Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

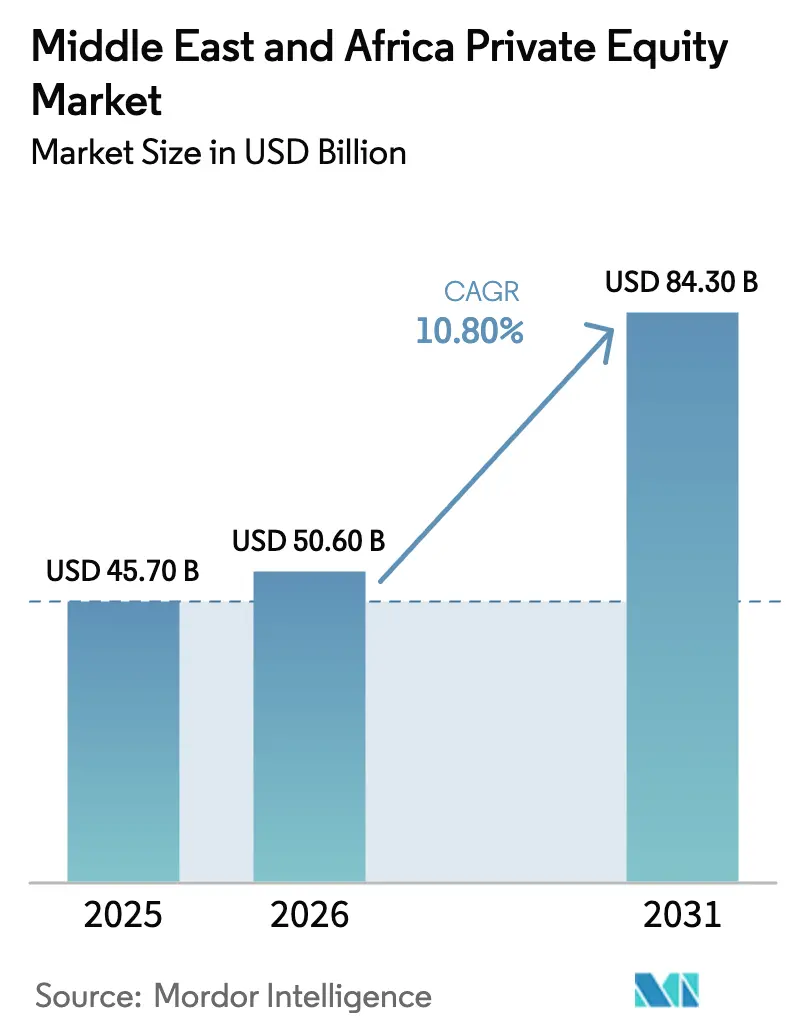

| Base Year Market Size (2025) | USD 45.70 Billion |

| Market Size (2026) | USD 50.60 Billion |

| Market Size (2031) | USD 84.30 Billion |

| Growth Rate (2026 - 2031) | 10.80% CAGR |

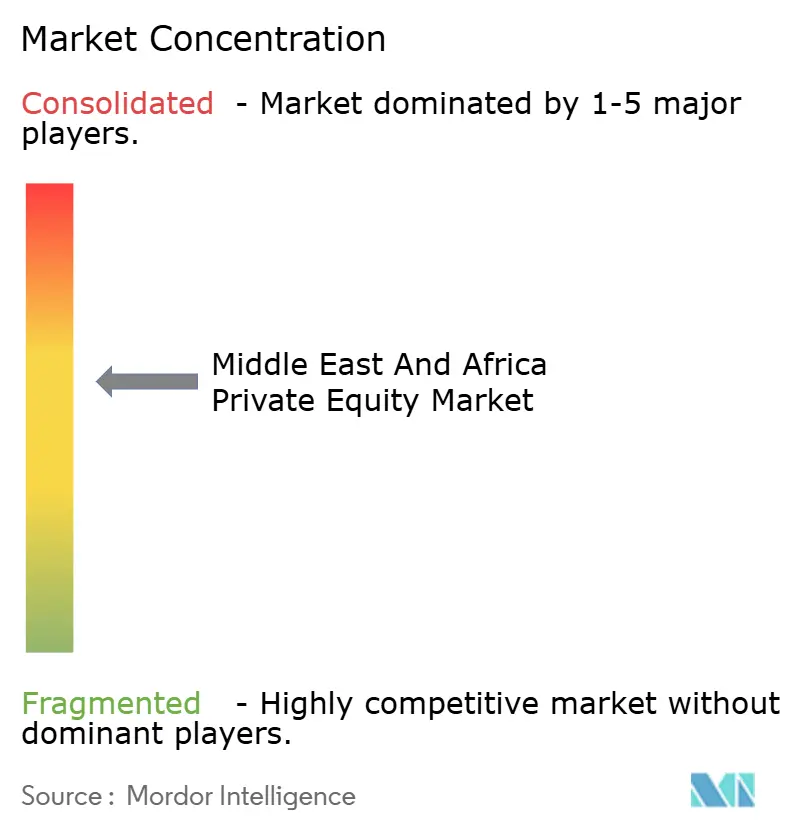

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Private Equity Market Analysis by Mordor Intelligence

The Middle East And Africa Private Equity Market size is expected to increase from USD 45.70 billion in 2025 to USD 50.60 billion in 2026 and reach USD 84.30 billion by 2031, growing at a CAGR of 10.80% over 2026-2031.

Strategic capital formation across the Gulf sovereign funds and targeted African platforms is shaping deal flow, with sovereign investors acting as anchors for large transactions and as catalysts for domestic ecosystems. Capital market reforms in Saudi Arabia and evolving fund regimes in the UAE are widening foreign access and creating more predictable structures for private funds. Startups in the GCC and select African hubs continue to attract venture and corporate venture participation, while infrastructure pipelines offer durable cash flows and inflation-linked returns. Exit bottlenecks and currency risks persist in several African markets, which are steering managers toward private credit, secondary solutions, and structured co-investments that preserve optionality for distributions and repatriation. Foreign participation in Saudi equities accelerated ahead of the 2026 reform and continues to deepen liquidity conditions that support later-stage exits and strategic consolidations.

Key Report Takeaways

- By sector, technology led with 18.9% of the Middle East & Africa private equity market share in 2025 and is projected to expand at an 11.3% CAGR through 2031.

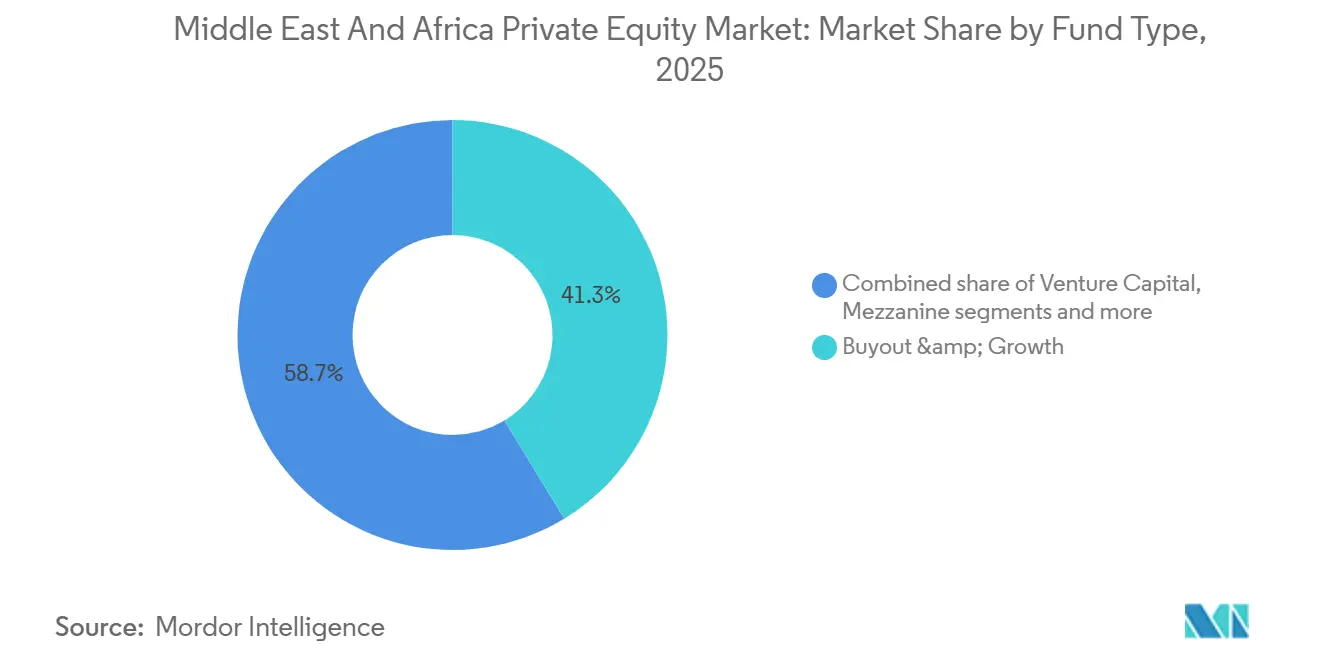

- By fund type, buyout and growth held 41.3% of the Middle East & Africa private equity market in 2025, while venture capital recorded the fastest outlook at a 10.9% CAGR through 2031.

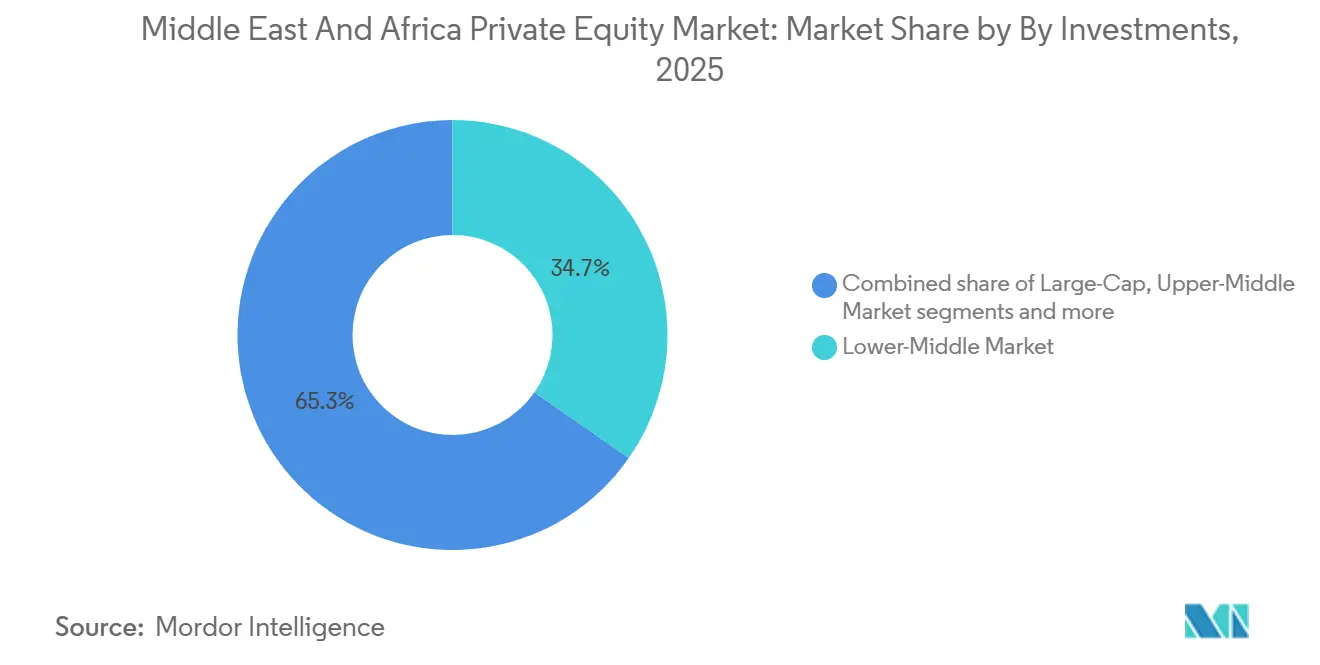

- By investment size, the lower-middle market accounted for 34.7% of the Middle East & Africa private equity market in 2025, and small and SMID-cap vehicles are forecast to grow at an 11.5% CAGR through 2031.

- By geography, Saudi Arabia captured 30.6% of the Middle East & Africa private equity market share in 2025, while South Africa is projected to post the fastest growth at a 10.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Private Equity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant sovereign-wealth dry-powder | +3.2% | GCC core with spill-over to Egypt and selective African co-investments | Medium term (2-4 years) |

| Gradual liberalization of foreign-ownership laws | +2.8% | Saudi Arabia and UAE, second-order effects in Egypt and Morocco | Short term (≤ 2 years) |

| Growing start-up ecosystems in GCC & Africa | +1.9% | UAE and Saudi Arabia in GCC, Nigeria, Kenya, South Africa, Egypt in Africa | Medium term (2-4 years) |

| Acceleration of infrastructure PPP pipelines | +1.5% | Saudi Arabia, UAE, South Africa | Long term (≥ 4 years) |

| Sharīʿah-compliant co-investment structures | +0.8% | GCC-wide with Kuwait and Bahrain trailing Saudi and UAE | Medium term (2-4 years) |

| Rising family-office club-deals | +0.5% | UAE and Saudi Arabia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Abundant Sovereign-Wealth Dry-Powder

GCC sovereign funds increased their deployment in 2025, with multiple Abu Dhabi and Saudi platforms stepping up direct transactions and co-anchoring large vehicles across AI, data infrastructure, and private credit. Mubadala’s activity reflects this shift, including its 2025 transaction slate and the continued build-out of adjacent platforms that extend into credit, infrastructure, and technology allocations tied to AI compute demand[1]Angus Anderson, “AI Anchors GCC Sovereign Wealth Fund Strategy in 2025,” Finance Middle East, financemiddleeast.com. Partnerships formed between Gulf institutions and global managers, such as Stonepeak and The Arab Energy Fund, are channeling long-duration capital into grid modernization and energy transition assets that offer visibility on cash flows. These sovereign-led initiatives provide stability when global venture cycles cool and help close funding gaps in late-stage rounds through co-investments and continuation strategies. Large allocations into AI-related funds and data center platforms underscore a strategic intent to shape next-generation infrastructure rather than passively follow benchmark exposure. The net effect is a deeper pool of regional liquidity for the Middle East & Africa private equity market, adding resilience against external shocks and amplifying the multiplier effect of sovereign anchor capital on third-party fund formation.

Gradual Liberalization of Foreign-Ownership Laws

Saudi Arabia’s abolition of the Qualified Foreign Investor regime in February 2026 allows all foreign investors to access the Tadawul Main Market directly, subject to aggregate and individual caps, and removes a key operational friction that constrained mid-tier institutions. The reform is expected to broaden participation and raise flows as global index funds and retail platforms that could not meet prior thresholds enter the market. In parallel, the UAE’s DIFC and ADGM have streamlined fund manager licensing and introduced digital-asset frameworks that compress fund-launch timelines and attract cross-border managers seeking hub domiciles for MENA and Africa[2]“Global alternatives, local ambition: How SWFs, regulation, and integration are shaping GCC private markets,” State Street Global Advisors, ssga.com. These changes improve investor confidence and reduce structural friction for general partners setting up Middle East & Africa private equity market vehicles targeting the region. Over time, the cumulative regulatory effect is a wider sponsor base, more co-investment capacity, and more credible exit options through local listings or regional strategic acquirers.

Growing Start-Up Ecosystems in GCC & Africa

Venture funding in the GCC held up better than global benchmarks through 2024, driven by government-backed initiatives, corporate venture arms, and targeted AI funds that align with national digital priorities. Saudi Arabia and the UAE account for the majority of regional deal activity, supported by incentives that compress early-stage costs and make Series A rounds more investable for international LPs. In Africa, a bifurcated picture has emerged, with the big four hubs absorbing most capital while the rest of the continent faces thinner pipelines and a growing reliance on DFI-backed vehicles to fill financing gaps. Seed and SMID managers backed by DFIs, such as LoftyInc and Seedstars Africa Ventures, are targeting embedded finance, connectivity, and climate-linked models that reach profitability faster and support earlier liquidity events. These currents are creating a more robust feeder into the Middle East & Africa private equity market for growth and buyout strategies, although the scarcity of later-stage equity in Africa still elongates holding periods for capital-intensive models.

Acceleration of Infrastructure PPP Pipelines

Saudi Arabia’s PPP pipeline spans transport, utilities, and social infrastructure and is building a steady cadence of large transactions that suit long-duration investors. Cross-border partnerships that include The Arab Energy Fund with Stonepeak and a separate initiative with I Squared Capital underline the appetite for regulated assets with clearer revenue frameworks. The UAE’s federal PPP framework has supported projects in healthcare, education, and renewables, while independent power rounds in South Africa continue to attract capital where credit risk can be ring-fenced. Yield premia relative to developed markets reflect a combination of perceived execution risk and regulatory heterogeneity, but they offer diversified return drivers to the Middle East & Africa private equity market. As bank lending remains selective, private credit and hybrid infrastructure equity have grown alongside PPP pipelines to provide flexible capital stacks that meet sponsor needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent exit-route bottlenecks | -2.1% | Africa, with a secondary impact on GCC GP-led continuation strategies | Medium term (2-4 years) |

| Currency-convertibility & repatriation risks | -1.6% | Nigeria, Egypt, Zimbabwe, Lebanon | Short term (≤ 2 years) |

| Limited GP track-records outside buyouts | -0.9% | Sub-Saharan Africa and Francophone markets | Medium term (2-4 years) |

| Fragmented regulatory disclosures | -0.7% | Africa’s 54 jurisdictions and heterogeneous MENA regimes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Exit-Route Bottlenecks

African exit volumes declined sharply in 2023, and public listings remain constrained by free-float rules, lock-ups, and valuation gaps that delay IPO readiness[3]Katie Hill et al., “Deals to Dollars: Navigating Successful Private Equity Exits in Africa,” Boston Consulting Group, bcg.com. Global factors also weighed on MENA IPOs in 2025, which pushed more exits toward M&A and GP-led solutions. Secondary markets in Africa are shallower than global norms, which limits PE-to-PE trades and prolongs holding periods for many growth assets. Continuation funds and NAV-based deals provide interim liquidity but introduce valuation and governance considerations for LPs. In this setting, strategic buyers remain selective and require scale, audited financials, and dollar-denominated structures before engaging, which narrows the immediate universe of exit-ready assets.

Currency-Convertibility & Repatriation Risks

Sharp devaluations in Nigeria and Egypt during 2024–2025 impaired hard-currency returns when distributions were delayed or held onshore due to FX constraints. Lebanon’s capital controls and banking sector losses continue to restrict outflows, with long-standing limits on withdrawals and transfers. Even in markets with flexible regimes, periodic administrative limits can arise during periods of stress, which introduces unpredictability into exit planning and fund-level cash flows. Sponsors mitigate through offshore holdcos, pre-agreed dollar pricing, and selective asset sales to foreign acquirers willing to assume convertibility risks. These measures preserve value but add cost and time to realizations, which weighs on the Middle East & Africa private equity market’s distribution profile for global LPs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fund Type: Buyouts Anchor Scale, Venture Captures Velocity

Buyout and growth strategies accounted for 41.3% in 2025, reflecting steady platform formation, carve-outs, and sovereign-led divestments that fit operational value-creation playbooks in the region. This share underscores how large pools of anchor capital and steady pipelines have supported the Middle East & Africa private equity market size for core control deals and structured minority transactions in 2025. Examples include scale moves by regional champions and cross-border corporate carve-outs, with several managers adding private credit sleeves to support capital-efficient acquisitions. The continued development of blind-pool vehicles in Saudi Arabia and the UAE has increased the local sponsor base and improved transaction certainty for family sellers and state-owned enterprises. As interest rates normalize, managers are blending equity with private credit solutions to protect returns and maintain pacing in a competitive environment. The overall result is a thicker mid-market for the Middle East & Africa private equity market, with more diversified sources of financing and a deeper bench of operating partners that can manage multi-country integration.

Venture capital is the fastest-growing fund type with a 10.9% CAGR outlook, supported by GCC public programs, corporate venture arms, and AI-focused vehicles that tie directly to sovereign compute and data plans. The build-out of late-stage funding bridges in 2026 is intended to ease pre-IPO gaps for companies that have outgrown traditional venture size but are still scaling toward listing thresholds. The Presight–Shorooq AI fund’s early activity illustrates the pace of deployments into frontier models aligned with enterprise demand and public-sector digitization needs. In Africa, DFI-backed seed and SMID funds continue to provide critical acceleration capital where commercial banks remain selective, which helps feed a pipeline of assets for subsequent growth-equity rounds. This combined momentum supports diversification within the Middle East & Africa private equity industry without displacing the central role of buyouts and growth in value creation.

By Sector: Software Supremacy, Energy Transition Ascendant

Technology accounted for 18.9% in 2025, the largest single sector, and is projected to grow at an 11.3% CAGR through 2031 on the back of data center expansion, AI workloads, and sovereign digital mandates. This is where the Middle East & Africa private equity market size intersects with public policy, as governments target national cloud, e-government, and cybersecurity capabilities that require sustained capex and strategic partnerships. Gulf investors deployed heavily into information technology segments in 2025 and launched AI infrastructure vehicles that pair compute with energy and grid assets. Healthcare, real estate, and financial services saw strong flows too, reflecting demographics, tourism, and financial inclusion themes that are durable through cycles. Sector specialists and corporate partners are aligning on platform strategies where roll-ups and digitization can unlock operational leverage over the medium term.

Healthcare investments accelerated across the GCC in 2025 and continued into 2026, while Africa saw new funds target supply chains, primary care, and digital health, widening the investable universe. In real estate, Riyadh-focused developments and transit-oriented projects created new private equity structures and long-duration cash-flow profiles. Financial services allocations surged in Q3 2025 for GCC investors, including major wealth and credit platform moves tied to North American consolidation. Energy transition themes cut across sectors, with private capital partnering on large renewable and grid assets under clear regulatory frameworks.

By Investments: Mid-Market Depth, SMID-Cap Acceleration

Lower-middle market deals represented 34.7% in 2025, a reflection of the region’s SME base, family-controlled enterprises, and SOE subsidiaries seeking operational partners for regional expansion. This layer is pivotal for the Middle East & Africa private equity market as platform strategies and roll-ups can scale across multiple jurisdictions without relying on mega-round financing. Blind-pool funds in Saudi Arabia and expanding manager rosters in the UAE continue to supply flexible capital for control and minority structures that unlock growth. Larger infrastructure and core-plus transactions remain active but are often sovereign-anchored, which can compress access for sub-scale managers in crowded processes.

Small and SMID-cap vehicles are forecast to grow fastest at an 11.5% CAGR, with DFIs catalyzing fund formation that targets the “missing middle” of USD 300,000 to USD 10 million tickets. Managers like LoftyInc and XSML are combining flexible debt and equity instruments with hands-on portfolio support to shorten time-to-profitability and derisk exits. Upper-middle market and large-cap transactions remain episodic and often sovereign-anchored, with dedicated GCC mega-vehicles pursuing concentrated bets in healthcare, technology, and industrials. This mix of ticket sizes and instruments broadens the investable universe for the Middle East & Africa private equity market and creates varied pathways to liquidity across economic cycles.

Geography Analysis

Saudi Arabia led with a 30.6% share in 2025, underpinned by the Public Investment Fund’s scale and capital-market reforms that expanded foreign access to local equities. This allocation reinforces Saudi Arabia’s anchor role in the Middle East & Africa private equity market size, given the Kingdom’s project pipeline and the integration of private sponsors into giga-project ecosystems. The 2026 reform that ended the QFI regime opens the door to a wider base of foreign institutions and retail platforms, which should deepen liquidity for future exits[4]Richard Manfredi, “Saudi CMA Liberalizes Foreign Investment Access and Regulates Real Estate Ownership by Listed Companies and Funds,” Gibson Dunn, gibsondunn.com. As the transaction environment matures, managers are pairing equity capital with private credit and structured solutions to maintain return targets while supporting growth under Vision 2030 priorities. Policy signals and pipeline visibility remain supportive of sponsor activity and platform expansion across consumer, logistics, energy transition, and healthcare adjacencies.

The United Arab Emirates continues as a regional financial hub with streamlined fund regimes, strong family-office growth, and an active sovereign investor base. Dubai and Abu Dhabi are competing with global domiciles by compressing licensing timelines and clarifying digital-asset rules for funds that target MENA and Africa. Active strategies span buyouts, growth, late-stage venture, and private credit, while sovereign affiliates and corporate investors co-anchor platforms and cross-border deals. Platform managers added scale in 2025 and 2026, with large funds raised for GCC portfolios and separate vehicles focused on North American and European technology and credit. This breadth underscores the UAE’s role as a launchpad for sponsors participating in the Middle East & Africa private equity market and in transatlantic strategies.

South Africa holds the fastest projected growth at a 10.9% CAGR to 2031 from a lower base, reflecting governance enhancements for collective investment schemes and a selective pipeline in healthcare, consumer services, and connectivity. Regulatory modernization under Conduct Standard 3 of 2025 supports risk management and investor protection while preserving proportionality for smaller managers. Currency volatility, power shortages, and port congestion remain challenges, but targeted sector opportunities and specialist managers are positioning for new platform plays. DFIs and regional funds continue to anchor mid-market transactions that can reach profitability and support earlier M&A outcomes. This momentum, combined with selective reforms, helps South Africa contribute a growing slice to the Middle East & Africa private equity market over the forecast period.

Competitive Landscape

The Gulf’s sovereign platforms shape the top end of deployment with multi-billion-dollar programs and cross-border partnerships, while Africa remains more fragmented across 54 jurisdictions. Sovereign-linked investors consolidated capabilities across equity, credit, and infrastructure, including high-profile wealth and credit platform moves that create multi-asset franchises. New GCC funds raised by emerging managers are scaling quickly, and complementary tech-focused vehicles target AI and advanced computing in developed markets. This bifurcation between sovereign concentration and African fragmentation informs fund formation, underwriting styles, and exit planning for the Middle East & Africa private equity market.

Three competitive archetypes stand out. Sovereign-backed platforms are integrating vertically across strategies and geographies to secure proprietary deal flow, including AI infrastructure and energy transition partnerships. Sector specialists build moats in healthcare, consumer, and logistics through operating leverage and regulatory familiarity, while opportunistic managers exploit information asymmetries in embedded finance and asset-light digital models. New vehicles are also addressing liquidity constraints through secondaries, continuation funds, and NAV-based solutions that relieve pressure from elongated exit timelines, especially in African portfolios. The growth of private credit across the region is reinforcing the toolkit available to sponsors, supporting acquisition financing and structured growth with lower dilution.

Access requirements in the GCC, such as local presence and talent commitments, are shifting international managers from a “fly-in” model to embedded operations, which strengthens regional capability and improves origination. Family-office club deals and corporate venture activity add to competition for mid- and late-stage assets, especially in the UAE and Saudi Arabia. Across the Middle East & Africa private equity market, the combination of sovereign anchors, specialist managers, and flexible credit providers is broadening the range of transaction structures and improving resilience to macro shocks.

Middle East And Africa Private Equity Industry Leaders

Investcorp

Actis

AfricInvest

Gulf Capital

EFG Hermes PE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: CedarBridge Partners began deploying capital from its USD 150 million CedarBridge High Growth III fund, targeting platform investments in education, healthcare, beauty, wellness, pet care, and essential consumer services across the GCC following its first close in November 2025, with up to 35% allocated for select opportunities in the UK and Europe.

- February 2026: Abu Dhabi-based BlueFive Capital raised a USD 3 billion Onyx Fund for tech and growth capital investments in AI, biotechnology, and advanced computing in the United States and Europe, anchored by Gulf sovereign investors, expanding the firm’s platform to USD 5 billion total assets following its July 2025 USD 2 billion Reef Private Markets Fund I.

- January 2026: The Arab Energy Fund acquired a minority stake in APSCO, a Saudi energy solutions provider, expanding its portfolio in aviation fuels, lubricants, and automotive retail services.

- October 2025: Mubadala Capital closed Private Equity Fund IV at USD 3.1 billion, surpassing its USD 2 billion target, to target middle-market companies in media, sports, consumer services, and financial services.

Middle East And Africa Private Equity Market Report Scope

This report aims to provide a detailed analysis of the Middle East and Africa private equity market. It focuses on the market dynamics, emerging trends in the segments and regional markets, and insights on various product and application types. Moreover, it analyses the key players and the competitive landscape in the Middle East and Africa's private equity market. The Middle East and Africa private equity market is segmented by industry / sector (utilities, oil & gas, financials, technology, healthcare, consumer goods & services, and others), By investment type (venture capital, growth, buyout, and others), by country (Saudi Arabia, UAE, Qatar, Kuwait, South Africa, and rest of the Middle East and Africa).

By Fund Type

| Buyout & Growth |

| Venture Capital |

| Mezzanine & Distressed |

| Secondaries & Fund-of-Funds |

By Sector

| Technology (Software) |

| Healthcare |

| Real Estate & Services |

| Financial Services |

| Industrials |

| Consumer & Retail |

| Energy & Power |

| Media & Entertainment |

| Telecom |

| Others (Transportation, etc.) |

By Investments

| Large-Cap |

| Upper-Middle Market |

| Lower-Middle Market |

| Small & SMID |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| South Africa |

| Nigeria |

| Rest of Middle East & Africa |

| By Fund Type | Buyout & Growth |

| Venture Capital | |

| Mezzanine & Distressed | |

| Secondaries & Fund-of-Funds | |

| By Sector | Technology (Software) |

| Healthcare | |

| Real Estate & Services | |

| Financial Services | |

| Industrials | |

| Consumer & Retail | |

| Energy & Power | |

| Media & Entertainment | |

| Telecom | |

| Others (Transportation, etc.) | |

| By Investments | Large-Cap |

| Upper-Middle Market | |

| Lower-Middle Market | |

| Small & SMID | |

| By Geography | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

Key Questions Answered in the Report

What is the 2026–2031 CAGR for the Middle East & Africa private equity space?

The forecast CAGR is 10.8% over 2026–2031, taking the market from USD 45.7 billion in 2025 to USD 84.3 billion by 2031.

Which sectors are leading deal flow in the Middle East & Africa private equity ecosystem?

Technology led with 18.9% in 2025 and is projected to grow at 11.3% CAGR to 2031, with healthcare, real estate, and financial services also drawing strong allocations.

What fund strategies are most prominent in the Middle East & Africa private equity opportunity set?

Buyout and growth commanded 41.3% in 2025, while venture capital is the fastest-growing strategy with a 10.9% CAGR outlook.

Which investment sizes are most active across the region?

The lower-middle market held 34.7% in 2025, and small and SMID-cap vehicles are expected to grow fastest at an 11.5% CAGR through 2031.

Which geographies are most significant within this regional private equity context?

Saudi Arabia led with 30.6% in 2025, and South Africa has the fastest projected growth at a 10.9% CAGR through 2031.

What structural challenges could affect realizations in the Middle East & Africa private equity landscape?

Persistent exit-route bottlenecks and currency convertibility risks in several African markets can extend holding periods and affect hard-currency returns, which is prompting greater use of private credit and GP-led solutions.

Page last updated on: