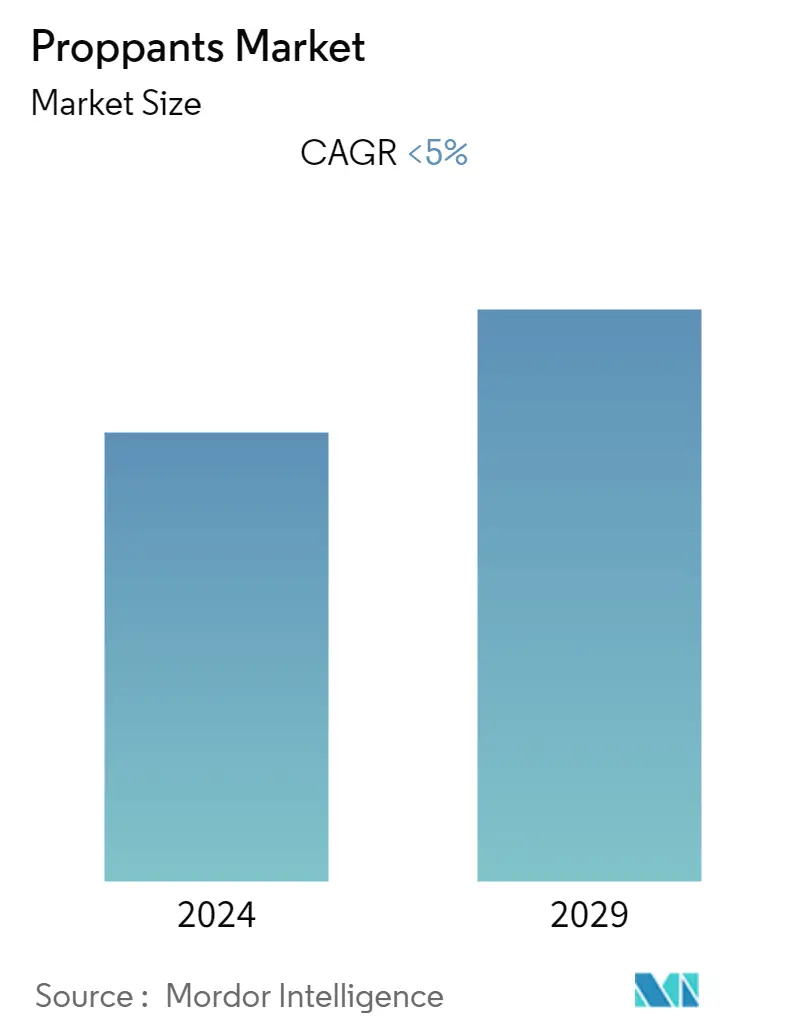

Proppants Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | < 5.00 % |

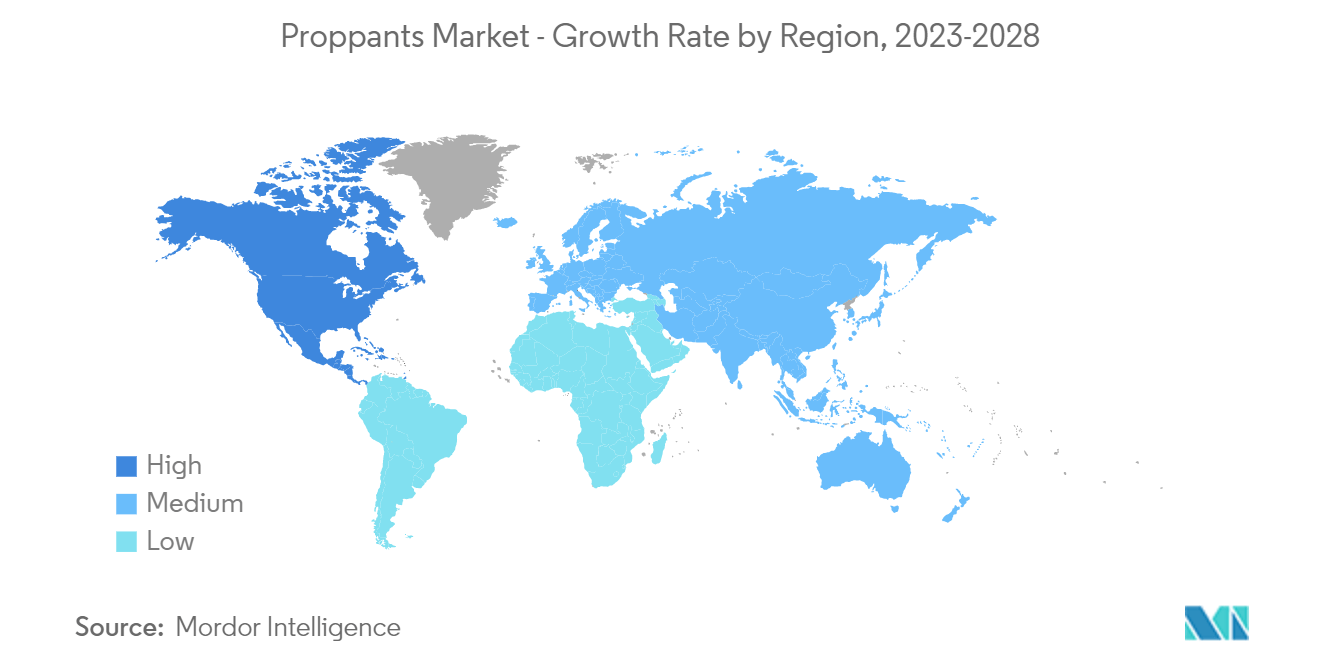

| Fastest Growing Market | North America |

| Largest Market | North America |

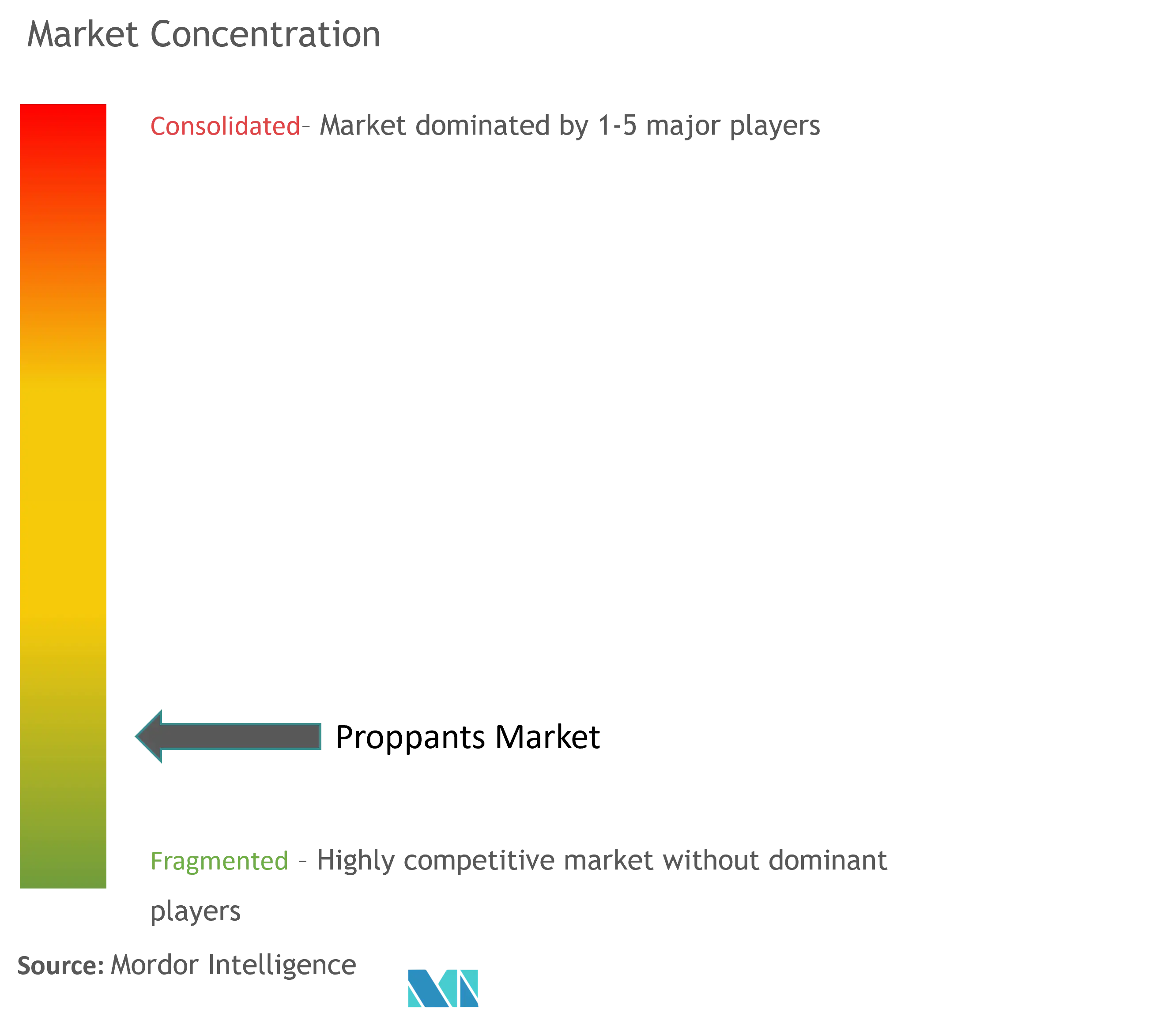

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Proppants Market Analysis

The proppants market is estimated at 157 million tons currently and is expected to reach 204 million tons over the forecast period, registering a CAGR of around 5% during the forecast period.

The major application of proppants is in oil and gas wells. Due to COVID-19 and geopolitics, the demand for crude oil decreased as markets had been over-supplied, thus forcing OPEC+ producers to cut the output. It is expected to affect the demand for various proppants such as frac sand, resin coated, and ceramics.

- In the medium term, improvements in fracking technology and increasing shale gas production activities are expected to drive the market studied. The Energy Information Administration (EIA) expects shale natural gas and oil production to double by 2040. According to EIA, shale gas and tight oil production will increase from about 14 trillion cubic feet (Tcf) in 2015 to 29 Tcf in 2040, enhancing market demand.

- However, environmental concerns and stringent regulations will likely hinder the studied market's growth.

- North America dominated the market across the world, with the largest consumption from the United States.

- Shifting focus toward using ceramic proppants is expected to provide opportunities for the market studied.

Proppants Market Trends

Frac Sand Segment Expected to Dominate the Market

- Frac sand proppants are the market's most widely used category for hydraulic fracturing. Frac sand proppants are highly pure and durable quartz sand with round grains.

- They are majorly made out of sandstone. Their size ranges from about 0.1 mm to 2 mm in diameter, depending on the requirement of the fracking job.

- Owing to its efficiency, low cost, and availability, frac sand accounts for around 83% of the total proppants usage. Superior characteristics of high-quality frac sand such as high-purity silica sand, a spherical shape that helps in enabling it to be further carried in hydraulic fracturing fluid with minimal turbulence. It possesses the durability to resist crushing forces of closing fractures, enhances its usage as a proppants, and thus increases the market demand.

- Raw frac sand is most widely used due to its broad applicability in oil and natural gas wells and its cost advantage relative to other proppants.

- Canada is producing shale gas since 2008, which is expected to increase and account for 30% of Canada's total natural gas production by 2040.

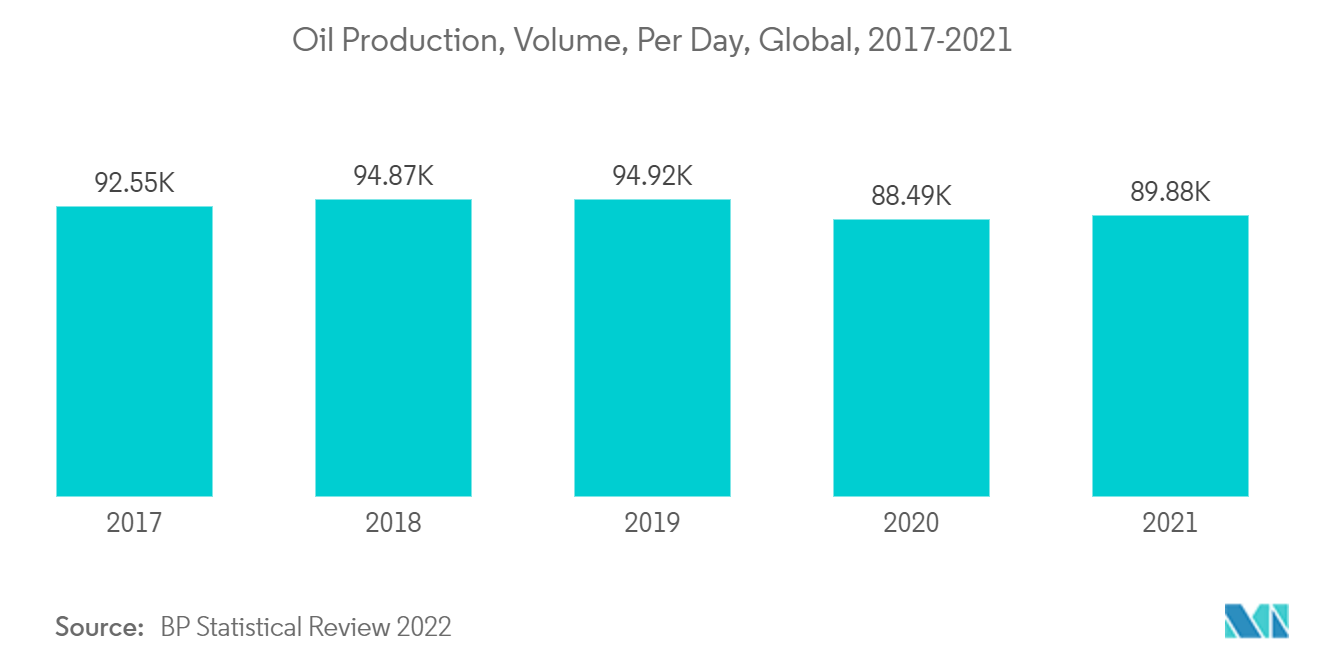

- According to the BP Statistical Review of World Energy 2022, global oil production hiked by 1.4 million barrels per day, with a three-fourth increase accountable to the OPEC+ oil production volume.

- ADNOC awarded framework agreements worth USD 658 million in March 2022 to expand drilling operations and crude oil production capacity further. ADNOC announced three oil discoveries in May 2022. One was at Bu Hasa, Abu Dhabi's largest onshore field, with a crude oil production capacity of 650,000 barrels per day.

- Further, developing ADNOC's downstream activities is central to the company's 2030 Integrated Strategy. ADNOC launched a USD 45 billion effort to upgrade its downstream operations.

- In May 2022, the development of the Crux natural gas field off the coast of Western Australia was given final investment approval by Shell Australia Pty Ltd (Shell Australia) and its joint venture partner, SGH Energy. The current Prelude floating liquefied natural gas (FLNG) facility will receive additional natural gas supplies from Crux. The project's construction was started in 2022, and the first gas is expected in 2027.

- Similarly, China is among the first countries outside North America to develop shale resources. Shale gas is projected to account for more than 40% of the country's total natural gas production by 2040. It is likely to make the country the second-largest shale gas producer in the world after the United States.

- With increasing hydraulic fracturing activities, the demand for frac sand is projected to increase over the forecast period.

North America Region to Dominate the Market

- The United States is one of the leading countries globally in exploring unconventional crude oil reserves and applying hydraulic fracturing for the same.

- The quantity of oil produced from hydraulically fractured wells is increasing significantly compared to that produced from conventionally fractured wells.

- With growing hydraulic fracturing applications in the country, especially for shale gas and tight oil purposes, the demand for proppants is witnessing a positive impact.

- About 95% of new wells drilled in the United States are hydraulically fractured, accounting for two-thirds of the total marketed natural gas production and about half of the country's crude oil production.

- The United States is one of the world's largest consumers and exporters of oil and gas. According to US Energy Information Administration (EIA), Crude oil production in the United States was expected to average 11.9 million barrels per day (b/d) in 2022, up 0.7 million b/d from 2021. Also, the output will exceed 12.8 million b/d in 2023, breaking the previous annual average record of 12.3 million b/d set in 2019.

- Pipeline companies completed 14 petroleum liquids pipeline projects in the United States in 2021. It includes 7 crude oil pipeline projects and 7 hydrocarbon gas liquids pipeline projects. Further, from 2021 to 2025, the United States is expected to begin operations on 169 midstream oil and gas projects, accounting for approximately 69% of all upcoming midstream project starts in North America by 2025.

- Mexico is America's fourth-largest oil producer after the United States, Canada, and Brazil. According to Statista, Mexico's crude oil production averaged around 1.63 million barrels daily in March 2022. Mexico's state-owned oil corporation, Pemex, produced approximately 1.53 million daily barrels. Meanwhile, private company output totaled 97.1 thousand barrels per day that month. Private companies' oil output in Mexico steadily increased in recent years.

- Although COVID-19 severely impacted the price and trade of crude oil, the region is anticipated to witness growth in demand for proppants in the coming years. It is owing to the increasing number of exploration and maturing wells.

- In April 2022, Exxon revealed it would invest USD 10 billion in a brand-new offshore project off the coast of Guyana. It will be the company's fourth oil production development in the nation and the biggest in Latin America. The Guyanan government approved the YellowTail project, which planned to generate 250,000 barrels of oil daily, production starting in 2025.

- However, the environmental and health concerns associated with the hydraulic fracturing process and the changing political scenario in the United States may serve as a restraint for the proppants market in the country.

Proppants Industry Overview

The proppants market is partially fragmented, with no player with a significant share to influence the market. The studied market's major players include Saint-Gobain, Hexion, CARBO Ceramics Inc., COVIA, and U.S. Silica.

Proppants Market Leaders

Hexion

U.S. Silica

CARBO Ceramics Inc.

Covia Holdings LLC

Saint-Gobain

*Disclaimer: Major Players sorted in no particular order

Proppants Market News

- May 2022: CARBO Ceramics Inc. announced the acquisition of Pinnacle Technologies Inc., which provides fracture diagnostic services, fracture mapping services, and fracture simulation models. It will enhance the company's product portfolio for the proppants market.

Proppants Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Improvements in Fracking Technology

4.1.2 Increasing Shale Gas Production Activities

4.2 Restraints

4.2.1 Environmental Concerns and Legislation

4.2.2 Impact of COVID-19 Outbreak

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Volume)

5.1 Product Type

5.1.1 Frac Sand

5.1.2 Resin Coated

5.1.3 Ceramics

5.2 Geography

5.2.1 Asia-Pacific

5.2.1.1 China

5.2.1.2 India

5.2.1.3 Indonesia

5.2.1.4 Malaysia

5.2.1.5 Thailand

5.2.1.6 Vietnam

5.2.1.7 Rest of Asia-Pacific

5.2.2 North America

5.2.2.1 United States

5.2.2.2 Canada

5.2.2.3 Mexico

5.2.3 Europe

5.2.3.1 Germany

5.2.3.2 United Kingdom

5.2.3.3 Russia

5.2.3.4 Norway

5.2.3.5 Rest of Europe

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Rest of South America

5.2.5 Middle-East and Africa

5.2.5.1 Saudi Arabia

5.2.5.2 South Africa

5.2.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%) **/ Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Badger Mining Corporation

6.4.2 CARBO Ceramics Inc.

6.4.3 China Ceramic Proppant (Guizhou) Ltd

6.4.4 ChangQing Proppant

6.4.5 CoorsTek Inc.

6.4.6 Covia Holdings LLC.

6.4.7 Eagle Materials Inc.

6.4.8 Emerge Energy Services (Superior Silica Sands)

6.4.9 Epic Ceramic Proppants Inc.

6.4.10 Fores LTD

6.4.11 General Electric (Baker Hughes Company)

6.4.12 Gongyi Yuanyang Ceramsite Co.,Ltd.

6.4.13 Halliburton

6.4.14 Henan Tianxiang New Materials Co., Ltd.

6.4.15 Hexion

6.4.16 Nika Petrotech

6.4.17 Preferred Sands LLC

6.4.18 Saint-Gobain

6.4.19 Unimin Energy Solutions (Sibelco)

6.4.20 U.S. Silica

6.4.21 Wanli Proppant

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Shifting Focus toward the Usage of Ceramic Proppants

Proppants Industry Segmentation

A proppant is a solid material, usually sand, treated sand, or artificial ceramic materials, used to maintain the openness of an induced hydraulic fracture during or after fracturing. The market is segmented by product type and geography. The market is segmented by product type into frac sand, resin coated, and ceramics. The report also covers the market size and forecasts for the proppants market in 17 countries across major regions. Each segment's market sizing and forecasts are based on volume (million tons).

| Product Type | |

| Frac Sand | |

| Resin Coated | |

| Ceramics |

| Geography | |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

|

Proppants Market Research FAQs

What is the current Proppants Market size?

The Proppants Market is projected to register a CAGR of less than 5% during the forecast period (2024-2029)

Who are the key players in Proppants Market?

Hexion, U.S. Silica, CARBO Ceramics Inc., Covia Holdings LLC and Saint-Gobain are the major companies operating in the Proppants Market.

Which is the fastest growing region in Proppants Market?

North America is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Proppants Market?

In 2024, the North America accounts for the largest market share in Proppants Market.

What years does this Proppants Market cover?

The report covers the Proppants Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Proppants Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Proppant Industry Report

Statistics for the 2024 Proppant market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Proppant analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.