Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

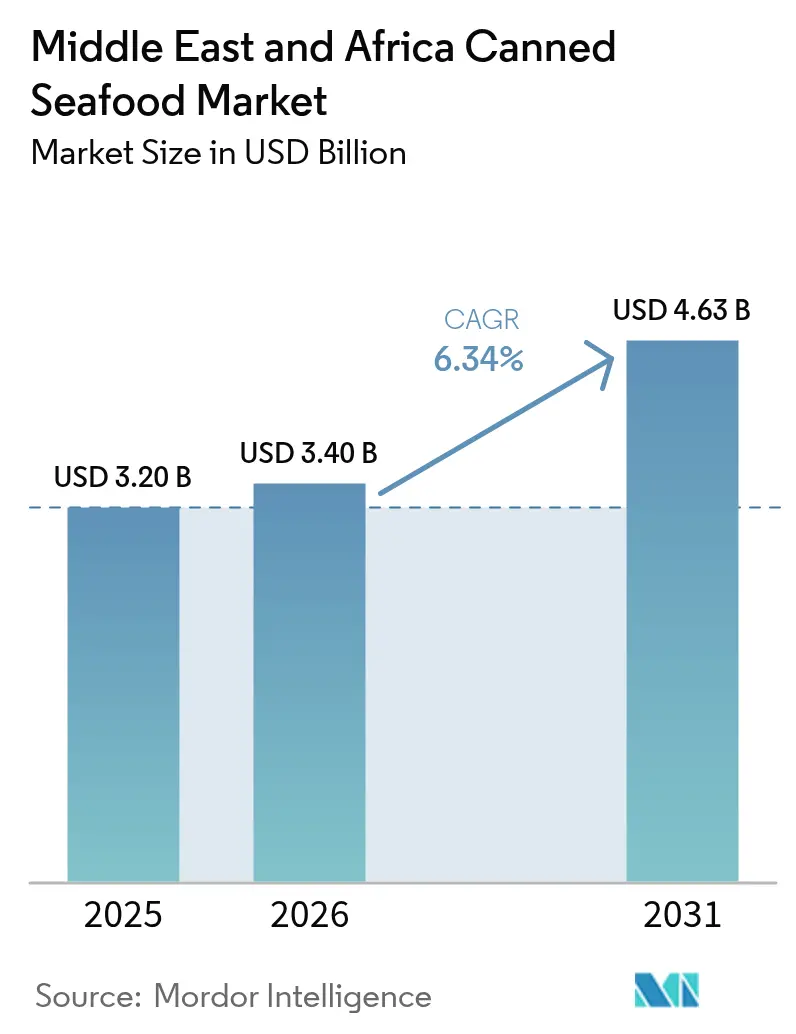

| Base Year Market Size (2025) | USD 3.20 Billion |

| Market Size (2026) | USD 3.4 Billion |

| Market Size (2031) | USD 4.63 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Canned Seafood Market Analysis by Mordor Intelligence

The Middle East and Africa canned seafood market size is expected to grow from USD 3.20 billion in 2025 to USD 3.40 billion in 2026 and is forecast to reach USD 4.63 billion by 2031 at 6.34% CAGR over 2026-2031. Government food-security stockpiles, rising urban incomes, and a growing consumer acceptance of shelf-stable proteins capable of withstanding the region's high temperatures drive the current expansion. While Saudi Arabia and the United Arab Emirates heavily import, they're also channeling investments into domestic processing hubs. These hubs not only shorten lead times but also bolster supply resilience. Suppliers, benefiting from upgraded logistics infrastructure ranging from cold-chain corridors in South Africa to free-zone warehousing in Dubai, can ensure product integrity, even in peak summer heat. Concurrently, the landscape of brand competition is evolving. Halal certification, sustainability labels, and digital traceability are becoming paramount, leading retailers to dedicate more shelf space to responsibly sourced products. Price differentiation remains constrained, largely due to the dominance of commodity fish such as tuna, sardines, and mackerel in the market basket. Yet, premium segments like canned prawns and salmon are drawing affluent consumers, who prioritize convenience and nutritional value. In Egypt, Nigeria, and the Gulf, e-commerce is speeding up product discovery and subscription models. Meanwhile, supermarket private labels retain volume leadership by positioning themselves at lower entry-level price points. Given the robust demand, strategic policy backing, and ongoing vertical integration, the canned seafood market in the Middle East and Africa is poised for sustained double-digit value growth throughout the decade.

Key Report Takeaways

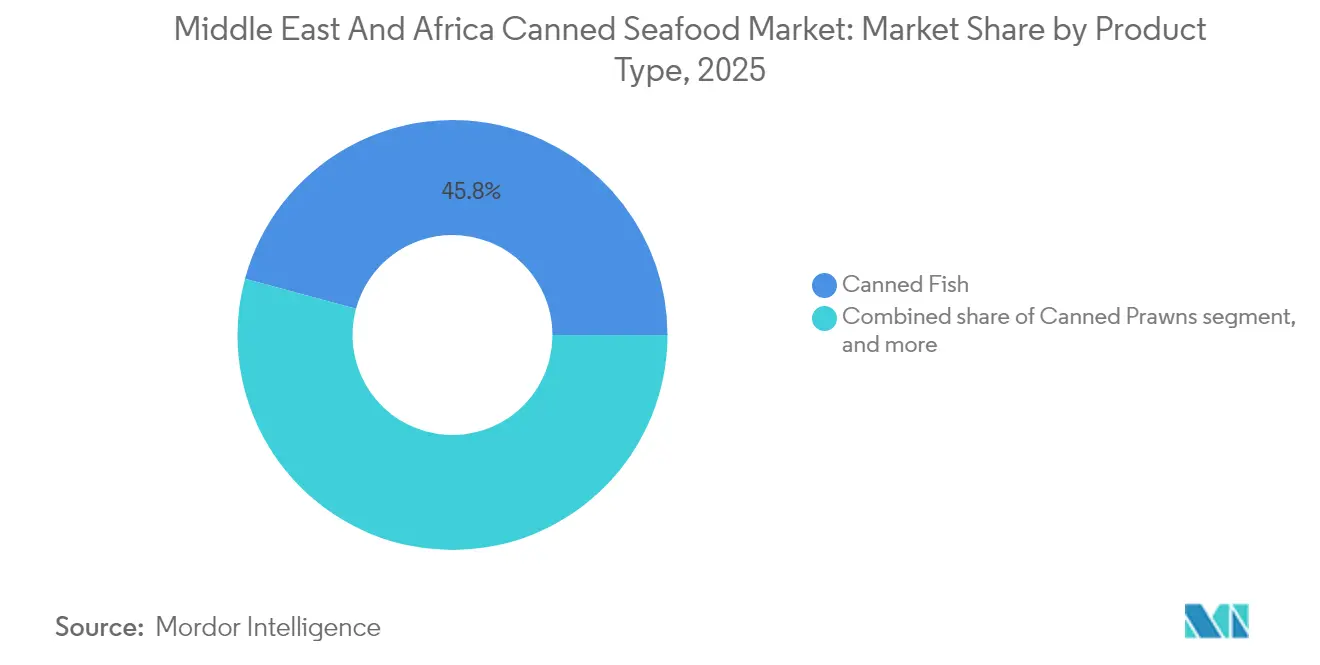

- By product type, canned fish led with a 45.78% share of the Middle East and Africa canned seafood market in 2025, whereas canned prawns are projected to advance at a 7.41% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets controlled 61.74% of the Middle East and Africa canned seafood market in 2025, but online retail is forecast to expand at a 7.05% CAGR between 2026 and 2031.

- By geography, Saudi Arabia accounted for 26.20% of 2025 revenue, while the United Arab Emirates is poised to record the fastest 7.18% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Canned Seafood Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient protein sources | +1.2% | United Arab Emirates, Saudi Arabia, Nigeria | Short term (≤ 2 years) |

| Expanding modern retail and e-commerce footprint | +1.8% | Gulf Cooperation Council core, North Africa | Medium term (2-4 years) |

| Growing domestic fish-processing capacity | +0.9% | Nigeria, South Africa, United Arab Emirates | Long term (≥ 4 years) |

| Government food-security stock-piling | +1.5% | Gulf Cooperation Council, Egypt | Medium term (2-4 years) |

| Halal-certified export opportunities | +0.8% | Southeast Asia, Europe | Long term (≥ 4 years) |

| Climate-driven shift from chilled to shelf-stable seafood | +1.1% | Middle East and North Africa, Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient protein sources

Urbanization, the rise of nuclear households, and a growing female workforce are reshaping meal planning, with ready-to-eat seafood taking center stage. These demographic and lifestyle shifts are driving demand for convenient, nutritious, and shelf-stable food options. Canned fish, rich in omega-3, protein, and iron, sidesteps the perishability issues of fresh catches, offering a practical solution for busy households. This makes it especially appealing during Ramadan, a time when households stock up on non-perishable staples to meet increased meal preparation needs. These now boast convenient, easy-open lids and healthier reduced-sodium formulations, catering to health-conscious consumers. In both Lagos and Riyadh, the inclusion of canned mackerel in school lunch programs highlights its growing institutional acceptance, as schools prioritize affordable and nutritious meal options for students. With rising purchasing power, consumers are leaning towards premium, ready-to-serve options that promise consistent taste, high nutritional value, and time-saving benefits.

Expanding modern retail and e-commerce footprint

In Abu Dhabi, Riyadh, and Accra, hypermarket giants Carrefour and LuLu, among others, unveil new outlets boasting broader selections and specialized seafood sections, catering to the growing demand for diverse product offerings. While private label canned sardines carve a niche by pricing lower than their branded counterparts, they also appeal to cost-conscious consumers seeking value without compromising on quality. However, it's the digital realm that witnesses the most pronounced growth. Egypt's online retail value is set to double from 2024 to 2029, driven by increasing internet penetration and consumer preference for convenience[1]Source: Egyptian Ministry of Communication,"ITIDA, CARITech Partner to Advance Software Development, Elevate IT Knowledge", mcit.gov.eg. Capitalizing on this trend, Talabat and Noon Grocery harness same-day delivery, positioning shelf-stable seafood as a convenient add-on for last-minute purchases. Meanwhile, subscription services facilitate monthly tuna multipack restocks, ensuring consistent availability for regular consumers. Retail analytics spotlight a trend: bundling canned seafood with pasta and tomato paste elevates average order values, signaling potential for cross-category promotions that could further enhance customer engagement and drive sales.

Growing domestic fish-processing capacity

Nigeria's Lekki processing complex aims to enhance local production capacity, reduce import dependence, and create thousands of skilled jobs. This initiative is expected to strengthen the country's seafood processing capabilities and contribute to economic growth by fostering local employment opportunities. In South Africa's Western Cape, upgrades to canning lines now feature automated retorts, which not only boost output but also significantly lower energy consumption per unit, making operations more sustainable and cost-efficient. Khalifa Port's food cluster in the UAE draws foreign direct investment, establishing integrated cold storage and canning facilities. These facilities are designed to consolidate regional supply, ensuring efficient storage and processing before streamlined distribution to Gulf supermarkets. Collectively, these efforts enhance local value addition, bolster traceability, and shorten lead times in the canned seafood market across the Middle East and Africa, addressing key challenges in the supply chain and meeting growing consumer demand.

Government food-security stock-piling

Gulf Cooperation Council states have designated canned tuna, sardines, and mackerel as vital staples in their national emergency reserves, recognizing their importance in ensuring food security during crises. In a move to bolster local aquaculture and ensure a steady supply for domestic canneries, Abu Dhabi has allocated a significant budget to bolster its aquaculture infrastructure and boost production capabilities. In a bid to counteract supply disruptions and stabilize prices, Egypt has added imported sardines to its strategic buffer stock, a move designed to shield the market from volatility. The African Development Bank, through multilateral programs, is training coastal cooperatives in value-added packaging techniques, such as vacuum sealing and labeling, to improve product quality. This initiative not only extends the shelf life of wild-caught species but also ensures safer storage and better marketability. Collectively, these actions solidify a consistent demand, even during economic downturns, by institutionalizing baseline consumption patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile wild-catch volumes/over-fishing limits | -1.4% | West African coast, Indian Ocean | Short term (≤ 2 years) |

| Rising consumer preference for fresh and frozen seafood | -0.8% | United Arab Emirates, Saudi Arabia | Medium term (2-4 years) |

| Fragmented import tariffs across regional blocs | -0.6% | ECOWAS, SADC, GCC | Long term (≥ 4 years) |

| Escalating sustainability-certification costs | -0.9% | Export-oriented producers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile wild-catch volumes and over-fishing limits

Europe quota cuts for mackerel and sardines, combined with NOAA's restrictions on Pacific cod, are tightening the raw-material supply for regional canneries, leading to increased competition for limited resources and higher procurement costs. Ghana's annual closed season significantly reduces coastal landings, compelling processors to depend on more expensive frozen imports to sustain production levels.. El Niño conditions have curtailed Peruvian anchovy harvests, significantly driving up fishmeal costs, which subsequently inflate sardine prices and strain profit margins for processors[2]Source: Food and Agriculture Organization of the United Nations," Globefish Highlights 2024", openknowledge.fao.org. This supply volatility not only complicates annual procurement planning by introducing unpredictability in raw material availability and costs but can also lead to temporary dips in plant utilization rates, falling short of optimal levels and negatively impacting overall operational efficiency and output consistency.

Rising consumer preference for fresh and frozen seafood

Affluent Gulf households, buoyed by rising disposable incomes and a pivot towards healthier eating, are increasingly favoring premium chilled Norwegian salmon and locally farmed sea bass. Recent surveys reveal that a significant number of UAE shoppers purchase fresh fillets at least bi-monthly, underscoring a robust demand for top-tier seafood. E-commerce studies highlight that seafood from coastal origins enjoys a purchasing edge over inland counterparts, hinting at a perception of superior quality that sidelines processed options[3]Source: Multidisciplinary Digital Publishing Institute, "Inland or Coastal? Neural and Psychological Mechanisms Underlying Consumer Preferences for Seafood Origin in E-Commerce", mdpi.com. Kuwait's newly automated distribution center is revolutionizing the cold chain, diminishing the once-convenient edge of canned products by ensuring fresh options with minimal spoilage. Meanwhile, as social media influencers tout sushi and poke bowls, fresh seafood is being elevated to an aspirational status, resonating with consumers desiring trendy, premium dining. This evolution is stifling the growth of canned seafood among affluent consumers, who now equate freshness with quality and lifestyle aspirations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Canned Fish Dominance Drives Market Leadership

In 2025, canned fish commands a dominant 45.78% share of the canned seafood market in the Middle East and Africa. This stronghold is bolstered by deep-rooted culinary traditions, competitive pricing, and heightened promotional efforts during peak retail seasons. Tuna stands out as the favored choice, seamlessly fitting into salads, stews, and school lunches, making it a staple in many households. Meanwhile, sardines and mackerel enrich North African diets, harmonizing with local recipes that emphasize tomato-based sauces, which are widely popular in the region. Although salmon occupies a niche position, it boasts impressive double-digit volume growth in UAE's duty-free and premium supermarket sectors, underscoring a growing health consciousness and a readiness to invest in omega-3-rich foods. This trend reflects a shift in consumer preferences toward healthier and more premium options.

Canned prawns are set to lead the market with a 7.41% CAGR through 2031. Their premium status and popularity among expatriates recreating Asian and Mediterranean dishes at home drive this growth. Their versatility across cuisines and appeal to consumers seeking high-quality seafood further boost demand. Halal-compliant processing assures Muslim consumers of religious adherence, broadening the product's accessibility. Canned shrimp, with steady mid-single-digit growth, is popular in fried rice and instant noodles, especially among college students valuing convenience and affordability. Niche offerings like canned octopus and squid, though starting from a modest base, are gaining traction as food-service operators in cities like Dubai and Cape Town incorporate them into tapas-style menus to meet evolving dining trends. Thai Union has introduced an algae-based tuna substitute, targeting the flexitarian market and signaling potential category expansions. This innovation highlights the industry's focus on sustainability and meeting the demands of health-conscious, environmentally aware consumers.

By Distribution Channel: Traditional Retail Maintains Dominance Amid Digital Disruption

In 2025, supermarkets and hypermarkets dominate the Middle East and Africa's canned seafood market, holding a 61.74% share. Their prominence underscores their pivotal role in weekly household shopping. Even as foot traffic stabilizes in the post-pandemic landscape, these retailers achieve volume gains through aggressive marketing campaigns, loyalty apps, and an expansion of private labels. These strategies not only drive customer retention but also enhance brand loyalty. Notably, end-aisle promotions during the Ramadan and Christmas seasons boost product visibility, encouraging consumers to stock their pantries with essential canned seafood products for festive meals and gatherings.

Online retail, starting from a smaller base, boasts a robust 7.05% CAGR. This growth is fueled by fast-grocery apps in cities like Cairo, Riyadh, and Nairobi, which promise deliveries in just 30 minutes. These platforms enhance consumer trust and justify premium pricing by offering detailed product information, such as origin, omega-3 content, and can-lining specifications. The convenience of quick delivery and transparency in product details appeals to a growing segment of tech-savvy and health-conscious consumers. In densely populated metropolitan areas, convenience stores flourish, with lunchtime patrons frequently topping up on single-serve tuna packs. These stores cater to the fast-paced lifestyles of urban dwellers, providing quick and easy meal solutions. Meanwhile, as tourism rebounds, food-service demand sees a resurgence. Hotel buffets in Dubai and safari lodges in Kenya are now bulk ordering 1 kg cans, catering to salad bars and sandwiches, which are popular among tourists seeking diverse and convenient dining options.

Geography Analysis

In 2025, Saudi Arabia, buoyed by its 35 million-strong population and robust purchasing power, commands a dominant 26.20% share of the market revenue. The nation's Vision 2030 is channeling investments into aquaculture clusters along the Red Sea, aiming to boost domestic production of canned tuna and sardines. These initiatives are designed to reduce reliance on imports while fostering local industries and creating employment opportunities. Meanwhile, retailers are harnessing loyalty programs, turning promotional data into targeted offers, effectively increasing sales among middle-income households. By leveraging these programs, retailers not only enhance customer retention but also drive higher basket penetration, contributing to overall market growth.

The United Arab Emirates, positioned as a global trade hub, is the fastest-growing player, eyeing a 7.18% CAGR through 2031. The United Arab Emirates re-exports imported canned fish to its neighbors, including Kuwait, Bahrain, and Iraq, capitalizing on its strategic location and efficient logistics infrastructure. At Dubai International Airport, duty-free outlets cater to transit passengers with premium salmon cans, expanding the country's market reach and tapping into high-spending international travelers. As dual-income households seek convenient, shelf-stable meals to accommodate their busy schedules, domestic per-capita consumption rises. This shift reflects changing consumer preferences driven by urbanization and longer working hours. Furthermore, with government investments in desalination and vertical aquaculture, the United Arab Emirates signals its ambition for partial import substitution, all while maintaining robust re-export volumes. These initiatives align with the country's broader strategy to enhance food security and reduce dependency on external suppliers.

South Africa, with its top-tier cold chains and experienced fishing fleet, adeptly balances a strong domestic market with exports to its landlocked neighbors. The country's advanced infrastructure and expertise in fisheries enable it to meet both local and regional demand efficiently. In Nigeria, while the demand is buoyed by a sizable population and swift urban migration, challenges like foreign-exchange volatility and port congestion occasionally hinder import volumes. These issues highlight the need for improved trade policies and infrastructure development to sustain growth. Meanwhile, emerging markets like Kenya, Ghana, and Côte d’Ivoire, though starting from a modest base, are witnessing double-digit volume growth. This surge is fueled by World Bank-backed cold-store projects and the expansion of supermarket chains into secondary cities, which improve access to canned fish products and stimulate local economies. Although political instability in Sudan and Ethiopia presents localized challenges, it hasn't significantly impacted the overall regional demand, thanks to a diversified country exposure. This diversification mitigates risks and ensures steady growth across the region.

Regulatory Landscape

Canned seafood marketed across the Gulf is shaped by GCC harmonization through the Gulf Standardization Organization (GSO), including product-specific requirements such as GSO 1817:2022 for canned tuna and canned bonitos, and cross-cutting labeling guidance under GSO 2406:2025 (approved 22 April 2025). In Saudi Arabia, imported canned/packaged foods are enforced through the Saudi Food and Drug Authority (SFDA), which tightened expectations for low-acid and acidified canned/packaged foods through SFDA.FD 5033:2025 (approved October 2025). In April 2026, SFDA notified a draft technical regulation covering requirements for storage facilities for dry and canned foodstuffs, with a comment period ending 25 April 2026. Together, these steps lift the compliance bar for labeling, shelf-life documentation, and handling controls, which affects supplier qualification and the documentation approach used by importers.

In Africa, regulatory moves that affect specifications and conformity assessment for canned fish are coming through both regional and national channels. The Southern African Development Community (SADC) signed a Model Technical Regulation for canned fish and fishery products on 24 June 2026, offering a reference framework for alignment across member states. In North Africa, Egypt adopted Ministerial Decree No. 57/2026 (22 February 2026) for canned finfish, requiring adherence to ES 1521 and reinforcing standardized product and safety requirements for both domestic producers and importers.

Competitive Landscape

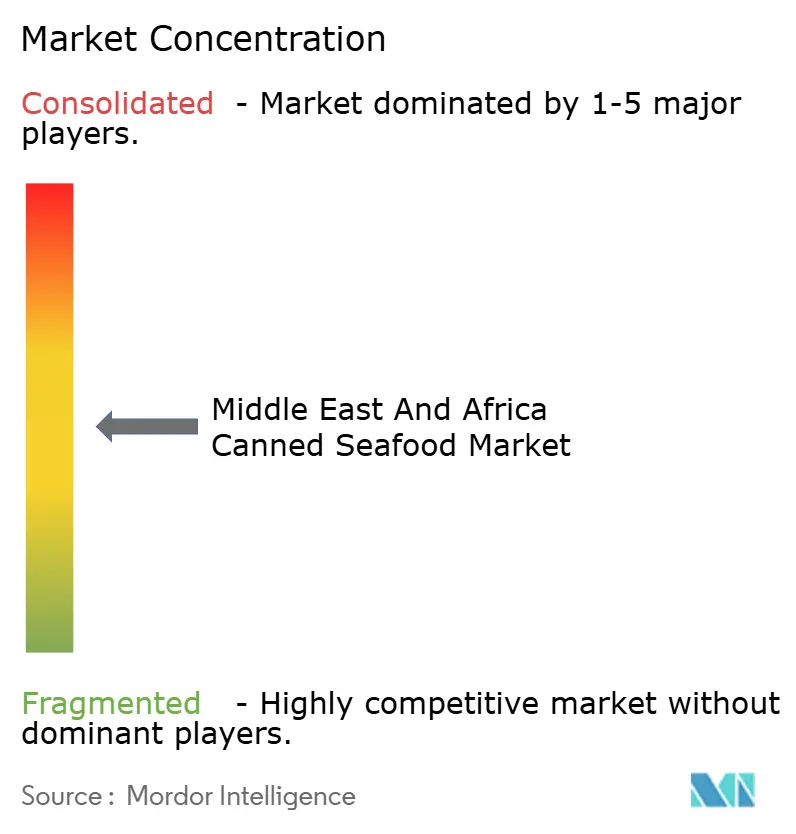

Market concentration shows a moderate level of concentration. Global giants like Thai Union, Bolton Food, and Del Monte are turning to multi-origin sourcing to mitigate raw material risks. They're also investing heavily in marketing to secure their shelf space. In May 2025, Thai Union bolstered its premium portfolio by acquiring King Oscar, promoting Norwegian-sourced Stock Keeping Units in Gulf supermarkets. This acquisition not only strengthens Thai Union's presence in the premium segment but also enables cross-promotion opportunities in high-demand regions. Meanwhile, Bolton Food's Rio Mare brand is championing MSC-certified(Marine Stewardship Council) tuna campaigns in Saudi Arabia, aligning with shoppers' growing concerns for ocean health. These campaigns emphasize sustainable fishing practices, which resonate with environmentally conscious consumers and enhance brand loyalty.

Regional players, such as Oman Fisheries and Sea Harvest from South Africa, are carving out market share by highlighting their product provenance and ensuring quicker delivery times. By entering co-manufacturing agreements with supermarket private labels, they're also maximizing their production capacity. These partnerships allow regional players to expand their reach and cater to diverse consumer needs while maintaining operational efficiency. In Nigeria, start-ups are experimenting with locally flavored chili-tomato sardines, catering to West African tastes. This move underscores the potential of culturally relevant innovation to challenge established players. By addressing local preferences, these start-ups are not only differentiating themselves but also fostering stronger connections with their target audience.

As firms increasingly adopt blockchain platforms for traceability, supply-chain digitization is gaining momentum. This traceability is not just a trend; it's essential for halal verification and MSC audits. Companies that can provide detailed vessel-level data find themselves in prime spots on Carrefour and LuLu's listings. This transparency not only sets branded products apart from dubious grey-market imports but also reinforces their market position. By leveraging blockchain technology, firms can build consumer trust and ensure compliance with stringent regulatory standards. In summary, the canned seafood market in the Middle East and Africa is a dynamic landscape, accommodating both large-scale cost leaders and agile niche players. The latter often carve out their space by offering unique flavor profiles or emphasizing sustainability credentials, which are increasingly valued by modern consumers.

Middle East And Africa Canned Seafood Industry Leaders

-

Thai Union Group PCL

-

Bolton Group B.V.

-

Oceana Group Ltd.

-

Terrasan Group of Companies

-

Trident Seafoods Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The clearest opportunity is in regional value-added processing and port-based manufacturing clusters that shorten lead times and improve supply resilience for shelf-stable seafood. Simak, backed by the Oman Investment Authority, moved from build-out to commercial production at Duqm and cited capacity of 100 million cans annually (over 30,000 metric tons). This positions Duqm SEZ as a key tuna and sardine canning anchor and supports co-packing and private-label opportunities for Gulf retail. In North Africa, Tunamax partnered with Gaictech to launch a high-tech tuna canning plant in Berrechid, Morocco, cited at 15,000 tons of whole tuna processing capacity per year, and output of over 50 million cans. That expands the regional base for tuna-centric SKUs and supports multi-origin sourcing strategies.

Retail and compliance requirements also create room for suppliers that can scale traceability, labeling readiness, and halal documentation, especially for Saudi Arabia where SFDA import controls are stringent. Free-zone and economic-cluster investments are broadening shelf-stable seafood portfolios and enabling cross-category manufacturing. This includes Solico Group opening its SoFood production facility in Jebel Ali Free Zone (Jafza) with initial capacity up to 40 tons per day to serve GCC and export markets, and Barakat Group starting construction in KEZAD (Abu Dhabi) on a facility that includes fish-based baby food purees with a 90 million unit annual capacity. These developments support premiumization through differentiated tuna formats and higher-value species, and they open new use-cases such as institutional packs and ready-to-eat variants, while aligning with modern retail and e-grocery platforms already expanding across key MEA cities.

Recent Industry Developments

- July 2026: Thai Union Group PCL reported that its 2026 World Oceans Day cleanup activities removed more than 8 metric tons of ocean-bound waste, with the largest collection in Tema, Ghana. While not a capacity expansion, it reinforces the company’s sustainability positioning that increasingly feeds into retailer sourcing requirements and audit readiness for canned seafood supply.

- June 2025: Oceana Group Ltd. disclosed continued execution of capital upgrades across its West Coast operations via JSE SENS communications, building on its multi-year investment program across canned fish and related facilities. The upgrades support higher plant efficiency and throughput, which can improve regional availability and competitiveness for canned fish brands supplied into Southern Africa and neighboring MEA trade corridors.

- December 2024: Simak (Fisheries Development Oman) launched consumer canned tuna products produced at its Duqm SEZ facility, signaling the start of commercialization from a new domestic canning hub. The move strengthens Oman’s food-security agenda and adds a regional supply source that can serve both local demand and Gulf distribution networks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market counts the value of shelf-stable seafood sold in sealed cans across the Middle East and Africa. It covers common canned fish and canned crustaceans that reach consumers through retail and foodservice channels.

The scope excludes frozen or chilled seafood, fresh fish counters, and non-canned shelf-stable formats such as pouches, jars, or ready meals where seafood is only an ingredient.

Segmentation Overview

-

By Product Type

-

Canned Fish

- Tuna

- Salmon

- Sardines

- Mackerel

- Canned Shrimp

- Canned Prawns

- Others(Octopus, Squid, Crab etc)

-

Canned Fish

-

Distribution Channel

- On trade

-

Off trade

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Retails

- Others

-

By Geography

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Oman

- Bahrain

- South Africa

- Nigeria

- Turkey

- Rest of Middle East and Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by setting the market boundary and building a demand map for canned seafood in the region. We reviewed public sources such as FAO FishStat, UN Comtrade, national customs and trade portals, and statistics sites from government bodies, then applied food safety and labeling guidance where it affects what can be sold as canned seafood.

Next, we used financial statements, annual reports, and investor presentations to understand product mixes and regional exposure. Channel signals were cross-checked using reputable press and retailer announcements. Where needed, paid subscription sources for company financials and intelligence and an import-export shipment-level database were used to sanity-check trade flows and supplier presence. The sources listed here are illustrative only, and other public and paid references were used to clarify, validate, and reconcile figures.

Primary Interviews and Surveys

Primary discussions were used to confirm which species and pack types move in volume and where pricing changes fastest, especially across modern retail and wholesale routes. We spoke with a mix of manufacturers, importers, distributors, large retailers, and foodservice buyers across key Middle East and African markets, so gaps from desk research could be filled and assumptions checked against on-the-ground trading patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 16% | |

| Mid tier: 43% | Functional/Unit leaders: 39% | |

| Smaller Players: 18% | Managers: 45% |

Market-Sizing & Forecasting

The core sizing logic uses a top-down build where production and trade data help reconstruct the available canned seafood supply by country. That supply is then adjusted for re-exports and translated into consumption value using observed price bands.

Once the country totals were created, they were checked against selective bottom-up approximations, including sampled brand and private-label price points, distributor channel checks, and a few supplier revenue splits. If the cross-checks did not align, totals were tuned and re-tested against the trade inputs.

Key inputs in the model include canned seafood import volumes and values, local canning and processing capacity signals, retail price movement for core species (tuna, sardines, mackerel, salmon), modern retail penetration and online share direction, and currency and inflation conditions that affect reported value. Where a country had limited public detail, gaps were filled using proxy indicators such as trade mirror data and the direction of per-capita seafood consumption, then filtered further using interview feedback.

For forecasting, scenario analysis was used with a base case anchored on expected seafood trade growth, packaging input costs, and channel expansion. The results were stress-tested for exchange-rate swings and supply shocks. The final forecast path was selected after primary inputs indicated the most likely price and volume progression by species and channel.

Data Validation & Update Cycle

Model outputs were triangulated using multiple checks, including country-level import value trends, species mix direction, and channel price observations. Results were then compared against independent signals from company commentary and retailer shelf pricing.

Outliers were investigated through variance checks, followed by a second analyst review focused on unit errors, currency timing issues, and potential double counting across re-export hubs.

If a material change is observed, such as a step-change in trade flows, a tax or labeling shift, or a major price reset, respondents are re-contacted to confirm whether the change is temporary or structural. Reports are refreshed annually, with interim updates for material events, and a final pre-delivery pass is completed so clients receive the latest consistent view.

Mordor Intelligence's Middle East and Africa Canned Seafood Market Estimate Compared With Other Published Estimates

Published market sizes for canned seafood in the Middle East and Africa often do not match because the included formats, the country list, and the pricing basis are not always consistent. Differences can also reflect how trade hubs are treated, how re-exports are netted out, and whether published numbers reflect retail value, ex-factory value, or a mix.

Import value trends by species are cross-checked with re-export adjustments in key hubs, then validated through channel price checks. This is the evidence base that keeps Mordor Intelligence's USD 3.40 B (2026) estimate tied to the region's actual canned seafood consumption pool.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.40 B (2026) | |

| Regional Consultancy A | USD 3.80 B (2026) | This figure appears to use a wider definition that can fold in non-can shelf-stable seafood formats and may not net out re-exports fully, which can inflate value in trade hub countries. |

| Trade Journal B | USD 3.10 B (2025) | This estimate is likely anchored to a narrower country set and a more conservative price basis for core fish species, and the base year choice can also lower the reported headline value versus a 2026 view. |

The spread mainly comes down to scope boundaries and how pricing and re-export effects are handled. By keeping the steps traceable to trade signals, channel pricing, and clear inclusions, the resulting market value is easier to reproduce and interpret for planning and budgeting.

Key Questions Answered in the Report

How large is the Middle East and Africa canned seafood market in 2026?

The Middle East and Africa canned seafood market size stands at USD 3.40 billion in 2026.

What is the projected growth rate for canned seafood demand across the region?

The market is forecast to grow at a 6.34% CAGR, reaching USD 4.63 billion by 2031.

Which product category is expanding the fastest?

Canned prawns exhibit the highest momentum with a 7.41% CAGR through 2031.

Why are Saudi Arabia and the UAE so important for suppliers?

Saudi Arabia delivers the largest 26.20% revenue share, while the UAE offers the fastest 7.18% CAGR, together making them pivotal commercial hubs.

Page last updated on: