Market Overview

| Study Period | 2020 - 2030 |

|---|---|

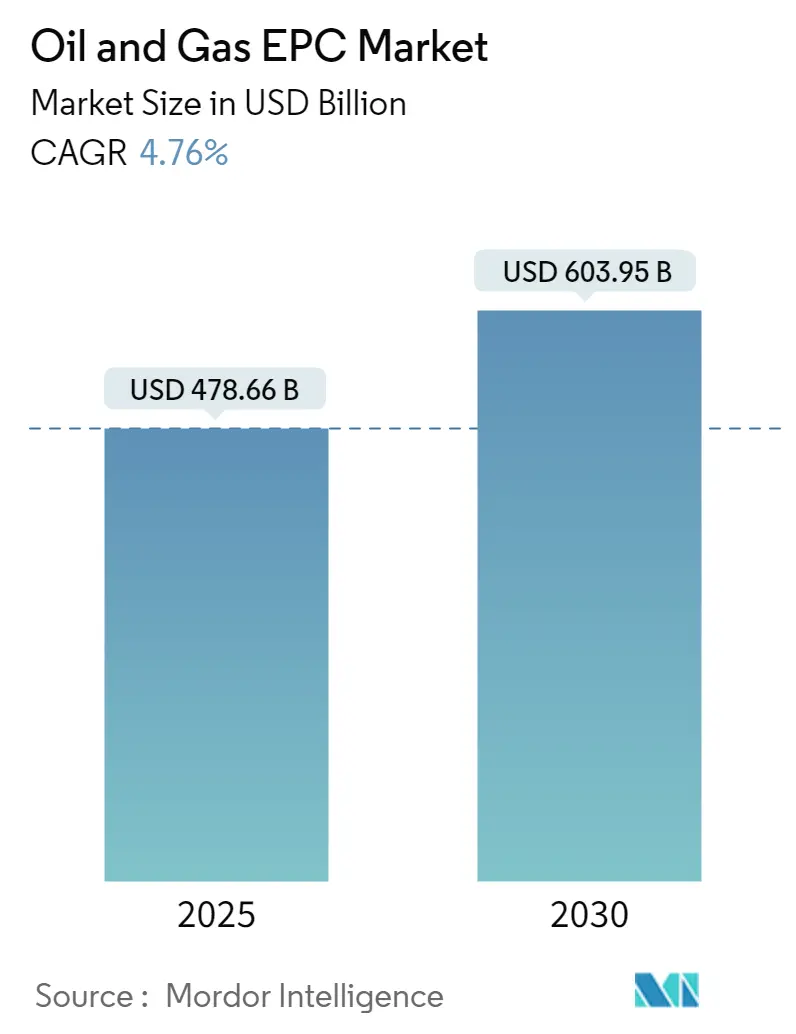

| Market Size (2025) | USD 478.66 Billion |

| Market Size (2030) | USD 603.95 Billion |

| Growth Rate (2025 - 2030) | 4.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oil & Gas EPC Market Analysis by Mordor Intelligence

The Oil & Gas EPC Market size is estimated at USD 478.66 billion in 2025, and is expected to reach USD 603.95 billion by 2030, at a CAGR of 4.76% during the forecast period (2025-2030).

The oil and gas engineering, procurement, and construction (EPC) industry continues to evolve amid shifting global energy dynamics and technological advancements. The sector has witnessed significant transformation in project execution approaches, with an increasing emphasis on modular construction and digital integration. Major oil and gas companies are adopting innovative EPC strategies to optimize project delivery timelines and cost efficiency, particularly evident in the United States, where the active rotary rig count reached 756 as of June 2022, with 738 being onshore rigs, demonstrating the industry's robust operational activity.

The industry is experiencing a notable shift toward natural gas infrastructure development, particularly in the LNG sector. This trend is exemplified by significant project investments such as Qatar Energy's North Field East development project worth USD 30 billion, announced in Q1 2021, representing one of the largest upstream projects sanctioned globally. The scale of such projects highlights the industry's commitment to expanding natural gas capabilities and the critical role of EPC contractors in delivering complex oil and gas infrastructure.

The offshore segment has emerged as a crucial growth area for EPC contractors, with an increasing focus on floating production systems and deep-water developments. Brazil's ambitious plans to deploy approximately 18 Floating Production Storage and Offloading (FPSO) units by 2025 exemplify this trend, showcasing the industry's push toward advanced offshore solutions. These developments are driving innovation in EPC project execution, particularly in areas requiring specialized oil and gas construction and engineering capabilities.

The market is witnessing substantial investments in unconventional gas field developments, illustrated by Saudi Aramco's award of EPC contracts worth USD 10 billion in November 2021 for the Jafurah unconventional gas field development. This project, along with similar developments globally, demonstrates the industry's focus on expanding gas production capabilities and the growing importance of EPC expertise in handling technically challenging projects. The trend toward larger, more complex projects is reshaping the competitive landscape, favoring EPC contractors with comprehensive capabilities and proven track records in managing mega-projects. The role of petroleum engineering in these projects is becoming increasingly significant as the industry seeks to enhance efficiency and sustainability.

Global Oil & Gas EPC Market Trends and Insights

Growing Development of Gas Fields and LNG Infrastructure

The increasing global focus on natural gas development and LNG Engineering, Procurement, and Construction infrastructure expansion has emerged as a significant driver for the oil and gas EPC market. The development of gas fields worldwide is creating substantial demand for oil and gas infrastructure, particularly for the transportation of natural gas through pipelines and LNG facilities. This is evidenced by major projects like Qatar's North Field East development project, where companies like Saipem secured contracts worth USD 1.7 billion for engineering, procurement, and construction of various offshore facilities, including platforms, supporting structures, and subsea cables.

The LNG sector is witnessing remarkable growth in infrastructure development across multiple regions. For instance, India is planning to expand its LNG import capacity by 40% through the commissioning of delayed new terminals. The country, being the world's fourth-largest LNG buyer, is actively developing its LNG infrastructure with projects like H-Energy's Jaigarh Floating Storage Unit and Swan Energy's 5 million ton/year FSRU at Jafrabad. Similarly, Germany announced plans to build two LNG terminals in Brunsbuttel and Wilhelmshaven, with the FSRU having a capacity of 7.3 MTPA, demonstrating the global scale of LNG infrastructure development.

Understand The Key Trends Shaping This Market

Download PDF

Rising Offshore Exploration and Production Activities

The increasing shift towards offshore exploration and production activities has become a major driver for the oil and gas EPC market, particularly as companies seek to tap into new reserves in deep and ultra-deep waters. According to industry data, floating platforms have gained significant importance as they eliminate the need for expensive long-distance pipeline Engineering, Procurement, and Construction from production facilities to onshore terminals, making them particularly economical for smaller oil fields. The EPC services for offshore structures now encompass a wide range of activities, from design and fabrication to installation and commissioning of fixed platforms, FPSOs, and floating production facilities.

The offshore sector is witnessing substantial investments in new projects and field developments. For instance, in the United Arab Emirates, ADNOC awarded two EPC contracts totaling USD 1.46 billion for the Dalma Gas Development Project, which aims to produce around 340 million standard cubic feet per day of natural gas. Similarly, Petrobras in Brazil is planning to deploy approximately 18 FPSOs by 2025, with significant EPC contracts being awarded for units like the P-80 FPSO with a capacity to produce 225,000 barrels per day of oil and 12 million cubic meters per day of natural gas. These developments highlight the growing importance of offshore activities in driving EPC market growth.

Increasing Energy Demand in Developing Economies

The surge in energy demand from developing economies, particularly in the Asia-Pacific region, has emerged as a crucial driver for the oil and gas EPC market. This is evidenced by the significant investments in upstream and midstream infrastructure development to meet the rising demand for both industrial and commercial sectors. For instance, CNOOC Ltd has announced ambitious plans to accelerate the exploration and development of natural gas, including deepwater reserves in the South China Sea and unconventional resources onshore in China, with plans to make gas 30% of its portfolio by 2025 and 50% by 2035.

The growing urbanization and industrialization in these regions have led to increased investments in oil and gas project management and infrastructure development. This is reflected in major investment announcements such as Indian Oil Corporation Limited's USD 102 billion commitment to petroleum, oil, and lubricant storage capacities, including new greenfield facilities. Additionally, national oil companies in various developing nations are actively expanding their exploration and production capabilities, as demonstrated by new exploration contracts signed in regions like Egypt, where companies like Eni have secured exploration rights in five blocks across the Eastern Mediterranean Sea, Western Desert, and Gulf of Suez.

Segment Analysis

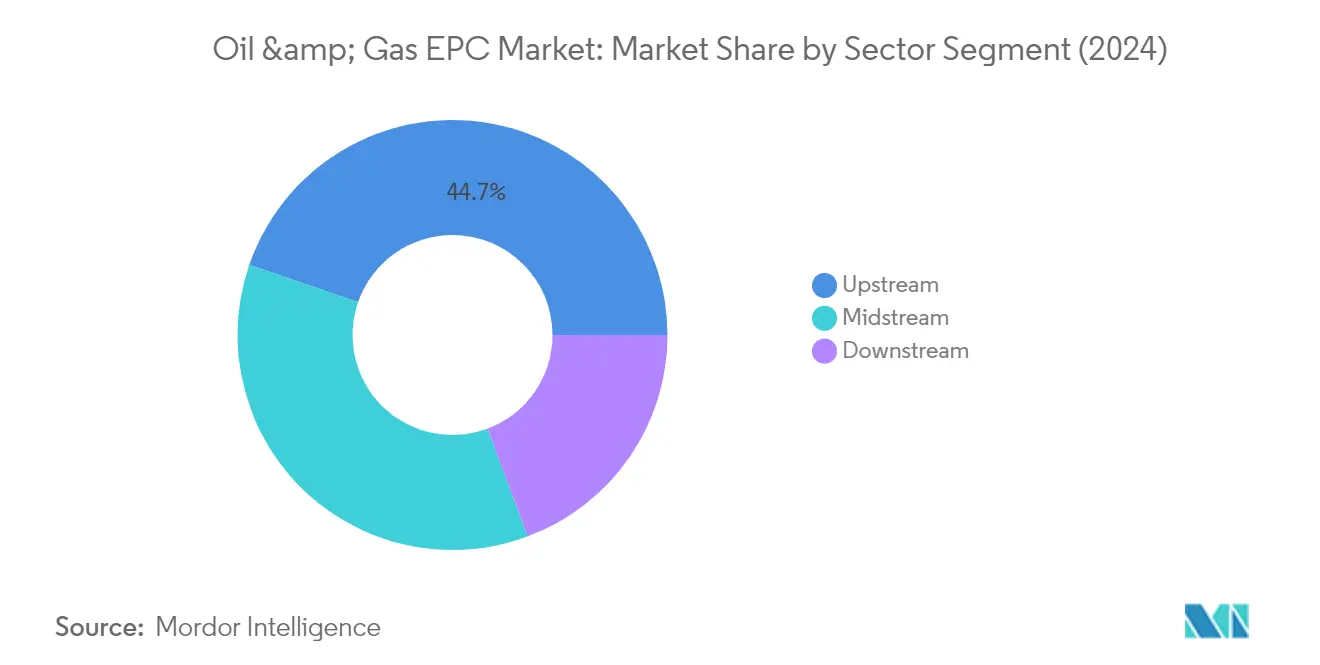

Upstream Segment in Oil & Gas EPC Market

The upstream segment dominates the global oil and gas EPC market, accounting for approximately 45% of the total market share in 2024. This segment encompasses onshore and offshore exploration and production-related services, including design, fabrication, installation, commissioning, and start-up of fixed platforms, floating production storage and offloading (FPSO) units, and floating production facilities for shallow, deepwater, and ultradeepwater regions. The identification and assessment of development options for offshore facilities, whether based on fixed or floating structures, remain crucial for EPC contractors. The segment's dominance is driven by major projects like Qatar's North Field East development and significant investments in offshore oil and gas infrastructure development across key regions like the Middle East, North America, and Asia-Pacific.

Midstream Segment in Oil & Gas EPC Market

The midstream segment is projected to experience substantial growth during the forecast period 2024-2029, driven by increasing investments in LNG infrastructure and pipeline networks globally. This growth is supported by the rising demand for natural gas transportation infrastructure, particularly in emerging economies. The segment's expansion is further bolstered by significant developments in LNG regasification terminals, gas treatment plants, and storage facilities. Major projects like the United States' LNG export terminal expansions and Qatar's LNG infrastructure development are expected to create substantial opportunities for oil and gas construction and EPC contractors in the midstream sector.

Remaining Segments in Oil & Gas EPC Market

The downstream segment, while smaller in market share, plays a vital role in the oil and gas EPCM market through refinery and petrochemical infrastructure development. This segment focuses on the construction and modernization of refineries, petrochemical plants, and related facilities. The segment's growth is primarily driven by capacity expansion projects in Asia-Pacific and the Middle East, where countries are investing in new refining capabilities to meet increasing domestic demand for refined products and reduce dependence on imports. The downstream sector continues to evolve with an increasing focus on clean fuel projects and modernization of existing facilities.

Geography Analysis

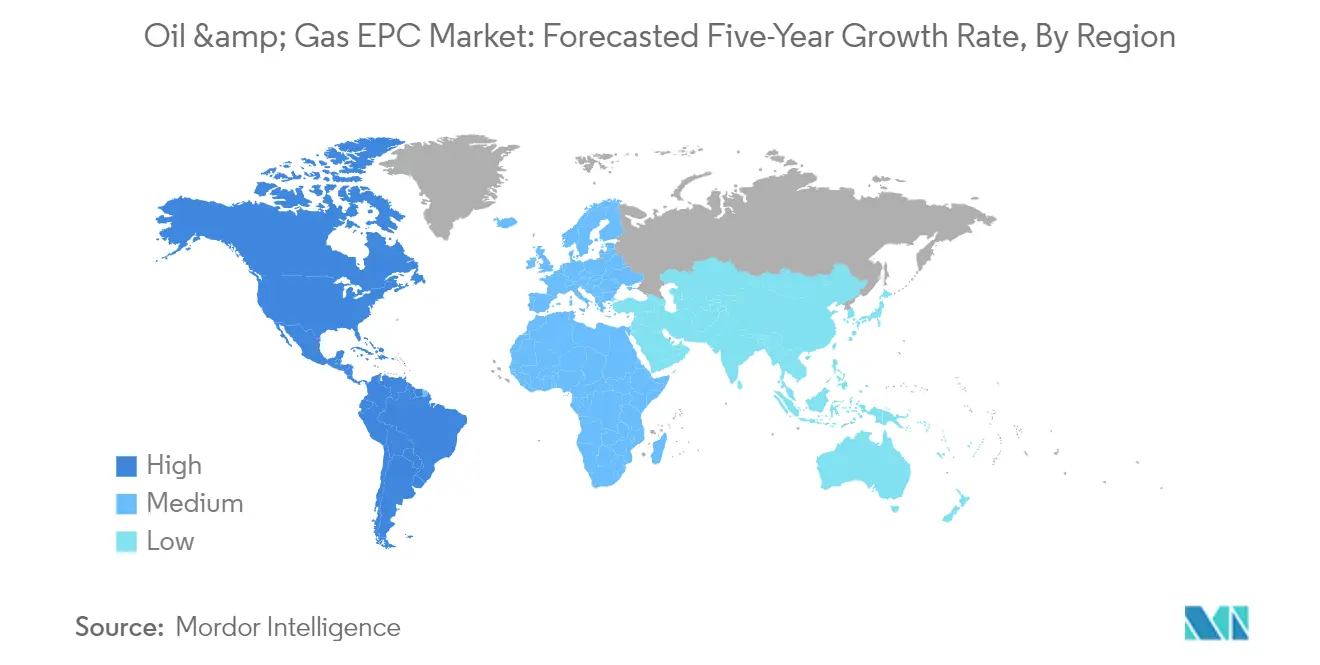

Oil & Gas EPC Market in North America

North America dominates the global oil and gas EPC market, commanding approximately 100% of the total market share in 2024. The region's prominence is driven by its extensive oil and gas infrastructure market, particularly in the United States, which has maintained its position as the world's largest crude oil producer since 2018. The market is characterized by a robust combination of onshore and offshore projects, with a particular focus on shale oil and gas developments. The region's EPC sector benefits from advanced technological capabilities, well-established regulatory frameworks, and significant investment in both conventional and unconventional resource development. The United States leads regional activities, accounting for about 70% of total EPC projects, with a strong emphasis on new build projects in the upstream sector. Canada and Mexico complement the market with their respective oil sands projects and ongoing energy reform initiatives, creating a diverse and dynamic market landscape.

Oil & Gas EPC Market in Asia-Pacific

The Asia-Pacific region has demonstrated remarkable resilience and growth in the oil and gas EPC market, registering approximately 17% growth from 2019 to 2024. The market is primarily driven by China, India, and emerging Southeast Asian economies, with significant investments in both upstream and downstream sectors. The region's growth trajectory is supported by increasing energy demand, rapid industrialization, and ambitious national energy security initiatives. China leads the regional market with its extensive refining capacity expansion plans and offshore development projects, while India focuses on modernizing its existing infrastructure and expanding its natural gas network. The market is characterized by a strong presence of both international and regional EPC contractors, fostering competitive dynamics and technological innovation. Southeast Asian countries are emerging as significant contributors to market growth, particularly in LNG infrastructure development and offshore projects.

Oil & Gas EPC Market in Europe

The European oil and gas EPC market is projected to grow at approximately 2% annually from 2024 to 2029, reflecting a measured but steady expansion trajectory. The region's market is undergoing significant transformation driven by energy transition initiatives and the modernization of aging infrastructure. Norway and the United Kingdom continue to be key markets for offshore projects, while Eastern European countries focus on expanding their natural gas infrastructure. The market is characterized by a strong emphasis on technological innovation, particularly in sustainable and efficient project execution. European EPC contractors are increasingly focusing on integrating renewable energy capabilities alongside traditional oil and gas expertise, creating a unique hybrid market environment. The region's stringent environmental regulations and focus on carbon reduction are shaping project designs and execution strategies.

Oil & Gas EPC Market in Middle East & Africa

The Middle East & Africa region represents a crucial market for oil and gas EPC projects, driven by substantial investments in both upstream and downstream sectors. Saudi Arabia and the United Arab Emirates lead the market with ambitious expansion plans and infrastructure development projects. The region's market is characterized by large-scale integrated projects that combine upstream production facilities with downstream processing capabilities. National oil companies play a pivotal role in driving market growth through strategic partnerships with international EPC contractors. The market benefits from the region's established oil and gas infrastructure market and continued investment in capacity expansion. African countries are emerging as significant growth markets, particularly in LNG infrastructure development and offshore projects, adding diversity to the regional market landscape.

Oil & Gas EPC Market in South America

South America's oil and gas EPC market is experiencing significant transformation, primarily driven by Brazil's offshore developments and Argentina's shale gas potential. The region's market is characterized by a strong focus on deepwater projects, particularly in Brazil's pre-salt areas, which offer competitive advantages due to lower breakeven prices. The market benefits from increasing investment in natural gas infrastructure and LNG facilities across multiple countries. Regional national oil companies are actively pursuing partnerships with international EPC contractors to access advanced technologies and project management expertise. The market is witnessing a gradual shift towards integrated project delivery models, combining traditional EPC services with innovative financing solutions. Emerging players like Guyana are adding new dimensions to the market with significant offshore discoveries and development projects.

Competitive Landscape

Top Companies in Oil & Gas EPC Market

The global oil and gas EPC companies market features prominent players including Samsung Engineering, Korea Shipbuilding & Offshore Engineering, Hyundai Engineering & Construction, John Wood Group, TechnipFMC, Bechtel Corporation, Saipem, McDermott International, KBR Inc., and Fluor Corporation. These oil and gas EPC companies are increasingly focusing on technological innovation through digital transformation initiatives like cloud-based construction management systems and automated welding solutions. Strategic partnerships and joint ventures, particularly in emerging markets, have become crucial for expanding geographic footprints and securing major projects. Companies are adopting modular construction approaches and standardized design processes to improve efficiency and reduce project timelines. The industry is witnessing a shift towards sustainability-focused solutions, with many players developing capabilities in carbon capture, renewable fuels, and green chemical projects alongside traditional oil and gas infrastructure.

Market Consolidation Drives Industry Evolution Pattern

The oil and gas EPC market structure is characterized by a mix of global engineering conglomerates and specialized regional players, with international firms dominating large-scale projects while local companies focus on specific geographic markets or specialized services. The industry is moving toward consolidation, with Western firms facing increasing competition from Asian companies that typically focus on lump-sum contracts and competitive pricing strategies. Market dynamics are shaped by strategic alliances between international and local players, particularly in key markets like the Middle East, where national content requirements drive partnership formation.

The market has witnessed significant merger and acquisition activity, exemplified by numerous strategic agreements and joint ventures, particularly in emerging markets. Companies are forming partnerships to enhance their technical capabilities, expand geographic reach, and strengthen their competitive position in specific market segments. These collaborations often involve technology transfer, local workforce development, and shared project execution responsibilities, creating integrated service offerings that combine global expertise with local market knowledge.

Innovation and Flexibility Key to Success

Success in the oil and gas EPC market increasingly depends on companies' ability to adapt to changing market conditions and evolving client requirements. Firms must develop comprehensive digital capabilities, including advanced oil and gas project management tools and automation technologies, while maintaining cost competitiveness. The ability to offer integrated solutions across the entire project lifecycle, from front-end engineering to maintenance services, has become crucial for maintaining market position. Companies need to balance their portfolio between traditional oil and gas projects and emerging energy transition opportunities, while building expertise in environmental compliance and sustainable project execution.

Market players must focus on developing flexible execution models that can accommodate varying project scales and complexity levels. This includes building strong supplier networks, maintaining efficient resource allocation systems, and developing standardized processes that can be adapted to different regional requirements. The increasing focus on local content requirements and environmental regulations necessitates strong relationships with local partners and investment in sustainable technologies. Companies must also maintain robust risk management frameworks to handle the cyclical nature of the industry and potential geopolitical challenges, while ensuring compliance with evolving regulatory standards across different markets.

Oil & Gas EPC Industry Leaders

Saipem SpA

TechnipFmc PLC

Fluor Corporation

Bechtel Corporation

Petrofac Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2023: QatarEnergy announced the award of the engineering, procurement, and construction (EPC) contract for the North Field South (NFS) project, which comprises two LNG mega trains with a combined capacity of 16 million tons per annum (MTPA). NFS, jointly with the North Field East (NFE) project, will expand Qatar’s LNG production capacity from the current 77 MTPA to 126 MTPA. QatarEnergy maintains a 75% interest in the NFS project and has already signed partnership agreements with TotalEnergies, Shell, and ConocoPhillips for the remaining 25%.

- July 2022: Saipem SpA was awarded several onshore and offshore contracts worth approximately USD 1.25 billion in the Middle East. The first group of contracts involves extending onshore drilling contracts in the Middle East for roughly USD 600 million. Another four new contracts in the region contain the EPC and installation of several offshore jackets, decks, subsea pipelines, subsea composite cables, umbilicals, fiber optic cables, and brownfield modifications. The combined value of these contracts is worth USD 650 million.

Global Oil & Gas EPC Market Report Scope

The oil and gas engineering, procurement, and construction (EPC) market comprises contract-based projects, including the engineering, procurement, and construction activities for upstream, midstream, and downstream oil and gas industries. Some of the EPC activities include design, fabrication, construction, installation, equipment production, pre-commissioning, and maintenance services involved at various stages of operations, right from the exploration and production of oil and gas and transporting the produced product to the refining and distribution activities.

The oil and gas EPC market is segmented by sector and geography. By sector, the market is segmented into upstream, midstream, and downstream. The report also covers the market size and forecasts for the oil and gas EPC market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

Sector

| Upstream |

| Downstream |

| Midstream |

Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| Sector | Upstream | |

| Downstream | ||

| Midstream | ||

| Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}) | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Oil & Gas EPC Market?

The Oil & Gas EPC Market size is expected to reach USD 478.66 billion in 2025 and grow at a CAGR of 4.76% to reach USD 603.95 billion by 2030.

What is the current Oil & Gas EPC Market size?

In 2025, the Oil & Gas EPC Market size is expected to reach USD 478.66 billion.

Who are the key players in Oil & Gas EPC Market?

Saipem SpA, TechnipFmc PLC, Fluor Corporation, Bechtel Corporation and Petrofac Limited are the major companies operating in the Oil & Gas EPC Market.

Which is the fastest growing region in Oil & Gas EPC Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Oil & Gas EPC Market?

In 2025, the Asia-Pacific accounts for the largest market share in Oil & Gas EPC Market.

What years does this Oil & Gas EPC Market cover, and what was the market size in 2024?

In 2024, the Oil & Gas EPC Market size was estimated at USD 455.88 billion. The report covers the Oil & Gas EPC Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Oil & Gas EPC Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: