Kuwait Oilfield Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.38 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kuwait Oilfield Services Market Analysis by Mordor Intelligence

The Kuwait Oilfield Services Market size is estimated at USD 1.82 billion in 2026, and is expected to reach USD 2.38 billion by 2031, at a CAGR of 5.55% during the forecast period (2026-2031).

Sustained capital spending by Kuwait Petroleum Corporation (KPC), the pivot toward offshore prospects such as Al-Nokhatha and Dorra, and the adoption of digital well-construction platforms are widening the addressable service base. Drilling remains the revenue anchor, yet rigless production and intervention offerings are expanding faster as operators squeeze extra barrels from aging wells. Integrated Project Management (IPM) contracts are reshaping competition by bundling drilling, completion, and production optimization scopes under multi-year performance terms. Offshore demand is accelerating despite tight jack-up supply, while heavy-oil and tight-carbonate plays are stimulating uptake of thermal and fracturing technologies.

Key Report Takeaways

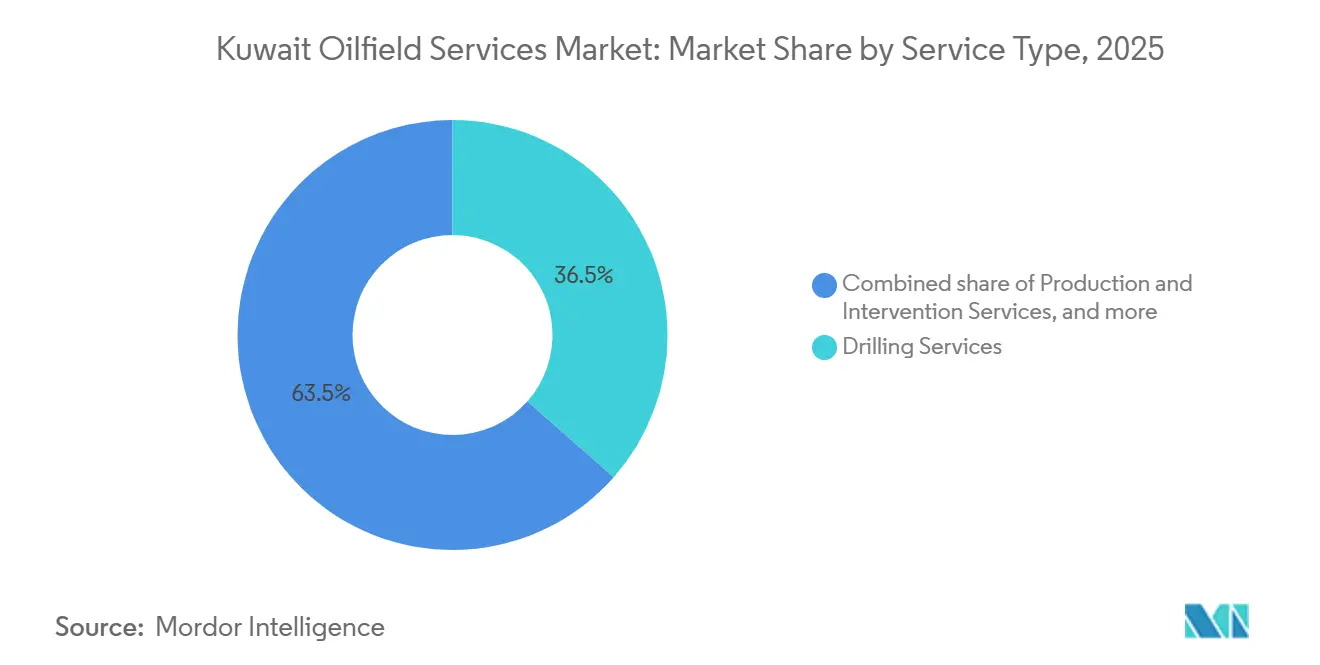

- By service type, drilling held 36.5% of the Kuwait oilfield services market share in 2025, whereas production and intervention services are forecast to post a 7.6% CAGR through 2031.

- By location, onshore commanded 80.1% of 2025 spending, while offshore is expected to advance at a 9.0% CAGR to 2031.

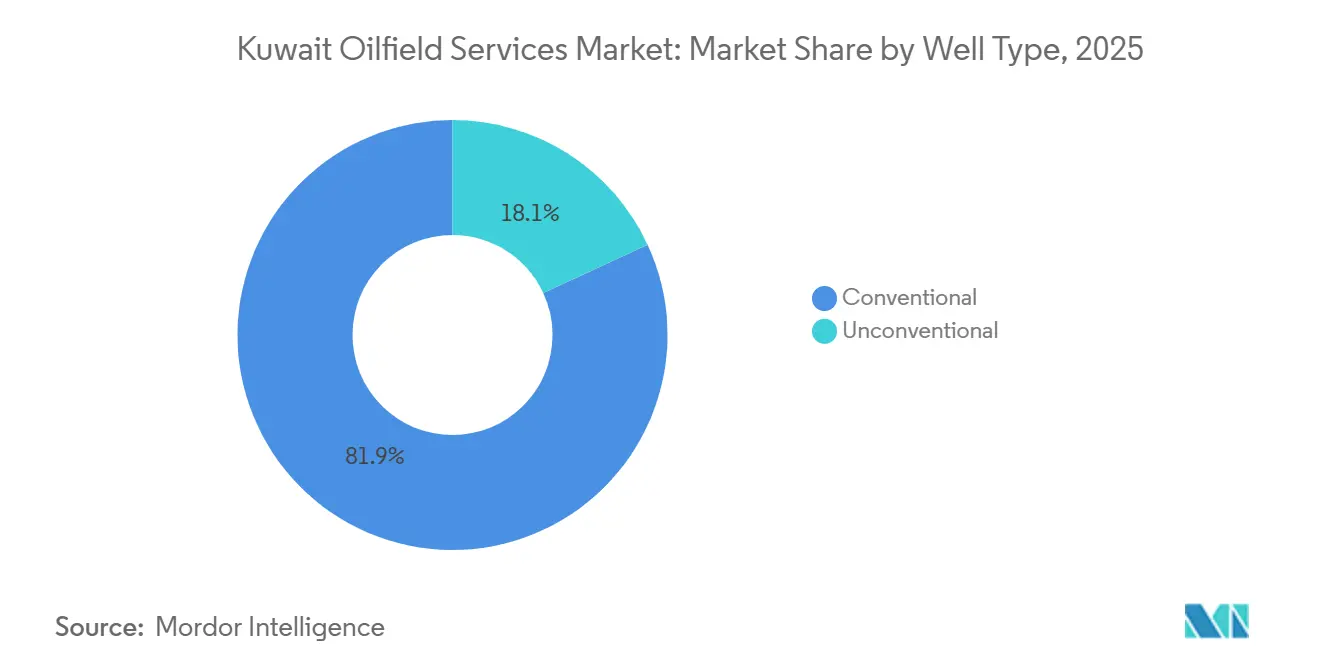

- By well type, conventional wells accounted for 81.9% of the Kuwait oilfield services market size in 2025, yet unconventional activity is projected to grow at an 8.3% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Kuwait Oilfield Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising investment in offshore projects | +1.2% | Al-Zour coast, Dorra sector | Medium term (2-4 years) |

| Accelerated infill drilling in mature fields | +1.5% | Greater Burgan, North Kuwait, Minagish | Long term (≥ 4 years) |

| Shift to Integrated Project Management | +0.9% | National | Medium term (2-4 years) |

| NOC-IOC partnership model | +1.0% | Heavy-oil South Ratqa, offshore gas-condensate plays | Long term (≥ 4 years) |

| Digital well-construction initiatives | +0.7% | North Kuwait, Burgan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Investment in Offshore Projects

KPC finished six offshore exploration wells by mid-2025 and plans 18 more, diversifying beyond its onshore core.[1]Zawya News Desk, “Al-Nokhatha and Al-Julaiah discoveries boost offshore plans,” zawya.com The July 2024 Al-Nokhatha find added roughly 1.5 billion boe, the January 2025 Al-Julaiah discovery contributed about 800 million boe, and the Jazza-1 test delivered over 29 MMscf/d plus 5,000 bpd of condensate. Kuwaiti and Saudi partners aim to bring Dorra onstream at 1 Bcf/d of gas and 84,000 bpd of condensate following December 2025 site approval in Al-Zour. Offshore demand now spans jack-up drilling, subsea positioning, and marine logistics, and will ease once Saudi Arabia releases nearly 27 jack-ups in 2026. The new marine frontier broadens the Kuwait oilfield services market by introducing activities that traditional onshore contractors rarely provide.

Accelerated Infill Drilling to Stem Mature-Field Decline

Greater Burgan slipped from 1.7 million bpd in 2005 to 1.3 million bpd in the 2020s, with a natural decline near 6% a year.[2]Zawya News Desk, “Al-Nokhatha and Al-Julaiah discoveries boost offshore plans,” zawya.com Kuwait Oil Company (KOC) counters this with continuous infill wells and rigless interventions. A structured workflow across 600 Sabria wells lifted output by 20% over three years through iterative water-shutoff, stimulation, and artificial-lift upgrades.[3]Schlumberger, “Integrated production optimization workflow lifts output in mature field,” slb.com Nine five-year drilling contracts awarded in July 2024 to local firms add 550-hp rigs focused on heavy-oil zones, generating local jobs and fleet depth. High-density full-azimuth seismic is now KOC’s standard for pinpointing bypassed pay, ensuring drilling activity continues even as production services accelerate.

Shift to Integrated Project Management Contracts

KOC is moving from discrete service awards to IPM frameworks that fold engineering, drilling, completion, and production optimization into single agreements. Technip Energies landed a EUR 250-500 million consultancy in 2024, and KBR secured FEED for the South Ratqa heavy-oil project targeting 60,000 bpd by 2030. Petrofac followed with a USD 4 billion heavy-oil award in January 2025, despite balance-sheet stress. IPM shifts more performance risk onto contractors, rewarding those able to blend subsurface insight, automation, and supply-chain muscle. Smaller local firms are adapting by teaming up or focusing on niche scopes such as workover rigs or wellsite logistics.

Digital Well-Construction Initiatives

Halliburton achieved Kuwait’s first fully automated directional run in the Bahra Field in 2025, cutting drilling time by 30% with zero engineer intervention using LOGIX automation and PulseStar telemetry. Schlumberger’s KwIDF program applies fiber-optic DAS and edge analytics to diagnose inflow control device failures, guiding coiled-tubing fixes that more than doubled well output in Minagish and Sabriyah. Baker Hughes’ December 2025 ESP contract integrates FusionPro drives and Leucipa real-time analytics to predict failures and trim downtime. Weatherford runs Real-Time Decision Centers, overseeing drilling and completions remotely. Although digital uptake is uneven, early adopters are demonstrating material cost savings and higher initial production rates.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher breakeven for deep HP/HT prospects | -0.8% | National, with concentration in deep Jurassic and offshore prospects | Medium term (2-4 years) |

| Renewable-energy targets dampening long-term demand | -0.5% | National, influenced by Shagaya solar and wind projects | Long term (≥ 4 years) |

| Shortage of high-spec offshore rigs in regional fleet | -0.4% | National offshore zones (Dorra, Al-Nokhatha, Al-Julaiah, Jazza sectors) with spillover from GCC regional constraints | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Breakeven for Deep HP/HT Prospects

While onshore wells break even near USD 40-50/bbl, deep Jurassic and offshore HP/HT prospects need USD 60-80/bbl due to specialized drilling fluids, high-spec casing, and long rig cycles. Middle East jack-up day rates averaged USD 80,000-100,000 in 2024-2025, inflating well costs and forcing schedule trade-offs. Even though KPC budgets USD 9-10 billion annually through 2030, capital will favor quicker-payback infill work when prices soften. Service firms are mitigating cost pressure through tailored bits, performance-based IPM models, and closer integration of drilling and completion data, yet the structural premium for HP/HT wells persists.

Renewable-Energy Targets Dampening Long-Term Demand

Kuwait aims for 15% renewables in the power mix by 2030, anchored by Shagaya solar and wind farms. Displacing 20% of the 400,000 bpd currently burned for power could free 80,000 bpd for export, trimming the urgency for fresh drilling. Nevertheless, KPC’s goal of 4 million bpd by 2035 underscores that renewables are meant to raise export capacity, not curtail upstream spending. Even so, the policy injects uncertainty into long-dated HP/HT and deepwater projects, nudging service buyers toward flexible, modular contracts and intensifying competition for near-term, low-cost opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Drilling Dominates While Production Services Accelerate

Drilling contributed 36.5% of the Kuwait oilfield services market share in 2025, buoyed by constant infill wells in Greater Burgan and the offshore appraisal program.[4]Zawya Energy, “Shagaya renewables target 15% of mix by 2030,” zawya.com Production and intervention lines, however, are slated for a 7.6% CAGR through 2031 as operators lean on rigless techniques to restore flow without mobilizing full workover spreads. High-density seismic, automated drilling tools, and digital ESP platforms are lifting recovery from mature reservoirs. Meanwhile, premium cement and multistage fracturing jobs are gaining traction in tight carbonate and heavy-oil zones, widening the Kuwait oilfield services market size available to specialty contractors.

The growth in production services benefits providers of coiled-tubing cleanouts, electric submersible pumps, and digital well surveillance. A December 2025 award saw Baker Hughes integrate FusionPro drives with Leucipa analytics across multiple fields, anchoring a multi-year revenue stream. Schlumberger’s digital-slickline-conveyed straddle system restored 800 bpd in a single well while bypassing a 60-day rig workover. Such case studies underline why the segment’s growth outpaces the broader Kuwait oilfield services market.

By Location: Onshore Base Meets Offshore Upswing

Onshore work accounted for 80.1% of 2025 spending, reflecting the dominance of Greater Burgan, North Kuwait heavy-oil sites, and West Kuwait assets that together produce above 2.4 million bpd. Continuous infill drilling, water injection, and artificial-lift optimization keep this base steady. Weatherford’s joint venture operates eight rigs onshore, while Halliburton’s 2025 fully automated run in Bahra highlights the push for efficiency.

Offshore activity, though smaller, is projected to clock a 9.0% CAGR until 2031, fueled by Dorra, Al-Nokhatha, Al-Julaiah, and Jazza. Kuwait Municipal Council’s December 2025 nod for Dorra infrastructure in Al-Zour removes a critical hurdle, and KOC plans 18 further wells. Marine demand spans anchor-handling tugs, subsea positioning, and uncrewed survey vessels supplied by GAC Marine and Fugro, expanding the Kuwait oilfield services market size beyond its traditional onshore core.

By Well Type: Conventional Base, Unconventional Pivot

Conventional wells made up 81.9% of 2025 activity, sustaining the bulk of current output with rotary steerable drilling, ICD completions, and ESP maturation programs. Smart multilateral designs in West Kuwait combine inflow control valves with downhole gauges to tame water-cut issues in highly permeable reservoirs.

Unconventional development, heavy oil at South Ratqa and tight carbonates in Bahra, is forecast to rise at an 8.3% CAGR through 2031. Thermal recovery, multistage fracturing, and sand-management technologies dominate the spend. KBR’s FEED assignment and Petrofac’s USD 4 billion heavy-oil award highlight the scale of forthcoming opportunities, underscoring why integrated contractors capable of bundling drilling, stimulation, artificial lift, and real-time optimization are poised to capture a growing share of the Kuwait oilfield services market.

Geography Analysis

Kuwait’s entire oilfield services activity unfolds within its borders, yet regional dynamics shape cost and availability. Onshore, Greater Burgan’s 6% annual decline forces continuous drilling and water-management projects, anchoring a large chunk of service demand. North Kuwait’s Lower Fars heavy-oil campaign leverages nine locally awarded drilling contracts to build domestic capacity, while West Kuwait fields deploy smart multilateral wells to counter early water breakthrough. These initiatives absorb rigs, fracturing spreads, and artificial-lift crews, sustaining the onshore portion of the Kuwait oilfield services market.

Offshore, Dorra’s bilateral alignment with Saudi Arabia, Al-Nokhatha’s 1.5 billion boe potential, and Al-Julaiah’s 800 million boe discovery collectively drive a 9.0% CAGR forecast for marine services. KOC shifted the Oriental Phoenix rig to the Jazza area and is shopping for additional jack-ups as Saudi supply loosens in 2026. Marine logistics firms such as GAC and subsea survey leaders like Fugro are lining up contracts for anchor handling, crew transfers, and GroundIQ geotechnical campaigns.

Regionally, Kuwait competes with GCC neighbors for rigs, vessels, and experienced crews, so utilization swings in Saudi or UAE projects ripple into Kuwaiti day rates. Evercore’s outlook for 2026 suggests jack-up availability will improve when Saudi lets 27 units go, potentially tempering cost inflation and widening the offshore component of the Kuwait oilfield services market.

Competitive Landscape

Innovation and Integration Key to Growth

International majors, Schlumberger, Halliburton, Baker Hughes, and Weatherford, dominate high-end drilling, completion, and digital optimization scopes. Their share is reinforced by KOC’s preference for IPM contracts that reward firms capable of delivering integrated solutions and outcome-based KPIs. Technip Energies and KBR have carved out engineering and project-management niches, while Petrofac’s recent wins demonstrate continued appetite for EPC-leaning contractors despite financial strain.

Local drillers such as Operational Energy, Kuwait Well Drilling, Emkan, Zenith Group, and Refineries Engineering gained ground after landing nine five-year heavy-oil rig contracts in July 2024, reflecting a policy push for domestic content. Niche specialists, including Fugro in geotechnical surveys and GAC in marine logistics, fill capability gaps in offshore programs, expanding the Kuwait oilfield services market roster beyond classic rig providers.

Technology differentiation is sharpening competition. Halliburton’s LOGIX automated drilling cut Bahra cycle time by 30%, Schlumberger’s ACTive fiber-optic diagnostics doubled output in selected wells, and Baker Hughes’ integrated ESP-analytics contract promises lower failure rates and longer run lives. Contractors that match technical depth with local partnerships are best placed to navigate Kuwait’s evolving procurement model and secure a lasting share of the Kuwait oilfield services market.

Kuwait Oilfield Services Industry Leaders

Kuwait Petroleum Corporation

Schlumberger Ltd.

Halliburton Company

Baker Hughes Co.

Weatherford International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Baker Hughes has been awarded a multi-year oilfield services contract by the Kuwait Oil Company (KOC). The agreement involves the supply of electrical submersible pumps (ESPs) and related services to enhance production in Kuwait's mature oil and gas fields.

- November 2025: Terra Drone Indonesia co-hosted a workshop in Kuwait focused on advanced non-destructive testing (NDT) using drone technology. The event highlighted the application of drones for inspecting oil and gas facilities, emphasizing their role in enhancing operational safety and efficiency.

- September 2025: China National Logging Corporation (CNLC) has secured a significant five-year oilfield services contract with Kuwait Oil Company (KOC). The contract includes well-logging, testing, and perforation services, which are essential for reservoir evaluation and productivity improvement.

- March 2025: Terra Drone Indonesia co-hosted a workshop in Kuwait focused on advanced non-destructive testing (NDT) using drone technology. The event highlighted the application of drones for inspecting oil and gas facilities, emphasizing their role in enhancing operational safety and efficiency.

Kuwait Oilfield Services Market Report Scope

Oilfield services (OFS) refer to all the services that support onshore and offshore oil and gas extraction and production processes. These include drilling and formation evaluation, well construction, and completion services.

Kuwait's oilfield services market is segmented by service type, location type, well type, and geography. The market is segmented by service type into drilling, completion, production, intervention services, and other services. By location of deployment, the market is segmented into onshore and offshore. By well type, the market is divided into conventional, unconventional. The market size and forecasts for each segment have been calculated based on USD.

| Drilling Services |

| Completion Services (Cementing, Hydraulic Fracturing) |

| Production and Intervention Services |

| Other Services (OSV, seismic, decomm., aviation) |

| Onshore |

| Offshore |

| Conventional |

| Unconventional |

| By Service Type | Drilling Services |

| Completion Services (Cementing, Hydraulic Fracturing) | |

| Production and Intervention Services | |

| Other Services (OSV, seismic, decomm., aviation) | |

| By Location | Onshore |

| Offshore | |

| By Well Type | Conventional |

| Unconventional |

Key Questions Answered in the Report

What is the expected value of the Kuwait oilfield services market in 2031?

It is forecast to reach USD 2.38 billion by 2031, reflecting a 5.55% CAGR during 2026-2031.

Which service line is growing fastest?

Production and intervention services are projected to expand at 7.6% CAGR through 2031 as operators favor rigless well work.

Why is offshore activity accelerating?

Large discoveries at Al-Nokhatha, Al-Julaiah, and the Dorra gas field are driving a 9.0% CAGR outlook for offshore services to 2031.

How does digital well construction benefit Kuwait?

Automation platforms like Halliburton LOGIX and Schlumberger KwIDF shorten drilling days, cut non-productive time, and raise initial production, boosting project economics.

What restraint could limit long-term growth?

Deep HP/HT wells demand USD 60-80/bbl breakeven prices, which may delay high-cost projects if oil prices soften.

Which unconventional play is most significant?

The South Ratqa heavy-oil project aims for 60,000 bpd by 2030, relying on steam injection and thermal recovery for development.

Page last updated on: