Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

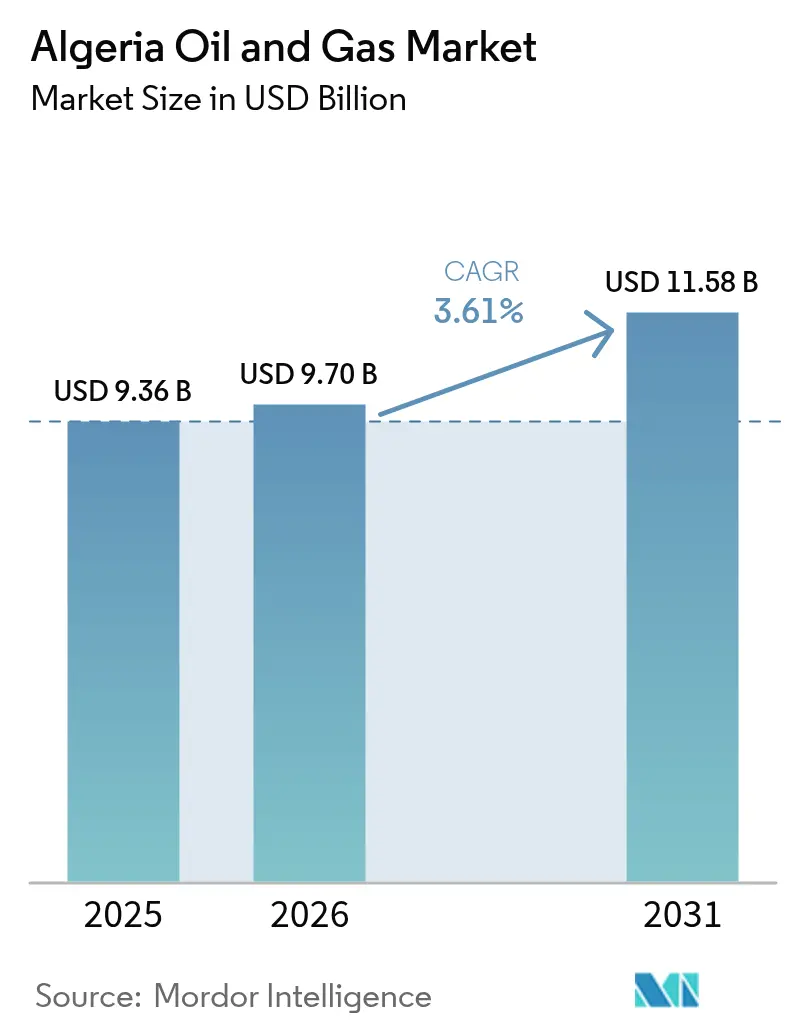

| Base Year Market Size (2025) | USD 9.36 Billion |

| Market Size (2026) | USD 9.7 Billion |

| Market Size (2031) | USD 11.58 Billion |

| Growth Rate (2026 - 2031) | 3.61% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algeria Oil And Gas Market Analysis by Mordor Intelligence

The Algeria Oil And Gas Market size was valued at USD 9.36 billion in 2025 and estimated to grow from USD 9.7 billion in 2026 to reach USD 11.58 billion by 2031, at a CAGR of 3.61% during the forecast period (2026-2031).

Strong upstream revenues, a pivot toward midstream upgrades, and fresh offshore prospects underpin this growth trajectory even as mature onshore reservoirs decline. Sustained investment stems from the 2019 Hydrocarbon Law, which aligns fiscal terms with investor expectations while preserving state oversight through Sonatrach. Domestic gas demand for power generation rises by 4–5% annually, squeezing export headroom; yet Algeria’s Mediterranean location still offers low-cost pipeline access to Europe. Capital-intensive offshore projects and decommissioning liabilities impact cash flows, but international technology partnerships enhance recovery rates and operational efficiency.

Key Report Takeaways

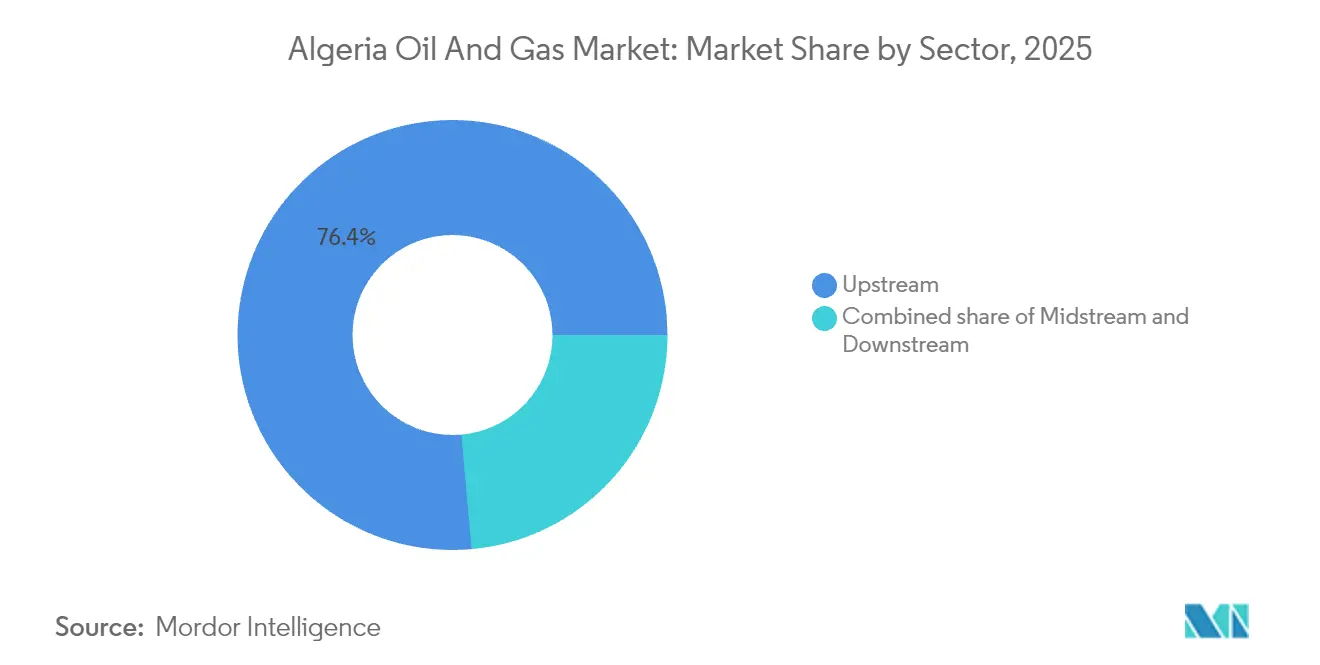

- By sector, upstream activities captured 76.42% of Algeria's oil and gas market share in 2025; midstream infrastructure is forecast to post a 9.46% CAGR through 2031.

- By location, offshore operations accounted for 88.35% of Algeria's oil and gas market size in 2025, while onshore developments are expected to grow at a 7.12% CAGR by 2031.

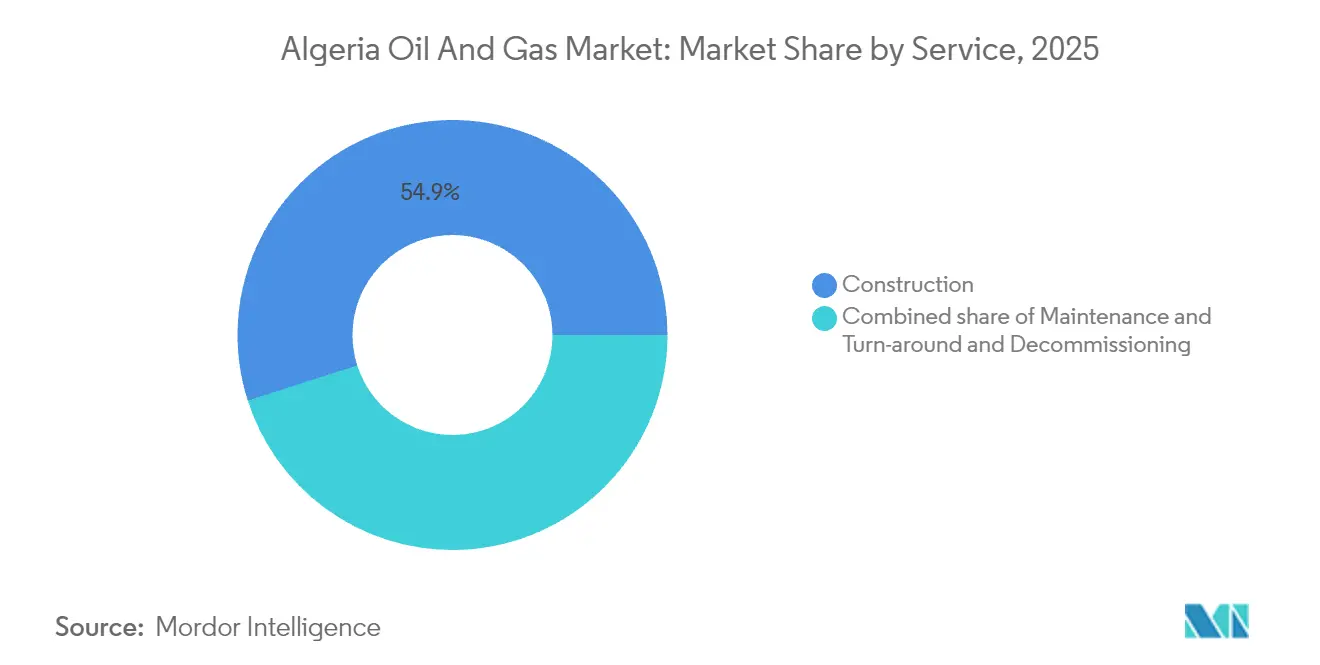

- By service, construction services held 54.93% of the Algerian oil and gas market share in 2025; decommissioning services are projected to advance at an 7.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Algeria Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| New Hydrocarbon Investment Law (2019) incentives | +0.80% | Hassi Messaoud and Hassi R’Mel basins | Medium term (2-4 years) |

| Recovery in global oil prices improving cash flows | +1.20% | National, with spillover along Mediterranean export corridors | Short term (≤ 2 years) |

| Upstream partnerships with majors accelerating exploration | +0.60% | Offshore blocks plus Ahnet and Gourara basins | Long term (≥ 4 years) |

| Offshore seismic programme unlocking deep-water potential | +0.50% | Mediterranean offshore blocks in >200 m water depths | Long term (≥ 4 years) |

| Petrochemical diversification push for value capture | +0.40% | Arzew and Skikda industrial complexes | Medium term (2-4 years) |

| Trans-Sahara & Medgaz capacity expansions | +0.30% | Trans-Saharan corridor and Mediterranean export routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

New Hydrocarbon Investment Law (2019) Incentives Drive Foreign Capital Inflows

Algeria lowered the mandatory Sonatrach equity stake from 51% to a minority participation, easing a key barrier to foreign entry and triggering ExxonMobil’s May 2024 memorandum on the Ahnet and Gourara basins. The streamlined tax regime also caps windfall levies, improving netbacks on liquids and gas. Early evidence of success includes five exploration blocks awarded in October 2024, with a guaranteed spending of USD 606 million. Implementation consistency remains vital because high-capex projects demand 20-year fiscal stability. The government’s public commitment to the law alleviates investor concerns, yet ministries must still expedite permitting to avoid schedule delays.(1)Exxon Mobil Corporation, “ExxonMobil Signs Algerian Exploration MoU,” exxonmobil.com

Recovery in Global Oil Prices Improving Cash Flows

Brent prices hovering above USD 70/bbl through 2024 restored Sonatrach’s balance sheet, enabling overdue maintenance and fresh seismic surveys. The company’s 2024 budget rose 18%, directing capital toward compressors at Hassi R’Mel and enhanced oil recovery pilots at Hassi Messaoud. Price resilience particularly favors Algeria’s light‐sweet Saharan Blend, which trades at a premium in European refineries configured for low-sulfur feeds. Nonetheless, Algeria’s fiscal break-even remains above USD 100/bbl, so macro volatility still threatens spending momentum. Hedging strategies and cost discipline, therefore, stay central to long-range planning.

Upstream Partnerships with Majors Accelerating Exploration

Sonatrach’s joint ventures with TotalEnergies at Timimoun, PTTEP at Touat, and Occidental in Berkine collectively introduce 4-D seismic, extended-reach drilling, and AI-based production optimization. TotalEnergies’ April 2024 commitment to deliver 2 million t of LNG to France in 2025 secured offtake for planned capacity ramp-ups. Knowledge transfer is equally material: digital well models cut workover downtime by 12% in pilot wells. Partner diversity now spans U.S., European, and Asian capital sources, spreading risk and broadening technology inflows.

Offshore Seismic Programme Unlocking Deep-Water Potential

A 24-month assessment agreement with Chevron, signed in January 2025, covers ultra-deep Mediterranean acreage and marks the first major U.S. offshore return since 2008. Broadband-wide azimuth seismic improves imaging beneath complex salt and carbonate layers, reducing dry-hole risk. Early workspace mapping suggests the presence of structurally trapped gas liquids at a water depth of 1,300 m. Development costs may exceed USD 1 billion per hub so that project sanctioning will hinge on fiscal incentives and proximity to existing Medgaz tie-ins. The survey also de-risks adjacent Eni-operated acreage, magnifying basin-wide interest.(2)Chevron Corporation, “Chevron Expands Mediterranean Deepwater Footprint,” chevron.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political & regulatory uncertainty post-2024 elections | -0.40% | Nationwide influence on FDI decisions | Short term (≤ 2 years) |

| Ageing onshore fields with high decline rates | -0.30% | Hassi Messaoud, Hassi R’Mel, In Amenas | Long term (≥ 4 years) |

| Rising domestic gas demand eroding export surplus | -0.50% | Consumption centers and power plants | Medium term (2-4 years) |

| Water scarcity limits unconventional fracking | -0.20% | Saharan basins earmarked for shale appraisal | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Political & Regulatory Uncertainty Post-2024 Elections

President Tebboune’s large victory margin signaled continuity, yet social pressures tied to 15% youth unemployment keep the risk of protest elevated. Investors recall the prior contract renegotiations in 2006 and therefore closely watch cabinet reshuffles. Persistent bureaucracy can stall field‐development plans by 12–18 months, inflating cost escalations in a high-inflation environment. Fiscal reform bills outside the hydrocarbon law also influence cash flows because sudden tax tweaks affect service import costs. Diplomatic outreach to the EU aims to demonstrate regulatory reliability, but credibility hinges on streamlined licensing timelines and swift dispute resolution.

Rising Domestic Gas Demand Eroding Export Surplus

Power generation consumes approximately 95% of the fuel input from natural gas, with peak summer demand topping 18 billion m³ annually. Household and industrial usage increases as subsidized pricing diminishes conservation incentives, narrowing the exportable surplus that generates 95% of hard-currency earnings. Pipeline commitments to Spain and Italy require minimum flows, so Sonatrach must juggle domestic load and contract obligations. Options include raising end-user tariffs and accelerating upgrades to combined-cycle efficiency. Until demand management matures, export revenues will remain capped despite incremental production gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Dominance Faces Midstream Acceleration

Upstream operations generated 76.42% of 2025 revenue, underscoring the Algeria oil and gas market’s reliance on mature field output and emerging offshore blocks. Midstream infrastructure, although smaller, is expected to grow at a 9.46% CAGR to 2031 as pipeline debottlenecking and the introduction of new gas treatment trains unlock additional volumes. The Algeria oil and gas market size for midstream assets is projected to swell once the Trans-Saharan line upgrades to 30 billion m³ capacity by 2028. European importers already book incremental throughput allocations, validating investment assumptions.

Sonatrach channels capital expenditures toward dual compressor platforms and gas-gathering systems, aiming to reduce flaring intensity to below 2% by 2027. Financing diversity also grows; Islamic sukuk issues in March 2025 raised USD 800 million, providing local currency hedging for pipeline metallurgy orders. Downstream expansion remains selective, focusing on petrochemical integration at Arzew and Skikda rather than fresh refinery builds. Private partners gain tariff guarantees under the hydrocarbon law, reducing payback risk and encouraging foreign EPC firms to enter Algeria’s midstream segment.

By Location: Offshore Growth Challenges Onshore Legacy Infrastructure

Offshore blocks delivered 88.35% of 2025 output value, yet rely heavily on two large complexes nearing plateau, making reserve replacement critical for the Algeria oil and gas market. Onshore assets experience a 6% annual decline, but still underpin cash flows thanks to sub-$25/bbl lifting costs. Enhanced oil recovery pilots deploy polymer flooding and horizontal re-entries, extending field life but raising water-cut handling requirements.

Offshore developments require a USD 40-60/bbl break-even, necessitating robust fiscal incentives to remain competitive. Subsea tie-backs into Medgaz spare capacity partially offset high capital intensity. Environmental agencies impose stringent discharge limits, compelling operators to budget for zero-flaring systems. The Algeria oil and gas market share for onshore projects could rebound if horizontal drilling reduces decline curves, though water scarcity and logistics challenges restrict large-scale unconventional adoption.

By Service: Construction Leadership Yields to Decommissioning Growth

Construction services retained a 54.93% share in 2025, reflecting a backlog of gas processing trains, compressor stations, and early-production facilities. The Algeria oil and gas market size for construction contracts exceeded USD 5.14 billion last year, following Petrofac’s USD 600 million EPC award. Maintenance spending increases as Hassi R’Mel pipeline compressors surpass their design cycles, prompting OEMs like Baker Hughes to enter into multi-year frame agreements.

Decommissioning is expected to command the fastest 7.88% CAGR to 2031 as offshore platforms built in the 1980s approach their cessation. Tenders now stipulate well plugging, subsea infrastructure removal, and site remediation under revised environmental codes. International contractors leverage specialized lift vessels and cuttings reinjection expertise to command premium prices. Regulatory escrow accounts for end-of-life liabilities, ensuring funding certainty, driving early planning, and widening the service mix beyond traditional construction activities.

Geography Analysis

Algeria's Sahara heartland, situated 1,500 km south of Mediterranean export hubs, incurs logistical costs that exceed those of coastal basins, yet the region still accounts for 80% of proven reserves. Pipeline corridors connect these deserts to Arzew and Skikda for the export of LNG and condensate, providing Algeria's oil and gas market participants with reliable monetization channels. The Algeria oil and gas market size tied to trans-Mediterranean flows reached USD 5.24 billion in 2025, aided by Medgaz expansion to 12 billion m³/y.

Mediterranean offshore acreage presents the primary growth frontier, with new 3-D seismic data indicating thick Pliocene gas sands analogous to Egypt's Zohr field. Water depths exceeding 1,000 meters necessitate floating production units, prompting feasibility studies on hybrid LNG-FPSO options that reduce the time to first gas. Coastal communities raise environmental concerns, so operators often fund marine biodiversity monitoring as part of the permitting process. European buyers prefer pipeline gas for carbon-intensity advantages over long-haul LNG, keeping Algerian volumes competitive under the EU methane regulation regime.

Northern Algeria's industrial belt is home to petrochemical clusters, where feedstock availability drives the development of polypropylene and methanol projects. Proximity to Mediterranean ports lowers freight bills into Southern Europe, encouraging downstream diversification. Inland infrastructure modernization, including dual-fuel power plants and strategic storage caverns, supports supply security for domestic consumers. Meanwhile, Saharan solar irradiation exceeding 2,400 kWh/m² annually underpins proposals for green hydrogen hubs that could leverage existing pipeline rights-of-way, adding an energy transition dimension to regional planning.

Competitive Landscape

Algeria’s market structure is moderately concentrated: Sonatrach dominates upstream equity but contracts out key service scopes, drawing intense competition among EPC, subsea, and digital solution providers. International majors operate through production-sharing or risk-service agreements, rather than outright asset ownership, accepting lower headline returns in exchange for access to resources. ExxonMobil’s upstream re-entry alongside TotalEnergies, Eni, Occidental, and PTTEP diversifies capital inflows and technology sources.

Digitalization emerges as a core differentiator. Sonatrach and Huawei deploy fiber-optic sensing for real-time leak detection across 2,000 km of trunk lines, while Repsol and Baker Hughes pilot AI-driven predictive maintenance that cuts unplanned downtime by 15%. Service companies position integrated offerings—from seismic to abandonment—helping operators optimize lifecycle economics. Decommissioning specialists anticipate a USD 1 billion opportunity through 2030 as offshore structures retire, spurring joint ventures that localize heavy-lift capacity.(3)Huawei Technologies, “Smart Pipeline Fiber Sensing Collaboration,” huawei.com

Strategic initiatives align with energy transition trends. TotalEnergies evaluates carbon capture at Skikda, pairing depleted reservoirs with CO₂ pipeline retrofits. Sonatrach studies blue hydrogen using existing reformers coupled with carbon sequestration in exhausted gas fields. Competitive advantage will hinge on balancing hydrocarbon cash flows with low-carbon investments, ensuring relevance as global demand patterns evolve.(4)Baker Hughes Company, “Advanced Compression Contract in Algeria,” bakerhughes.com

Algeria Oil And Gas Industry Leaders

Eni S.p.A.

Sonatrach S.p.A.

China National Petroleum Corporation

Equinor ASA

BP Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: ExxonMobil signed a memorandum of understanding with Sonatrach for exploration opportunities in the Ahnet and Gourara basins. The agreement marks ExxonMobil's return to Algeria after a 16-year absence and demonstrates the 2019 Hydrocarbon Law's effectiveness in attracting international majors

- April 2024: TotalEnergies has extended its partnership with Sonatrach for the development of the Timimoun gas field and is committed to delivering 2 million tons of LNG to France in 2025.

- March 2024: Sonatrach and Huawei have announced a joint innovation initiative for smart pipeline monitoring, utilizing fiber optic sensing technology. The partnership was unveiled at Mobile World Congress 2024 and represents Algeria's commitment to digital transformation in energy infrastructure.

- February 2024: Repsol partnered with Baker Hughes to implement artificial intelligence solutions for enhanced oil recovery at Algerian operations.

Algeria Oil And Gas Market Report Scope

The oil and gas market is one of the significant sectors across all industries that play a critical role in the development of the global economy. The oil and gas sector is an entire value chain comprised of upstream, midstream, and downstream segments. The upstream segment oversees the exploration and production of hydrocarbons, whereas the midstream segment has transportation and storage activities. The downstream sector includes the refining and distribution business.

Algeria oil and gas market is segmented by sector. By sector, the market is segmented into upstream, midstream and downstream. The report also offers market size and demand forecasts for the segment based on production volume.

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Service

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

| By Sector | Upstream |

| Midstream | |

| Downstream | |

| By Location | Onshore |

| Offshore | |

| By Service | Construction |

| Maintenance and Turn-around | |

| Decommissioning |

Key Questions Answered in the Report

What is the current value of the Algeria oil and gas market?

The Algeria oil and gas market size reached USD 9.7 billion in 2026 and is projected to reach USD 11.58 billion by 2031.

How fast is Algeria’s midstream segment expanding?

Midstream infrastructure is forecast to grow at 9.46% CAGR between 2026 and 2031, the fastest among all segments.

Which segment holds the largest market share right now?

Upstream activities accounted for 76.42% of the Algeria oil and gas market share in 2025.

What factors threaten Algeria’s export capacity?

Rising domestic gas demand for power generation and aging onshore field declines both erode exportable gas volumes.

How is Algeria attracting foreign investment?

The 2019 Hydrocarbon Law reduced mandatory state equity, introduced tax incentives, and already enabled ExxonMobil and Chevron partnerships.

What opportunity does decommissioning present?

Platform retirements mean decommissioning services are set to grow at 7.88% CAGR, creating a USD 1.08 billion market by 2031.

Page last updated on: