Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

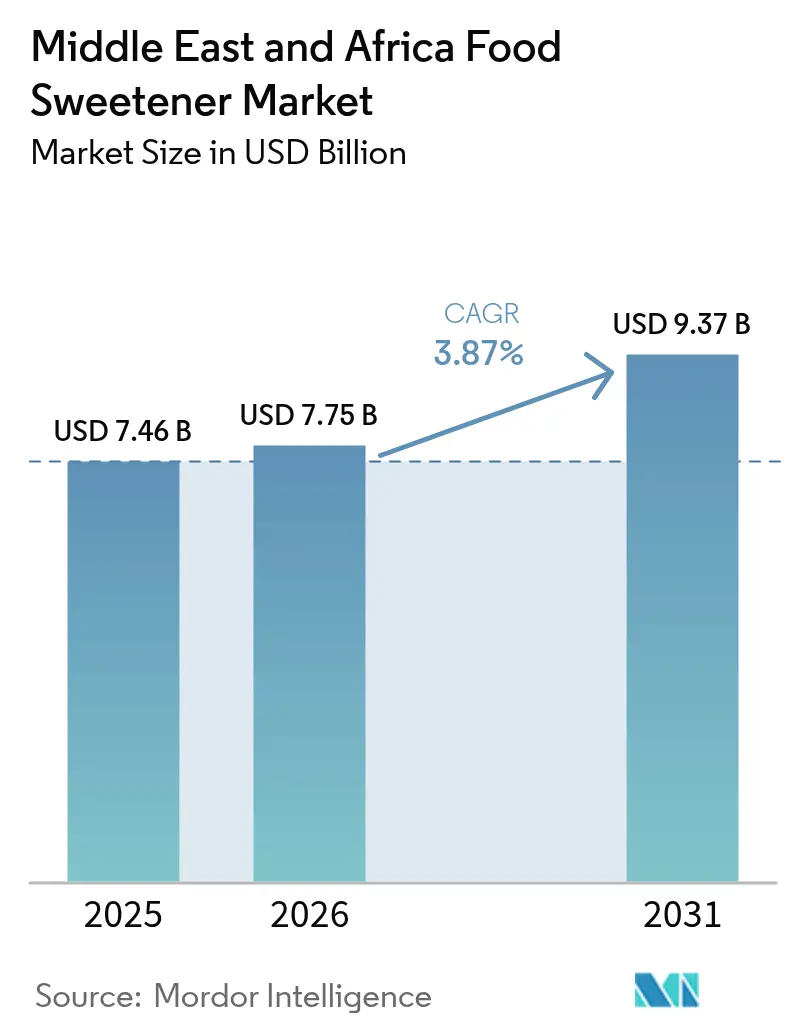

| Base Year Market Size (2025) | USD 7.46 Billion |

| Market Size (2026) | USD 7.75 Billion |

| Market Size (2031) | USD 9.37 Billion |

| Growth Rate (2026 - 2031) | 3.87% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Food Sweetener Market Analysis by Mordor Intelligence

The Middle East and Africa food sweetener market size was valued at USD 7.46 billion in 2025 and estimated to grow from USD 7.75 billion in 2026 to reach USD 9.37 billion by 2031, at a CAGR of 3.87% during the forecast period (2026-2031). While the overall market growth appears stable, the underlying dynamics reveal significant portfolio shifts. Beverage and processed-food manufacturers are actively reformulating their products to reduce sugar content in preparation for the implementation of a four-tier sugar tax in the GCC, scheduled to commence in 2026. The rising prevalence of diabetes, particularly in Saudi Arabia and the UAE, has elevated product reformulation from a marketing-driven initiative to a critical public health requirement. In urban areas, heightened scrutiny of product labels is driving a growing preference for high-intensity sweeteners derived from plant-based and fermentation processes. These sweeteners not only help manufacturers avoid tax penalties but also ensure taste consistency, meeting consumer expectations. Additionally, advancements in enzymatic technologies are enabling the production of rare sugars such as allulose and tagatose. These sugars serve as bulk alternatives that replicate the functional properties of sucrose while offering minimal caloric content, providing formulators with innovative solutions. As a result, the competitive landscape is undergoing a transformation. The focus is shifting beyond mere cost efficiency to include factors such as sensory performance, adaptability to regulatory changes, and clean-label positioning. These evolving priorities are reshaping procurement strategies across the value chain, influencing how companies approach product development and market positioning.

Key Report Takeaways

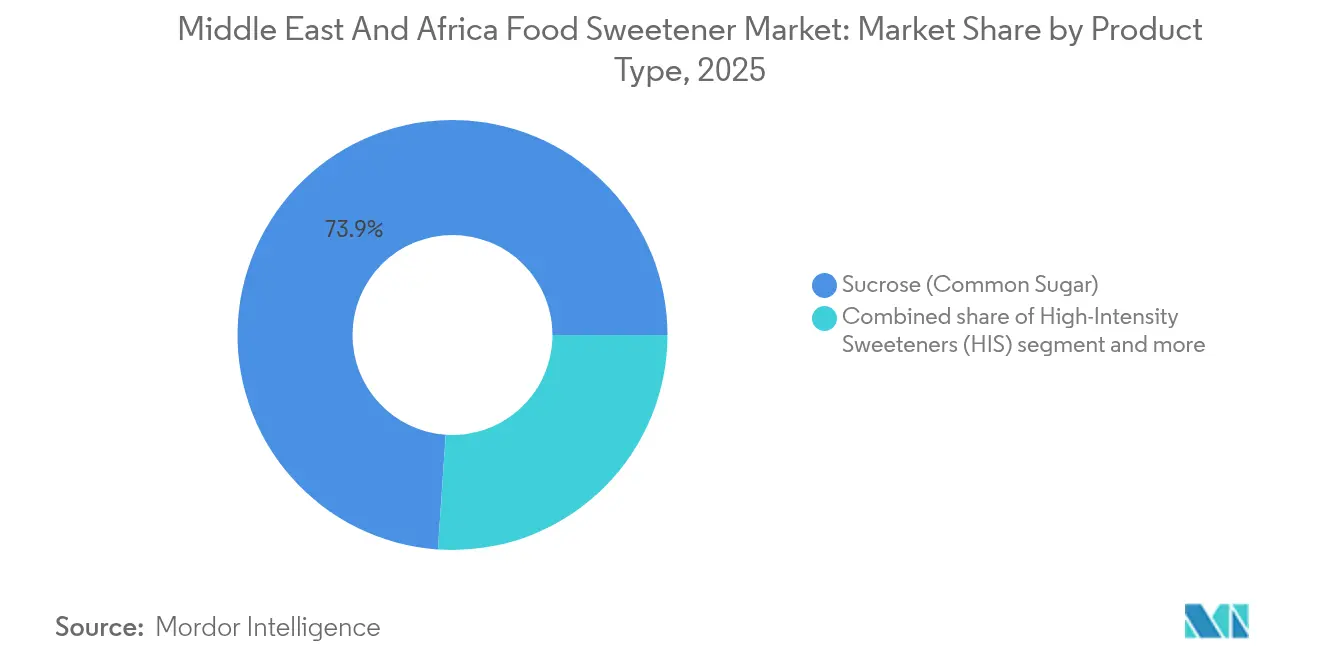

- By product type, sucrose retained 73.92% of the Middle East and Africa food sweetener market share in 2025, while high-intensity sweeteners are forecast to expand at a 4.06% CAGR through 2031.

- By source, artificial variants captured 75.40% of 2025 revenue, but plant-based alternatives are rising at a 4.23% CAGR to 2031.

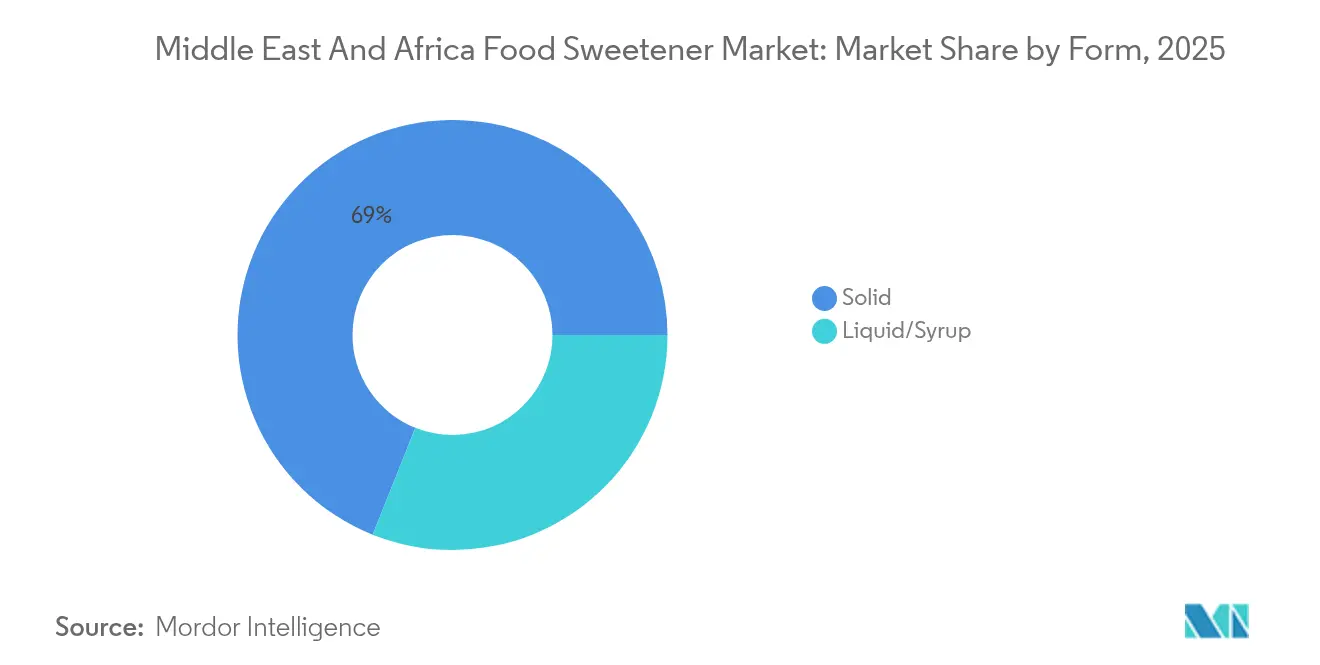

- By form, solid products led with 68.95% share in 2025; liquid and syrup formats are set to grow 4.83% annually on the back of beverage-sector demand.

- By application, food products commanded 58.10% of 2025 demand, yet beverages are accelerating at a 4.66% CAGR, powered by soft-drink reformulation and ready-to-drink tea launches.

- By geography, Saudi Arabia held 35.55% revenue share in 2025; the United Arab Emirates is the fastest-growing market at a 4.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Food Sweetener Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diabetes-led reformulation wave in Gulf Cooperation Council | +0.8% | Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman | Medium term (2-4 years) |

| Growing health awareness and label scrutiny | +0.6% | UAE, Saudi Arabia, South Africa urban centers | Long term (≥4 years) |

| Shift toward natural and clean-label ingredients | +0.7% | UAE, Saudi Arabia, Egypt metropolitan areas | Medium term (2-4 years) |

| Expansion of processed food and beverage categories | +0.5% | Saudi Arabia, Egypt, South Africa, Nigeria | Long term (≥4 years) |

| Breakthrough in enzymatic production of rare sugars (allulose, tagatose) | +0.4% | UAE and Saudi Arabia premium segments | Long term (≥4 years) |

| Localization incentives for starch-based sweetener plants | +0.3% | UAE, Saudi Arabia, Egypt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Diabetes-led reformulation wave in gulf cooperation council

In 2024, Saudi Arabia and the United Arab Emirates reported adult diabetes prevalence rates of 23.1% and 20.7%, respectively, highlighted by the International Diabetes Federation [1]Source: International Diabetes Federation, "Diabetes in the United Arab Emirates (2024 )", idf.org. These figures emphasize the critical need for sweetener reformulation in the Gulf Cooperation Council (GCC), transforming it from a marketing strategy into a public health priority. Unlike general health trends, the rapid pace of regulatory measures is accelerating reformulation timelines. The GCC's four-tier sugar tax, set to be implemented in 2026, imposes increasing levies based on sugar content per 100 milliliters. This framework encourages manufacturers to develop products with less than 5 grams of sugar per serving. High-intensity sweeteners like sucralose and stevia, which provide equivalent sweetness in minimal quantities, are preferred over sugar alcohols that require larger amounts. In response, beverage companies in the region have expedited reformulation efforts. For instance, PepsiCo has reduced sugar levels in its Pepsi variant across select GCC markets, using a blend of acesulfame-K and sucralose to maintain flavor. This reformulation trend extends beyond carbonated beverages to dairy desserts and baked goods, where manufacturers are leveraging allulose for its ability to replicate sugar's browning and moisture-retention properties without adding calories.

Shift toward natural and clean-label ingredients

In urban markets across the Middle East and Africa, consumer distrust of artificial sweeteners is on the rise. This skepticism is driven by health concerns amplified through social media and a growing clean-label movement that emphasizes ingredient transparency. To address this, manufacturers are adapting their product development strategies by turning to natural alternatives such as stevia, monk fruit, and erythritol. These options appeal to label-conscious consumers who are willing to pay more for products they perceive as natural. Reflecting this shift, food producers are increasingly focusing on organic production. For instance, Nigeria had 706 certified organic food producers in 2024, representing 9% of Africa's total, according to the International Federation of Organic Agriculture Movement (IFOAM) [2]Source: International Federation of Organic Agriculture Movement (IFOAM), "Journal of Organic Agriculture research and Innovation", ifoam.bio. However, challenges remain: stevia extracts, particularly Reb A, often leave a metallic or licorice-like aftertaste, which limits their use in certain applications. Precision fermentation technologies are helping overcome this issue by producing advanced stevia glycosides like Reb M and Reb D, which offer improved taste profiles and are gaining popularity in premium beverages. The clean-label trend is also boosting demand for sugar alcohols like erythritol, which provides 70% of sucrose's sweetness with minimal glycemic impact. However, its cooling effect restricts its application in warm products like baked goods.

Breakthrough in enzymatic production of rare sugars (allulose, tagatose)

Advancements in enzymatic conversion technologies have enabled the commercial production of rare sugars, which were previously restricted to niche applications due to high production costs. Allulose, created by converting fructose with D-psicose 3-epimerase enzymes, replicates the sweetness of sucrose with just 0.4 calories per gram. Additionally, it mirrors table sugar's functional properties, including browning, moisture retention, and freezing-point depression. These attributes make allulose a suitable direct replacement in bakery and confectionery products, particularly where sugar alcohols are inadequate, such as in items requiring Maillard reactions for color and flavor. Tagatose, another rare sugar, is produced from lactose through enzymatic isomerization. It offers similar advantages to allulose while also providing prebiotic properties, appealing to consumers focused on gut health. However, regulatory approval remains inconsistent: allulose is classified as Generally Recognized as Safe in the United States but lacks explicit approval in several Middle Eastern and African regions, creating challenges for manufacturers aiming for regional expansion. Production is primarily dominated by Japanese and South Korean biotechnology firms, with limited localized manufacturing in the Middle East and Africa. Nevertheless, licensing agreements are increasing as demand grows in premium market segments.

Expansion of processed food and beverage categories

Urbanization and increasing disposable incomes in Egypt, Nigeria, and South Africa are boosting the consumption of packaged foods and beverages. These categories inherently drive sweetener demand due to their formulation requirements. For instance, Nigeria's National Bureau of Statistics reported a 12.91% increase in National Disposable Income in Q1 and a 17.44% rise in Q2 of 2024 [3Source: National Bureau of Statistics, "Nigerian Gross Domestic Product Report - Microdata", microdata.nigerianstat.gov.ng]. Egypt's processed food sector is growing as modern retail gains traction and working households prioritize convenience, creating opportunities for sweetener suppliers in dairy desserts, sauces, and ready-to-eat meals. Although Nigeria's beverage market faces challenges such as infrastructure issues and regulatory approval delays, it presents a volume opportunity fueled by the growing consumption of carbonated soft drinks among urban youth. In South Africa's mature retail environment, premiumization trends are evident, with manufacturers differentiating their products through functional claims, such as reduced sugar, added fiber, and fortification, which require advanced sweetener blends to balance taste and nutrition. However, this growth is not uniform. Rural markets, being price-sensitive, prefer traditional sucrose-sweetened products, while urban centers are more willing to pay for reformulated offerings. This geographic segmentation is driving multinational brands to implement tiered product strategies, offering standard formulations in mass markets and premium, reduced-sugar variants in metropolitan areas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety perceptions and skepticism toward artificial sweeteners | -0.5% | GCC urban centers and South Africa | Short term (≤2 years) |

| Regulatory complexity and compliance burden | -0.4% | Egypt, Nigeria, Rest of Middle East and Africa | Medium term (2-4 years) |

| Sensory and formulation challenges | -0.3% | Middle East and Africa | Long term (≥4 years) |

| Patent cliffs squeezing royalty-based innovators | -0.2% | Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Safety perceptions and skepticism toward artificial sweeteners

Consumers continue to exhibit skepticism toward synthetic sweeteners, despite decades of regulatory approvals. This hesitation creates challenges for the adoption of aspartame, saccharin, and acesulfame-K, particularly among health-conscious demographics. The World Health Organization's 2023 recommendation against using non-sugar sweeteners for weight control, due to inconclusive evidence regarding their long-term metabolic benefits, has heightened this skepticism. Advocacy groups questioning the safety of artificial ingredients have further fueled these concerns. This perception gap is especially significant in Gulf Cooperation Council markets, where affluent consumers avoid products containing synthetic additives and are willing to pay a premium for plant-based alternatives. Manufacturers face a strategic challenge: while artificial sweeteners are cost-effective and well-established from a regulatory perspective, their inclusion on ingredient labels can deter label-conscious buyers. To address this, some brands are introducing hybrid formulations that combine small amounts of artificial sweeteners with stevia or monk fruit. This approach allows them to claim "naturally sweetened" products while managing production costs. Additionally, trust in regulatory bodies remains a critical factor. Surveys indicate that consumers in the Middle East and Africa have less confidence in government food safety agencies compared to those in Europe or North America, complicating efforts to educate these markets on the safety of approved sweeteners.

Regulatory complexity and compliance burden

Manufacturers pursuing regional distribution in the Middle East and Africa face considerable time and cost challenges due to the absence of unified sweetener regulations. The Gulf Standards Organization provides standardized technical regulations for its member states, specifying acceptable daily intake limits and labeling requirements for approved sweeteners. However, countries like Egypt, Nigeria, and South Africa implement distinct approval processes. In Egypt, the Organization for Standardization requires domestic testing, which can extend approval timelines to as long as 24 months. In Nigeria, the National Agency for Food and Drug Administration and Control struggles with resource limitations, causing delays in application reviews. This regulatory fragmentation forces multinational ingredient suppliers to prepare separate regulatory dossiers and reformulate products to comply with country-specific limits, reducing their economies of scale. Smaller regional players, lacking the resources to manage these diverse compliance requirements, face restricted geographic expansion, which strengthens the competitive position of established global conglomerates. Additionally, this fragmented regulatory environment creates arbitrage risks, where products approved in one jurisdiction may encounter import restrictions in neighboring markets. These challenges complicate supply chain planning and inventory management for food and beverage manufacturers operating across multiple countries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: High-Intensity Sweeteners Challenge Sucrose Dominance

In 2025, sucrose accounted for 73.92% of the market share, highlighting its entrenched role in traditional applications. Its functional properties, such as bulk, texture, browning, and moisture retention, remain difficult to replicate with alternative sweeteners. High-intensity sweeteners are projected to grow at an annual rate of 4.06% from 2026 to 2031, driven by beverage reformulation mandates and the increasing availability of zero-calorie product lines targeting diabetic and weight-conscious consumers. Within the high-intensity sweetener category, sucralose and stevia are gaining traction as manufacturers prioritize cost efficiency and clean-label positioning. In contrast, aspartame, despite regulatory approval in most Middle Eastern and African markets, faces challenges due to safety concerns. Starch sweeteners and sugar alcohols occupy a middle ground, with erythritol and xylitol gaining popularity in confectionery applications where their cooling effects are less problematic. High-fructose corn syrup continues to hold its position in cost-sensitive processed food categories. These segment dynamics reveal a strategic challenge: while sucrose's functional versatility ensures its indispensability in bakery and dairy applications, regulatory pressures and evolving consumer preferences are gradually reducing its share in beverages and reformulated snacks.

The "Others" category, which includes rare sugars like allulose and tagatose, remains small in scale but represents a hub of innovation. Advances in enzymatic production are enabling these sugars to achieve functional equivalence with sucrose while offering reduced caloric content. Neotame and cyclamate occupy niche roles. Neotame's extreme potency limits its use to applications requiring minimal dosages, while cyclamate, banned in the United States but approved in many African and Middle Eastern countries, offers a cost-effective option for manufacturers. Saccharin, once a dominant player, has experienced a decline in market share as newer sweeteners with improved taste profiles gain popularity. However, it continues to be used in pharmaceutical products and low-cost beverages. This segmentation of product types reflects a broader industry shift: the transition from single-sweetener formulations to blends that optimize synergistic sweetness effects and mask individual off-notes. This trend is particularly evident in carbonated soft drinks and ready-to-drink tea products, where achieving a complex taste profile is essential.

By Source: Plant-Based Alternatives Gain Ground Amid Artificial Dominance

Artificial sources accounted for 75.40% of the market share in 2025, a dominance attributed to decades of regulatory familiarity, cost efficiency, and established supply chains for aspartame, saccharin, and acesulfame-K. Meanwhile, plant-based alternatives are expected to grow at an annual rate of 4.23% through 2031. This growth is fueled by increasing clean-label consumer preferences and manufacturers' efforts to position premium product lines with natural ingredients. Stevia, derived from the leaves of Stevia rebaudiana, leads the plant-based segment. Advances in precision fermentation technologies now enable the production of high-purity glycosides like Reb M, which eliminate the metallic aftertaste associated with earlier extracts. While monk fruit extract is popular in North America, its penetration into price-sensitive markets in the Middle East and Africa is limited by supply chain challenges and higher costs. The plant-based category also includes sugar alcohols derived from natural sources, such as erythritol from fermented glucose and xylitol from birch or corn. However, consumer perceptions of these ingredients as "natural" vary, complicating marketing efforts.

Fermentation and bio-engineered sources represent the fastest-growing segment, utilizing microbial platforms to produce sweeteners through innovative metabolic pathways that bypass traditional extraction or synthesis methods. This segment includes precision-fermented stevia glycosides, bio-engineered thaumatin, and rare sugars developed through enzymatic conversions. These advancements position the segment at the intersection of natural positioning and biotechnology innovation. Regulatory acceptance of fermentation-derived sweeteners is progressing, with the Gulf Standards Organization and Egyptian authorities classifying these ingredients as natural or nature-identical. However, labeling requirements remain under development. The current source segmentation highlights a critical turning point: while artificial sweeteners maintain cost and performance advantages, the rapid growth of plant-based and fermentation-derived options indicates a potential long-term shift in formulator preferences. As production scales up, narrowing price gaps and improving sensory profiles could further accelerate this transition.

By Form: Liquid and Syrup Formats Accelerate in Beverage Applications

Between 2026 and 2031, beverage manufacturers are expected to drive a 4.83% annual growth by increasingly favoring liquid and syrup sweetener formats. This growth surpasses the solid form, which accounted for a 68.95% market share in 2025. Liquid formats offer significant operational benefits, including ease of blending, consistent dispersion, and reduced processing time. These advantages are essential in high-volume beverage production, where precise formulation ensures consistent taste across batches. High-intensity sweeteners are now predominantly available as liquid concentrates or syrups, enabling accurate dosing and minimizing issues like clumping or uneven distribution, which are common with powdered forms. This trend is particularly prominent in the ready-to-drink tea and coffee segments, where manufacturers combine liquid stevia extracts with erythritol syrups to achieve desired sweetness levels while maintaining clean-label standards. Conversely, solid forms remain dominant in bakery and confectionery applications, where the flowability of powders and compatibility with existing equipment make crystalline or granular sweeteners the preferred option.

Form segmentation in sweeteners also underscores supply chain challenges. Liquid sweeteners, which require cold-chain logistics and have shorter shelf lives, face distribution obstacles in regions with limited infrastructure, such as Nigeria and parts of Egypt. Consequently, manufacturers catering to these markets often choose solid formats, which can be stored at ambient temperatures and simplify inventory management. In the confectionery sector, syrup forms of sugar alcohols, particularly sorbitol and maltitol, are gaining popularity due to their humectant properties, which help retain moisture and extend product shelf life. The competitive dynamics within sweetener formats favor suppliers with expertise in both liquid and solid forms. This flexibility allows them to meet diverse customer requirements and capture market share in both beverage and food sectors as formulation needs continue to evolve.

By Application: Beverages Outpace Food Amid Reformulation Pressures

Food applications constituted 58.10% of sweetener demand in 2025, encompassing bakery and confectionery, dairy and desserts, meat and savory products, nutraceuticals, and sauces. Meanwhile, the beverage sector is growing at an annual rate of 4.66% through 2031, driven by sugar tax regulations and the increasing popularity of zero-calorie products. Soft drinks lead the beverage segment, with manufacturers combining sweeteners, commonly sucralose or aspartame with acesulfame-K, to create taste profiles similar to full-sugar versions while complying with regulatory standards. The ready-to-drink tea and coffee categories are also expanding rapidly, as formulators use stevia and monk fruit to offset bitterness without adding calories. This technical challenge has historically hindered the acceptance of unsweetened products.

In food applications, bakery and confectionery face the most significant reformulation challenges. Sugar's structural roles, such as bulk, texture, and browning, are difficult to replicate with high-intensity sweeteners. Manufacturers are exploring allulose and tagatose, which closely mimic sucrose's functionality, though their higher costs limit their use to premium product lines. The dairy and dessert sectors represent a middle ground, where sugar alcohols like erythritol and maltitol can partially replace sucrose without compromising texture. However, their cooling effects require precise formulation. Nutraceuticals and functional foods, a high-growth niche, use sweeteners to improve the taste of protein powders and meal replacements while supporting health claims like low glycemic index or diabetic-friendly positioning. In sauces, dressings, and spreads, sweeteners are primarily used to balance flavor. Sucralose and stevia are gaining market share as manufacturers work to reduce added sugar content in response to stricter labeling regulations. This segmentation highlights a critical distinction: beverages can reformulate relatively easily with high-intensity sweeteners, whereas food applications require more complex solutions to balance taste, texture, and cost.

Geography Analysis

In 2025, Saudi Arabia captured 35.55% of the regional market share, driven by its strong processed food manufacturing sector, high per-capita beverage consumption, and government initiatives to localize food ingredient production under the Vision 2030 economic diversification plan. The United Arab Emirates is projected to grow at an annual rate of 4.94% from 2026 to 2031, the fastest in the region. This growth is attributed to its role as a re-export hub, early adoption of clean-label trends among its diverse expatriate population, and regulatory alignment with Gulf Standards Organization protocols, which streamline product approvals. Dubai's strategic position as a logistics hub enables ingredient suppliers to efficiently serve Middle Eastern and African markets through centralized distribution centers, reducing lead times and inventory costs. Qatar, Kuwait, Bahrain, and Oman, grouped under the "Rest of Middle East and Africa" category, exhibit similar consumption patterns to Saudi Arabia and the UAE but on a smaller scale. Government-led sugar reduction initiatives and excise taxes in these countries create comparable reformulation pressures.

Egypt represents a volume-driven market where price sensitivity limits the penetration of premium sweeteners. The Egyptian Organization for Standardization's approval processes, which can take up to 24 months, create barriers for new sweetener entrants, favoring established suppliers with existing regulatory dossiers. In South Africa, the Health Promotion Levy, a sugar tax applied to beverages containing more than 4 grams of sugar per 100 milliliters, has driven reformulation efforts toward high-intensity sweeteners and sugar alcohols. The country's mature retail environment and relatively high consumer awareness support premiumization trends, with manufacturers differentiating their products through functional claims and natural ingredient positioning.

Despite being Africa's most populous nation, Nigeria faces significant challenges. Regulatory approval delays from the National Agency for Food and Drug Administration and Control, infrastructure gaps that hinder cold-chain distribution of liquid sweeteners, and economic volatility limit consumer purchasing power for premium reformulated products. The geographic segmentation highlights a bifurcated market. Gulf Cooperation Council countries demonstrate regulatory sophistication and a consumer base willing to pay for health-oriented reformulations. In contrast, African markets offer substantial volume potential but are constrained by infrastructure and regulatory challenges, favoring cost-efficient, shelf-stable sweetener formats.

Competitive Landscape

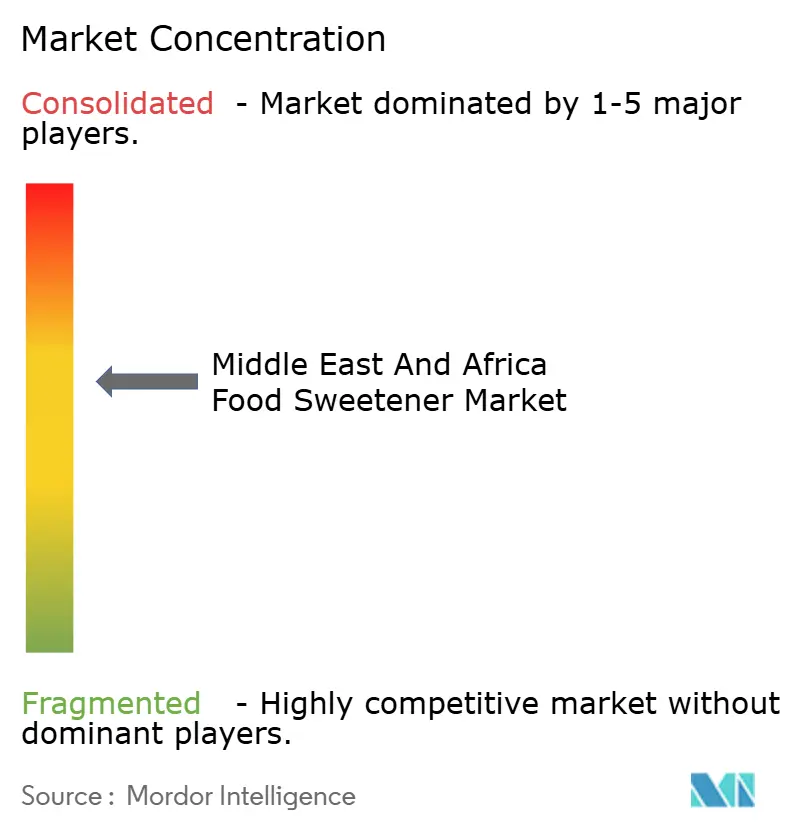

The Middle East and Africa food sweetener market is moderately consolidated. Global giants like Tate and Lyle Plc, Cargill Incorporated, Archer Daniels Midland Company, Ingredion Incorporated, and Roquette dominate the supply chains for starch and high-intensity sweeteners. They achieve this through vertically integrated production and strong customer ties. Meanwhile, regional players like Al Khaleej Sugar in Dubai and Saudi Arabia's Savola Group leverage their proximity to raw material sources and long-term contracts with food and beverage manufacturers to maintain their sucrose volumes. As patents for aspartame and sucralose expire, generic competition is intensifying. This shift is squeezing margins for innovators who once thrived on royalty streams, pushing them to pivot strategically towards next-gen sweeteners with robust intellectual property protection.

Biotech firms like SweeGen, Amyris, and Sweegen are seizing opportunities in precision fermentation. By licensing high-purity stevia glycoside production processes to established suppliers, they're carving a niche in premium beverage segments where taste justifies a price premium. Technology is becoming a key differentiator. Companies are pouring investments into enzymatic conversion platforms for rare sugars and fermentation methods for next-gen sweeteners, aiming for functional parity with sucrose but at lower caloric values. Kerry Group and DuPont-IFF are at the forefront, using taste-masking technologies and enzyme solutions to assist food manufacturers. Their goal is to mitigate sensory challenges linked to high-intensity sweeteners, positioning themselves as essential formulation partners rather than mere commodity suppliers.

Smaller players like Tiba Starch and Sweeteners in Egypt and Nile Valley Foods in Sudan are carving out their space. They primarily compete on cost and local insights, catering to price-sensitive segments where multinationals struggle. The evolving competitive landscape indicates that future gains will favor suppliers adept at navigating regulatory complexities, investing in sensory technologies, and providing adaptable formulation support. This approach will cater to the diverse needs of beverage, bakery, and dairy sectors, all while considering regional consumer preferences and regulatory landscapes.

Middle East And Africa Food Sweetener Industry Leaders

-

Tate and Lyle Plc

-

Cargill Incorporated

-

Archer Daniels Midland Company

-

Ingredion Incorporated

-

Tereos S.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Ingredion Incorporated introduced its latest sugar reduction innovation at Gulfood Manufacturing 2025 in Dubai. The company launched DULCENT sweetener solutions, designed to support manufacturers in balancing taste, cost-effectiveness, and consumer appeal.

- February 2025: Archer Daniels Midland (ADM), a global leader in food processing and nutrition, has officially launched its latest facility at the Lagos Free Trade Zone (LFZ), Nigeria. This facility is designed to serve as a hub for innovation and collaboration, leveraging LFZ's strategic location, modern infrastructure, and business-friendly environment.

- November 2024: Tate and Lyle has launched a new range of sweetener and stabilizer solutions tailored for the Middle Eastern food and beverage industry, aiming to improve taste, texture, and nutritional quality in products across the region. This latest product range includes EUOLIGO FOS, a non-GMO dietary fiber, and TASTEVA M, a stevia-based sweetener, designed to cater to the increasing demand for healthier, reduced-sugar options.

Middle East And Africa Food Sweetener Market Report Scope

By Product Type

| Sucrose (Common Sugar) | |

| Starch Sweeteners and Sugar Alcohols | Dextrose |

| High-Fructose Corn Syrup (HFCS) | |

| Maltodextrin | |

| Sorbitol | |

| Xylitol | |

| Erythritol | |

| Other Sugar Alcohols | |

| High-Intensity Sweeteners (HIS) | Sucralose |

| Aspartame | |

| Saccharin | |

| Neotame | |

| Stevia | |

| Acesulfame-K | |

| Cyclamate | |

| Other HIS | |

| Others |

By Source

| Artificial |

| Plant-based |

| Fermentation/Bio-engineered |

By Form

| Solid |

| Liquid/Syrup |

By Application

| Food | Bakery and Confectionery |

| Dairy and Desserts | |

| Meat and Savory Products | |

| Nutraceuticals and Functional Foods | |

| Sauces, Dressings and Spreads | |

| Other Processed Foods | |

| Beverages | Soft drinks |

| RTD Tea and Coffee | |

| Juices | |

| Energy and Sports Drinks |

By Country

| Others |

| United Arab Emirates |

| Saudi Arabia |

| South Africa |

| Egypt |

| Nigeria |

| Rest of Middle East and Africa |

| By Product Type | Sucrose (Common Sugar) | |

| Starch Sweeteners and Sugar Alcohols | Dextrose | |

| High-Fructose Corn Syrup (HFCS) | ||

| Maltodextrin | ||

| Sorbitol | ||

| Xylitol | ||

| Erythritol | ||

| Other Sugar Alcohols | ||

| High-Intensity Sweeteners (HIS) | Sucralose | |

| Aspartame | ||

| Saccharin | ||

| Neotame | ||

| Stevia | ||

| Acesulfame-K | ||

| Cyclamate | ||

| Other HIS | ||

| Others | ||

| By Source | Artificial | |

| Plant-based | ||

| Fermentation/Bio-engineered | ||

| By Form | Solid | |

| Liquid/Syrup | ||

| By Application | Food | Bakery and Confectionery |

| Dairy and Desserts | ||

| Meat and Savory Products | ||

| Nutraceuticals and Functional Foods | ||

| Sauces, Dressings and Spreads | ||

| Other Processed Foods | ||

| Beverages | Soft drinks | |

| RTD Tea and Coffee | ||

| Juices | ||

| Energy and Sports Drinks | ||

| By Country | Others | |

| United Arab Emirates | ||

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Middle East and Africa food sweetener market?

The market stands at USD 7.75 billion in 2026 and is forecast to reach USD 9.37 billion by 2031.

Which country contributes the largest revenue?

Saudi Arabia leads with 35.55% of regional revenue owing to its sizeable beverage and processed-food sectors.

Why are beverage formulations changing so rapidly?

A four-tier GCC sugar tax effective in 2026 penalizes high-sugar drinks, prompting manufacturers to switch to high-intensity and rare-sugar sweeteners.

Which sweetener types are growing fastest?

High-intensity sweeteners such as sucralose and plant-based stevia are expanding at a 4.06% CAGR through 2031.

Page last updated on: