Aerospace And Defense Telemetry Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

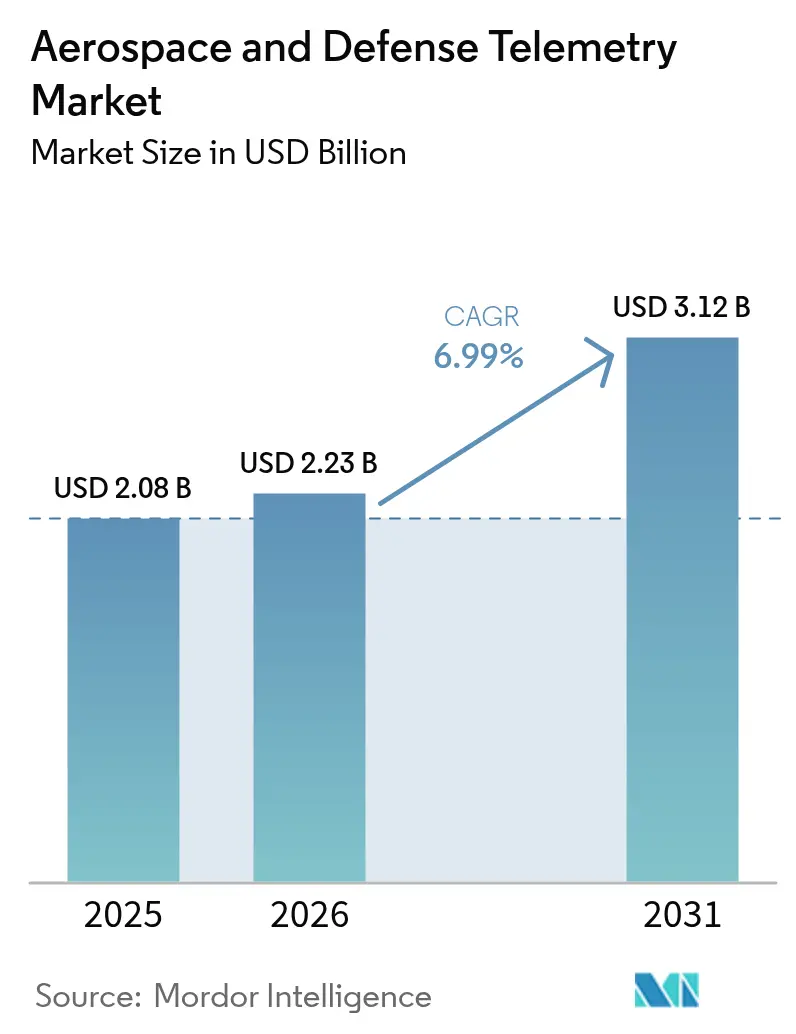

| Market Size (2026) | USD 2.23 Billion |

| Market Size (2031) | USD 3.12 Billion |

| Growth Rate (2026 - 2031) | 6.99% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace And Defense Telemetry Market Analysis by Mordor Intelligence

The aerospace and defense telemetry market size is expected to grow from USD 2.08 billion in 2025 to USD 2.23 billion in 2026 and is forecast to reach USD 3.12 billion by 2031 at 6.99% CAGR over 2026-2031. Demand growth reflects the transition from legacy data pipes to edge-enabled telemetry architectures that process mission data in real time and compress non-essential traffic before transmission. Hypersonic weapon programs, proliferating satellite constellations, and onboard artificial intelligence collectively reshape telemetry design rules. At the same time, NATO and Indo-Pacific modernization plans elevate bandwidth requirements across airborne ISR, naval, and missile platforms. Radio Frequency links retain scale advantages, yet laser and optical systems secure rapid adoption where spectrum congestion threatens mission continuity. Ongoing integration of space-based edge AI allows satellites to triage data on-orbit, trimming ground-station backlogs and improving decision speed. Consolidation activity—exemplified by BAE Systems’ USD 5.5 billion purchase of Ball Aerospace—shows how incumbents bolt on specialized telemetry assets to retain strategic dominance.

Key Report Takeaways

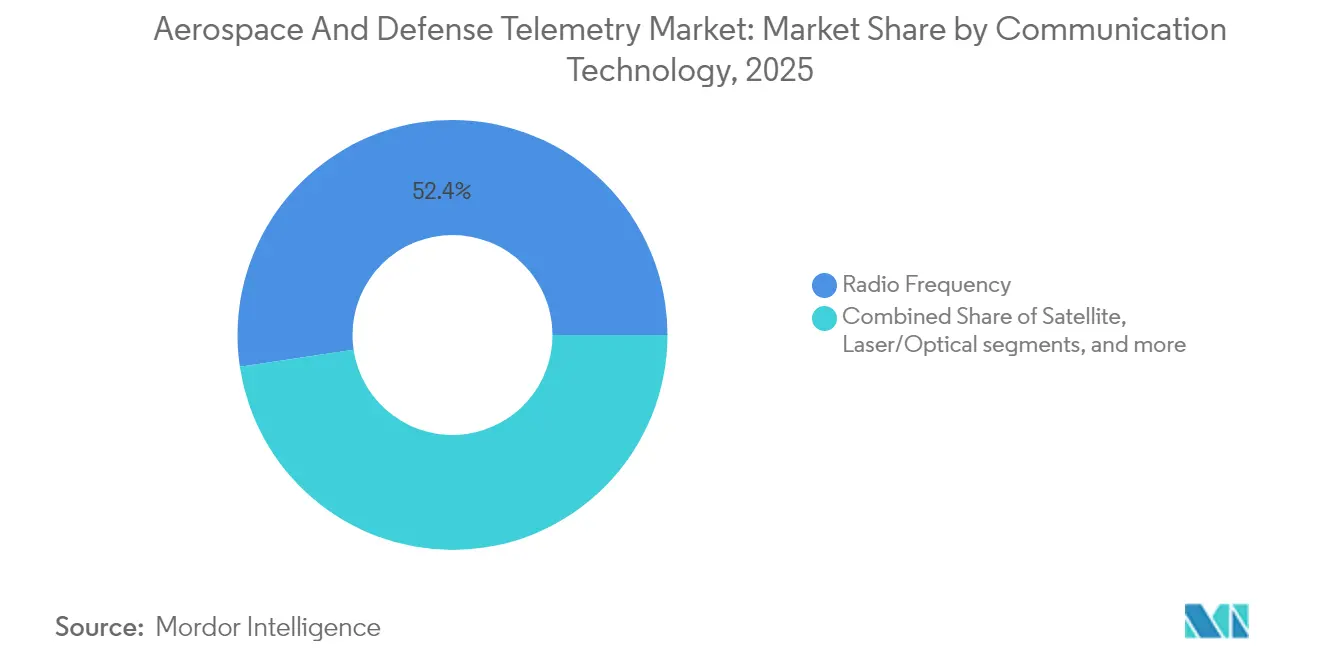

- By communication technology, radio frequency links held 52.35% of the aerospace and defense telemetry market share in 2025, while laser/optical systems are set to compound at a 9.07% CAGR through 2031.

- By component, transmitters and sensors account for 26.10% of the aerospace and defense telemetry market size in 2025; software and data analytics platforms are projected to expand at an 8.43% CAGR by 2031.

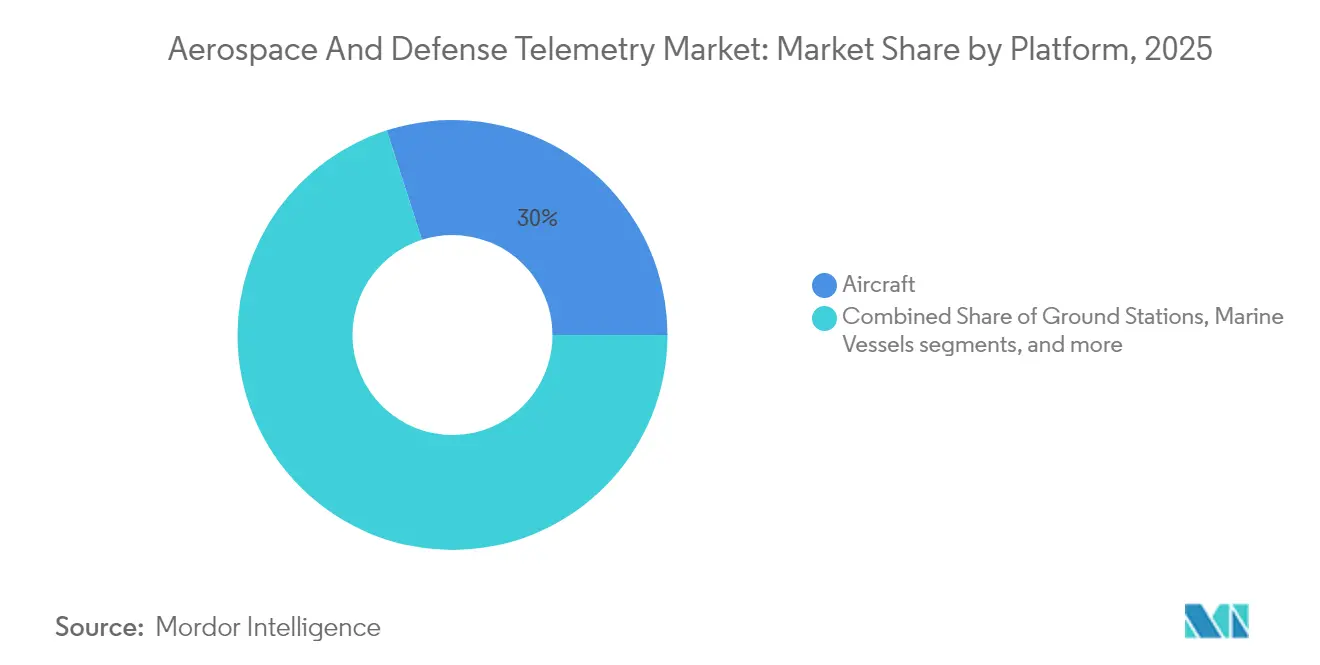

- By platform, aircraft maintained a 29.95% revenue share in 2025, yet UAVs registered the fastest growth at 10.72% CAGR over the forecast horizon.

- By end user, defense represented 63.30% of the aerospace and defense telemetry market in 2025, while the commercial aerospace segment accelerates at an 8.41% CAGR through 2031.

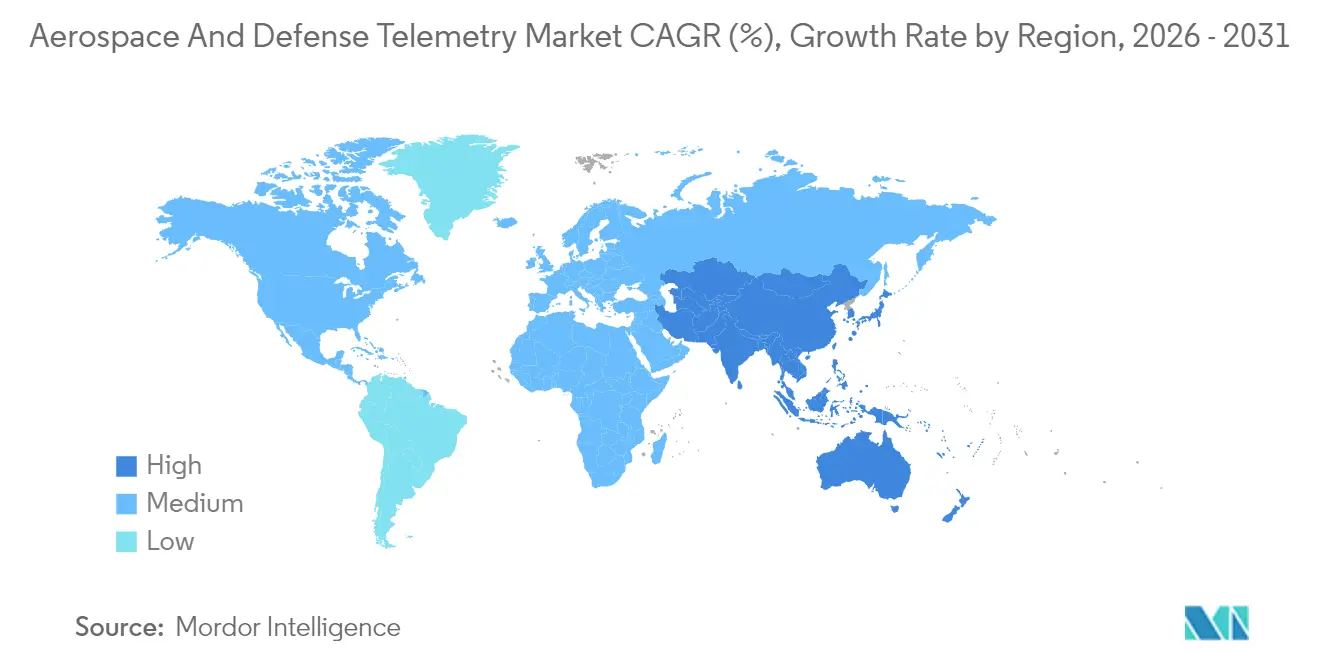

- North America led with a 35.70% revenue share in 2025; Asia-Pacific is poised for the quickest advance, with a 8.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aerospace And Defense Telemetry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of hypersonic and reusable launch vehicle programs | +1.2% | United States, China, Russia, wider global spillover | Medium term (2-4 years) |

| Proliferation of small satellite constellations requiring high-bandwidth telemetry | +0.8% | North America and Europe lead | Short term (≤ 2 years) |

| Modernization of airborne ISR platforms across defense alliances | +1.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Emergence of space-based edge AI for real-time data processing | +0.9% | Early adoption in United States and China | Long term (≥ 4 years) |

| Increased adoption of commercial software-defined radios in defense telemetry | +0.7% | North America, Europe, emerging Asia-Pacific uptake | Short term (≤ 2 years) |

| Growing use of passive telemetry for condition-based maintenance | +0.6% | United States, United Kingdom, Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Hypersonic and Reusable Launch Vehicle Programs

Hypersonic flight places unprecedented thermal and plasma-induced stress on data links, forcing designers to develop telemetry modules that sustain lock at velocities above Mach 5. Stratolaunch’s Talon-A2 test flights in 2024 proved the need for shock-hardened antennas that survive multiple sorties while delivering health-monitoring data at kilohertz refresh rates. Reusability compounds the engineering challenge because avionics must tolerate repeated heat-cycle loading without drifts in calibration. L3Harris has embedded multi-band transmitters inside its hypersonic glide vehicles to stream trajectory and seeker-status packets that feed real-time fire-control algorithms.[1]L3Harris Technologies, “Hypersonic Solutions Overview,” l3harris.com The cumulative effect elevates the Aerospace and Defense Telemetry market as defense ministries allocate dedicated budgets for survivable flight-test instrumentation and production-grade weapon telemetry.

Proliferation of Small Satellite Constellations Requiring High-Bandwidth Telemetry

Starlink’s deployment of more than 10,000 laser communication terminals has set the reference architecture for low-earth-orbit mesh networks that shuttle traffic laterally before downlink. Smaller operators emulate the approach, driving sustained demand for optical terminals and software-defined radios that negotiate bandwidth dynamically across thousands of nodes. The Aerospace and Defense Telemetry market benefits because military planners value inter-satellite links for resilient command-and-control when adversaries jam ground gateways. Dynamic waveform agility allows constellation managers to throttle bandwidth toward urgent sensor data while compressing housekeeping traffic, honing resource utilization, and protecting margins.

Modernization of Airborne ISR Platforms Across Defense Alliances

NATO’s E-7 Wedgetail adoption and the US Air Force Distributed Common Ground System upgrade hinge on telemetry refreshes that merge signals intelligence, radar, and electro-optical feeds into unified tactical pictures. Data rates climb as fifth-generation aircraft stream sensor-fusion packets to allied command centers, requiring real-time encryption and low-probability-of-intercept signaling. The Aerospace and Defense Telemetry market meets these needs by fielding phased-array antennas and embedded cyber-hardening firmware that preserve link integrity in contested spectra. Interoperability standards agreed within Five Eyes and NATO further accelerate procurement cycles because allied forces can now plug telemetry payloads into mixed-fleet platforms without bespoke integration.

Emergence of Space-Based Edge AI for Real-Time Data Processing

Advances in radiation-tolerant GPUs allow satellites to process images, extract anomalies, and even reprioritize pointing schedules without human intervention. Experiments under NASA’s Pathfinder program showed how on-board convolutional neural networks cut downlink volume by 75% while boosting tactical relevance. AI-enabled telemetry also empowers spacecraft to issue self-healing commands when sensors flag degradation, prolonging mission life. In defense scenarios, satellites can autonomously cue ISR assets when they detect missile launches, executing cross-domain workflows faster than ground operators could react. Such autonomy contributes directly to the Aerospace and Defense Telemetry market expansion because each edge node still requires secure metadata links to propagate decisions across the wider constellation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum congestion and international coordination delays impacting bandwidth access | -0.9% | High pressure in Europe and Asia | Short term (≤ 2 years) |

| Size, weight, and power (SWaP) limitations in small UAV platforms constrain telemetry integration | -0.5% | Global UAV operators | Medium term (2-4 years) |

| Export controls and cyber-sovereignty clauses restricting cross-border technology transfer | -0.6% | Global, with primary impact on US-China-EU technology flows | Long term (≥ 4 years) |

| Rising satellite launch insurance costs limiting available budgets for telemetry systems | -0.3% | Global, concentrated in commercial space sector | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Spectrum Congestion and International Coordination Delays Impacting Bandwidth Access

The ITU’s Master International Frequency Register faces mounting backlogs as operators file for thousands of constellations overlapping Ku-, Ka-, and V-band allocations. Defense platforms seeking protected bands must now wait several months for clearance, impeding program schedules. In national jurisdictions like the United States, FCC auctions repurpose legacy C-band for 5G, squeezing telemetry users into narrower slices. Cross-border coalition exercises suffer when frequency conflicts force last-minute re-planning, reducing training value. Adaptive spectrum-sharing radios show promise, yet regulators have not fully codified real-time coordination rules, prolonging uncertainty for the Aerospace and Defense Telemetry market.

Size, Weight, and Power (SWaP) Limitations in Small UAV Platforms Constrain Telemetry Integration

Ultralight drones operate on tight energy budgets, making every gram and milliwatt count. TinySense avionics, weighing 78.4 mg, illustrate how extreme miniaturization opens new mission envelopes but imposes stringent thermal management limits. Multirotor endurance drops sharply if high-throughput transmitters draw constant power, forcing designers to schedule burst transmissions or adopt elastic-rate coding. The Aerospace and Defense Telemetry market addresses the dilemma through system-on-chip radios that merge modulation, encryption, and processing blocks on a single die. Yet, overall progress remains gated by battery chemistry advances and lightweight antenna materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Communication Technology: Laser Communications Drive Next-Generation Capabilities

Laser/optical links recorded the strongest expansion, advancing at a 9.07% CAGR between 2026 and 2031. Adoption surged after the Space Development Agency published its Optical Communication Terminal Standard v4.0.0, giving primes a clear compliance roadmap. Compared with microwave systems, optical beams deliver 10 to 100-fold bandwidth with tighter spatial confinement that curtails interception risk. In conjunction with adaptive beam-steering mirrors, satellites now switch companions in microseconds, supporting mesh routing no longer bottlenecked by ground relays.

Radio Frequency architectures retained 52.35% revenue in 2025, underscoring the deep installed base and all-weather robustness that militaries trust for command-critical tasks. Spectrum pressure and growing anti-spoofing demands push integrators to blend the two modalities, launching hybrid terminals that can hop between Ka-band and optical carrier. This duality sustains Radio Frequency procurement while infusing new revenue into the aerospace and defense telemetry market. The Starlink rollout creates double-digit demand for optical terminal components, positioning laser equipment suppliers for sustained backlog growth.

By Component: Software Platforms Transform Data Analytics

Software and data analytics platforms post the fastest 8.43% CAGR over 2026-2031 as operators shift from raw packet storage to predictive insight generation. Integrated dashboards now fuse telemetry, logistics, and environmental feeds to produce maintenance recommendations minutes after flight termination. For instance, Boeing’s Condition-Based Smart Maintenance suite blends engine vibration spectra with flight regime tags to flag parts approaching fatigue thresholds.

Transmitters and sensors remained the largest slice at 26.10% in 2025 because every node—a hypersonic vehicle, a nanosatellite, or a UAV—needs physical transducers and power-amplifier chains. Continuous miniaturization compresses these elements into chip-scale packages, freeing space for edge processors. Improved component yields and declining ASIC mask costs lower entry barriers, attracting new suppliers into the Aerospace and Defense Telemetry market and fueling price competition that accelerates volume adoption.

By Platform: UAVs Lead Innovation in Autonomous Systems

Unmanned Aerial Vehicles (UAVs) achieved the highest 10.72% CAGR, propelled by swarming concepts that demand resilient, low-latency links for coordinated maneuvers. Militaries test attributable drones that ferry expendable EW payloads, each requiring telemetry streams that confirm the electronic effect on targets before self-destructing. Commercial parcel-delivery pilots also intensify data needs for route verification and airspace deconfliction.

Manned aircraft still commanded 29.95% of total revenue in 2025, reflecting large fleets of fighters, tankers, and transports undergoing avionics refresh cycles. Missile and projectile segments remain niche yet mission-critical: telemetry modules behind warheads collect impact analytics that guide design tweaks in subsequent blocks. These varied use cases enlarge the Aerospace and Defense Telemetry market because suppliers must tailor ruggedization, encryption, and frequency agility to each domain while sustaining economies of scale.

By End User: Commercial Aerospace Accelerates Growth

Defense requirements anchored 63.30% of 2025 turnover, but the commercial and civil aerospace segment accelerates at 8.41% CAGR as advanced air-mobility prototypes move from concept to certification. eVTOL platforms integrate multi-redundant telemetry buses, simultaneously conveying battery chemistry, structural load, and air-traffic data.

Satellite broadband providers likewise escalate procurement, embedding health-monitoring sensors in every bus to protect uptime guarantees for consumer subscribers. As civilian missions converge with militarized space traffic management, dual-use demand strengthens the aerospace and defense telemetry market. Shared component standards allow volume pricing that benefits both sides of the customer base.

Geography Analysis

North America retained the largest 35.70% share in 2025 as the US Department of Defense contracts for hypersonic glide vehicles and next-generation ISR platforms kept domestic lines busy. Prime contractors bundle telemetry R&D with full-system bids, keeping value onshore and sustaining robust engineering pipelines. Strong venture-capital appetite for space start-ups further cements regional leadership.

Asia-Pacific posts the most rapid 8.88% CAGR through 2031. China scales factory output of small satellite buses that ship with plug-and-play optical terminals, while India's reusable launch ambitions drive consistent telemetry component requisitions for thermal-cycle testing. Japan channels robotics expertise into miniaturized lunar and asteroid probes' transceivers, turning regional suppliers into global price setters for ultra-compact hardware.

Europe pursues autonomous and sustainable air-traffic goals under SESAR 3.0, prompting local integrators to adopt cyber-resilient software-defined radios inside crewed and uncrewed airframes. The forthcoming EU Space Act, scheduled for late-2025 implementation, will mandate compliance logs for telemetry encryption algorithms operating in EU orbital slots. This new rulebook could marginally slow procurement, yet ultimately harmonizes standards, enlarging addressable demand for certified vendors within the aerospace and defense telemetry market.

Regulatory Landscape

Telemetry programs operate under spectrum licensing requirements, range-test interoperability standards, and export control regimes. In the United States, the Range Commanders Council (RCC) IRIG 106 standard remains a core compliance anchor for flight-test and range telemetry, and the January 2025 publication of IRIG 106-24R1 reinforces unified criteria for telemetry transmitting, receiving, and signal processing across government ranges.

On the space side, regulators and standards bodies shape TT&C and mission data handling through both policy and technical protocols. The FCC advanced rulemaking activity in April 2026 to expand spectrum access for emergent space operations, including proposals tied to Space Operation Service (SOS) classifications and secondary allocations to ease TT&C spectrum constraints. Export governance also affects cross-border supply of telemetry-capable systems; in January 2026, an Interim Final Rule amended the Export Administration Regulations (EAR) following E.O. 14307 (June 2025), streamlining certain civil UAV exports to non-adversarial partners while maintaining controls for dual-use defense-relevant technology. For multi-agency and international space missions, CCSDS recommended standards continue to serve as a key interoperability reference for packetized telemetry and related services.

Value Chain Analysis

The aerospace and defense telemetry value chain starts with specialized electronic and RF inputs, including radiation-tolerant and high-reliability semiconductors, sensors and transducers, power amplifiers, RF materials, optics and photonics for laser links, and secure embedded compute. These feed subsystem manufacturing for transmitters, receivers, antennas and modulators, signal processing units, and data recorders, followed by platform integration on aircraft, spacecraft and launch vehicles, UAVs, missiles and projectiles, and ground stations. System-level delivery typically combines hardware with software-defined radios, encryption, key management, and data analytics platforms, then moves through qualification, range certification, and sustainment activities such as spares, depot repair, calibration, and upgrades.

Standards and interoperability bodies shape interfaces and test compliance across the chain, including the International Foundation for Telemetering (IFT) and its Telemetry Standards Coordinating Committee (TSCC), as well as industry standards efforts via the Aerospace Industries Association (AIA) and ASD-STAN. Government-guided modularity initiatives, including the Space Systems MOSA Interface Standards Alliance, support open interfaces that broaden the supplier base and reduce proprietary lock-in. Supply chain resilience practices are increasingly tied to digital tools, including digital twins for configuration baselines, AI/ML for demand and inventory visibility, and traceability methods for high-assurance parts, reflecting the need to manage long qualification cycles, obsolescence risk, and cybersecurity requirements for telemetry endpoints and ground segments.

Competitive Landscape

The aerospace and defense telemetry market displays moderate consolidation, whereby top system integrators control complete value chains from sensor to analytics. BAE Systems plc’s USD 5.5 billion purchase of Ball Aerospace expanded optical communications and ground-segment capacity overnight. In early 2025, AeroVironment closed a USD 4.1 billion deal for BlueHalo, adding electronic warfare expertise that complements its unmanned systems franchise.

Teledyne Technologies sustains a 53.21% share in its high-end sensor niche thanks to iterative acquisitions and robust 13.02% net margins. Kratos Defense differentiates on software-defined flexibility, fielding quantumRadio and quantumFEP units that swap waveforms without hardware changes.[4]Kratos Defense, “Software-Defined Ground Segment Portfolio,” kratosdefense.com Edge-AI convergence pressures classical hardware vendors to pair silicon with machine-learning toolkits or risk displacement by cloud-native entrants.

White-space pockets exist in quantum-encrypted links and self-healing mesh protocols that maintain command resilience when individual nodes jam or fail. Export-control reforms published in the United States Federal Register during October 2024 eased civil-space telemetry shipments while preserving ITAR guardrails for defense payloads. Players that internalize compliance engineering early will reduce time-to-market and secure leadership as regulatory complexity rises.

Aerospace And Defense Telemetry Industry Leaders

BAE Systems plc

Lockheed Martin Corporation

L3Harris Technologies, Inc.

Safran SA

RTX Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity area is modernization of flight-test and hypersonic telemetry infrastructure, as programs shift from legacy dish-centric architectures toward mobile, reconfigurable, and all-digital range assets aligned to network-based telemetry. In May 2026, AeroVironment secured a USD 43 million TRMC contract to integrate PANTHER phased-array antenna systems on SkyRange platforms for hypersonic flight testing, which points to active spend on resilient tracking and high-data-rate collection in stressed RF environments. Alongside this, procurement activity for NSA-certified secure airborne telemetry units, including large, compact, and miniature support packages, highlights demand for cybersecurity-hardened telemetry endpoints aligned to modern defense cybersecurity requirements.

Space-based sensing layers and proliferated LEO architectures also expand the need for TT&C, inter-satellite links, and secure data movement between space and ground. In July 2026, the Space Development Agency awarded USD 1.75 billion to L3Harris and Sierra Space for 36 Accelerated Missile Defense Tranche 3 satellites, and the US Space Force awarded SpaceX a USD 4.16 billion contract for an AMTI constellation, reinforcing the value of high-bandwidth and anti-jam telemetry pathways across distributed nodes. Standardization further supports entry for subsystem specialists: the RCC IRIG 106 updates (including 106-24 and 106-24R1) and the DoD shift toward Telemetry Network Standard (TmNS) concepts increase pull-through for software-defined, MOSA-aligned interfaces, ground segment automation, and edge processing that reduces downlink burden while preserving verifiable data integrity for test and operational missions.

Recent Industry Developments

- July 2026: The Space Development Agency awarded contracts totaling about USD 1.75 billion to L3Harris and Sierra Space to build 36 Accelerated Missile Defense Tranche 3 satellites. The awards expand a proliferated LEO tracking layer, increasing demand for satellite TT&C, crosslink-ready terminals, and ground processing designed for rapid constellation-scale operations.

- December 2025: The Space Development Agency awarded L3Harris up to USD 843 million to build 18 infrared tracking satellites for Tranche 3 of the Proliferated Warfighter Space Architecture. The program supports serial production and integration of mission data handling, telemetry links, and resilient networking across distributed spacecraft.

- March 2024: Safran announced InRange, a global satellite telemetry service designed to receive real-time launcher data across trajectories, including oceanic regions. The offering shifts portions of launch telemetry reception toward managed services, widening options for operators that need continuous coverage without building dedicated ground infrastructure.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define aerospace and defense telemetry as the hardware, software, and supporting equipment used to measure, transmit, receive, and process mission or test data from platforms such as aircraft, spacecraft, UAVs, missiles, and ground stations.

Scope exclusions: This sizing excludes adjacent onboard communications, navigation, and general avionics spending that is not directly tied to telemetry data capture and downlink workflows.

Segmentation Overview

- By Communication Technology

- Radio Frequency

- Satellite

- Laser/Optical

- Ethernet/Fiber-Optic

- By Component

- Transmitters and Sensors

- Antennas and Modulators

- Software and Data Analytics Platforms

- Signal Processing Units

- Ground Receiving Equipment

- By Platform

- Aircraft

- Spacecraft and Launch Vehicles

- Unmanned Aerial Vehicles (UAVs)

- Missiles and Projectiles

- Marine Vessels

- Ground Stations

- By End User

- Aerospace

- Defense

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Paific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the baseline structure of the telemetry value chain and to anchor assumptions that can be checked in public sources. We relied on materials such as defense budget documents and procurement disclosures, spectrum and communications references from regulators such as the FCC and ITU, trade and shipment signals from customs and statistical offices, and aerospace program context from NASA and ESA publications.

To keep the model grounded, we also reviewed company annual reports, investor presentations, press releases, and trade association updates tied to flight test, range modernization, and space launch activity. Where useful, we referenced paid subscriptions for company financials and intelligence, a patent database to track telemetry component innovation, and aerospace and aviation databases for aircraft and engine level program visibility. The desk sources listed here are illustrative, and other public and paid references were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work was completed through structured interviews and targeted surveys with program managers, engineering leads, procurement teams, integrators, and component suppliers involved in airborne, space, and range telemetry deployments. We covered the main demand pockets across APAC, EMEA, and the Americas so pricing logic, platform mix, and adoption timing could be validated, and then used to close gaps where desk sources do not explain drivers well.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | APAC: 46% |

| Mid tier: 41% | Functional/Unit leaders: 35% | EMEA: 31% |

| Smaller Players: 22% | Managers: 53% | Americas: 23% |

Market-Sizing & Forecasting

Sizing started with a top-down build where aerospace and defense platform activity and program spend signals were translated into a telemetry demand pool by applying telemetry fit rates and typical content-per-platform ranges (for example, flight test intensity, range infrastructure upgrades, and space launch cadence). Once the overall picture was formed, we corroborated it with selective bottom-up approximations, such as sampled supplier revenues, program level channel checks, and volume times ASP checks for key components, which are then used to adjust outliers.

Key inputs used in the model included the number of flight tests and qualification campaigns, modernization cycles for test ranges and ground receiving equipment, the mix of communication technologies used for telemetry links, platform deliveries and upgrades across air and space, and observable pricing direction for transmitters, antennas, and processing units. When gaps existed in bottom-up evidence for smaller contracts or classified programs, assumptions were filled using proxy ratios from comparable platform classes, then validated through follow-up calls.

For forecasting, we used scenario analysis supported by a simple multivariate regression overlay, where demand was linked to platform activity, defense and space budget direction, and replacement timing for aging telemetry infrastructure. The final forecast was reviewed with primary respondents to keep the pacing of adoption and the timing of larger program ramps realistic.

Data Validation & Update Cycle

Outputs were validated through triangulation across three layers, desk indicators, primary feedback, and internal consistency checks within the model. Variance checks were run by region and by platform type so unusual jumps in ASPs, shipment volumes, or growth rates could be flagged and explained before sign-off.

Each estimate goes through multi-step analyst reviews, with re-contacts triggered when a major contract, program delay, budget revision, or technology shift changes the demand outlook. Reports are refreshed annually, and interim updates are added when material events are seen. Before delivery, a fresh analyst pass is completed so clients receive the most up-to-date view aligned to the latest available data.

Mordor Intelligence's Aerospace and Defense Telemetry Market Estimate Compared With Other Published Estimates

Published numbers for aerospace and defense telemetry often do not match because the market can be framed narrowly around telemetry links and range equipment, or more broadly around adjacent communications and avionics value. Differences also come from how each publisher treats platform coverage, currency timing, and whether estimates are updated after major program or budget changes.

The table shows a wide spread, and in Mordor Intelligence's model the total is tied to telemetry-specific components and software used for measurement, transmission, reception, and processing across aerospace and defense platforms, rather than folding in broader satcom or general onboard communications spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.23 B (2026) | |

| Industry Research Publisher A | USD 4.20 B (2024) | Uses an earlier base year and appears to include a wider set of real-time monitoring and satellite communications related spending, which can pull in adjacent communications value beyond telemetry equipment and processing. |

| Research Publisher B | USD 1.69 B (2024) | Anchors the model to a narrower component basket and a different forecast window, which can undercount software, data analytics layers, and range infrastructure spend that is often procured outside component line items. |

Looking across the three figures, most of the difference can be traced back to what gets counted as telemetry versus adjacent communications, plus the year used to anchor prices and volumes. Our approach stays traceable to platform activity and repeatable pricing and adoption assumptions, which makes the final number easier to reconcile when inputs move.

Key Questions Answered in the Report

What is the current size of the Aerospace and Defense Telemetry market and how fast is it growing?

The market stands at USD 2.23 billion in 2026 and is forecasted to reach USD 3.12 billion by 2031, registering a 6.99% CAGR.

Which communication technology is expanding the quickest?

Laser/optical telemetry solutions are advancing at a 9.07% CAGR because they deliver 10-100x higher bandwidth and face fewer spectrum constraints than radio links.

Why are unmanned aerial vehicles (UAVs) attracting so much telemetry investment?

UAV telemetry posts the highest 10.72% CAGR as autonomous and swarming concepts demand resilient, low-latency links for navigation, data fusion, and health monitoring.

Which region presents the strongest growth opportunity for telemetry suppliers?

Asia-Pacific is expected to expand at a 8.88% CAGR through 2031, driven by China’s satellite production, India’s launch programs, and Japan’s miniaturized electronics initiatives.

How are hypersonic programs influencing telemetry specifications?

Hypersonic vehicles require shock-hardened, high-temperature transceivers that maintain lock above Mach 5 and survive multiple reuse cycles, pushing vendors to deliver ultra-reliable, plasma-resistant links.

Page last updated on: