Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

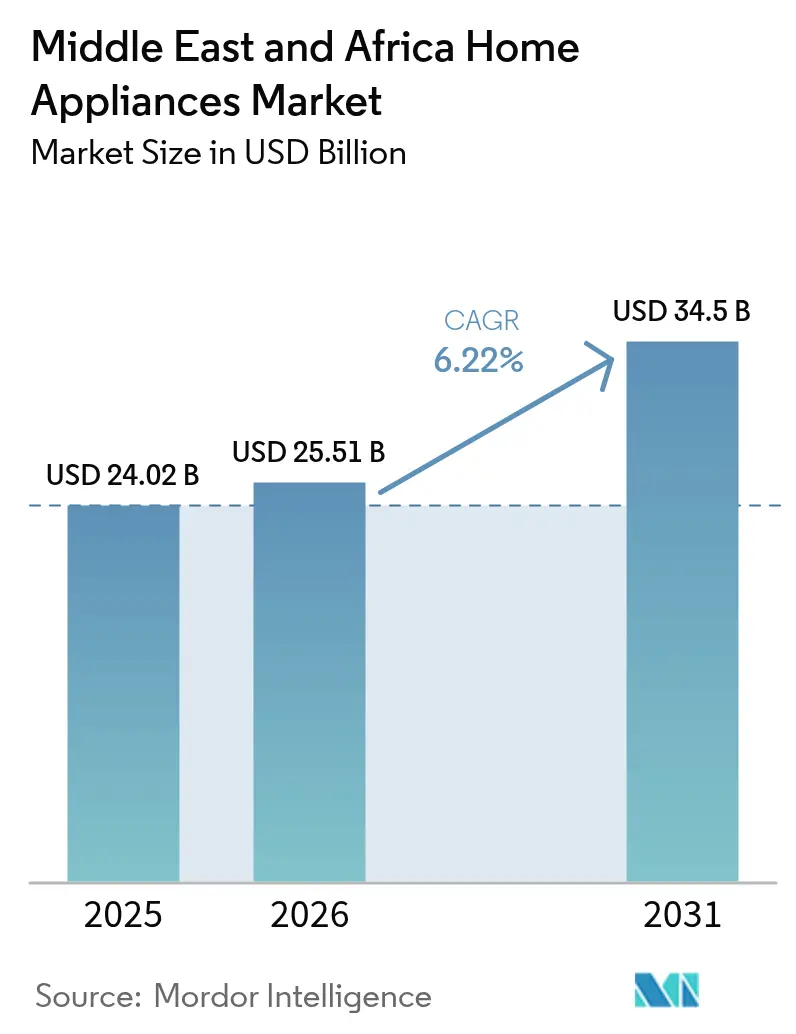

| Base Year Market Size (2025) | USD 24.02 Billion |

| Market Size (2026) | USD 25.51 Billion |

| Market Size (2031) | USD 34.5 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

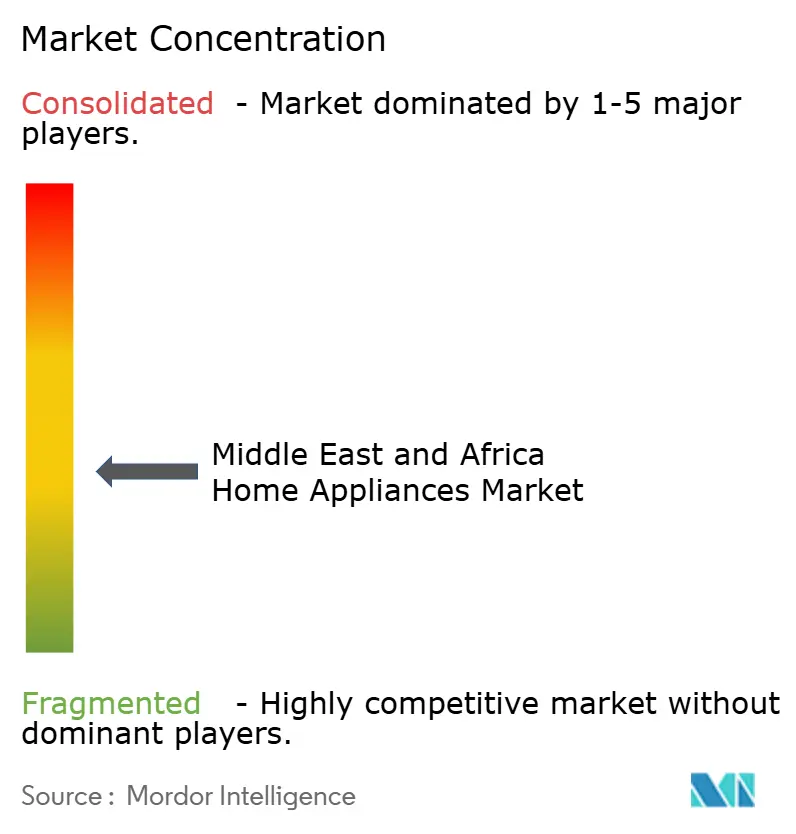

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Home Appliances Market Analysis by Mordor Intelligence

Middle East and Africa home appliances market size in 2026 is estimated at USD 25.51 billion, growing from 2025 value of USD 24.02 billion with 2031 projections showing USD 34.5 billion, growing at 6.22% CAGR over 2026-2031. This market size trajectory rests on rapid urban migration, state-sponsored electrification projects, and widening e-commerce access that combine to create both first-time purchases and quicker upgrade cycles. Premium demand in Gulf Cooperation Council (GCC) states co-exists with value-driven growth in sub-Saharan Africa, giving the Middle East and Africa home appliances market a dual-speed profile that rewards smart-home innovators and cost-efficient producers. Energy-efficiency regulations across GCC states and South Africa accelerate replacements, while off-grid solar solutions open rural revenue streams where the grid lags. Currency swings, import duties, and water scarcity moderate growth but prompt global brands to invest in regional assembly and resource-efficient design.

Key Report Takeaways

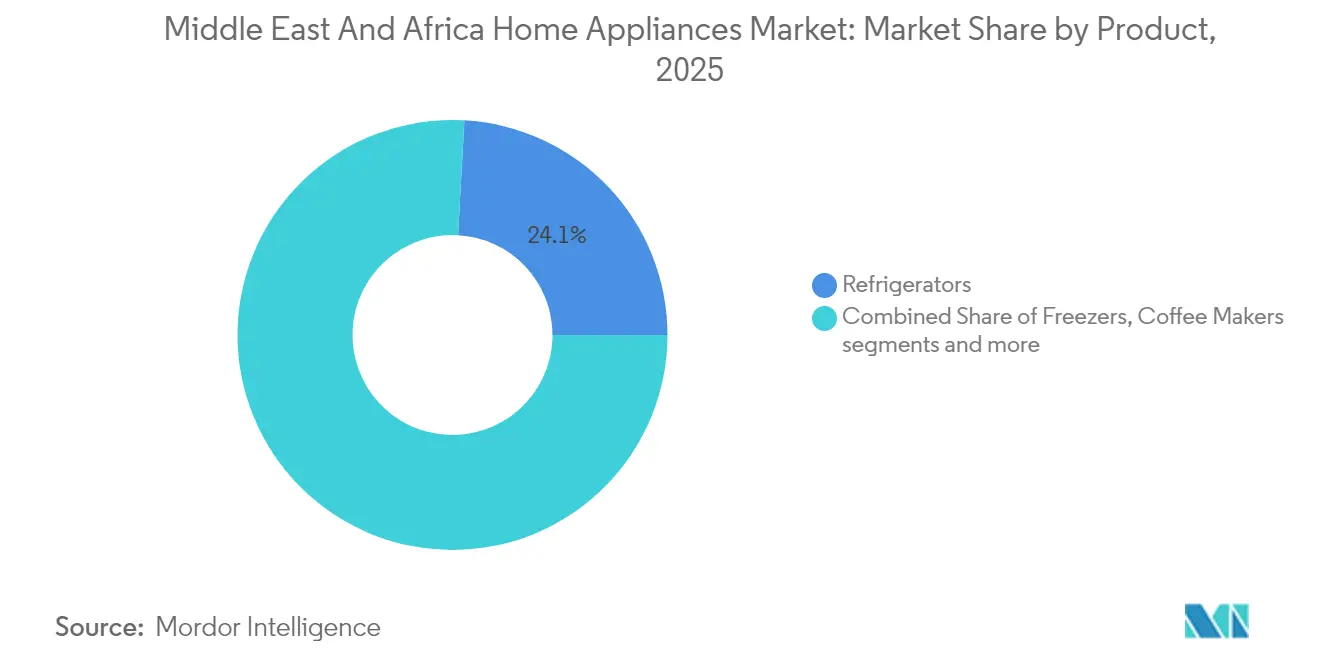

- By product category, refrigerators led with 24.12% revenue share of the Middle East and Africa home appliances market in 2025, while air fryers are forecast to expand at a 7.02% CAGR to 2031.

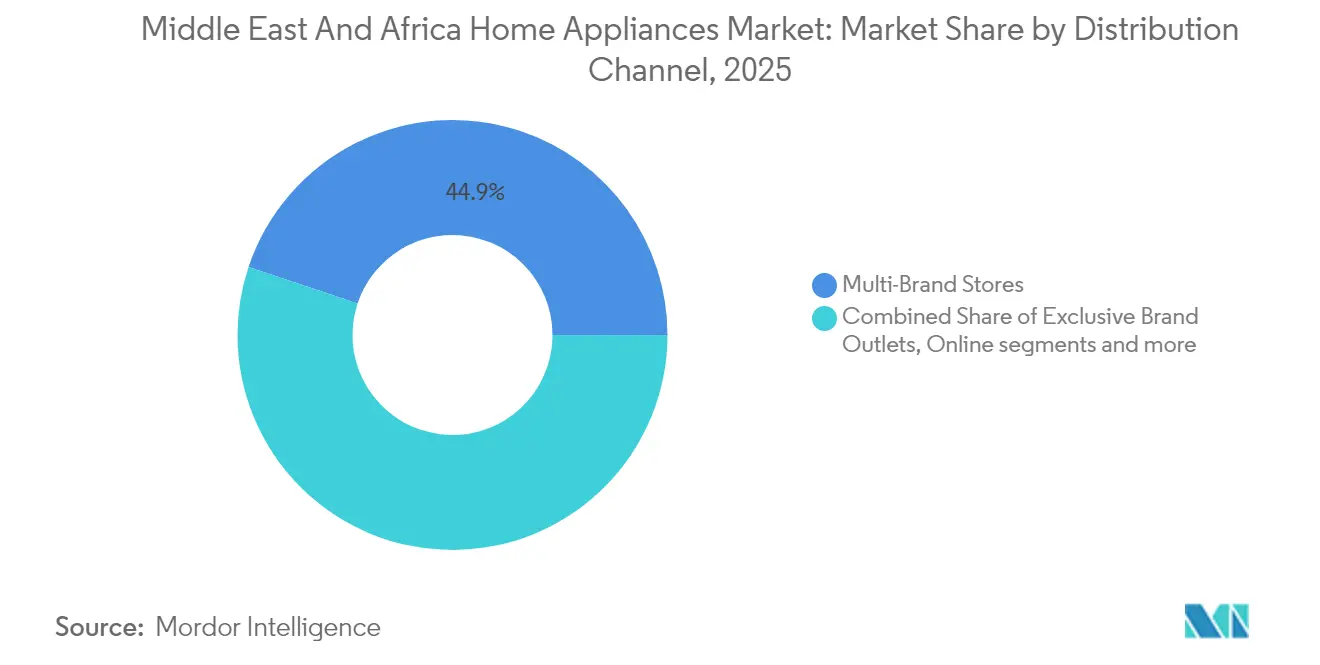

- By distribution channel, multi-brand stores accounted for 44.88% of the Middle East and Africa home appliances market size in 2025, and online channels are advancing at a 7.28% CAGR through 2031.

- By geography, Saudi Arabia led with a 14.35% share of the Middle East and Africa home appliances market in 2025, and Nigeria recorded the highest projected CAGR at 6.67% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urbanization & disposable income | +1.8% | Nigeria, South Africa, and Saudi Arabia urban centers | Medium term (2-4 years) |

| Government electrification programs | +1.2% | Sub-Saharan Africa, rural Saudi Arabia | Long term (≥4 years) |

| Growing e-commerce penetration | +1.0% | UAE, Saudi Arabia, Nigeria's major cities | Short term (≤2 years) |

| Energy-efficiency regulations spurring replacements | +0.9% | GCC states, South Africa | Medium term (2-4 years) |

| Off-grid solar-powered appliances uptake | +0.6% | Rural Africa, Kenya, Ghana | Long term (≥4 years) |

| High-end smart-home adoption in Gulf states | +0.5% | UAE, Qatar, Saudi Arabia | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Urbanization & Disposable Income

Accelerating urban migration strengthens demand nodes because city residents favor branded appliances that promise reliability and warranty coverage[1]U.S. Department of Agriculture Foreign Agricultural Service, “Retail Foods Annual (NI2024-0014),” usda.gov. Wage growth in Riyadh, Jeddah, and Dubai feeds premium uptake, while burgeoning middle-class households in Lagos and Johannesburg focus on entry-to-mid tiers that blend functionality with affordability. Apartment living drives interest in space-saving washer-dryer combos, air fryers, and robotic vacuums. Higher residential density also lowers last-mile logistics costs, encouraging retailers to offer same-day delivery on large items. Manufacturers that provide micro-financing or buy-now-pay-later plans extend reach to credit-thin consumers, making urbanization a structural tailwind for the Middle East and Africa home appliances market.

Government Electrification Programs

Grid-extension schemes in Kenya, Ghana, and Nigeria collectively connect millions of rural homes each year, creating new first-time buyers for refrigerators and fans. Public incentives often package appliance discounts with energy-efficient bulbs, moving households immediately toward compliant products. Saudi Arabia’s air-conditioner replacement plan, which refunds up to SAR 1,000 per compliant unit, shows how government support can move volumes in months[2]Saudi Energy Efficiency Center, “Initiative to Replace Old Window Air Conditioners Expands Nationwide,” seec.gov.sa. Electrification also attracts component suppliers, because reliable power reduces operational risk for local assembly. For the Middle East and Africa home appliances market, each electrified village represents demand that compounds as income rises.

Growing E-Commerce Penetration

The increasing adoption of smartphones and advancements in warehousing infrastructure have significantly boosted online conversion rates, even for bulky goods. Leading e-commerce platforms in Nigeria now offer two-day shipping for select refrigerators, enhancing accessibility in rural regions. These platforms provide detailed product information, enabling smaller manufacturers to compete effectively by showcasing energy efficiency and smart-home features alongside global brands. Shopper analytics are leveraged to design targeted advertisements, reducing customer acquisition costs and improving marketing efficiency. Hybrid purchasing behaviors are gaining momentum, as consumers research products online, verify dimensions in physical stores, and complete transactions through mobile apps that integrate delivery and installation services. This shift underscores the growing importance of omnichannel strategies in the market. The combination of improved logistics, data-driven marketing, and hybrid shopping models is reshaping the competitive landscape for bulky goods in Nigeria.

Energy-Efficiency Regulations Spurring Replacements

Ghana enacted 19 appliance efficiency standards in late 2023, joining the UAE and Saudi Arabia in banning low-efficiency imports[3]Nemko, “Energy Efficiency Regulations in Ghana: Steps Toward a Greener Future,” nemko.com. Labels that translate kilowatt-hours into monthly cost comparisons nudge buyers toward inverter technology and eco modes. Utilities in South Africa offer top-up rebates, shortening payback periods for efficient washers that cut electricity and water consumption simultaneously. Compliance requirements favor incumbents with global R&D because they certify new models quickly. As replacements accelerate, the Middle East and Africa home appliances market gains incremental volume without waiting for population growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import duties & tariffs | -1.1% | Nigeria, South Africa, Kenya | Short term (≤2 years) |

| Currency volatility in key African markets | -0.8% | Nigeria, Ghana, Kenya, Mozambique | Short term (≤2 years) |

| GCC water scarcity limiting washer demand | -0.4% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Vibrant second-hand appliance market | -0.3% | Nigeria, Ghana, Kenya, South Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Import Duties & Tariffs

Nigeria's tariff structure increases the landed costs of washers by up to 30%, reducing affordability and driving consumers toward refurbished products. To mitigate these costs, major manufacturers adopt semi-knocked-down kits, which qualify for lower duties but require investments in tooling, local labor, and skills development. Tariff volatility poses a significant challenge for quarterly forecasting, as shipments ordered under one tariff regime may arrive after rates have changed. This unpredictability disproportionately impacts smaller brands, which struggle to hedge against such risks. In contrast, larger multinational companies leverage their resources to gain a competitive advantage. However, these dynamics contribute to higher consumer prices across the Middle East and Africa home appliances market. The interplay of tariffs, supply chain adjustments, and market competition continues to shape the region's pricing landscape.

Currency Volatility in Key African Markets

The naira's successive devaluations have introduced significant volatility in retail prices, discouraging discretionary spending on appliances such as refrigerators and washers. Retailers are adopting strategies like dollar-indexed pricing or reducing inventory cycles to manage exposure, though these measures increase operating costs. Importers relying on foreign currency letters of credit face liquidity pressures, often resulting in shipment delays. Efforts by brands to localize production, such as manufacturing plastic parts and metal cabinets domestically, have been constrained by the continued reliance on imported compressors and electronics for key components. These currency fluctuations have hindered the adoption of premium models, shifting consumer demand toward lower-spec alternatives. The overall market dynamics reflect a challenging environment for both retailers and manufacturers, driven by currency instability and rising costs. Consequently, the focus remains on cost management and adapting to shifting consumer preferences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Major Appliances Drive Volume, Small Appliances Capture Growth

Refrigerators held a 24.12% share of the Middle East and Africa home appliances market in 2025, reflecting their status as a durable necessity in hot climates. By contrast, air fryers led growth with a 7.02% CAGR, underscoring lifestyle shifts toward quick, oil-light cooking. Major appliances remain the revenue anchor because electrification and urban housing programs expand addressable households. Regulations that phase out inefficient compressors encourage repeat sales and lift the Middle East and Africa home appliances market size through premium tiers. Small appliances benefit from shorter innovation cycles; new coffee-grinder variants or multi-purpose blenders spark habitual upgrades. Chinese newcomers leverage global supply chains to introduce affordable smart-enabled models, raising competitive stakes.

Urban kitchens drive demand for compact microwave-oven combos and collapsible food processors. In GCC states, built-in appliances gain favor because luxury villas integrate open-plan kitchens. African buyers prioritize robustness and aftermarket parts availability when selecting major appliances, especially in countries where voltage fluctuations are common. Cross-selling strategies bundle kettles or toasters with refrigerator purchases, elevating basket value. Air conditioners and washers face divergent water-resource realities: high penetration in humid West Africa versus cautious adoption in arid Gulf cities. Energy labels stimulate competition around kWh savings, and marketing now frames purchase decisions around lifetime operating cost rather than upfront price.

By Distribution Channel: Multi-Brand Dominance Faces Digital Disruption

Multi-brand retailers captured 44.88% of 2025 sales because shoppers rely on side-by-side comparisons and in-store demonstrations. Trained salespeople explain inverter technology, warranty terms, and financing options, sustaining trust with first-time buyers. Stores embed QR codes that link to virtual catalogs, extending shelf space without physical inventory. Yet the online channel posts a 7.28% CAGR, driven by improved courier networks and mobile wallets that lower payment friction. Cross-border e-commerce allows Gulf expatriates to ship gifts directly to African relatives, injecting incremental demand into the Middle East and Africa home appliances market.

Manufacturers now enforce price parity across outlets to deter grey imports. Exclusive brand boutiques showcase flagship refrigerators with AI temperature controls, creating experiential touchpoints that justify premium mark-ups. Hypermarkets still move large volumes of basic kettles and irons during monthly promotions. In Nigeria, where traditional trade remains 70% of retail, distributors deploy mobile vans as rolling showrooms for peri-urban areas. Consumer-to-consumer marketplaces facilitate resale, extending product life cycles but also cannibalizing new sales. Successful channel strategies synchronize inventory feeds, so online shoppers' views align with real-time store availability, boosting click-and-collect transactions.

Geography Analysis

Saudi Arabia leads the Middle East and Africa home appliances market with a 14.35% share, buoyed by Vision 2030 construction projects and generous consumer lending. Appliance importers benefit from predictable customs regimes and well-regulated after-sales networks. Sustainability mandates prompt households to replace old window air conditioners with inverter split units that save energy and qualify for rebates. UAE remains the region’s design trendsetter, as Dubai’s free-zone logistics shorten lead times and duty-free re-exports. Its multicultural consumer base embraces global brands and demands connected features that integrate with Arabic-language voice assistants.

Nigeria records the fastest growth at 6.67% CAGR because its urban population expands by over 4 million people annually. The market’s fragmentation forces producers to segment offerings finely by state, income, and cultural cooking preferences. Currency risks deter premium expansion, yet local assembly projects counterbalance, positioning Nigeria as both a sales hub and a potential export base to neighboring ECOWAS states. South Africa contributes scale through nationwide retail chains, reliable credit bureaus, and repair-technician networks that accommodate extended warranties. Buyers protect budgets through holiday sales, but brand loyalty is strong when service is dependable.

Rest-of-Middle East and Africa markets vary widely. Kenya and Ghana leverage last-mile motorcycle couriers to distribute small appliances to rural households, while Egypt’s cluster of component factories anchors North African supply chains. Morocco integrates European efficiency norms quickly, giving EU-based appliance makers a staging ground. Qatar and Kuwait, though smaller, add premium volume via hospitality projects tied to the 2030 Asian Games and other mega events. Across this diversity, the Middle East and Africa home appliances market rewards manufacturers that calibrate feature sets—such as dual-voltage transformers or Arabic recipe libraries—by micro-region.

Competitive Landscape

The Middle East and Africa home appliances market demonstrates moderate concentration, with a few key players dominating the market. Samsung and LG maintain a stronghold in the premium segment by offering innovative features such as embedded cameras in refrigerators and seamless integration with their SmartThings and ThinQ ecosystems, enabling advanced remote diagnostics. Hisense and Midea capitalize on strategic manufacturing operations in Egypt and Ethiopia, which help mitigate tariff challenges and facilitate quicker product launches. Dreametech's planned entry into the major appliances category reflects a strategic shift among vacuum-focused brands, aiming to diversify their offerings and capture a larger share of consumer spending across the home appliances market.

Regional assemblers in Egypt, Kenya, and South Africa leverage duty shelters to produce refrigerator cabinets and washer drums locally, then import compressors and control boards. Such hybrids shorten lead times and enable mass customization, including Arabic interface panels and voltage stabilizers. Competitive strategy increasingly centers on sustainability claims such as R600a refrigerators and water-recycling washer cycles. Brands invest in customer-experience platforms that schedule service within 48 hours, trying to satisfy directly to repeat sales. Digital trade-in portals accept old appliances for recycling, a tactic that secures raw materials and reinforces green branding.

Strategic alliances dominate 2025 headlines. Hisense partners with Jumbo Electronics unlock GCC omnichannel reach, while Whirlpool aligns with regional developers to supply built-ins for new housing. Tuya Smart embeds its IoT modules in local OEM lines, ensuring smaller players offer smart-home compatibility. Price competition, while present, is moderated by import duties that limit the volume of ultra-low-cost entrants. Warranty duration, energy label ratings, and connectivity features thus emerge as decisive purchase criteria in the Middle East and Africa home appliances market.

Middle East And Africa Home Appliances Industry Leaders

Samsung Electronics

Whirlpool Corporation

Haier Smart Home (incl. Hisense)

BSH Hausgeräte

LG Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Dreametech announced a strategic leap beyond its vacuum heritage by debuting air conditioners, refrigerators, and washing machines at AWE 2025. Executives confirmed the line-up would leverage proprietary brushless-motor technology for energy savings and integrate with the firm’s existing app ecosystem. The company also revealed that its global retail footprint had surpassed 4,000 offline stores, signaling serious intent to compete with incumbent majors.

- February 2025: Hisense formed an expanded distribution alliance with Jumbo Electronics that grants the Chinese brand shelf priority and shared marketing budgets across GCC malls. The deal complements Hisense’s ongoing construction of an Egyptian manufacturing plant designed to supply North and East Africa with duty-free stock. Management stated that regional revenue has doubled since 2019, underscoring the partnership’s potential to sustain momentum.

- January 2025: Samsung launched a multi-country trade-in initiative that lets consumers exchange functioning older appliances for credit toward premium models. The program includes free haul-away and certified recycling, reducing e-waste while nudging households toward higher-margin smart refrigerators and washers. Early sign-ups exceeded projections in the UAE and Saudi Arabia, pointing to strong latent demand for eco-friendly upgrade paths.

- December 2024: KBN Group Holding and Whirlpool celebrated surpassing 50,000 B2B appliance installations in Qatar’s hotel and residential projects within two years. The firms mapped expansion into B2C channels via flagship brand shops, promising unified after-sales service and omni-channel ordering. Executives highlighted that consistent bulk orders lowered per-unit logistics cost, improving price competitiveness.

Middle East And Africa Home Appliances Market Report Scope

A complete background analysis of the Middle East and Africa Home Appliances Industry, which includes an assessment of the industry associations, overall economy, and emerging market trends by segments, significant changes in the market dynamics, and market overview is covered in the report. Middle East and Africa Home Appliances Market is Segmented by Major Appliances (Refrigerators, Freezers, Dishwashing Machines, Washing Machines, and Cookers & Ovens), Small Appliances (Vacuum Cleaners, Small Kitchen Appliances, Hair Clippers, Irons, Toasters, Grills & Roasters, and Hair Dryers), Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, E-Commerce and Others). The Report Offers Market Size and Forecasts for the Middle East and Africa Home Appliances Market in Value (USD Billion) for all the above Segments.

By Product

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Countertop Ovens | |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| South Africa |

| Nigeria |

| Rest of Middle East And Africa |

| By Product | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Roasters | ||

| Electric Kettles | ||

| Juicers & Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Toasters | ||

| Countertop Ovens | ||

| Other Small Home Appliances | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the projected value of the Middle East and Africa home appliances market by 2031?

The market is expected to reach USD 34.5 billion by 2031, reflecting a 6.22% CAGR.

Which product currently dominates sales in the region?

Refrigerators hold the largest share at 24.12% as of 2025.

Which country is expanding fastest in appliance demand?

Nigeria posts the highest forecast CAGR at 6.67% because of rapid urbanization and a growing middle class.

How are efficiency rules influencing buying behavior?

Mandatory standards in GCC and selected African states push consumers toward inverter air conditioners and energy-rated refrigerators, shortening replacement cycles.

Which channel is gaining the most traction for appliance purchases?

Online platforms lead growth at a 7.28% CAGR, helped by improved logistics and mobile payments.

How do import duties affect appliance pricing?

Duties as high as 30% in markets like Nigeria raise retail prices and encourage manufacturers to invest in local assembly to remain competitive.

Page last updated on: