Soldier Modernization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.47 Billion |

| Market Size (2031) | USD 22.17 Billion |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

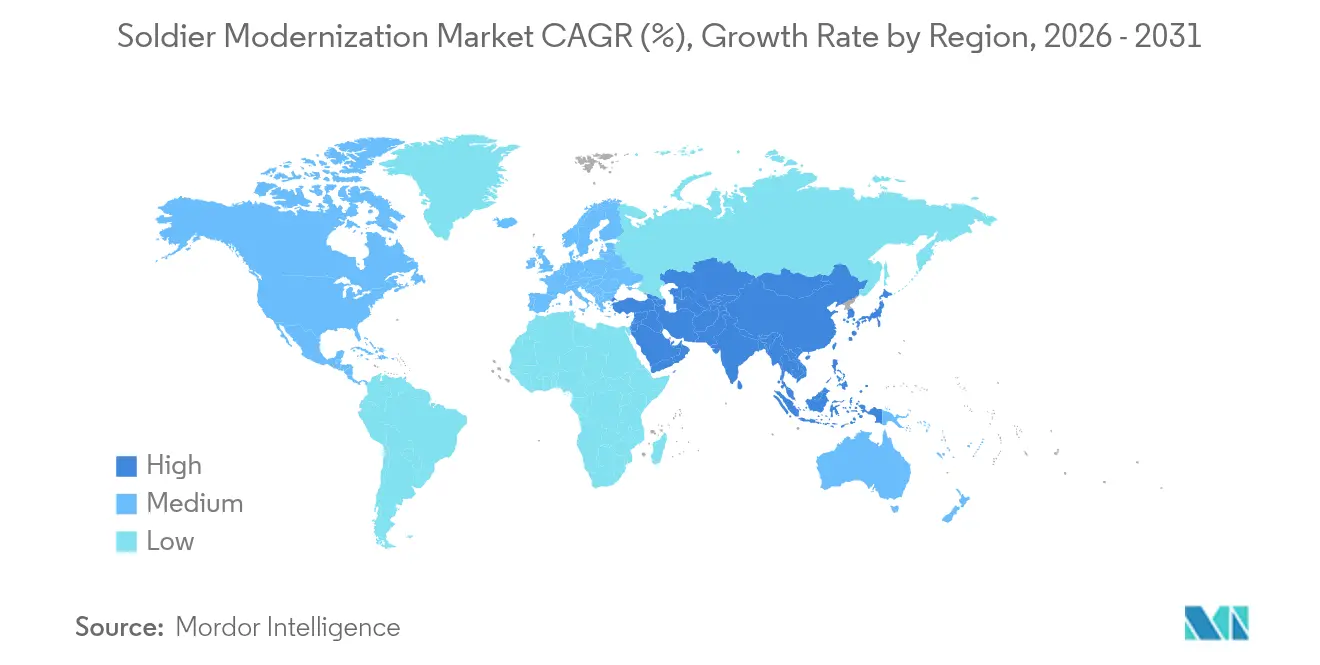

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soldier Modernization Market Analysis by Mordor Intelligence

Market Analysis

The soldier modernization market size is expected to grow from USD 17.81 billion in 2025 to USD 18.47 billion in 2026 and is forecast to reach USD 22.17 billion by 2031 at 3.72% CAGR over 2026-2031. The steady trajectory reflects a transition from urgent, post-Afghanistan replacement buy-to structured capability integration, incorporating battlefield lessons from the Ukraine conflict. Defense ministries now emphasize interoperable architectures that comply with NATO STANAG standards, software-defined flexibility that lengthens hardware lifecycles, and human-machine teaming concepts that elevate survivability and lethality. Growth also stems from lighter ballistic composites that ease soldier load, AI-assisted targeting that raises first-shot hit probability, and battery-agnostic power solutions that extend mission duration. Competition remains moderate as primes leverage scale and integration expertise, but niche innovators gain ground by pairing commercial agility with military ruggedization.

Key Report Takeaways

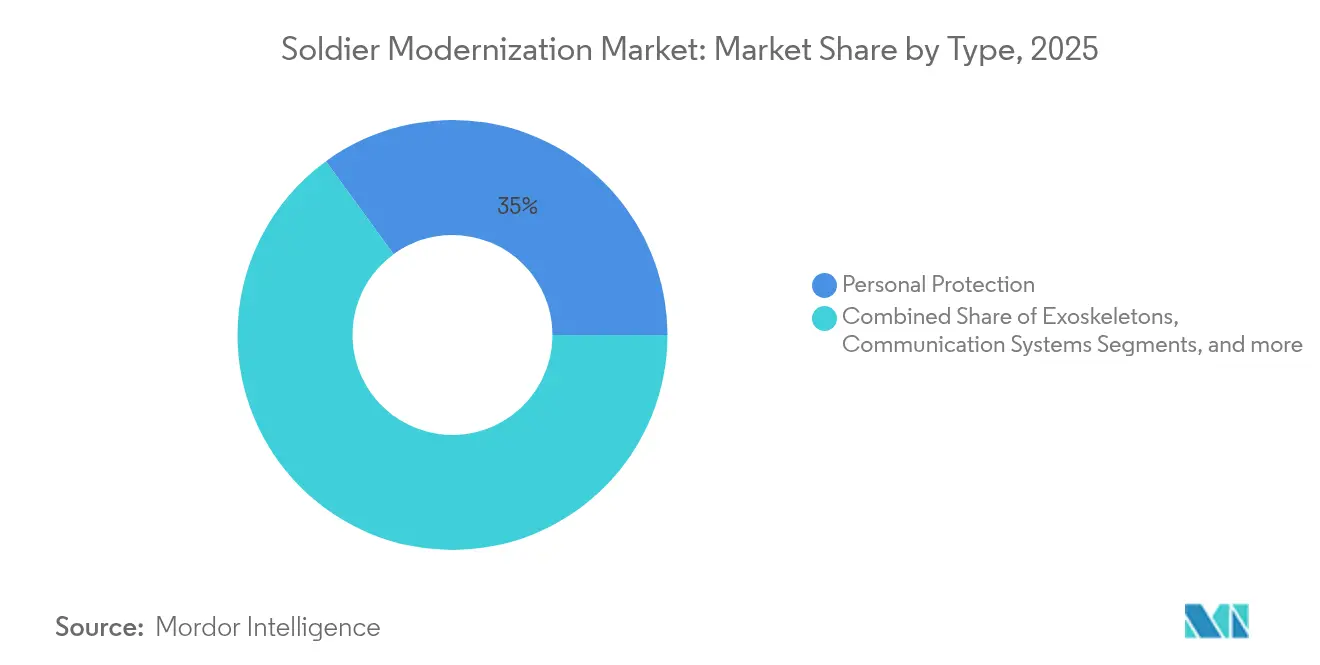

- By type, personal protection led with 35.02% revenue share in 2025; exoskeletons are projected to grow at a 7.28% CAGR through 2031.

- By technology, C4ISR and data fusion captured 46.20% of 2025 revenue, whereas augmented-reality (AR)/heads-up displays (HUDs) record the fastest forecast CAGR at 6.02% to 2031.

- By end user, Army infantry held 58.30% of the 2025 soldier modernization market share, while special operations forces exhibit a 4.05% CAGR through 2031.

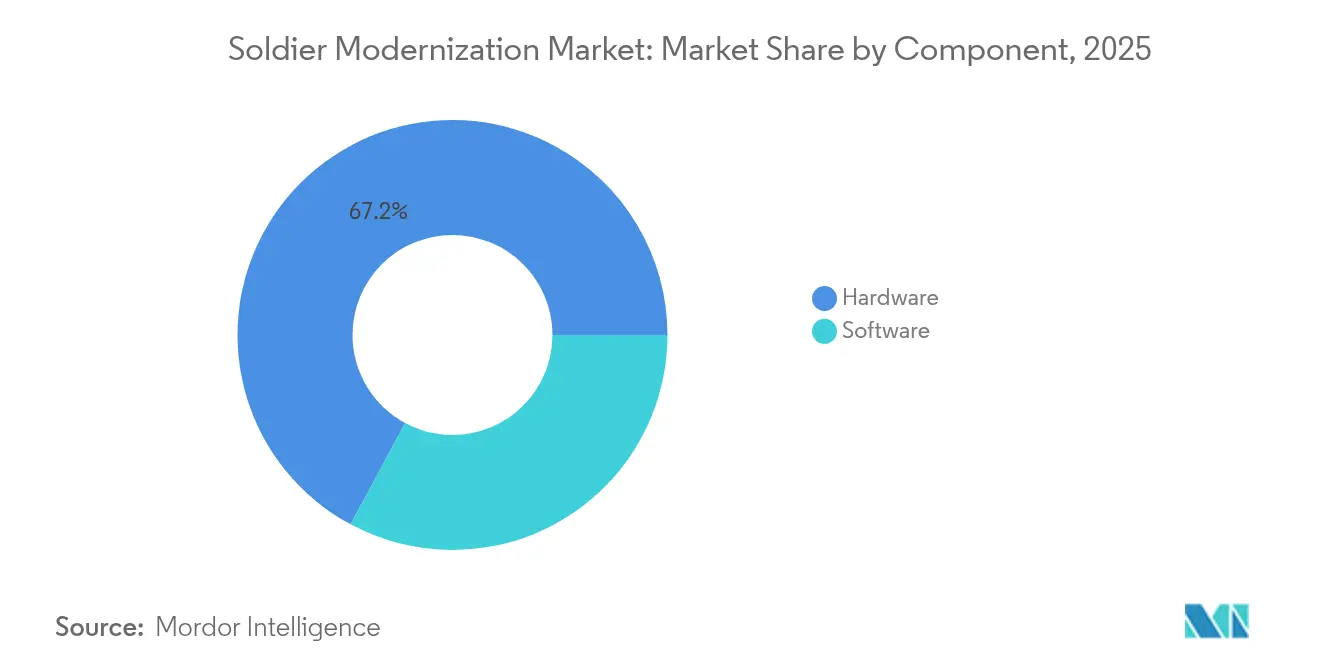

- By component, hardware commanded 67.15% revenue in 2025; software is poised to climb at a 5.62% CAGR during the outlook.

- By platform, dismounted-soldier solutions accounted for 54.80% of 2025 revenue as wearable robotics expanded at a 7.44% CAGR to 2031.

- By geography, North America dominated with a 44.92% share in 2025, yet Asia-Pacific is set to post the strongest regional CAGR at 6.52% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Soldier Modernization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Next-gen AI-assisted targeting systems | +1.2% | Global; early adoption in North America and Europe | Medium term (2-4 years) |

| Soldier-worn software-defined radios (SDR) adoption | +0.8% | NATO countries; APAC modernization programs | Short term (≤2 years) |

| Lightweight ballistic-composite breakthroughs | +0.6% | Global; manufacturing hubs in North America and Europe | Long term (≥4 years) |

| NATO STANAG-driven interoperability upgrades | +0.5% | NATO member states and partner nations | Medium term (2-4 years) |

| Battery-agnostic portable power packs | +0.4% | Global; emphasis on expeditionary forces | Short term (≤2 years) |

| Post-Ukraine rapid re-equipment programs | +0.7% | Europe, North America, select APAC allies | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Next-gen AI-assisted targeting systems

Precision fire-control optics such as Smart Shooter’s SMASH series deliver 95% hit probability under combat stress, compared with historical 20-30% accuracy rates, illustrating transformative lethality gains.[1]Smart Shooter, “SMASH Fire Control Systems,” smartshooter.com Machine-learning algorithms embedded in the US Army ATLAS prototypes generate ballistic solutions within milliseconds, allowing moving-target engagement at extended ranges. High validation in Israel and ongoing US field testing accelerate procurement confidence. AI layers bolt onto existing weapons, minimizing retraining burdens while spurring demand for edge-compute processors ruggedized for battlefield shock and temperature extremes. Rising adoption supports premium pricing that offsets modest top-line defense growth, thus adding 1.2 percentage points to the soldier modernization market CAGR.

Soldier-worn software-defined radios adoption

L3Harris’s RF-7850S SPR radio operates multiple legacy and future waveforms via field-loadable software, reducing unit-level radio inventories by 40%.[2]L3Harris Technologies, “Falcon III RF-7850S SPR Advanced Wideband Secure Personal Radio,” l3harris.com Thales’s AN/PRC-154 rifleman radio adds a self-forming mesh that maintains voice and data links even when individual nodes drop, raising network resilience during electronic-warfare attacks.[3]Thales Group, “AN/PRC-154 Rifleman Radio,” thalesgroup.com Software-centric architectures align with NATO interoperability doctrine and slash future upgrade costs, pushing widespread fielding into active units within 24 months.

Lightweight ballistic-composite breakthroughs

Ultra-high-molecular-weight-polyethylene (UHMWP) plates now satisfy NIJ Level IIIA while weighing 40% less than legacy aramid inserts, easing musculoskeletal injury rates during 20-mile forced marches. Ceramic-graphene hybrids demonstrate multi-hit defeat of 7.62 mm armor-piercing rounds at one-third the thickness of previous plates, freeing load budget for sensors or extra ammunition. Manufacturing scalability in the US and European facilities supports surge orders tied to Ukraine-informed readiness directives, placing sustained pressure on legacy steel-armor suppliers.

NATO STANAG-driven interoperability upgrades

Rohde & Schwarz’s SOVERON radios achieved ESSOR compliance that harmonizes waveforms across eight alliance members, trimming integration lead time by six months on multinational task forces. STANAG 4586 data-link conformance for drones and ground troops unlocks real-time targeting feeds to squad leaders. Open-architecture mandates invite small-business innovation while curtailing vendor lock-in, broadening supplier diversity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lithium supply-chain volatility | -0.3% | Global; acute for battery-reliant programs | Medium term (2-4 years) |

| RF spectrum congestion on tactical bands | -0.4% | Global; severe in urban and contested regions | Short term (≤ 2 years) |

| Exoskeleton cost-benefit skepticism | -0.2% | North America and Europe procurement offices | Medium term (2-4 years) |

| Export-control limitations on advanced optics | -0.25% | The US and EU exporters; impacts MEA and APAC buyers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lithium supply-chain volatility

China refines 80% of global lithium, and tightening export controls raise spot prices, jeopardizing battery pack affordability for dismounted soldiers. The US Department of Defense (DoD) funneled USD 11.8 million to domestic processors to dilute single-nation risk, yet commercial electric-vehicle demand still outstrips projected supply, constraining military allocation.[4]U.S. Army, “Premature Battery Failure in Maintenance,” army.mil Battery failure costs the Army over USD 75 million annually in premature replacements. Alternative chemistries are promising but remain five-plus years from scale, damping near-term growth by 0.3 percentage points.

RF spectrum congestion on tactical bands

Urban cellular build-outs and adversary jamming shrink clean spectrum slices, forcing units to time-share channels and limit link dwell. DARPA’s spectrum-sharing pilots advance machine-learning mitigations, but field deployment lags due to cyber accreditation hurdles. Spectrum scarcity hinders high-bandwidth applications like AR video streams, shaving 0.4 points off CAGR until adaptive-waveform radios proliferate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Protective Gear Dominance Meets Exoskeleton Momentum

Personal protection systems accounted for 35.02% of the 2025 soldier modernization market, cementing their role as the foundational survivability layer for every combatant. Advanced UHMWPE and ceramic-graphene plates cut weight while keeping NIJ III+ protection, which feeds consistent replacement demand from armies rotating into readiness cycles. Meanwhile, exoskeletons grew fastest at 7.28% CAGR, reflecting a pivot toward performance enhancement rather than mere protection. Programs such as Lockheed Martin ONYX documented a 27% metabolic-cost drop during 38 kg load marches, validating operational value. The soldier modernization market size for exoskeleton solutions will expand steadily as prices fall and maintenance logistics mature.

The broader protective gear category now integrates blast sensors that log concussive events for post-mission health checks. Smart textiles embed heating filaments that sustain body temperature in high-altitude deployments. Weapon and ammunition sub-clusters intertwine with AI-aiming modules, linking directly to squad C4ISR networks. Communication and target-acquisition kits increasingly arrive factory-paired with ballistic carriers, creating ecosystem stickiness that favors vendors offering bundled solutions. Exoskeleton makers partner with body-armor suppliers to align mounting points, ensuring modular compatibility across soldier equipment suites.

By Technology: C4ISR Pre-eminence as AR Speeds Ahead

C4ISR and data-fusion systems held 46.20% of 2025 revenue, underscoring that situational awareness underwrites every lethality and survivability gain. Modular sensor hubs aggregate drone feeds, counter-battery radars, and AI-generated target nominations. Open-source frameworks accelerate application upgrades, preserving platform relevance across a decade of threat evolution. Concurrently, AR and HUDs clocked a 6.02% CAGR, boosted by the US Army’s plan to field 3,000+ integrated visual augmentation system units valued at USD 255 million. The soldier modernization market size attributed to AR optics remains small but rises quickly as optics weight, battery life, and occlusion improve.

Artificial-intelligence modules enrich every technology node. Predictive-maintenance suites flag cooling-fan failures before mission aborts, while cognitive radio algorithms auto-de-conflict frequencies mid-battle. Non-lethal systems gain share via directed-energy dazzlers that offer escalation-of-force options for peacekeeping. Mobility and power-assist technologies dovetail with the wearable-robotics push, as passive load frames morph into powered gait-augmentation gear that halves knee strain on 24-hour patrols.

By End User: Conventional Scale vs. SOF Innovation

Army infantry consumed 58.30% of total spending in 2025, a testament to universal kit refresh cycles across large standing forces. Procurements emphasize rugged reliability, multi-national interoperability, and reasonable life-cycle cost. Special operations forces, though smaller, registered the highest CAGR at 4.05%, acting as technology incubators. USSOCOM’s USD 2.5 billion FY 2025 procurement funnels budget into niche sensors, suppressors, and digitized mission-planning tablets, which later trickle to regular units. Soldier modernization market share concentration remains lower in SOF because boutique suppliers coexist with primes, yet successful pilots often lead to bulk infantry orders once systems prove field-worthy.

Joint experimentation centers expedite cross-pollination. The 82nd Airborne adopted a VR-based behavioral-health trainer developed originally for SOF cultural-immersion prep, illustrating diffusion dynamics. As multi-domain operations demand synchronized fires, both end-user groups converge on common waveform standards, narrowing long-term divergence while sustaining near-term segmentation.

By Component: Hardware Weight vs. Software Agility

Hardware still captured 67.15% of 2025 revenue, encompassing helmets, vests, sensors, radios, and power packs that physically outfit soldiers. Yet software revenues rose at 5.62% CAGR as militaries recognized that algorithm refreshes unlock step-change capability without depot-level refits. The soldier modernization market size for software components will climb steadily with cloud-edge integration efforts that deliver periodic AI-model updates. Rheinmetall’s IdZ-ES architecture demonstrates how containerized apps drop onto in-service tablets, extending system relevance for fifteen years.

Meanwhile, hardware designers now prioritize open electrical and mechanical interfaces to sidestep obsolescence, encouraging third-party app ecosystems. Power budgets, thermal envelopes, and weight allowances become software-tuned parameters rather than fixed engineering constraints, shifting value capture toward digital intellectual property and subscription-based analytics.

By Platform: Dismounted Core with Wearable Robotics Upswing

Dismounted soldier kits represented 54.80% of revenue in 2025, reflecting the timeless centrality of foot infantry for seizing and holding terrain. Upgrades center on intuitive sensor fusion that limits cognitive overload. Wearable robotics platforms showed a 7.44% CAGR, the highest among platforms. Harvard University soft exosuits demonstrated double-digit speed gains during casualty evacuation drills, spurring command-level interest. The soldier modernization market share for wearable robotics will expand as endurance improvements persuade logisticians that added maintenance complexity is offset by reduced injury-related downtime.

Mounted-soldier packages advance through vehicle-soldier interface kits that channel vehicle sensors into helmet displays. Cross-platform convergence blurs traditional boundaries, allowing a single digital backbone to support mounted and dismounted states. Integration rigor ensures that exoskeleton control loops remain stable when stepping off armored carriers, preserving gait assistance without sudden torque spikes.

Geography Analysis

North America commanded 44.92% of 2025 spending due to the US programs like the enhanced night vision goggle-binocular, which received a USD 263 million follow-on award for 40,000 goggles. Canada pursues the DICE network, emphasizing joint integration while nurturing local electronics suppliers. Mexico cooperates through foreign military sales, adding a stable baseline demand.

Asia-Pacific, propelled by sovereignty initiatives and contested-island scenarios, posts a 6.52% CAGR. Japan’s record defense budgets channel funds into soldier C4ISR kits that synchronize with the US systems, whereas South Korea prototypes power armor to deter incursions. India balances cost and capability via Make in India, which mandates pairing foreign OEMs with public-sector ordnance factories.

Europe accelerates procurement under NATO readiness pledges, exemplified by Germany’s USD 3.6 billion IdZ-ES contract. The UK fits next-generation modular armor on Challenger 3 without disrupting local supply chains, keeping 58 jobs while harvesting British talent. Middle East and Africa favor off-the-shelf optics and radio bundles with proven reliability in desert climates, though Gulf states increasingly pilot AR headsets for armored crews.

Competitive Landscape

Incumbent primes such as BAE Systems plc, Rheinmetall AG, and Thales leverage broad portfolios, deep engineering benches, and government program-office intimacy to secure multiyear soldier kit contracts. BAE Systems plc won USD 656.20 million for Bradley M2A4 upgrades, ensuring integrated infantry-vehicle alignment. Rheinmetall specializes in modular architectures, capturing the landmark IdZ-ES deal that bundles body armor, tablet, radio, and power hubs into one logistics package. Thales dominates handheld radios in France and Australia by offering waveforms tailored to national crypto.

Disruptors seize white space by fusing commercial technology with MIL-STD ruggedization. Anduril’s partnership with Meta on the EagleEye XR headset promises a wider field of view and lower latency than Microsoft’s IVAS, signaling a shift toward Silicon Valley–style sprint cycles. Smart Shooter, a small Israeli firm, scaled global sales through a simple AI-optic clip-on that converts legacy rifles into smart weapons at sub-USD 1,000 per unit, eroding barriers to entry. Power-management specialists Amprius and Galvion carve niches via materials science that incumbents traditionally outsourced.

Supply-chain strategies pivot from sole-source to dual-production lines, hedging geopolitical risk around battery minerals and microelectronics. Vendors that prequalify multiple second-tier component suppliers score higher in recent requests for proposal evaluations. Cyber accreditation and data sovereignty compliance emerge as differentiators, nudging hardware-centric firms to acquire software boutiques with DevSecOps proficiency.

Soldier Modernization Industry Leaders

Rheinmetall AG

Thales Group

BAE Systems plc

L3Harris Technologies, Inc.

Elbit Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Nokia expanded its defense portfolio by introducing the Nokia Mission-Safe phone and an enhanced version of the Nokia Banshee 5G tactical radio.

- June 2025: TATA Advanced Systems Limited (TASL), in partnership with the DRDO, announced the development of a passive exoskeleton specifically designed for the Indian Armed Forces.

- February 2025: Galvion disclosed receiving orders for its Baltskin helmet systems from clients in the Middle East during the International Defence Exhibition (IDEX) held in Abu Dhabi, United Arab Emirates.

- August 2023: RTX secured a USD 6.6 million contract to lead a consortium tasked with producing multi-hop mobile ad hoc networks (MANETs) for the US DoD.

Global Soldier Modernization Market Report Scope

The soldier modernization priorities mainly by upgrading combat gear, long-range precision fires, soldier lethality army network, air and missile defense, and procuring the next generation of combat vehicles.

The Soldier Modernization Market is segmented based on Type, Application, and Geography. By Type, the market is segmented into Weapons and Ammunition, Personal Protection, Communication, Surveillance and Target Acquisition, Exoskeleton, Training and Simulation, and Other Types. The other segment includes the details regarding the power supply systems, data transmission, navigation, and health monitoring systems, among others. The report also covers the market sizes and forecasts for the market in major countries across various regions. For each segment, the market sizing and forecasts have been represented based on value (USD million).

| Personal Protection |

| Communication Systems |

| Surveillance and Target Acquisition |

| Exoskeletons |

| Power and Energy Management |

| Training and Simulation |

| Lethal |

| Non-Lethal |

| C4ISR and Data Fusion |

| Mobility and Power-Assist |

| Augmented-Reality (AR)/Heads-Up Display (HUD) |

| Army Infantry |

| Special Operations Forces |

| Hardware |

| Software |

| Dismounted Soldier |

| Mounted Soldier |

| Wearable Robotics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| Weapons and Ammunition | Personal Protection | ||

| Communication Systems | |||

| Surveillance and Target Acquisition | |||

| Exoskeletons | |||

| Power and Energy Management | |||

| Training and Simulation | |||

| By Technology | Lethal | ||

| Non-Lethal | |||

| C4ISR and Data Fusion | |||

| Mobility and Power-Assist | |||

| Augmented-Reality (AR)/Heads-Up Display (HUD) | |||

| By End User | Army Infantry | ||

| Special Operations Forces | |||

| By Component | Hardware | ||

| Software | |||

| By Platform | Dismounted Soldier | ||

| Mounted Soldier | |||

| Wearable Robotics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Soldier Modernization market in 2026?

The soldier modernization market size stands at USD 18.47 billion in 2026 and is forecasted to reach USD 22.17 billion by 2031.

What CAGR is expected for global soldier-system spending through 2031?

Global spending is projected to grow at a 3.72% CAGR between 2026 and 2031.

Which segment shows the highest growth rate?

Exoskeleton solutions register the fastest segment CAGR at 7.28% during the forecast over 2026-2031.

Which region is growing quickest?

Asia-Pacific leads regional growth with a 6.52% CAGR driven by indigenous defense programs over 2026-2031.

How dominant is software in upcoming soldier upgrades?

Although hardware still holds two-thirds of spending, software is set to expand at 5.62% CAGR as armies adopt AI-enabled applications over 2026-2031.

Who won the largest recent European soldier-system contract?

Rheinmetall secured the EUR 3.1 billion (USD 3.62 billion) IdZ-ES framework to modernize German infantry platoons.

Page last updated on: