Military Platforms Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 265.91 Billion |

| Market Size (2030) | USD 361.40 Billion |

| Growth Rate (2025 - 2030) | 6.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Platforms Market Analysis by Mordor Intelligence

The military platforms market size is valued at USD 265.91 billion in 2025 and is forecasted to reach USD 361.4 billion by 2030, advancing at a 6.33% CAGR. The growth outlook mirrors robust defense spending, which rose to USD 2.72 trillion in 2024, as nations accelerate platform modernization, adopt artificial intelligence (AI), and invest in hybrid-electric propulsion. Intensifying regional security rivalries push governments to prioritize large-scale procurement cycles, while open-systems architectures shorten upgrade windows and create new vendor entry points. Unmanned assets gain traction for risk reduction, yet manned systems still dominate frontline inventories, reinforcing a dual-track acquisition model. Supply-chain resilience programs for micro-electronics and rare-earth elements shape platform design choices, and vertical integration among prime contractors tightens competitive dynamics.

Key Report Takeaways

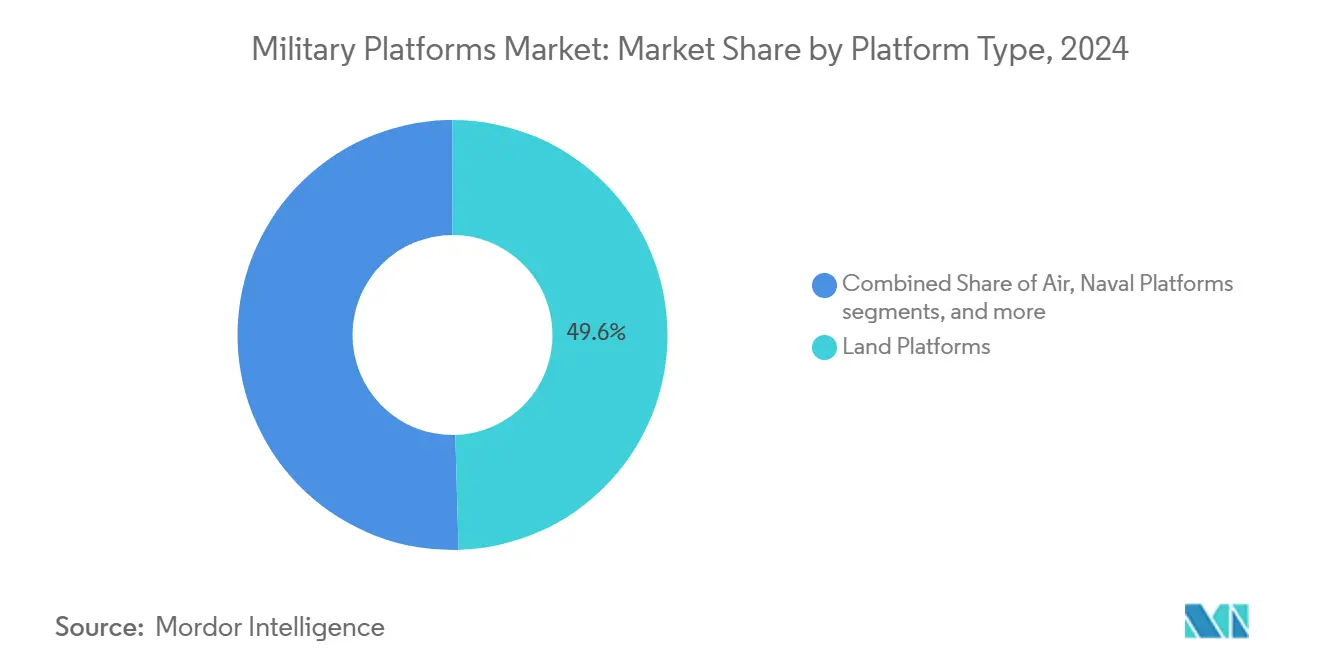

- By platform type, land platforms led the military platforms market with a 49.55% revenue share in 2024, whereas naval platforms are projected to expand at a 6.58% CAGR through 2030.

- By operation, manned systems held 71.28% of the military platforms market share in 2024, while unmanned platforms recorded the highest projected CAGR at 6.61% through 2030.

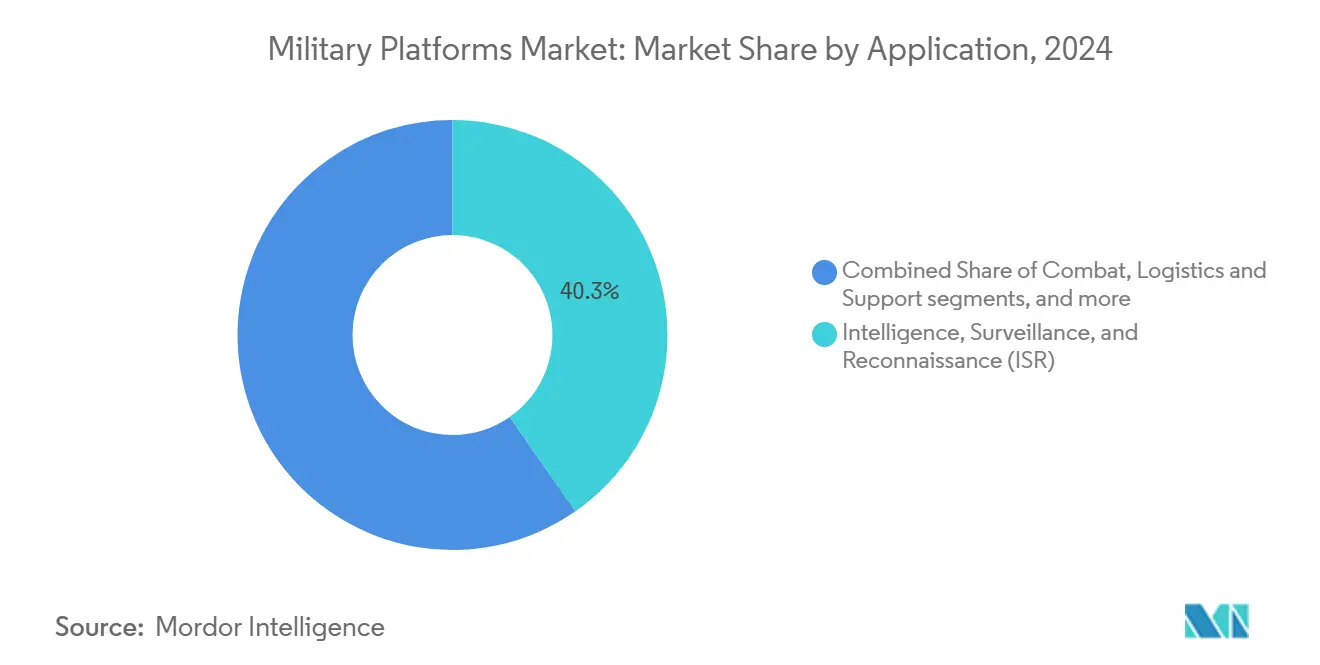

- By application, intelligence, surveillance, and reconnaissance (ISR) accounted for a 40.31% share of the military platforms market in 2024, and combat applications are advancing at a 7.56% CAGR through 2030.

- By end user, the Army commanded 52.89% of the military platforms market size in 2024, whereas the Air Force segment is set to grow at a 6.98% CAGR to 2030.

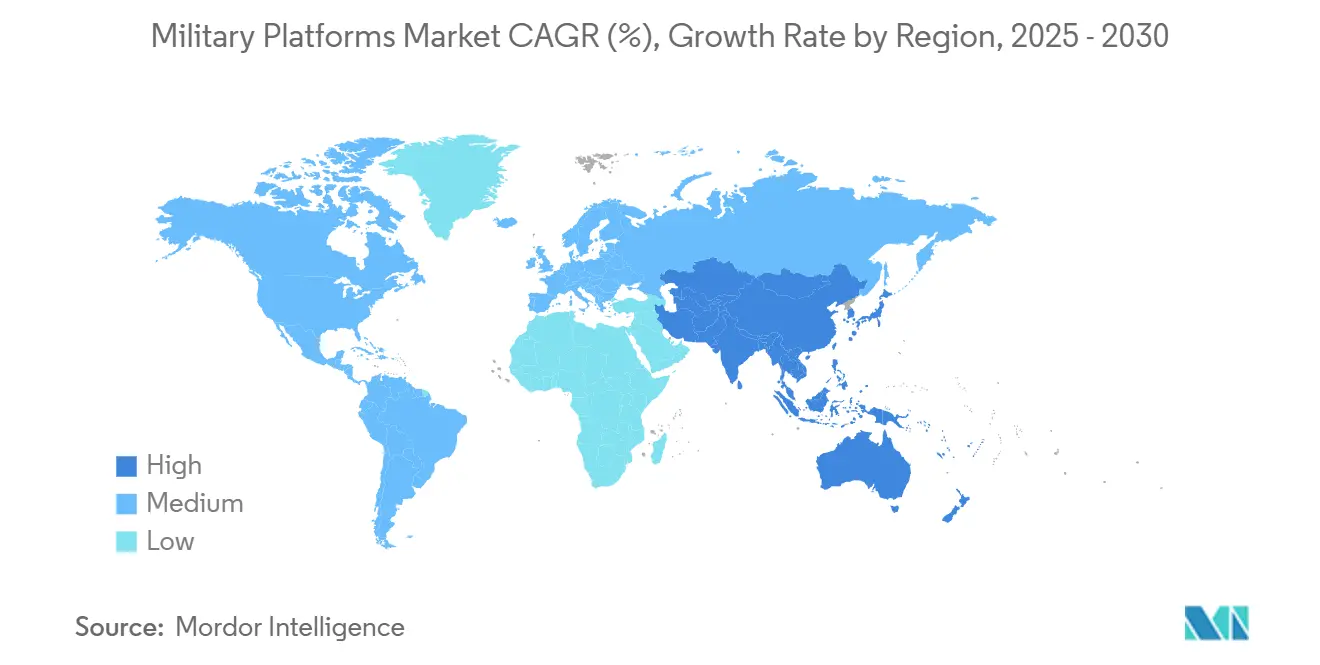

- By geography, North America captured 43.78% of the military platforms market in 2024, while Asia-Pacific is projected to post a 7.45% CAGR through 2030.

Global Military Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense budgets amid escalating geopolitical tensions | +1.20% | Global — highest in Europe, Middle East, Asia-Pacific | Short term (≤ 2 years) |

| Modernization programs replacing aging platforms | +1.00% | North America, Europe expanding to Asia-Pacific | Medium term (2-4 years) |

| Accelerated demand for unmanned systems to reduce warfighter risk | +0.80% | Global — early adoption in North America, Europe | Medium term (2-4 years) |

| Integration of C4ISR and AI for network-centric warfare (NCW) | +0.60% | North America, Europe lead; Asia-Pacific following | Long term (≥ 4 years) |

| Electrification mandates to shrink logistic fuel tails | +0.50% | North America, Europe; selective in Asia-Pacific | Long term (≥ 4 years) |

| Modular open-systems architecture enabling rapid upgrades | +0.40% | North America lead; adoption among allied nations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Defense Budgets Amid Escalating Geopolitical Tensions

Global military expenditure reached USD 2.72 trillion in 2024, and governments continue to allocate larger shares of national budgets to defense.[1]Stockholm International Peace Research Institute, “Global military expenditure reaches new record high of USD 2.718 trillion,” sipri.org Japan’s USD 734 billion allocation for 2025 and Germany’s EUR 83 billion (USD 96.84 billion) earmarked for 2026 signal long-term spending commitments toward high-end platforms. Saudi Arabia’s USD 70 billion 2025 realignment prioritizes counter-drone and asymmetric capabilities, underscoring demand for agile systems. The European Union’s EUR 800 billion (USD 933.45 billion) ReArm Europe initiative institutionalizes collective procurement, boosting economies of scale. Heightened allocations translate into accelerated contract awards, larger order quantities, and more frequent mid-life upgrades that collectively expand the military platforms market.

Modernization Programs Replacing Aging Platforms

Cold War assets reach end-of-life, prompting multi-domain replacement drives. The US Army’s Ripsaw M5 Robotic Combat Vehicle enters testing as part of the Next Generation Combat Vehicle line-up. Boeing’s USD 20 billion NGAD F-47 contract moves sixth-generation fighters toward production, replacing legacy fleets. European programs extend replacement cycles to allied states, such as Portugal’s EUR 1.24 billion (USD 1.45 billion) army overhaul and the UK's GBP 1.90 billion (USD 2.22 billion) Collective Training Service. These modernization pipelines secure long-term revenue visibility for platform suppliers and stimulate upgrades in electronics, power plants, and survivability.

Accelerated Demand for Unmanned Systems to Reduce War-Fighter Risk

Battlefield experience in Ukraine and Gaza amplifies demand for autonomous systems capable of carrying diverse payloads. Ukrainian Magura V5 unmanned surface vessels downed a Russian Su-30, demonstrating asymmetrical advantages. The US Air Force partners with RTX and Shield AI under the Collaborative Combat Aircraft program to operationalize teaming concepts.[2]RTX Corporation, “RTX and Shield AI team for Collaborative Combat Aircraft,” rtx.com General Atomics’ USD 20 billion MQ-9B SeaGuardian order from Saudi Arabia validates export appetite for persistent unmanned reconnaissance and strike systems. Institutionalization of autonomous doctrine fuels procurement budgets, expands data-link infrastructure, and prompts doctrinal changes across services.

Integration of C4ISR and AI for Network-Centric Warfare

Platforms evolve into data nodes within real-time command architectures. Lockheed Martin's partnership with Google Cloud embeds AI into flight and mission systems. The Department of Defense's (DoD's) Modular Open Systems Architecture Guidebook mandates standardized interfaces, already applied in 14 of 20 major programs. Saudi-French cooperation on AI-driven applications demonstrates global diffusion. Cyber-hardening requirements inform software design, elevating demand for secure processors and resilient networks, extending product lifecycles, and supporting fee-based software upgrades.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget ceilings and program cost overruns | −0.9% | Global — highest in North America, Europe | Short term (≤ 2 years) |

| Lengthy procurement and export-control approval cycles | −0.7% | Global — constraints in international sales | Medium term (2-4 years) |

| Supply-chain fragility for micro-electronics and rare-earth metals | −0.6% | Global — highest risk in Asia-Pacific dependencies | Long term (≥ 4 years) |

| Societal/environmental push-back on lethal autonomy | −0.4% | North America, Europe; expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Ceilings and Program Cost Overruns

Fiscal ceilings and escalating costs delay capabilities and threaten industrial bases. The Aircraft Carrier Industrial Base Coalition warned that the lack of USD 600 million advance procurement jeopardizes 73% of supplier lines, potentially rising to 96% by 2028.[3]Seapower Magazine, “Carrier suppliers warn of funding gaps,” seapowermagazine.org The National Defense Stockpile identified a USD 18.5 billion funding gap across 99 critical materials, underscoring how raw-material shortages compound financial stress. Budget pressure often forces buyers to reduce quantities, delay block buys, or negotiate scope reductions that raise unit costs and degrade economies of scale. These compromises erode supplier confidence, slow technology refresh cycles, and mute near-term expansion of the military platforms market.

Lengthy Procurement and Export-Control Approval Cycles

Procurements that stretch three to seven years and stringent export-control reviews discourage some buyers and redirect demand to nontraditional vendors. Saudi Arabia’s pursuit of Turkish KF-21 fighters reflects frustration with limited access to the US F-35, illustrating how approval bottlenecks alter competitive dynamics. The UAE selected South Korea’s Cheongung-II air-defense system for similar reasons, citing faster delivery guarantees. Lengthy cycles expose platforms to obsolescence risk, inflate update costs, and complicate life-cycle budgeting. Delays also strain diplomatic relationships by signaling uncertainty to prospective partners, ultimately disadvantaging suppliers bound by restrictive export regimes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Maritime Modernization Lifts Naval Growth

Naval assets constitute the fastest-growing slice of the military platforms market with a 6.58% CAGR to 2030. The USS Iowa (SSN 797) commissioning and a USD 12.4 billion Virginia-class contract underscore sustained submarine demand. Greece’s intent to acquire a fourth FDI frigate further evidences maritime appetite. Land platforms retain 49.55% 2024 revenue dominance through programs such as the M1E3 Abrams hybrid-electric tank and Germany’s order for 568 Rheinmetall logistics trucks.[4]Rheinmetall, “Rheinmetall wins major logistics vehicle order,” rheinmetall.com Air platforms benefit from sixth-generation fighter contracts, while space platforms rise on missile-tracking constellations like Lockheed Martin’s Golden Dome. The convergence of undersea, surface, air, land, and orbital domains pushes designers toward modular architectures that facilitate cross-domain payload integration, strengthening the military platforms market.

Intense fleet recapitalization across littoral states drives naval investment in multi-role corvettes, autonomous mine-countermeasure vessels, and air-independent propulsion submarines. Simultaneously, land vehicle upgrades integrate active protection systems, hybrid powertrains, and open-systems electronics. Collectively, these trends elevate platform unit values and broaden aftermarket revenue, reinforcing the steady expansion of the military platforms industry.

By Operation: Unmanned Systems Reshape Doctrine

Manned assets still own 71.28% of 2024 revenues as armies leverage existing training ecosystems and proven performance. Unmanned systems, however, grow at a 6.61% CAGR as militaries seek to reduce personnel exposure. Textron’s Ripsaw M5 debuts with an autonomous drive suite, while Ukrainian forces adapt surface drones to carry air-to-air weapons, demonstrating field creativity. The dual-track model spurs investments in common control stations, secure data links, and AI-enabled mission planning, expanding the military platforms market size for enabling technologies.

Legacy manned fleets undergo retrofits that add autonomy features, blurring operational categories. The VENOM program funds AI-controlled F-16 variants, illustrating incremental migration. Doctrine evolves toward human-machine teaming, where manned assets orchestrate swarms of expendable platforms, deepening integration layers, and sustaining procurement momentum across both operational modes.

By Application: AI Integration Accelerates Combat Growth

ISR platforms held a 40.31% share in 2024, reflecting the continued need for wide-area awareness. Yet combat applications rose fastest at 7.56% CAGR as AI permits precision engagement with reduced latency. Examples include F-35 pilot-directed drone swarms and Saudi multisensor air-defense nodes that fuse laser counter-UAV weapons with AI-enhanced radars. The multi-role design philosophy enables software toggling between ISR and strike, making application labels fluid.

Training platforms receive robust investment through synthetic environments. V2X’s USD 3.7 billion US Army training contract and the UK’s GBP 1.9 billion (USD 2.54 billion) service deal exemplify demand for immersive systems. Logistics applications capitalize on autonomous convoys and hybrid propulsion, reinforcing back-end support. Combined, these segments diversify revenue and ensure resilience against cycle fluctuations.

By End User: Air Force Modernization Drives Growth

Army customers account for 52.89% of 2024 revenues due to extensive land combat vehicle fleets. The Air Force segment leads growth at 6.98% CAGR through 2030, fueled by the NGAD F-47 program and expanding space constellations. Space Force refueling requirements and responsive launch contracts add emerging demand tiers.

Naval service demand remains steady via submarine and destroyer modernization, coupled with up-gunned frigates. Joint All-Domain Command and Control (JADC2) mandates interoperable systems across services, incentivizing primes to deliver open-architecture platforms that scale from ground vehicles to satellites, enlarging the total addressable military platforms market.

Geography Analysis

North America sustains a 43.78% 2024 share in the military platforms market, anchored by record US outlays and continuous capability refresh cycles. Signature programs—NGAD F-47 fighters, Virginia-class submarines, and hybrid-electric combat vehicles—reinforce prime contractor backlogs. Canada’s NORAD upgrades and Mexico’s border security investments add incremental demand. Regional leadership in AI research and semiconductor design underpins export competitiveness, while domestic rare-earth initiatives target supply resilience.

Asia-Pacific records the fastest regional CAGR at 7.45% through 2030 as China’s modernization prompts neighboring states to scale procurement. Japan allocates USD 734 billion for defense in 2025, and Australia commits an additional USD 50.30 billion through 2034. South Korea’s KF-21 fighter and Cheongung-II air-defense exports diversify regional supplier networks. The Philippine Re-Horizon 3 program and India’s multi-billion-dollar shipbuilding plan further elevate demand for naval and aerial platforms.

Europe’s defense spending reached EUR 343 billion (USD 400.17 billion) in 2024, a 19% rise driven by NATO commitments and proximity to the Ukraine war. Germany’s EUR 83 billion (USD 96.84 billion) 2026 budget and the EU’s EUR 800 billion (USD 933.45 billion) ReArm Europe fund stabilize long-term procurement. Interoperability drives consortium bids, promoting joint research and local industrialization.

The Middle East leverages oil revenues to pursue air defense, naval frigates, and unmanned aircraft acquisitions. Saudi Arabia’s USD 100 billion pending US equipment package and ongoing THAAD deployments illustrate sustained capital flows.

Competitive Landscape

Prime contractors maintain leadership through vertical integration and strategic mergers. BAE Systems acquired Ball Aerospace for USD 5.50 billion to strengthen its space-based portfolio and remove a rival mid-tier competitor. Lockheed Martin partners with Google Cloud for AI while forming a European armory alliance with Rheinmetall, blending defense and technology expertise. RTX collaborates with Shield AI to embed autonomy in Collaborative Combat Aircraft, showing how primes secure specialist capabilities through alliances rather than organic development.

Competition intensifies in unmanned and hybrid-electric niches where start-ups introduce disruptive architectures. Open-system mandates create entry points for subsystem suppliers specializing in sensors, power modules, and cybersecurity. Supply-chain challenges around rare-earth elements and semiconductors incentivize primes to co-invest in domestic sources, tilting competitive advantages toward vertically integrated firms.

White-space opportunities include tethered drone resupply systems, battery-swappable ground vehicles, and edge-compute mission pods. Firms able to validate technology readiness, attain export approvals, and align with allied interoperability standards are positioned to capture incremental share within the military platforms market.

Military Platforms Industry Leaders

Lockheed Martin Corporation

BAE Systems plc

RTX Corporation

Thales Group

Northrop Grumman Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The Indian Ministry of Defence (MoD) finalized a contract with Hindustan Aeronautics Limited for 97 Tejas Mark-1A light combat aircraft for the Indian Air Force, valued at INR 62,370 crore (USD 7.03 million). The procurement includes 68 fighter jets and 29 twin-seater aircraft, as well as associated equipment.

- August 2025: The Australian Government selected the upgraded Mogami-class frigate as the platform for the Royal Australian Navy's new general-purpose frigates. Mitsubishi Heavy Industries' (MHI) Mogami-class frigate won the contract over Thyssenkrupp Marine Systems' MEKO A-200.

- June 2025: Textron Systems unveiled the Ripsaw M5 Robotic Combat Vehicle in armed configuration during the US Army's 250th Birthday Parade.

Global Military Platforms Market Report Scope

| Land Platforms |

| Air Platforms |

| Naval Platforms |

| Space Platforms |

| Manned Platforms |

| Unmanned Platforms |

| Combat |

| Intelligence, Surveillance, and Reconnaissance (ISR) |

| Logistics and Support |

| Training |

| Other Applications |

| Army |

| Navy |

| Air Force |

| Space Force |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Platform Type | Land Platforms | ||

| Air Platforms | |||

| Naval Platforms | |||

| Space Platforms | |||

| By Operation | Manned Platforms | ||

| Unmanned Platforms | |||

| By Application | Combat | ||

| Intelligence, Surveillance, and Reconnaissance (ISR) | |||

| Logistics and Support | |||

| Training | |||

| Other Applications | |||

| By End User | Army | ||

| Navy | |||

| Air Force | |||

| Space Force | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the military platforms market and its expected growth by 2030?

The military platforms market stands at USD 265.91 billion in 2025 and is projected to reach USD 361.40 billion by 2030, growing at a 6.33% CAGR.

Which platform type leads revenue and which is the fastest growing?

Land platforms hold 49.55% revenue share, while naval platforms show the highest CAGR at 6.58% through 2030.

How significant are unmanned systems in upcoming defense budgets?

Unmanned platforms are growing at a 6.61% CAGR as militaries invest in autonomous vehicles to reduce personnel risk and expand mission reach.

Which geographic region is expanding the fastest in defense platform procurement?

Asia-Pacific leads regional growth with a 7.45% CAGR, driven by China’s modernization and heightened maritime security competition.

What factor most constrains near-term market expansion?

Budget ceilings and cost overruns pose the strongest restraint, trimming potential CAGR by 0.9% as programs face funding gaps and schedule delays.

How is open-systems architecture influencing platform procurement?

Standardized interfaces shorten upgrade cycles, allow multi-vendor integration, and create new opportunities for subsystem specialists, supporting steady market expansion.

Page last updated on: