Middle-East Industrial Gases Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

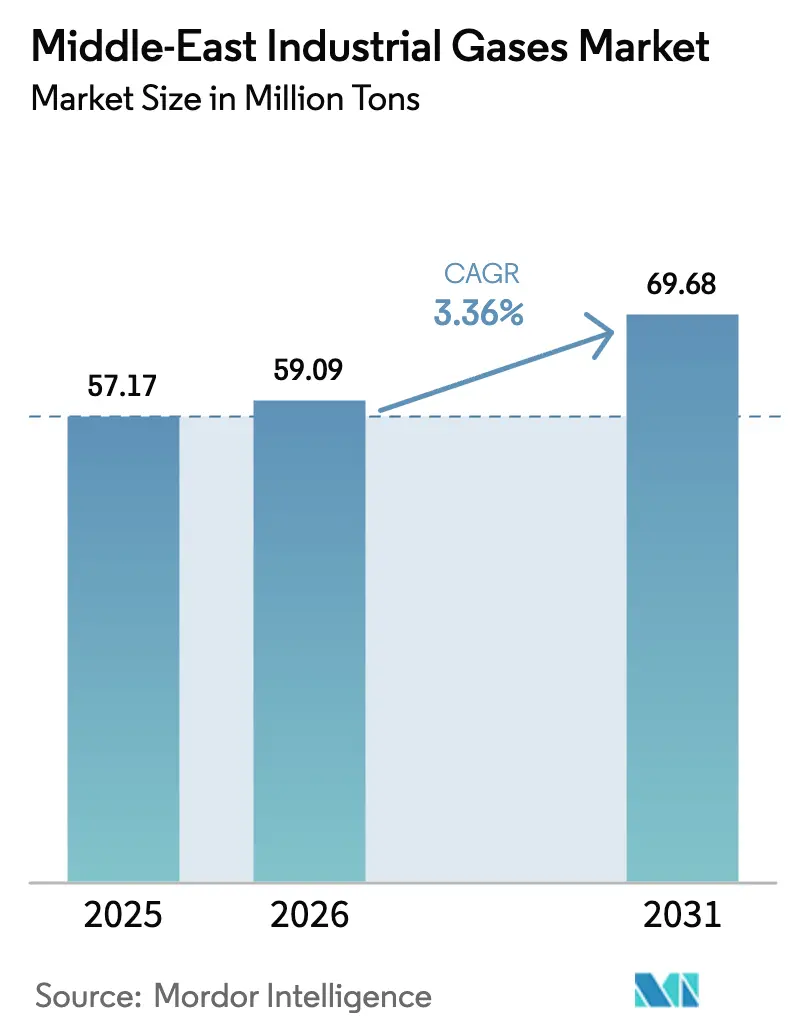

| Base Year Market Size (2025) | 57.17 Million tons |

| Market Volume (2026) | 59.09 Million tons |

| Market Volume (2031) | 69.68 Million tons |

| Growth Rate (2026 - 2031) | 3.36% CAGR |

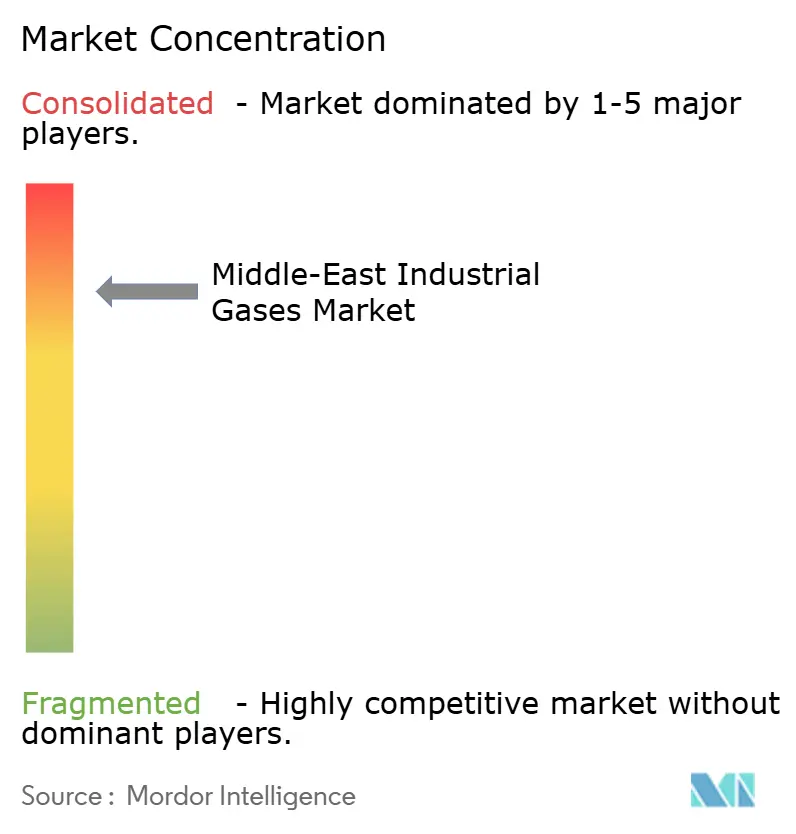

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East Industrial Gases Market Analysis by Mordor Intelligence

The Middle-East Industrial Gases Market size is expected to grow from 57.17 Million tons in 2025 to 59.09 Million tons in 2026 and is forecast to reach 69.68 Million tons by 2031 at 3.36% CAGR over 2026-2031. Robust capital spending on petrochemicals, green hydrogen, and new hospitals underpins the steady expansion. Investment momentum in upstream and mid-stream hydrocarbons, estimated at USD 730 billion through 2030, keeps demand for separation and purification gases buoyant. Diversification strategies targeting semiconductor fabrication, food preservation, and logistics hubs add fresh consumption corridors, while tight safety rules and rising energy efficiency standards prompt companies to favor on-site generation contracts and low-carbon technologies. The competitive field stays moderately concentrated as multinationals leverage long-term supply deals, yet country plans for hydrogen and carbon capture leave white-space for innovators.

Key Report Takeaways

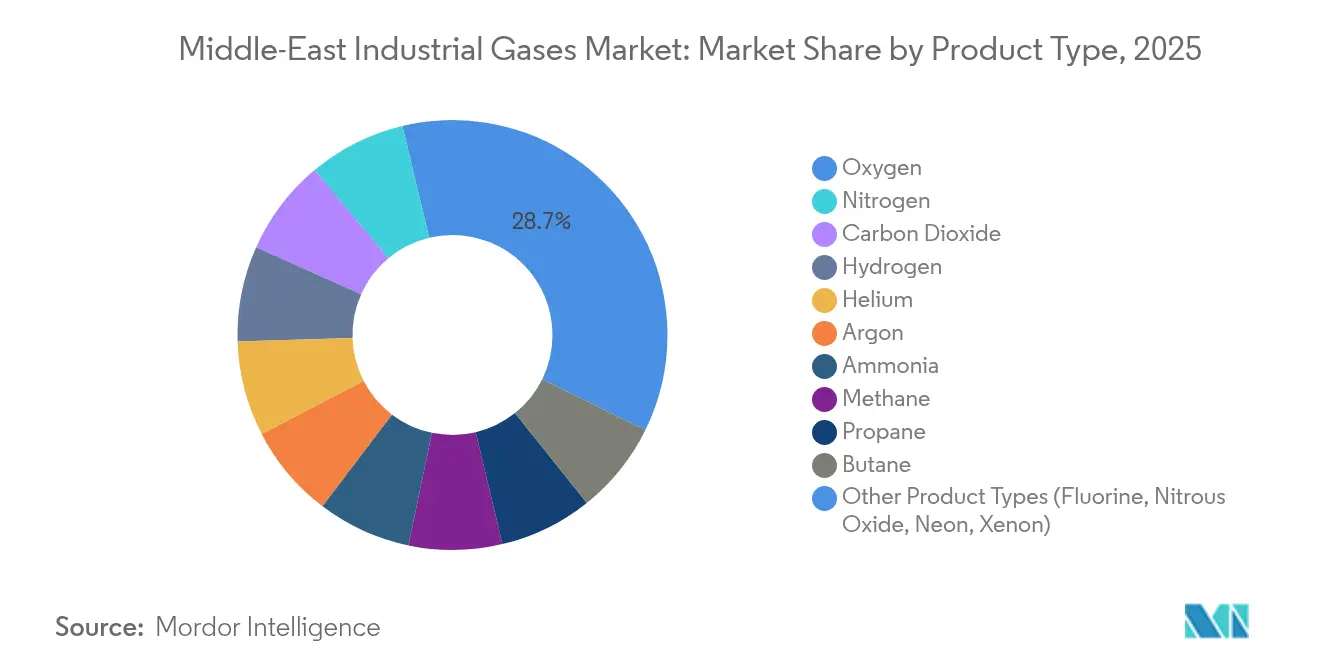

- By product type, oxygen led with 28.74% of Middle-East industrial gases market share in 2025, whereas nitrogen is projected to expand at a 4.44% CAGR through 2031.

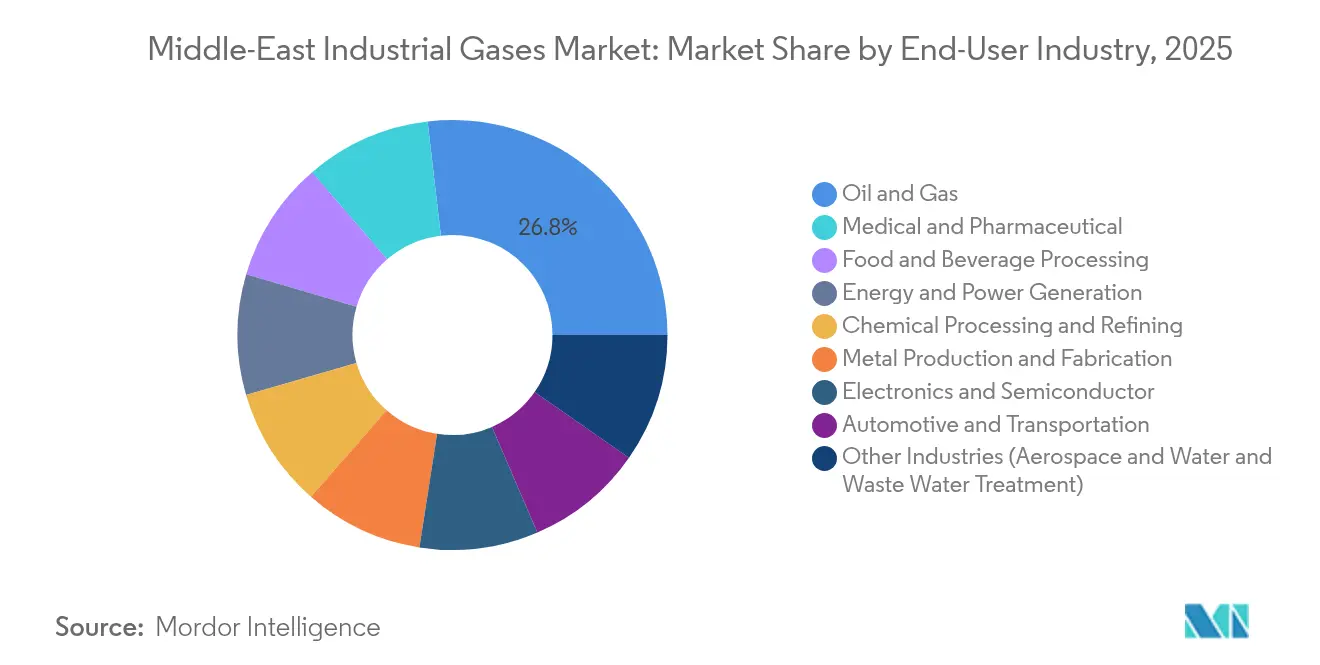

- By end-user industry, the oil and gas sector accounted for 26.85% share of the Middle-East industrial gases market size in 2025, while medical and pharmaceutical applications post the highest 4.59% CAGR to 2031.

- By geography, Saudi Arabia commanded 34.78% of Middle-East industrial gases market share in 2025 whereas the UAE shows the fastest 4.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle-East Industrial Gases Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from upstream and mid-stream oil and gas operations | +1.2% | Saudi Arabia, UAE, Qatar, Kuwait | Medium term (2-4 years) |

| Expanding regional petrochemicals and refinery CAPEX pipeline | +0.9% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Accelerated build-out of healthcare infrastructure | +0.6% | Global | Short term (≤ 2 years) |

| Rise of government-backed green-hydrogen mega-projects | +0.8% | Saudi Arabia, UAE, Oman | Long term (≥ 4 years) |

| Large construction giga-projects boosting welding and cutting gases | +0.4% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand from Upstream and Mid-Stream Oil and Gas Operations

Enhanced recovery, sour-gas treatment, and new LNG trains are lifting usage of high-purity nitrogen, hydrogen, and CO₂. Saudi Aramco and ADNOC add separation plants that inject nitrogen for pressure maintenance and hydrogen for hydrocracking, multiplying gas intensity per barrel processed. Qatar expects output to reach 244 billion m³ by 2030 with an extra 83 billion m³ of industrial gas needs, equal to 57% of forecast growth[1]Gulf Times, “Qatar Gas Output Set for Sharp Rise,” gulf-times.com. Offshore projects such as Hail and Ghasha require 1.5 million t of captured CO₂ each year, sharpening demand for purification units. Continuous upstream activities therefore cascade into on-site supply contracts across the value chain.

Expanding Regional Petrochemicals and Refinery CAPEX Pipeline

Projects like the USD 11 billion Amiral complex in Saudi Arabia integrate refining with chemicals, lifting gas demand per feedstock unit[2]TotalEnergies, “Aramco and TotalEnergies Finalize USD 11 Billion Amiral Project,” totalenergies.com. The complex targets 1.65 million t of ethylene annually, calling for large volumes of nitrogen for inerting, oxygen for oxidation, and hydrogen for hydrotreating. New builds move product slates toward specialty polymers, which need ultra-high purity gases in compounding and quality control. Carbon capture modules inside these plants raise the call for purification and compression equipment, aligning environmental targets with operational efficiency.

Accelerated Build-Out of Healthcare Infrastructure (Medical Gases)

Middle-East hospital and clinic projects embed centralized gas piping and large bulk storage. Air Liquide’s regional revenue rose 7.1% in H1 2024 to EUR 553 million on stronger medical oxygen and specialty mixtures. Gulf Cryo Med Gas extended supply contracts that meet European and US Pharmacopoeia norms. Pandemic lessons drive stockpiling mandates and redundancy planning, keeping demand for portable cylinders and vacuum-insulated tanks high. Medical tourism growth in the UAE and Saudi Arabia further sustains volume expansion in nitrous oxide and helium for imaging.

Rise of Government-Backed Green-Hydrogen Mega-Projects

The USD 8.4 billion NEOM plant has reached 80% completion and will output 600 tons of hydrogen daily by 2026. Oman earmarked USD 40-60 billion for hydrogen corridors, including shared pipelines and desalination. Egypt’s planned USD 17 billion South Sinai complex targets 400,000 tons annually. These ventures create large captive demand for nitrogen, argon, and oxygen within electrolysis, liquefaction, and ammonia conversion systems, cementing long-term off-take for gas producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening EH&S regulations and compliance costs | -0.7% | Global | Short term (≤ 2 years) |

| Crude-oil price volatility curbing new industrial investments | -0.5% | Saudi Arabia, UAE, Kuwait, Qatar | Medium term (2-4 years) |

| Scarce regional CO₂-capture & purification infrastructure | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening EH&S Regulations and Compliance Costs

Regional laws are aligning with international benchmarks, requiring detailed environmental impact reviews and strict flaring limits. The UAE’s Federal Law 24 mandates cradle-to-grave emission reporting, and satellite imagery shows regulators increasing enforcement against illegal venting. BBC investigations uncovered toxic plumes over several Gulf facilities, prompting faster adoption of sealed combustion and high-efficiency capture systems. Meeting >99% CO₂ purity for storage elevates capital and operating costs for small suppliers, encouraging consolidation among firms with robust compliance infrastructure.

Crude-Oil Price Volatility Curbing New Industrial Investments

Price swings reshape GDP growth and budget priorities across producer economies, influencing capex cycles for refineries, metals, and power projects that consume bulk gases. Academic studies covering Saudi Arabia, UAE, Kuwait, and Qatar confirm a long-run linkage between oil price variance, inflation, and investment. Petrochemical competitiveness erodes during downturns when naphtha-based producers elsewhere gain cost advantage, as shown by SABIC’s USD 320 million loss in Q1 2025. Volatility therefore delays some debottlenecking projects and defers fresh demand for industrial gases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Oxygen Dominance amid Nitrogen’s Technological Surge

Oxygen accounted for 28.74% of Middle-East industrial gases market share in 2025, driven by steel mills, petrochemicals, and aluminum smelting. Nitrogen is set to grow fastest at a 4.44% CAGR to 2031 on expanded use in food packaging, electronics soldering, and inerting for oil recovery. Carbon dioxide volumes rise with enhanced oil recovery and beverage carbonation, while hydrogen sees tailwinds from refinery upgrades and electro-fuels. Argon supports welding during giga-project construction, and helium demand stems from MRI and semiconductor lithography. Air Liquide’s helium liquefaction build in Qatar aims to ease chronic shortages. Linde commissioned 59 small on-site nitrogen and oxygen plants in 2024, highlighting a shift toward distributed production that tightens customer integration.

The segment’s evolution shows a pivot from volume-driven commodity supply to purity-driven specialty demand. Construction, energy, and consumer goods shape oxygen and carbon dioxide sales, while clean fuels, electronics, and packaged food tilt growth toward nitrogen and hydrogen. The Middle-East industrial gases market continues to deepen on-site models that provide steady offtake and cost certainty for end users.

By End-User Industry: Oil and Gas Leadership Challenged by Healthcare Acceleration

Oil and gas retained 26.85% of the Middle-East industrial gases market size in 2025, supported by LNG expansions and sour-gas processing. Medical and pharmaceutical demand logs a 4.59% CAGR through 2031 as hospitals upgrade piped oxygen networks and emergency reserves. Petrochemicals and refining remain large buyers of hydrogen, nitrogen, and carbon monoxide as integrated complexes expand. Electronics and semiconductor lines in Saudi Arabia and the UAE need ultra-high purity gases, lifting demand for bulk nitrogen and trace-level dopant mixtures.

Food and beverage processors widen nitrogen uptake for modified atmosphere packaging that reduces spoilage. Construction growth sustains welding gas sales, and renewable power projects require calibration gases for monitoring. Water treatment plants adopt oxygen-enhanced aeration, and environmental labs test flue gases to meet stricter emission ceilings. The diversification push inside regional economies therefore spreads industrial gas demand across legacy and emerging sectors, limiting reliance on crude.

Geography Analysis

Saudi Arabia captured 34.78% of Middle-East industrial gases market share in 2025 owing to concentrated petrochemical clusters in Jubail and Yanbu. Vision 2030 boosts demand through NEOM’s green hydrogen plant and semiconductor fabrication lines that require high-purity gases. Large pipeline networks cut distribution cost and support investments in cryogenic air separation units. Continued refinery integration and blue-hydrogen projects ensure resilient baseline consumption.

The UAE is forecast to grow at a 4.72% CAGR, the region’s quickest pace, as it develops technology parks, health tourism, and advanced manufacturing. ADNOC’s USD 13 billion gas projects and Ruwais LNG’s 9.6 million t capacity expand demand for nitrogen, helium, and hydrogen. Strategic free-zones and world-class ports make the UAE a distribution hub, smoothing last-mile delivery of cylinders and bulk tankers across the wider Middle East and Africa. Qatar focuses on LNG and petrochemicals with North Field output heading to 142 million t by 2030. The Ammonia-7 project integrates carbon capture, creating needs for high-purity CO₂ compression. Kuwait gains from new petrochemical assets and its first CO₂ recovery plant that processes 280 t every day. Israel leverages offshore gas discoveries and tech expansion, while Oman channels investment into large green-hydrogen valleys served by shared infrastructure. Diverse economic blueprints across these countries thus anchor future growth in the Middle-East industrial gases market.

Competitive Landscape

The Middle-East industrial gases market is highly concentrated. Air Liquide, Linde, and Air Products operate integrated service platforms that bundle gas supply, plant design, and operational expertise, locking in multiyear take-or-pay agreements. Air Products acquired Air Liquide’s UAE and Bahrain businesses to gain scale in bulk and merchant segments. Gulf Cryo retains strong local partnerships and tailors solutions for healthcare and specialty segments.

Strategic joint ventures underpin capex-heavy projects as partners share risk and secure feedstock. Gulf Cryo’s alliance with Aramco on lower-carbon hydrogen trials signals regional appetite for cleaner molecules. Technology leadership matters as firms deploy digital twins, membrane separation, and energy-efficient cryogenic cycles that lower cost per ton and improve compliance metrics.

Competitive differentiation now also hinges on ESG readiness. Suppliers able to certify low-carbon molecules or provide onsite renewable power integration win bids for green-hydrogen and carbon-capture contracts. While barriers to classic bulk gases stay high, specialty niches around electronics, biotechnology, and green fuels offer entry points for agile players that can meet stringent purity and sustainability thresholds.

Middle-East Industrial Gases Industry Leaders

Linde PLC

Air Liquide

AHG

Air Products and Chemicals Inc.

Gulf Cryo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Linde will invest USD 150 million to build, own, and operate an air separation unit (ASU) in Boden, Sweden. The ASU will supply oxygen, nitrogen, and argon to H2 Green Steel’s plant, reducing carbon emissions by up to 95% compared to traditional steelmaking. Scheduled to start by 2026, it will also serve Linde’s local merchant market customers.

- May 2023: Air Products signed a USD 1 billion agreement with Uzbekistan’s government and Uzbekneftegaz JSC to acquire, own, and operate a natural gas-to-syngas facility in Qashqadaryo Province. The facility supports Uzbekneftegaz’s gas-to-liquid complex, producing 1.5 million tonnes of synthetic fuels annually for domestic use and export.

Middle-East Industrial Gases Market Report Scope

Industrial gases are produced in relatively large quantities by gas manufacturing companies for use in various industrial manufacturing processes. These gases are sold to other enterprises and industries, including oil and gas, petrochemicals, chemicals, power, mining, steelmaking, metals, environmental protection, medicine, pharmaceuticals, biotechnology, food, water, fertilizers, nuclear power, and electronics.

The Middle Eastern industrial gases market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into nitrogen, oxygen, carbon dioxide, hydrogen, helium, argon, ammonia, methane, propane, butane, and other types (fluorine and nitrous oxide). By end-user industry, the market is segmented into chemical processing and refining, electronics, food and beverage, oil and gas, metal manufacturing and fabrication, medical and pharmaceutical, automotive and transportation, energy and power, and other end-user industries (water treatment and environmental protection). The report also covers the market size and forecasts for the Middle Eastern industrial gases market in three countries across the Middle Eastern region.

For each segment, the market sizing and forecasts are provided on the basis of volume (tons).

| Nitrogen |

| Oxygen |

| Carbon Dioxide |

| Hydrogen |

| Helium |

| Argon |

| Ammonia |

| Methane |

| Propane |

| Butane |

| Other Product Types (Fluorine, Nitrous Oxide, Neon, Xenon) |

| Chemical Processing and Refining |

| Electronics and Semiconductor |

| Food and Beverage Processing |

| Oil and Gas |

| Metal Production and Fabrication |

| Medical and Pharmaceutical |

| Automotive and Transportation |

| Energy and Power Generation |

| Other Industries (Aerospace and Water and Waste Water Treatment) |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Israel |

| Rest of Middle East |

| By Product Type | Nitrogen |

| Oxygen | |

| Carbon Dioxide | |

| Hydrogen | |

| Helium | |

| Argon | |

| Ammonia | |

| Methane | |

| Propane | |

| Butane | |

| Other Product Types (Fluorine, Nitrous Oxide, Neon, Xenon) | |

| By End-User Industry | Chemical Processing and Refining |

| Electronics and Semiconductor | |

| Food and Beverage Processing | |

| Oil and Gas | |

| Metal Production and Fabrication | |

| Medical and Pharmaceutical | |

| Automotive and Transportation | |

| Energy and Power Generation | |

| Other Industries (Aerospace and Water and Waste Water Treatment) | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Israel | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the current size of the Middle-East industrial gases market?

The market stands at 59.09 million tons in 2026 and continues to expand steadily.

Which product segment holds the largest share of the regional market?

Oxygen leads with a 28.74% share, driven by steelmaking, petrochemical processing, and metal fabrication.

Which end-user industry is growing at the fastest pace?

Medical and pharmaceutical applications post the highest growth at a 4.59% CAGR thanks to healthcare infrastructure upgrades.

Which Middle-East country is expected to record the quickest market growth?

The UAE is forecast to achieve the fastest expansion at a 4.72% CAGR through 2031.

Page last updated on: