Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

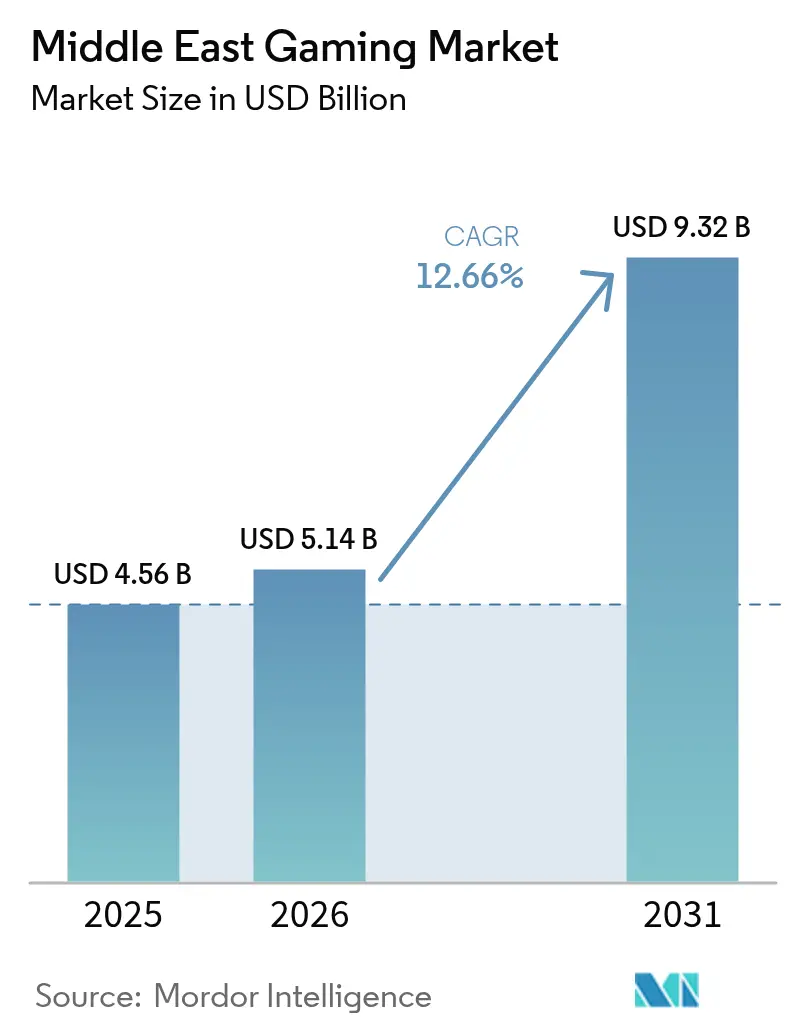

| Base Year Market Size (2025) | USD 4.56 Billion |

| Market Size (2026) | USD 5.14 Billion |

| Market Size (2031) | USD 9.32 Billion |

| Growth Rate (2026 - 2031) | 12.66% CAGR |

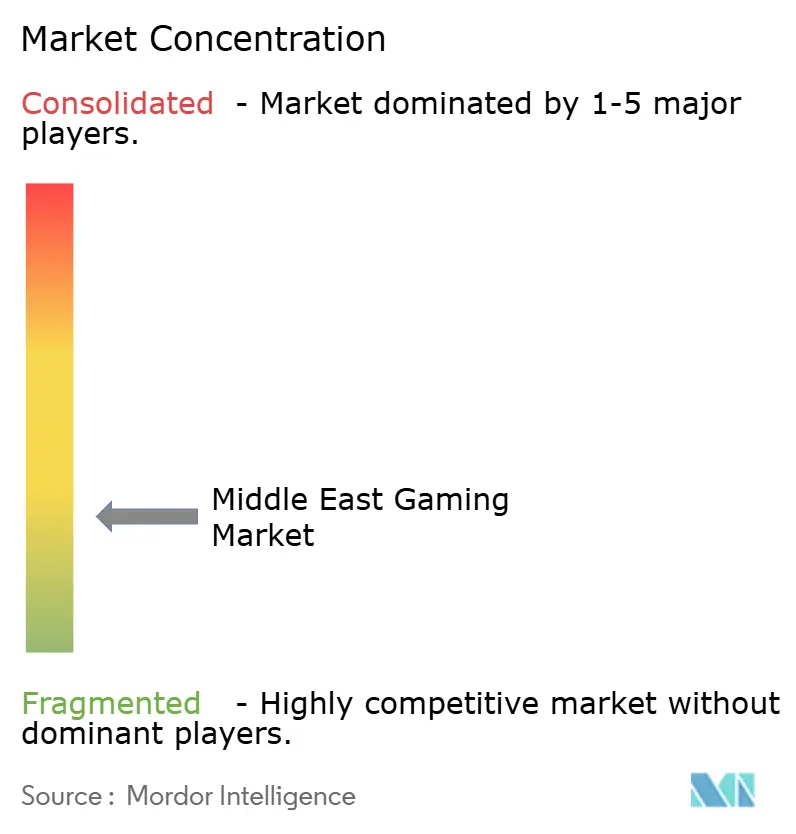

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Gaming Market Analysis by Mordor Intelligence

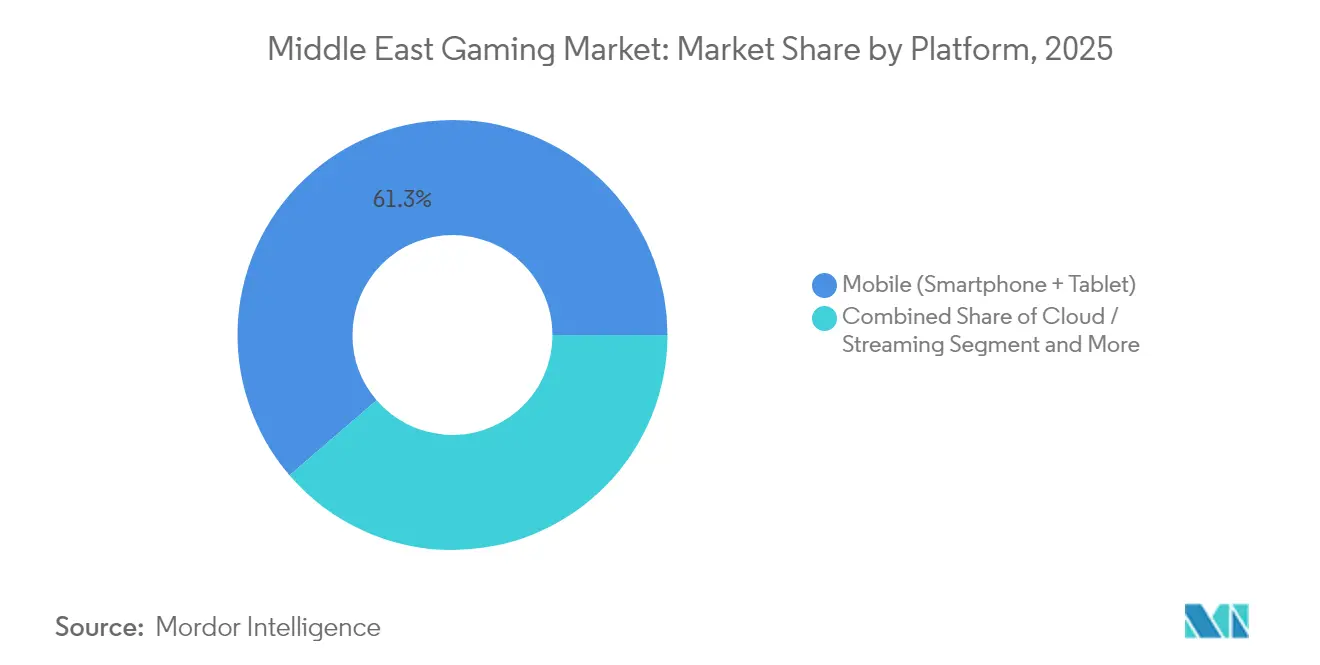

The Middle East gaming market size in 2026 is estimated at USD 5.14 billion, growing from 2025 value of USD 4.56 billion with 2031 projections showing USD 9.32 billion, growing at 12.66% CAGR over 2026-2031. A surge of sovereign investments, cloud-first infrastructure rollouts and supportive policy reforms is accelerating platform innovation and content localization. Saudi Arabia’s Public Investment Fund (PIF) has led the shift by acquiring Niantic’s mobile-and-AR portfolio for USD 3.5 billion in March 2025, anchoring domestic intellectual-property ownership.[1]Andrew Ross Sorkin, “Pokémon Go Maker Niantic Sells Unit to Saudi Fund for USD 3.5 Billion,” The New York Times, nytimes.com Regional telecom operators are monetizing 5G network slicing and edge computing to support console-quality titles on smartphones, while the UAE’s first federal gambling license, awarded to Wynn Resorts in 2024, signals regulatory modernization that attracts new revenue models. Data-center power in the Gulf is projected to climb from 1 GW in 2025 to 3.3 GW by 2030, meeting the latency targets of cloud and streaming platforms. [2]Staff Reporter, “Race for AI Supremacy in Middle East Is Measured in Data Centers,” Bloomberg, bloomberg.com Mobile titles hold a 52% share, yet cloud-gaming channels register the fastest 17.2% CAGR as device-agnostic play removes console price barriers. Genre preferences remain led by shooter and battle-royale formats, but Arabic-localized RPGs are closing the gap as cultural relevance improves.

Key Report Takeaways

- By platform, mobile commanded 61.30% of the Middle East gaming market share in 2025, while cloud and streaming platforms are projected to expand at a 16.74% CAGR through 2031.

- By revenue model, free-to-play captured 62.10% revenue share in 2025; subscription services exhibit 17.65% CAGR to 2031.

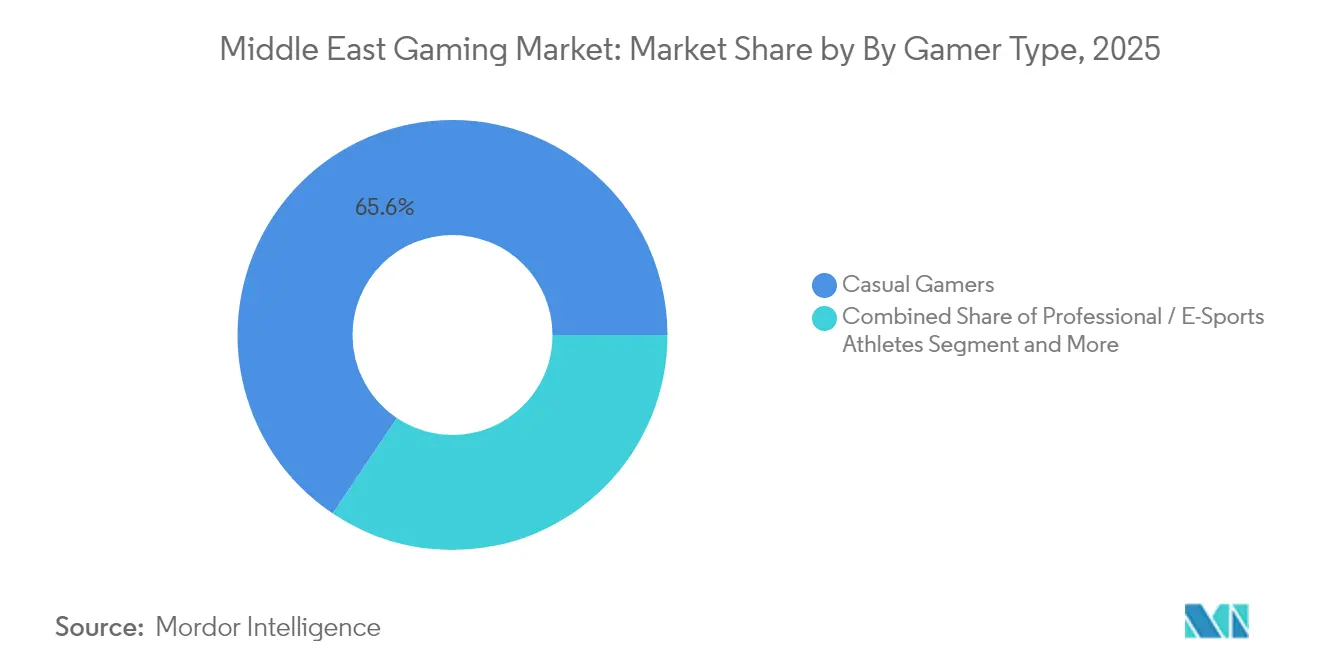

- By gamer type, professional esports athletes represent the fastest-growing cohort with a 18.92% CAGR supported by rising prize pools.

- By genre, shooter and battle-royale titles held 34.60% of the Middle East gaming market size in 2025; Arabic-localized RPGs are advancing at a 13.58% CAGR.

- By country, Saudi Arabia led with a 33.40% share of the Middle East gaming market size in 2025, while Kuwait is forecast to post a 11.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Gaming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of 5G and fiber broadband | +2.10% | GCC core, spill-over to Turkey | Short term (≤ 2 years) |

| Rising government esports investments | +1.80% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Increase in Arabic-localized AAA and indie content | +1.50% | Middle East region | Medium term (2-4 years) |

| Proliferation of digital wallets and carrier billing | +1.30% | GCC, Turkey, Iran | Short term (≤ 2 years) |

| High smartphone penetration, falling data prices | +1.20% | Iran, Turkey | Short term (≤ 2 years) |

| Telco-tech cloud-gaming alliances | +0.90% | GCC core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of 5G and Fiber Broadband Among GCC Nations Enabling High-Quality Mobile Gaming

Record 5G downstream speeds of 30.5 Gbps, achieved by eand in 2024, demonstrate the bandwidth now underpinning real-time multiplayer, 4K-streamed sessions and ultra-low-latency esports matches. As Zain Bahrain sunsets 3G, spectrum is refarmed to boost 5G capacity, allowing operators to promise 20 ms round-trip latency. Network-slicing pilots dedicate isolated bandwidth to gaming traffic, improving jitter and leading to premium data packs bundled with publishers’ subscription passes. Edge nodes deployed inside carrier facilities shorten content-delivery hops, up-lifting conversion rates for cloud-gaming trials. Taken together, connectivity modernization is shortening session-start times and encouraging longer average play per day, directly accelerating in-game monetization.

Rising Government Investments in Esports Infrastructure in Saudi Arabia and UAE

Saudi Arabia earmarked USD 38 billion for gaming under Vision 2030 and targets 250 local studios by 2030, validating the sector as a pillar of economic diversification. The Kingdom’s inaugural Esports World Cup features a record USD 70 million purse, amplifying global viewership and sponsorship inflow. Complementing this, Abu Dhabi’s USD 40 million partnership with Ninjas in Pyjamas embeds talent academies and broadcast studios, turning esports into a vocational track . Venue construction and production spending ripple into hospitality and media sectors, reinforcing governments’ non-oil GDP aspirations.

Increase in Arabic-Localized AAA and Indie Content Driving Gen-Z Engagement

Roughly 375 million Arabic-speaking gamers display longer retention when narratives, UI and character arcs reflect regional culture. Right-to-left text rendering, voice-over dialects and culturally appropriate avatars require co-development with local scriptwriters, spawning partnerships between global publishers and Jordanian or Lebanese studios. The demographic skew—89% of Saudis are under 30—creates sustained demand for titles mirroring contemporary Middle Eastern life. As localization matures, role-playing and story-rich genres—historically niche—are climbing the download charts and opening premium-priced DLC opportunities.

Proliferation of Digital Wallets and Carrier Billing Boosting In-Game Microtransactions

Carrier billing sidesteps low credit-card penetration across parts of the GCC and Turkey, enabling one-tap micro-payments that lift average revenue per paying user. Telcos now co-launch wallet brands, embedding game-credit top-ups inside everyday finance apps. Cross-promotion with music and video subscriptions further deepens stickiness, while loyalty schemes reward frequent purchases with data bonuses. The frictionless flow translates into higher basket frequency, allowing publishers to optimize season-pass and skin-sale calendars.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulations on loot boxes and in-game gambling | -1.40% | GCC, Turkey | Medium term (2-4 years) |

| High console hardware import duties | -1.10% | Turkey, Iran | Short term (≤ 2 years) |

| Energy-subsidy reforms lifting data-center opex | -0.80% | GCC core | Long term (≥ 4 years) |

| Economic-sanctions impact on payment processing | -0.60% | Iran | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulations on Loot Boxes and In-Game Gambling Across GCC

Legal definitions of chance-based rewards differ across Saudi Arabia, the UAE and Qatar, forcing publishers to maintain multiple codebases or disable monetization mechanics altogether. The UAE’s distinction between skill and chance means a single patch can trigger re-classification, exposing developers to penalties. Iran’s past blocking of Google Play, which slashed local studio revenue by up to 40%, underscores the volatility. For smaller studios the compliance cost erodes margins, delaying regional launches and limiting content variety.

High Console Hardware Import Duties in Turkey and Iran

Turkey applies special consumption taxes on electronics that can add 20-40% to retail console prices, steering consumers toward mobile titles or PC cafés. Sanctions complicate parts procurement for Iranian distributors, constraining supply and inflating second-hand prices. Consequently, publishers prioritize cross-platform releases and cloud-gaming formats to reach console-oriented audiences without physical imports.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Mobile Dominance Drives Cloud Innovation

Mobile captured 61.30% of the Middle East gaming market in 2025 on the back of ubiquitous smartphones, affordable data bundles and low entry barriers. Cloud services are set to outpace all other formats at a 16.74% CAGR, bridging handset convenience with console-grade visuals by off-loading computation to regional GPU clusters. Console growth lags where import tariffs persist, while PC maintains a stable share through esports and free-to-play ecosystems. The mobile contribution to the Middle East gaming market size is projected to remain above USD 4.8 billion by 2031, even as cloud siphons premium spend. Cross-play via single sign-on keeps players inside publisher ecosystems, boosting lifetime value.

Consumer hours spent on tablets are also climbing as larger screens improve control accuracy for strategy and MOBA titles. Meanwhile, smart-TV and set-top-box apps act as secondary access points for family gaming, illustrating how platform lines blur in a cloud-first future. For telcos, bundling unlimited gaming data with 5G home broadband reinforces churn-reduction strategies.

By Revenue Model: Subscription Growth Challenges F2P Dominance

Free-to-play still commanded 62.10% revenue share in 2025, but game-pass subscriptions are sprinting at an 17.65% CAGR as exclusive libraries and zero-ads tiers gain traction. The Middle East gaming market size for subscriptions could exceed USD 1.92 billion by 2031 if current uptake persists. Microtransaction success is fueled by carrier billing, with operators taking single-digit revenue shares in exchange for frictionless payments. Hybrid monetization is emerging: titles launch as F2P, then upsell cosmetic passes or PvE expansions via monthly packs.

Advertising-only models decline as privacy regulation curtails third-party tracking. Instead, rewarded video formats and in-house ad networks fill gaps, keeping CPI acquisition costs manageable for indie studios.

By Gamer Type: Professional Esports Drives Engagement

Casual users constitute 65.60% of players, generating breadth of DAU but lower ARPU. Professional athletes, growing at 18.92% CAGR, draw sponsorship dollars and media-rights revenue, key levers for platform profitability. The Middle East gaming market share captured by pro and semi-pro gamers is projected to reach 8.8% by 2031 as state-funded leagues expand. Mid-core players provide a stable bridge, toggling between mobile convenience and PC depth, and serve as early adopters of subscription bundles.

Government-sponsored academies in Riyadh and Abu Dhabi run scouting programs, while prize pools surpassing USD 70 million elevate esports to mainstream entertainment. Streaming deals with regional broadcasters push viewership beyond Twitch and YouTube, tapping households that prefer Arabic commentary.

By Genre: Battle Royale Leadership Faces RPG Challenge

Shooter and battle-royale games achieved a 34.60% share in 2025, retaining dominance through frequent live-ops events and influencer-driven marketing. Role-playing titles are advancing at a 13.58% CAGR as deeper localization, including dialogue tailored to Gulf dialects, reduces cultural friction. The Middle East gaming market size attributed to RPGs is expected to double by 2030 amid demand for character-driven plots. Sports, racing and simulation genres gain incremental momentum via licensed regional tournaments and local athlete endorsements.

Persistent-world mechanics and cross-platform progression keep engagement highs; publishers deploy AI moderation to ensure community safety, a feature increasingly required by regulators.

Geography Analysis

Saudi Arabia’s 33.40% leadership is underpinned by a USD 38 billion public-investment roadmap and marquee events such as the Esports World Cup’s USD 70 million prize pool. PIF’s Niantic takeover externalizes Saudi IP influence, while NEOM’s planned gaming cluster promises 30,000 jobs. Steam concurrent user data shows Riyadh delivering the region’s highest weekend peak, indicating a consumption base ready for premium PC and cloud licenses.

In the UAE, Dubai’s Gaming 2033 program forecasts USD 1 billion GDP contribution and 30,000 new roles, supported by the emirate’s digital-free-zone visas that ease talent import. The federal gaming regulator’s first casino license to Wynn Resorts in Ras Al Khaimah broadens monetization possibilities and may spur adjacent in-game wagering frameworks. Abu Dhabi’s twofour54 free zone offers 100% foreign ownership for studios, catalyzing inbound FDI.

Kuwait’s telecom-grade average download speed of 250 Mbps empowers high-definition mobile esports. Attractive ARPU levels drive publishers to soft-launch titles there before wider GCC rollout. Turkey, while facing Lira volatility and 20-40% console tariffs, remains resilient through mobile esports; Dream Games’ USD 2.75 billion valuation underscores local creative capacity. Iran’s platform bans route consumers to domestic app stores; yet the absence of Google Play’s commission structure ironically lifts developer margins for ad-supported releases.

Bahrain, Qatar and Oman represent emerging clusters where government innovation hubs and fintech sandboxes intersect with gaming. Jordan’s Tamatem demonstrates how a lean Arabic-first studio can scale to 150 million downloads, highlighting localization’s export potential.

Competitive Landscape

Ownership shifts driven by sovereign wealth funds are redrawing the competitive map. PIF’s USD 3.5 billion Niantic deal vaults Saudi Arabia into augmented-reality leadership and adds proprietary location-based tech to its portfolio. Tencent, Sony and Microsoft maintain global catalog depth but must negotiate localization and billing partnerships to resonate with Arabic users. Regional independents such as Tamatem and Boss Bunny exploit cultural proximity to secure IP licenses from the West, then re-skin mechanics for local audiences, capturing loyalty without the overhead of full triple-A production.

Infrastructure providers act as silent power players. Ooredoo’s Nvidia GPU grids supply white-label streaming capacity to smaller publishers, weaving a multi-tenant fabric that lowers entry barriers. E-commerce giants are also testing direct-to-consumer launchers, leveraging payment data to refine targeting.

The market remains moderately fragmented: top five publishers account for roughly 25% combined revenue, leaving room for local breakouts. Strategic moves—state equity stakes, cloud hosting alliances, and IP-localization deals—will decide share shifts over the next cycle.

Middle East Gaming Industry Leaders

Tencent Holdings Ltd.

NetEase Inc.

Shanghai miHoYo Network Technology Co. Ltd.

Perfect World Co. Ltd.

37 Interactive Entertainment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Saudi Arabia’s PIF acquires Niantic for USD 3.5 billion, expanding its mobile-AR portfolio and signaling sustained outbound M&A.

- January 2025: Abu Dhabi secures a USD 40 million partnership with Ninjas in Pyjamas to create a regional esports HQ.

- January 2025: Saudi Arabia’s National Development Fund launches an USD 80 million financing window for studios and tournament operators.

- January 2025: Sandbox VR inks a franchise agreement with Apparel Group to open 25 Middle-East venues by 2027.

Middle East Gaming Market Report Scope

Gaming is defined as playing electronic games conducted through multiple varieties of means, such as using computers, smartphones, consoles, or other mediums altogether. There is an increasing prevalence of high-speed internet connections, especially in emerging economies, which has made online gaming practical for more people in recent years. The market witnessed rapid growth in terms of users and games being downloaded primarily due to the outbreak of the COVID-19 pandemic.

The Middle East Gaming Market is segmented by Platform (Browser PC, Smartphone, Tablet, Gaming Console, and Downloaded Box/PC), Country (United Arab Emirates, Saudi Arabia, Turkey, Iran, Kuwait, and the Rest of Middle East). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

By Platform

| Mobile (Smartphone, Tablet) |

| Cloud / Streaming |

| Console |

| PC (Browser, Download/Box) |

By Revenue Model

| Free-to-Play (F2P) |

| Pay-to-Play / Premium |

| Subscription and Game-Pass |

By Gamer Type

| Casual Gamers |

| Mid-Core Gamers |

| Professional / E-Sports Athletes |

By Genre

| Action/Adventure |

| Shooter and Battle Royale |

| Role-Playing (RPG/MMORPG) |

| Sports and Racing |

| Others |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Turkey |

| Iran |

| Kuwait |

| Rest of Middle East (Bahrain, Qatar, Oman, Jordan, Lebanon, Iraq, Yemen) |

| By Platform | Mobile (Smartphone, Tablet) |

| Cloud / Streaming | |

| Console | |

| PC (Browser, Download/Box) | |

| By Revenue Model | Free-to-Play (F2P) |

| Pay-to-Play / Premium | |

| Subscription and Game-Pass | |

| By Gamer Type | Casual Gamers |

| Mid-Core Gamers | |

| Professional / E-Sports Athletes | |

| By Genre | Action/Adventure |

| Shooter and Battle Royale | |

| Role-Playing (RPG/MMORPG) | |

| Sports and Racing | |

| Others | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Iran | |

| Kuwait | |

| Rest of Middle East (Bahrain, Qatar, Oman, Jordan, Lebanon, Iraq, Yemen) |

Key Questions Answered in the Report

What is the current size of the Middle East gaming market?

The market stands at USD 5.14 billion in 2026 and is set to reach USD 9.32 billion by 2031.

Which segment is growing fastest within the region?

Cloud and streaming platforms are expanding at a 16.74% CAGR thanks to 5G and regional GPU deployments.

Why is Saudi Arabia leading regional market share?

Large-scale sovereign funding, acquisitions such as Niantic and record esports prize pools give the Kingdom a 33.40% share.

How are telcos influencing monetization?

Operators bundle subscription passes, enable carrier billing and deploy edge infrastructure to capture a portion of in-game revenue.

What regulatory issues most affect publishers?

Inconsistent loot-box rules across GCC states and high console import duties in Turkey and Iran pose the greatest compliance and cost challenges.

Is localization important for success in the region?

Yes. Games that integrate Arabic language, cultural motifs and region-specific social features show higher retention and spending metrics.

Page last updated on: