Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

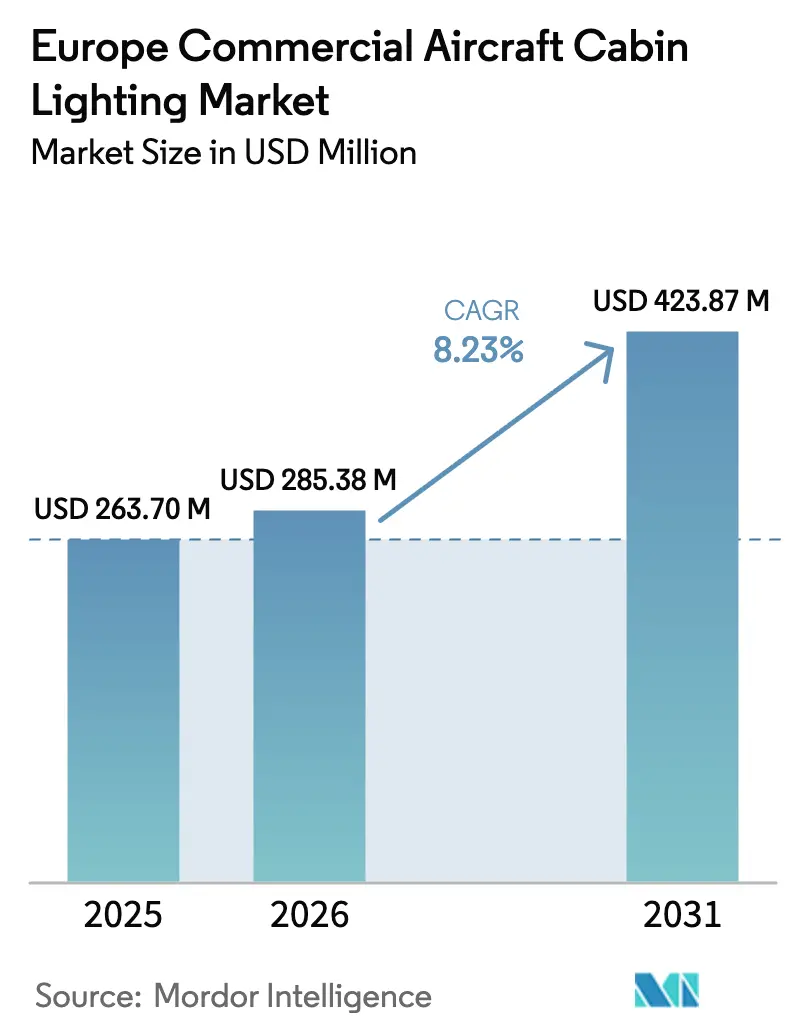

| Base Year Market Size (2025) | USD 263.70 Million |

| Market Size (2026) | USD 285.38 Million |

| Market Size (2031) | USD 423.87 Million |

| Growth Rate (2026 - 2031) | 8.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Commercial Aircraft Cabin Lighting Market Analysis by Mordor Intelligence

Market Analysis

The European commercial aircraft cabin lighting market size in 2026 is estimated at USD 285.38 million, growing from 2025 value of USD 263.70 million with 2031 projections showing USD 423.87 million, growing at 8.23% CAGR over 2026-2031. Recovery in passenger demand, large-scale fleet renewals, and Fit-for-55 energy-efficiency targets elevate cabin-lighting investment, primarily LED retrofits that cut on-board electrical load and maintenance labor. Airlines treat lighting as an operational lever and a brand signature, deploying dynamic color programs that differentiate service without adding seat weight. OEM delivery delays funnel capital toward in-service upgrades, so specialist retrofit suppliers gain momentum. Finally, narrowbody growth sustains baseline volume while widebody retrofits raise average value per aircraft as operators chase circadian-rhythm functionality on long-haul flights.

Key Report Takeaways

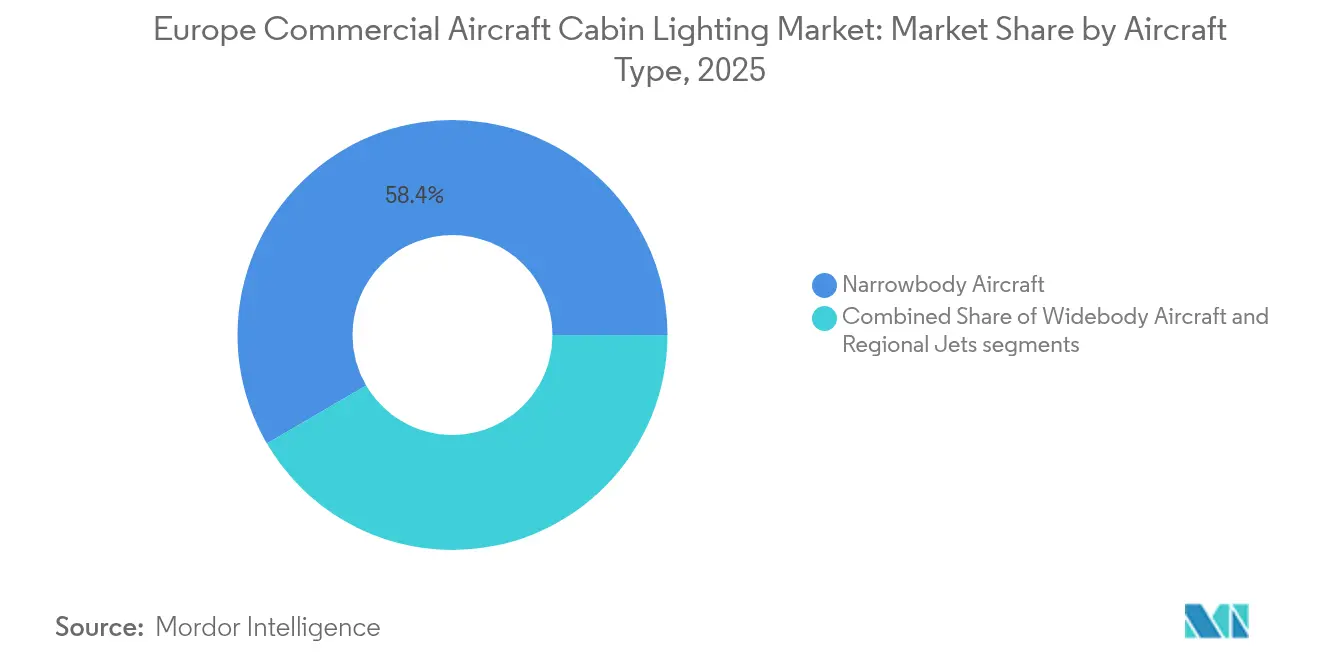

- By aircraft type, narrowbody jets led the European commercial aircraft cabin lighting market with a 58.42% share in 2025, whereas widebody aircraft are expected to post the fastest growth of 7.05% CAGR through 2031.

- By light type, ceiling and wall fixtures captured 31.12% of the European commercial aircraft cabin lighting market size in 2025; emergency floor-path strips are forecasted to expand at a 6.73% CAGR to 2031.

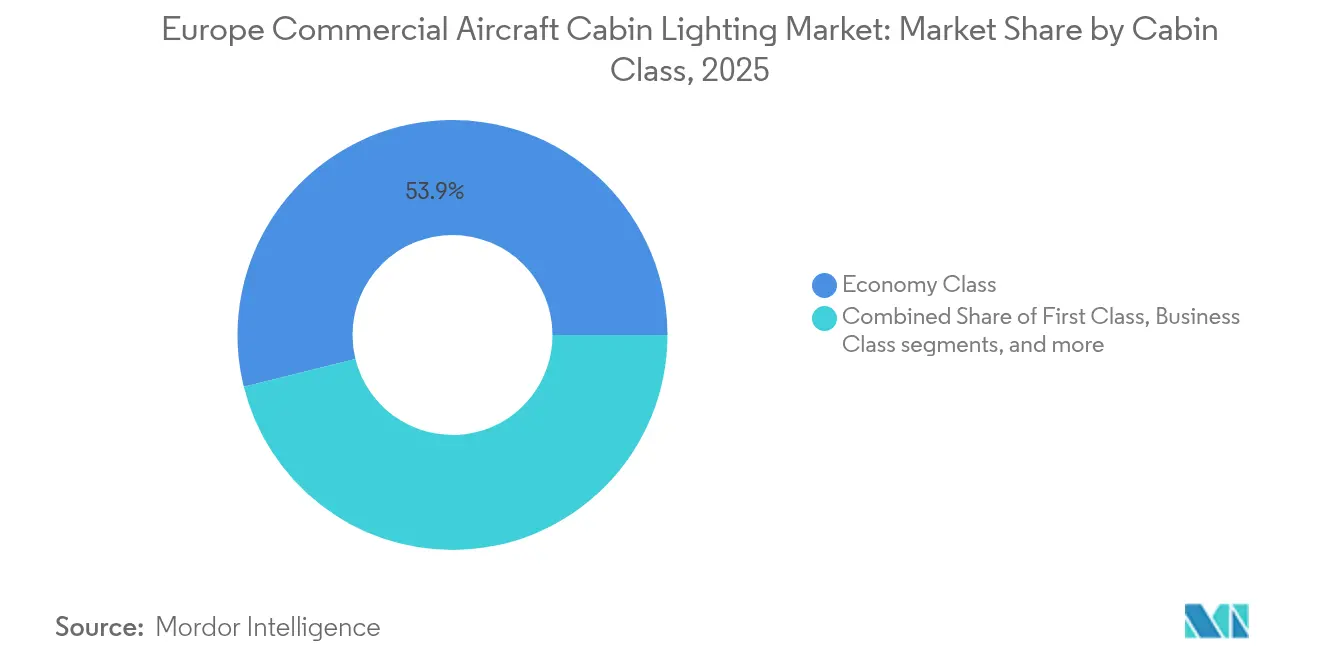

- By cabin class, economy rows represented 53.86% of 2025 installations, but business-class systems are on track for the highest 7.16% CAGR.

- By end user, OEM linefit held 51.83% share in 2025, while aftermarket activity is rising at a 7.66% CAGR as operators refurbish aging fleets.

- By geography, Germany dominated with 27.54% revenue in 2025; Turkey will deliver the quickest 8.04% annual growth to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Commercial Aircraft Cabin Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising narrowbody aircraft deliveries in Europe | +1.2% | Germany, France, Spain | Medium term (2-4 years) |

| Fleet-wide LED retrofits to cut power and maintenance | +1.8% | Pan-European, strongest Western Europe | Short term (≤ 2 years) |

| Airline brand-differentiation through mood lighting | +1.1% | Premium hubs across Europe | Medium term (2-4 years) |

| EU “Fit-for-55” energy-efficiency mandates | +0.9% | EU-27 plus United Kingdom | Long term (≥ 4 years) |

| Lighting tuned for in-flight e-commerce displays | +0.8% | Northern Europe digital-first markets | Long term (≥ 4 years) |

| Circadian-rhythm lighting for ultra-long-haul flights | +0.5% | Germany, Netherlands, United Kingdom hub carriers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Narrowbody Deliveries in Europe

The backlogs of A320neo and B737-8 extend to 2030, prompting carriers to secure early production slots even as supply chains remain tight. Each new narrowbody leaves the factory with fully integrated LED suites that cut electrical draw versus legacy halogen kits, raising the baseline penetration of efficient lighting. The dense intra-Europe network keeps daily utilization above 10 cycles, accelerating lamp-life savings and amplifying retrofit justification on older frames. Aircraft lessors prefer standardized, low-maintenance interiors, so they stipulate LED packages in lease return conditions, ensuring uptake across both flag and budget carriers. Finally, the higher seating density of narrowbodies means a single family order can shift regional demand curves, magnifying the driver’s 1.2% positive effect on the forecast.[1]EUROCONTROL, “European Aviation 2024 Snapshot,” eurocontrol.int

Fleet-wide LED Retrofits to Cut Power and Maintenance

European operators push LED conversions because the technology slashes cabin-power consumption by up to 75%, extending mean-time-between-failure to 50,000 flight-hours.[2]STG Aerospace, “ArkeFly Completes LED Retrofit,” stgaerospace.com Cost models show 18-24-month paybacks through combined fuel burn and lamp-replacement avoidance, a metric that satisfies even cash-focused low-cost carriers (LCCs). EASA Part-145 approvals permit night-stop installation, protecting tight schedule integrity for aircraft that average 11-hour daily utilization. Integrated modules also reduce spares inventory because one LED board replaces multiple bulb variants, freeing warehouse space at line stations. This clear operational upside explains the driver’s top 1.8% uplift on the region’s CAGR.

Airline Brand-differentiation Through Mood Lighting

Full-service airlines weaponize cabin lighting as an emotional branding layer that passengers can see and remember. Lufthansa’s Allegris program times warm hues with boarding, cool neutrals during cruise, and sunrise tones before arrival, reinforcing a premium narrative without structural seat changes.[3]Lufthansa Group, “Allegris Cabin Concept,” lufthansagroup.com SWISS Senses synchronizes light cycles with meal phases, giving the crew an intuitive environmental cue to manage service rhythm. These distinctive palettes become visual trademarks in social-media imagery, amplifying unpaid brand reach while raising Net Promoter Scores. Because the systems ride on existing LED hardware, incremental investment is primarily in software, widening adoption among mid-tier carriers that now compete on passenger sentiment rather than seat pitch alone.

EU Fit-for-55 Energy-efficiency Mandates

Although the legislative pack centers on emission trading and sustainable aviation fuel quotas, airlines exploit cabin electrical savings to demonstrate early wins in compliance dashboards.[4]European Commission, “Fit for 55,” ec.europa.eu Lighting upgrades yield quantifiable kilowatt-hour cuts that feed directly into reported Scope 1 figures, providing quick validation to regulators and investors. National governments link airport slot incentives and reduced navigation charges to visible sustainability actions, nudging lighting projects higher on capital priority lists. Equipment suppliers market carbon-footprint calculators that translate lumen-per-watt improvements into CO₂-equivalent emissions, streamlining shareholder communication. The cumulative policy and reputational benefits anchor the driver’s +0.9% influence on regional CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LCC budget pressure delaying retrofits | –0.7% | Pan-European, strongest Eastern Europe | Short term (≤ 2 years) |

| Certification lead-times for software-controlled lights | –0.4% | EU, EASA jurisdiction | Medium term (2-4 years) |

| Supply-chain risk for rare-earth phosphors | –0.3% | Global supply, EU manufacturing impact | Long term (≥ 4 years) |

| Scope-3 ESG accounting dampening cabin mods | –0.2% | Western Europe sustainability-first markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

LCC Budget Pressure Delaying Retrofits

Ultra-lean operators such as Ryanair adhere to single-class cabins and minimal frills, allocating capital to growth aircraft rather than interior upgrades. Because these fleets already average 8 years of age, CFOs hesitate to invest in systems that may not amortize before retirement. Fuel hedging volatility and local currency swings in Eastern Europe further compress discretionary spending. Board approvals often hinge on demonstrable maintenance savings, yet shorter sector lengths dilute per-flight energy advantages. Consequently, the restraint trims 0.7% off regional CAGR until macro-economic stability returns.

Certification Lead-times for Software-controlled Lights

EASA requires full software hazard analyses for any cabin system that interfaces with power management or passenger devices, adding 12-18 months to approval cycles. Development teams must prepare model-based safety assessments and source-code traceability, inflating engineering budgets. Airlines are wary of program slip, therefore shelve advanced concepts like passenger-selectable color zones. Deferred projects depress near-term demand, especially among smaller suppliers that cannot bankroll lengthy certification without purchase commitments. The knock-on delay represents a –0.4% drag on aggregate market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Narrowbody dominance drives volume

Narrowbody jets held 58.42% of the market share in 2025, benefiting from a fleet base where the A320 and the B737 variants comprise 78% of active frames. This dominance ensures recurring retrofit cycles because high daily utilization accelerates cabin wear, prompting airlines to refresh interiors every five years. Narrowbody operators favor plug-and-play LED kits installed during overnight A-checks, minimizing revenue loss. Although the European commercial aircraft cabin lighting market size tied to narrowbody orders grows steadily, the widebody subclass enjoys a faster 7.05% CAGR as carriers equip aging A330, B777, and A340 fleets with mood and circadian features that raise long-haul yields.

Widebody programs benefit from greater cabin surface area: a single A350 retrofit commands 2-3 times the bill of material of a B737. Airlines justify spending by linking lighting with upgraded business-class suites, boosting ancillary revenue streams such as bid-for-upgrade auctions. Regional and commuter aircraft represent a small slice, but they adopt LED strips mainly for maintenance cost reduction rather than passenger experience. Certification parity under EASA Part-25 keeps safety requirements consistent across airframe sizes, allowing suppliers to repurpose modules between segments, streamlining inventory and training.

By Light Type: Ceiling systems lead while floor-path innovation accelerates

Ceiling and wall fixtures captured 31.12% of the European commercial aircraft cabin lighting market size in 2025 because they deliver the primary illumination canvas that defines perceived cabin spaciousness. Airlines moving to ultra-wide cabins deploy distributed LED panels with tunable white to eliminate dark corners and support biometric boarding facial-capture accuracy. Reading lights evolve into multi-function units that combine directional beams, USB-C ports, and capacitive switches compatible with gloved hands. Emergency floor-path strips post the highest 6.73% CAGR because EASA evacuation-time revisions in 2024 incentivize better way-finding, and photoluminescent hybrids lower battery count in escape-slide packs.

Signage lights expand into multilingual OLED labels that airlines can reprogram when wet-leasing aircraft across jurisdictions, avoiding physical placard swaps. Lavatory modules adopt diffused blue hues that reduce perceived wait anxiety according to passenger-feedback trials. LED technology also mitigates heat load in compact washrooms, decreasing air-conditioning draw. Across every sub-type, suppliers standardize connector types to accelerate seat-map reconfiguration, enhancing fleet flexibility during scheduling peaks.

By Cabin Class: Premium segments drive innovation investment

The economy class accounted for 53.86% installations in 2025 because of seat volume, but most upgrades target energy savings rather than ambiance. Business cabins deliver the highest 7.16% CAGR as operators install individual zone controls, allowing travelers to select reading or relaxation modes without disturbing neighbors. Airlines like Lufthansa embed brand-themed hues that align with corporate identity, ensuring consistent visual language across lounges, boarding bridges, and in-flight service. Premium economy sits between cabins, adopting subtle warm tones during meal service to differentiate product tier at low incremental cost.

Though limited in number, first-class suites function as launch pads for forward-looking concepts such as biometric presence sensors that adjust light intensity based on passenger movement. Successful features migrate downstream once cost curves permit, creating a cascading technology diffusion effect. The European commercial aircraft cabin lighting market share of premium sections should rise modestly as more European carriers reinstate long-haul first-class after pandemic-era suspensions.

By End User: Aftermarket retrofits accelerate past OEM growth

OEM linefit retained 51.83% share in 2025, fueled by backlog deliveries from Airbus and Boeing, where integrated lighting ships under warranty. Yet the aftermarket segment grows at 7.66% CAGR because airlines face 24-month lead times for new aircraft and must refurbish aging cabins to keep Net Promoter Scores competitive. The European commercial aircraft cabin lighting market revenue generated by retrofits benefits from turnkey offerings: STG Aerospace bundles supplemental type certificates, GSE tooling, and crew training into flat-rate packages that slip inside heavy-maintenance visits. Lessors also mandate neutral, modern interiors before lease returns, propelling retrofit volume regardless of airline appetite.

Because aftermarket units must interface with diverse cabin-management systems, suppliers deliver modular controllers with auto-detection software, shortening installation time. Airlines prefer pay-as-you-go service contracts that treat lighting as operational expenditure, freeing capex for widebody engine overhauls. OEMs respond by launching factory-retrofit divisions, yet their cost structures often trail specialists, intensifying price competition.

Geography Analysis

Germany generated 27.54% of European revenue in 2025, anchored by Lufthansa Group’s 750-plus aircraft and the country’s EUR 48.20 billion (USD 55.82 billion) aerospace sector, including Diehl’s lighting hub at Laupheim. Strong technical universities feed a skilled workforce, allowing local suppliers to iterate LED boards quickly and fulfil Lufthansa Technik maintenance slots without import delays. Frankfurt and Munich operate as test beds for circadian-rhythm programs, helping German operators collect quantifiable jet-lag mitigation data. Government R&D incentives reduce prototype costs, accelerating commercialization timelines.

Turkey records the fastest 8.04% CAGR because Turkish Airlines plans to surpass 500 aircraft by 2028, stimulating both linefit and retrofit demand. Istanbul Airport’s status as a tri-continent hub forces carriers to focus on passenger wellness for 12-hour journeys. Local supplier collaborations under Turkey’s National Aviation Plan enable partial component sourcing within the free zone, trimming customs duties and speeding delivery. Regional MRO shops earn EASA Part-145 approvals, positioning Istanbul as a service center for Middle East operators.

France and Spain display steady growth tied to Air France-KLM and Iberia modernization cycles. Both flag carriers integrate lighting upgrades with galley repositioning, leveraging Airbus’s Airspace cabin architecture. Through post-Brexit dual-certification hurdles, the UK maneuvers create modest delays but retain strong engineering capability around Crawley and Belfast. Eastern European members, grouped under Rest-of-Europe, prioritize minimum regulatory compliance due to budget constraints; EU cohesion-fund grants are earmarked for safety equipment, including emergency path lights.

Throughout the continent, EASA harmonization permits a single supplemental type certificate to cover installations across EU and UK registrations, streamlining supplier sales. Cross-border leasing further diffuses LED penetration as aircraft rotate between airlines with differing brand palettes that can be reprogrammed rather than physically replaced.

Competitive Landscape

Innovation and Customer Relations Drive Success

Success in the market increasingly depends on companies' ability to develop innovative lighting solutions that address airlines' needs for energy efficiency, weight reduction, and enhanced passenger experience. Incumbent players are strengthening their market positions by expanding their product portfolios to include sophisticated mood lighting systems, developing more efficient LED technologies, and offering integrated cabin management systems. Companies also focus on building stronger relationships with airlines through customized solutions and comprehensive aftermarket support, while investing in manufacturing capabilities to ensure reliable supply chain operations.

For contenders looking to gain market share, specialization in specific aircraft types or lighting applications offers a viable market entry and growth strategy. Companies increasingly focus on developing proprietary technologies and obtaining necessary certifications to compete effectively. The market's future success factors include the ability to adapt to evolving airline requirements, particularly in terms of sustainability and passenger comfort. Companies must also consider potential regulatory changes regarding standards for aircraft cabin components and environmental regulations, while maintaining strong relationships with aircraft manufacturers and airlines to ensure long-term success in the commercial aircraft interiors market.

Europe Commercial Aircraft Cabin Lighting Industry Leaders

Astronics Corporation

Collins Aerospace (RTX Corporation)

Diehl Stiftung & Co. KG

Safran SA

SCHOTT AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Satair and Collins Aerospace announced a four-year extension of their distribution agreement for cabin interior components. This renewed contract also encompasses lighting solutions.

- March 2025: Diehl Aviation showcased its state-of-the-art cabin illumination technologies at the AIX in Hamburg. These advancements, which include accent lighting and high-quality materials, aim to enhance the passenger experience significantly.

- June 2023: STG Aerospace announced the launch of the Curve, a new flexible cabin lighting product from STG Aerospace's universal lighting family. The Curve is intended for the business jet cabin market.

Europe Commercial Aircraft Cabin Lighting Market Report Scope

Narrowbody, Widebody are covered as segments by Aircraft Type. France, Germany, Spain, Turkey, United Kingdom are covered as segments by Country.By Aircraft Type

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

By Light Type

| Reading Lights |

| Ceiling and Wall Lights |

| Signage Lights |

| Lavatory Lights |

| Floor-path Lighting Strips |

By Cabin Class

| First Class |

| Business Class |

| Premium Economy Class |

| Economy Class |

By End User

| OEM Linefit |

| Aftermarket/Retrofit |

By Geography

| United Kingdom |

| France |

| Germany |

| Spain |

| Turkey |

| Rest of Europe |

| By Aircraft Type | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| By Light Type | Reading Lights |

| Ceiling and Wall Lights | |

| Signage Lights | |

| Lavatory Lights | |

| Floor-path Lighting Strips | |

| By Cabin Class | First Class |

| Business Class | |

| Premium Economy Class | |

| Economy Class | |

| By End User | OEM Linefit |

| Aftermarket/Retrofit | |

| By Geography | United Kingdom |

| France | |

| Germany | |

| Spain | |

| Turkey | |

| Rest of Europe |

Market Definition

- Product Type - The interior lights of aircraft which provide illumination for instruments, cabins, and other sections that are occupied by passengers are included in this study.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms