Energy Harvesting Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.38 Billion |

| Market Size (2031) | USD 6.06 Billion |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

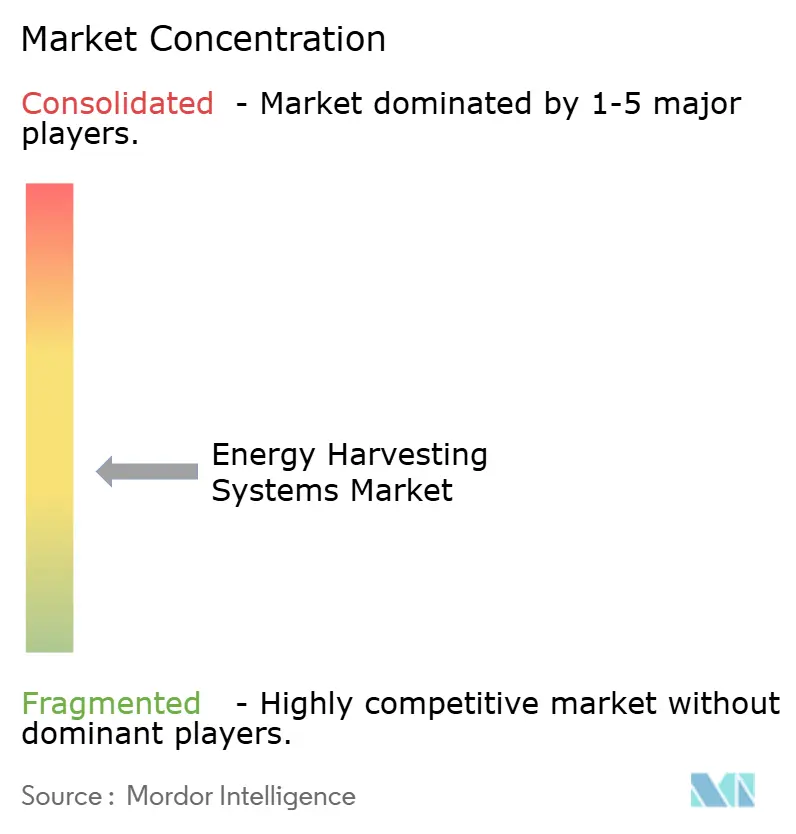

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Energy Harvesting Systems Market Analysis by Mordor Intelligence

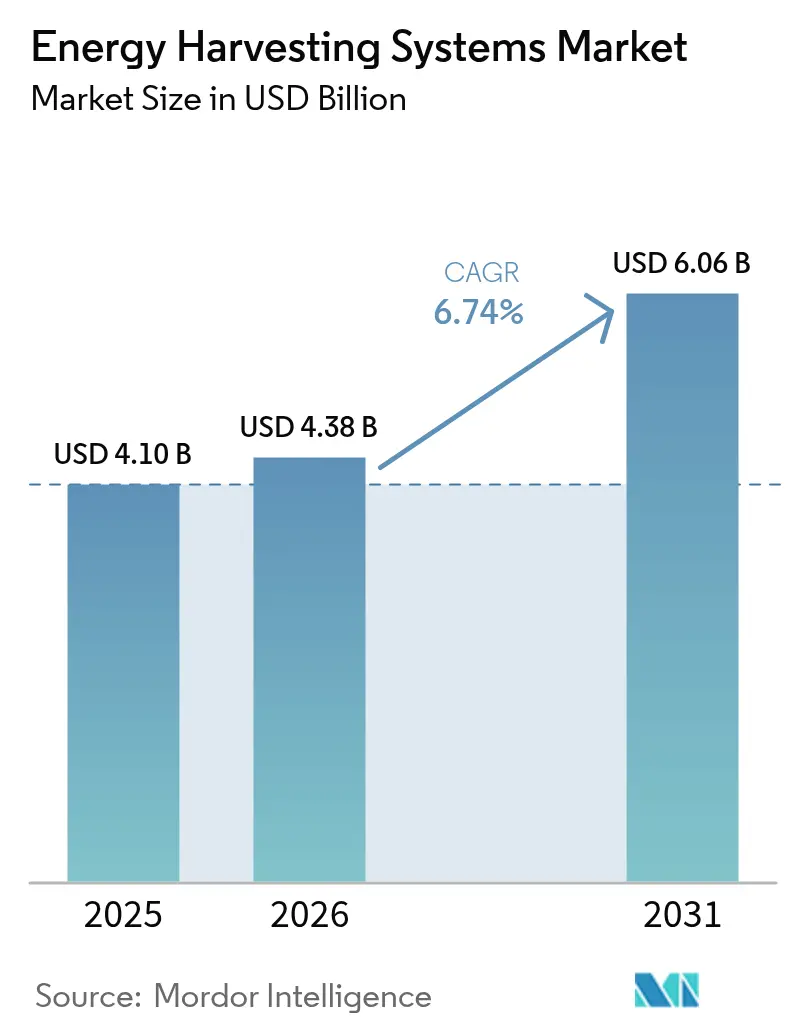

The energy harvesting systems market size in 2026 is estimated at USD 4.38 billion, growing from 2025 value of USD 4.10 billion with 2031 projections showing USD 6.06 billion, growing at 6.74% CAGR over 2026-2031. Rising demand for battery-free Internet-of-Things (IoT) devices and the spread of ultra-low-power electronics across industrial and consumer environments underpin this growth. Momentum stems from rapid miniaturization in power-management integrated circuits that now squeeze sophisticated regulation functions into sub-millimeter footprints, while policy pressure to cut disposable battery waste reinforces the value proposition for energy harvesting solutions. Developers also benefit from ecosystem partnerships that speed time-to-market for turnkey modules and reference designs, further lifting adoption in smart buildings, factories, and wearables. Together, these forces strengthen the energy harvesting systems market outlook during the current decade.

Key Report Takeaways

- By technology, light-based photovoltaic harvesters led with 41.65% of the energy harvesting systems market share in 2025; RF harvesting is projected to expand at a 10.62% CAGR through 2031.

- By application, building and home automation accounted for 29.55% of the energy harvesting systems market size in 2025, while industrial IoT is set to grow at a 9.62% CAGR to 2031.

- By component, power-management ICs held a 37.40% stake in the energy harvesting systems market share in 2025; energy-harvesting transducers represent the fastest-growing component at a 9.05% CAGR.

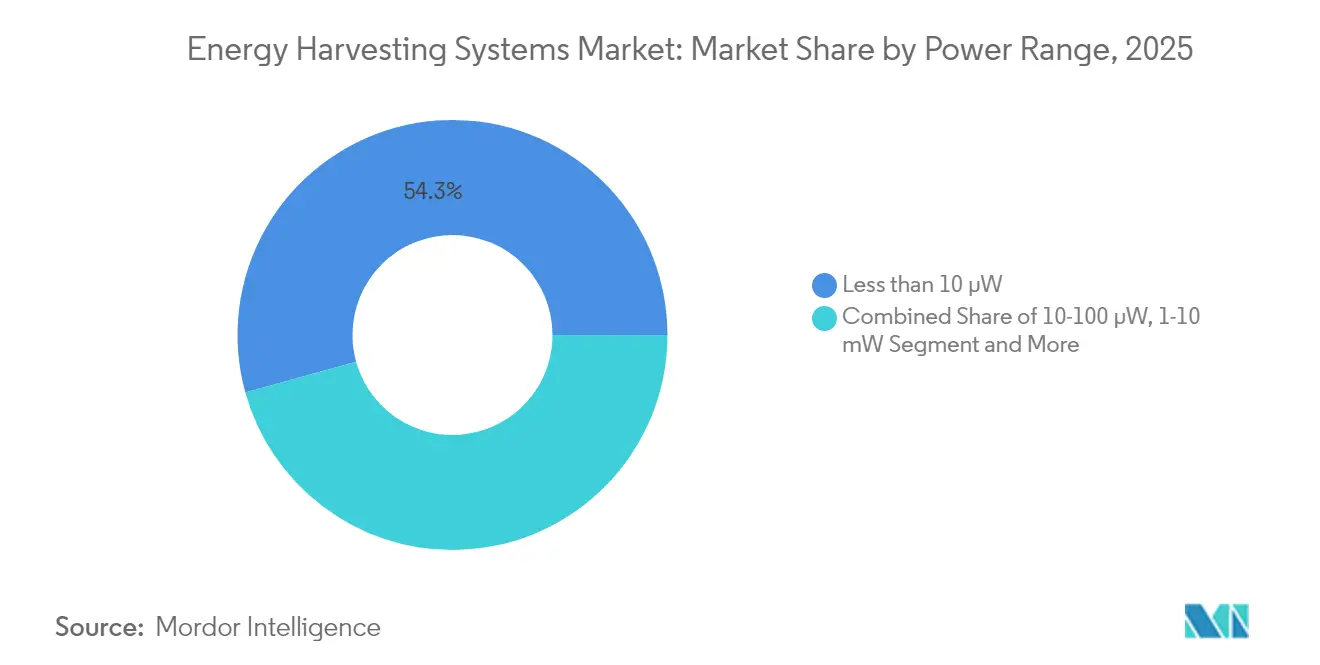

- By power range, the sub-10 µW class commanded 54.30% of shipments in 2025, whereas the 10-100 µW bracket records the highest projected CAGR at 7.62% to 2031.

- By geography, Asia retained 34.70% revenue share in 2025, and the Middle East is positioned for the quickest regional growth at a 8.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Energy Harvesting Systems Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Proliferation of Battery-less IoT Sensor Nodes in Smart Buildings | +2.1% | Europe & North America | Medium term (2-4 years) |

| Mandates for Sustainable Low-Power Automation in APAC Factories | +1.8% | APAC core; spill-over to MEA | Short term (≤ 2 years) |

| Rapid Miniaturization of Ultra-Low-Power MCUs Enabling Sub-µW Thresholds | +1.5% | Global | Long term (≥ 4 years) |

| Growing Deployment of Wireless Condition-Monitoring in Rail & Aviation OEMs | +1.2% | North America & EU | Medium term (2-4 years) |

| Integration of Photovoltaic Harvesters into Wearables & Medical Patches | +0.9% | Global | Long term (≥ 4 years) |

| Smart-City Initiatives and Energy Diversification Mandates in GCC Nations | +0.7% | Middle East (GCC) | Short–Medium term (≤ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Battery-less IoT Sensor Nodes in Smart Buildings

The European Union Ecodesign Regulation 2024/1781 obliges commercial properties to use energy-efficient control systems, which pushes building managers toward battery-free wireless sensors Demonstrations in Paris and Oviedo logged 36.8 kW average power savings after integrating solar and RF-powered sensors that communicate occupancy and environmental data. RF harvesters convert 10-50% of ambient energy and more than 70% in tuned indoor zones, keeping sensors operational for the entire building life cycle. Facility owners increasingly weigh total cost of ownership and find that three battery replacement cycles eclipse initial sensor hardware costs, accelerating migration to harvesting solutions. As procurement teams pivot budgets from maintenance to analytics-ready hardware, the energy harvesting systems market gains sustained demand from the commercial real-estate sector.[1]Rubén Muñiz et al., “Solar-Powered Smart Buildings,” electronics journal, doi.org

Mandates for Sustainable Low-Power Automation in APAC Factories

Industrial groups across China, Japan, and South Korea install harvesters to satisfy corporate carbon pledges and cut unscheduled downtime tied to battery swaps. Telefónica Tech rolled out ATEX-certified thermoelectric generators that power vibration nodes in oil and gas refineries where battery access is tightly restricted. Researchers at the Korea Institute of Science and Technology combined thermoelectric and piezoelectric effects in a hybrid harvester that boosts power output by more than 50% for heavy-machinery monitoring. Dense manufacturing ecosystems allow quick feedback loops between pilot deployments and component suppliers, further trimming bill-of-materials cost. As regulatory audits emphasize energy baselines in production plants, executives increasingly standardize harvesting platforms across multiple factory sites, reinforcing regional momentum.

Rapid Miniaturization of Ultra-Low-Power MCUs Enabling Sub-µW Thresholds

STMicroelectronics’ STM32U3 family delivers 117 CoreMark per milliwatt while drawing only 10 µA per MHz in active mode, a benchmark that qualifies even indoor lighting as a reliable energy source. Renesas RA2A2 devices run at 100 µA per MHz and drop to 0.40 µA in standby, integrating power-budget algorithms for energy harvesting nodes. Lower power budgets widen the pool of viable harvester technologies, and higher harvesting conversion ratios now support edge inference workloads. This virtuous cycle reshapes design priorities so that the default bill-of-materials for next-generation IoT boards starts with a harvester and storage element rather than a primary cell, lifting long-term growth for the energy harvesting systems market.[2]STMicroelectronics, “STM32U3 Launch Press Release,” stocktitan.net

Growing Deployment of Wireless Condition-Monitoring in Rail & Aviation OEMs

European rolling-stock builders mount piezo harvesters on pantographs to feed vibration diagnostics that warn of contact wire fatigue. Aerospace integrators couple flexible piezo films to fuselage panels where flight-induced vibrations generate enough power for autonomous health-monitoring nodes. A prototype quadcopter from the University of Southern Denmark recharges through power lines while inspecting high-voltage cables, removing the downtime linked to battery swaps. Safety regimes in transport sectors justify premium pricing for high-reliability harvesters, and this willingness to pay shortens payback periods for suppliers. As a result, transport OEMs become key reference customers that validate performance claims for emerging harvester materials.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Low Energy Density of Ambient RF in Rural Installations | -1.4% | Global; acute in rural areas | Short term (≤ 2 years) |

| Absence of Universal Power-Management Standards | -1.1% | Global | Medium term (2-4 years) |

| High Upfront Cost of Hybrid Multi-Source Harvesting Architectures | -0.8% | Global | Short-Medium term (≤ 4 years) |

| Limited Interoperability Between Proprietary RF Harvesting Protocols | -0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Energy Density of Ambient RF in Rural Installations

Field trials show that 70% of growers abandon wireless sensor pilots because nodes exhaust batteries faster than expected, a gap magnified where RF density dips below harvestable levels. Agritech integrators now blend small solar tiles with vibration strips on irrigation pumps to hedge against cloudy seasons and weak RF signals. Even so, hybrid designs raise costs and complicate maintenance schedules, delaying wide deployment in cost-sensitive farms. Until rural connectivity infrastructure expands, this restraint caps immediate upside for the energy harvesting systems market in agriculture and environmental monitoring.

Absence of Universal Power-Management Standards

Power-management integrated circuits vary by harvester type and lack harmonized pinouts or firmware interfaces, which forces system integrators to maintain multiple design variants. Although the EU requires USB-C for external power supplies from 2025 onward, no comparable directive covers ambient energy modules. Custom engineering adds weeks to project timelines and inflates non-recurring expenses, discouraging procurement teams that value vendor-agnostic architectures. Standardization efforts under IEEE P2668 remain in early stages, so interoperability challenges will persist through the medium term and temper the pace at which the energy harvesting systems market penetrates multi-vendor IoT platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: RF Harvesting Drives Next-Generation Ambient IoT

Light-based photovoltaic harvesters controlled 41.65% of the energy harvesting systems market share in 2025. Superior maturity, low cost per watt, and predictable diurnal energy profiles keep photovoltaics in pole position for building and outdoor installations. RF harvesting, however, posts an 10.62% CAGR to 2031 as dense 5G deployments raise ambient electromagnetic levels that can be scavenged for sensor power. Vibration and electromagnetic harvesters serve machinery where rotational energy is plentiful, while thermal Seebeck devices find niches in automotive exhaust and industrial furnaces. Hybrid architectures that blend multiple modalities deliver continuity during light or motion lulls, appealing to mission-critical use cases. The energy harvesting systems market gains resilience as integrators pair intelligent maximum-power-point tracking with adaptive storage to optimize yield across variable sources.

Hybrid proof points abound. Ambient Photonics records triple the power output in 200 lux compared with legacy cells, unlocking indoor remote controls and keyboards. Meanwhile, the Korea Institute of Science and Technology reports a 50% power bump by merging thermoelectric and piezoelectric channels in a cantilever platform. These advances compress payback periods and extend uptime guarantees, encouraging original-equipment manufacturers to specify multi-source designs in request-for-proposal documents. As RF harvesting efficiency rises and component prices drop, the energy harvesting systems market will witness converged modules that auto-select the most productive source every few milliseconds to sustain load demands.

By Component: Power Management ICs Enable System Integration

Power-management ICs captured 37.40% of the energy harvesting systems market size in 2025 by value because every harvester topology requires accurate voltage regulation and storage orchestration. Energy-harvesting transducers exhibit a 9.05% CAGR to 2031 as designers diversify beyond single-source architectures and need specialized conversion layers. Thin-film batteries and supercapacitors buffer intermittent energy streams, while ultra-low-power microcontrollers perform the analytics that justify sensor deployments. STMicroelectronics’ SPV1050 achieves up to 99% conversion efficiency for photovoltaic and thermoelectric inputs, highlighting how sophisticated regulation extends node lifetimes. Asahi Kasei’s AP4413 series integrates cell-balancing and trickle-charge control in a 1.43 mm² die, bringing harvesting solutions to cost-sensitive consumer gadgets.

Industry roadmaps converge on system-on-chip packages that embed harvesting front ends, buck-boost converters, and microcontrollers within a single laminate. This consolidation removes board-level interconnect losses and simplifies certification, expanding addressable use cases from industrial automation to smart toys. Over the forecast window, falling ASPs for integration-ready PMICs will spur volume shipments, further fortifying the energy harvesting systems market.

By Power Range: Sub-10 µW Segment Dominates Ultra-Low-Power Applications

Devices operating below 10 µW represented 54.30% of shipments in 2025, reflecting widespread deployment of duty-cycled sensors that wake only to log temperature or occupancy. A new wave of edge-AI workloads lifts interest in the 10-100 µW band, which is set to grow at 7.62% annually. Above 1 mW sit condition-monitoring systems that sample high-resolution vibration signatures or transmit real-time video in defense settings. Researchers at Daegu Gyeongbuk Institute of Science and Technology unveiled a stretchable piezo film that boosts strain energy conversion by 280×, making sub-µW wearables practical without external batteries. Improvements in energy-aware firmware such as adaptive sampling widen functional envelopes while keeping average power budgets under micro-watt thresholds. Consequently, more designers target the sub-10 µW class, elevating unit volumes and reinforcing its dominance within the energy harvesting systems market.

Over time, machine-learning accelerators with 100 TOPS per watt enable local inference at milliwatt levels, blurring boundaries between the mid-range and high-power brackets. Integrators increasingly design boards with power-scalable domains that run in deep sleep at sub-µW yet spike to tens of milliwatts for short compute bursts. This architectural flexibility maximizes harvested-energy utilization and positions the energy harvesting systems market for cross-vertical expansion.

By Application: Industrial IoT Accelerates Predictive Maintenance Adoption

Industrial IoT applications advance at a 9.62% CAGR as operators retrofit rotating equipment with sensors that harvest mechanical or thermal energy, eliminating hazardous battery swaps. Building and home automation retained the largest 2025 share at 29.55% because EU regulations compel energy-efficient control systems. Healthcare wearables rely on flexible photovoltaic and RF harvesters to deliver continuous monitoring without user intervention, while transport sectors embed harvesters in rail tracks and aircraft fuselage for structural health analytics. Telefónica Tech’s ATEX-certified thermogenerators now power wireless nodes in explosive gas zones, highlighting cost avoidance in maintenance downtime.

Consumer electronics vendors adopt photovoltaic cells for remote controls that never need replacement batteries, a selling point tied to sustainability goals. Defense programs specify RF and vibration harvesting for autonomous perimeter sensors whose logistics tail cannot support battery resupply. Agriculture deployments link solar harvesters to soil-moisture probes, though energy scarcity in rural RF bands still curbs uptake. Across these verticals, superior total cost of ownership and regulatory alignment underpin sustained expansion of the energy harvesting systems market.

Geography Analysis

Asia held 34.70% of 2025 global revenue, benefiting from China’s immense IoT roll-outs and Japan’s leadership in piezoelectric materials through firms such as TDK Corporation tdk.com. Government-backed smart-city programs from Seoul to Shenzhen subsidize sensor infrastructure, while contract manufacturers in Taiwan and Malaysia offer cost-efficient assembly paths that shorten product cycles. South Korea’s semiconductor ecosystem extends bespoke PMIC fabrication, and Singapore’s logistics parks test large-scale ambient IoT arrays that showcase real-world harvester robustness.

The Middle East records the fastest trajectory at a 8.78% CAGR to 2031. Saudi Arabia’s Vision 2030 positions renewable energy at the center of megacity planning, and indoor navigation beacons at the Al-Haram mosque now trial piezo tile flooring that converts pilgrim footsteps into grid power doi.org. Gulf Cooperation Council utilities integrate photovoltaic harvesters into smart-meter housings to avoid truck rolls for battery service. Israel and the United Arab Emirates anchor regional R&D clusters that pair nano-material labs with venture funds, accelerating commercialization timelines for high-efficiency harvesters.

North America and Europe show mature yet solid demand tied to regulatory frameworks that emphasize lifecycle sustainability. The United States Department of Energy proposes stricter standby limits for chargers, nudging appliance makers toward ambient power paths. Germany and the United Kingdom equip factories with vibration harvesters for rotating machinery, citing net present value gains over three to five years. Across these economies, engineering teams now quantify carbon abatement when selecting sensor platforms, a trend that channels steady orders into the energy harvesting systems market even where initial capital outlay is higher.

Competitive Landscape

The energy harvesting systems market features moderate fragmentation. Semiconductor majors such as STMicroelectronics, Texas Instruments, and Analog Devices wield manufacturing scale and broad sales channels to bundle harvesters with microcontroller families. Niche innovators like Powercast, EnOcean, and e-peas carve share by offering specialized RF front ends, self-powered Bluetooth Low Energy beacons, and power-management chips tailored for indoor light. Competitive intensity focuses on conversion efficiency, package miniaturization, and design-in support rather than price alone, reflecting mission-critical reliability expectations.

Strategic partnerships continue to shape the field. Powercast and Kyocera AVX pair long-range RF power with super-capacitor storage to extend RFID sensor lifespans. Ambient Photonics aligns with Google to integrate bifacial solar cells into consumer electronics, potentially lifting unit volumes sharply. Emerging entrants explore MXene-polymer composites that promise high capacitance and flexible form factors, while 3D-printed nanocomposites could reduce development iterations. The absence of universal power-management standards leaves room for proprietary ecosystems yet also exposes integrators to vendor lock-in, a duality that savvy suppliers exploit by offering migration pathways between product generations. These dynamics collectively sustain healthy rivalry and innovation across the energy harvesting systems market.

Energy Harvesting Systems Industry Leaders

Texas Instruments Inc.

Analog Devices Inc.

STMicroelectronics N.V.

Microchip Technology Inc.

TDK Corporation (InvenSense)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ABB E-mobility launched three new EV chargers with unified architecture, targeting the USD 35 billion EV charging market by 2030 with modular designs ensuring 99% uptime and faster deployment

- April 2025: Asahi Kasei Electronics began mass production of AP4413 series charging control ICs for energy harvesting applications, featuring ultra-low power consumption and voltage monitoring for unstable energy sources like indoor light

- March 2025: STMicroelectronics launched STM32U3 microcontrollers achieving record performance-per-watt efficiency with 117 Coremark-per-milliwatt scores, enabling coin cell and ambient energy operation for IoT devices

Global Energy Harvesting Systems Market Report Scope

Energy harvesting, also known as power harvesting or energy scavenging, is the process by which energy is derived from external sources. Ambient energy, the energy source for energy harvesting systems, is present as ambient background and is freely available.

The Global Energy Harvesting Systems Market is segmented by Technology (Light Energy Harvesting, Vibration Energy Harvesting, Thermal Energy Harvesting, and RF Energy Harvesting), Application (Consumer Electronics, Building, and Home Automation, Industrial, Transportation), and Geography.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Light (Solar/Photovoltaic) Energy Harvesting |

| Vibration (Piezoelectric and Electromagnetic) Energy Harvesting |

| Thermal (Seebeck / Thermoelectric) Energy Harvesting |

| RF (Radio-Frequency) Energy Harvesting |

| Hybrid / Multi-Source Energy Harvesting |

| Energy-Harvesting Transducers |

| Power-Management ICs |

| Energy-Storage Units (Thin-Film Batteries, Supercapacitors) |

| Ultra-Low-Power Sensors and MCUs |

| Less than 10 micro W |

| 10-100 micro W |

| 100 micro W-1 mW |

| 1-10 mW |

| Greater than 10 mW |

| Consumer Electronics | |

| Building and Home Automation | |

| Industrial IoT and Automation | |

| Transportation | Automotive |

| Rail | |

| Aviation | |

| Healthcare and Wearables | |

| Defense and Security | |

| Agriculture and Environmental Monitoring |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics (Sweden, Norway, Denmark, Finland) | |

| Benelux (Belgium, Netherlands, Luxembourg) | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN (Singapore, Malaysia, Thailand, Indonesia, Philippines, Vietnam) | |

| South America | Brazil |

| Argentina | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Israel | |

| Turkey | |

| Africa | South Africa |

| Nigeria | |

| Kenya |

| By Technology | Light (Solar/Photovoltaic) Energy Harvesting | |

| Vibration (Piezoelectric and Electromagnetic) Energy Harvesting | ||

| Thermal (Seebeck / Thermoelectric) Energy Harvesting | ||

| RF (Radio-Frequency) Energy Harvesting | ||

| Hybrid / Multi-Source Energy Harvesting | ||

| By Component | Energy-Harvesting Transducers | |

| Power-Management ICs | ||

| Energy-Storage Units (Thin-Film Batteries, Supercapacitors) | ||

| Ultra-Low-Power Sensors and MCUs | ||

| By Power Range | Less than 10 micro W | |

| 10-100 micro W | ||

| 100 micro W-1 mW | ||

| 1-10 mW | ||

| Greater than 10 mW | ||

| By Application | Consumer Electronics | |

| Building and Home Automation | ||

| Industrial IoT and Automation | ||

| Transportation | Automotive | |

| Rail | ||

| Aviation | ||

| Healthcare and Wearables | ||

| Defense and Security | ||

| Agriculture and Environmental Monitoring | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics (Sweden, Norway, Denmark, Finland) | ||

| Benelux (Belgium, Netherlands, Luxembourg) | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN (Singapore, Malaysia, Thailand, Indonesia, Philippines, Vietnam) | ||

| South America | Brazil | |

| Argentina | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Israel | ||

| Turkey | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

Key Questions Answered in the Report

What is the current size of the energy harvesting systems market?

The energy harvesting systems market size stands at USD 4.38 billion in 2026 and is projected to reach USD 6.06 billion by 2031.

Which technology holds the largest share of the energy harvesting systems market?

Light-based photovoltaic harvesting leads with 41.65% market share in 2025.

Which application segment is growing the fastest?

Industrial IoT and automation is advancing at a 9.62% CAGR through 2031 due to predictive maintenance deployments.

Why is the Middle East an attractive region for suppliers?

Gulf smart-city programs and renewable-energy mandates push demand, driving a 8.78% CAGR for the regional market.

What is the main restraint slowing adoption?

The absence of universal power-management standards creates integration complexity and hampers multi-vendor interoperability.

How are power-management ICs influencing design choices?

High-efficiency PMICs reduce conversion losses and merge harvesting, regulation, and processing into single chips, cutting cost and board area for new products.

Page last updated on: