Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

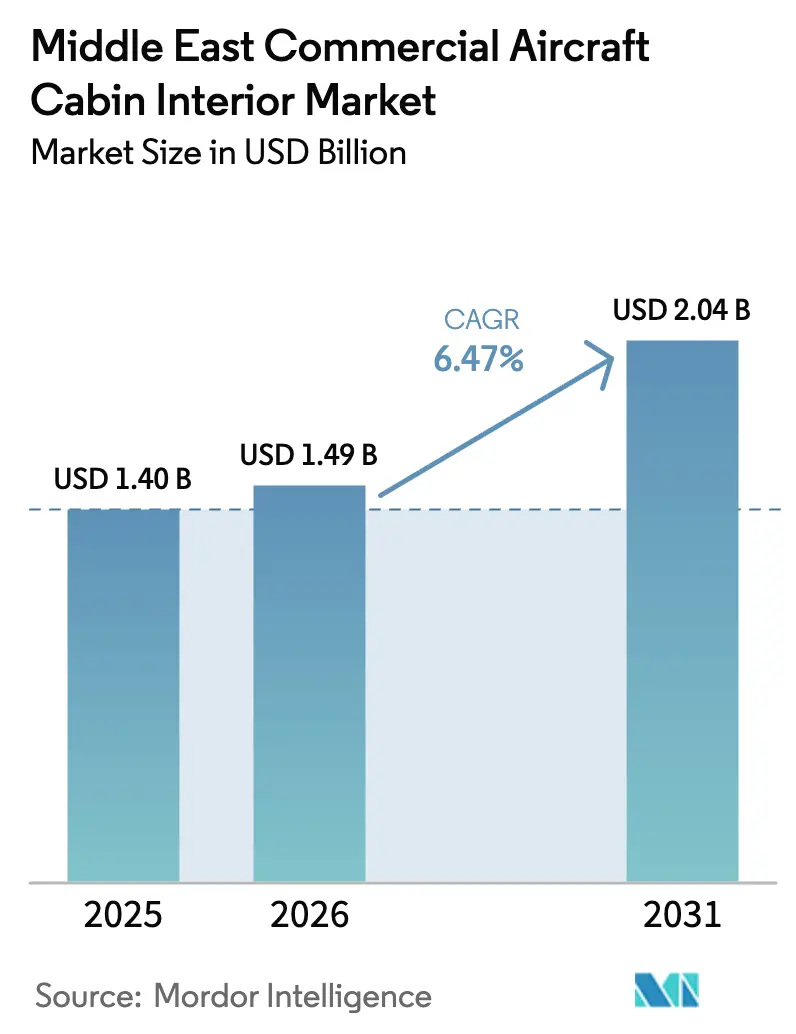

| Base Year Market Size (2025) | USD 1.40 Billion |

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 2.04 Billion |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Commercial Aircraft Cabin Interior Market Analysis by Mordor Intelligence

The Middle East commercial aircraft cabin interior market size was valued at USD 1.40 billion in 2025 and estimated to grow from USD 1.49 billion in 2026 to reach USD 2.04 billion by 2031, at a CAGR of 6.47% during the forecast period (2026-2031). Sustained fleet expansion by Gulf carriers, a post-2024 tourism resurgence, and mounting premium-travel expectations underpin this trajectory. Composite material adoption, smart-cabin technologies, and regulatory pressure for lighter, greener cabins further reinforce demand. Saudi Vision 2030 programs, including NEOM’s bespoke VVIP requirements, reshape procurement toward ultra-premium configurations. Meanwhile, supply-chain diversification, localized MRO capabilities, and predictive-maintenance platforms position suppliers for aftermarket growth. Competitive intensity remains moderate as global majors and niche innovators target differentiated seating, in-flight entertainment and connectivity (IFEC), and sustainable material solutions to capture share across the Middle East commercial aircraft cabin interior market.

Key Report Takeaways

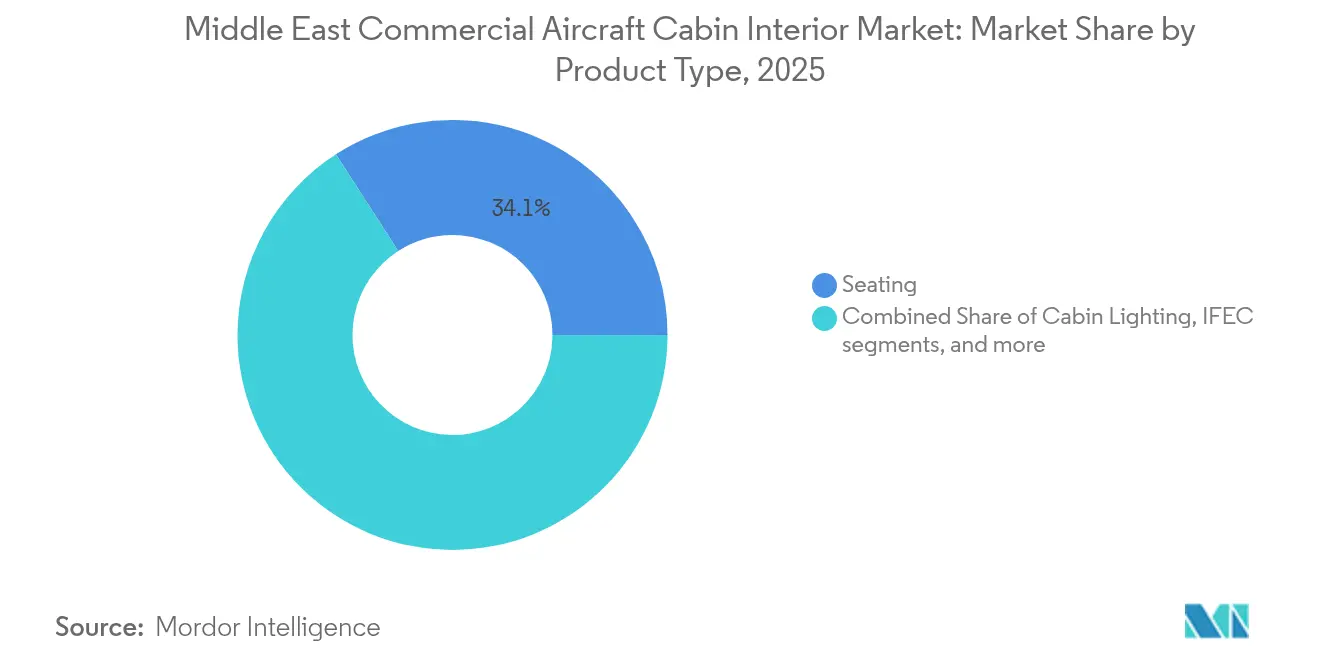

- By product type, seating led the Middle East commercial aircraft cabin interior market with a 34.12% revenue share in 2025; IFEC is projected to expand at an 8.63% CAGR to 2031.

- By aircraft type, narrowbodies held 57.35% of the Middle East commercial aircraft cabin interior market size in 2025, while widebodies recorded the fastest CAGR at 6.82% through 2031.

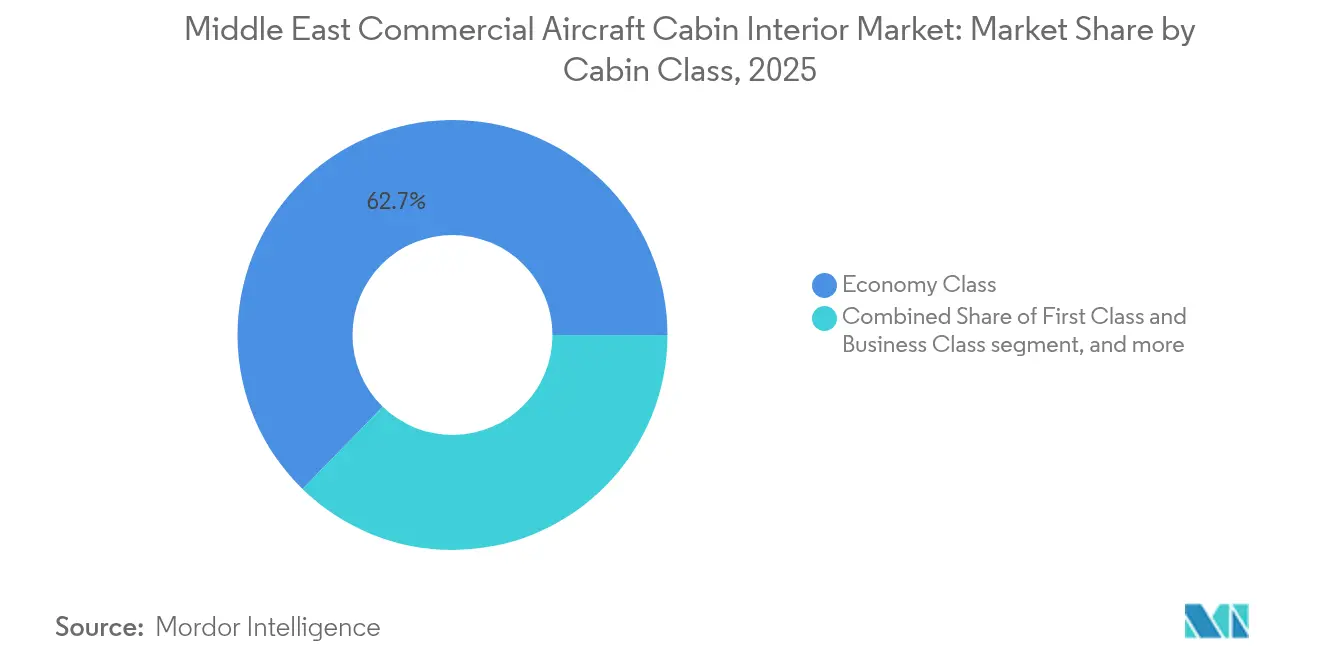

- By cabin class, the economy accounted for a 62.71% share of the Middle East commercial aircraft cabin interior market in 2025, and premium cabins are advancing at an 8.02% CAGR through 2031.

- By fit type, OEM installations represented 72.60% of the Middle East commercial aircraft cabin interior market share in 2025; aftermarket services are growing at a 7.87% CAGR to 2031.

- By geography, Saudi Arabia captured 42.20% of the Middle East commercial aircraft cabin interior market share in 2025, while Qatar posts the highest CAGR at 8.11% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Commercial Aircraft Cabin Interior Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gulf carriers’ fleet-expansion programs | 1.80% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Premium-travel experience expectations | 1.20% | Gulf states | Short term (≤ 2 years) |

| Regulatory push for lighter, greener cabins | 0.90% | Region-wide | Long term (≥ 4 years) |

| Post-2024 tourism boom | 1.10% | Saudi Arabia, UAE | Short term (≤ 2 years) |

| Saudi giga-projects driving bespoke VVIP demand | 0.70% | Saudi Arabia | Medium term (2-4 years) |

| Smart-material adoption enabling predictive maintenance | 0.60% | Early-adopter carriers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Gulf Carriers’ Fleet-Expansion Programs

More than 795 aircraft sit in the region’s collective orderbooks, led by Emirates’ 200-unit backlog and Saudi Airlines’ plan to double its fleet to 381 jets by 2032.[1]Angus Batey, “Middle East carriers sign record orders at Dubai,” Aviation Week, aviationweek.com These deliveries are expected to accelerate the Middle East commercial aircraft cabin interior market, as airlines demand turnkey cabins for new builds and early retrofits. Widebody orders from Qatar Airways amplify premium-cabin requirements, prompting suppliers to localize production to meet volume and customization needs. The scale of these programs justifies dedicated regional certification and testing centers, shrinking lead times while strengthening supplier–airline partnerships. The resulting demand encompasses seating, IFEC, lighting, and smart-cabin systems, bolstering OEM revenue pipelines and fueling aftermarket upgrades over the next decade.

Premium-Travel Experience Expectations

Regional carriers hold a 14.7% global share of premium traffic, prompting cabin specifications that exceed industry norms. Riyadh Air’s debut cabin showcases Safran Unity business seats, RECARO economy models, and Panasonic’s MI platform, reflecting a shift from service-based differentiation to technology-enabled personalization.[2]Source: “Riyadh Air unveils cabin featuring Safran Unity,” Panasonic Avionics Press Release, panasonic.aero Modular designs allow rapid reconfiguration, aligning capacity with seasonal demand spikes. Suppliers integrating IoT sensors, AI-based preference engines, and immersive lighting gain priority in carrier RFPs. Heightened passenger expectations extend to premium economy, driving demand for hybrid seating that bridges comfort gaps without eroding business-class yields.

Post-2024 Tourism Boom

Saudi Arabia aims to target 300 million passengers annually by 2030, nearly triple the 2024 volumes, catalyzing fleet growth and interior refresh cycles.[3]Source: General Authority of Civil Aviation, “Sustainability Roadmap,” gaca.gov.sa Expanded airport capacity, led by King Salman International Airport’s 120 million-passenger goal, supports higher aircraft utilization, accelerating wear-and-tear replacements. NEOM Airlines’ sustainability-focused cabin blueprint highlights the role of tourism in advancing material and technological standards. Airlines upgrade cabins to capture higher-yield travelers lured by destination marketing, thereby enhancing the revenue mix of the Middle East commercial aircraft cabin interior market toward premium products and connected-cabin ecosystems.

Regulatory Push for Lighter, Greener Cabins

Alignment with EASA sustainability rules drives carriers to substitute aluminum and steel with composites and advanced thermoplastics. Collins Aerospace’s SWITCH prototype, finalized in October 2024, demonstrates weight savings and end-of-life recyclability. Environmental pledges in national aviation strategies incentivize airlines to pay premiums for materials that reduce fuel consumption and support circular economy goals. Suppliers offering traceable, bio-based inputs secure long-term contracts, reinforcing the shift toward greener interiors in the Middle East commercial aircraft cabin interior market.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Composite-material supply disruptions | -0.80% | Global chains, regional assembly | Short term (≤ 2 years) |

| Lengthy certification cycles | -0.60% | Region-wide | Medium term (2-4 years) |

| Cyber-security risks in connected IFEC | -0.40% | Gulf states | Long term (≥ 4 years) |

| Limited regional composite-repair MRO capacity | -0.50% | Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Composite-Material Supply Disruptions

Raw-material shortages and geopolitical friction are stretching lead times for composites, which account for a 47.90% share of the global demand for cabin materials. Airlines face delivery pushbacks or must pivot to heavier substitutes, jeopardizing fuel-saving targets. Sparse regional repair shops exacerbate lifecycle costs, as damaged components require replacement rather than refurbishment. Suppliers prioritize established programs over new thermoplastic lines, constraining the fastest-growing 8.78% CAGR material segment and tempering growth in the Middle East commercial aircraft cabin interior market.

Lengthy Certification Cycles

Additional validation steps between GACA and international regulators prolong certification by up to 12 months. Smart materials and IoT integrations undergo extensive cyber-resilience checks, delaying their entry into service. Limited local test facilities force rerouting to Europe or North America, which inflates costs and deters the adoption of breakthrough technologies. Airlines tend to favor pre-certified solutions, which slows the diffusion of innovation across the Middle East commercial aircraft cabin interior market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Seating Dominance Masks IFEC Acceleration

Seating retained a 34.12% share in 2025, reinforcing its central revenue role across the Middle East commercial aircraft cabin interior market. In contrast, IFEC systems are projected to outpace the market at an 8.63% CAGR to 2031 as carriers leverage high-speed connectivity for differentiation. Suppliers align modular seat architecture with next-gen displays and personalized content hubs, ensuring cabin coherence and future-proofing retrofit programs.

Cabin lighting, galleys, and lavatories post steady, replacement-driven demand, while overhead bins shift toward ultra-light composites. Emerging smart-cabin subsystems, bundled under “Others,” integrate sensors and AI to streamline maintenance and enhance ambiance, expanding the addressable revenue pool.

By Aircraft Type: Narrowbody Volume Versus Widebody Value

Narrowbodies captured 57.35% of the Middle East commercial aircraft cabin interior market size in 2025, supporting dense regional networks. Yet widebodies lead value growth at 6.82% CAGR, propelled by Gulf hubs’ intercontinental routes. Premium seating, large-format IFE screens, and enhanced galleys command higher per-aircraft spend. Suppliers targeting widebody programs secure larger work-packages and stronger aftermarket tails as cabin refresh cycles accelerate.

Regional transporters occupy a niche in domestic and point-to-point Gulf services, requiring lighter-weight interiors that prioritize quick-turn maintenance over luxury. Nevertheless, their fleet replacements sustain baseline demand within the Middle East commercial aircraft cabin interior market.

By Cabin Class: Economy Scale Enables Premium Growth

Economy class, with a 62.71% share, underpins fleet economics, while first and business classes expand at an 8.02% CAGR through 2031, driven by premium travel momentum. Premium economy gains traction, offering upsell potential without cannibalizing business class yields. Seating vendors craft hybrid designs that scale from economy to premium, easing airline reconfiguration between leisure and business peaks.

Advanced IFEC and personalized lighting migrate from premium to economy cabins as unit costs fall, broadening technology adoption and elevating passenger expectations market-wide. This trickle-down effect drives continuous innovation and supports diversified revenue streams in the Middle East commercial aircraft cabin interior market.

By Fit Type: OEM Leadership Faces Aftermarket Challenge

OEM installations accounted for 72.60% of 2025 revenue, reflecting a robust new-delivery pipeline. However, a 7.87% CAGR in aftermarket services highlights maturing fleets and rising MRO sophistication. Regional players, such as Etihad Engineering and Saudia Technic, invest in cabin-upgrade lines, capturing value once the products are exported to Europe or Asia. Predictive-maintenance add-ons unlock recurring revenue, encouraging suppliers to bundle hardware with analytics subscriptions across the Middle East commercial aircraft cabin interior market.

By Material: Composite Leadership Enables Thermoplastic Innovation

Composites retained a 39.74% share, while advanced thermoplastics posted the highest 8.65% CAGR due to increased recyclability and regulatory support. Bio-based fibers and flame-retardant resins are gaining traction as airlines track their Scope 3 emissions. Aluminum and steel persist where durability outweighs the weight penalties, though innovation pressure accelerates the adoption of alternative materials.

Geography Analysis

Saudi Arabia’s 42.20% share reflects Vision 2030’s aviation ambitions, the scale of King Salman International Airport, and NEOM’s VVIP demand, ensuring a consistent order flow. The national regulator’s alignment with global standards reassures suppliers about certification pathways, fostering localized production partnerships to serve the Middle East commercial aircraft cabin interior market.

Qatar advances at an 8.11% CAGR driven by Qatar Airways’ widebody acquisitions and unwavering premium strategy. Premium-heavy fleets demand sophisticated cabins with top-tier IFEC, reinforcing high per-aircraft spend. Rapid regulatory approvals enable quick rollouts of cabin refreshes, making Qatar a bellwether for next-generation interiors.

The UAE remains influential through Emirates and Etihad, while Kuwait, Oman, and Bahrain present smaller but stable opportunities, anchored by carrier fleet renewal cycles. Emerging Middle East states are expected to add incremental growth, although access barriers and infrastructure gaps are likely to temper the near-term impact. Expanding MRO footprints in Dubai, Bahrain, and Amman strengthen regional aftermarket capacity, raising competitive stakes across the Middle East commercial aircraft cabin interior market.

Competitive Landscape

Safran SA, Collins Aerospace (RTX Corporation), RECARO Aircraft Seating GmbH & Co. KG (RECARO Holding GmbH), Panasonic Holdings Corporation, and Diehl Stiftung & Co. KG vie with each other as carriers seek differentiated premium products. Safran’s USD 1.2 billion Emirates deal, Unity seats on Riyadh Air, and Mubadala manufacturing pact establish end-to-end regional coverage. Panasonic’s Converix launch embeds AI analytics, locking in long-term IFEC revenues and cross-selling cabin-management modules.

Moderate fragmentation persists: the top five suppliers share 58% revenue, leaving room for niche disruptors. Lightweight-seat pioneer Expliseat leverages 30% weight savings to penetrate narrowbody lines, while Diehl Aviation’s Dubai facility targets rapid customization requests. Cybersecurity certifications and sustainability metrics emerge as decisive bid criteria, intensifying R&D investment across the Middle East commercial aircraft cabin interior market.

Middle East Commercial Aircraft Cabin Interior Industry Leaders

Collins Aerospace (RTX Corporation)

Diehl Stiftung & Co. KG

Panasonic Holdings Corporation

RECARO Aircraft Seating GmbH & Co. KG (RECARO Holding GmbH)

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Panasonic Avionics Corporation announced that Riyadh Air is set to be the inaugural airline to debut its cutting-edge IFE tool named Modular Interactive (MI). As the industry's pioneering interactive authoring platform, MI epitomizes Panasonic Avionics' ambition to transform the in-flight experience. The tool aims to establish a dynamic digital "seat back" channel for airlines, aligning seamlessly with other guest touchpoints.

- February 2025: Diehl Aviation inaugurated its new facility in the Dubai Airport Freezone. Spanning 1,100 sqm, the facility is located in the airport's logistics hub within its free trade zone. With this new setup, Diehl can conduct the final assembly, finishing touches, rework, and delivery of select cabin components directly on-site. Being an EASA Part 21G certified manufacturing entity, Diehl Aviation possesses the requisite aviation approvals to certify its products on-site.

Middle East Commercial Aircraft Cabin Interior Market Report Scope

By Product Type

| Seating |

| Cabin Lighting |

| In-flight Entertainment and Connectivity (IFEC) |

| Galley and Monument |

| Lavatory Systems |

| Cabin Windows and Windshields |

| Overhead Stowage Bins |

| Interior Panels and Floorboards |

| Others |

By Aircraft Type

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

By Cabin Class

| First and Business Class |

| Premium Economy Class |

| Economy Class |

By Fit Type

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

By Material

| Composites |

| Aluminum Alloys |

| Steel and Other Alloys |

| Advanced Thermoplastics |

By Geography

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Turkey | |

| Oman | |

| Bahrain | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Product Type | Seating | |

| Cabin Lighting | ||

| In-flight Entertainment and Connectivity (IFEC) | ||

| Galley and Monument | ||

| Lavatory Systems | ||

| Cabin Windows and Windshields | ||

| Overhead Stowage Bins | ||

| Interior Panels and Floorboards | ||

| Others | ||

| By Aircraft Type | Narrowbody Aircraft | |

| Widebody Aircraft | ||

| Regional Jets | ||

| By Cabin Class | First and Business Class | |

| Premium Economy Class | ||

| Economy Class | ||

| By Fit Type | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Material | Composites | |

| Aluminum Alloys | ||

| Steel and Other Alloys | ||

| Advanced Thermoplastics | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Turkey | ||

| Oman | ||

| Bahrain | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Market Definition

- Product Type - Commercial Aircraft cabin interior products such as passenger seats, cabin lighting, inflight entertainment system, cabin windows, lavatories, galley, and stowage bins have been included under the product type in this study.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms