Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

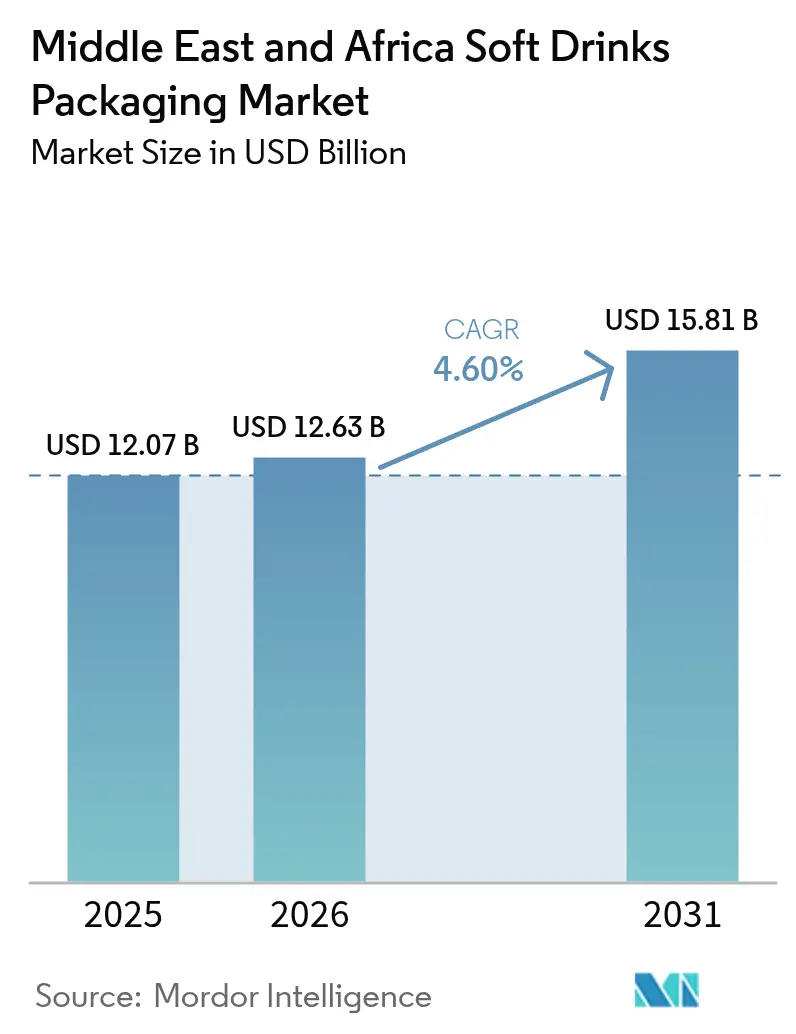

| Base Year Market Size (2025) | USD 12.07 Billion |

| Market Size (2026) | USD 12.63 Billion |

| Market Size (2031) | USD 15.81 Billion |

| Growth Rate (2026 - 2031) | 4.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Soft Drinks Packaging Market Analysis by Mordor Intelligence

The Middle East and Africa soft drinks packaging market size in 2026 is estimated at USD 12.63 billion, growing from 2025 value of USD 12.07 billion with 2031 projections showing USD 15.81 billion, growing at 4.60% CAGR over 2026-2031. This trajectory flows from rapid urbanization, youthful demographics, and rising demand for convenient, ready-to-consume beverages across bottled water, carbonates, and emerging functional categories. Shrinking household sizes, the spread of modern retail, and government-backed industrial programs in the Gulf further intensify packaging requirements. Suppliers benefit from integrated petrochemical chains that lower PET resin costs, while investors target aseptic filling, lightweighting, and in-country manufacturing to align with localization mandates. Heightened Extended Producer Responsibility (EPR) fees and looming single-use plastic bans push brand owners toward aluminum, paperboard, and tethered-cap solutions, opening white-space for material innovators ready to meet tightening sustainability targets.

Key Report Takeaways

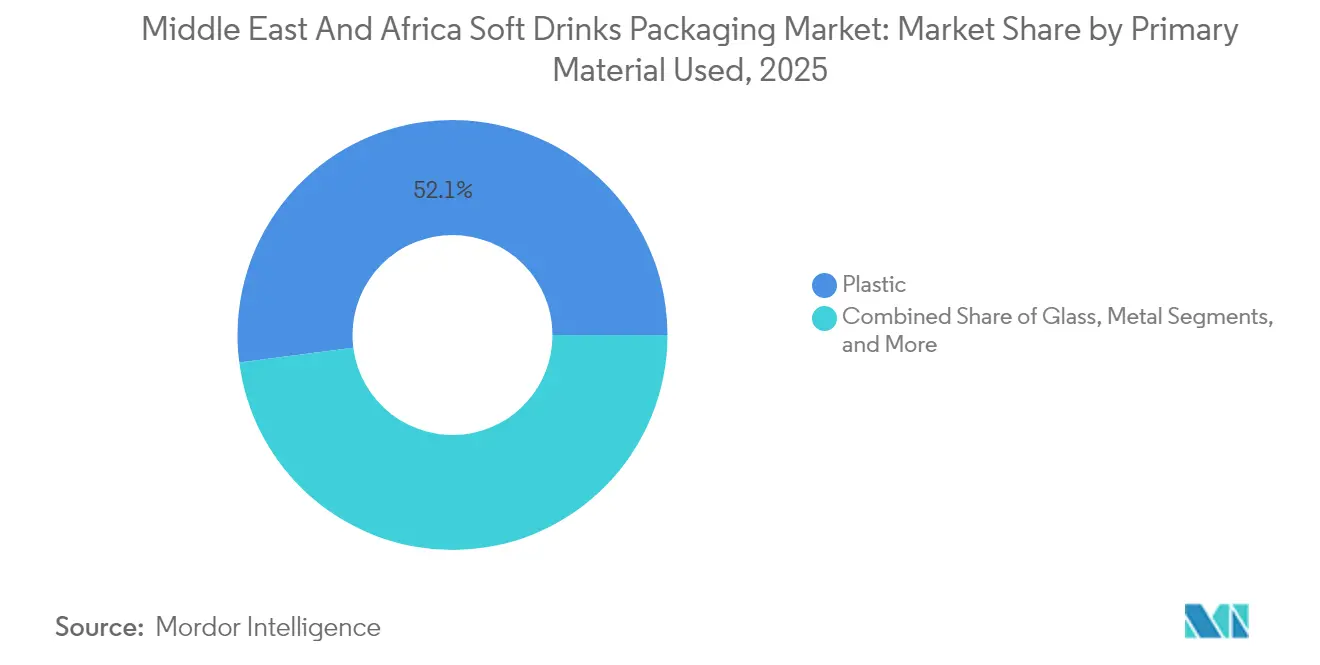

- By primary material, plastic held 52.05% of the Middle East and Africa soft drinks packaging market share in 2025, whereas paper and paperboard are forecast to expand at a 6.05% CAGR to 2031.

- By packaging format, bottles dominated with 61.10% revenue share of the Middle East and Africa soft drinks packaging market in 2025; cartons and aseptic bricks are projected to grow at a 5.78% CAGR through 2031.

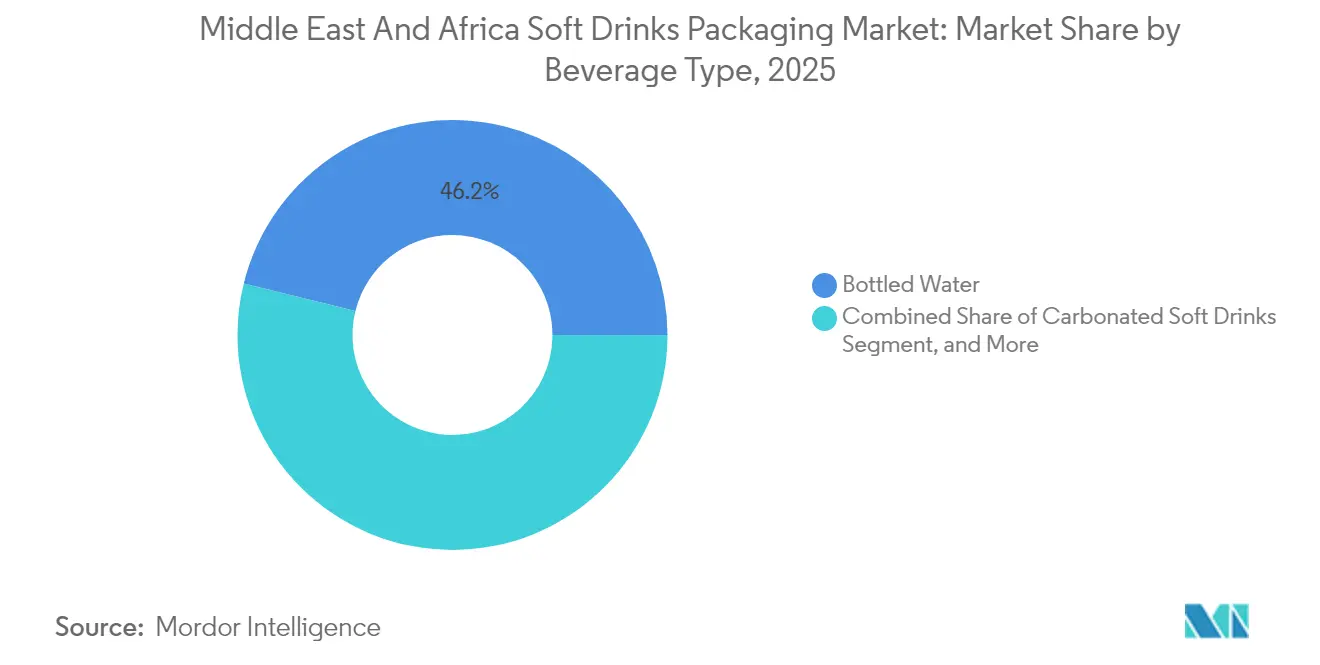

- By beverage type, bottled water accounted for 46.15% of the Middle East and Africa soft drinks packaging market size in 2025, while ready-to-drink tea and coffee are advancing at a 5.95% CAGR to 2031.

- By pack capacity, the 501-1000 mL range led with 46.60% share of the Middle East and Africa soft drinks packaging market in 2025; packs of ≤330 mL register the fastest 5.55% CAGR through 2031.

- By country, Saudi Arabia commanded a 34.80% share of the Middle East and Africa soft drinks packaging market in 2025, whereas South Africa is set to post the highest 5.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Soft Drinks Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising bottled-water consumption in GCC | +0.8% | GCC core, wider MEA spillover | Medium term (2-4 years) |

| Surge in demand for convenience and on-the-go single-serve packs | +0.7% | UAE, Saudi Arabia, South Africa first movers | Short term (≤ 2 years) |

| Hydrocarbon-to-polymer capacity expansions lowering PET cost | +0.6% | Middle East core, North Africa secondary | Medium term (2-4 years) |

| Brand shift toward tethered and lightweight caps | +0.4% | Regionwide via EU rules influence | Long term (≥ 4 years) |

| Localization incentives under Saudi Vision 2030 encouraging can lines | +0.5% | Saudi Arabia primary | Medium term (2-4 years) |

| Growth of aseptic filling hubs for fermented and plant-based drinks | +0.6% | Saudi Arabia, UAE, South Africa hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Bottled-Water Consumption in GCC

Persistent water-scarcity concerns and variable municipal supply quality continue to steer Gulf households toward packaged hydration. Saudi Arabia’s National Water Strategy 2030 has prioritized diversified sourcing, indirectly sustaining bottled water demand as utilities modernize.[1]“Highlights,” Tetra Laval, tetralaval.com Sidel’s 80,000-bph PET lines, deployed with regional bottlers, illustrate how plant investments capture this surge. A youthful population, more than 60% under 30, gravitates to premium and functional waters, lifting packaging value per unit and reinforcing the primacy of PET containers in the Middle East and Africa soft drinks packaging market.

Surge in Demand for Convenience and On-the-Go Single-Serve Packs

Compressed work routines and the expansion of convenience retail have made sub-330 mL packs commonplace. Unit volumes in this size band are rising at a 5.8% CAGR, outpacing larger formats as consumers blend portion control with mobility. SIG’s DomeMini carton bottle (180-350 mL) pairs portability with aseptic integrity, making carton options viable for on-the-go consumption.[2]“SIG Launches On-the-Go Carton Bottle DomeMini,” BevNET, bevnet.com Uptake concentrates in Riyadh, Dubai, and Johannesburg, where busy lifestyles and food-service channels intersect, propelling the Middle East and Africa soft drinks packaging market toward higher-margin, single-serve applications.

Hydrocarbon-to-Polymer Capacity Expansions Lowering PET Cost

Integrated refinery-to-polymer investments across Saudi Arabia and the broader Gulf generate material cost advantages. These chains insulate converters from global resin volatility and underpin PET’s 52.7% share. Lower feedstock expenses flow directly to high-volume bottled-water lines, preserving the cost competitiveness that keeps plastic the anchor substrate in the Middle East and Africa soft drinks packaging market.

Brand Shift Toward Tethered and Lightweight Caps

To anticipate EU Single-Use Plastics rules, multinationals now specify tethered closures for regional roll-outs. Crown’s 330 mL CrownSleek can embraces enhanced decoration while remaining compatible with lightweight cap assemblies. Filling OEMs and closure suppliers thus coordinate earlier in project cycles, opening consultancy and machinery upgrade revenue streams even before formal legislation arrives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened EPR fees and potential plastic-tax roll-out in UAE and KSA | -0.9% | UAE primary, Saudi Arabia secondary, broader GCC adoption likely | Short term (≤ 2 years) |

| Chronic deficit in food-grade rPET collection infrastructure | -0.7% | Regional, with acute challenges in Africa | Long term (≥ 4 years) |

| Water-scarcity policies discouraging high-volume PET bottling licences | -0.5% | GCC core, North Africa secondary | Medium term (2-4 years) |

| Rising aluminium feedstock price volatility impacting can adoption | -0.4% | Global, with particular impact on cost-sensitive MEA markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened EPR Fees and Potential Plastic-Tax Roll-out in UAE and KSA

Pilot EPR schemes in the UAE already lift compliance costs for high-volume segments such as bottled water. Legislators plan broader single-use plastic bans by 2026, sharpening price pressure on PET packaging. Saudi Arabia is evaluating comparable levies within its circular-economy roadmap, injecting uncertainty that could delay capital deployment or push brands toward aluminum and paperboard options. The Middle East and Africa soft drinks packaging market accordingly faces margin compression on legacy formats while sustainable alternatives gain traction.

Chronic Deficit in Food-Grade rPET Collection Infrastructure

Brand pledges to adopt recycled content to counter against scarce, food-grade rPET supply. Informal waste-picking networks dominate across many African cities, creating traceability gaps that preclude beverage-grade output.[3]“2024 Top 100 Food and Beverage Packaging Companies,” Packaging Strategies, packagingstrategies.com Without a scale recycling backbone, converters must rely on virgin PET, limiting circularity progress and exposing the Middle East and Africa soft drinks packaging market to any surge in global resin prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Primary Material Used: Plastic Dominance Faces Sustainable Alternatives

Plastic retained a 52.05% share of the Middle East and Africa soft drinks packaging market in 2025, supported by abundant Gulf feedstocks and established PET blowing infrastructure. Favorable resin economics make PET the default for bottled water, carbonates, and sports drinks. However, paper and paperboard registered a 6.05% CAGR, accelerating on the back of plant-based beverage launches that leverage cartons’ extended shelf life and sustainable positioning.

Rising EPR fees and tethered-cap requirements push brand owners to diversify substrates, elevating carton suppliers as strategic partners. SIG’s Egyptian recycling pilot and Pulpac collaborations on paper closures exemplify innovation cycles aimed at lowering total environmental impact. Glass continues to serve premium juice and craft soda lines, whereas aluminum garners attention for energy drinks and premium waters. The material mix shift underscores how regulatory and consumer expectations reshape vendor roadmaps within the Middle East and Africa soft drinks packaging market.

By Packaging Format: Bottles Lead While Cartons Gain Momentum

Bottles commanded 61.10% of 2025 revenues, anchored by the widespread PET base and familiarity among fillers and consumers. Large-scale lines such as Sidel’s 80,000-bph systems keep throughput high and unit costs low. Yet cartons and aseptic bricks grew fastest, clocking a 5.78% CAGR as dairy alternatives, probiotic drinks, and premium juices move into ambient-stable packs that signal sustainability.

SIG’s DomeMini bottle confirms how carton technology now targets traditionally plastic-dominated convenience occasions. Aluminum cans hold steady due to infinite recyclability, particularly for carbonates and energy drinks promoted through sports marketing. Pouches and sachets serve rural and price-sensitive shoppers, highlighting the divergent needs the Middle East and Africa soft drinks packaging market must satisfy across socio-economic tiers.

By Beverage Type: Bottled Water Dominates as RTD Categories Accelerate

Bottled water secured a 46.15% share of the Middle East and Africa soft drinks packaging market size in 2025, underpinned by water scarcity realities and desalination trust gaps. Premiumized functional variants further enhance package value density. Ready-to-drink tea and coffee delivered the quickest 5.95% CAGR as urban professionals seek flavor, caffeine, and convenience in one grab-and-go option.

Carbonated soft drinks stay prominent but face sugar-tax headwinds that redirect some budgets to low- and no-sugar RTD teas. Sports and energy drinks accelerate among fitness-focused youth, while juices straddle a premium–price tension amid fruit-cost inflation. Each sub-segment’s packaging demands orienting around barrier protection, shelf life, and branding real estate drive upstream investments in format flexibility across the Middle East and Africa soft drinks packaging market.

By Pack Capacity: Mid-Size Formats Lead While Small Packs Accelerate

The 501-1000 mL range held 46.60% share in 2025, balancing multi-serve practicality and fridge fit. Family occasions and at-home consumption keep this size relevant across water and teas. Small packs of ≤330 mL, however, grew 5.55% CAGR as portion-controlled indulgence meets portability. Ball’s 330 mL can remains the archetypal carbonate pack, prized for distribution efficiency and merchandising density.

Intermediate 331-500 mL packs cater to personal hydration in gyms and offices, whereas large sizes above 1000 mL serve bulk buyers and cash-and-carry outlets. Capacity diversification shows how one beverage brand may require three or more pack sizes to satisfy divergent channel missions within the Middle East and Africa soft drinks packaging market.

Geography Analysis

Saudi Arabia captured a 34.80% share in 2025, propelled by Vision 2030 policies that blend localization incentives, youth-centric marketing, and capital access for fillers. Saudi Arabia anchors regional revenues through a combination of Vision 2030 industrialization, favorable demographics, and rising consumption of functional beverages. Localization grants spur investments in can lines and PET preform molding, deepening in-kingdom capabilities and shortening supplier lead times. The country’s regulatory dialogue on circular economy stimulates trials in tethered caps and higher recycled content, setting de facto standards that spill over to adjoining Gulf markets.

The wider Gulf Cooperation Council benefits from high disposable income and chronic water scarcity, sustaining a robust bottled-water pipeline. The UAE’s impending single-use plastic restrictions, effective in 2026, act as a catalyst for aluminum and paperboard adoption. Kuwait and Qatar, though smaller, mirror sustainability mandates, nudging regional brand owners toward harmonized packaging portfolios across the Middle East and Africa soft drinks packaging market.

Across Africa, South Africa’s enforced EPR since 2021 positions it as a regulatory bellwether. South Africa recorded the region’s fastest 5.86% CAGR as mandatory EPR raised awareness and bolstered recycling rates that justify premium formats. Rising middle-class purchasing power feeds demand for premium cartons and energy drinks, while established retail chains broaden distribution of convenience packs. Nigeria and Egypt, with large urban populations, promise volume but still wrestle with collection infrastructure deficits that restrain recycled substrate uptake. Cross-continental trade routes improve as Red Sea and East African ports modernize, allowing Middle Eastern polymer surplus to backfill African resin shortfalls and tightening MEA integration.

Competitive Landscape

Global incumbents maintain a balanced yet contested foothold. Ball Corporation streamlined its presence by selling a UAE joint venture stake but reinforcing Saudi assets, illustrating a portfolio pivot that retains exposure to the largest national market while trimming lower-return geographies. Crown Holdings completed a multi-year global can expansion, enabling MEA supply without large fresh capex and freeing funds for decorative and tethered-cap upgrades.[4]“Crown Holdings Reports FY 2024 Results,” Crown Holdings, crowncork.com

M&A reshapes the supplier map. Sonoco’s USD 3.9 billion Eviosys buy enriches metal can depth, while Amcor’s planned USD 8.4 billion Berry Global acquisition would fuse rigid and flexible plastic expertise at scale. Both deals enhance end-to-end offerings, vital as brand owners seek fewer but broader suppliers. SIG’s carton bottle launch underscores a focus on convenience and on-the-go shifts, complemented by Egyptian recycling pilots that boost collection rates.

Technology competition centers on aseptic fillers, lightweighting, and digital decoration. OEMs that furnish modular changeovers and multi-substrate handling gain traction as beverage portfolios diversify. Regional converters such as Takween and Arabian Plastic Industrial Co. exploit proximity and cost advantages, partnering with European machine makers to bridge technology gaps. As EPR frameworks tighten, recyclers and rPET processors emerge as strategic assets, attracting private-equity interest and embedding circularity into the Middle East and Africa soft drinks packaging market’s value chain.

Middle East And Africa Soft Drinks Packaging Industry Leaders

Tetra Pak International SA

SIG Group AG

Amcor plc

Ball Corporation

Crown Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Castillo Hermanos agreed to acquire Harvest Hill Beverage Company, owner of SunnyD, Juicy Juice, and Little HUG.

- April 2025: KJ Holding Corp acquired plant-based drink startup Mela Water to fast-track functional hydration offerings.

- March 2025: PepsiCo announced the acquisition of prebiotic soda brand Poppi for USD 1.95 billion, broadening its functional beverage slate.

- February 2025: Ball Corporation completed the acquisition of Florida Can Manufacturing for USD 160 million to add U.S. aluminum capacity and hedge tariff risks.

Middle East And Africa Soft Drinks Packaging Market Report Scope

The scope of the study includes glass bottles, vials/ampoules, jars, and other types of containers. As part of the scope of the report, key end-user industries, such as beverage, food, beauty, personal care, and cosmetics, healthcare and pharmaceuticals, and other end-user industries, have been considered. The market is segmented as follows:

By Primary Material Used

| Plastic |

| Paper and Paperboard |

| Glass |

| Metal |

| Others |

By Packaging Format

| Bottles |

| Cans |

| Cartons / Aseptic Bricks |

| Pouches and Sachets |

| Others |

By Beverage Type

| Bottled Water |

| Juices and Nectars |

| Carbonated Soft Drinks |

| Ready-to-Drink Tea and Coffee |

| Sports and Energy Drinks |

| Others |

By Pack Capacity

| ≤330 mL |

| 331 – 500 mL |

| 501 – 1 000 mL |

| >1 000 mL |

By Region

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Primary Material Used | Plastic | |

| Paper and Paperboard | ||

| Glass | ||

| Metal | ||

| Others | ||

| By Packaging Format | Bottles | |

| Cans | ||

| Cartons / Aseptic Bricks | ||

| Pouches and Sachets | ||

| Others | ||

| By Beverage Type | Bottled Water | |

| Juices and Nectars | ||

| Carbonated Soft Drinks | ||

| Ready-to-Drink Tea and Coffee | ||

| Sports and Energy Drinks | ||

| Others | ||

| By Pack Capacity | ≤330 mL | |

| 331 – 500 mL | ||

| 501 – 1 000 mL | ||

| >1 000 mL | ||

| By Region | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Middle East and Africa soft drinks packaging market today?

In 2026 the market stands at USD 12.63 billion and is tracking toward USD 15.81 billion by 2031.

Which material leads beverage packaging across the region?

Plastic—including PET bottles—held 52.05% share in 2025, though cartons are growing fastest at a 6.05% CAGR.

Why is Saudi Arabia pivotal for suppliers?

The kingdom commands 34.80% of regional value, fueled by Vision 2030 incentives that localize can and PET production.

What is driving demand for small packs?

Urban lifestyles and convenience retail boost ≤330 mL formats, which are expanding at a 5.55% CAGR.

How are sustainability rules reshaping packaging choices?

EPR fees and upcoming single-use bans in the Gulf accelerate shifts toward aluminum, paperboard, and tethered-cap solutions.

Which beverage category is growing quickest?

Ready-to-drink tea and coffee leads with a 5.95% CAGR, supported by aseptic filling and changing consumer routines.

Page last updated on: