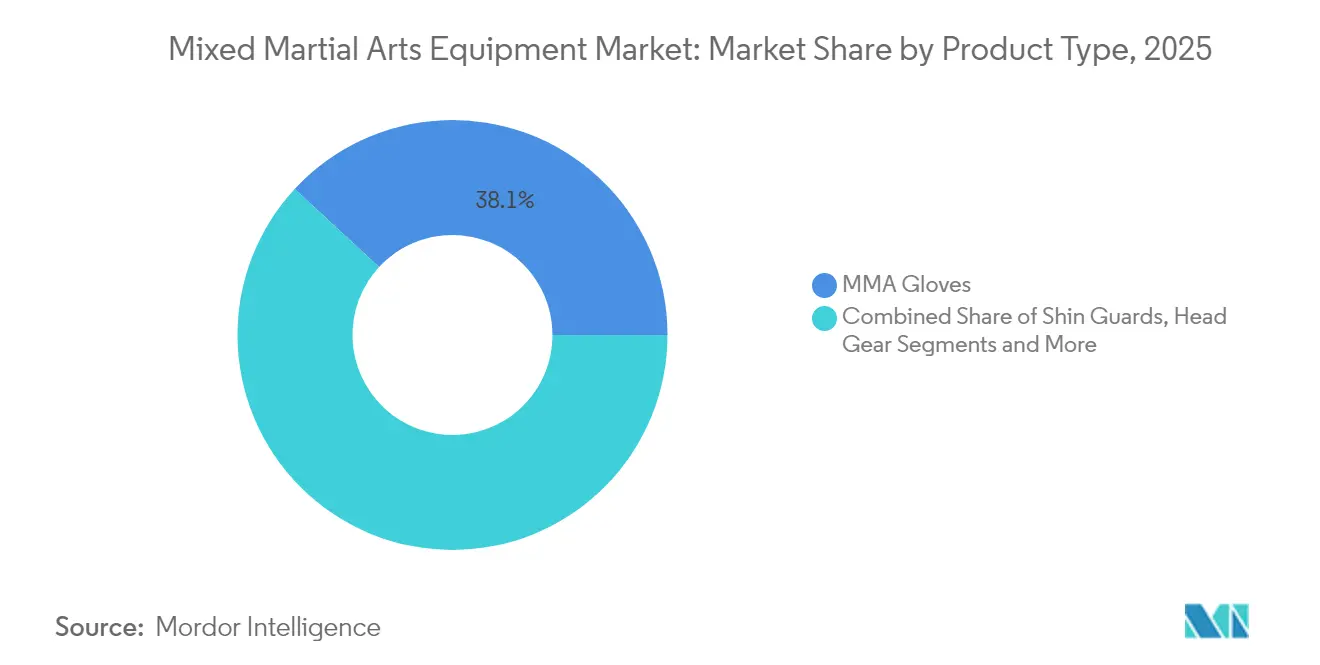

- By product type, MMA gloves led with 38.12% of mixed martial arts market share in 2025; shin guards are projected to grow fastest at a 4.96% CAGR through 2031.

- By end-user, the male segment accounted for 75.10% of the mixed martial arts market in 2025, whereas the female cohort is set to expand at a 5.12% CAGR to 2031.

- By category, mass-market products captured 63.08% revenue in 2025, while premium offerings are forecast to post a 5.55% CAGR to 2031.

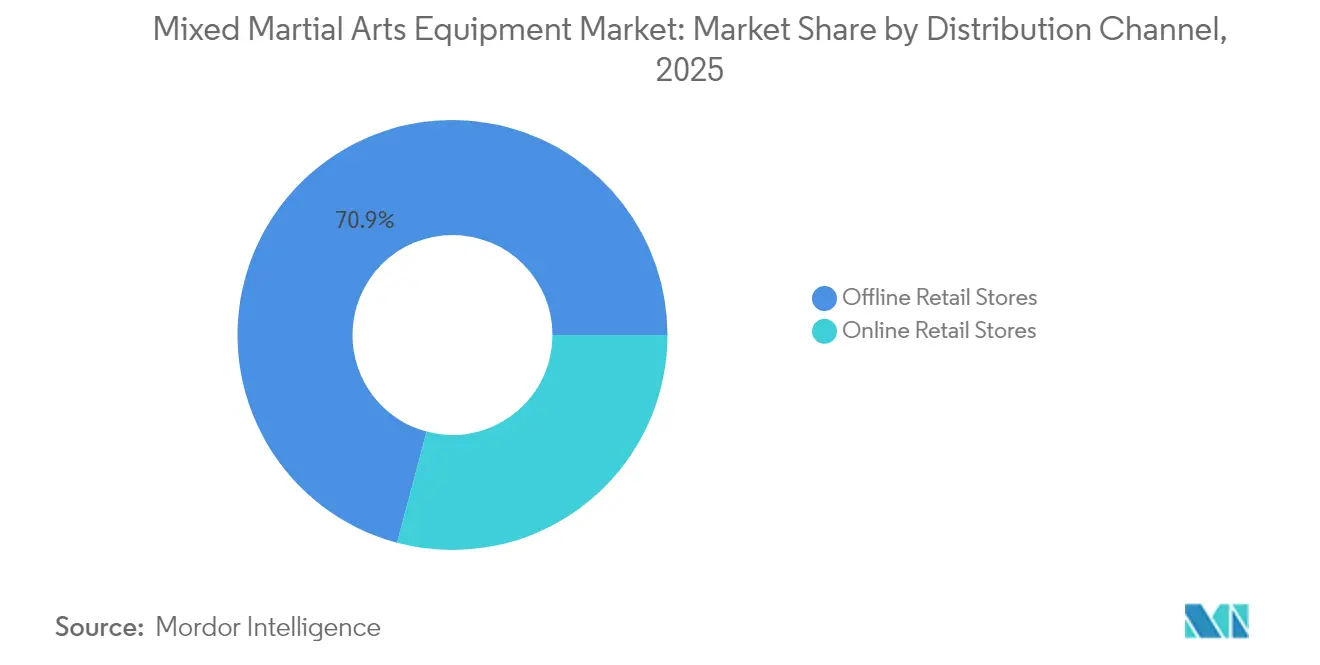

- By distribution, offline retail controlled 70.85% of 2025 sales, but online retail is pacing at a 5.92% CAGR toward 2031.

- By geography, North America commanded 32.56% of 2025 revenue; Europe is on track for the fastest growth at a 5.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mixed Martial Arts Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of MMA as a sport and fitness activity | +1.2% | Global, with strongest impact in North America and Europe | Long term (≥ 4 years) |

| Growth in the number of fitness centers offering MMA training | +0.8% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Technological advancements in product design and smart wearables | +0.6% | Global, led by North America innovation hubs | Medium term (2-4 years) |

| Proliferation of professional MMA competitions and leagues | +0.5% | Global, with regional concentration in established markets | Long term (≥ 4 years) |

| Endorsements by high-profile athletes, celebrities, and social media influencers | +0.4% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Diversification and innovation in product portfolios by leading brands | +0.3% | Global, concentrated in manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising popularity of MMA as a sport and fitness activity

Mainstream adoption of MMA training methodologies transforms traditional fitness paradigms, with UFC Gym Group's 2025 expansion targeting 150+ locations globally and projecting USD 7 million in annual revenue from structured warrior training programs. This institutional scaling reflects MMA's evolution from combat sport to comprehensive fitness discipline, incorporating strength training, cardiovascular conditioning, and flexibility development. The integration of MMA techniques into mainstream fitness programming drives demand for specialized equipment beyond traditional boxing gear, particularly protective equipment designed for grappling and ground-based training. Moreover, congressional testimony highlighted MMA's rapid growth into a multibillion-dollar industry with extensive social media reach, indicating sustained consumer engagement that translates into equipment procurement across amateur and professional segments [1]Source: U.S. Government Publishing Office, " PERSPECTIVES ON MIXED MARTIAL ARTS", www.govinfo.gov. The sport's appeal to diverse demographics, particularly younger consumers seeking high-intensity training alternatives, creates sustained demand for entry-level and progressive equipment categories.

Growth in the number of fitness centers offering MMA training

The growing number of fitness centers offering MMA training is a key driver for the Mixed Martial Arts Equipment market, reflecting the rising global popularity of MMA as both a fitness and competitive sport. This expansion is further energized by significant industry developments such as Mixed Martial Arts Group Limited's record-breaking sign-ups for its 20 Week Warrior Training Program, which is set to debut across 30 gyms in the US, Europe, Australia, and New Zealand during the first calendar quarter of 2025 [2]Source: Mixed Martial Arts Group Limited, "MMA.inc Announces Record-Breaking Sign-ups for First Calendar Quarter and 192% Year-over-Year Growth with Launch of 30 Programs Across 4 Countries", mma.inc. This program, offering an intensive 20-week training subscription culminating in a fully sanctioned amateur MMA fight, has seen unprecedented growth and expansion with new gym partners, underscoring increasing consumer engagement and demand. Such strategic and rapid expansions by prominent players not only boost the market for MMA training equipment but also foster innovation and higher standards within the industry, strengthening the overall market ecosystem globally.

Technological advancements in product design and smart wearables

UFC's 2024 glove redesign, featuring VICIS RFLX foam technology and VeChain blockchain authentication, marks a pivotal moment in the evolution of protective equipment design. This development underscores the industry's dedication to enhancing performance, improving athlete safety, and ensuring product authenticity through advanced materials and traceability solutions. Products like FightCamp's sensor-laden heavy bags, which monitor punch counts and deliver real-time performance insights, highlight the swift integration of smart technology in equipment. This innovation is further bolstered by a substantial USD 90 million investment from high-profile backers, including Mike Tyson and Floyd Mayweather, showcasing the growing interest in merging technology with traditional training tools. The melding of conventional protective gear with biometric monitoring is birthing novel product categories, enticing data-centric athletes and commercial training hubs eager for performance insights and analytics. OPRO's advanced mouthguards, which meld head-impact monitoring with standard protective features, spotlight this trend, especially in light of the heightened awareness around concussions in contact sports. These tech-driven advancements not only command a premium price but also address the increasingly stringent regulatory and compliance requirements emphasized by athletic commissions and insurance entities, ensuring both safety and accountability in the market.

Proliferation of professional MMA competitions and leagues

Leagues are driving demand for certified competition equipment by expanding and standardizing their operations. ONE Championship, which has achieved a valuation of USD 1.2 billion, demonstrates this trend by actively expanding its presence across Asia-Pacific markets. This growth in professional leagues significantly impacts amateur and training markets, as aspiring athletes actively seek equipment that aligns with professional standards. The Association of Boxing Commissions has adopted unified rules across state jurisdictions, creating standardized equipment requirements. This standardization benefits manufacturers that produce certified products meeting these regulatory specifications. Additionally, the proliferation of competitions encourages leagues to innovate and differentiate themselves through strategic equipment partnerships and technological advancements. For instance, UFC has introduced blockchain-authenticated gloves, which connect specific equipment to individual competitions, enhancing transparency and traceability. This expanding professional ecosystem consistently drives demand for high-performance equipment while establishing quality benchmarks that strongly influence consumer purchasing decisions across all market segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of specialized MMA equipment and gear | -0.7% | Global, most pronounced in emerging markets | Long term (≥ 4 years) |

| Risk of injury associated with MMA training and competition | -0.5% | Global, with regulatory focus in North America and Europe | Medium term (2-4 years) |

| Difficulty in penetrating underdeveloped regions due to low awareness | -0.3% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Competition from other combat sports and alternative fitness activities | -0.2% | Global, varies by regional sport preferences | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of specialized MMA equipment and gear

The high cost of specialized MMA equipment and gear presents a significant restraint for the Mixed Martial Arts Equipment Market. Professional-grade gear, which offers advanced protection, durability, and performance, typically comes with a hefty price tag, making it less accessible for beginners and casual practitioners. This financial barrier can discourage potential participants from investing in high-quality MMA equipment, leading them to opt for lower-cost alternatives or forego some equipment purchases altogether. Additionally, the cost factor may limit the frequency of equipment replacement, impacting overall market growth. The expense is further exacerbated by the need for multiple types of gear, including gloves, shin guards, headgear, and training aids, which collectively represent a considerable investment. Consequently, the high cost restricts broader market penetration by narrowing the customer base primarily to dedicated athletes and serious enthusiasts willing to invest in premium products.

Risk of injury associated with MMA training and competition

Regulatory scrutiny and insurance complications, driven by safety concerns, hinder market expansion. Congressional testimony has underscored the risks of traumatic brain injuries, pushing for stricter standards on protective equipment. Medical research linking chronic traumatic encephalopathy to repetitive head impacts is shaping equipment design mandates and regulatory guidelines, often leading to costlier manufacturing due to the push for advanced protective features. According to the American Orthopaedic Society for Sports Medicine, an epidemiological study on injuries in combat sports found that 27% of injuries in MMA were fractures [3]Source: American Orthopaedic Society for Sports Medicine, "MMA injuries and common misconceptions", www.sportsmed.org, further emphasizing the need for enhanced protective equipment. State athletic commissions, with their diverse medical requirements and equipment standards, complicate compliance for manufacturers and operators, and may even limit market access for products lacking certification. The perception of injury risks sways consumer adoption, especially among recreational participants and parents weighing youth programs, fueling a demand for better protective gear but also limiting overall market engagement. As safety equipment standards gain prominence in insurance requirements for MMA events and training facilities, they introduce added costs, potentially stunting facility growth and program uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gloves Dominate While Protection Innovations Accelerate

The largest market share in the Mixed Martial Arts Equipment Market in 2025 is held by MMA gloves, commanding 38.12% of the market. This dominant position is driven primarily by the frequent replacement cycles due to wear and tear, as gloves undergo constant impact during both training and competition. The professional and amateur segments contribute significantly to the sustained demand, as athletes continuously seek gloves offering enhanced durability, comfort, and safety. Additionally, technological advancements in glove materials and design remain a key driver, with consumers investing in features like improved padding, ventilation, and wrist support. The gloves segment benefits from a broad user base across gyms, training centers, and sporting events, sustaining its leadership in terms of both volume and value. Brands continuously innovate to meet evolving athlete needs, reinforcing the gloves' market dominance.

In contrast, shin guards have emerged as the fastest-growing segment within the MMA equipment market, boasting a CAGR of 4.96% projected through 2031. This notable growth reflects an increased emphasis on leg protection as MMA training integrates more Muay Thai and kickboxing techniques, which involve heavy use of kicks. The rising awareness among athletes and trainers about injury prevention has driven the demand for high-quality shin guards with superior cushioning and ergonomic designs. Availability of advanced materials and adjustable fits has further popularized shin guards among both professionals and amateurs. The expansion of MMA gyms and the growing number of participants worldwide are also significant growth catalysts for this segment. Overall, shin guards represent a dynamic and expanding niche that aligns perfectly with the evolving technical trends and safety priorities in modern MMA training.

By End-User: Male Dominance Faces Female Growth Surge

Male participants dominate the Mixed Martial Arts Equipment Market in 2025, commanding a substantial 75.10% share. This large share reflects historical demographic trends where MMA has traditionally attracted more male athletes, largely influenced by exposure through professional leagues and established combat sports pathways. The participation of men in MMA has been consistently strong due to the sport’s physical intensity and competitive nature, appealing broadly to this group. Additionally, the professional segment, with numerous male fighters competing at high levels, further solidifies male dominance in the market. The availability of specialized equipment designed for male athletes also supports this sustained market share. Moreover, retail and promotional activities have predominantly targeted male consumers, reinforcing the existing demographic imbalance.

On the other hand, female participation in the MMA equipment market is the fastest growing segment, accelerating at a 5.12% CAGR through 2031. This growth is fueled by a rising number of women engaging in fitness-focused MMA programs and the increased visibility of female fighters in professional competitions. The sport’s evolution has included more opportunities and divisions specifically for women, which has broadened the market base and stimulated demand for female-specific gear and apparel. Fitness-centric MMA classes have attracted women interested in self-defense and maintaining good health, contributing to this growth trend. Media representation and endorsements by prominent female fighters also play a vital role in enhancing female participation. As a result, the female segment, although currently smaller than the male segment, is poised to expand significantly, shaping product innovation and marketing in MMA equipment.

By Category: Premium Segment Gains Despite Mass Market Dominance

The mass market segment retains the largest share of the Mixed Martial Arts Equipment Market in 2025, accounting for 63.08% of the total revenue. This dominance is primarily due to the segment's appeal to price-conscious consumers and entry-level participants who prioritize affordability over advanced features or premium materials. The segment benefits significantly from manufacturing scale economies, which allow producers to offer MMA equipment at competitive prices. Additionally, the widespread distribution of mass-market products through general sporting goods retailers ensures accessibility to a broader consumer base. Many beginners and casual fighters opt for these cost-effective options, sustaining the segment's market leadership. Moreover, the mass segment’s ability to meet basic safety and performance needs makes it a foundational part of the overall MMA equipment ecosystem.

Conversely, the premium segment represents the fastest-growing category, showing a CAGR of 5.55% projected through 2031. This growth indicates increasing consumer willingness to invest in higher-quality, technologically advanced equipment as MMA participation deepens and athletes demand enhanced performance features. The premium segment features gear made from superior materials that offer greater durability, comfort, and safety benefits. It caters largely to professional fighters and serious enthusiasts who require top-tier products for optimal training and competition conditions. Innovations such as custom fittings, ergonomic designs, and smart wearable integrations are driving demand within this segment. As MMA continues to grow as both a sport and a fitness pursuit, the premium equipment market is poised for sustained expansion, shaping the future landscape of MMA gear.

By Distribution Channel: Digital Transformation Accelerates Traditional Retail

Offline retail stores accounted for the largest market share in the Mixed Martial Arts Equipment Market in 2025, holding 70.85% of the total market. This dominance is largely due to consumer preference for physically evaluating products before purchase, which is especially important for protective gear where proper fit and comfort directly impact safety and performance. Traditional sporting goods retailers and specialized combat sports stores offer valuable expertise, personalized fitting services, and hands-on assistance, making them a preferred choice for purchasing complex MMA equipment such as gloves and protective gear. The ability to try equipment prior to purchase builds consumer confidence in their investment and leads to higher satisfaction rates. Additionally, offline stores benefit from established relationships with local gyms and MMA trainers who recommend trusted retailers. The personalized shopping experience provided by these stores continues to be a key advantage that supports their market leadership.

On the other hand, online retail stores represent the fastest growing segment in the MMA equipment market, accelerating at a CAGR of 5.92% through 2031. The growth of online channels is driven by direct-to-consumer strategies that offer convenience, wider product selection, and competitive pricing. Subscription models for MMA gear and digital fitness integrations have further enhanced the appeal of online shopping. E-commerce platforms allow consumers to access global brands and specialized products that may not be available locally. The increasing adoption of technology and the rise of digital fitness programs also boost online sales as customers seek convenient ways to purchase equipment aligned with their training needs. As the online retail infrastructure continues to improve, and customer trust in digital purchasing increases, this segment is poised for robust expansion in the MMA equipment market.

Geography Analysis

In 2025, North America commands a leading position with a 32.56% market share, bolstered by its well-established MMA infrastructure and robust regulatory frameworks. These frameworks, shaped by state athletic commissions and professional league mandates, play a pivotal role in the region's dominance. The UFC's headquarters in Las Vegas, coupled with a vast media ecosystem, amplifies consumer awareness and standardizes equipment across both amateur and professional arenas. While U.S. markets thrive on established distribution networks and a penchant for premium equipment, Canada and Mexico are emerging as significant players, increasingly adopting MMA programming in fitness facilities. State-level regulations ensure standardized equipment, benefiting certified manufacturers. Organizations like NOCSAE set safety standards, influencing procurement choices in both commercial and amateur settings. Furthermore, the region's mature regulatory landscape fosters innovation, evident in UFC's adoption of blockchain-authenticated gloves and state-of-the-art protective gear meeting rigorous safety benchmarks.

Europe emerges as the fastest-growing region, boasting a 5.70% CAGR projected through 2031. This growth is fueled by an expanding professional competition infrastructure and the fitness industry's embrace of MMA methodologies across various national markets. Efforts toward regulatory harmonization, combined with a growing consumer acceptance of combat sports as legitimate fitness disciplines, further bolster the region's prospects. Key markets like the United Kingdom, Russia, Poland, and the Netherlands, with their rich combat sports cultures, are witnessing a surge in commercial fitness adoption of MMA programming. This European growth mirrors broader fitness industry trends, emphasizing functional training and high-intensity workouts infused with MMA techniques. Such trends amplify the demand for protective equipment and training gear, not just for competitive use but also for recreational purposes. Moreover, SGS testing services across Europe play a crucial role, ensuring product compliance with safety standards. This not only facilitates market access for certified manufacturers but also erects barriers for non-compliant products.

Regions like Asia-Pacific, South America, and the Middle East and Africa present burgeoning growth opportunities, each with its unique market dynamics and adoption trends. In the Asia-Pacific, Japan and Australia spearhead development, thanks to their entrenched combat sports cultures and a fitness industry increasingly embracing these disciplines. Singapore's ONE Championship headquarters further amplifies regional promotion and awareness, spurring equipment demand. Meanwhile, Brazil stands tall in South America, boasting deep-rooted martial arts traditions. The country's regulatory bodies, including INMETRO and other governmental entities, play a crucial role in product certification and market access. Despite facing hurdles from economic constraints and cultural nuances that might hinder premium equipment adoption, these emerging regions hold immense long-term growth promise. As disposable incomes rise and fitness infrastructures evolve to incorporate specialized combat sports programming, the potential becomes even more pronounced.

Competitive Landscape

With a score of 4, the Mixed Martial Arts equipment market demonstrates moderate concentration, reflecting a competitive landscape where numerous established players operate across diverse product categories without any single entity achieving dominant market control. This fragmented nature of the market fosters an environment ripe for innovation and specialization, enabling smaller players to carve out niche segments. The lack of a dominant player allows for a dynamic competitive environment where both established brands and emerging manufacturers can thrive by leveraging unique strategies and offerings.

This fragmentation creates significant opportunities for specialized manufacturers to differentiate themselves through technological advancements and targeted positioning strategies. Leading companies such as Adidas AG and Everlast Worldwide Inc. leverage their strong brand recognition and extensive distribution networks to maintain a competitive edge. Meanwhile, niche players like Hayabusa Fightwear Inc. and Venum International focus on delivering performance-oriented products that cater to professional athletes and enthusiasts alike. These specialized products, often supported by athlete endorsements and a commitment to technical superiority, enable these companies to command premium pricing and build a loyal customer base.

In response to the evolving market dynamics, competitive strategies are increasingly centered on technological innovation and fostering direct consumer relationships. For instance, UFC has partnered with VICIS to develop advanced glove designs, showcasing a commitment to enhancing athlete safety and performance. Additionally, UFC's collaboration with VeChain for blockchain-based product authentication highlights the growing importance of transparency and trust in the market. These strategic initiatives underscore the critical role of innovation and consumer engagement in shaping the competitive landscape of the Mixed Martial Arts equipment market.

Mixed Martial Arts Equipment Industry Leaders

-

Adidas AG

-

Everlast Worldwide, Inc.

-

Hayabusa Fightwear Inc.

-

Century LLC

-

Ringside, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Mixed Martial Arts Group Limited launched its integrated community and commerce platform targeting 640 million global MMA fans, with the mobile-first application entering closed beta before Q2 2025 official launch. The platform unifies fans, fighters, coaches, gym owners, and brands into a monetized ecosystem, leveraging the company's existing 5 million social followers and 530,000 user profiles across 16 countries.

- May 2024: Everlast unveiled multi-year partnership with Muhammad Ali Enterprises for co-branded apparel and fight-sports equipment, launching limited-edition collection including graphic hoodies, boxing trunks, and training gear sold exclusively through Everlast.com and Sports Direct.

- April 2024: UFC debuted its transformative Official Fight Glove redesign at UFC 302, incorporating VICIS RFLX foam technology and VeChain blockchain authentication. The new 3EIGHT and 5EIGHT series gloves feature reduced weight, enhanced finger positioning to minimize eye pokes, and embedded NFC chips for provenance tracking, representing significant technological advancement in professional competition equipment.

- August 2023: OPRO launched Prevent Instrumented Mouthguard in partnership with Prevent Biometrics, integrating head-impact monitoring technology with traditional mouthguard protection. The smart mouthguard provides real-time impact alerts and data analytics for coaches managing player welfare and training load optimization.

Global Mixed Martial Arts Equipment Market Report Scope

Mixed Martial Arts equipment is the sports equipment used in playing Mixed Martial Arts. The global Mixed Martial Arts Equipment Market (henceforth referred to as the market studied) is segmented by product, end-user, by distribution channel, and geography. By product, the market is segmented into (MMA gloves, Ankle/ Knee/ Elbow Guard, Punching Bags, Hand Wraps, Shin guards, Mouth guards, and Head Gear). Based on the End-Use, the market studied is segmented into (Personal users and Institutions). Based on the distribution channel, the market studied is segmented into (Offline retail stores and Online retail stores). It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| MMA Gloves |

| Punching Bags |

| Shin Guards |

| Hand Wraps |

| Ankle / Knee / Elbow Guards |

| Head Gear |

| Others |

| Male |

| Female |

| Mass |

| Premium |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Mexico | |

| Canada | |

| Rest of North America | |

| Europe | United Kingdom |

| Russia | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | Japan |

| Australia | |

| South Korea | |

| Singapore | |

| Philippines | |

| Thailand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | MMA Gloves | |

| Punching Bags | ||

| Shin Guards | ||

| Hand Wraps | ||

| Ankle / Knee / Elbow Guards | ||

| Head Gear | ||

| Others | ||

| By End-User | Male | |

| Female | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Mexico | ||

| Canada | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Russia | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | Japan | |

| Australia | ||

| South Korea | ||

| Singapore | ||

| Philippines | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the mixed martial arts market in 2026?

It is valued at USD 1.58 billion, with projections indicating USD 1.96 billion by 2031.

Which product category leads current sales?

Gloves top revenue with 38.12% share, driven by mandatory use and frequent replacement.

What is the fastest-growing geographic region?

Europe is forecast to grow at a 5.70% CAGR through 2031 on the back of regulatory harmonization and rising gym adoption.

How fast are online sales expanding?

Online retail revenue is pacing at a 5.92% CAGR as brands embrace direct-to-consumer and connected-fitness bundles.

Page last updated on: