Barite Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

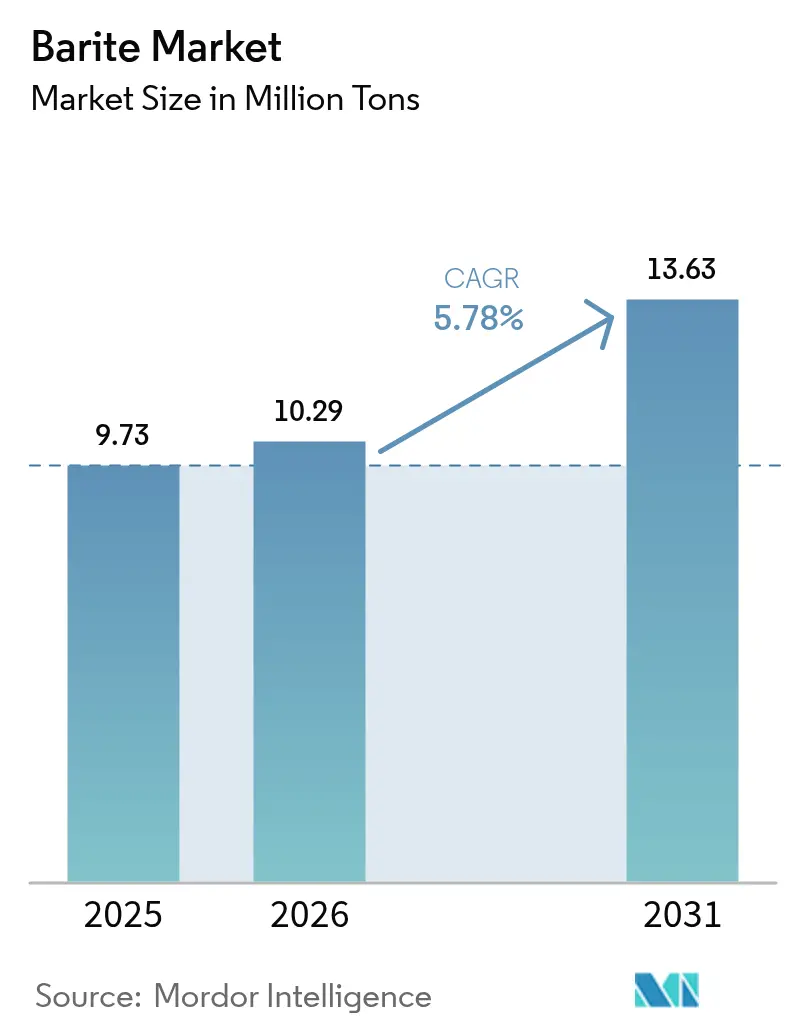

| Market Volume (2026) | 10.29 Million tons |

| Market Volume (2031) | 13.63 Million tons |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

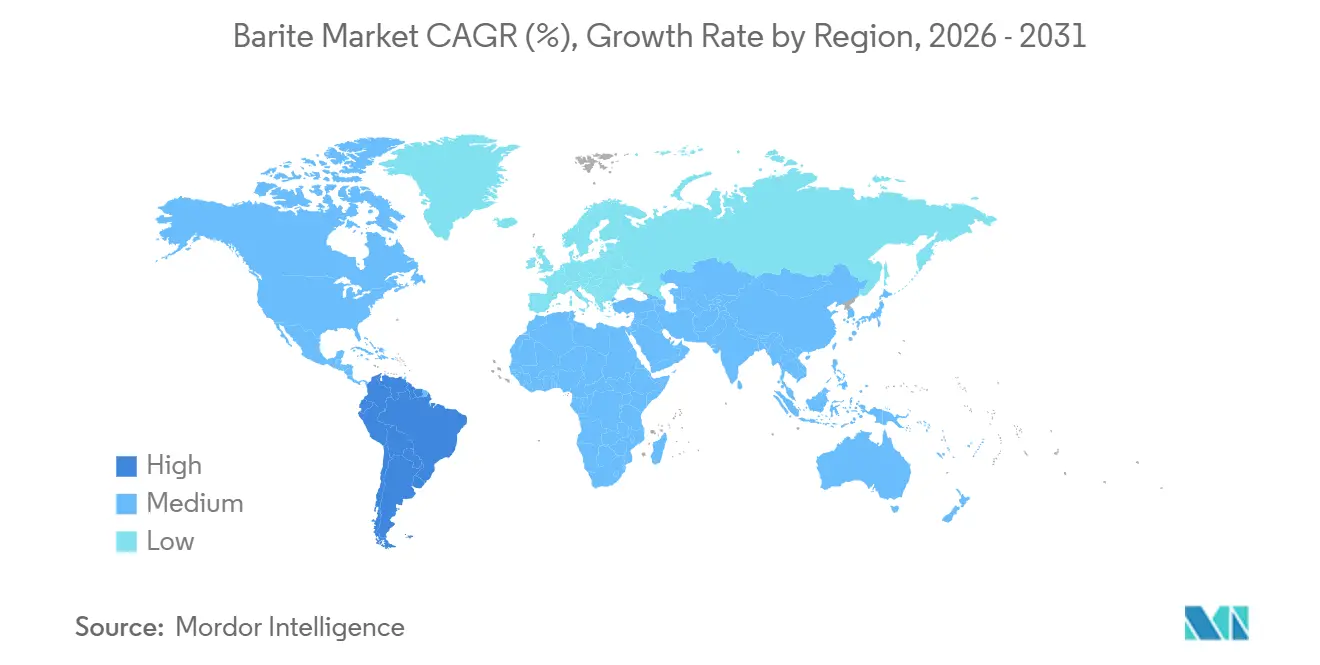

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Barite Market Analysis by Mordor Intelligence

The Barite Market size was valued at 9.73 million tons in 2025 and is estimated to grow from 10.29 million tons in 2026 to reach 13.63 million tons by 2031, at a CAGR of 5.78% during the forecast period (2026-2031). High-specific-gravity grades remain indispensable in drilling fluids, sustaining a solid demand floor even when rig activity fluctuates. Emerging uses in medical diagnostics, radiation-shielding polymers, and specialty composites are broadening the customer base and gradually reducing dependence on oil-price cycles. Chinese export-quota cuts in 2024 raised spot prices 12% in early 2025 and catalyzed a geographic re-allocation of supply toward India and Morocco. Automated dosing systems that cut barite waste by 8-10% on long laterals are improving project economics for offshore and unconventional wells alike. Meanwhile, synthetic hematite and ilmenite blends are gaining a measured foothold, introducing competitive pressure but not yet displacing the mineral’s entrenched role in most drilling programs

Key Report Takeaways

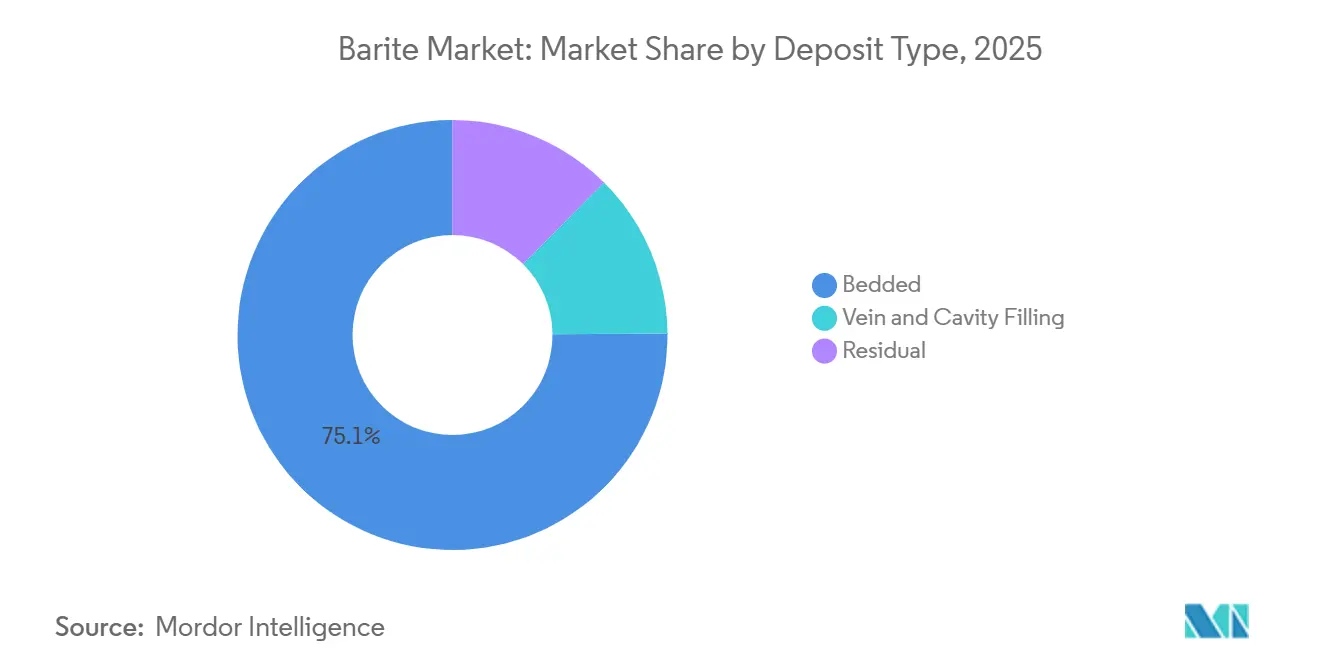

- Bedded deposits led with 75.12% of the Barite market share in 2025, while residual deposits are projected to post the fastest 6.12% CAGR during the forecast period (2026-2031).

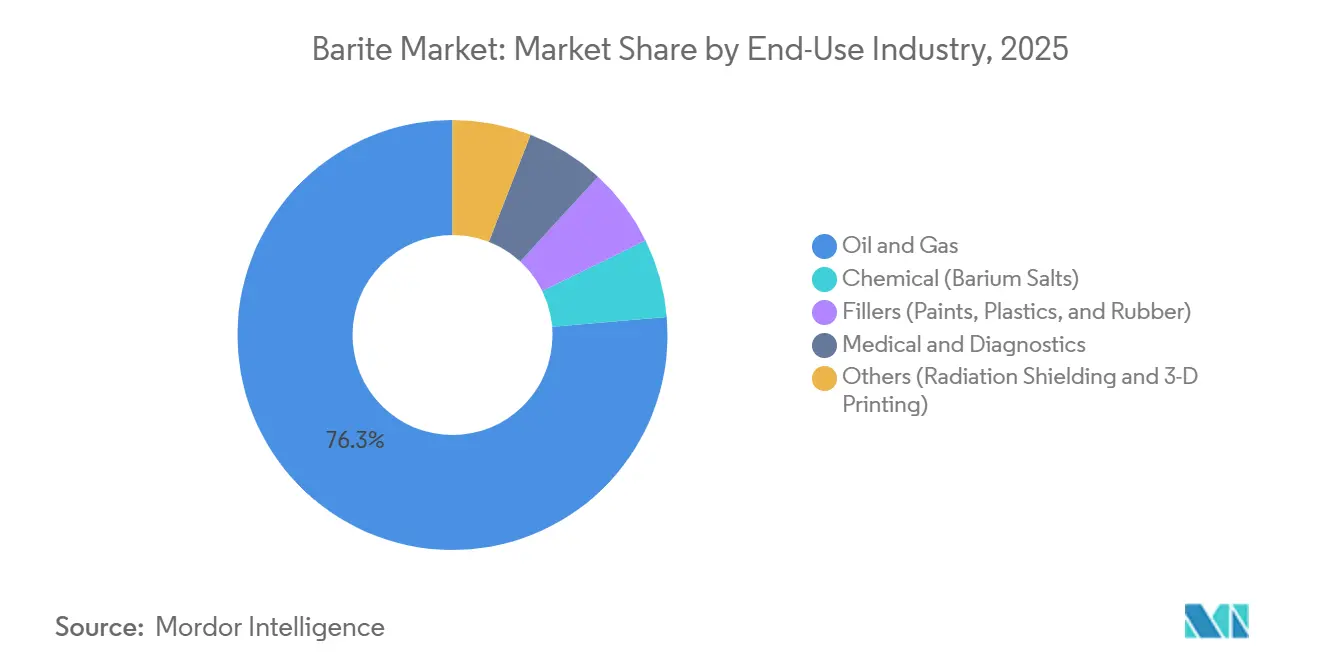

- Oil and gas applications dominated with a 76.33% share of the Barite market in 2025, but medical and diagnostics are expected to expand at a 6.31% CAGR during the forecast period (2026-2031).

- The Asia-Pacific region held 42.21% of the Barite market share in 2025, yet South America is forecasted to grow at the fastest growth rate of 6.11% CAGR over the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Barite Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming deep-water and HPHT drilling in Latin America | +1.20% | South America (Brazil pre-salt, Argentina offshore), spillover to West Africa | Medium term (2-4 years) |

| Rise of unconventional hydrocarbons in North America | +0.90% | United States (Permian, Haynesville), Canada (Montney, Duvernay) | Short term (≤ 2 years) |

| Infrastructure stimulus in India's oilfield services | +0.80% | India (KG Basin, Andaman Sea), with ripple effects across South Asia | Medium term (2-4 years) |

| High-gravity barite grades enabling lower mud volumes | +0.60% | Global, with early adoption in North Sea, Gulf of Mexico, and Middle East | Long term (≥ 4 years) |

| Barite-polymer composites for 3-D-printing filaments | +0.30% | North America and Europe (medical devices, aerospace tooling), emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Booming Deep-Water and HPHT Drilling in Latin America

Brazil’s pre-salt province is setting the regional pace, requiring mud weights of 16-18 lb/gal that translate to more than 400 kg of barite per cubic meter of drilling fluid[1]BP plc, “Bumerangue Discovery Update,” bp.com. Petrobras and partners have pre-positioned inventories at Rio de Janeiro to avoid supply-vessel demurrage, a strategy copied by operators in Argentina’s Austral Basin. Schlumberger reported a 15% YoY (Year-Over-Year) drilling-revenue jump in Latin America during 2025, underscoring the barite market momentum. Floating Production Storage and Offloading (FPSO) deployments with ultra-deep subsea tie-backs further hard-wire demand because any fluid-density shortfall risks well control incidents. These structural factors elevate Latin America to the fastest-growing export destination for high-SG barite over the next four years.

Rise of Unconventional Hydrocarbons in North America

Longer laterals in the Permian and Haynesville consume 30-40 tons of barite for every extra 1,000 feet drilled, anchoring volume even when rig counts decline. Canada’s condensate-rich Montney and Duvernay plays mirror this pattern as higher mud weights manage gas influxes[2]Natural Resources Canada, “Montney and Duvernay Activity,” nrcan.gc.ca. While public-equity pressure curbs aggressive spending, the technical need for high-density fluids creates a baseline that insulates a portion of regional barite demand. Automated mud-weight management tools are also limiting wastage, but the efficiency gains are smaller than the volume pull created by longer wells.

Infrastructure Stimulus in India’s Oilfield Services

ONGC’s USD 550 million appraisal push in the Krishna-Godavari Basin and deepwater Andaman Sea program is fully relying on Mangampet-sourced barite that meets API 13A specs. The Production Linked Incentive scheme rewards domestic beneficiation, prompting miners to add wet-grinding and magnetic-separation lines. As a result, India is redirecting ore that once went to Chinese processors toward in-house upgrading, nudging China’s finished-barite export share down by several points. This reshoring trend positions India as a swing supplier for Middle East and Southeast Asian drillers facing Chinese export-quota constraints.

High-Gravity Barite Grades Enabling Lower Mud Volumes

Premium ores testing at 4.35-4.40 SG let drillers hit density targets with 8-10% fewer solids. Halliburton’s Baroid blend delivered a 12% fluid-volume cut on a Gulf of Mexico deepwater well, shaving non-productive time and storage costs. Quality control remains stringent because elevated silica or carbonate must be stripped out, adding USD 15-20 per ton in beneficiation expense. Operators accept the premium because denser particles settle more slowly, reducing differential sticking risks that can cost millions in sidetracks. These benefits outweigh the incremental cost in harsh-environment basins where downtime penalties are severe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Synthetic hematite mud substitutes | -0.50% | Global, with early adoption in North Sea, West Africa, and Middle East HPHT wells | Medium term (2-4 years) |

| Volatility in crude-linked drilling budgets | -0.70% | North America land markets, with secondary effects in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Radio-opacity regulations curbing filler grades | -0.40% | Europe and North America (medical and industrial filler applications), potential spread to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Synthetic Hematite Mud Substitutes

Hematite’s 5.0-5.3 SG allows operators to hit 18 lb/gal densities with 25% less solids, trimming hydraulic horsepower and bit wear. Norwegian North Sea operators pioneered these blends, cutting equivalent circulating density by 0.3-0.5 lb/gal. Cost parity is inching closer as Chinese steel-mill by-products flood the market at USD 180 per ton versus barite’s USD 140 per ton. If hematite penetration rises from 8% to 12% of weighting-agent volumes by 2029, roughly 350,000 tons of annual barite demand could be displaced. Ilmenite and manganese tetroxide remain niche due to rheological concerns, keeping overall substitution pressure moderate for now.

Volatility in Crude-Linked Drilling Budgets

Brent dipping from USD 80 in 2024 into the low USD 70s in 2025 triggered 6% fewer North American land rigs by January 2026. Distributors slashed inventories, and marginal pits idled, shaving up to 15% off spot barite prices within one quarter. International programs by Middle East National Oil Companies (NOCs) and Asian state firms continued drilling, preventing a global demand contraction. The uneven impact highlights why miners with sales diversity outperform those tied exclusively to the United States shale, where budgets can swing within weeks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deposit Type: Bedded Reserves Support Cost Leadership

Bedded deposits captured 75.12% of 2025 volume, underpinning the barite market size through laterally continuous ore bodies that allow low-strip-ratio open-pit mining. These seams in China’s Guizhou and India’s Cuddapah Basin often exceed 10 meters thick and hit API purity straight from the pit, saving beneficiation costs that vein miners must absorb. The barite market share commanded by bedded ore is therefore unlikely to erode quickly, even as environmental reviews for new quarries stretch beyond two years.

Residual deposits are forecast to grow at a 6.12% CAGR to 2031, outpacing overall barite industry expansion. Near-surface lateritic zones in Andhra Pradesh and West Africa require only washing and screening, shortening permitting cycles and lowering capex. Improved hydrocyclone classification has lifted residual-ore recovery rates to 78% in 2025, narrowing the cost gap with bedded producers. As freight rates stay volatile, inland residual sources located closer to domestic basins gain an incremental advantage by trimming transport expense.

By End-Use Industry: Medical Segment Gains Strategic Weight

Oil and gas applications held 76.33% of consumption in 2025, a dominance rooted in drilling-fluid necessity. However, the demand for barite in medical and diagnostics is growing at a CAGR of 6.31% during the forecast period (2026-2031), nudging the barite market size toward a more diversified demand mix. Each CT or fluoroscopy study uses up to 400 g of United States Pharmacopeia (USP)-grade material, and the rapid rollout of outpatient imaging centers adds steady tonnage not tied to crude cycles.

Chemical derivatives such as barium carbonate provide a demand hedge linked to glass and ceramics rather than energy investment. Filler-grade barite in paints, plastics, and rubber is valued for opacity and UV resistance. Additive-manufactured radiation-shielding filaments are rising as aerospace and medical prototyping embrace 3D printing. Producers capable of meeting stringent purity monographs can command USD 800-1,200 per ton, tripling drilling-grade margins and shielding revenue against oil-price swings.

Geography Analysis

Asia-Pacific accounted for 42.21% of the 2025 volume, with China supplying 3.2 million tons from Guizhou alone. India’s Mangampet belt added 1.1 million tons that met API specs without beneficiation, enabling APMDC to capture premium sales into Middle East offshore campaigns. Export-quota cuts slashed Chinese outbound shipments 18% in 1H 2025, pushing buyers to pay 10-12% higher landed costs from Indian and Moroccan sources. Deepwater projects in Malaysia’s Sarawak and Indonesia’s Mahakam keep regional imports firm, while Japan and South Korea remain wholly import-dependent.

In North America, the United States' production from Nevada and Georgia covers 40% of domestic demand, leaving a balance imported from China, India, and Mexico. Canada relies on United States rail imports to supply Alberta heavy oil and British Columbia condensate plays that require equal to or more than 12 lb/gal muds. Mexico’s Campeche Basin continues a steady draw as Pemex pursues infill wells, sourcing barite from Coahuila and Sonora.

Europe's demand, driven by North Sea HPHT wells using hematite-barite blends to stay within fracture limits. The region is almost entirely import-dependent after legacy German and United Kingdom mines shuttered. South America, forecast to grow at a CAGR of 6.11% during the forecast period (2026-2031), is propelled by Brazil’s pre-salt and Argentina’s Vaca Muerta, where Petrobras sealed a USD 1.2 billion integrated-services deal bundling barite supply. In Middle East and Africa, GCC offshore rigs import high-grade barite, while Morocco and Algeria export to Europe and West Africa, creating a regional buffer against Asian supply shocks.

Competitive Landscape

The Barite market is moderately fragmented. Strategically, suppliers with upstream mine ownership plus downstream blending and logistics assets are better insulated from policy shocks and freight inflation. Smaller traders reliant on single-country sourcing face price-volatility risk, especially when quotas change. Patent activity in barite-polymer composites remains sparse, suggesting an early-stage opportunity for niche material science entrants before commoditization sets in.

Barite Industry Leaders

Andhra Pradesh Mineral Development Corporation (APMDC)

Cimbar Performance Minerals

Halliburton

SLB

Guizhou Saboman Import & Export Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Voyageur Pharmaceuticals Ltd., a Canadian developer of pharmaceutical-grade barium and iodine for medical imaging contrast media, announced independent laboratory test results for its barium sulfate active pharmaceutical ingredient (API). The API barite was sourced from the company’s Frances Creek barite property in British Columbia.

- March 2025: Chinese barite producers, including Shaanxi Fuhua Chemical Co., Ltd. and Jimei Jinghua Technology, among others, have announced coordinated price increases of CNY 200 per ton, reflecting the tightening of the supply chain and the pressures on raw material costs that are affecting global pricing dynamics.

Global Barite Market Report Scope

Barite is a mineral consisting of barium sulfate, typically occurring as colorless prismatic crystals or thin white flakes. Barite is usually used as an additive in drilling mud, as it increases hydrostatic pressure, allowing it to compensate for high-pressure zones experienced during the drilling.

The barite market is segmented by type, end-user industry, and geography. By type, the market is segmented into bedded, vein and cavity filling, and residual. By end-user industry, the market is segmented into oil and gas, chemical, and fillers. The report also covers the market size and forecasts for the barite market in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Bedded |

| Vein and Cavity Filling |

| Residual |

| Oil and Gas |

| Chemical (Barium Salts) |

| Fillers (Paints, Plastics, Rubber) |

| Medical and Diagnostics |

| Others (Radiation Shielding, 3-D Printing) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Deposit Type | Bedded | |

| Vein and Cavity Filling | ||

| Residual | ||

| By End-use Industry | Oil and Gas | |

| Chemical (Barium Salts) | ||

| Fillers (Paints, Plastics, Rubber) | ||

| Medical and Diagnostics | ||

| Others (Radiation Shielding, 3-D Printing) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected barite market size by 2031?

The Barite market size is forecast to reach 13.63 million tons by 2031 at a 5.78% CAGR from 2026-2031.

Which segment is growing fastest within barite demand?

Pharmaceutical-grade barite for medical diagnostics is expanding at a 6.31% CAGR through 2031, outpacing oil and gas growth.

How will export quotas affect global barite prices?

China’s 15% quota cut for 2026 already lifted Asian spot prices 11%; continued restrictions are likely to keep prices firm while buyers diversify toward India and Morocco.

What regions offer the strongest demand upside?

South America leads with a 6.11% CAGR during the forecast period (2026-2031) owing to Brazil’s pre-salt and Argentina’s Vaca Muerta, while Asia-Pacific remains the largest consuming region.

Page last updated on: