Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

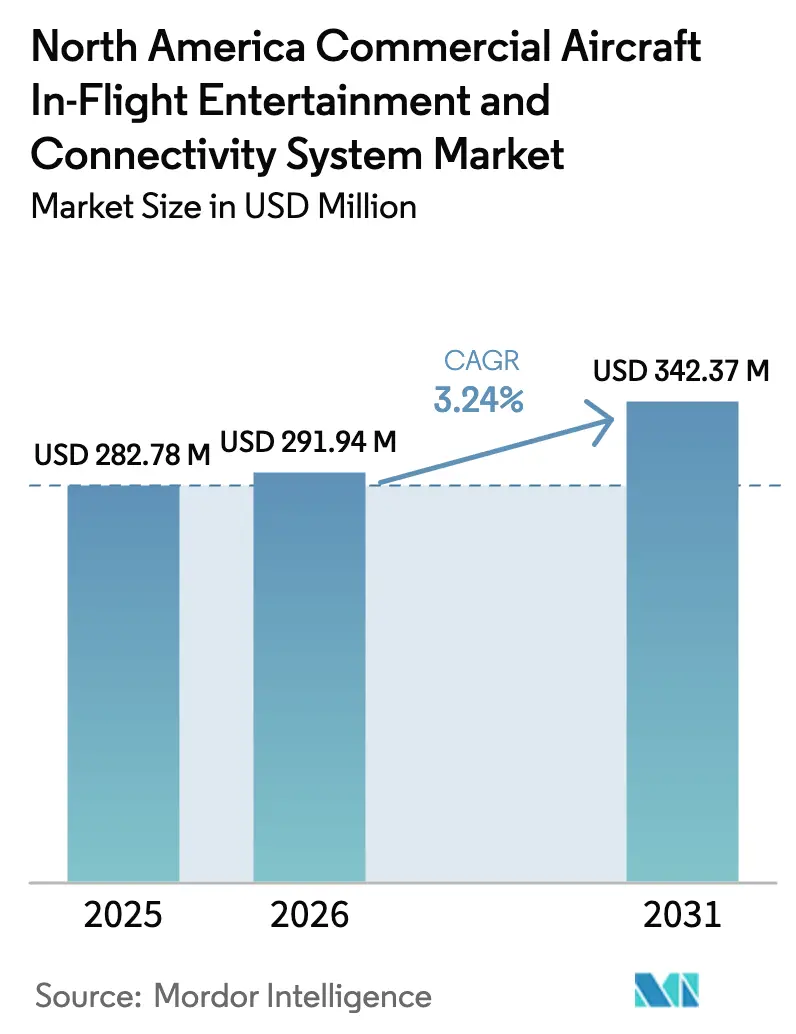

| Base Year Market Size (2025) | USD 282.78 Million |

| Market Size (2026) | USD 291.94 Million |

| Market Size (2031) | USD 342.37 Million |

| Growth Rate (2026 - 2031) | 3.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Commercial Aircraft In-Flight Entertainment And Connectivity System Market Analysis by Mordor Intelligence

The North America commercial aircraft in-flight entertainment and connectivity (IFEC) system market size was valued at USD 282.78 million in 2025 and estimated to grow from USD 291.94 million in 2026 to reach USD 342.37 million by 2031, at a CAGR of 3.24% during the forecast period (2026-2031). Solid passenger traffic recovery, a pivot toward wireless streaming platforms, and a shift in airline focus on generating ancillary revenue underpin this steady trajectory. Airlines are continuing to reduce weight by shifting to wireless systems, freeing up devices, reducing cabin weight, and thereby supporting rapid upgrades for high-bandwidth connectivity. Growing passenger readiness to pay for reliable internet boosts revenue diversification, while premium-economy upgrades help lift yields on mature North American routes. Competitive rivalry centers on integrated hardware-software platforms that merge content, connectivity, and targeted advertising within a single architecture, enabling carriers to monetize every passenger touchpoint. Regulatory accessibility mandates and cybersecurity compliance also shape purchasing criteria, rewarding suppliers that bring certified, future-proof solutions.

Key Report Takeaways

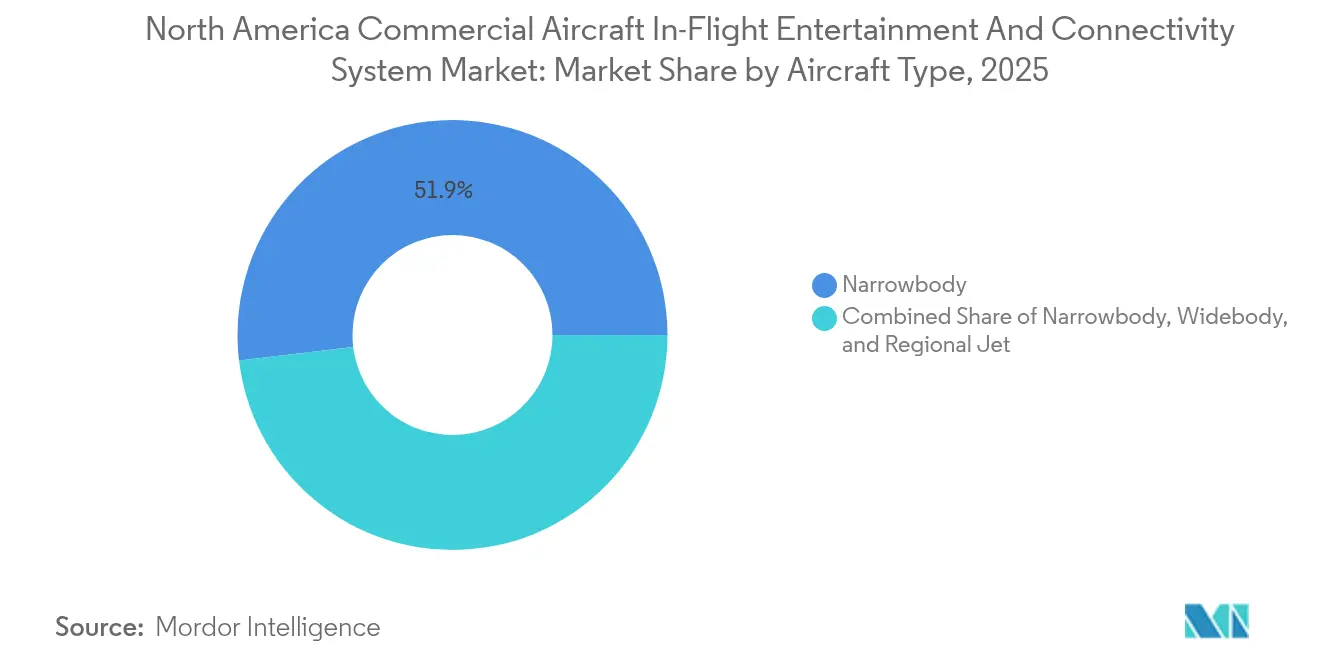

- By aircraft type, narrowbody models held 51.90% of the North America commercial aircraft in-flight entertainment and connectivity (IFEC) system market share in 2025, whereas regional jets are on track for the fastest 6.05% CAGR through 2031.

- By system type, seat-back IFEC platforms led with 51.85% revenue share in 2025; wireless and BYOD solutions are projected to expand at a 7.35% CAGR to 2031.

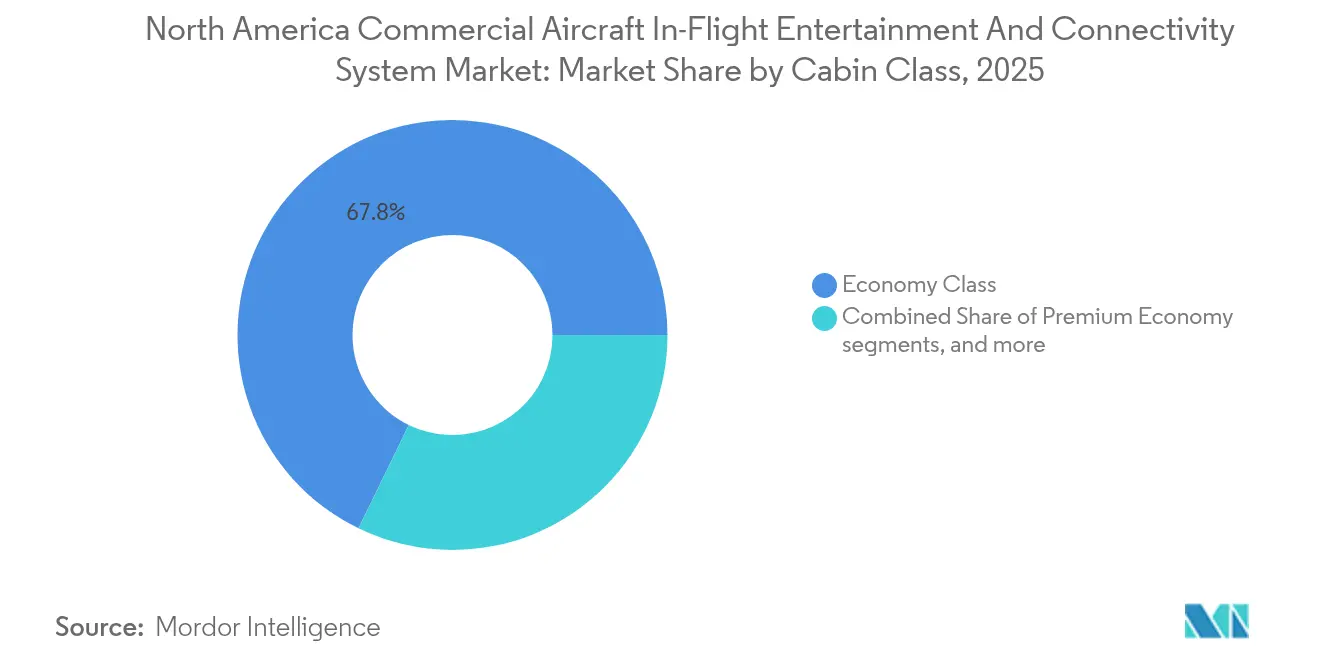

- By cabin class, economy accounted for 67.80% of installations in 2025, while premium economy is projected to advance at a 6.45% CAGR over 2026-2031.

- By fit, OEM solutions commanded a 66.10% share of the North America commercial aircraft in-flight entertainment and connectivity (IFEC) system market size in 2025. In contrast, aftermarket programs are expected to show a 6.78% CAGR outlook.

- By country, the United States is projected to account for the largest share of the North America commercial aircraft in-flight entertainment and connectivity (IFEC) system market in 2025, representing 84.05%, while Canada is expected to hold a 5.90% share.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Commercial Aircraft In-Flight Entertainment And Connectivity System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of wireless streaming IFE systems | +1.2% | United States major hubs | Medium term (2-4 years) |

| Fleet renewal favoring lightweight high-efficiency IFE | +0.8% | United States and Canada | Long term (≥ 4 years) |

| Monetization via targeted ads and e-commerce | +0.9% | United States with spillover to Canada | Short term (≤ 2 years) |

| High-bandwidth Ka-band satellite roll-outs | +1.1% | North America wide | Medium term (2-4 years) |

| Contact-less BYOD solutions post-COVID | +0.7% | Business travel corridors | Short term (≤ 2 years) |

| Accessibility mandates accelerating upgrades | +0.5% | United States | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Rapid Adoption of Wireless Streaming IFEC Systems

Airlines are increasingly viewing wireless platforms as the optimal balance between passenger satisfaction and unit economics. A large US Full-service carrier equipped more than 700 aircraft with streaming solutions that eliminate several hundred pounds of seat-back hardware and reduce maintenance costs by up to 60%. Scalability across mixed fleets shortens deployment cycles from months to weeks, keeping downtime below three days per narrowbody aircraft. Passenger uptake exceeds 85% when free high-speed connectivity is bundled, creating a self-funding model in which lower capital expenditures support higher bandwidth investments. The Commercial aircraft in-flight entertainment system market, therefore, tilts toward software-defined architectures that future-proof fleets against rapid technology refresh.[1]Delta Air Lines, “Wireless IFE Expansion Press Release,” news.delta.com

Fleet Renewal Favoring Lightweight, High-Efficiency IFE

Aircraft from the Airbus A320neo and Boeing 737 MAX lines ship with OLED displays, distributed processing, and native interfaces to cabin management networks. These line-fit architectures reduce power draw by 30-40% compared to prior-generation systems and trim per-seat acquisition costs by a quarter. Airlines avoid the seven- to fourteen-day retrofit outage typical of legacy installations, a decisive advantage for low-margin operators. Regional carriers adopting the new Embraer E2 and Airbus A220 families specify fully integrated entertainment during purchase contracts, preserving cabin commonality and protecting residual asset values.[2]United Airlines, “Kinective Media Launch,” united.com

Monetization via Targeted Ads and E-Commerce

Leading US network airlines harness anonymized passenger data to serve hyper-relevant adverts that deliver click-through rates three to four times higher than web benchmarks. One carrier’s proprietary media platform now generates over USD 100 million in annual advertising revenue, with an average ancillary spend per engaged passenger ranging from USD 45 to USD 65 per flight. Duty-free sales, destination excursions, and seat-upgrade bids are accessible directly from the IFE homepage, converting screen time into high-margin transactions and repositioning entertainment from a fixed cost to a profit center.

High-Bandwidth Ka-Band Satellite Roll-Outs

New multi-terabit Ka-band satellites supply 100 Mbps-plus throughput per aircraft and halve megabit pricing compared with widespread Ku-band service. Consistent cabin speeds above 25 Mbps unlock 4K video streaming and real-time gaming, elevating net promoter scores on long-haul and remote-route operations. Capacity increases support 200 simultaneous users without throttling, enabling tiered pricing models and higher take-rates on premium data packages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High retrofit cost and cabin downtime | -0.9% | North America overall | Medium term (2-4 years) |

| Bandwidth cost and reliability challenges | -0.7% | Regional and rural routes | Short term (≤ 2 years) |

| Cyber-security and data-privacy compliance burden | -0.4% | United States | Long term (≥ 4 years) |

| Passenger preference for personal devices | -0.6% | Younger demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Retrofit Cost and Cabin Downtime

Seat-back retrofits average USD 500,000-1.5 million per aircraft and involve up to two weeks of downtime, equating to another USD 200,000-400,000 in foregone income. Legacy airframes often require structural reinforcements to support modern displays, which can complicate labor hours and certification paperwork. These economics delay upgrade cycles among low-cost and regional operators, nudging them toward lighter wireless alternatives or deferring investment altogether.[3]U.S. Department of Transportation, “Airline Connectivity Cost Study 2024,” transportation.gov

Bandwidth Cost and Reliability Challenges

Annual connectivity bills range from USD 75,000 to USD 150,000 per aircraft, a volatile expense tied to data usage peaks and orbit-coverage surcharges. Weather-related fade, capacity saturation on transcontinental corridors, and service gaps over polar tracks can depress passenger take-rates and refund requests. Carriers deploy throttling or session caps to control spend, but such measures erode user experience and risk negative brand sentiment.[4]Federal Aviation Administration, “Part 382 Accessibility Guidance,” faa.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Narrowbody Stronghold, Regional Jet Momentum

Narrowbodies generated 51.90% of 2025 revenue in the North America commercial aircraft in-flight entertainment and connectivity (IFEC) system market, supported by fleets exceeding 3,500 units across the US majors. Homogeneous cabin layouts simplify wireless rollouts that span over 700 airframes at a single carrier. Widebodies remain important for long-haul networks that demand multi-language, multi-camera seat-back suites with second-screen pairing. Regional jets, however, are expected to show a 6.05% CAGR through 2031, underpinned by up-gauging to 90-seat platforms that merit complete streaming solutions on stage lengths exceeding 90 minutes. Leasing companies are increasingly stipulating factory-installed entertainment to retain remarketing value, further propelling upgrades in this sub-fleet.

Passenger sentiment also drives the shift: satisfaction surveys reveal a 15-point difference between regional flights entertaining and those that are not, influencing airline Net Promoter Scores. Suppliers therefore tailor low-weight servers, seat-pocket wireless chargers, and compact content loaders for Embraer E2 and Mitsubishi SpaceJet cabins. As route mapping expands into secondary US cities, airlines aim to replicate mainline experiences and minimize churn to competing carriers.

By System Type: Wireless Ascendancy Meets Seat-Back Loyalty

Seat-back platforms held a 51.85% share in 2025, owing to their entrenched presence in long-haul cabins, where passengers expect large, high-resolution displays. Content control, closed captions, and accessibility integration remain superior on embedded screens, pushing airlines to keep them in premium and ultra-long-range aircraft. Wireless and BYOD systems, however, register a 7.35% CAGR trajectory as carriers leverage cloud libraries accessible on personal devices. The North America commercial aircraft in-flight entertainment and connectivity (IFEC) system market size for wireless installations on narrowbodies is forecast to surpass USD 156.8 million by 2031, reflecting reduced hardware outlay and minimal downtime during cabin turnarounds.

Hybrid concepts arise: seat-back in premium zones paired with wireless in economy to balance cost and passenger expectations. Airlines allocate hardware savings toward faster satellite links, reinforcing the appeal of streaming content. Accessibility regulations still require captioned media and voice navigation, prompting software-level solutions that draw parity with traditional embedded screens.

By Cabin Class: Economy Scale, Premium Economy Upside

Economy dominates the installed base with a 67.80% share, driven by cabin density and fleet scale. Common wireless portals host basic movies and music free of charge, while high-bandwidth streaming or gaming tiers carry incremental fees that average USD 8-15 per passenger on equipped flights. Premium economy, though smaller, shows the highest 6.45% CAGR as airlines recognize strong elasticity between enhanced IFEC features and willingness to pay 40-100% fare premiums over standard economy. Typical upgrades include 13-inch 4K screens, USB-C charging, and curated regional content.

Business and first-class cabins continue to demand top-tier experiences, including actual 4K resolution, curated studio releases before terrestrial launch, and privacy headsets. Personalization engines push bespoke playlists based on loyalty-program data, deepening engagement and loyalty. The North America commercial aircraft in-flight entertainment and connectivity (IFEC) system market, therefore, evolves from class-based differentiation to data-driven individual tailoring.

By Fit: Original Equipment Manufacturer (OEM) Efficiency versus Aftermarket Necessity

OEM solutions captured 66.10% of the revenue in 2025 as airlines embed entertainment systems during production to avoid later downtime. Integrated wiring harnesses, power management, and seat certification cut per-seat cost by 25-35% and streamline spares logistics. The North America commercial aircraft in-flight entertainment and connectivity (IFEC) system market share for the aftermarket will still expand at a 6.78% CAGR, driven by airlines refreshing the interiors of craft scheduled to fly beyond 2035. Wireless retrofits are installable in two to three calendar days, have a lower barrier to entry, and appeal to operators with slim schedule buffers.

Accessibility upgrades and cybersecurity patches often coincide with cabin refresh programs, ensuring compliance with relevant regulations. Specialized MRO firms grow revenue by offering turnkey retrofit packages that include certification, content services, and post-install maintenance support.

Geography Analysis

The United States accounts for roughly 83-88% of the total North American commercial aircraft in-flight entertainment and connectivity (IFEC) system market installations, owing to its fleet of over 4,000 active aircraft. Robust demand stems from high flight frequencies, rapid Wi-Fi adoption, and intense competition among legacy carriers to differentiate passenger experience. Domestic enplanements now exceed 800 million annually, and customer surveys rank reliable streaming as one of the top three selection criteria, alongside schedule and price. Major carriers lead monetization innovation, introducing media platforms that sell retail, advertising, and destination services through single sign-on portals. These initiatives lift average ancillary yield and justify continuous cabin technology refresh.

Canada contributes approximately 6-10% of regional demand, anchored by a fleet of 400-500 aircraft. Longer average stage lengths magnify the value proposition for robust entertainment, prompting flag carriers to specify the latest generation wireless suites paired with Ka-band connectivity on new A320neo deliveries. Canada’s stringent environmental goals align with lighter IFE designs that curb fuel burn and emissions. Regulatory harmonization with the United States simplifies cross-border fleet sharing and vendor commonality, further stimulating investment.

Cross-border alliances and code-share agreements prompt Aircraft In-Flight Entertainment System carriers to deliver uniform entertainment experiences regardless of the operating airline. The US major carriers partner with regional affiliates flying under shared brands, compelling synchronized content libraries and interface design. This interoperability goal extends the Commercial aircraft in-flight entertainment system market beyond primary operators to encompass leasing firms, MROs, and software integrators serving both countries.

Competitive Landscape

The market structure is moderately concentrated, dominated by long-established avionics companies supplemented by connectivity specialists and software innovators. Panasonic Holdings and Thales Group leverage their decades-long track records in type certification, extensive spare parts networks, and bundled content services. Collins Aerospace capitalizes on its strengths in cockpit-cabin integration, while satellite operators Viasat and Intelsat shape system architecture through high-throughput orbit assets. Suppliers winning recent line-fit awards offer comprehensive packages that include displays, servers, antennas, content management, and advertising engines, all under a single contract, thereby reducing interface risk for airlines.

Technological differentiation now centers on revenue enablement, rather than hardware specification. Panasonic’s Astrova platform integrates AI-driven content curatio, reportedly elevating click-through rates by 30%. Viasat’s multi-terabit satellites deliver bandwidth cost savings, enabling carriers to reduce Wi-Fi pricing and thereby increase penetration from 25% to 45% on select routes. Specialized entrants target regional jet and business aviation sub-niches with cloud-based media servers and portable wireless players that sidestep heavy wiring.

Barriers to entry remain high due to stringent FAA and Transport Canada certification requirements, Part 382 accessibility compliance, and increasing cybersecurity obligations. Established barriers to entry remain high, so OEMs, therefore, enjoy an incumbency advantage. Yet, software-defined architectures open up space for agile developers who can update features over the air, integrate third-party merchant ecosystems, and more.

North America Commercial Aircraft In-Flight Entertainment And Connectivity System Industry Leaders

Thales Group

Panasonic Holdings Corporation

Safran SA

Viasat, Inc.

Collins Aerospace (RTX Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Airbus signed a Memorandum of Understanding (MoU) with Panasonic Avionics to explore a strategic partnership for the future Connected Aircraft platform. Both parties plan to develop a new on-board architecture using Panasonic Avionics' next-generation in-flight entertainment (IFE) hardware and software server platform, Converix, subject to a definitive agreement expected later in 2025.

- September 2024: Anuvu signed an agreement with Air Canada to provide in-flight entertainment services. Anuvu offers entertainment solutions and high-speed in-flight connectivity for mobility markets.

- May 2024: Panasonic Avionics Corporation and EVA Air signed an agreement to install in-flight entertainment (IFE) and connectivity systems, along with digital services, across 54 of their widebody and narrowbody aircraft.

- June 2023: United Airlines signed an agreement with Panasonic Avionics to install the Astrova in-flight entertainment system on its new long-haul international aircraft.

North America Commercial Aircraft In-Flight Entertainment And Connectivity System Market Report Scope

Narrowbody, Widebody are covered as segments by Aircraft Type. Canada, United States are covered as segments by Country.By System Type

| Seat-back IFEC |

| Wireless and BYOD IFE |

| In-seat Power and Peripherals |

By Aircraft Type

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

By Fit Type

| Original Equipment Manufacturers (OEMs) |

| Aftermarket |

By Cabin Class

| First Class |

| Business Class |

| Premium Economy Class |

| Economy Class |

By Country

| United States |

| Canada |

| By System Type | Seat-back IFEC |

| Wireless and BYOD IFE | |

| In-seat Power and Peripherals | |

| By Aircraft Type | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| By Fit Type | Original Equipment Manufacturers (OEMs) |

| Aftermarket | |

| By Cabin Class | First Class |

| Business Class | |

| Premium Economy Class | |

| Economy Class | |

| By Country | United States |

| Canada |

Market Definition

- Product Type - Entertainment provided to aircraft passengers during a flight refers to In-flight entertainment. The seatback screens which are used to provide entertainment are included under the IFE system product type.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms