Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

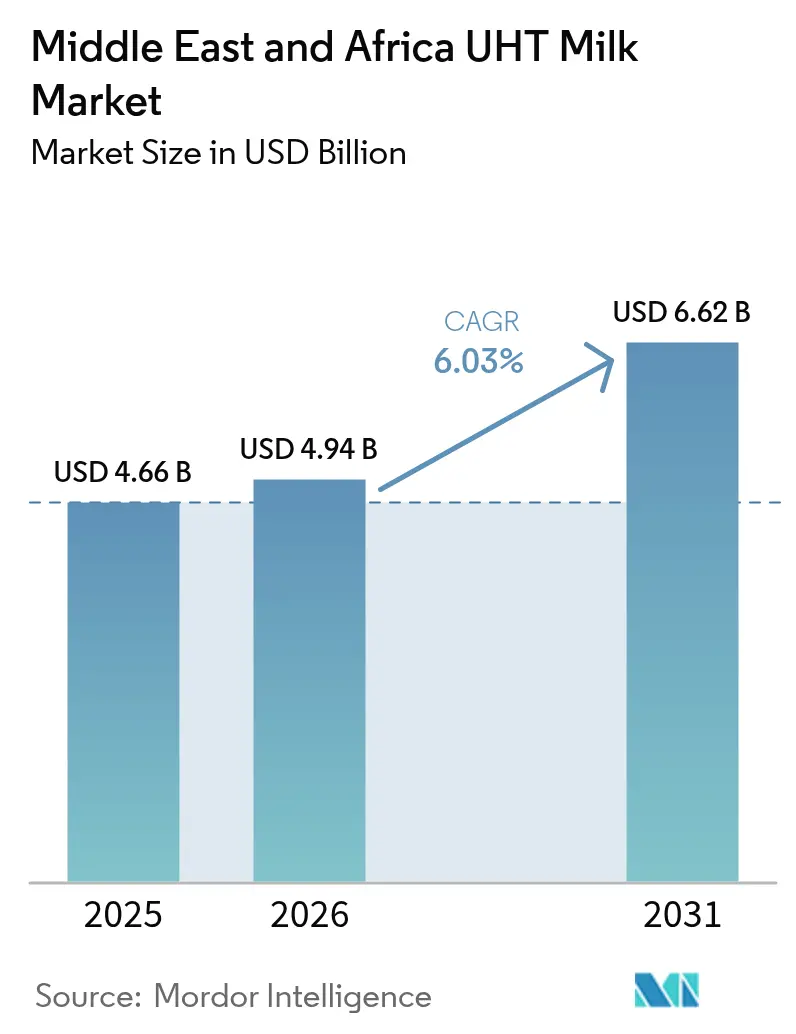

| Base Year Market Size (2025) | USD 4.66 Billion |

| Market Size (2026) | USD 4.94 Billion |

| Market Size (2031) | USD 6.62 Billion |

| Growth Rate (2026 - 2031) | 6.03% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa UHT Milk Market Analysis by Mordor Intelligence

The Middle East and Africa UHT milk market size was valued at USD 4.66 billion in 2025 and estimated to grow from USD 4.94 billion in 2026 to reach USD 6.62 billion by 2031, at a CAGR of 6.03% during the forecast period (2026-2031). This solid trajectory is tied to retail modernization, low-carbon cold-chain upgrades, and a visible shift toward fortified dairy. South Africa anchors regional demand through an established processing base, while Oman posts the most rapid growth after aligning food-security capital with capacity additions. Whole and full-cream variants still dominate but skimmed milk is the fastest climber, prompted by public health campaigns in the GCC and South Africa. Unflavoured options command volume share, though flavoured lines are on a premiumization upswing. Flexible pouches are poised to trim logistics costs, and foodservice operators are pivoting to micro-foam-stable products to meet specialty coffee demand. Competition remains fragmented; multinationals expand fortification pipelines while regional specialists trial low-carbon packaging to meet emerging waste rules.

Key Report Takeaways

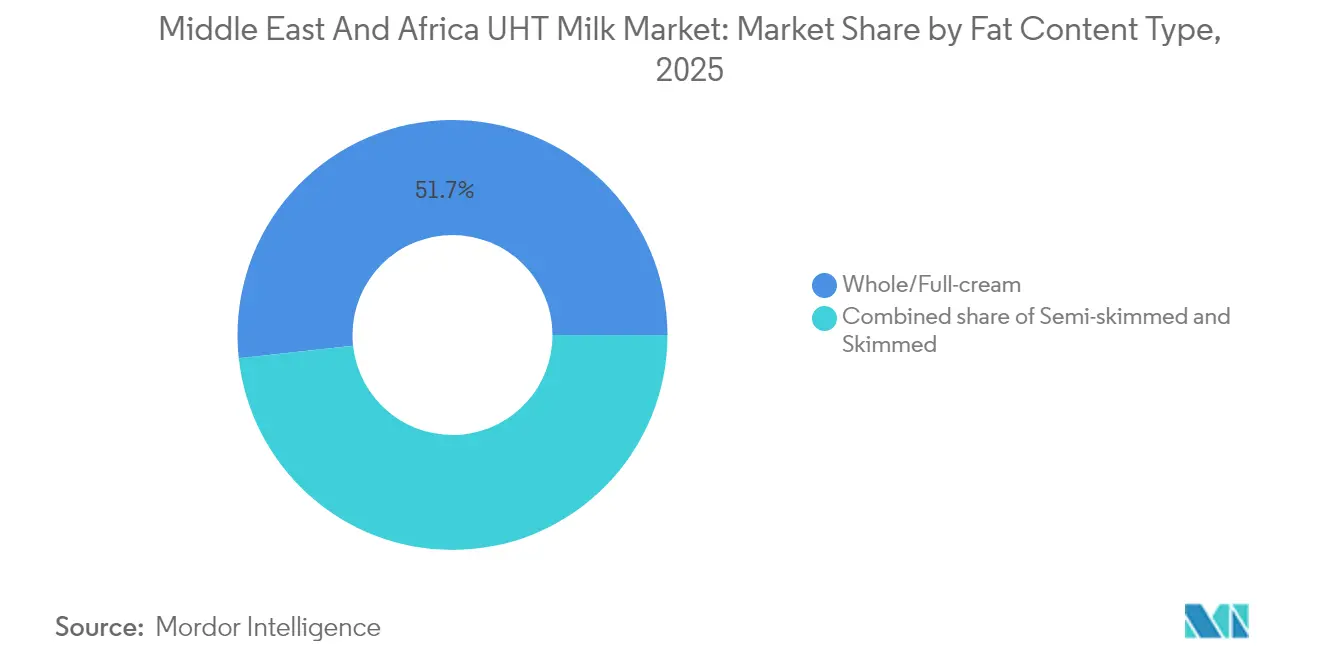

- By fat content, whole and full-cream accounted for 51.72% of the Middle East and Africa UHT Milk Market share in 2025, while skimmed milk is projected to expand at a 6.82% CAGR to 2031.

- By flavor, unflavoured held 63.80% of the Middle East and Africa UHT Milk Market size in 2025; flavoured variants are advancing at an 8.34% CAGR through 2031.

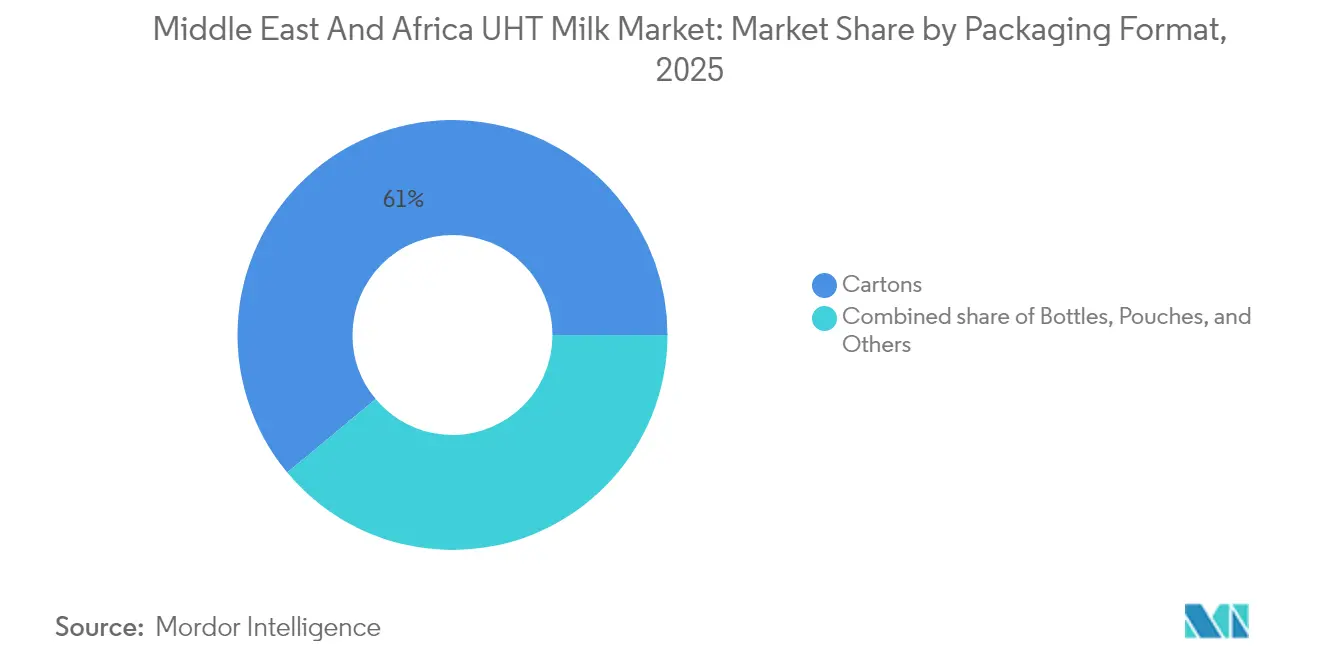

- By packaging, cartons led with 61.05% of the Middle East and Africa UHT Milk Market share in 2025, yet pouches are forecast to rise at a 6.65% CAGR between 2026 and 2031.

- By distribution channel, retail captured 70.25% of the Middle East and Africa UHT Milk Market size in 2025, while foodservice and HoReCa are growing at a 6.96% CAGR to 2031.

- By geography, South Africa commanded 26.20% of regional volume in 2025, whereas Oman is set to record a 6.68% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa UHT Milk Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to sustainable, low-carbon cold-chain alternatives | +1.2% | Global, with early gains in Kenya, Tunisia, South Africa | Medium term (2-4 years) |

| Growth of supermarkets and hypermarkets improves UHT milk visibility | +1.4% | Saudi Arabia, UAE, Egypt, Qatar, Algeria | Short term (≤ 2 years) |

| Consumer preference for long shelf-life products | +1.1% | Global, particularly Nigeria, Morocco, Egypt | Short term (≤ 2 years) |

| Foodservice preference for micro-foam-stable UHT milk | +0.8% | GCC core, Turkey, spill-over to North Africa | Medium term (2-4 years) |

| Rising demand for fortified UHT milk | +0.9% | East Africa, Egypt, Morocco, Saudi Arabia | Long term (≥ 4 years) |

| Health awareness and nutritional benefits | +0.7% | Global, with urban concentration in GCC and South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to Sustainable, Low-Carbon Cold-Chain Alternatives

Governments and multilateral institutions are prioritizing investments in renewable-powered cold-chain infrastructure to address post-harvest losses and reduce carbon emissions. The International Finance Corporation has implemented solar-powered cooling units in Kenya and Tunisia, reducing diesel dependency by up to 60% and enabling smallholder farmers to integrate into formal supply chains. According to the Global Cold Chain Alliance's 2024 report, unreliable energy, skill gaps, and fragmented logistics continue to hinder cold-storage capacity in Sub-Saharan Africa, leading to higher spoilage rates and diminishing UHT milk's cost advantage over fresh milk[1]Global Cold Chain Alliance, "The Cold Chain in Africa", www.gcca.org. Renewable-powered cold chains not only reduce carbon emissions but also help producers meet sustainability goals while expanding access to peri-urban and rural markets. UHT milk stands to gain the most, as it requires only ambient storage after processing, significantly lowering its energy footprint compared to chilled dairy products.

Growth of Supermarkets and Hypermarkets Improves UHT Milk Visibility

Modern retail formats are expanding rapidly across the Middle East and North Africa, driven by higher disposable incomes, urbanization, and increased foreign investments in grocery infrastructure. In 2024, Qatar and Algeria signed an agreement to open over 100 megastores and hypermarkets. These stores will allocate dedicated shelf space for packaged dairy products, reducing dependence on traditional wet markets. Saudi Arabia's retail market has grown steadily in 2024, with modern trade channels capturing a larger share of dairy sales as consumers prefer convenience, trusted brands, and a wider variety of products. In the UAE, modern trade penetration has reached approximately 70%, with hypermarkets and supermarkets acting as key distribution points for UHT milk brands catering to both expatriates and locals. Air-conditioned retail spaces enhance the perceived quality of products, support promotional campaigns, enable cross-merchandising with breakfast cereals, and encourage impulse purchases. This growth in modern retail channels is particularly important in regions where informal dairy trade was dominant, as it helps formalize supply chains and introduces traceability standards that comply with food safety regulations.

Consumer Preference for Long Shelf-Life Products

Households are changing their buying habits to reduce food waste, shop less frequently, and manage budgets more effectively in response to rising inflation. A 2024 study by Kerry Group found that 72% of global consumers see longer shelf-life as a key way to cut down on food waste. In the Middle East and Africa, many consumers also value storage convenience and cost savings. UHT milk, which can be stored without refrigeration for 6 to 12 months when unopened, meets these needs. This is particularly important in regions with unreliable electricity or limited access to refrigeration. For example, in Nigeria, where urban areas experience power outages lasting 10 to 15 hours daily, UHT milk is a practical alternative to fresh milk, which spoils within 48 hours. Similarly, in Egypt, economic instability and currency devaluation in 2024 led consumers to stock up on shelf-stable products like UHT milk during periods of price stability. Retailers have supported this shift by offering discounts on bulk purchases of UHT milk, making it cheaper per liter compared to fresh milk. As more households switch to UHT milk, distribution networks are expanding, improving availability and making it even more competitively priced.

Health Awareness and Nutritional Benefits

As incomes rise and urbanization spreads, consumers are becoming more discerning about their dietary choices, paying closer attention to fat content, protein density, and micronutrient profiles. In response, households are gravitating towards skimmed and semi-skimmed UHT milk variants, aiming to cut down on saturated fats without sacrificing calcium and protein. In 2024, the UAE's Ministry of Health rolled out a "Healthy Eating, Active Living" campaign, advocating for low-fat dairy in balanced diets to tackle obesity and diabetes, issues plaguing nearly 25% of Emiratis[2]UAE Ministry of Health and Prevention. "Healthy Eating, Active Living Campaign." mohap.gov.ae. Similarly, South Africa's National Department of Health, in 2024, updated its dietary guidelines, spotlighting low-fat dairy to combat cardiovascular diseases, responsible for 18% of the nation's annual deaths. Producers are not standing still: In 2024, Danone launched a high-protein, low-fat UHT milk in South Africa, eyeing fitness enthusiasts and marketing it as an ideal post-workout drink. This movement dovetails with fortification trends, as brands enhance low-fat UHT offerings with functional perks—like vitamin D for bones or probiotics for digestion, justifying premium pricing and standing out in a saturated market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer preference for fresh milk | -1.3% | East Africa, Egypt, Morocco, Nigeria | Short term (≤ 2 years) |

| Challenges in maintaining cold storage for distribution | -0.9% | Nigeria, Egypt, Morocco, South Africa | Medium term (2-4 years) |

| Packaging waste and environmental concerns | -0.6% | GCC, South Africa, Egypt | Medium term (2-4 years) |

| Competition from alternative plant-based milks | -0.8% | GCC, South Africa, urban centers across MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer Preference for Fresh Milk

Cultural norms, taste preferences, and distrust of processed foods continue to drive the demand for fresh milk in regions where informal dairy trade dominates. In East Africa, around 80% of dairy products are sold through informal channels. Consumers in this region often purchase raw or minimally pasteurized milk directly from farmers or local vendors, as it is typically more affordable than branded UHT milk. A 2024 study on East African dairy consumption revealed that households perceive fresh milk as more nutritious and "natural" compared to UHT milk, even though both have similar nutrient profiles after processing. In Egypt, the dairy market remains highly fragmented. Traditional baladi milk constitutes a significant portion of rural consumption, particularly in areas with limited cold-chain infrastructure and high price sensitivity, according to the Egyptian Ministry of Agriculture. Similarly, in Morocco, dairy cooperatives reported in 2024 that consumers are willing to pay 15% to 20% less for UHT milk compared to fresh milk. This pricing disparity limits profit margins and restricts the retail reach of UHT milk outside urban areas. Generational habits and a lack of awareness about the benefits of UHT processing further reinforce this preference. To shift consumer behavior, sustained efforts in education and brand-building are essential.

Challenges in Maintaining Cold Storage for Distribution

In Sub-Saharan Africa, energy shortages, inadequate infrastructure, and the high costs of cold-chain logistics are significantly increasing distribution expenses and spoilage risks. The Global Cold Chain Alliance's 2024 Africa report highlights unreliable electricity, a shortage of skilled refrigeration technicians, and fragmented logistics networks as the primary barriers to cold-chain development. In 2024, South Africa experienced severe power outages, with Eskom enforcing prolonged Stage 6 load-shedding. This compelled dairy distributors to invest in diesel generators and backup refrigeration systems, driving up operating costs by 12% to 18%. In Nigeria, cold-storage facilities are heavily concentrated in Lagos and Abuja, leaving rural areas and smaller cities underserved. Distributors in these regions report spoilage rates of 20% to 30% for chilled dairy products during last-mile delivery, which significantly impacts profitability. In Egypt, cold-chain infrastructure is expanding but remains insufficient to meet growing demand. Importers and processors frequently encounter delays at ports and a lack of refrigerated warehouses, which continue to hinder operations. Although UHT milk can be stored without refrigeration, it still requires cold-chain handling during raw milk collection and pre-processing, exposing producers to the same infrastructure challenges as fresh milk. Solving these issues requires coordinated investments in renewable energy, advanced refrigeration technologies, and logistics training programs. Public-private partnerships are beginning to make progress in addressing these critical areas, offering hope for improved cold-chain systems in the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fat Content Type: Low-Fat Variants Gain Traction

Skimmed milk is the fastest-growing segment in the fat content category, expected to grow at a 6.82% CAGR from 2026 to 2031. This growth is driven by health-conscious consumers who aim to reduce saturated fat intake while maintaining protein and calcium levels. In 2024, the UAE's Ministry of Health launched the "Healthy Eating, Active Living" campaign, promoting low-fat dairy as part of a balanced diet to combat obesity and diabetes, which affect about 25% of the Emirati population. Similarly, South Africa's National Department of Health updated its dietary guidelines in 2024, emphasizing low-fat dairy to address cardiovascular diseases, which account for 18% of annual deaths. In the same year, Danone introduced a high-protein, low-fat UHT milk in South Africa, targeting fitness enthusiasts and marketing it as a post-workout recovery drink. Semi-skimmed milk is gaining popularity in Egypt and Morocco, where consumers seek a balance between taste and health. Meanwhile, skimmed milk, though still niche, is growing rapidly in GCC markets, driven by expatriates adopting Western dietary habits.

Whole and full-cream milk dominated the fat content segment in 2025, holding a 51.72% market share. This preference is rooted in cultural traditions and a liking for richer taste profiles, particularly in Saudi Arabia, Egypt, and Turkey. Almarai's full-cream UHT milk remains the top-selling product in Saudi Arabia, with the company processing 4 million liters of milk daily. In Turkey, Sütaş produces 3,600 tons of dairy products daily, with full-cream UHT milk making up the majority of its exports to Egypt, UAE, Qatar, Libya, Iraq, and Kuwait. In Egypt, Juhayna leads the plain milk market, with full-cream UHT milk as its flagship product. However, the growth of this segment is slowing as younger, urban consumers shift towards lower-fat options. To address this trend, producers are introducing fortified full-cream milk variants, adding functional benefits like vitamin D for bone health and omega-3 fatty acids for brain health to traditional formulations.

By Flavor: Chocolate and Vanilla Drive Premiumization

Flavoured UHT milk is expected to be the fastest-growing segment, with a projected CAGR of 8.34% from 2026 to 2031. This growth is driven by innovations in product offerings, a focus on pediatric nutrition, and the increasing demand for convenient, on-the-go consumption options. At Gulfood 2025, PROMESS introduced new flavoured UHT milk products, including chocolate, vanilla, and strawberry variants fortified with essential vitamins and minerals, targeting children and adolescents. In 2024, Juhayna launched iron-fortified chocolate milk in Egypt, positioning it as a nutritional supplement for school-age children and pregnant women. Brookside Dairy entered the flavoured UHT milk market in Kenya in 2024, leveraging its strong distribution network to reach peri-urban and rural areas where refrigeration is limited. Lacnor expanded its flavoured UHT milk range in the UAE in 2024 by adding banana and caramel flavors, aiming to attract impulse buyers at convenience stores and petrol stations. Similarly, Baladna introduced flavoured UHT milk in Qatar in 2024, targeting expatriate families and promoting it as a healthier alternative to carbonated soft drinks.

Unflavoured UHT milk accounted for 63.80% of the flavor segment in 2025, reflecting traditional consumption habits and price sensitivity in Middle Eastern and African markets. In Saudi Arabia, plain UHT milk continues to dominate the retail market, with key players like Almarai, Saudia Dairy, and NADEC competing on pricing, brand reputation, and distribution reach. In Egypt, the traditional baladi milk culture sustains demand for unflavoured UHT milk, particularly in rural areas where consumers prioritize functional nutrition over flavor variety. In South Africa, the UHT milk market is divided between plain and flavoured options. Retailers often promote private-label unflavoured UHT milk at discounted prices to attract budget-conscious households. However, the growth of the unflavoured segment is slowing as producers shift their focus to flavoured and fortified variants. These products offer higher profit margins and appeal to younger, urban consumers who value convenience and diverse taste options.

By Packaging Format: Flexible Pouches Gain Ground

Forecasted to grow at a 6.65% CAGR from 2026 to 2031, pouches are rapidly emerging as the leading segment in packaging. This surge is attributed to benefits like material cost savings, sustainability mandates, and enhanced logistics efficiency. In 2024, Nissha and Tetra Pak unveiled a paper-based aseptic carton, crafted from 90% renewable materials and boasting a 30% reduction in plastic content, specifically targeting markets with stringent packaging regulations. Huhtamaki rolled out recyclable cups for dairy products in 2024, utilizing mono-material polypropylene to streamline recycling and cut down landfill waste. Liquibox debuted a self-sealing cap for bag-in-box systems in 2024, which not only extends the post-opening shelf-life to 90 days but also slashes packaging waste by 60% compared to traditional cartons. Pouches have found a particular resonance in price-sensitive markets like Nigeria, Egypt, and Morocco, where affordability is paramount for consumers and retailers aim to optimize shelf space and cold-storage needs.

In 2025, cartons dominated the packaging landscape, holding a 61.05% share, bolstered by a well-established aseptic-filling infrastructure, strong brand equity, and consumer familiarity. In a move underscoring sustainability, Tetra Pak teamed up with Lactalis in 2024 to roll out cartons made with 33% recycled polymers, achieving a commensurate reduction in carbon footprint and aligning with EU circular economy benchmarks. Targeting producers with bold sustainability goals, SIG Combibloc introduced the Terra carton in 2024, boasting a paper-based barrier that curtails CO2 emissions by 63% compared to standard cartons. Major players like Almarai, Danone, and Lactalis are ramping up investments in carton-filling capacities across Saudi Arabia, Egypt, and South Africa, leveraging their brand strength and economies of scale to fortify their market positions. While bottles cater to niche premium segments and single-serve needs, other formats like bag-in-box systems are gaining traction in foodservice, and bulk packaging is appealing to institutional buyers.

By Distribution Channel: HoReCa Segment Accelerates

The foodservice and HoReCa distribution segment is projected to grow at a strong 6.96% CAGR from 2026 to 2031. This growth is driven by the expansion of the hospitality sector, increasing popularity of specialty coffee, and rising demand for institutional catering services. In 2024, Sütaş launched "Barista Milk" in Turkey, a UHT product specifically designed to create stable micro-foam for cappuccinos and lattes, targeting the growing specialty coffee market in the country. Bag-in-box UHT systems are becoming increasingly popular in HoReCa channels due to their benefits, such as portion control, reduced packaging waste, and the ability to store milk at room temperature for up to 90 days after opening, compared to just 7 days for chilled milk. The GCC hospitality sector welcomed 85 million international visitors in 2024, significantly boosting the demand for UHT milk. Operators are focusing on standardizing beverage quality across multiple outlets while reducing spoilage and labor costs.

Retail channels accounted for 70.25% of the distribution segment in 2025, supported by the growth of supermarkets and hypermarkets, increased competition from private-label brands, and the rising penetration of e-commerce. In 2024, Qatar and Algeria signed a bilateral agreement to establish over 100 megastores and hypermarkets. These stores aim to provide dedicated shelf space for packaged dairy products, reducing reliance on traditional wet markets. In the UAE, modern trade penetration stands at approximately 60%, with hypermarkets and supermarkets serving as key distribution points for UHT milk brands catering to both expatriates and local consumers. Convenience stores and online retail are also growing rapidly. For instance, Lulu Group partnered with India's Milma cooperative in 2024 to distribute long-shelf-life dairy products across hypermarkets in the Middle East, further strengthening the retail distribution network.

Geography Analysis

In 2025, South Africa captured 26.20% of the regional UHT milk market, supported by its strong dairy processing base, SADC export corridors, and modern retail infrastructure. Despite a 3.7% drop in average prices, the UHT milk segment saw positive retail volume growth, driven by competition and private-label expansion. UHT milk is a key part of South Africa's liquid dairy production, with annual exports of about 87,696 tonnes to SADC member states, making the country a regional hub for shelf-stable dairy. Lactalis South Africa, employing 501 to 1,000 workers, produces brands like Melrose, Parmalat, and Steri Stumpie, competing with Clover, Woodlands, and Fair Cape in a fragmented market. However, load-shedding in 2024 forced distributors to invest in diesel generators and backup refrigeration, raising operating costs by 12% to 18% and limiting profit margins. In 2025, the South African Competition Commission filed a complaint alleging anti-competitive practices in the dairy sector, signaling potential regulatory changes.

Oman is the fastest-growing market, with a projected 6.68% CAGR from 2026 to 2031, driven by government food security initiatives, capacity investments, and rising dairy consumption. At HORECA Oman 2024, Mazoon Dairy highlighted its 180 million liters of raw milk production and 140 million liters of processing capacity, prioritizing UHT milk. UHT milk, with its long shelf life and reduced cold-chain needs, is well-positioned to address this gap. The hospitality sector in Muscat and Salalah is expanding, boosting demand for UHT milk in foodservice, especially for coffee and tea where foam stability is essential.

Saudi Arabia, UAE, Egypt, Turkey, Nigeria, and Morocco show varied growth trends shaped by retail modernization, demographics, and infrastructure investments. In March 2024, Saudi Arabia's Almarai announced an 18 billion riyal (USD 4.8 billion) plan to expand processing and diversify into protein categories. Nestlé invested USD 72 million in 2024 to build its first food manufacturing facility in Saudi Arabia for local dairy and nutritional products. In May 2025, the UAE's Al Ain Farms Group unified five brands to streamline distribution. Mleiha Dairy, in November 2024, announced plans to expand its herd to 20,000 cows to boost UHT milk production for domestic and export markets. In October 2024, Egypt's Arla Foods bid USD 183 million to acquire Domty, aiming to expand its Middle Eastern presence and leverage Domty's distribution network. Turkey's Sütaş processes 3,600 tons of dairy daily, exporting UHT milk to 47 countries, including Egypt and UAE, while managing a 49% rise in raw milk prices in 2024. Nigeria's FrieslandCampina received a USD 5 million Gates Foundation grant in 2024 for the Value4Dairy program, supporting 10,000 herders and smallholders to improve milk quality and supply-chain integration.

Competitive Landscape

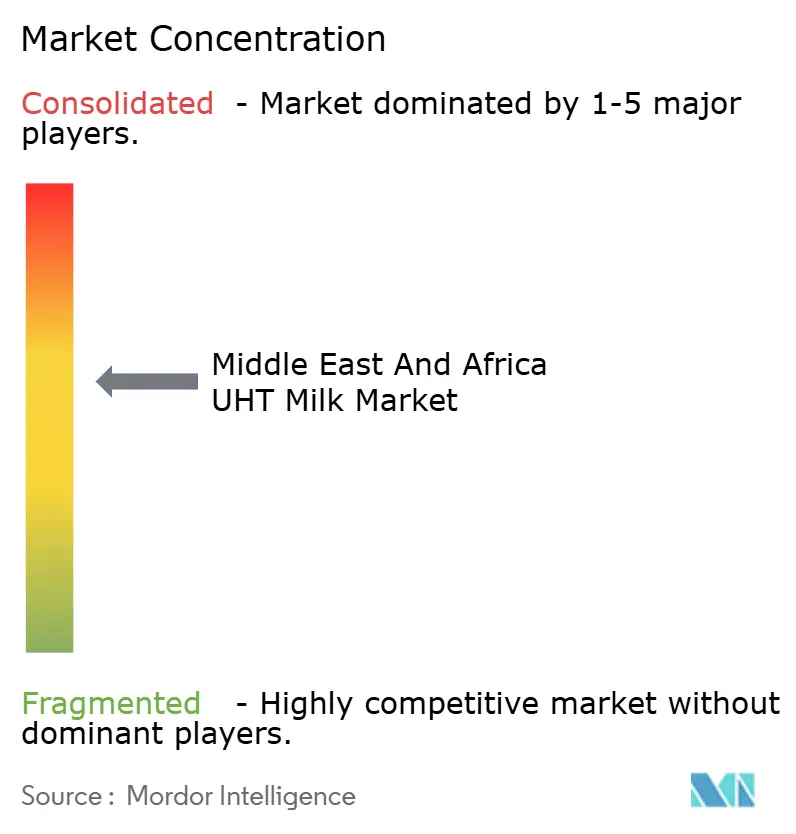

The Middle East and Africa UHT milk market is moderately consolidated, with a mix of established regional dairies and multinational players driving competition through strong distribution capabilities and brand recognition. Leading companies leverage scale advantages, long-life processing technologies, and wide product portfolios to secure dominant shelf presence across supermarkets, small grocers, and institutional channels. Their ability to maintain consistent supply in regions with variable cold-chain infrastructure further reinforces their market position.

Meanwhile, mid-sized local producers are gradually gaining traction by offering competitively priced variants tailored to regional taste preferences. However, high capital requirements for UHT processing and packaging continue to limit rapid new entry. Overall, competition centers on pricing efficiency, value-added fortification, and expanding reach into underserved semi-urban and rural markets.

Technology adoption is accelerating, with Tetra Pak and SIG Combibloc introducing paper-based aseptic cartons that reduce carbon footprint by 33% to 63%, enabling producers to meet sustainability mandates while maintaining product integrity. However, regulatory compliance remains a strategic imperative, with ISO 22000 food safety management systems and Hazard Analysis and Critical Control Points (HACCP) certifications serving as baseline requirements for export-oriented producers targeting GCC and European markets.

Middle East And Africa UHT Milk Industry Leaders

-

Almarai

-

Saudia Dairy & Foodstuff Co. (SADAFCO)

-

Lactalis Group

-

Nestlé S.A.

-

Clover Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Beyti Food Industries, a leading dairy and juice producer and a subsidiary of the Almarai Group, has introduced Egypt’s first UHT milk packaged in PET bottles. The PET initiative is part of Beyti’s broader EGP 1 billion expansion at its expansive 120-feddan Nubaria complex, one of the largest integrated food manufacturing hubs in the region.

- November 2025: Dairy Group South Africa has introduced a new Creamline product, the Creamline Full Cream UHT Long Life Milk. The product is available in various pack sizes, making it suitable for both individual consumption and family use.

- November 2024: Clover S.A. Proprietary Limited has introduced two new dairy innovations to the South African market: Clover 1L UHT Flavoured Milk and the Tropika Drinking Yoghurt. According to the brand, its new Clover 1L UHT Flavoured Milk is available in two flavors, Chocolate and Strawberry.

- November 2024: Kinangop Dairy has introduced 4US Long Life Whole Milk, expanding its 4US brand to cater to Kenya’s growing demand for nutritious, convenient dairy options. According to Kinangop Dairy, the 4US Long Life Whole Milk emphasizes a creamy texture and rich flavor.

Middle East And Africa UHT Milk Market Report Scope

The Middle East & Africa UHT milk market is segmented by type into full cream UHT milk, low-fat UHT milk, skimmed UHT milk, and semi-skimmed UHT milk. Also, the study provides an analysis of the UHT milk market in the emerging and established markets across the region, including South Africa, Saudi Arabia, and the Rest of Middle East & Africa.

Fat Content Type

| Whole/Full-cream |

| Semi-skimmed |

| Skimmed |

Flavor

| Unflavoured |

| Flavoured |

Packaging Format

| Cartons |

| Bottles |

| Pouches |

| Others |

Distribution Channel

| Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Others |

Country

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Oman |

| Rest of Middle East and Africa |

| Fat Content Type | Whole/Full-cream | |

| Semi-skimmed | ||

| Skimmed | ||

| Flavor | Unflavoured | |

| Flavoured | ||

| Packaging Format | Cartons | |

| Bottles | ||

| Pouches | ||

| Others | ||

| Distribution Channel | Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| Country | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Oman | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Middle East and Africa UHT milk Market in 2026?

The market is valued at USD 4.94 billion in 2026 and is projected to reach USD 6.62 billion by 2031.

Which country currently leads regional demand?

South Africa contributes 26.20% of 2025 volume thanks to its processing base and SADC export reach.

What segment is growing fastest within the market?

Flavoured UHT milk is expanding at an 8.34% CAGR as brands add chocolate, vanilla, and fortified options.

Why are pouches gaining popularity in packaging?

Pouches cut material use by up to 40%, lower freight costs, and align with tightening recycling mandates.

Page last updated on: