Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

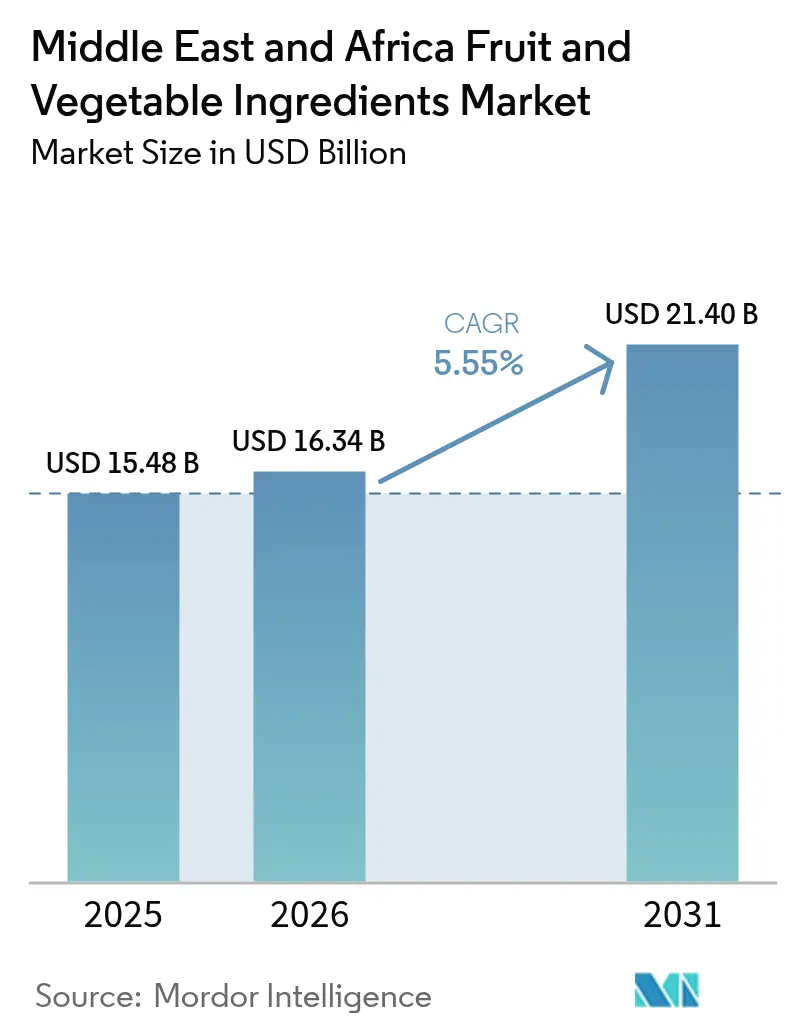

| Base Year Market Size (2025) | USD 15.48 Billion |

| Market Size (2026) | USD 16.34 Billion |

| Market Size (2031) | USD 21.4 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

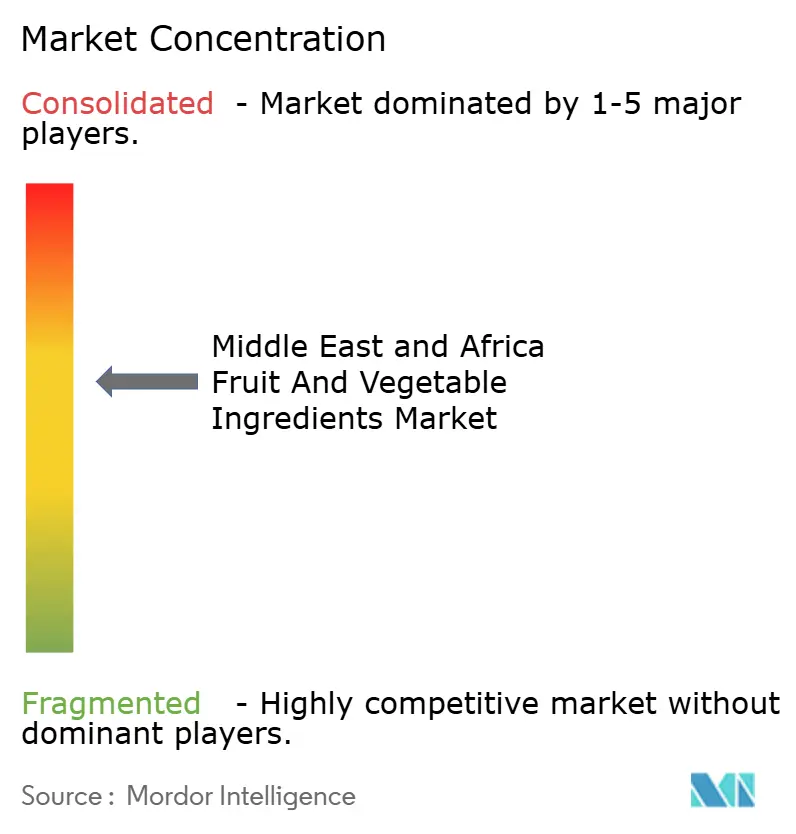

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Fruit And Vegetable Ingredients Market Analysis by Mordor Intelligence

The Middle East and Africa fruits and vegetables ingredients market size in 2026 is estimated at USD 16.34 billion, growing from 2025 value of USD 15.48 billion with 2031 projections showing USD 21.4 billion, growing at 5.55% CAGR over 2026-2031. The increasing demand is fueled by a shift toward natural formulations, the implementation of front-of-pack sugar-reduction regulations, and the expansion of horticulture programs. Additionally, advancements in drying and encapsulation technologies are enabling the development of innovative products. In response, ingredient manufacturers are offering a variety of solutions, such as date- and grape-based sweeteners, carotenoid-rich concentrates, and shelf-stable powders that help reduce cold-chain costs. While cost-conscious processors continue to rely on synthetic options, stricter regulations in Gulf markets are driving the adoption of natural alternatives. Competitive success in this market increasingly depends on local sourcing, technical support, and fast delivery, providing regional processors with an advantage in securing short lead-time contracts. Although challenges like limited shelf life, tariffs on exotic concentrates, and post-harvest losses persist, investments in freeze-drying technologies and solar-powered cold storage are contributing to the development of more resilient supply chains.

Key Report Takeaways

- By ingredient type, fruits led with 58.45% of the Middle East and Africa fruits and vegetables ingredients market share in 2025; vegetables are forecast to expand at a 5.72% CAGR through 2031.

- By form, concentrates accounted for a 32.88% share of the Middle East and Africa fruits and vegetables ingredients market size in 2025, while powders are advancing at a 5.68% CAGR to 2031.

- By application, beverages held 29.46% revenue share in 2025 and are set to grow at a 6.45% CAGR through 2031.

- By geography, the United Arab Emirates captured 27.61% of the market in 2025; South Africa posts the fastest forecast CAGR at 5.83% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Fruit And Vegetable Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of fruit-based sugar-replacers by beverage formulators | +1.2% | UAE, Saudi Arabia, Egypt, with spillover to South Africa | Medium term (2-4 years) |

| Growing consumer shift to clean-label and natural additives | +1.0% | UAE and Saudi Arabia | Long term (≥ 4 years) |

| Demand for preservatives in RTE/RTC foods and beverages drives ingredient adoption | +0.8% | UAE, Saudi Arabia, South Africa, Egypt | Medium term (2-4 years) |

| Growth of plant-based and vegan foods | +0.7% | UAE, Saudi Arabia, South Africa | Medium term (2-4 years) |

| Government-backed horticulture expansion programs | +0.9% | Saudi Arabia, UAE, Egypt, with early gains in Riyadh, Cairo, Alexandria | Long term (≥ 4 years) |

| Technological advancements in drying, freeze-drying, and encapsulation improve the product | +0.6% | UAE processing hubs and South African citrus zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing adoption of fruit-based sugar-replacers by beverage formulators

Beverage manufacturers in the Gulf Cooperation Council are replacing high-fructose corn syrup with date, apple, and grape concentrates to meet front-of-pack labeling regulations that penalize added sugars. In 2024, Saudi Arabia's Food and Drug Authority implemented nutrient-profiling thresholds requiring beverages with more than 5 grams of added sugar per 100 milliliters to display warning labels. This has triggered a wave of reformulations among carbonated soft drink and juice producers. Date syrup, with a glycemic index of 55 to 60, enables formulators to claim it as a "naturally occurring sugar." This approach helps avoid added-sugar penalties while providing caramel notes that mask off-flavors from plant proteins. These regulatory changes are driving increased demand for naturally sweet fruit concentrates, which reduce reliance on crystalline sucrose and avoid consumer resistance to artificial sweeteners. The growing beverage manufacturing sector in the Middle East and Africa (MEA) is fueling demand for fruit and vegetable ingredients, as formulators seek low-calorie, clean-label alternatives to refined sugars in response to health trends and regulations. The General Authority for Statistics in Saudi Arabia reported that the beverage manufacturing industry generated USD 3.13 billion in revenue in 2024 [1]Source: General Authority for Statistics in Saudi Arabia, "Manufacture of Beverages", stats.gov.sa. Ingredients such as concentrates, purees, and powders derived from apples, pears, dates, and berries are effective sugar substitutes. They provide sweetness, bulk, texture, and flavor while lowering calorie content in juices, soft drinks, and functional beverages.

Growing consumer shift to clean-label and natural additives

Consumers in the Middle East and Africa are placing greater emphasis on ingredient transparency. This change is driving dairy, bakery, and confectionery manufacturers to adjust their procurement strategies. These manufacturers are increasingly choosing natural alternatives, such as anthocyanin-rich berry extracts and beta-carotene from carrot concentrates, to replace synthetic colors like tartrazine and sunset yellow. In premium retail outlets across Dubai, Riyadh, and Johannesburg, clean-label products are commanding a price premium. This trend incentivizes formulators to offset the higher costs of natural fruit and vegetable ingredients. Regulatory developments are further supporting this shift: In 2024, the UAE's Emirates Authority for Standardization and Metrology updated its additive whitelist, banning certain synthetic colorants in products targeted at children. This change effectively mandates the use of natural alternatives in items like juice boxes and dairy desserts. The clean-label trend also extends to flavor and preservation, with citrus extracts and rosemary oleoresin increasingly replacing sodium benzoate and potassium sorbate in ambient-stable beverages. The growing number of certified organic food producers in the Middle East and Africa (MEA) is encouraging consumer preferences for clean labels and natural additives. By increasing the availability of verifiable, pesticide-free fruits and vegetables, these producers are building trust in processed foods. For example, Nigeria has 706 certified organic food producers in 2024, representing 9% of Africa's total, according to the International Federation of Organic Agriculture Movement (IFOAM) [2]Source: International Federation of Organic Agriculture Movement (IFOAM), "Journal of Organic Agriculture Research and Innovation (JOARI)", ifoam.bio.

Demand for preservatives in RTE/RTC foods and beverages drives ingredient adoption

Ready-to-eat and ready-to-cook meal kits are becoming increasingly popular in urban areas across the UAE, Saudi Arabia, and South Africa, driven by the growth of dual-income households and a reduction in home cooking. To extend the refrigerated shelf life of these meal kits from 3-5 days to 7-10 days while maintaining clean-label claims, processors are turning to natural antimicrobials. Extracts from fruits and vegetables, such as cranberries, pomegranate, and beetroot, are particularly effective. These extracts, which are rich in organic acids and polyphenols, inhibit Listeria monocytogenes and Salmonella enterica at concentrations below sensory-detection thresholds. Currently, processors are incorporating these extracts into products like hummus, tzatziki, and marinated vegetables. This approach ensures microbial stability, meets food-safety audit requirements, and supports "no artificial preservatives" claims on packaging. Additionally, ready-to-eat product exporters targeting European Union markets are further motivated to adopt validated natural-preservative protocols. Higher expenditure on all food and beverage products supports the Middle East and Africa fruit and vegetable ingredients market by accelerating demand for preservatives in RTE/RTC foods and beverages, which in turn drives adoption of fruit- and vegetable-based preservative systems and related ingredients. Per capita expenditure on all food and beverage products in the United Arab Emirates was USD 16,442.7 in 2024, according to the Government of Canada [3]Source: Government of Canada, "Expenditure on all food and beverage products", canada.ca. As households allocate more budget to processed, packaged, and out‑of‑home consumption, manufacturers intensify use of preservation technologies to maintain safety, quality, and shelf life, increasing volumes of ingredient use per unit of demand.

Growth of plant-based and vegan foods

Plant-based meat and dairy alternatives are gaining popularity in the Middle East and Africa. In the UAE and South Africa, new product launches utilize fruits and vegetables to enhance color, texture, and nutritional value. For example, beetroot juice concentrate provides the red color for plant-based burger patties, while carrot fiber improves moisture retention and mouthfeel in vegan sausages. Saudi Arabia, as part of its Vision 2030 initiative, is promoting food security by encouraging alternative protein production. The Ministry of Environment, Water, and Agriculture supports this effort by offering subsidized land leases for vertical farms and processing facilities, aiming to reduce reliance on imported animal products. In 2024, Almarai, the largest dairy producer in the region, expanded its plant-based product line by introducing oat milk options with mango and strawberry purees. These products target flexitarian consumers seeking familiar flavors in non-dairy formats. The vegan food market is expected to grow at a faster rate than the overall ingredients market, as formulators increasingly recognize the functional advantages of fruit and vegetable derivatives, such as emulsification, water-binding, and color stability, over synthetic additives in clean-label formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent post-harvest losses in Sub-Saharan supply chains | -0.9% | Sub-Saharan Africa, particularly Nigeria, Kenya, Ethiopia | Long term (≥ 4 years) |

| Competition from synthetic substitutes | -0.6% | Egypt and Nigeria | Medium term (2-4 years) |

| Short shelf life and stability challenges | -0.7% | Sub-Saharan Africa, Egypt, with distribution constraints in Nigeria and Kenya | Medium term (2-4 years) |

| High import tariffs on specialty concentrates | -0.5% | Nigeria, Egypt, Kenya, with secondary impact on South Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent post-harvest losses in Sub-Saharan supply chains

Sub-Saharan Africa experiences significant losses in fruit and vegetable production between harvest and consumption, a problem less prevalent in developed markets. These losses weaken the economic feasibility of ingredient processing, forcing manufacturers to rely on concentrate imports from Europe and Asia. The cold-chain infrastructure in the region remains fragmented. In nations such as Nigeria, Kenya, and Ethiopia, only a small proportion of smallholder farmers have access to refrigerated transport within four hours of harvest. This delay results in enzymatic browning and microbial spoilage, rendering the produce unsuitable for premium ingredient applications. Although solar-powered cold-storage solutions, like Nigeria's ColdHubs network, are expanding, they still cover only a small portion of the national horticultural output. Consequently, a large share of crops, including mangoes, pineapples, and tomatoes, suffers quality degradation during the critical 24 to 48 hours between the farm gate and processing facilities. This deterioration reduces profit margins and limits reinvestment in advanced technologies, such as drying and encapsulation, which could enhance competitiveness against imported concentrates.

Competition from synthetic substitutes

Synthetic colorants, flavors, and preservatives continue to be more cost-effective than natural fruit and vegetable ingredients on a cost-per-function basis, exerting ongoing substitution pressure in price-sensitive segments such as carbonated soft drinks and hard-discount confectionery. In Egypt and Nigeria, formulators targeting mass-market channels focus on minimizing input costs rather than emphasizing clean-label claims, as consumers in these markets are less inclined to pay a premium for natural ingredients. Additionally, regulatory frameworks in several African jurisdictions allow synthetic additives that are restricted or banned in the European Union and Gulf Cooperation Council, reducing the compliance-driven motivation to switch to natural alternatives. By 2025, the cost gap is expected to grow further. Energy-intensive processes like freeze-drying and spray-drying are facing higher electricity tariffs, while synthetic-additive manufacturers benefit from economies of scale in procuring petrochemical feedstocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Vegetables Gain Ground on Functional Benefits

In 2025, fruits accounted for 58.45% of the ingredient market share, driven by apple, orange, and mango concentrates, which dominate beverage and bakery applications. However, the segment's maturity is limiting further growth as reformulation cycles slow and price competition increases. From 2026 to 2031, vegetables are expected to grow at a rate of 5.72%. Formulators have identified that derivatives from carrots, beetroot, and tomatoes provide color stability, nutritional density, and a clean-label advantage, benefits that fruit concentrates alone cannot offer. Carrots contribute beta-carotene, delivering a natural orange color to processed cheese and margarine. Beetroot extracts add red hues to plant-based meat alternatives and strawberry-flavored dairy products, meeting the demand for heat-stable pigments essential for retort and ultra-high-temperature processing. Tomato paste and puree enhance flavor while acting as natural preservatives in soups, sauces, and ready-to-eat meals. They utilize lycopene's antioxidant properties to extend shelf life without requiring synthetic additives.

Berries, such as strawberries, raspberries, and blueberries, are capturing premium niches within the fruit category. Their anthocyanin content provides purple and red hues for confectionery and dairy products. However, high import tariffs in Nigeria and Egypt create challenges, restricting their penetration mainly to Gulf Cooperation Council markets. Pineapple and mango concentrates are gaining traction in tropical juice blends and smoothie bases, particularly in South Africa, where local production reduces freight costs and shortens lead times. Banana puree is expanding in infant nutrition and bakery applications, valued for its natural sweetness and creamy texture, which minimizes the need for added fats. Kiwi remains a niche segment, constrained by limited cultivation in the Middle East and Africa and higher raw material costs compared to apple and pear. Zucchini, butternut, and pumpkin purees are emerging in plant-based dairy and bakery products. Their neutral flavors and moisture-retaining properties make them suitable for clean-label reformulations without altering sensory characteristics.

By Form: Powders Advance on Ambient Stability and Formulation Flexibility

In 2025, concentrates accounted for 32.88% of the form-based beverage market, highlighting their significant role in beverage formulation. While liquid formats integrate seamlessly into operations, the segment's reliance on refrigerated logistics restricts its adoption in regions with fragmented cold-chain infrastructures. Advancements in spray-drying and freeze-drying are driving powder formats to a forecasted growth rate of 5.68% from 2026 to 2031, the highest among all segments. Processors and formulators are increasingly opting for ambient-stable ingredients, which reduce cold-chain dependency and expand distribution capabilities. Powders, by eliminating refrigeration requirements, offer a shelf life of 12 to 18 months under ambient conditions. This not only reduces freight and warehousing costs, due to lower water content in spray-dried concentrates, but also enhances their market viability. Additionally, encapsulation technologies are improving powder functionality by protecting volatile aromatics and bioactive compounds from oxidation and enabling controlled-release applications in beverages and confections.

Pastes and purees serve a critical role in bakery, dairy, and ready-to-eat (RTE) applications, where viscosity and particulate suspension are essential for texture and mouthfeel. However, their refrigerated shelf life of 6 to 9 months limits their distribution reach in Sub-Saharan Africa. Pieces and slices are preferred in premium yogurt, ice cream, and bakery segments. In these applications, visible fruit or vegetable inclusions not only convey quality and authenticity but also command a price premium over puree-based alternatives. Not-from-concentrate juices and extracts, while delivering superior flavor intensity and clean-label appeal, particularly for premium beverages and cocktails in Gulf Cooperation Council hospitality channels, remain niche. Their adoption is constrained by a short shelf life of 3 to 6 months under refrigeration and higher logistics costs. The shift toward powders is most evident in Egypt and South Africa, where domestic processors are increasing investments in spray-drying capacities to support export markets and reduce reliance on imported concentrates.

By Application: Beverages Lead Growth on Sugar-Reduction Mandates

In 2025, beverages accounted for 29.46% of the application market and are expected to grow at a rate of 6.45% through 2031, the fastest among all segments. This growth is primarily fueled by sugar-reduction mandates from the Gulf Cooperation Council and reformulation initiatives by global bottlers aiming to avoid penalties linked to front-of-pack labeling. Fruit concentrates are replacing high-fructose corn syrup in carbonated soft drinks, juice blends, and sports beverages. At the same time, vegetable extracts, such as carrot and beetroot, are being used as natural colorants, meeting clean-label requirements without triggering synthetic-additive disclosures. Confectionery products, including gummies, hard candies, and chocolate fillings, are increasingly incorporating fruit purees and powders to replace artificial flavors and colors. This shift is driven by retailer mandates in the UAE and Saudi Arabia that emphasize natural ingredients for children's products. In bakery applications, fruit pastes and vegetable fibers are being utilized to improve moisture retention, extend shelf life, and enhance nutritional profiles, addressing the growing consumer demand for whole-grain and fiber-enriched breads, cakes, and biscuits.

Soups and sauces are adopting tomato paste, carrot puree, and pumpkin concentrates as flavor bases and natural thickeners, reducing reliance on modified starches and synthetic emulsifiers to align with clean-label strategies. Dairy products, such as yogurt, ice cream, and flavored milk, are incorporating fruit pieces, purees, and concentrates to provide visible inclusions and authentic flavor profiles, with strawberry, mango, and mixed-berry variants dominating SKU assortments in Middle Eastern and South African retail markets. Ready-to-eat (RTE) products, including meal kits, marinated vegetables, and ready-to-heat entrees, are leveraging fruit and vegetable extracts as natural preservatives. This approach has extended refrigerated shelf life from 3-5 days to 7-10 days, enabling broader distribution and reducing the risk of product recalls. Additionally, smaller but rapidly growing niches, such as infant nutrition, sports supplements, and pharmaceutical excipients, are utilizing fruit and vegetable ingredients to deliver functional benefits, including vitamin fortification, flavor masking, and bioavailability enhancement.

Geography Analysis

In 2025, the United Arab Emirates (UAE) strengthens its role as a key re-export and blending hub, holding a 27.61% market share. The Jebel Ali Free Zone serves as a central hub where ingredient distributors import concentrates from Europe, Asia, and South America. These concentrates are then blended to create custom formulations for beverage and dairy manufacturers across the Gulf Cooperation Council and East Africa. Dubai's advanced logistics infrastructure, including refrigerated warehousing, bonded zones, and efficient customs processes, ensures timely deliveries. This operational efficiency reduces working-capital requirements for regional food processors. Additionally, the UAE's "Plant the Emirates" initiative, which aims to plant 100 million trees by 2030, is increasing domestic production of dates and citrus fruits. However, due to water scarcity and limited arable land, the country will continue to depend on imports for specialty fruit and vegetable ingredients. South Africa, with a 6.05% market share, is expected to grow from 2026 to 2031, driven by investments in freeze-drying and spray-drying capacities. Citrus processors in the Western Cape are implementing energy-efficient systems that enhance the color and flavor retention of lemon, orange, and grapefruit powders, which are exported to European beverage formulators.

Saudi Arabia, through its Vision 2030 initiative, is advancing its food-security strategy by heavily investing in horticulture infrastructure. The Ministry of Environment, Water, and Agriculture is leading efforts by offering subsidized land leases for vertical farms and processing facilities to reduce reliance on imported animal products and fruit concentrates. In Egypt, the New Administrative Capital project encompasses 20,000 hectares of controlled-environment agriculture zones. These zones, designed to operate year-round and insulated from Nile Delta water constraints, are set to produce tomatoes, peppers, and leafy greens. This positions Egypt as a significant regional supplier of vegetable concentrates and pastes for soup, sauce, and ready-to-eat (RTE) applications. In Nigeria, a growing population and increasing urbanization are driving demand for RTE meals and beverages. However, significant post-harvest losses reduce processor margins and increase dependence on imported concentrates, limiting the country's ability to capture value-added processing revenues. Kenya and Ethiopia are establishing themselves as processors of citrus and tropical fruits, serving both regional and European export markets. Kenya's SM Fruit Processing and Ethiopia's Africa Juice Tropical are investing in cold-chain infrastructure and obtaining organic certifications, enabling access to premium European buyers. In Oman, Barka Fresh is expanding its date-paste production to meet the needs of the bakery and confectionery sectors within the Gulf Cooperation Council. Their proximity to demand centers in Saudi Arabia and the UAE allows them to offer shorter lead times compared to North African suppliers. However, regulatory frameworks across the region vary significantly. The UAE's Emirates Authority for Standardization and Metrology and Saudi Arabia's Food and Drug Authority enforce strict additive whitelists that favor natural ingredients. In contrast, Nigeria and Kenya allow synthetic colorants and preservatives, which are restricted in Gulf markets. This regulatory disparity creates challenges for multinational brands operating across multiple jurisdictions. For RTE exporters targeting the European Union market, compliance with the ISO 22000 food-safety management system is mandatory. This requirement incentivizes the adoption of validated natural-preservative protocols and traceability systems that document the journey of ingredients from farm gate to finished product.

Regulatory Landscape

Regulation of fruit and vegetable ingredients across MEA is shaped by tighter Gulf market controls on food additives, labeling, and import clearance, along with gradual harmonization in parts of Africa. In Saudi Arabia, the SFDA requires food product registration and compliance with GCC/GSO standards for additives and safety, which influences the selection of permitted colors, flavors, and preservative systems in beverage, dairy, and RTE formulations. In April 2025, SFDA updated its Conditions and Requirements for Food Clearance, explicitly flagging that pesticide residue-free certificates may be requested for frozen and processed vegetable products, raising the compliance bar for importers of concentrates, purees, and powders.

In the UAE, MOIAT anchors federal standardization and uses GSO technical regulations across product categories, alongside broader federal food safety requirements and controls on food contact materials. For exporters selling across multiple jurisdictions, regulatory disparity remains a constraint: Gulf markets operate stricter additive whitelists and documentation expectations, while several African markets allow a wider set of synthetic additives, complicating regional SKU alignment. On the regional side, COMESA and SADC frameworks guide SPS measures from primary production to distribution, while Codex Alimentarius texts via CCAFRICA continue to serve as reference points for countries strengthening risk-based food safety controls and analytical testing requirements.

Value Chain Analysis

The value chain starts with horticulture production (dates, citrus, tomatoes, mangoes, berries and other crops), followed by aggregation and pre-cooling, primary processing into purees/pastes and concentrates, secondary processing into powders and encapsulated systems, and then blending, packaging, and distribution to beverage, dairy, bakery, confectionery, soups and sauces, and RTE manufacturers. The UAE functions as a regional re-export and blending node, leveraging free-zone logistics and consolidated inventories to supply short lead-time contracts across the Gulf and into East/West Africa, while Egypt and South Africa act as processing anchors for tomato/citrus and fruit-based ingredients. Large exporters and ingredient houses source specialty concentrates globally, but regional processors gain share by locating near crop belts and optimizing lead times and freight costs.

Key bottlenecks remain post-harvest losses and limited cold-chain access in parts of Sub-Saharan Africa, plus exposure to logistics disruptions on major shipping lanes that affect input costs for energy-intensive drying and imported concentrates. In response, value chain participants are investing in localized processing and partnerships that tighten sourcing-to-delivery loops. Examples include MAFI for Agricultural Produce Industries operating a 157,000 sqm agri-food complex in Sadat City, Egypt, focused on citrus, tomato, and broader fruit/vegetable concentrates for B2B export, and June 2026 distribution expansion where Solevo Group became an authorized partner for IFF in West and Central Africa, supporting localized inventory and last-mile logistics for manufacturers that depend on consistent ingredient availability.

Competitive Landscape

The Middle East and Africa fruits and vegetables ingredients market is moderately consolidated, with multinational ingredient houses such as Archer Daniels Midland Company, Döhler Group, and Olam International leading the market. These companies establish formulation partnerships with top-tier beverage and dairy brands. Their technical-service teams collaborate to co-develop custom blends and provide application support, particularly for clean-label reformulations. By leveraging global procurement networks, these companies source specialty concentrates, such as berry, tropical fruit, and exotic vegetables, that regional processors cannot supply at scale. They also employ advanced technologies like encapsulation and freeze-drying to preserve volatile aromatics and bioactive compounds during thermal processing. Meanwhile, regional players like Dohler-Massara Egypt, Africa Juice Tropical Ethiopia, and SM Fruit Processing Kenya are gaining market share by strategically locating near citrus and tropical fruit belts. This approach enables them to offer shorter lead times and lower freight costs, appealing to mid-tier food manufacturers focused on supply-chain resilience over ingredient novelty.

Opportunities exist in vegetable-based natural preservatives for ready-to-eat meals, where beetroot and carrot extracts can extend shelf life without raising clean-label concerns. Additionally, powder formats for plant-based dairy alternatives present potential, as they require dispersibility and neutral flavor profiles. Major players in this market include Döhler Group, Archer Daniels Midland Company, AGRANA Beteiligungs AG, Kanegrade Ltd., and SunOpta Inc. These companies are adopting strategies such as new product launches, partnerships, expansions, and acquisitions to strengthen their market presence.

Encapsulation technology is being utilized to protect anthocyanins and carotenoids from oxidation, while freeze-drying techniques are preserving volatile aromatics in premium juice blends. Döhler and Sensient Technologies have patented multi-layer encapsulation systems designed to release flavor compounds at specific pH or temperature thresholds. Almarai's entry into the plant-based dairy sector in 2024, incorporating mango and strawberry purees for unique flavor differentiation, highlights a growing trend. Regional dairy players are diversifying into alternative proteins and seeking ingredient partners who can deliver functional benefits, such as emulsification, water-binding, and color stability, that clean-label formulations require and synthetic additives often cannot provide. Emerging disruptors like Nigeria's solar-powered ColdHubs are transforming the market by reducing post-harvest losses and enabling smallholder farmers to supply ingredient-grade produce to regional processors. Competitive intensity is expected to rise as South African citrus processors expand freeze-drying capacity and Egyptian vegetable processors scale up tomato paste and puree production, narrowing the cost and quality gap with European and Asian suppliers.

Middle East And Africa Fruit And Vegetable Ingredients Industry Leaders

-

Dohler Group

-

AGRANA Beteiligungs AG

-

Kanegrade Ltd.

-

SunOpta Inc.

-

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An immediate opportunity sits in scaling local concentrate and puree capacity in North and West Africa to reduce dependence on imported inputs and shorten lead times for beverage, dairy, and RTE manufacturers executing clean-label reformulations. Cairo 3A for Agriculture opened the third phase of its Qutoof citrus factory (EGP 1.3 billion), increasing the availability of citrus concentrates, oils, and purees for both domestic and export-oriented customers. Similar capacity build-outs strengthen the case for localized sourcing programs and contract processing models that connect growers to ingredient-grade outlets while improving traceability and documentation for cross-border trade.

A second whitespace is the shift toward ambient-stable formats and integrated ingredient systems that help processors manage cold-chain constraints and comply with additive and sugar-related labeling rules. New downstream manufacturing assets increase pull-through for fruit and vegetable ingredients used in baby food, beverages, and prepared foods, with February 2026 construction started by Barakat Group on an AED 150 million baby food facility in KEZAD, which typically requires reliable supplies of fruit/vegetable purees and concentrates with controlled specifications. In parallel, powder formats and encapsulation platforms that protect color and aroma during processing are being adopted where distribution distances are long or refrigeration is costly, creating room for regional toll-drying, co-development services, and application support tied to beverage sugar-reduction and clean-label color replacement programs in Gulf markets.

Recent Industry Developments

- June 2026: Solico Group launched an AED 130 million SoFood production facility in Jebel Ali Free Zone (Jafza), Dubai. The new facility expands regional processing capacity for sauces and ambient-stable products, strengthening the supply of fruit and vegetable ingredients across the GCC and neighboring markets.

- June 2025: Sensient Flavors and Extracts expanded its MEA portfolio with BioSymphony natural flavors designed for broad food and beverage applications, aligning with clean-label trends and providing integrated flavor systems to MEA manufacturers.

- March 2024: Tiger Brands announced a USD 24 million expansion at its Langeberg Valley facility in South Africa, upgrading fruit puree, concentrate, and powder processing to improve local supply and reduce imports.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of fruit and vegetable ingredients sold for use in food and beverage formulations across the Middle East and Africa. It includes commonly traded forms such as concentrates, purees, pieces, and powders that are used to add flavor, color, texture, or nutrition.

Scope exclusions: Excludes fresh whole produce sold for direct consumption and any retail, foodservice, or distribution markups applied after ingredient-level sales.

Segmentation Overview

-

Ingredient Type

-

Fruits

- Apple

- Orange

- Pineapple

- Mango

- Banana

- Kiwi

-

Berries

- Strawberries

- Raspberries

- Blueberries

- Other Berries

- Other Fruits

-

Vegetables

- Carrots

- Beetroots

- Tomato

- Zucchinis

- Butternuts

- Pumpkins

- Other Vegetables

-

Fruits

-

Form

- Concentrates

- Pastes and Purees

- Pieces and Slices

- Powders

- Others (NFC Juices, extracts)

-

Application

- Beverages

- Confectionary Products

- Bakery Products

- Soups and Sauces

- Dairy Products

- RTE Products

- Others

-

By Country

- United Arab Emirates

- Saudi Arabia

- South Africa

- Egypt

- Nigeria

- Rest of Middle East and Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the ingredient supply chain and the main demand pools across the Middle East and Africa, because imported concentrates and locally processed outputs can behave very differently in pricing and availability. For grounding, we refer to public sources such as FAOSTAT for crop and processing context, UN Comtrade for trade flows of key processed fruit and vegetable lines, and national statistical offices that publish food manufacturing and price series.

We also use materials like company annual reports and investor presentations, relevant customs and food control authority updates, and association websites that track processing and packaging developments. When needed, paid subscriptions are used for cross-checking company financials and for shipment-level import and export patterns so outliers can be questioned early. The sources named above are illustrative rather than exhaustive, and many other public references are used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work is used to confirm what ingredient means in day-to-day buying, how pricing is contracted (spot versus annual), and where volumes are actually consumed across beverages, bakery, dairy, soups and sauces, and ready-to-eat items. We speak with manufacturers, processors, importers, distributors, and large buyers, and then we validate assumptions across core MEA trade corridors and local production hubs so the final model reflects on-the-ground realities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 18% | |

| Mid tier: 56% | Functional/Unit leaders: 37% | |

| Smaller Players: 18% | Managers: 45% |

Market-Sizing & Forecasting

The core sizing is built using a top-down approach where production and trade signals are used to reconstruct the regional ingredient demand pool, and then it is split using application mix patterns that were validated through interviews. To keep the estimate practical, the model is checked using selective bottom-up approximations, such as sampled price per ton ranges for concentrates and powders multiplied by inferred volumes in key channels, followed by adjustments when the two views do not line up.

A few inputs that matter a lot for this market include import dependence for processed fruit and vegetable inputs, share of beverages and dairy in packaged food demand, changes in cold chain and storage capacity, local crop seasonality and post-harvest loss levels, and average selling price movement linked to freight rates and currency shifts. Forecasting is done using scenario analysis supported by trend lines on these variables, and then the scenarios are narrowed based on what industry respondents expect for reformulation demand and capacity additions. Where coverage gaps exist in smaller countries, we extrapolate using per capita packaged food consumption and trade intensity proxies, and we flag the assumptions for further review.

Data Validation & Update Cycle

Validation is done by comparing the model outputs against independent signals, like trade totals, processed food output indicators, and pricing direction seen in contracts and public price series, before the numbers move to final review. Variance checks are run at country and form levels so sudden jumps in volume or value are explained by a visible driver and not by a spreadsheet artifact.

The work goes through multi-step analyst review, and callbacks are triggered when we see mismatches between modeled ASPs and what buyers report as current purchase ranges. Reports are refreshed annually, and interim updates are made when material events occur, such as major currency moves, tariff changes, or supply disruptions affecting concentrates and powders. Before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Middle East and Africa Fruit and Vegetable Ingredient Market Size Versus Other Published Estimates

Different published market sizes for MEA fruit and vegetable ingredients can look far apart, even when they use similar words, because the scope boundary and the pricing basis often shift quietly. Differences also show up when one study anchors to a different base year, uses a distinct currency conversion timing, or assumes a faster ingredient ASP climb than what buyers are actually seeing.

A refresh-led gap is common in this category since freight rates, FX movements, and concentrate pricing can change the value number without a similar change in tons. By aligning currency timing to the base year, rechecking current ASP ranges for key forms like concentrates and powders, and rerunning consistency checks against trade patterns before each refresh, Mordor Intelligence helps keep the value line tied to what is actually traded and purchased across MEA.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.48 B (2025) | |

| Regional Consultancy A | USD 14.26 B (2024) | Uses an earlier base year, which can understate value when recent FX and freight-linked cost pass-through has lifted ingredient ASPs, and the scope language is less clear on whether all ingredient forms are consistently captured. |

| Industry Publisher B | USD 1.50 B (2024) | The figure likely applies a narrower product scope or pricing level, which can exclude high-volume categories like concentrates and purees, and it appears to represent only a subset of MEA demand rather than the full regional ingredient market. |

Taken together, the spread is mainly explained by timing and scope differences more than by true demand disagreement. When the inputs are tied to observable trade and consumption signals, and the pricing logic is kept consistent across forms and countries, the final size becomes easier to trace and repeat as conditions change.

Key Questions Answered in the Report

What is the current value of the Middle East and Africa fruits and vegetables ingredients market?

The market stands at USD 16.34 billion in 2026 and is on course for USD 21.4 billion by 2031.

Which application is growing fastest?

Beverage formulations post the highest 6.45% CAGR thanks to sugar-reduction mandates and clean-label trends.

Why are vegetable ingredients gaining share over fruit?

Carrot, beetroot, and tomato derivatives offer heat-stable colors, antioxidants, and preservative traits that appeal to clean-label reformulations.

How do powders benefit processors?

Spray- and freeze-dried powders cut cold-chain costs, extend shelf life to 18 months, and improve formulation flexibility across bakery, beverage, and RTE foods.

Page last updated on: