Military Truck Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.88 Billion |

| Market Size (2031) | USD 30.32 Billion |

| Growth Rate (2026 - 2031) | 3.21% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

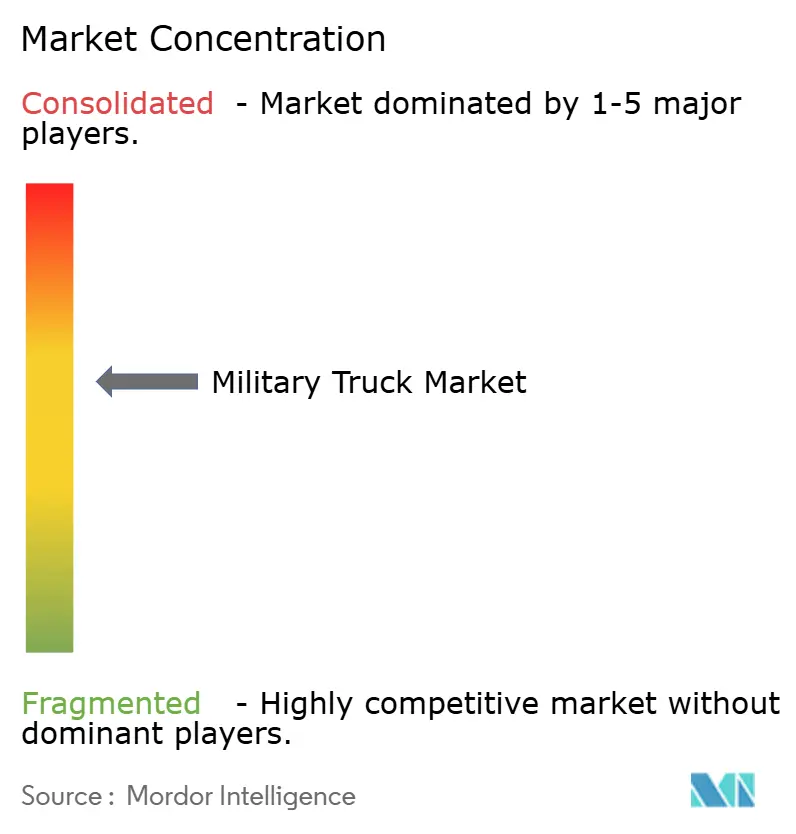

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Truck Market Analysis by Mordor Intelligence

The military truck market size was valued at USD 25.08 billion in 2025 and estimated to grow from USD 25.88 billion in 2026 to reach USD 30.32 billion by 2031, at a CAGR of 3.21% during the forecast period (2026-2031). Growth remains steady rather than explosive because defense ministries focus on high-value capabilities such as hybrid-electric propulsion, open-systems electronics, and modular mission payloads. Budgets still tilt toward recapitalizing aging fleets that entered service in the 1990s, yet commanders now insist that new vehicles arrive network-ready and fuel-efficient. Demand continues to reflect two intertwined realities: geopolitical flashpoints that raise requirements for rapid logistics and the fiscal pressure to stretch every dollar. As a result, premium valuations persist even while total procurement volumes no longer expand at the rates seen a decade ago, and vendors differentiate on technology rather than raw production scale.

Key Report Takeaways

- By application, troop transport held 39.85% of the military truck market share in 2025, whereas command and control shelter vehicles are forecast to expand at a 6.02% CAGR to 2031.

- By weight class, heavy vehicles (greater than 10 tons Gross Vehicle Weight (GVW)) led with 43.10% of the military truck market size in 2025, while light vehicles (less than 4 tons GVW) are poised to advance at a 5.32% CAGR through 2031.

- By propulsion type, diesel systems accounted for 61.05% of the military truck market size in 2025; hybrid-electric platforms are projected to grow at a 7.31% CAGR.

- By end-user, army forces represented 59.20% revenue in 2025, while special operations units recorded the highest 5.18% CAGR to 2031.

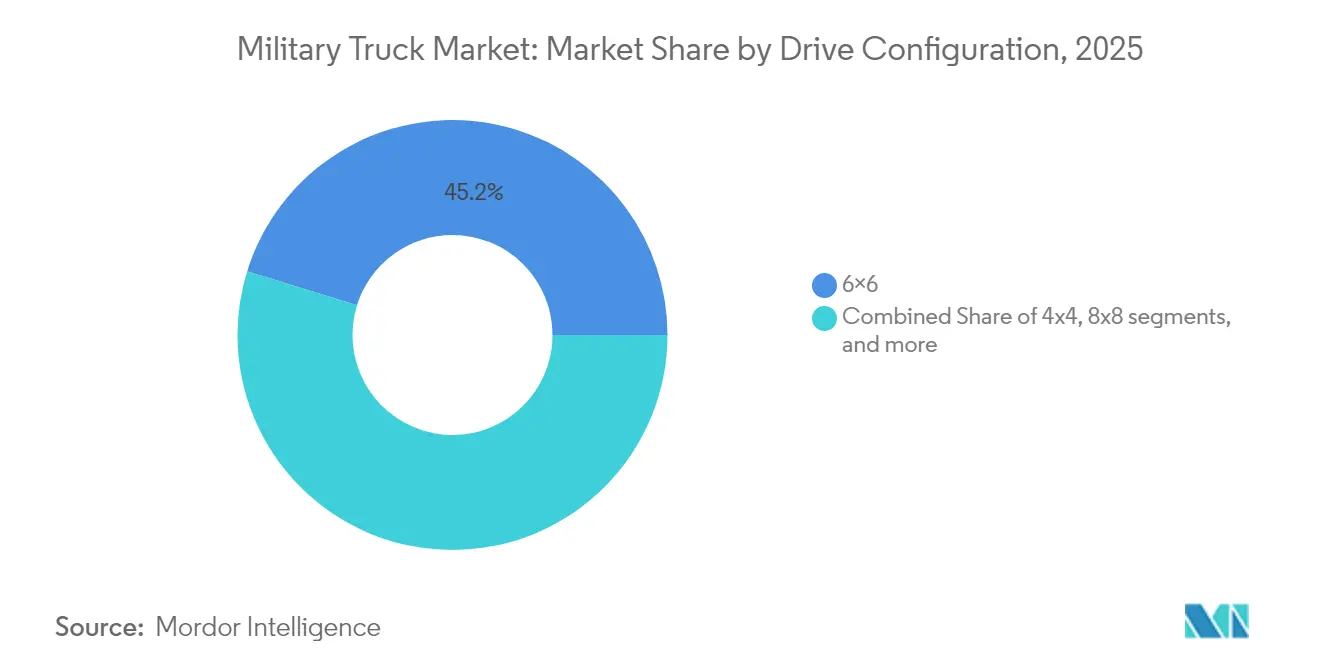

- By drive configuration, 6×6 units controlled 45.20% revenue share in 2025, yet 8×8 designs are expected to show the fastest 6.71% CAGR.

- By transmission, manual retained 67.30% of the market share in 2025, yet automatic is projected to advance at a 7.10% CAGR across the forecast horizon.

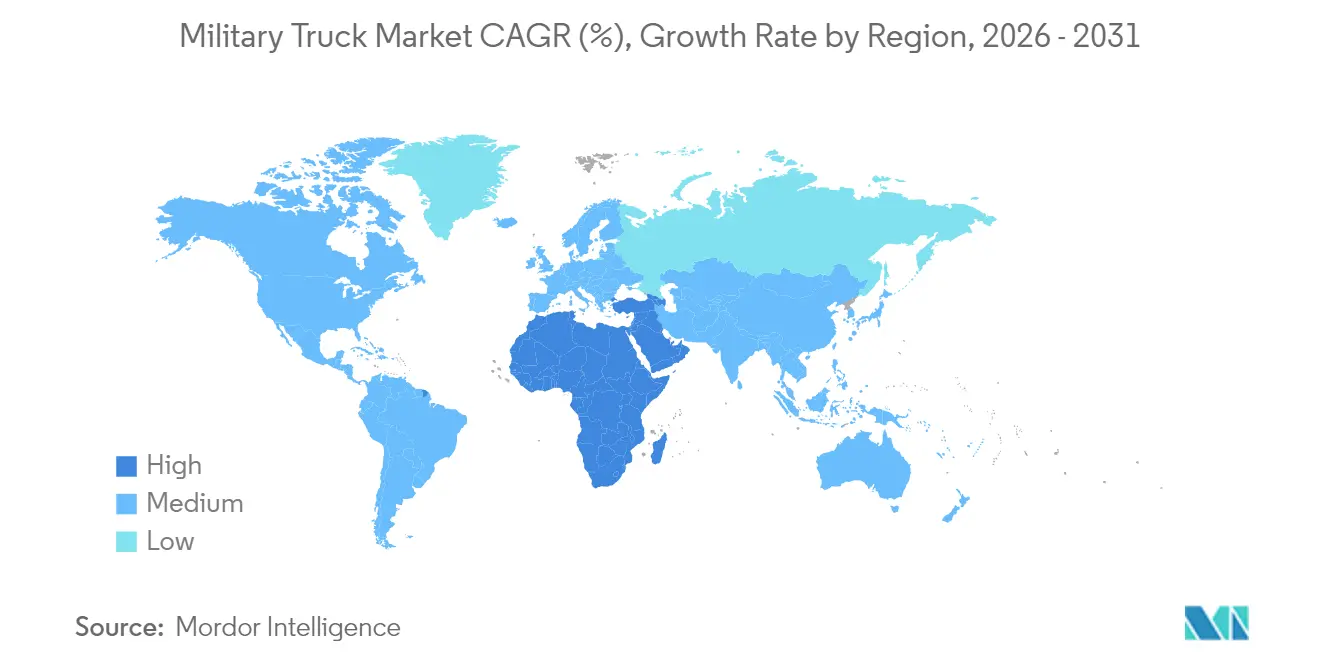

- By geography, Asia-Pacific commanded a 33.55% share in 2025, whereas the Middle East is on track for the highest 5.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Military Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense‐equipment modernization budgets | +0.8% | Asia-Pacific and Middle East | Medium term (2-4 years) |

| Fleet recapitalization to replace ageing tactical trucks | +0.6% | North America and Europe | Long term (≥ 4 years) |

| Surge in demand for multi-role logistics platforms | +0.5% | Global (early adoption in NATO) | Short term (≤ 2 years) |

| Modular open-systems architecture enabling plug-and-play mission kits | +0.4% | North America and Europe | Medium term (2-4 years) |

| Hybrid-electric drivetrains that slash fuel-convoy signatures | +0.3% | United States and EU allies | Long term (≥ 4 years) |

| Offset-driven local assembly lines in emerging economies | +0.2% | Middle East and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Defense Equipment Modernization Budgets

Military planners are replacing decades-old fleets that no longer match today’s networked battlefield. Saudi Arabia lifted its 2025 appropriation to USD 78 billion and set a 2030 goal of sourcing 50% of systems domestically, a policy that stimulates factory partnerships and knowledge transfer.[1]Army Recognition, “Saudi Arabia Targets 50% Defense Localization,” armyrecognition.com Similar priorities appear across Asia, where governments insist that each new truck integrates encrypted radios, counter-IED wiring, and modular armor. Fresh platforms thus cost more per unit, yet buyers tolerate the premium because they value payload flexibility and digital resilience.

Fleet Recapitalization to Replace Ageing Tactical Trucks

Legacy vehicles that date to the Cold War suffer mounting maintenance bills and cybersecurity gaps. The US Army’s Family of Heavy Tactical Vehicles order, worth USD 1.54 billion, placed with Oshkosh through 2029, illustrates structured replacement that sweeps away 1980s-era trucks. European forces followed suit; Germany signed a logistics contract for EUR 330 million (USD 383.6 million) covering 568 new Rheinmetall trucks in 2025. The recapitalization wave is global because incremental upgrades can no longer fix obsolete electrical architectures.

Surge in Demand for Multi-Role Logistics Platforms

Doctrinal emphasis on expeditionary operations now requires one chassis to serve several missions. The US Marine Corps specifications for its medium tactical truck include hybrid-electric drive, 10 kW onboard power, and palletized modules that swap from cargo to shelter in under an hour. Similar flexibility appears in Dutch procurement of 1,185 modular Manticore vehicles capable of homeland security, disaster relief, and conventional logistics roles. Versatility lowers the overall vehicle count, so commanders favor trucks that re-role quickly.

Modular Open-Systems Architecture Enabling Plug-and-Play Mission Kits

The US Army’s Ground Combat Systems Common Infrastructure Architecture standardizes electronics so that sensors, radios, and electronic-warfare suites bolt onto any new or legacy platform without rewriting code.[2]United States Army, “Hybrid Electric Bradley Demonstrator Advances,” army.mil The result is faster tech insertion and a curb on vendor lock-in. NATO programs now demand VICTORY-compliant data buses, ensuring that a future radar or counter-drone suite can be fielded in months rather than years. Armor, weapons, and power systems are modular, letting commanders tailor protection or firepower to the threat.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-conflict budget contraction and re-prioritization | -0.7% | Global (particularly Western nations) | Short term (≤ 2 years) |

| High acquisition and life-cycle cost of next-gen platforms | -0.5% | Global (acute in budget-constrained markets) | Medium term (2-4 years) |

| Supply-chain fragility for armor steel and power electronics | -0.4% | Global (China-dependent supply chains) | Medium term (2-4 years) |

| Carbon-footprint scrutiny limiting new diesel procurements | -0.2% | North America and EU (expanding to allied nations) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-Conflict Budget Contraction and Re-Prioritization

Following major operations, treasuries often trim defense outlays to fund domestic programs. Recent US Army helicopter cancellations show how quickly procurement plans can change when lawmakers seek savings. Truck programs become soft targets because militaries can extend service lives through rebuilds, postponing replacement. This creates a near-term dip in orders even though capability gaps persist.

High Acquisition and Life-Cycle Cost of Next-Gen Platforms

Automatic transmissions, hybrid drives, and active protection raise sticker prices above legacy equivalents. The Army’s cost study found that automatic gearboxes cut long-run expenses but force a higher upfront bill that some budget-constrained states cannot justify. Alternative propulsion further requires charging or hydrogen infrastructure, compounding cost. Supply chain volatility for armor steel and microelectronics adds unpredictability, prompting ministries to delay or scale back contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Command Centers Drive Growth

Command and control shelter trucks remain the fastest-rising category at a 6.02% CAGR, reflecting the imperative for mobile headquarters that can process battlefield data in real time. The military truck market size for these vehicles will widen as each brigade specifies at least one dedicated digital node to host advanced C4ISR software. In contrast, troop transport still held the dominant 39.85% slice of the military truck market share in 2025, because every army needs to move personnel regardless of technological shifts. Logistics, fuel, and water tanker fleets follow a steady replacement curve since they underpin everyday sustainment operations. Field ambulances grow modestly yet command a high price per unit due to integrated ICU modules and ballistic protection. Recovery and fire-fighting variants receive renewed attention where military forces support civilian disaster relief.

Second-order effects cascade across the supply chain. More shelter variants create a pull for high-capacity alternators and climate-control units. Modular body suppliers also see increased demand as armies prefer ISO-compatible containers that slot onto flatbeds. Vendors that already ship open-architecture mission computers have a strategic advantage because they can port software across the expanding fleet with minimal adaptation. For troop carriers, ergonomic seating and blast-attenuating floors differentiate offerings, especially for special operations units. The competitive gap widens for companies that can integrate transport and digital command formats on a common chassis, reducing training and spares complexity.

By Weight Class: Light Vehicles Gain Momentum

Heavy trucks above 10 tons Gross Vehicle Weight (GVW) held 43.10% revenue in 2025, driven by strategic lift roles such as tank transporters and bridging units that cannot be downsized. Yet the light segment below 4 tons GVW is growing quickly at 5.32% CAGR as urban and special operations scenarios dominate planning assumptions. Lightweight 4×4 pickups, many based on commercial designs but militarized with rollover protection and weapon mounts, give commanders an inexpensive platform that can be air-lifted in C-130 or sling-loaded under helicopters. Medium vehicles from 4 to 10 tons GVW remain the backbone because they balance payload and mobility for day-to-day logistics.

The shift to lighter classes reshapes procurement logistics. Fewer heavy low-boys are ordered, freeing funds for agile units inside a tilt-rotor aircraft. Tire and suspension suppliers pivot to run-flat designs optimized for lower weights, while additive spares manufacturing at forward bases becomes viable for simpler drivelines. On the other hand, heavy segment vendors defend their share by adding advanced driver assistance and prognostics that boost uptime, emphasizing that one oversized truck can sometimes replace three light units in rough terrain. Decision-makers, therefore, view fleet composition as a portfolio, blending classes rather than pivoting entirely to one end of the spectrum.

By Propulsion Type: Electrification Accelerates

Diesel retains 61.05% of the 2025 fleet thanks to its global fueling network and proven cold-start reliability. Even so, hybrid-electric powertrains lead growth at 7.31% CAGR as armies experiment with silent approach missions and fuel savings that shrink convoy footprints. Early trials under US Department of Defense climate plans confirm double-digit range gains while auxiliary power units disappear because traction batteries handle sensor loads. Full-battery and hydrogen platforms remain prototypes, yet research budgets rise because governments tie carbon-reduction targets to procurement awards.

Technology transition triggers new vendor dynamics. Engine builders partner with inverter specialists, and battery suppliers court militaries with ruggedized modules that meet shock and electromagnetic hardening standards. Training schools must update curricula since technicians now handle high-voltage systems. Forward operators still worry about charging in austere environments, so hybrid rather than pure-electric becomes the bridge technology of choice. Caterpillar and Cummins have demonstration gen-sets that convert JP-8 into electricity, offering a path to charge plug-in hybrids without civilian grid support.

By End-User: Special Operations Lead Growth

Conventional army formations consumed 59.20% of 2025 revenue because they field the broadest force structures. Special operations commands, however, advance at a 5.18% CAGR since they secure funding priority for precision raids and counter-terror missions that rely on low-profile trucks. SOCOM’s Ground Mobility Vehicle 1.1 fleet, for example, fits inside CH-47 and V-22 aircraft yet carries remote-weapon stations and electronic-warfare pods. Navy-Marine and air-force users follow a flatter replacement curve tied to amphibious capabilities and expeditionary air-base support. At the same time, paramilitary and homeland security agencies buy modest volumes keyed to border patrol and disaster response tasks.

Growth in special operations orders incentivizes suppliers to offer modular turrets, lightweight armor, and quick-detach mission kits. Commercial off-the-shelf passenger vehicles converted for military use win some competitions when budgets stress speed over bespoke design. Nevertheless, purpose-built platforms still dominate where survivability against small arms and mines remains non-negotiable. Industry observers expect more public-private partnerships that pool small series production across allied nations to keep unit costs manageable.

By Drive Configuration: 8×8 Systems Advance

The familiar 6×6 format represented 45.20% of revenue in 2025 because it offers ample payload at an acceptable cost. Yet 8×8 growth at a 6.71% CAGR signals rising payload and crew protection requirements in rough terrain. Newer 8×8 trucks feature independent suspensions, central-tire-inflation, and all-wheel steering that rival tracked vehicles off-road. Armies in Europe, the Middle East, and South America now compete for transporters that can keep pace with wheeled infantry fighting vehicles. Four-by-four designs dominate liaison, command, and special operations niches where curb weight must stay under helicopter limits.

Logistics planners recalculate deck space aboard roll-on, roll-off ships and railcars because 8×8 chassis are longer and taller. Vendors respond with folding ROPS structures and air suspension that drops ride height for strategic sealift. Meanwhile, predictive-maintenance sensors now ship on most configurations, and data analytics reveal that 8×8 drivetrains need fewer unscheduled repairs thanks to reduced axle loading per wheel. This fact feeds a cost-of-ownership argument that offsets the higher acquisition price.

By Transmission: Automation Gains Traction

Manual gearboxes retained 67.30% of the global truck count in 2025, largely because many countries prize simple field-level repairability. Even so, automatic transmissions advance at 7.10% CAGR due to easier driver training and smoother power delivery. Allison Transmission’s militarized 4000-series now appears in both North American and European tenders, reflecting newly accepted trade-offs between initial expense and lifecycle value. Automation dovetails with hybrid drives since torque converters and electronic controls blend seamlessly with electric motors.

As adoption rises, doctrinal debates over driver skill fade. Combat units point out that automatic shifts cut fatigue on long convoys and improve acceleration under fire. Maintenance data show fewer clutch overhauls, and simulators shorten license qualification by weeks. Meanwhile, suppliers integrate health monitoring into transmission control units, sending alerts before failures. Over the next decade the tipping point is expected where fully automatic or automated-manual boxes become default except in ultra-light pickups.

Geography Analysis

The Asia-Pacific region retained leadership with a 33.55% revenue share in 2025, reflecting sustained modernization across China, India, South Korea, and Australia. Recent spending programs, such as Australia’s Land 8116 heavy truck acquisition and India’s field artillery tractor replacement, prioritize domestic production lines, aligning with strategic industrial policies. This deep procurement pipeline ensures capacity utilization for local chassis builders and promotes technology transfer in transmissions, armor, and telematics. Regional growth also benefits from rising amphibious and disaster-response missions tied to climate events, creating supplemental demand for all-terrain logistics trucks.

The Middle East registers the fastest 5.55% CAGR through 2031 on the back of Saudi Arabia’s USD 78 billion allocation that mandates 50% industrial localization by the end of this decade. Off-take agreements underpin new joint ventures between Riyadh and European primes, covering 4×4 utility vehicles, 6×6 tactical cargo trucks, and 8×8 missile carriers. Meanwhile, the United Arab Emirates and Qatar pursue similar offsets to broaden national workforces in advanced welding, powertrain assembly, and software integration. Ongoing regional conflicts continue to stress logistics chains, reinforcing the argument for fresh fleets that can move supplies under threat.

North America remains a mature but sizable buyer driven by fleet recapitalization rather than sheer expansion. The US Army resets its inventory with FMTV A2 and JLTV-based command variants, focusing on cyber-hardened electronics and hybrid prototypes to lower fuel demand. Canada mirrors this approach by contracting 85 enhanced recovery trucks capable of towing modern heavy armor. European demand tracks a similar replacement rhythm, anchored by Germany’s multi-year Rheinmetall framework and the adoption of the Netherlands’ JLTV. South America and Africa record slower procurement, constrained by fiscal ceilings. Yet, Brazil’s army continues incremental purchases of 6×6 Guarani support trucks assembled domestically, while select African states rely on foreign military financing for light utility vehicles.

Regulatory Landscape

Military truck procurements are increasingly shaped by acquisition policies that aim to accelerate commercial technology insertion and encourage open architectures. In the United States, the Army has been reexamining ground-vehicle programs and using Commercial Solutions Openings (CSOs) to accelerate timelines for efforts such as the Common Tactical Truck (CTT). The service also operates under an updated Tactical Wheeled Vehicle Strategy that emphasizes contested logistics, COTS-based platforms, and autonomy-oriented transport concepts.

In Europe, cross-border procurement and industrial-policy instruments have become more explicit. Regulation (EU) 2025/2643 (European Defence Industry Programme, EDIP) provides support through 2027 to strengthen the European Defence Industrial and Technological Base, with the European Commission launching the 2026 EDIP work program and a large grant envelope targeting common procurement and industrial reinforcement. Interoperability and qualification requirements also affect designs for NATO-aligned buyers, where STANAG-based standardization (for example, towing and related fit-for-service requirements) influences platform interfaces and qualification pathways.

Value Chain Analysis

The value chain begins with defense-qualified subsystems, including powertrains, transmissions, axles, armor materials, electronics and communications backbones, and mission-specific bodies such as shelters, tankers, and recovery modules. This is followed by vehicle integration by primes and specialist OEMs, then testing, certification, and customer acceptance. Delivery is typically paired with long-tail sustainment, including spares, depot-level overhauls, field service representatives, and configuration management for mission kits and communications and cyber hardening.

Recent program activity points to two dynamics across the chain. First, large IDIQ or framework structures and fixed-price contracts with economic price adjustment clauses are used to manage inflation and material volatility, including in major US heavy tactical vehicle contracting and subsequent call-off orders. Second, production is increasingly tied to commercial manufacturing footprints, but still constrained by defense-unique parts and visibility gaps. Long lead times for selected components, dependence on single-source items, and obsolescence issues continue to affect delivery cadence, while DoD and oversight bodies have flagged the need for better supply chain illumination, including more consistent digital BOM and SBOM practices, to reduce foreign dependency and single-point failures.

Competitive Landscape

The military truck market is moderately concentrated. Oshkosh Corporation sits at the forefront with an end-to-end range covering light, medium, and heavy classes, plus ongoing FMTV A2 and heavy tactical vehicle contracts worth over USD 1.7 billion combined. Rheinmetall follows closely in Europe, capitalizing on its HX3 family that secured a EUR 330 million (USD 383.5 million) order for 568 Bundeswehr logistics trucks in 2025. BAE Systems leverages combat-vehicle experience to develop hybrid electric demonstrators under a USD 32.2 million US Army program, positioning itself for future production awards.

Competitive intensity now hinges on technology rather than price alone. Vendors differentiate through open-architecture electronics, autonomous convoy aids, and predictive maintenance software. Rheinmetall’s HX3 Common Tactical Truck prototype integrates drive-by-wire steering and remote-operated gun mounts to align with emerging US Army standards. Oshkosh answers with advanced intelligent suspension and anti-lock braking tuned for off-road braking on 55° slopes. Meanwhile, niche suppliers such as MATBOCK and Polaris Defense carve space in the light tactical sub-segment, offering hybrid kits and fuel cell auxiliaries that extend silent range.[5]Fuelcellsworks, “Polaris and SFC Energy Partner on Fuel-Cell Defense Vehicles,” fuelcellsworks.com

Partnership ecosystems expand under localization mandates. European primes enter equity ventures in the Middle East and Asia to satisfy offset quotas, transferring chassis weld lines while retaining engine and electronics supply. US companies pursue similar models through licensed assembly plants in Poland and Kuwait. As modular standards mature, subsystem specialists, including gearbox, sensor, and armor vendors, can sell across multiple prime contractors, gradually eroding traditional platform lock-in. Over the next five years, competitive edges will likely depend on the depth of digital twin data and the ability to deliver incremental software upgrades without pulling the vehicle from service.

Military Truck Industry Leaders

Rheinmetall AG

Oshkosh Corporation

Iveco Group

Dongfeng Motor Group

BAE Systems plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Ongoing fleet recapitalization and logistics standardization are creating opportunities for suppliers that can offer common chassis families and scalable call-offs across vehicle variants. Europe offers a clear example: Rheinmetall has received large Bundeswehr logistics-vehicle commissions under framework arrangements, including a May 2026 call-off for more than 2,000 UTF trucks across 4x4, 6x6, and 8x8. France has also shifted to a high-volume logistics truck procurement under the PL6T program (Zetros-based trucks), with the stated aim of simplifying training and sustainment across fleets. These procurements support demand for modular bodies, open-architecture vehicle electronics, and cross-platform mission kits aligned with standardized fleets.

A second opportunity cluster is forming around specialized derivatives and enabling infrastructure for expeditionary operations. US orders for Oshkosh FMTV A2 variants, including LVAD cargo configurations and bridge-transport support assets, highlight requirements for airdrop-capable logistics and heavy engineering support vehicles. Mack Defense activity on the M917A3 program further points to continued investment in construction and route-repair capabilities. Alongside these procurements, localization and industrial-resilience initiatives, including EDIP in the EU and offset-driven in-country assembly policies in parts of the Middle East, create openings for licensed production, regional integration partners, and tier suppliers that can meet security-of-supply and qualification requirements.

Recent Industry Developments

- June 2026: Oshkosh Defense received USD 142 million in orders for Family of Medium Tactical Vehicles (FMTV) A2 variants from US and international customers. The mix of 4x4 and 6x6 cargo configurations reinforces ongoing recapitalization demand while keeping a standardized platform in production for multiple users.

- August 2025: Rheinmetall reported a Bundeswehr order for over 1,000 logistics vehicles under its truck family programs. The continued call-offs from framework arrangements emphasize fleet commonality and provide volume stability for suppliers of driveline, protection, and mission-module subsystems.

- July 2024: Rheinmetall announced a record truck framework order covering more than 6,500 vehicles with an order value reported at EUR 3.5 billion. The scale of the agreement pointed to a multi-year logistics modernization cycle in Europe and reinforced the importance of long-term frameworks in military truck procurement.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue from military-specific wheeled trucks that are designed and procured for defense and security forces, and used for logistics, troop movement, and support missions across operating environments.

Scope exclusions: tracked combat vehicles, civilian commercial pickups used without military procurement specs, armored cars, and unmanned ground robots are excluded.

Segmentation Overview

- By Application

- Cargo Logistics

- Troop Transport

- Fuel and Water Tanker

- Command and Control Shelter

- Field Ambulance

- Recovery/Fire-fighting

- Special-purpose (Mine-clearing, Bridging, NBC)

- By Weight Class

- Light (Less than 4 tons GVW)

- Medium (4 to 10 tons GVW)

- Heavy (Greater than 10 tons GVW)

- By Propulsion Type

- Diesel

- Hybrid-Electric

- Full-Electric

- Hydrogen Fuel-cell

- By End-user

- Army

- Navy/Marine Corps

- Air Force

- Special Operations Forces

- Paramilitary and Homeland Security

- By Drive Configuration

- 4×4

- 6×6

- 8×8 and Above

- By Transmission

- Manual

- Automatic

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- Israel

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped set a clear boundary for what is counted as a military truck and to map the procurement demand signals behind reported orders. The first pass focused on public defense purchasing evidence, fleet plans, and technical definitions, so adjacent ground vehicles were less likely to be mixed in.

We used non-paywalled sources such as U.S. Department of Defense budget documents and procurement justifications, U.S. Federal Procurement Data System award records, NATO publications where relevant, SIPRI defense spending datasets, and UN Comtrade trade statistics for relevant vehicle categories. For macro indicators, we referenced OECD data, and for specifications language we used SAE International technical publications. Where available, we also used public tender portals. These desk inputs were complemented by company annual reports, investor presentations, and reputable defense press for program timelines and delivery milestones, and we used paid subscriptions for company financials, patent databases, and defense contract and tender tracking. The sources mentioned are not exhaustive, and many additional references were used for collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work was used to check procurement timing, the typical configuration mix, and how pricing changes with payload class and drivetrain needs. We spoke with respondents across OEM and subsystem participants, defense procurement and logistics stakeholders, and channel partners involved in service and refurbishment. Coverage was balanced across major buying regions, so assumptions were not anchored to a single country view.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 51% |

| Mid tier: 45% | Functional/Unit leaders: 36% | EMEA: 30% |

| Smaller Players: 16% | Managers: 52% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where defense vehicle procurement and replacement demand were reconstructed by region, then translated into value using typical truck mixes and pricing ranges. After shaping the demand pool, we ran selective bottom-up checks, including sampling announced contract values, using unit deliveries where disclosed, and applying ASP-by-weight-class to validate totals and flag outliers.

Key inputs used in the model included defense budget direction and ground-vehicle allocation signals, announced fleet renewal cycles, typical splits across light, medium, and heavy trucks, the share of 4x4 versus 6x6 and 8x8 platforms for logistics missions, and the rate at which legacy fleets are refurbished versus replaced. Pricing was not treated as a single average, since mission kits and protection levels can shift the final contract value. Instead, ranges were used and reviewed with industry respondents.

For forecasting, scenario analysis was applied around procurement pacing and modernization intensity. The scenarios were then translated into annual demand using replacement cycles and program ramp profiles. Where program data was incomplete, gaps were handled with comparable program benchmarks and conservative timing assumptions, and those assumptions were revisited during primary validation.

Data Validation & Update Cycle

We validated the model by checking it against independent signals such as defense vehicle contract announcements, stated delivery schedules, and budget line movement across years. When large variances appeared, we flagged the drivers and rechecked assumptions, and adjustments were made only when the change could be traced to a clear input like timing, unit mix, or a price range.

Before sign-off, the work goes through multi-step analyst review to keep logic and arithmetic consistent across regions and years. Reports are refreshed annually, and interim updates are triggered when material events occur, such as a major procurement program shift or a sizable budget revision. Right before delivery, an analyst completes a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Military Truck Market Size Compared Against Other Published Estimates

Published market sizes for military trucks can vary because authors do not always count the same vehicle boundary, buying entities, and timing of contract recognition. Differences also show up when pricing is treated as a single average, or when refurbishments are either counted as new demand or left out completely.

By checking procurement-led demand signals and refreshing inclusion rules, for example keeping tracked combat platforms and armored cars outside the market, Mordor Intelligence keeps the total tied to newly built wheeled military trucks rather than broader ground-vehicle spending. Gaps are often driven by whether paramilitary and homeland security purchases are included, how heavy logistics trucks above 10 tons GVW are treated, the exchange-rate timing used for multi-currency contracts, and how ASP ranges step up across the forecast.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.88 B (2026) | |

| Global Consultancy A | USD 25.70 B (2024) | Uses a broader military trucks label that can include some adjacent protected vehicles, and it applies earlier-year currency conversion for multi-country contracts, which shifts the USD total. |

| Industry Publisher B | USD 18.70 B (2024) | Leans on a narrower scope that can exclude part of heavy logistics and special-purpose trucks, and it tends to compress pricing by using simplified averages without configuration-level uplift. |

The spread in the table is mainly explained by scope boundaries and by how pricing and currency timing are handled for defense contracts. Our steps are transparent because each total can be traced back to programs, replacement cycles, and configuration mix, and then rechecked when new awards or budget changes come through.

Key Questions Answered in the Report

What is the current value of the military truck market?

The military truck market is valued at USD 25.88 billion in 2026, with a projected CAGR of 3.21% through 2031.

Which application segment is expanding fastest?

Command and control shelter vehicles are growing at a 6.02% CAGR because militaries need dedicated digital command platforms on mobile chassis.

Why are hybrid-electric trucks gaining momentum?

Hybrid drivetrains cut battlefield fuel use by about 20%, reduce acoustic signatures, and generate silent onboard power, making them attractive despite higher upfront costs.

Which region shows the highest growth?

The Middle East leads regional growth at a 5.55% CAGR, supported by Saudi Arabia’s increased defense budget and localization initiatives.

Who are the top competitors in the market?

Oshkosh Corporation, Rheinmetall AG, and BAE Systems plc hold a combined 38% share of recent contract awards, differentiating through hybrid propulsion and modular designs.

How are localization policies influencing procurement?

Offset mandates in regions such as the Middle East drive joint ventures and in-country assembly, giving an edge to manufacturers willing to transfer technology and skills.

Page last updated on: