Middle East and North Africa Oilfield Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

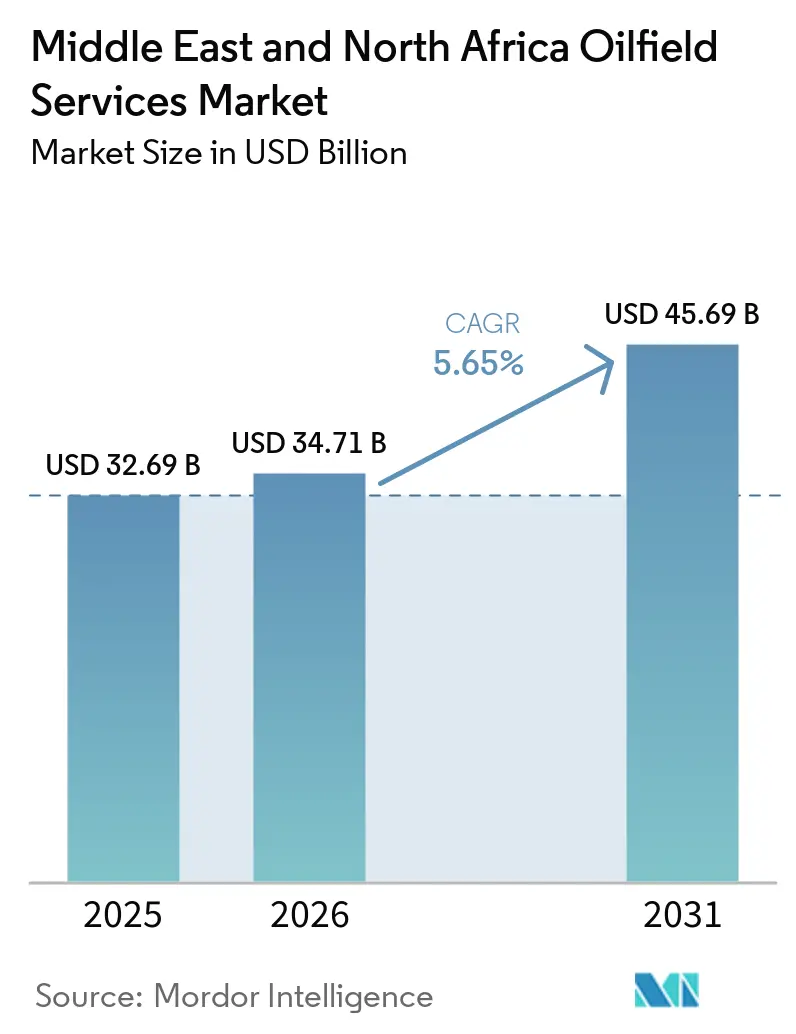

| Base Year Market Size (2025) | USD 32.69 Billion |

| Market Size (2026) | USD 34.71 Billion |

| Market Size (2031) | USD 45.69 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

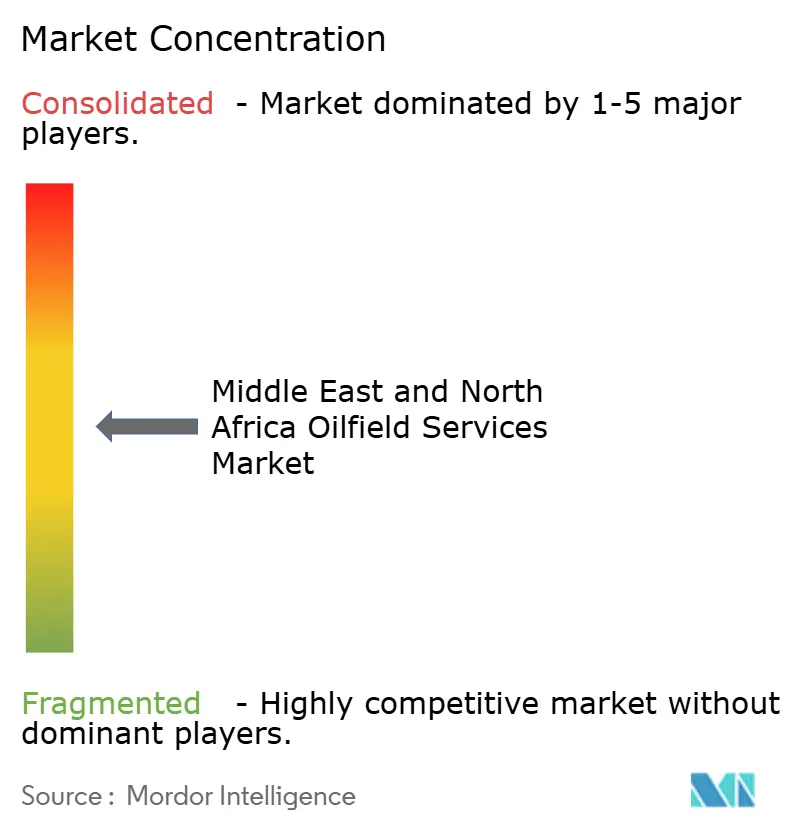

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and North Africa Oilfield Services Market Analysis by Mordor Intelligence

The Middle East and North Africa Oilfield Services Market size was valued at USD 32.69 billion in 2025 and is estimated to grow from USD 34.71 billion in 2026 to reach USD 45.69 billion by 2031, at a CAGR of 5.65% during the forecast period (2026-2031). The region’s growth is anchored in a structural pivot toward gas monetization, expansive unconventional programs, and localization mandates that funnel spending into domestic supply chains. Saudi Arabia’s Jafurah tight-gas project, Qatar’s North Field West LNG expansion, and Egypt’s aggressive exploration agenda collectively underpin a multi-year backlog for drilling, completion, and production support. National oil companies set localization thresholds above 70%, compelling global contractors to establish in-region plants and training centers or accept reduced tender scores.[1]Saudi Aramco, “Jafurah Gas Field,” ARAMCO.COM Digital-oilfield adoption is accelerating, with ADNOC installing AI-enabled sensors on 2,000 wells to trim non-productive time by 15%.[2]ADNOC, “In-Country Value Program,” ADNOC.AE At the same time, OPEC+ quota discipline, headline price swings, and an aging workforce temper near-term spending, creating a market that rewards contractors able to blend cost efficiency with local content and advanced technology.

Key Report Takeaways

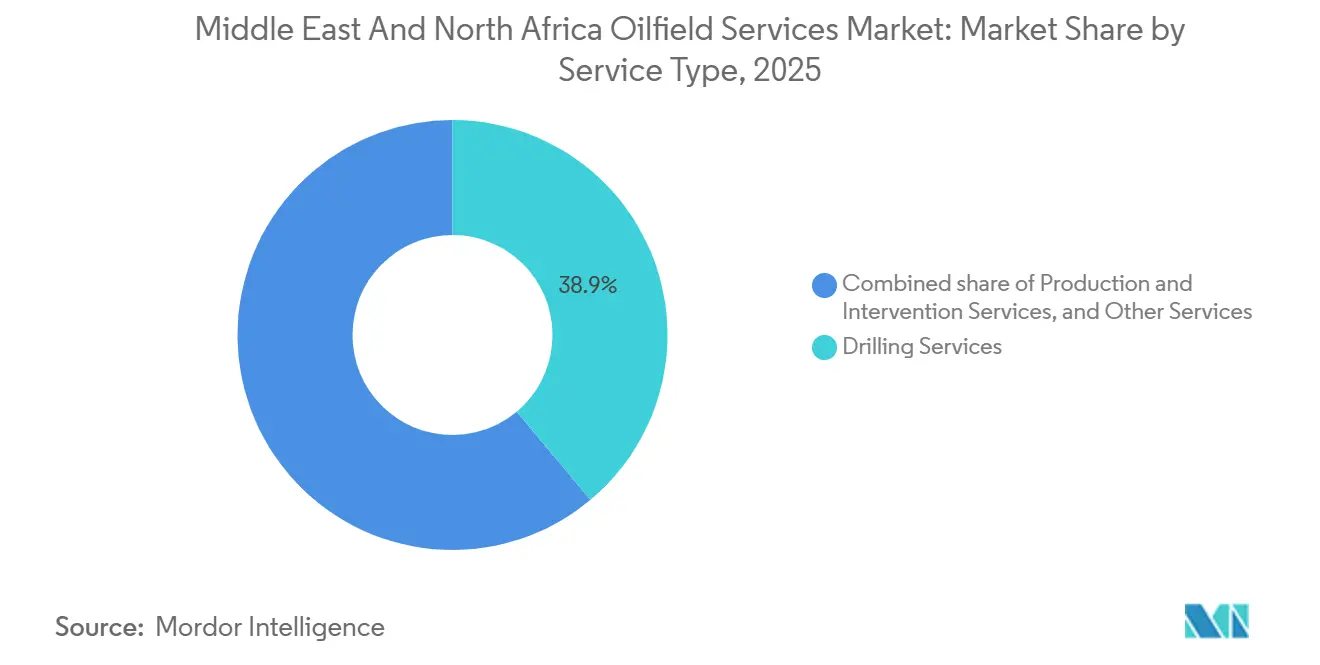

- By service type, drilling services led with 38.9% of the Middle East & North Africa oilfield services market share in 2025, while production and intervention services are projected to expand at a 7.7% CAGR through 2031.

- By location, onshore operations accounted for 81.1% of 2025 revenue, whereas offshore services are forecast to grow at a 9.6% CAGR through 2031.

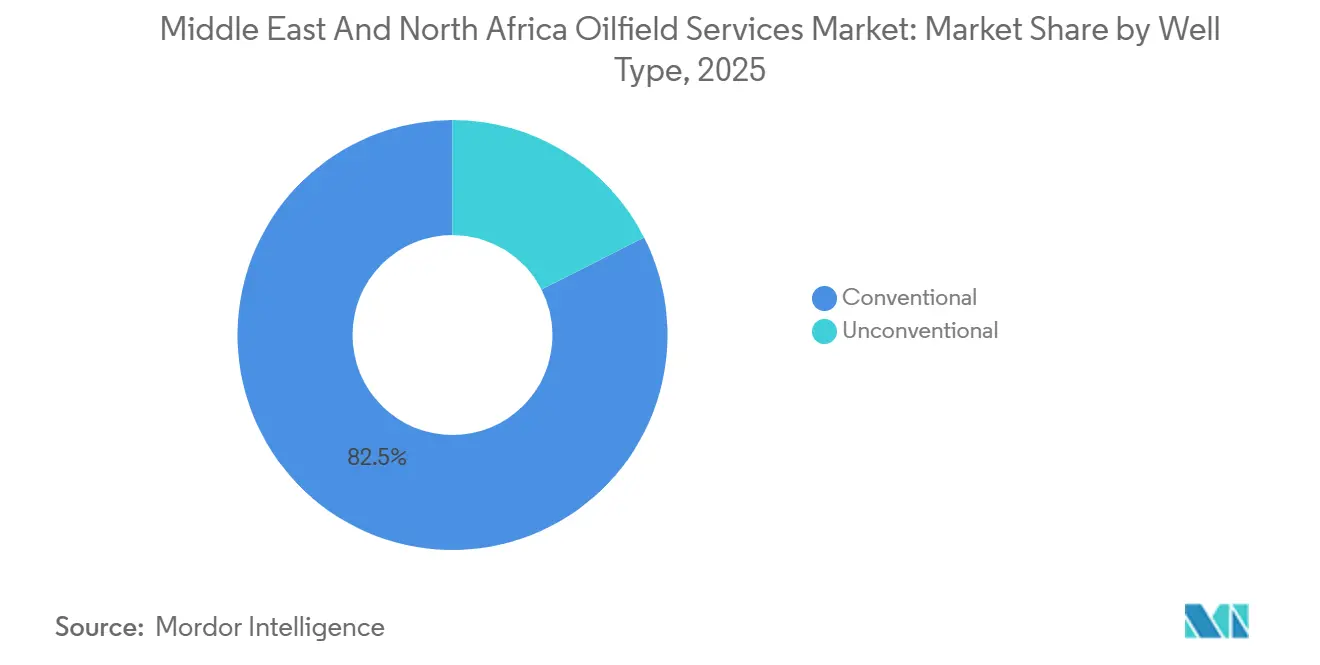

- By well type, conventional wells held 82.5% of 2025 revenue, but unconventional wells are expected to rise at an 8.3% CAGR to 2031.

- By geography, Saudi Arabia held 30.1% of 2025 revenue, while Egypt is set to advance at 7.9% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and North Africa Oilfield Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising drilling activity backed by USD 143 billion E&P budgets through 2030 | +1.2% | Saudi Arabia, UAE, Qatar, Kuwait | Medium term (2-4 years) |

| Accelerated gas-focused megaprojects (Jafurah, North Field) | +1.5% | Saudi Arabia, Qatar, spillover to Oman and Bahrain | Long term (≥4 years) |

| National oil companies’ localization mandates boosting service tenders | +0.8% | Saudi Arabia, UAE, Qatar, Kuwait, Algeria | Medium term (2-4 years) |

| Digital-oilfield adoption (AI rigs, real-time reservoirs) | +1.0% | UAE, Saudi Arabia, Kuwait, expanding to Egypt and Algeria | Short term (≤2 years) |

| Ultra-deep HP/HT discoveries demanding high-spec services | +0.7% | UAE offshore, Saudi Arabia Eastern Province, Kuwait | Medium term (2-4 years) |

| Early carbon-capture and hydrogen pilots creating niche service demand | +0.4% | Saudi Arabia (Jubail, Shaybah), UAE (Hail & Ghasha) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Drilling Activity Backed by USD 143 Billion E&P Budgets Through 2030

Regional exploration and production budgets of USD 143 billion for 2025-2030 underpin a land-rig count that the International Energy Agency expects to climb 31% over the prior five-year span.[3]International Energy Agency, “Middle East Energy Outlook 2025,” IEA.ORG Saudi Aramco alone committed USD 7 billion in 2025 to keep 680 rigs active, accentuating the Middle East & North Africa oilfield services market’s dependence on sustained drilling intensity.[4]Saudi Aramco, “Jafurah Gas Field,” ARAMCO.COM Algeria earmarked USD 60 billion for 1,450 wells targeting tight-gas prospects, extending service demand into North Africa. Kuwait is channeling USD 3.9 billion into offshore Phase 2 exploration to unlock 4.5 billion BOE and add 150,000 bpd by 2035. High-pressure, high-temperature zones, where a single well can cost over USD 20 million, amplify requirements for premium drillstrings, mud-logging, and managed-pressure drilling systems. These allocations reinforce a multi-year backlog across the Middle East & North Africa oilfield services market, incentivizing contractors to expand fleets and local workshops.

Accelerated Gas-Focused Megaprojects (Jafurah, North Field)

Saudi Aramco’s USD 100 billion Jafurah program targets 2 bcf/d of sales gas by 2030, necessitating continuous horizontal drilling and intensive multi-stage fracturing. Schlumberger captured a multi-billion-dollar five-year stimulation contract that redefines completion-service intensity in the Middle East & North Africa oilfield services market. Qatar’s North Field East and West phases will lift LNG capacity to 142 mtpa by 2030, creating long-cycle subsea-tree, pipeline, and accommodation-vessel demand. Awards to TechnipFMC, Saipem, and Chinese yards secure fabrication slots yet concentrate schedule risk: delays in gas-processing trains can idle rigs and spread cost overruns across the service chain. These megaprojects anchor the Middle East & North Africa oilfield services market size outlook, but they also heighten exposure to commissioning milestones.

National Oil Companies’ Localization Mandates Boosting Service Tenders

Saudi Aramco’s iktva program achieved a 70% localization rate in 2025, channeling USD 280 billion into the domestic economy and setting a 75% target for 2030. ADNOC’s In-Country Value framework scores bids on Emirati content, training, and technology transfer, effectively gating contract awards. Algeria and Egypt mirror these rules, forcing international firms in the Middle East & North Africa oilfield services market to establish fabrication yards and joint ventures or face 200- to 300-basis-point margin compression. Early movers secure preferential tender access and lower logistics costs, whereas late entrants endure extended approval cycles. The mandate dynamic embeds localization spend as a structural growth vector within the Middle East & North Africa oilfield services market.

Digital-Oilfield Adoption (AI Rigs, Real-Time Reservoirs)

ADNOC awarded a USD 920 million contract to outfit 2,000 wells with AI sensors, digital twins, and predictive-maintenance platforms, targeting a 15% drop in non-productive time. Kuwait Oil Company integrated big-data analytics and automated drilling controls, cutting well-delivery cycles by roughly 10%. Halliburton’s DeepQuest HT suite, rated to 375 °F and 21,000 psi, feeds real-time data to cloud models that update drilling parameters every 30 seconds. Gulf Cooperation Council operators spearhead adoption thanks to capital depth, yet Algeria and Egypt are piloting similar platforms to replicate efficiency gains. A looming talent gap 48% of the workforce is 45 or older, slowing scaling and elevating demand for training services. Overall, digitalization augments the Middle East & North Africa oilfield services market by blending data analytics with legacy rig fleets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-price volatility and OPEC+ production quotas | −0.9% | Saudi Arabia, UAE, Kuwait, Iraq, Algeria, Libya | Short term (≤2 years) |

| Geopolitical flashpoints and sanctions risk | −0.6% | Libya, Algeria, Iraq, spillover to Egypt and Lebanon | Medium term (2-4 years) |

| Local-content rules squeezing foreign firms’ margins | −0.4% | Saudi Arabia, UAE, Qatar, Kuwait, Algeria | Medium term (2-4 years) |

| Critical talent shortage for next-gen digital rigs | −0.5% | Region-wide, acute in UAE, Saudi Arabia, Kuwait | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Oil-Price Volatility and OPEC+ Production Quotas

OPEC+ carried 3.24 million bpd of cuts into 2026, adding only a 206,000 bpd uptick for April. Brent traded between USD 70 and USD 85 per barrel in Q1 2026, a band that supports maintenance capital but discourages ultra-deepwater or tight-oil exploration in high-cost areas. Quota discipline presses member states to prioritize value over volume, postponing marginal field final-investment decisions and dampening short-cycle rig demand. Service companies with fixed-rate fleet contracts shoulder utilization swings, whereas those with performance-linked pricing secure partial downside protection. The constraint subtracts up to 0.9 percentage points from the regional growth trajectory of the Middle East & North Africa oilfield services market.

Geopolitical Flashpoints and Sanctions Risk

Libya’s 2025 licensing round saw only 5 of 22 blocks awarded amid governance fragmentation, underscoring execution risk in politically volatile zones. TotalEnergies and ConocoPhillips pledged USD 20 billion to lift Libyan output to 2 million bpd by 2030, but the plan hinges on long-term stability. Algeria’s framework mandating Sonatrach majority stakes deters some Western operators, narrowing the pool of service bidders. U.S. and EU sanctions on specific Syrian and Iranian entities require meticulous compliance vetting, extending tender cycles. These uncertainties subtract roughly 0.6 percentage points from forecast CAGR and bifurcate the Middle East & North Africa oilfield services market between incumbents with deep local ties and newcomers facing elevated barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Completion Spend Accelerates While Drilling Holds Scale

Drilling services retained 38.9% of the Middle East and North Africa oilfield services market share in 2025, driven by Saudi Aramco’s land-rig fleet expansion and Qatar’s offshore appraisal campaigns. Yet production and intervention services are forecast to grow at 7.7% annually, reflecting artificial-lift retrofits, coiled-tubing jobs, and real-time surveillance across maturing assets. The Middle East & North Africa oilfield services market size for stimulation contracts is rising as Jafurah alone will require 1,000 horizontal wells by 2030, each demanding multi-stage fracturing and proppant logistics. Western majors capture high-tech completion scopes, while regional contractors compete on commodity cementing and wellhead fabrication. Other services, seismic, marine logistics, aviation, and nascent decommissioning, round out revenue, buoyed by Egypt’s 101 exploration wells in 2026 and Algeria’s 24-block bid round.

Parallel competitive dynamics shape pricing: performance-based completion contracts in unconventional plays fetch premiums, whereas drilling day-rates remain range-bound by OPEC+ quota uncertainty. High-pressure, high-temperature projects off the UAE and Kuwait’s Mutriba field require specialized drilling fluids and downhole tools, allowing suppliers to command higher margins. In contrast, mid-depth land wells across North Africa stay cost-focused, favoring contractors with localized supply chains. Over 2026-2031, the Middle East & North Africa oilfield services market sees the fastest percentage growth in production and intervention, but drilling retains the largest absolute revenue pool, reflecting the region’s sheer rig intensity.

By Location: Offshore Momentum Outpaces Onshore Dominance

Onshore activity contributed 81.1% of 2025 revenue, anchored by Ghawar, Burgan, and Hassi Messaoud, yet offshore services are projected to grow at 9.6%, the highest location-based rate in the Middle East and North Africa oilfield services market. ADNOC Drilling’s USD 1.15 billion, 15-year jack-up deal and Saudi Aramco’s Marjan and Berri campaigns exemplify a shift toward long-tenure rig contracts that ensure capacity amid tight global supply. Egypt’s ultra-deep Mediterranean prospects and Oman’s Yumna Field jack-up award broaden offshore geography, creating fresh demand for subsea trees, riser inspection, and remotely operated vehicles.

Nevertheless, onshore unconventional projects Jafurah, Al Dhafra, and Kuwait’s Jurassic sequence continue to scale, sustaining the largest share of the Middle East and North Africa oilfield services market size. Land-rig contractors benefit from multi-pad campaigns that lower move costs and standardize well designs. Service differentiation tilts toward drilling automation and advanced mud systems to handle high-pressure, high-temperature zones. Ultimately, offshore delivers superior growth percentages, but onshore retains volume leadership given regional geology and infrastructure maturity.

By Well Type: Unconventional Wells Capture Growth Premium

Unconventional wells are forecast to grow at 8.3% to 2031, eclipsing conventional growth in the Middle East and North Africa oilfield services market. Jafurah’s December 2025 first gas unlocked 229 tcf of reserves, catalyzing a five-year hydraulic-fracturing blitz led by Schlumberger. The UAE’s Block 3 holds an estimated 220 billion barrels of oil-in-place, with EOG Resources piloting North American fracturing playbooks. Kuwait’s Mutriba HP/HT award and Algeria’s Illizi South tight-gas pilot extend unconventional demand beyond the Gulf heartland.

Conventional wells still command 82.5% revenue, but reservoir maturity drives a pivot to enhanced oil recovery and infill drilling rather than greenfield expansion. OPEC+ caps force operators to optimize barrels per well rather than add volume, heightening interest in downhole sensing, artificial lift, and water-shutoff chemistries. The Middle East and North Africa oilfield services market size is tied to conventional wells, thus grows more slowly, while unconventional projects absorb incremental service intensity and specialized technology, widening the value differential.

Geography Analysis

Saudi Arabia’s 30.1% share of 2025 revenue is rooted in Aramco’s scale: Jafurah alone will deploy over 50 land rigs by 2030, and the Tanajib plant reached 2.6 bcf/d of capacity in 2026. Offshore jack-ups at Marjan and Berri sustain plateau production, while the Jubail carbon-capture hub targets 9 mtpa by 2027, opening CO₂ compression and injection niches. Egypt, forecast to grow at 7.9%, is exploration-led: 101 wells planned for 2026, USD 13 billion in Eni-BP commitments, and Western Desert finds such as SKAL-1X accelerate seismic and drilling demand. The West Meina project aims for 160 mmcfd by end-2026, underscoring production upside.

The United Arab Emirates balances LNG megaprojects with unconventional pilots. ADNOC’s Ruwais LNG plant achieved 9.6 mtpa, and the USD 920 million digital-well initiative embeds AI across its portfolio. Qatar’s North Field West boosts capacity by 16 mtpa, triggering a cascade of subsea and fabrication awards. Kuwait channels USD 3.9 billion into exploration through 2030 while tackling HP/HT Mutriba development. Algeria’s 24-block round and USD 60 billion spend demonstrate intent but face water scarcity and logistical headwinds. Libya offers high-reward upside if political stability materializes. Morocco remains a frontier, where success in Guercif could reduce LNG imports.

Overall, Gulf Cooperation Council states dominate absolute spend, but North African growth rates outpace the Gulf as new acreage opens and international majors diversify exposure. This geographic mosaic diversifies revenue streams across the Middle East & North Africa oilfield services market, mitigating single-country risk for diversified contractors.

Competitive Landscape

The market is moderately concentrated. Schlumberger, Halliburton, and Baker Hughes are top players leveraging integrated portfolios that span drilling to digital, giving them scale advantages in the Middle East & North Africa oilfield services market. Schlumberger’s multi-billion-dollar Jafurah stimulation contract and Halliburton’s DeepQuest HT launch showcase technology depth. ADNOC Drilling’s USD 1.15 billion jack-up award signals national oil companies’ preference for 10-15-year accords that lock in rigs and shift utilization risk. Regional challengers National Energy Services Reunited, Arabian Drilling, and Shelf Drilling capitalize on local content, Arabic engineering support, and faster mobilization, eroding day-rate premiums enjoyed by Western majors.

Chinese state-backed players, including COSL and Seatrium-design rigs, gain share via tied financing and cost-competitive bids in Qatar and Algeria. White-space exists in carbon-capture infrastructure, decommissioning, and data analytics platforms. Saudi Aramco’s Jubail hub needs specialized CO₂ services, while aging Gulf platforms will require plug-and-abandonment expertise, areas where European and Southeast Asian contractors with North Sea heritage can outflank incumbents. Digital platforms that stitch real-time downhole data into reservoir models remain sparsely contested, offering margin headroom for software-heavy entrants.

Middle East and North Africa Oilfield Services Industry Leaders

Schlumberger Limited

Weatherford International PLC

Baker Hughes Company

Halliburton Company

Transocean Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Schlumberger won a USD 1.5 billion, five-year Mutriba HP/HT contract from Kuwait Oil Company.

- February 2026: Saudi Aramco commenced commercial production at Jafurah, unlocking 229 tcf of tight-gas reserves.

- January 2026: Masirah Oil hired the Energy Emerger jack-up for Oman’s Yumna Field, expanding offshore activity beyond the Gulf core.

- May 2025: ADNOC Drilling secured a USD 1.15 billion, 15-year jack-up contract, embedding performance incentives.

Middle East and North Africa Oilfield Services Market Report Scope

Oilfield services are defined as services provided by services associated with the oil and gas exploration and production processes, i.e., the upstream sector of the energy industry.

The Middle East and North Africa Oilfield Services Market is segmented into service type, location of deployment, well type, and geography. By service type, the market is segmented into drilling, completion, production, intervention, and other services. By location of deployment, the market is segmented into onshore and offshore. By well type, the market is segmented into conventional and unconventional wells. The report also covers the market size and forecasts for the oilfield services market across key countries in the Middle East and North Africa, including Saudi Arabia, the United Arab Emirates, Iran, Iraq, Egypt, Algeria, and other countries in the region. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Drilling Services |

| Completion Services (Cementing, Hydraulic Fracturing) |

| Production and Intervention Services |

| Other Services (OSV, seismic, decomm., aviation) |

| Onshore |

| Offshore |

| Conventional |

| Unconventional |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Algeria |

| Egypt |

| Libya |

| Morocco |

| Rest of Middle East and North Africa |

| By Service Type | Drilling Services |

| Completion Services (Cementing, Hydraulic Fracturing) | |

| Production and Intervention Services | |

| Other Services (OSV, seismic, decomm., aviation) | |

| By Location | Onshore |

| Offshore | |

| By Well Type | Conventional |

| Unconventional | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Algeria | |

| Egypt | |

| Libya | |

| Morocco | |

| Rest of Middle East and North Africa |

Key Questions Answered in the Report

How large will the Middle East & North Africa oilfield services market be by 2031?

The market is projected to reach USD 45.69 billion by 2031, expanding at a 5.65% CAGR from 2026.

Which service segment is growing fastest in the region?

Production and intervention services are forecast to rise at 7.7% annually through 2031 on the back of artificial-lift upgrades and coiled-tubing programs.

What is driving offshore spending growth?

Long-term jack-up contracts in Saudi Arabia and ADNOC plus ultra-deepwater drilling off Egypt are pushing offshore services toward a 9.6% CAGR.

How significant are unconventional resources?

Unconventional wells, now 17.5% of revenue, are set to grow at 8.3% to 2031, spearheaded by Saudi Arabias Jafurah and the UAEs Al Dhafra pilots.

What risks could slow market growth?

OPEC+ production quotas, oil-price swings, and geopolitical instability in Libya and Algeria collectively trim up to 0.9 percentage points from projected CAGR.

How are localization rules reshaping competition?

Mandatory in-country value programs in Saudi Arabia and the UAE require ?70% local content, prompting foreign contractors to build regional plants or risk a 200-300 bps margin squeeze.

Page last updated on: