Middle East And Africa Meat Substitute Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

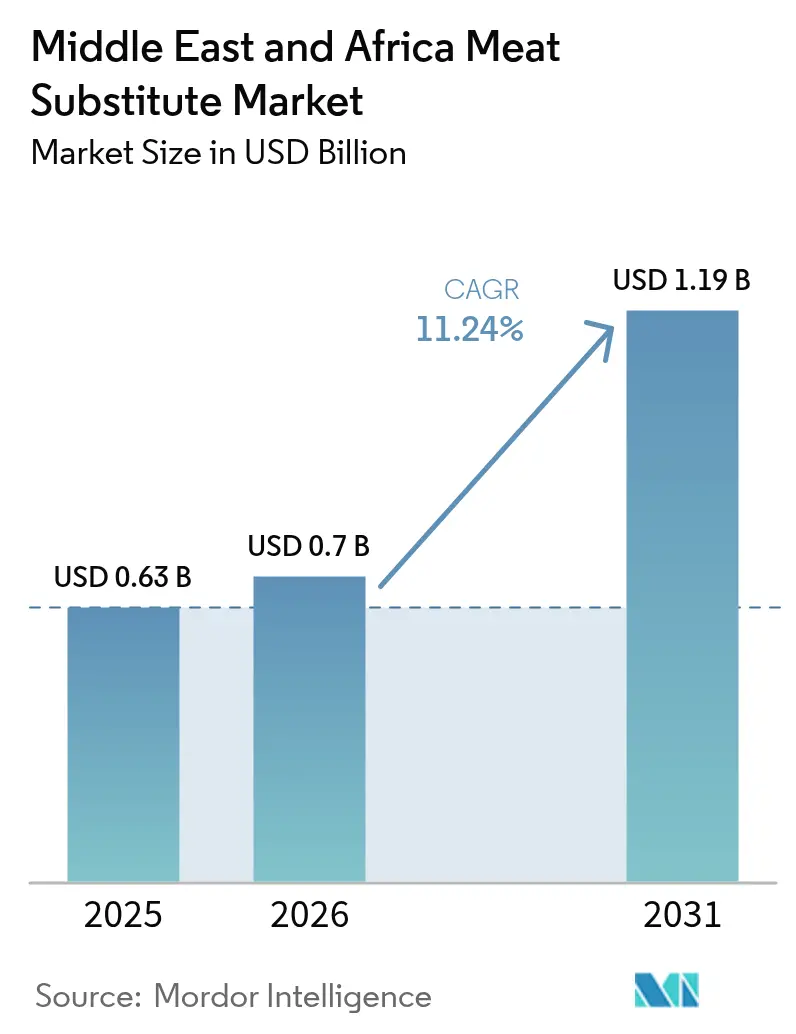

| Base Year Market Size (2025) | USD 0.63 Billion |

| Market Size (2026) | USD 0.7 Billion |

| Market Size (2031) | USD 1.19 Billion |

| Growth Rate (2026 - 2031) | 11.24% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Meat Substitute Market Analysis by Mordor Intelligence

The Middle East and Africa Meat Substitute Market size was valued at USD 0.63 billion in 2025 and estimated to grow from USD 0.7 billion in 2026 to reach USD 1.19 billion by 2031, at a CAGR of 11.24% during the forecast period (2026-2031). This expansion is driven by shifting dietary preferences, increasing health awareness, and sustainability concerns across the region. The market is transitioning from a niche segment targeting vegetarian and vegan consumers to a mainstream protein category adopted by flexitarians, health-conscious individuals, and younger urban populations. This trend is further supported by growing awareness of chronic lifestyle diseases, including obesity, diabetes, and cardiovascular conditions, encouraging consumers and institutions to opt for healthier, low-fat, and cholesterol-free protein alternatives. Additionally, government initiatives are accelerating adoption by incorporating alternative proteins into national wellness and food security strategies.

Key Report Takeaways

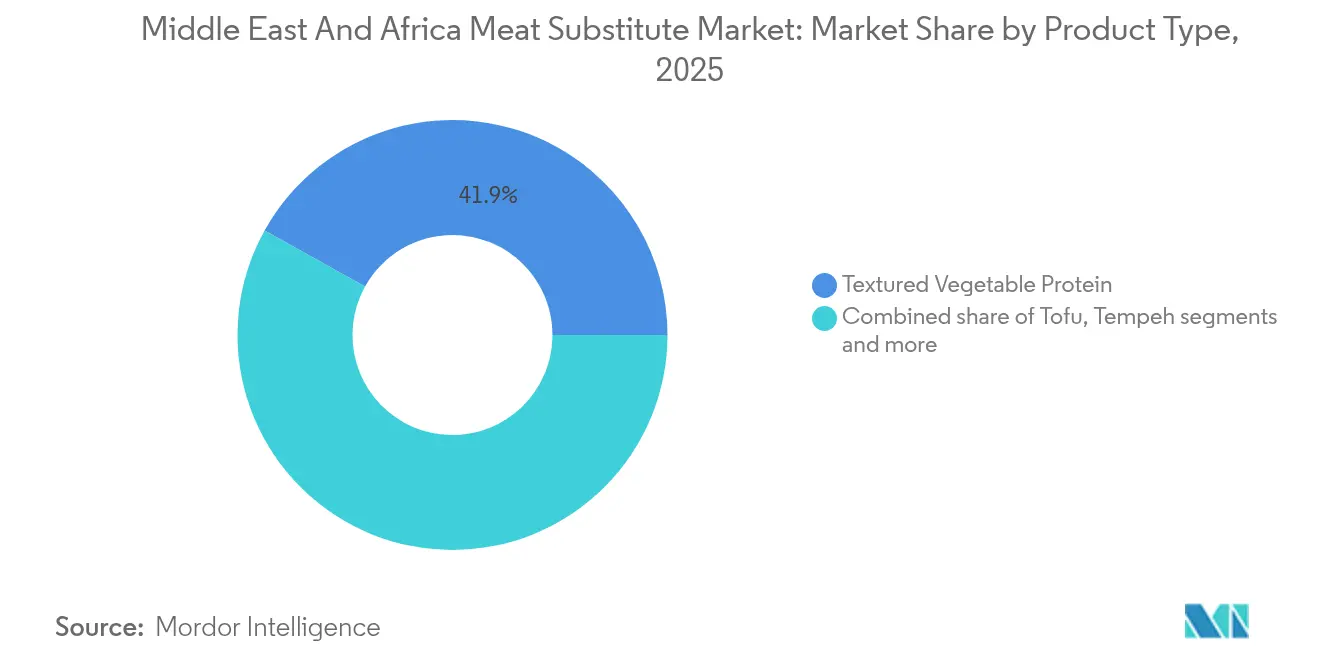

- By product type, textured vegetable protein led with 41.92% revenue share in 2025; tempeh is projected to advance at an 11.33% CAGR through 2031.

- By source, soy accounted for 50.78% of the meat substitutes market share in 2025, while mycoprotein is forecast to grow at a 12.02% CAGR to 2031.

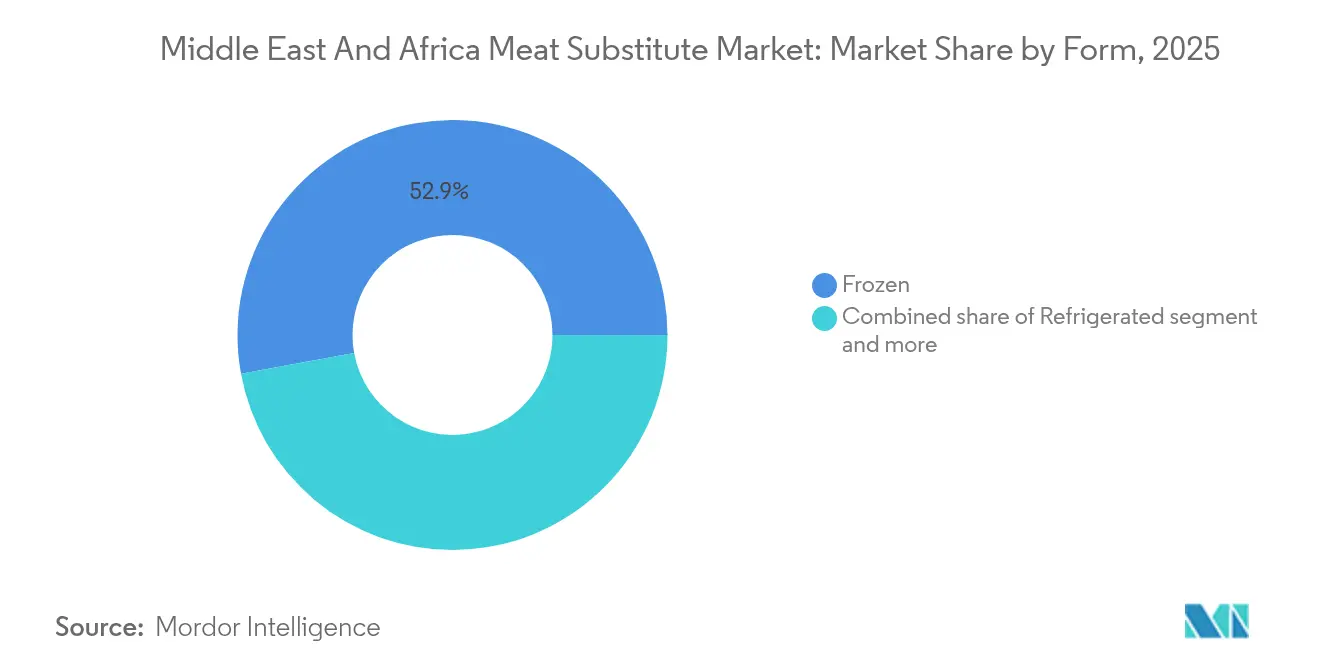

- By form, frozen items captured 52.88% of the meat substitutes market size in 2025; refrigerated formats are set to progress at a 12.19% CAGR during 2026-2031.

- By distribution channel, off-trade held a 68.10% share in 2025, whereas on-trade is expected to register an 11.66% CAGR through 2031.

- By geography, South Africa commanded 26.21% revenue share in 2025; the United Arab Emirates is anticipated to log a 12.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Meat Substitute Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and wellness awareness | +2.1% | United Arab Emirates, Saudi Arabia, South Africa, with spillover to Turkey | Medium term (2-4 years) |

| Urban lifestyle changes and demand for convenience foods | +1.8% | United Arab Emirates, Saudi Arabia, South Africa, Egypt urban centers | Short term (≤ 2 years) |

| Government support, food-security and institutional initiatives | +2.3% | United Arab Emirates, Saudi Arabia, Israel, South Africa | Long term (≥ 4 years) |

| Innovations in product technology and formulation | +1.9% | GCC, with early adoption in United Arab Emirates, Israel, South Africa | Medium term (2-4 years) |

| Growing flexitarian, vegetarian and vegan diet trends | +1.6% | United Arab Emirates, Saudi Arabia, South Africa, Turkey | Medium term (2-4 years) |

| Ethical and animal welfare considerations | +1.2% | United Arab Emirates, South Africa, Israel | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health and wellness awareness

Rising health and wellness awareness is a significant driver of the Middle East and Africa meat substitute market, influencing consumer behavior, institutional priorities, and long-term food strategies across the region. With chronic diseases such as obesity, diabetes, and cardiovascular disorders reaching alarming levels, particularly in Gulf Cooperation Council (GCC) countries, consumers increasingly view dietary choices as a form of preventive healthcare. This trend is further supported by policy initiatives. Saudi Arabia’s Vision 2030 wellness pillar emphasizes healthier nutritional habits and aims to reduce lifestyle-related diseases, while the UAE’s National Food Security Strategy 2051 identifies alternative proteins as critical for addressing the national burden of diabetes and heart disease [1]Source: United Arab Emirates' Government Platform, "National Food Security Strategy 2051", u.ae. These frameworks position plant-based and meat-substitute products as key components of public health management rather than mere lifestyle choices.

Urban lifestyle changes and demand for convenience foods

Changes in urban lifestyles and the growing demand for convenience foods are key factors driving the Middle East & Africa meat substitute market. These trends are reshaping dietary habits and promoting the adoption of quick-preparation, high-protein alternatives. Rapid urbanization is significantly influencing how people live, work, and eat. As more individuals move to cities, their increasingly busy schedules drive a preference for convenient, ready-to-cook, and easy-to-store food products. This shift aligns well with meat substitutes, particularly in frozen, refrigerated, and ready-meal formats, which provide quick meal solutions without compromising on nutrition or taste. The transition toward urban living is especially evident in Africa. According to the Africa Center for Strategic Studies, Africa is the fastest-urbanizing region globally, with cities growing at an average annual rate of 3.5%. By 2050, the continent is projected to have a significantly larger urban population, which is expected to boost demand for modern retail formats, packaged foods, and convenient protein sources [2]Source: Africa Center for Strategic Studies, "Africa’s Unprecedented Urbanization is Shifting the Security Landscape", africacenter.org.

Government support, food-security and institutional initiatives

Government support, food security priorities, and institutional initiatives are significant drivers of the Middle East and Africa meat substitute market, accelerating the adoption of alternative proteins and reshaping long-term food systems. Governments across the region increasingly recognize meat substitutes not only as consumer products but also as strategic assets to enhance national resilience, reduce reliance on imported animal protein, and address the environmental and health challenges associated with traditional livestock production. In the Middle East, particularly in the Gulf, harsh climatic conditions severely limit domestic livestock expansion due to water scarcity, land constraints, and high feed costs. These challenges make alternative proteins a compelling solution for strengthening food security. As a result, national strategies are actively incorporating plant-based and novel proteins into future food planning, reflecting a proactive approach to sustainable food systems.

Innovations in product technology and formulation

Advancements in product technology and formulation are significantly influencing the Middle East and Africa meat substitute market. These innovations enable manufacturers to produce products that are more nutritious, cleaner, tastier, and closer in texture to traditional meat. Developments in extrusion technology, fermentation processes, flavor engineering, and ingredient optimization have notably improved sensory attributes. Additionally, these advancements facilitate the creation of clean-label, allergen-free, and minimally processed options, meeting growing consumer demand for transparency and natural ingredients. For example, brands like Wholesome Provisions in Saudi Arabia have introduced advanced meat substitute products, such as Textured Vegetable Protein and plant-based meat made from 100% hexane-free, graded yellow soybeans. This reflects a shift toward higher-quality inputs and safer, cleaner extraction methods. These innovations enhance product quality and build consumer trust, particularly in markets where clean-label assurance is becoming a key competitive factor.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost/price premium over conventional meat | -1.8% | Egypt, Nigeria, Morocco, South Africa lower-income segments | Short term (≤ 2 years) |

| Taste, texture and sensory limitations | -1.3% | GCC, with acute sensitivity in Turkey, Saudi Arabia, Egypt | Medium term (2-4 years) |

| Limited product variety | -0.7% | Nigeria, Morocco, Egypt, Rest of MEA | Short term (≤ 2 years) |

| Cultural, dietary and traditional resistance | -1.1% | Turkey, Saudi Arabia, Egypt, Nigeria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost/price premium over conventional meat

The high cost and price premium of meat substitutes compared to conventional meat remain significant restraints on the Middle East and Africa market, hindering widespread adoption, particularly among price-sensitive consumers. Although there is increasing interest in healthier and more sustainable protein options, meat substitute products are often priced considerably higher than traditional protein sources such as poultry, beef, and lamb. These conventional proteins are widely available and, in many GCC and African countries, heavily subsidized. The price disparity is driven by factors such as higher production costs, dependence on imported raw materials, specialized processing technologies, and limited local manufacturing capacity, all of which contribute to elevated retail prices. In many markets across the region, where a substantial portion of the population remains highly cost-conscious, these price premiums make plant-based alternatives less economically viable, especially for households that purchase in bulk or prioritize cost-effective options.

Taste, texture and sensory limitations

Taste, texture, and sensory limitations continue to act as significant restraints on the growth of the Middle East and Africa meat substitute market, hindering wider consumer acceptance despite increasing awareness of health and sustainability benefits. Culinary traditions in the region are deeply rooted in richly flavored and texturally distinct meat dishes such as kebabs, shawarma, kofta, and grilled meats, where the sensory experience plays a critical role in meal satisfaction. Plant-based alternatives that fail to replicate the juiciness, chewiness, aroma, and savory depth of conventional meat are often perceived as inferior substitutes rather than appealing standalone options. These sensory shortcomings, whether related to mouthfeel, aftertaste, or overall flavor accuracy, discourage flexitarians and omnivores who are willing to reduce meat consumption but are unwilling to compromise on the enjoyment of their meals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tempeh Gains on TVP's Functional Dominance

Textured Vegetable Protein (TVP) is the leading product type in the Middle East and Africa meat substitute market, accounting for approximately 41.92% of the market share in 2025. This dominance is driven by its nutritional, functional, economic, and logistical benefits, which appeal to both consumers and manufacturers. TVP's fibrous, meat-like texture closely replicates the chewiness and bite of real meat, enabling its seamless incorporation into various dishes such as patties, sausages, kebabs, stews, and curries. This makes it a suitable alternative for consumers transitioning from traditional meat-based diets. Nutritionally, Textured Vegetable Protein is high in protein, low in fat, and free of cholesterol, aligning with the growing health and wellness trends in the region, particularly among urban, health-conscious, and flexitarian consumers.

Tempeh is expected to witness significant growth, with a projected CAGR of 11.33% through 2031. This growth is driven by its unique attributes as a fermented soy product, offering high protein content along with additional nutritional benefits such as enhanced digestibility and probiotic properties. These features resonate with the increasing health consciousness among consumers in the region. Rising awareness of gut health, immunity, and functional foods has further positioned tempeh as an appealing option for urban populations seeking both nutrition and wellness benefits. Additionally, tempeh's culinary versatility supports its expansion; its firm texture makes it suitable for grilling, sautéing, or inclusion in a variety of traditional and fusion dishes, catering to both household and foodservice markets.

By Source: Mycoprotein Challenges Soy's Ingredient Hegemony

Soy has emerged as the leading source segment in the Middle East and Africa meat substitute market, accounting for a significant 50.78% share in 2025. This dominance is attributed to its nutritional benefits, functional properties, and robust supply-chain infrastructure, making it the preferred base for a wide range of meat substitute products. Additionally, soy's versatility enables manufacturers to develop products with meat-like textures and flavors, enhancing consumer acceptance across retail and foodservice channels. The strong availability and well-established import infrastructure for soy further solidifies its position as the primary source for meat substitutes in the region. For example, according to the Observatory of Economic Complexity (OEC), Saudi Arabia imported USD 290 million worth of soybeans in 2023, ranking as the 28th largest importer globally . This substantial import volume highlights the increasing regional demand for soy-based products and the reliance on imported soy to support the expanding plant-based and meat substitute industries.

Mycoprotein is projected to grow at a compound annual growth rate (CAGR) of 12.02% through 2031, driven by several key factors. Derived from fungi, mycoprotein provides a high-quality, complete amino acid profile, low-fat content, and high dietary fiber, making it particularly attractive to health-conscious and environmentally aware consumers. Unlike conventional plant-based proteins, mycoprotein naturally possesses a fibrous, meat-like texture, closely replicating the sensory experience of meat and meeting the taste and texture expectations of flexitarians, vegetarians, and some omnivores. Additionally, rising consumer awareness of sustainable food sources is a significant growth driver. Mycoprotein production requires considerably fewer natural resources, such as land and water, and generates lower greenhouse gas emissions compared to traditional livestock production, aligning with the increasing environmental and ethical concerns in the region.

By Form: Refrigerated Products Gain on Frozen's Logistical Edge

Frozen formats accounted for a significant 52.88% share of the Middle East and Africa meat substitute market in 2025, highlighting their strong appeal among both consumers and manufacturers. This dominance is largely attributed to their convenience, extended shelf-life, and versatility. Frozen meat substitutes enable long-term storage without substantial quality loss, making them suitable for households, retailers, and foodservice providers across the region. This is particularly relevant in countries with reliable cold-chain infrastructure, where shelf-stable alternatives may not fully meet culinary requirements. Additionally, frozen formats preserve the taste, texture, and nutritional quality of products such as Textured Vegetable Protein, tempeh, and mycoprotein, ensuring a meat-like experience that fosters repeated consumer adoption.

Refrigerated meat substitute products in the Middle East and Africa are expected to grow at a robust CAGR of 12.19% through 2031, driven by their increasing appeal to health-conscious, convenience-focused, and quality-oriented consumers. These products offer freshness and superior texture, closely mimicking the sensory experience of freshly prepared meat, making them particularly attractive for premium and ready-to-cook meal solutions. The refrigerated format supports minimally processed, clean-label, and preservative-light offerings, aligning with the rising consumer demand for healthier and more natural food options. Furthermore, the segment benefits from factors such as increasing urbanization, the expansion of modern retail channels, and advancements in cold-chain infrastructure, which collectively improve distribution efficiency and product accessibility across the region.

By Distribution Channel: Foodservice Partnerships Accelerate On-Trade Momentum

Off-trade channels accounted for a significant 68.10% share of the Middle East and Africa meat substitute market in 2025, underscoring their importance in enhancing accessibility, convenience, and the adoption of plant-based protein products across the region. These channels, which include supermarkets, hypermarkets, convenience stores, and online retail platforms, provide consumers with a wide range of products, competitive pricing, and the ease of at-home consumption. This makes them the preferred purchasing option for both individual households and bulk buyers. Supermarkets and hypermarkets, in particular, play a key role by offering high visibility, organized product displays, and promotional activities that educate consumers about new meat substitute products, encourage trials, and drive repeat purchases. Additionally, the growth of e-commerce and online grocery retail has bolstered off-trade channels by enabling direct-to-consumer delivery, expanding geographic reach, and facilitating easy comparison shopping, catering to the needs of digitally savvy and time-constrained urban consumers.

The on-trade segment of the Middle East and Africa meat substitute market is anticipated to grow at a strong CAGR of 11.66% through 2031, driven by the increasing integration of plant-based alternatives in the foodservice and hospitality sectors. This growth reflects rising consumer demand for healthier, sustainable, and protein-rich dining options, as more individuals seek alternatives to traditional meat while dining out. Culinary trends are also evolving, with chefs and foodservice operators incorporating meat substitutes such as textured vegetable protein (TVP), tempeh, and mycoprotein into mainstream menus to cater to vegetarian, vegan, and flexitarian customers. Furthermore, the segment's expansion is supported by robust dining-out activity across the region. For instance, the General Authority for Small and Medium Enterprises reported 714,019 point-of-sale (POS) transactions in the Accommodation & Food Service sector in 2025, highlighting the dynamic nature of the on-trade market and the growing opportunities for meat substitute offerings in restaurants, hotels, and catering services.

Geography Analysis

In 2025, South Africa solidifies its position as the leading market for plant-based meat in the Middle East and Africa, capturing approximately 26.21% of the regional sales. This dominance is attributed to South Africa's mature and structured ecosystem. Urban centers like Johannesburg and Cape Town, with their heightened awareness of flexitarian and vegan diets, bolster the demand for meat substitutes in both retail and foodservice. The country's relatively advanced food processing industry and deep penetration of modern retail further fuel this demand. South Africa's edge in innovation, marked by domestic startups, collaborations with global brands, and early adoption of technologies like precision fermentation, allows it to maintain its dominant share, even as competition intensifies from Gulf markets.

Meanwhile, the United Arab Emirates is rapidly emerging as the region's fastest-growing market. With a dense expatriate base, premium retail formats, and robust government-backed sustainability initiatives, plant-based meat in the UAE is projected to grow at a double-digit CAGR of approximately 12.88% through 2031. Saudi Arabia, aligning with this momentum, is backing it through policy and capital. The nation's Vision 2030 emphasizes wellness, sustainability, and food security. Coupled with allocations from the Public Investment Fund into agri-tech and alternative protein ventures, these initiatives pave a favorable path for both domestic plant-based brands and foreign collaborations, even as adoption remains predominantly among younger urbanites.

While these two nations lead, many others in the region grapple with structural challenges that hinder growth. Turkey's plant-based meat market is in its infancy, with limited brand visibility and a small group of early adopters in major cities. The broader consumer base still leans towards conventional meat, driven by habit and price sensitivity. Egypt faces even steeper challenges: its price-sensitive populace grapples with affordability issues, and the country's weak cold-chain and retail infrastructure outside major cities further complicate matters. Additionally, recurrent currency depreciation inflates the costs of both imported ingredients and finished plant-based products, limiting penetration to premium niches. In Morocco, organized activity in meat substitutes is scant, with only scattered imports and minimal local manufacturing. Without strategic investments in distribution, consumer education, and tailored offerings, Morocco's role in the region's plant-based growth trajectory appears limited in the foreseeable future.

Competitive Landscape

The Middle East and Africa meat substitutes market is moderately fragmented, featuring a combination of global brands and emerging regional players that shape the competitive dynamics. Global companies such as Beyond Meat, Impossible Foods, Nestlé, and Unilever leverage robust Research and Development (R&D) pipelines and partnerships with modern trade retailers to secure prime shelf space and menu placements. These companies typically target mid- to premium-price segments, emphasizing health, sustainability, and taste parity. Their strategies often include extensive marketing efforts and influencer-driven campaigns to build category awareness among affluent urban consumers.

Regional and local companies, including Al Islami Foods, Switch Foods, and IFFCO’s THRYVE platform, are increasingly shaping the competitive landscape. These players combine halal certification and regional flavor profiles with a deeper understanding of local price elasticity and distribution channels. They frequently collaborate with hotels, restaurants, and catering operators in the Gulf region to co-develop menus, enhancing their visibility in the on-trade segment and helping them maintain market share against imported brands.

Technological advancements are becoming a key differentiator, particularly in process capabilities such as high-moisture extrusion for fibrous, whole-muscle analogues, precision fermentation for next-generation fats and functional proteins, and co-extrusion for layered products. While global leaders continue to innovate in these areas, well-funded regional players are increasingly licensing or partnering to access such technologies, narrowing the competitive gap.

Middle East And Africa Meat Substitute Industry Leaders

-

Beyond Meat Inc.

-

Impossible Foods Inc.

-

Monde Nissin Corp. (Quorn Foods)

-

Nestlé S.A.

-

Conagra Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Impossible Foods, a plant-based meat company, has introduced a comprehensive brand refresh, featuring bold red packaging that emphasizes flavor and nutrition as key aspects of its products.

- January 2023: IFFCO Group launched THRYVE, which is described as the Gulf Cooperation Council's (GCC) first 100% plant-based meat venture. THRYVE is a plant-based food hub focused on developing, manufacturing, and marketing a sustainable and healthy portfolio of plant-based meat and alternative food products.

Middle East And Africa Meat Substitute Market Report Scope

Meat substitutes are food products made from plant-based ingredients and eaten as a replacement for meat. The Middle East and African meat substitute products market is segmented by type, distribution channel, and geography. By product type, the market is segmented into tofu, tempeh, TVP (textured vegetable protein), seitan, and other product types. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retailers, and other distribution channels. By geography, the market is segmented into South Africa, United Arab Emirates, Saudi Arabia, Turkey, and Rest of Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Tofu |

| Tempeh |

| Textured Vegetable Protein |

| Seitan |

| Other Meat Substitutes |

| Soy |

| Wheat |

| Mycoprotein |

| Others |

| Frozen |

| Refrigerated |

| Shelf-Stable |

| On-trade | Hotels |

| Restaurants | |

| Catering | |

| Off-trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Tofu | |

| Tempeh | ||

| Textured Vegetable Protein | ||

| Seitan | ||

| Other Meat Substitutes | ||

| By Source | Soy | |

| Wheat | ||

| Mycoprotein | ||

| Others | ||

| By Form | Frozen | |

| Refrigerated | ||

| Shelf-Stable | ||

| By Distribution Channel | On-trade | Hotels |

| Restaurants | ||

| Catering | ||

| Off-trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Middle East and Africa meat substitutes market in 2026?

The market stands at USD 0.7 billion in 2026 and is projected to reach USD 1.19 billion by 2031.

Which country will grow fastest in adopting plant-based meat across MEA?

The United Arab Emirates leads with an expected 12.88% CAGR through 2031, backed by local manufacturing and supportive food-security policies.

What product type is gaining most quickly?

Tempeh is forecast to rise at an 11.33% CAGR, thanks to its clean-label fermentation profile and growing diaspora influence.

Why is halal certification critical for brands?

Halal approval is a non-negotiable entry requirement for Saudi Arabia and the Emirates, giving certified players a significant competitive edge in foodservice and retail.

Page last updated on: