Middle-East And Africa Animal-based Meat And Dairy Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

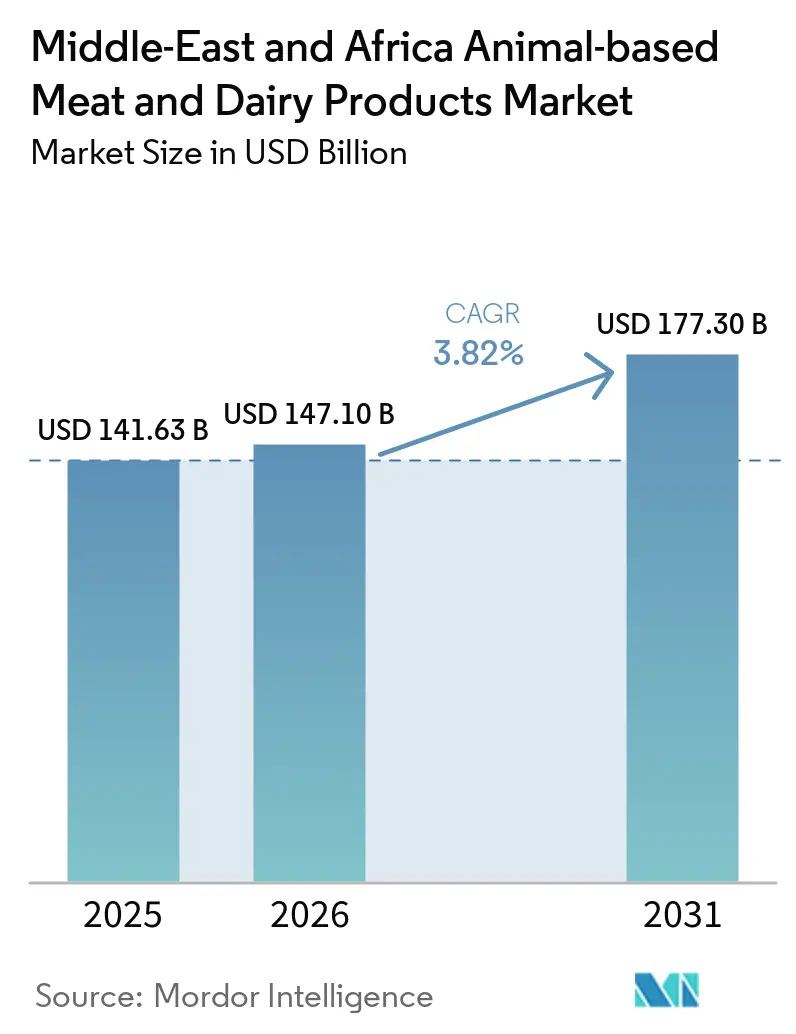

| Base Year Market Size (2025) | USD 141.63 Billion |

| Market Size (2026) | USD 147.10 Billion |

| Market Size (2031) | USD 177.30 Billion |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

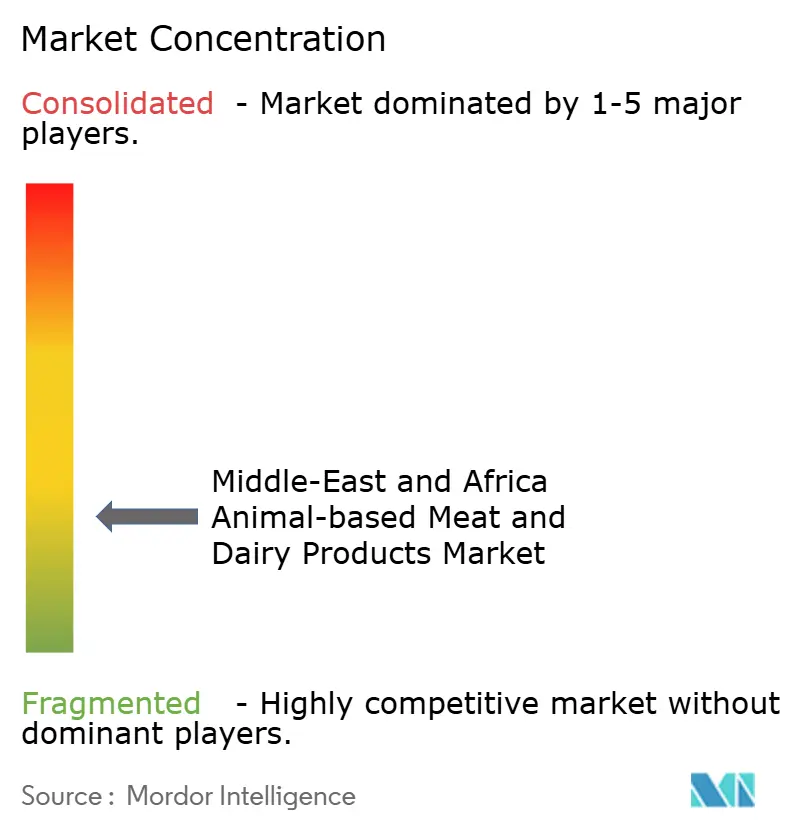

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East And Africa Animal-based Meat And Dairy Products Market Analysis by Mordor Intelligence

The Middle East and Africa animal-based meat and dairy products market size is projected to expand from USD 141.63 billion in 2025 to USD 147.10 billion in 2026. The market is expected to reach USD 177.30 billion by 2031, growing at a 3.82% CAGR over 2026-2031. The region’s moderate headline growth masks big structural change. Saudi Arabia’s Vision 2030 has already directed USD 10 billion to vertically integrated livestock complexes, while South Africa’s cheese exports climbed 50% in 2024 on the back of artisan demand despite health-related trade bans. Food-security mandates channel state capital toward domestic feed, slaughter, and cold-chain assets, insulating operators from currency swings and Red Sea freight premiums that jumped 250-500% during 2024-2025. At the same time, regulatory convergence under GSO 993:2015 is nudging processors to automate halal compliance, trimming non-conformance waste below 2% and favoring scaled incumbents able to amortize SAR 15,000-50,000 (USD 4,000.5-13,335.0) certification fees per SKU. Rising disposable incomes in GCC cities lift premium segments, while Nigeria, Egypt, and Morocco leverage fiscal incentives to localize yogurt and cheese capacity in a bid to reduce their USD 1.5 billion annual dairy-powder import bill.

Key Report Takeaways

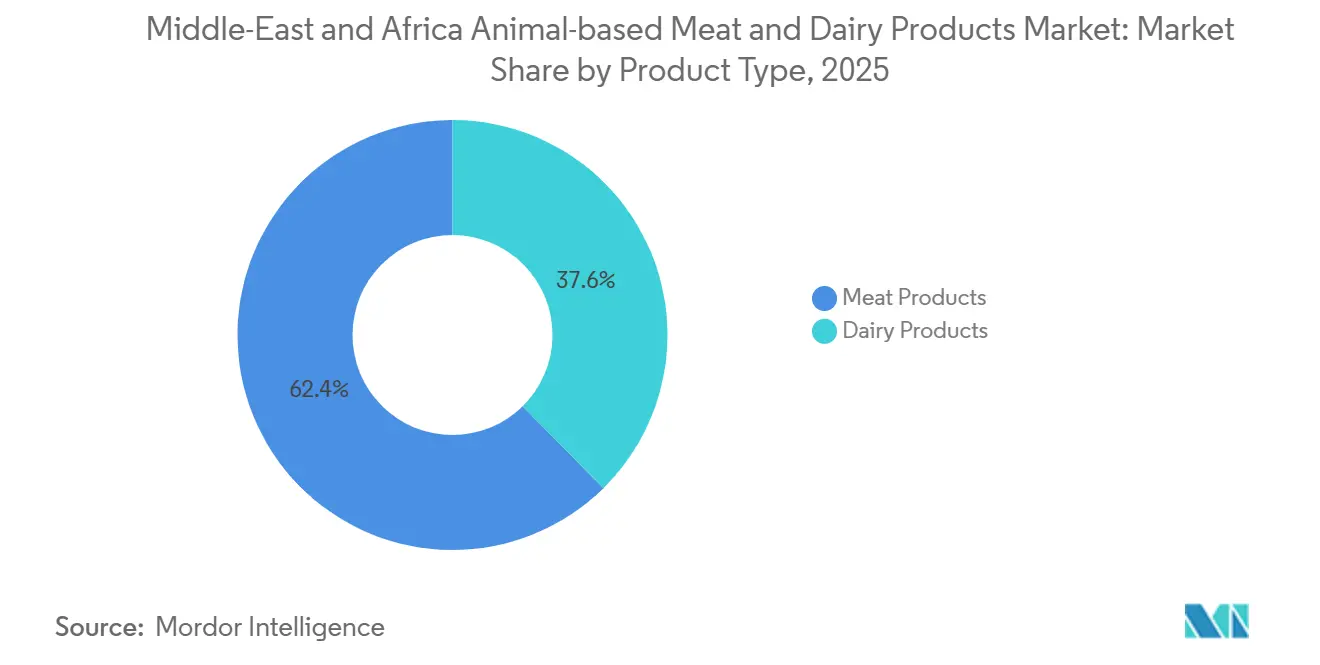

- By product type, meat products led with 62.38% of the Middle East and Africa animal-based meat and dairy products market share in 2025, whereas dairy beverages are forecast to post the fastest 5.46% CAGR through 2031.

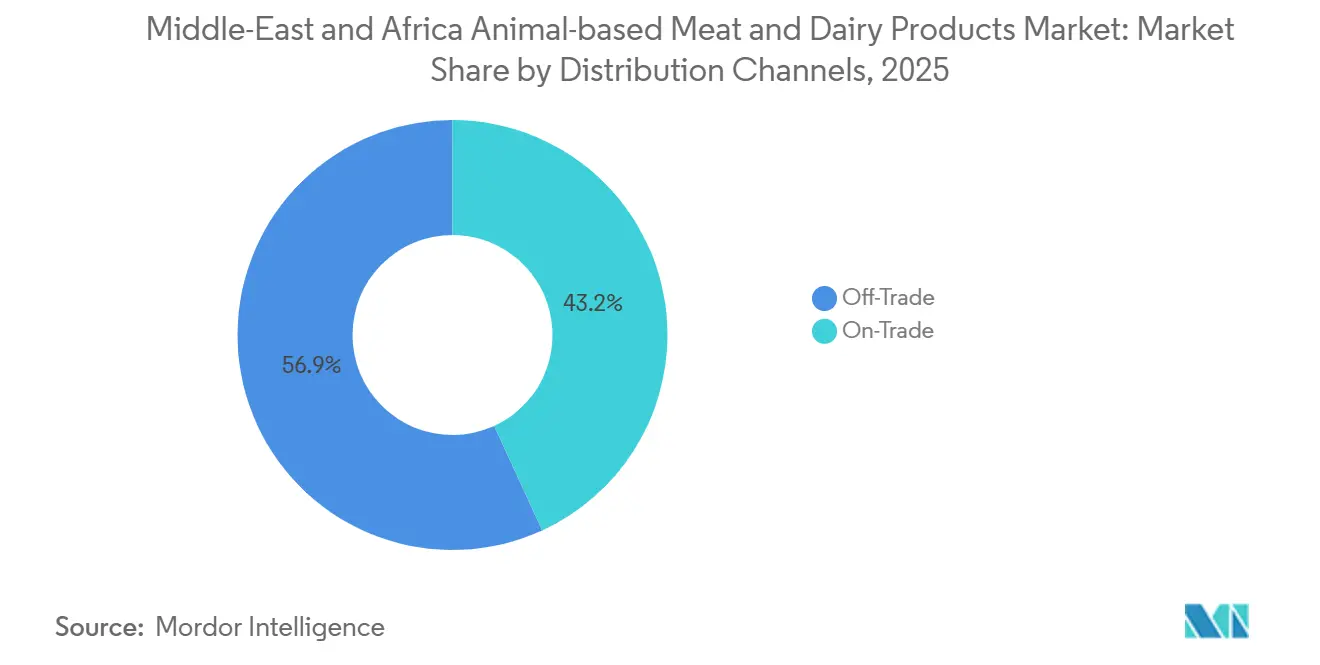

- By distribution channel, off-trade formats held 56.85% of the Middle East and Africa animal-based meat and dairy products market size in 2025, but on-trade is advancing at a 6.02% CAGR over 2026-2031.

- By geography, Saudi Arabia accounted for 58.68% of 2025 demand; South Africa is the quickest grower at a 5.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle-East And Africa Animal-based Meat And Dairy Products Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand For Protein‑Rich Products | +1.2% | Global, strongest in Saudi Arabia, UAE, South Africa | Medium term (2-4 years) |

| Population Growth And Urbanization Boost Consumption Of Convenient Processed Products | +0.9% | Nigeria, Egypt, Morocco, with spillover to Gulf expatriate communities | Long term (≥ 4 years) |

| Technological Advances Enhance Production Efficiency And Quality Control | +0.6% | Saudi Arabia, UAE, South Africa (automated dairy farms, IoT cold-chain) | Medium term (2-4 years) |

| Shift To Premium Artisanal Dairy And Meat Appeals To Affluent Segments | +0.5% | GCC core (Saudi Arabia, UAE, Qatar), South Africa urban centers | Short term (≤ 2 years) |

| Infrastructure Investments Improve Cold Chain Logistics For Perishables | +0.7% | Egypt, Nigeria, Morocco, Kenya spillover | Long term (≥ 4 years) |

| Rising Government Food‑Security Investment Programs | +0.8% | Saudi Arabia, UAE, Egypt (sovereign funds, bilateral loans) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Protein-Rich Products

Per-capita animal-protein intake in the Gulf Cooperation Council reached 63 kilograms in 2025, outpacing the global average by 40%, yet micronutrient deficiencies persist among lower-income expatriate cohorts who rely on cheaper processed meats with suboptimal amino-acid profiles. This paradox drives premiumization: Al Safi Danone launched a 36-gram-protein milk format in 2025, targeting fitness enthusiasts willing to pay a 30% premium over commodity UHT milk, while Almarai's protein smoothie line delivers 30 grams per 330-milliliter serving, embedding whey isolates sourced from its vertically integrated dairy farms. South Africa's poultry sector, supplying 60% of national meat consumption, benefits from maize-price deflation, local yellow maize fell 12% year-on-year in December 2025, enabling processors to hold retail prices flat while expanding margins, according to the United States Department of Agriculture[1]Source: USDA Foreign Agricultural Service, “Dairy and Products Annual – South Africa,” APPS.FAS.USDA.GOV. Nigeria's National Livestock Transformation Plan, allocating 5-year tax holidays and import-duty waivers, aims to triple domestic yogurt capacity by 2028, reducing reliance on powdered imports that accounted for USD 1.5 billion in 2024. The protein pivot also reshapes retail: hypermarkets in Riyadh and Dubai now dedicate 18-20% of chilled space to high-protein SKUs, up from 12% in 2023, signaling structural demand rather than fad.

Population Growth and Urbanization Boost Consumption of Convenient Processed Products

Nigeria's urban population surpassed 110 million in 2025, with Lagos and Abuja metro areas absorbing 2.8 million net migrants annually, compressing meal-preparation time and elevating demand for pre-marinated chicken, portion-controlled meatballs, and single-serve yogurt cups. Egypt's convenience-store footprint expanded 22% in 2024-2025, stocking ambient-stable processed cheese and UHT flavored milk that bypasses cold-chain gaps in secondary cities like Aswan and Luxor. Saudi Arabia's Vision 2030 target of 150 million annual tourists by 2030, up from 109 million in 2024, fuels quick-service restaurant proliferation; Dubai welcomed 19.5 million visitors in 2025, each generating 4.2 kilograms of meat and dairy consumption during their stay, according to UAE Ministry of Economy estimates. Processed-meat formats, like sausages, burgers, and kebabs, capture 38% of total meat volume in the GCC, versus 22% in sub-Saharan Africa, reflecting infrastructure maturity and disposable income. Morocco's dairy cooperatives introduced 200-milliliter flavored-milk pouches in 2025, priced at MAD 5 (USD 0.50), undercutting imported Tetra Pak cartons by 35% and penetrating rural souks previously reliant on loose milk.

Technological Advances Enhance Production Efficiency and Quality Control

Almarai deployed IoT-enabled milking parlors across its 170,000-head dairy herd in 2025, cutting labor costs per liter by 18% and lifting average yields to 11,200 liters per cow annually, 30% above the Middle East baseline. South Africa's Clover Industries integrated blockchain traceability for its artisanal cheese line, allowing retailers to verify pasture-to-shelf provenance within 48 hours, a capability that secured listings in Woolworths' premium tier and export contracts to the UAE at USD 6.68 per kilogram, double the commodity-beef rate. Egypt's cold-chain investments, USD 29 million committed by UAE-based Agthia and local partners in 2024, install 12,000 refrigerated lockers in Cairo and Alexandria, enabling direct-to-consumer dairy delivery within 4 hours of milking, preserving probiotic viability that ambient distribution destroys. Automated halal-slaughter lines, certified under GSO 993:2015, process 180 birds per minute with real-time pH and temperature monitoring, reducing non-compliance waste from 8% to under 2% and satisfying Saudi Food and Drug Authority export prerequisites, according to the Saudi Food and Drug Authority[2]Source: Saudi Food and Drug Authority, “Halal Certification Requirements,” SFDA.GOV.SA. Nigeria's FrieslandCampina WAMCO piloted solar-powered milk-collection centers in 2025, extending procurement reach to 14,000 smallholder farms and cutting spoilage from 22% to 9%, a breakthrough that narrows the import-substitution gap.

Shift to Premium, Artisanal Dairy and Meat Appeals to Affluent Segments

South Africa's artisanal cheese sector swept 12 medals at the 2024 World Cheese Awards, with entries from Stellenbosch and Western Cape commanding retail premiums of 40-60% over commodity cheddar, yet production remains constrained to 8,000 tons annually, less than 2% of national cheese output, leaving export potential largely untapped. Gulf consumers, particularly Emirati and Saudi nationals earning above USD 8,000 monthly, allocated 14% of grocery spend to organic and grass-fed labels in 2025, up from 9% in 2023, driving Al Rawabi Dairy to launch a certified-organic laban line priced at AED 12 (USD 3.27) per liter. Egypt's Juhayna introduced a Greek-style yogurt in 2025, fortified with 15 grams of protein per 150-gram cup and priced 25% above standard offerings, targeting Cairo's expatriate and upper-middle-class segments. The premiumization wave also reshapes packaging: single-origin dairy, traceable to specific farms, and heritage-breed beef gain shelf space in Dubai's Spinneys and Carrefour, signaling that affluent shoppers prioritize narrative over price

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy reliance on imports | -0.8% | Egypt, Nigeria, GCC (feed grains 80-90% imported) | Short term (≤ 2 years) |

| Competition from plant-based alternatives | -0.3% | UAE, Saudi Arabia urban centers, South Africa metros | Medium term (2-4 years) |

| Regulatory hurdles and food safety standards | -0.5% | GCC (SFDA, GSO), Nigeria (NAFDAC), South Africa (NFSA) | Short term (≤ 2 years) |

| High production costs limit scalability | -0.6% | Egypt, Nigeria, Morocco (feed, energy, cold-chain deficits) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heavy Reliance on Imports

Egypt imported 90% of its feed crops in 2024, exposing dairy and poultry margins to currency devaluation. The Egyptian pound weakened 38% against the dollar during 2024-2025, inflating maize costs by 40% and forcing processors to raise retail prices 12-18%, dampening volume growth. Nigeria's USD 1.5 billion annual dairy-powder import bill persists despite government incentives, as local milk collection remains fragmented across 180,000 smallholders lacking refrigeration, resulting in 22% spoilage before processing. The GCC's 80-85% food-import dependency spiked logistics costs when Red Sea disruptions in 2024-2025 rerouted shipments around the Cape of Good Hope, adding 14 days transit time and lifting freight premiums 250-500%, eroding processor margins by 3-5 percentage points. Sudan's civil conflict curtailed livestock exports to Egypt and Saudi Arabia, removing 1.2 million head of cattle from the regional supply in 2024 and pushing beef prices up 40% in Cairo's wholesale markets. South Africa's foot-and-mouth outbreak in 2024 triggered import bans from the UAE, Saudi Arabia, and Qatar, costing the industry ZAR 1.25 billion (USD 68 million) in lost beef exports and forcing producers to absorb inventory at 30% discounts domestically.

Competition from Plant-Based Alternatives

Plant-based meat and dairy alternatives remain niche in the Middle East and Africa, holding under 2% market penetration in 2025, yet niche growth in the UAE and South Africa urban centers signals emerging pressure on commodity animal-protein segments. Halal certification ambiguity constrains adoption: the GCC Standardization Organization has not issued unified guidance on plant-based products, leaving importers to navigate fragmented national rulings that add 6-12 weeks to launch timelines and SAR 15,000-50,000 in compliance costs per SKU. Price premiums of 40-60% over conventional dairy and meat deter price-sensitive shoppers in Egypt and Nigeria, where per-capita incomes average USD 3,800 and USD 2,200, respectively. However, affluent Gulf consumers, particularly expatriates and millennials, allocated 8% of their protein spend to plant-based options in 2025, up from 4% in 2023, driven by environmental and health narratives amplified on social media. South Africa's Woolworths expanded its plant-based range to 42 SKUs in 2025, capturing 3.2% of chilled-protein sales in metro stores, a share that could double by 2028 if pricing converges with conventional products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Dairy Beverages Outpace Commodity Segments

In 2025, meat products accounted for 62.38% of total revenues. However, dairy beverages are on the rise, boasting a 5.46% CAGR through 2031, the fastest growth rate among all product categories. This shift comes as Gulf consumers transition from sugary soft drinks to protein-fortified milk and probiotic smoothies. Al Safi Danone introduced a 36-gram protein milk format in 2025, targeting fitness enthusiasts and priced at a 30% premium over standard UHT milk. Their Greek Gelato yogurt line, featuring 15 grams of protein in a 150-gram cup, swiftly captured 8% of Saudi Arabia's chilled yogurt market within just six months. In the GCC, processed meats, encompassing sausages, burgers, and meatballs, constitute 38% of the total meat volume. This surge is fueled by the proliferation of quick-service restaurants and a booming tourism sector. In 2025, Dubai's 19.5 million visitors each consumed an estimated 4.2 kilograms of meat and dairy, heightening the demand for portion-controlled, halal-certified products. In South Africa, poultry, dominating the white meat category, accounts for 60% of the nation's meat consumption. Benefiting from a 12% year on year deflation in maize prices as of December 2025, processors managed to keep retail prices stable while boosting their margins. Meanwhile, red meats, comprising beef, lamb, and mutton, grapple with challenges. A foot and mouth outbreak in 2024 led to import bans in South Africa, halting exports to the UAE and costing the industry USD 68 million. Yet, premium lamb products, despite making up only 6% of the volume, command a notable 11% share of red meat revenue, driven by heightened demand during Ramadan gifting.

Cheese premiumization is reshaping the dairy landscape. South Africa's artisanal cheese producers clinched 12 medals at the 2024 World Cheese Awards. However, with an annual output of just 8,000 tons, less than 2% of the national production, their export potential remains largely untapped. Ice cream and frozen dairy products are witnessing steady growth, buoyed by Saudi Arabia's ambitious target of attracting 150 million tourists annually by 2030. The UAE's hospitality sector, with 650 hotel projects adding 161,574 rooms by 2032, is embedding dessert offerings as lucrative upsells. While health-conscious millennials are pressuring traditional dairy and butter volumes, Nigeria's National Livestock Transformation Plan, featuring 5-year tax holidays, is set to triple the country's yogurt capacity by 2028. This move aims to replace the USD 1.5 billion spent annually on dairy powder imports. The rising prominence of dairy beverages is underscored by structural demand shifts: Gulf hypermarkets have increased their chilled space allocation for high protein SKUs from 12% in 2023 to 18-20% now, highlighting the mainstreaming of functional nutrition.

By Distribution Channels: On-Trade Gains as Tourism and HoReCa Expand

In 2025, off-trade channels captured 56.85% of sales, led by supermarkets and hypermarkets offering ambient stable processed cheese and UHT milk. However, the on-trade sector is set to grow at a 6.02% CAGR through 2031. Saudi Arabia's Vision 2030 aims for an increase in annual tourists from 109 million in 2024 to 150 million by 2030. This surge fuels the rapid expansion of quick-service restaurants. Notably, each tourist is expected to consume 4.2 kilograms of meat and dairy, as per estimates from the UAE Ministry of Economy. In 2025, Dubai, with 19.5 million visitors, saw the rise of 650 hotel projects, translating to 161,574 rooms under construction. These establishments necessitate dairy and meat suppliers who prioritize consistency and halal certification over cost. Meanwhile, Egypt, with 14.9 million tourist arrivals in 2024, witnessed heightened demand in hotels, restaurants, and cafés for portion-controlled yogurt cups and pre-marinated chicken. These formats adeptly navigate cold chain challenges in secondary cities such as Aswan and Luxor.

Online retail channels within the off-trade sector are experiencing a surge at double-digit rates. Notably, average order values stand at USD 102 in the UAE and USD 52.50 in Saudi Arabia. In a significant move, UAE-based Agthia committed USD 29 million in 2024 to bolster Egypt's cold chain infrastructure. Their investment led to the installation of 12,000 refrigerated lockers in Cairo and Alexandria. This setup facilitates direct-to-consumer dairy deliveries within a mere 4 hours post milking, ensuring probiotic viability, something ambient distribution compromises. In Nigeria, convenience stores in the metro areas of Lagos and Abuja saw a 22% expansion between 2024 and 2025. These stores began stocking single-serve yogurt and processed meat, catering to urban migrants seeking quicker meal solutions. While supermarkets and hypermarkets continue to be foundational, their growth is outpaced by both the on-trade and online sectors. Price-sensitive consumers in Morocco and Egypt are increasingly drawn to discount formats and traditional wet markets. Here, they can purchase loose milk at MAD 5 (USD 0.50) for 200 milliliters, a price that undercuts branded UHT milk by 35%.

Geography Analysis

Saudi Arabia, leveraging its sovereign wealth, has established vertically integrated dairy poultry complexes, reducing its fresh milk import dependency from 80% to under 40%. This move, a cornerstone of Vision 2030's USD 10 billion food security initiative, has positioned the nation to seize 58.68% of the 2025 demand. With an eye on tourism, Saudi Arabia targets 150 million annual visitors by 2030, fueling a surge in quick-service restaurants. Each tourist, as per the UAE Ministry of Economy, is projected to consume about 4.2 kilograms of meat and dairy[3]Source: Hospitality Net Reporter, “MENA Hospitality Market to Reach $487 Billion by 2032,” HOSPITALITYNET.ORG. The United Arab Emirates, though smaller in scale, is echoing Saudi Arabia's strategies. Dubai, anticipating 19.5 million visitors in 2025, is witnessing a hotel boom with 650 projects adding 161,574 rooms by 2032. These establishments are embedding contracted dairy and meat suppliers, emphasizing halal compliance and consistency.

South Africa, the fastest-growing nation at a 5.78% CAGR, is shifting its focus from commodity beef to artisanal cheese. Producers proudly clinched 12 medals at the 2024 World Cheese Awards and celebrated a 50% surge in export volume, even amidst trade bans due to foot and mouth disease. Backed by a government investment of ZAR 1.8 billion (USD 98 million), the nation is rolling out a vaccination campaign for its 12.1 million head of cattle. The goal? To reclaim export access to the UAE and Saudi Arabia, markets where South African beef once fetched a premium USD 6.68 per kilogram, double the commodity rate. Poultry, accounting for 60% of the nation's meat consumption, is reaping benefits from a 12% year on year drop in maize prices as of December 2025. This price stability has allowed processors to maintain retail prices while boosting their margins, as reported by the Global Agricultural Information Network. In Nigeria, a staggering USD 1.5 billion annual dairy import bill has led to a 5-year tax holiday for local processors. However, with over 90% dependency on feed crop imports, margins remain vulnerable to currency fluctuations and freight costs. In Morocco, dairy cooperatives made significant strides in 2025, deploying 340 mobile refrigerated trucks. This initiative connected 11,000 smallholders to Casablanca processors within a mere 6 hours of milking, resulting in an 18% uplift in farmgate prices and a stabilized supply.

The broader Middle East and Africa region, which includes Morocco, Nigeria, and several smaller Gulf states, is witnessing fragmented growth. Challenges like cold chain gaps and regulatory inconsistencies loom large. Yet, with government incentives and infrastructure loans, there is a burgeoning opportunity for processors. Investments are flowing into on-farm feed mills and direct to consumer e-commerce platforms. Morocco's ambitious Green Generation strategy has earmarked MAD 12 billion (USD 1.2 billion) through 2030. The funds are directed towards subsidizing cooperative dairy plants and halal-certified slaughterhouses, with a goal to elevate domestic meat processing from 52% to 68% of total output. Meanwhile, Nigeria's National Livestock Transformation Plan is setting its sights on tripling the nation's yogurt capacity to 180,000 tons annually by 2027, aiming to curtail imports and tap into lucrative margin pools beyond the reach of commodity players.

Competitive Landscape

The market shows low consolidation, with Almarai, Savola, and Juhayna coexisting alongside agile private-label entrants. These newcomers are adeptly exploiting cold chain gaps in Morocco and Nigeria. Almarai, with a USD 4.8 billion capital program set through 2028, is set to double its poultry capacity to an impressive 450 million birds annually. This move not only embeds backward integration, shielding Almarai from the whims of volatile maize prices, but also positions the company as the supplier of 63.7% of Saudi Arabia's fresh milk market. In 2024, Savola Group made waves with its SAR 8 billion (USD 2.13 billion) acquisition of Panda Retail. This strategic move vertically integrates distribution for Savola, ensuring prime shelf space for its dairy and processed meat brands in 300 hypermarkets, all while slashing logistics costs by 14%, as reported by Arab News. Juhayna Food Industries, commanding a 40% share of Egypt's domestic yogurt market, is pioneering direct-to-consumer e-commerce. They've installed 12,000 refrigerated lockers in Cairo and Alexandria, facilitating deliveries within 4 hours of milking. This innovation preserves probiotic viability, a feat often compromised by ambient distribution. Competing in South Africa, RCL Foods and Astral Foods are at the forefront of automation. They've rolled out IoT-enabled slaughter lines, processing 180 birds per minute. With real-time pH monitoring, they've successfully reduced non-compliance waste from 8% to under 2%, meeting the stringent export prerequisites of the Saudi Food and Drug Authority.

Three primary vectors highlight the clustering of white space opportunities: processors are investing in on farm feed mills, sidestepping import dependencies and currency risks, thus tapping into margin pools elusive to commodity players; direct to consumer e-commerce platforms are bypassing traditional retail routes, ensuring cold chain integrity and commanding premium pricing; and ultra high temperature dairy formats are making inroads into secondary cities in Egypt and Nigeria, navigating cold chain gaps that hinder chilled distribution. Emerging disruptors are making their mark: South Africa's artisanal cheese cooperatives, boasting 12 medals from the 2024 World Cheese Awards, are currently limited to an annual output of 8,000 tons.

Meanwhile, Nigeria's FrieslandCampina WAMCO is making strides with its solar-powered milk collection centers, launched in 2025. These centers have broadened procurement reach to 14,000 smallholder farms and significantly reduced spoilage from 22% to 9%. Technology adoption is a key differentiator among industry leaders: Almarai, in 2025, integrated IoT-enabled milking parlors across its expansive 170,000-head dairy herd. This move not only trimmed labor costs per liter by 18% but also boosted average yields to an impressive 11,200 liters per cow annually, outpacing the Middle East baseline by 30%.

Middle-East And Africa Animal-based Meat And Dairy Products Industry Leaders

Almarai Company

Al-Watania Poultry Co.

Al Islami Foods

Danone S.A.

Al Kabeer Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Slim Chickens marked its regional debut by opening its first Middle East restaurant in Dubai, entering the UAE’s fast‑casual dining scene with a US‑style comfort‑chicken concept. The launch, carried out in partnership with Emirates Leisure Retail, positioned the brand as a new Southern‑inspired chicken‑tenders and wings offering in Dubai.

- July 2025: Milky Ice Cream expanded its footprint in the Middle East by debuting new flagship cafes in the UAE and Saudi Arabia, reinforcing its presence in the region’s premium dessert‑and‑ice‑cream segment. The rollout included high‑visibility locations and concept‑driven outlets, targeting tourists and local consumers seeking indulgent, Instagram‑worthy ice‑cream.

- March 2025: Fairfield Dairy launched a new range of kids’ yogurt cups in blueberry, strawberry, and litchi flavors, specifically formulated to appeal to children’s taste preferences while maintaining a smooth, creamy texture.

Middle-East And Africa Animal-based Meat And Dairy Products Market Report Scope

Animal-based meat and dairy products market cover milk and meat-derived food and beverage products. The market studied is segmented by type, distribution channel, and geography. Based on type, the market studied is segmented into processed meat, dairy beverages, ice cream, cheese, yogurt, and food spreads. Based on distribution channel, the market studied is segmented into hypermarkets/supermarkets, convenience stores, online retail channels, and other distribution channels. Based on geography, the market studied is segmented into South Africa, the United Arab Emirates, Saudi Arabia, Egypt, and Rest of Middle-East and Africa. The report offers market size and forecasts in value (USD million) for all the above segments.

| Dairy Products | Milk | |

| Yogurt | ||

| Cheese | ||

| Butter | ||

| Ice Cream & Frozen Dairy | ||

| Dairy Beverages (Flavored / Functional) | ||

| Others | ||

| Meat Products | Red Meat | Beef |

| Lamb & Mutton | ||

| Others | ||

| White Meat | Chicken | |

| Others | ||

| Processed Meat | Sausages | |

| Burgers & Patties | ||

| Meatballs | ||

| Others | ||

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Channels | |

| Other Distrbution Channels |

| Saudi Arabia |

| South Africa |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Rest of Middle East and Africa |

| Product Type | Dairy Products | Milk | |

| Yogurt | |||

| Cheese | |||

| Butter | |||

| Ice Cream & Frozen Dairy | |||

| Dairy Beverages (Flavored / Functional) | |||

| Others | |||

| Meat Products | Red Meat | Beef | |

| Lamb & Mutton | |||

| Others | |||

| White Meat | Chicken | ||

| Others | |||

| Processed Meat | Sausages | ||

| Burgers & Patties | |||

| Meatballs | |||

| Others | |||

| Distribution Channels | On-Trade | ||

| Off-Trade | Supermarkets/Hypermarkets | ||

| Convenience Stores | |||

| Online Retail Channels | |||

| Other Distrbution Channels | |||

| Geography | Saudi Arabia | ||

| South Africa | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

How fast will dairy beverages grow in the Middle East and Africa animal based meat and dairy products market?

Dairy beverages are on track for a 5.46% CAGR through 2031, the highest among all product lines.

Which country contributes the most demand?

Saudi Arabia supplied 58.68% of regional value in 2025, driven by Vision 2030 food-security investments.

What is the biggest restraint to supply growth?

Heavy reliance on imported feed grains subtracts 0.8 percentage points from forecast CAGR.

How are companies protecting margins from freight volatility?

Leading processors invest in on-farm feed mills and subsidized cold-chain assets to cut external exposure.

Page last updated on: