Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

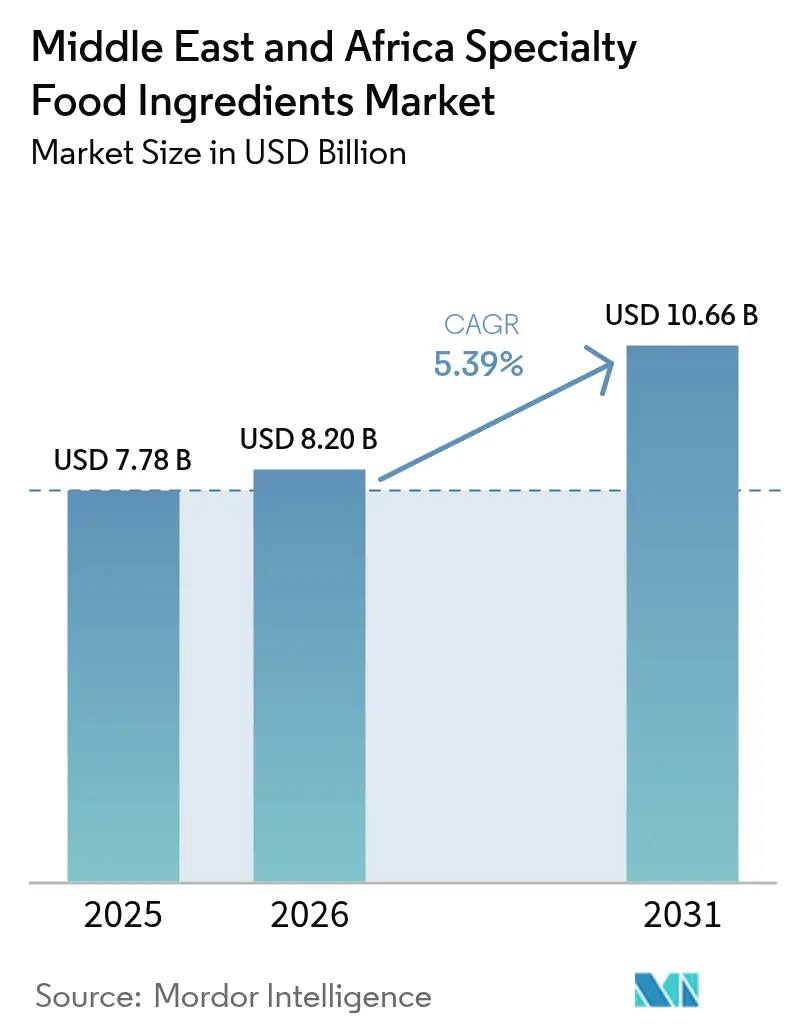

| Base Year Market Size (2025) | USD 7.78 Billion |

| Market Size (2026) | USD 8.2 Billion |

| Market Size (2031) | USD 10.66 Billion |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Specialty Food Ingredients Market Analysis by Mordor Intelligence

The Middle East and Africa specialty food ingredients market size was valued at USD 7.78 billion in 2025 and estimated to grow from USD 8.2 billion in 2026 to reach USD 10.66 billion by 2031, at a CAGR of 5.39% during the forecast period (2026-2031). This trajectory reflects a structural shift as governments mandate fortification to address micronutrient deficiencies while consumers increasingly demand functional benefits beyond basic nutrition. Saudi Arabia's requirement that all milk products contain vitamin D, implemented by the Saudi Food and Drug Authority in 2024, exemplifies how regulatory intervention is converting optional enrichment into baseline compliance [1]Source: SFDA, "Regulatory Intervention", sfda.gov.sa. The UAE's Nutri-Mark front-of-pack labeling system, launched in November 2024 with mandatory adoption by mid-2025, is pushing manufacturers to reformulate with cleaner ingredient profiles [2]Source: UAE Ministry of Health, "Nutri-Mark front-of-pack labeling system", mohap.gov.ae. Investment incentives under Saudi Vision 2030 and the UAE Food Security Strategy 2051 are stimulating domestic production capacity, gradually reducing dependence on European and Asian suppliers. Supply-chain upgrades, including temperature-controlled logistics and regional ingredient hubs, are enabling faster product launches across the Middle East and Africa specialty food ingredients market, even as manufacturers navigate divergent national standards and certification regimes.

Key Report Takeaways

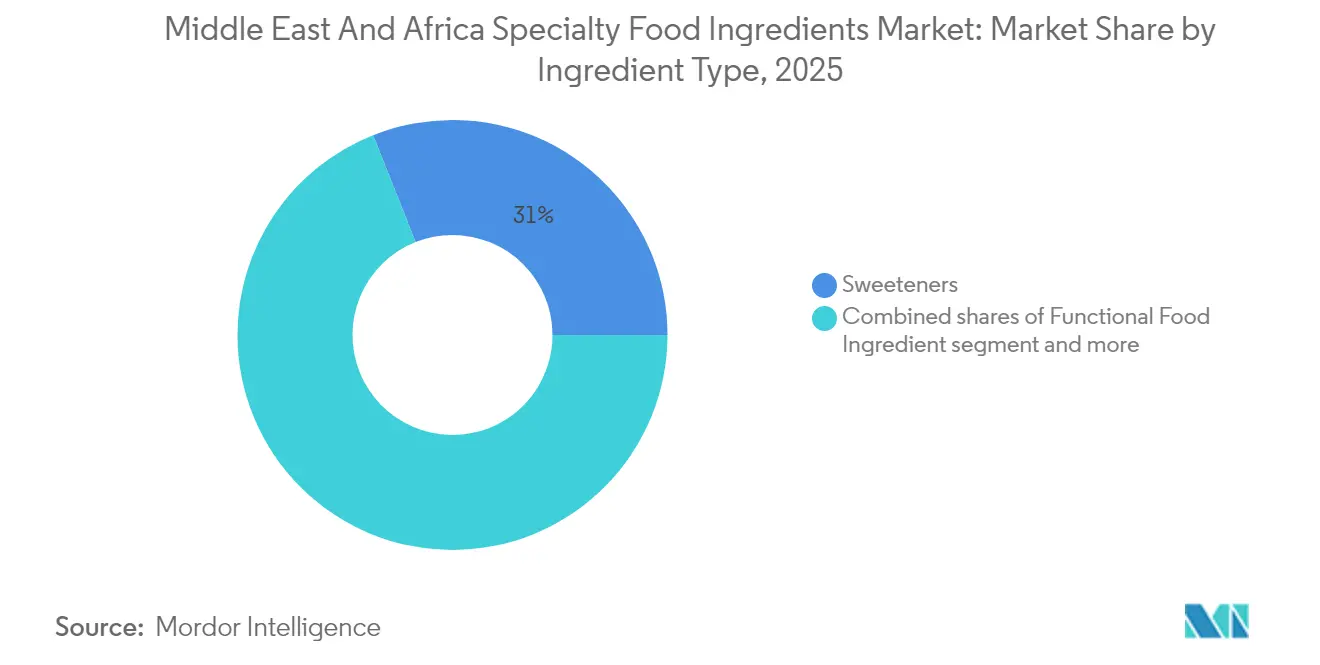

- Sweeteners captured 31.02% of the Middle East and Africa specialty food ingredients market share in 2025, Functional food ingredients are forecast to grow at a 6.48% CAGR to 2031.

- Powder and granular forms accounted for 66.78% of 2025 revenue; the liquid segment is projected to climb at 6.82% CAGR through 2031.

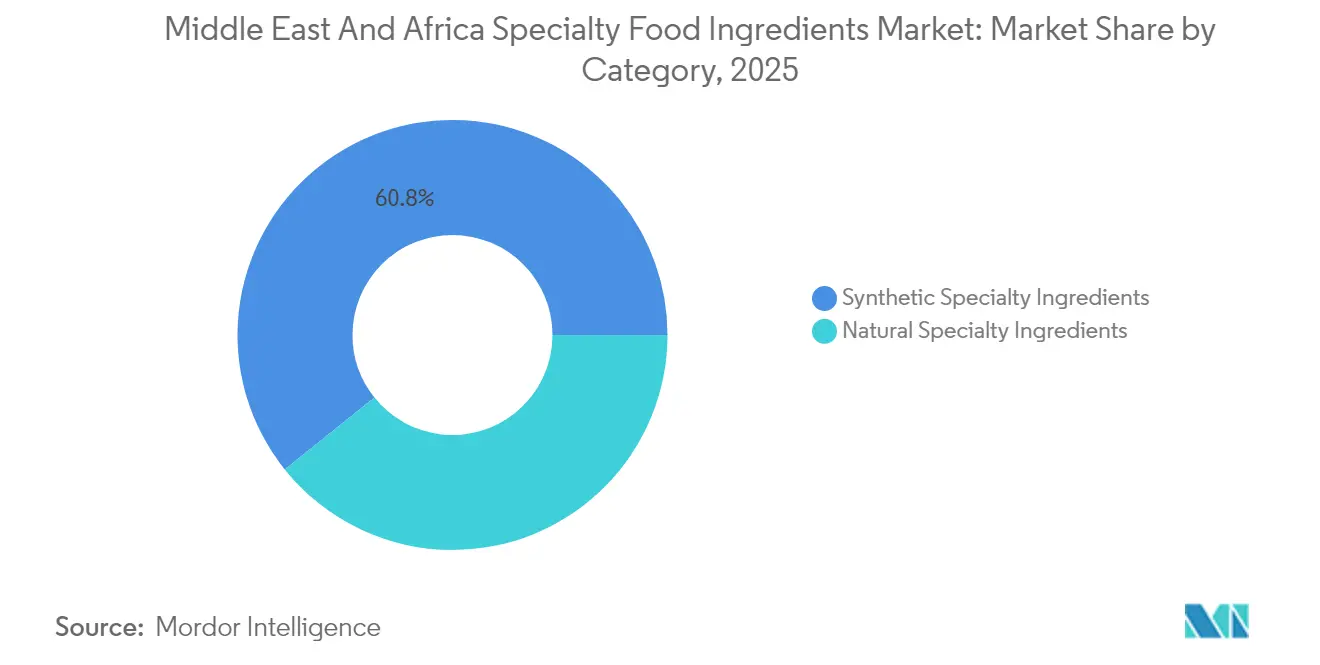

- Synthetic sources still held 60.75% share in 2025, but natural alternatives are expanding at a 6.12% CAGR.

- Beverages led applications with 29.72% revenue in 2025, whereas dairy products are forecast to post the highest 6.05% CAGR to 2031.

- South Africa generated 22.08% of 2025 regional revenue, while Nigeria is expected to record a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Specialty Food Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand for healthier, functional food options | +1.2% | Saudi Arabia, UAE, South Africa, with spillover to urban Nigeria | Medium term (2-4 years) |

| Local flavor traditions plus globalization | +0.8% | Saudi Arabia, UAE (date-based ingredients), South Africa (rooibos), Nigeria (indigenous crops) | Long term (≥ 4 years) |

| Strong bakery and bread culture | +0.9% | Middle East (flatbreads, pita), North Africa (baguettes), Sub-Saharan Africa (fortified bread programs) | Short term (≤ 2 years) |

| Demand for fortified staples and affordable nutrition | +1.4% | Nigeria, South Africa, Kenya, Tanzania (government-mandated fortification programs) | Short term (≤ 2 years) |

| Food manufacturers reformulating with bioactive ingredients | +1.0% | UAE, Saudi Arabia, South Africa (clean-label reformulation) | Medium term (2-4 years) |

| Rise in demand for processed/packaged food | +1.1% | Nigeria, Kenya, urban centers across MEA (middle-class expansion) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Healthier, Functional Food Options

Urban populations in Saudi Arabia and the UAE are driving demand for fortified dairy, probiotic beverages, and omega-3-enriched products as chronic disease prevalence rises. The Saudi Ministry of Health reported in 2024 that 35.4% of adults are obese, prompting consumers to seek functional ingredients that deliver tangible health outcomes beyond basic nutrition [3]Source: Saudi Ministry of Health, "Let us serve you better", moh.gov.sa. DSM-Firmenich's vitamin premix sales in the Middle East grew 18% year-over-year in 2024, reflecting manufacturers' shift toward fortification as a competitive differentiator. Probiotic cultures, particularly Lactobacillus and Bifidobacterium strains, are being incorporated into yogurt and fermented milk drinks, with South Africa's dairy sector mandating vitamin A and D fortification to address micronutrient deficiencies. This trend is creating premium pricing opportunities for ingredient suppliers who can demonstrate clinical efficacy through peer-reviewed studies.

Local Flavor Traditions Plus Globalization

Date syrup and date sugar are gaining traction as natural sweeteners in Saudi Arabia and the UAE, leveraging regional agricultural heritage while meeting clean-label demands. A 2024 study published in the Journal of Food Science documented date syrup's lower glycemic index compared to sucrose, positioning it as a functional sweetener for diabetic consumers. South African rooibos extract is being adopted in functional beverages across the Gulf Cooperation Council for its antioxidant properties, while Nigerian manufacturers are exploring Bambara nuts and cowpea as protein sources for fortified snacks. Ingredion's launch of FIBERTEX citrus fiber in EMEA in May 2024 exemplifies how global suppliers are adapting formulations to accommodate regional taste preferences while delivering functional benefits like improved satiety. This fusion of local and global flavors is expanding the addressable market for specialty ingredients beyond commodity sweeteners and preservatives.

Demand for Fortified Staples and Affordable Nutrition

Micronutrient deficiencies remain widespread across Sub-Saharan Africa, with the World Health Organization estimating that 42% of children under 5 in Nigeria are stunted due to inadequate nutrition. Government-mandated fortification of maize flour, edible oils, and salt is driving volume growth for vitamin A, iron, and iodine premixes, with Nigeria's National Agency for Food and Drug Administration and Control enforcing compliance across domestic and imported products. South Africa's fortification program, operational since 2003, has reduced neural tube defects by 31%, demonstrating the public health impact that justifies regulatory mandates. Kerry Group's taste and nutrition center in Dubai, opened in 2022, is formulating cost-effective micronutrient blends that maintain organoleptic properties in fortified staples, addressing the challenge of metallic off-flavors from iron compounds. This driver is creating predictable, regulation-driven demand that insulates ingredient suppliers from discretionary spending cycles.

Rise in Demand for Processed/Packaged Food

Nigeria's middle class is projected to reach 58 million by 2030, driving consumption of packaged snacks, beverages, and dairy products that require specialty ingredients for shelf stability and sensory appeal. Cold chain infrastructure remains limited outside major urban centers, placing a premium value on emulsifiers, stabilizers, and preservatives that maintain product integrity at ambient temperatures. Symrise's acquisition of Probi probiotics in 2023 positions it to supply shelf-stable probiotic strains for ambient yogurt drinks popular in West Africa. The UAE's food service sector, which grew 12% in 2024, is demanding clean-label emulsifiers and enzymes for industrial bakery and dairy applications. This urbanization-driven trend is creating sustained volume growth for specialty ingredients that enable processed food manufacturers to compete on convenience and shelf life.

Restraints Impact Analysis*

| Restraint | () % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost of specialty food ingredients | -0.9% | Global, with an acute impact in Nigeria and Kenya due to currency depreciation | Short term (≤ 2 years) |

| Stringent regulatory compliance requirements hinders growth | -0.6% | Saudi Arabia (SFDA), UAE (ESMA), South Africa (SABS), Nigeria (NAFDAC) | Medium term (2-4 years) |

| Supply chain complexities for niche ingredient sourcing | -0.5% | Sub-Saharan Africa (infrastructure gaps), landlocked countries (transit delays) | Long term (≥ 4 years) |

| Short shelf life and stability challenges of ingredients | -0.4% | High-temperature regions (Gulf states, Sub-Saharan Africa) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production Cost of Specialty Food Ingredients

Raw material price volatility is compressing margins for ingredient manufacturers and limiting adoption of premium functional ingredients. Cocoa prices surged to USD 10,000 per ton in April 2024, driven by crop failures in Côte d'Ivoire and Ghana, forcing confectionery manufacturers to reduce cocoa content or switch to compound coatings. Vanilla extract prices climbed 25-30% in 2024 due to cyclone damage in Madagascar, prompting flavor houses to develop synthetic vanillin blends that sacrifice clean-label positioning for cost control. Palm oil price fluctuations directly impact emulsifier costs, with Malaysian palm oil futures averaging 15% higher in 2024 compared to 2023. Currency depreciation in Nigeria and Kenya is amplifying import costs for specialty ingredients, with the naira losing 42% against the dollar in 2024, making locally produced alternatives increasingly competitive despite quality gaps.

Stringent Regulatory Compliance Requirements Hinders Growth

Divergent regulatory frameworks across the Middle East and Africa impose duplicative testing and certification costs on ingredient suppliers. Saudi Arabia's SFDA requires separate registration for each ingredient variant, with approval timelines extending 6-9 months, delaying product launches and increasing working capital requirements. The Gulf Cooperation Council Standardization Organization has harmonized some food standards, but individual member states retain discretion over additive approvals, forcing suppliers to navigate country-specific dossiers. South Africa's SABS mandates compliance with Codex Alimentarius standards but adds local testing requirements that can add USD 50,000-100,000 per ingredient to market entry costs. Halal certification from recognized bodies like JAKIM (Malaysia) or ESMA (UAE) is effectively mandatory for Gulf markets, requiring dedicated production lines and traceability systems that smaller suppliers struggle to afford.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Functional Fortification Drives Premium Shift

Functional food ingredients will expand at 6.48% CAGR through 2031, outpacing the overall market as governments mandate micronutrient enrichment and consumers seek health benefits beyond basic nutrition. Vitamins and minerals dominate this segment, driven by Saudi Arabia's requirement for vitamin D in all milk products and Tanzania's fortification of wheat and maize flour with iron and folic acid. Omega-3 ingredients are gaining traction in premium dairy and bakery products, with encapsulation technology improving oxidative stability in high-temperature climates. Probiotic cultures, particularly Lactobacillus and Bifidobacterium strains, are being incorporated into yogurt and fermented beverages, though cold chain limitations constrain adoption in rural markets. Amino acids like lysine and methionine are finding application in fortified porridges and infant nutrition products across Sub-Saharan Africa.

Sweeteners commanded 31.02% market share in 2025, reflecting their ubiquity in beverages, confectionery, and bakery applications, but growth is moderating as sugar taxes reshape consumption patterns. Saudi Arabia's 50% tax on sweetened beverages and 100% levy on energy drinks, implemented in 2024, is accelerating substitution toward natural sweeteners like stevia, monk fruit, and date syrup. Food flavors and enhancers are experiencing steady demand as manufacturers reformulate to mask off-flavors from fortification minerals and natural preservatives. Preservatives face headwinds as clean-label preferences drive substitution toward natural alternatives like rosemary extract and fermented ingredients, with Corbion's Verdad line capturing share from sodium benzoate. Emulsifiers, colorants, and enzymes serve specialized applications, with Novonesis reporting 22% growth in bakery enzyme sales in Africa during 2024 as artisanal bakers adopt clean-label dough conditioners.

By Form: Powder Dominance Reflects Climate Realities

Liquid formats will grow at 6.82% CAGR through 2031, driven by beverage reformulation and enzyme applications in dairy processing, yet powder and granular forms held 66.78% market share in 2025 due to superior shelf stability in high-temperature distribution networks. The Middle East and Africa's ambient temperatures, often exceeding 40°C during summer months, accelerate degradation of liquid ingredients, making powder formats the default choice for vitamins, minerals, and flavor compounds. Microencapsulation technology is enabling powder formats for previously liquid-only ingredients like omega-3 oils and probiotics, with DuPont's Danisco HOLDBAC YM-C culture offering improved heat tolerance in powder form. Reconstitution challenges in hard water regions are driving innovation in instant-dispersible powders that maintain functionality across varying water quality.

Liquid ingredients are gaining share in applications where immediate solubility and uniform dispersion are critical, particularly enzyme solutions for dairy and bakery processing. Kerry Group's taste and nutrition center in Dubai is formulating liquid flavor systems optimized for beverage reformulation, where powder formats can cause sedimentation or cloudiness. Liquid emulsifiers and stabilizers are preferred in industrial bakery applications for consistent dough handling properties. The beverage sector's 29.72% market share in 2025 is supporting liquid ingredient growth, as manufacturers adopt liquid sweetener blends and flavor systems that integrate seamlessly into production lines. Cold chain expansion in urban centers is gradually reducing the shelf-life disadvantage of liquid formats, though rural distribution remains powder-dominated.

By Category: Natural Gains Ground Despite Cost Premium

Natural specialty ingredients will expand at a 6.12% CAGR through 2031, closing the gap with synthetic alternatives that held 60.75% market share in 2025. Clean-label preferences are reshaping ingredient selection, with the UAE's Nutri-Mark front-of-pack labeling system incentivizing manufacturers to reformulate with recognizable, natural ingredients. Rosemary extract and green tea extract are replacing synthetic antioxidants in meat and dairy applications, with South African processors reporting 15-20% longer refrigerated shelf life compared to BHA and BHT. Givaudan's acquisition of DDW natural colors in 2023 reflects strategic positioning for the clean-label transition, as synthetic azo dyes face regulatory scrutiny. Date-based sweeteners, rooibos extract, and indigenous African crops like Bambara nuts are creating differentiation opportunities for regional suppliers.

Synthetic ingredients retain the majority share due to cost advantages and functional consistency, particularly in price-sensitive markets like Nigeria and Kenya, where affordability outweighs clean-label preferences. Synthetic vitamins and minerals cost 30-50% less than natural equivalents, making them the default choice for government-mandated fortification programs targeting low-income populations. Aspartame and acesulfame-K remain dominant in sugar-free beverages despite consumer skepticism, as natural sweeteners like stevia require higher usage rates and can impart bitter aftertastes. Halal certification requirements in the Gulf Cooperation Council are constraining synthetic ingredient choices, as alcohol-based extraction processes disqualify otherwise compliant ingredients. The cost-performance trade-off will continue favoring synthetic ingredients in staple fortification while natural alternatives capture premium segments.

By Application: Dairy Fortification Accelerates

Dairy products will post 6.05% CAGR through 2031, driven by mandatory vitamin D fortification in Saudi Arabia and probiotic innovation across the region, yet beverages commanded 29.72% market share in 2025 as the largest application segment. Sugar reduction mandates are reshaping beverage formulations, with Saudi Arabia's 50% tax on sweetened drinks accelerating adoption of natural sweeteners and functional ingredients that deliver health positioning. Functional beverages enriched with vitamins, minerals, and probiotics are capturing share from traditional carbonated soft drinks, with DSM-Firmenich reporting 18% growth in Middle East vitamin premix sales during 2024. Ambient-stable probiotic strains are enabling yogurt drinks that bypass cold chain constraints in West Africa, with Symrise's Probi acquisition in 2023 targeting this opportunity.

Bakery and confectionery applications are benefiting from the region's strong bread culture, with enzyme technologies extending shelf life and improving dough handling in high-temperature climates. Novonesis reported 22% growth in African bakery enzyme sales during 2024, as artisanal bakeries replace chemical dough conditioners with clean-label amylases and xylanases. Fortification of wheat flour with iron, folic acid, and B vitamins creates captive demand for micronutrient premixes, with Tanzania's 2024 National Nutrition Survey revealing that fortified flour reaches 68% of rural households. Meat, poultry, and seafood applications are adopting natural preservatives like nisin and rosemary extract to extend refrigerated shelf life, addressing cold chain limitations in distribution networks. Other applications, including sauces, dressings, and snacks, are incorporating emulsifiers and stabilizers to maintain texture and prevent separation in ambient storage conditions.

Geography Analysis

South Africa captured 22.08% of regional revenue in 2025, anchored by its established food processing infrastructure and compliance with South African Bureau of Standards fortification protocols that mandate vitamin A and iron enrichment in maize meal and wheat flour. The country's dairy sector is incorporating probiotic cultures and vitamin D to address micronutrient deficiencies, with local manufacturers partnering with DSM-Firmenich and Kerry Group for premix formulations. Rooibos extract is emerging as a regional specialty ingredient, leveraging South Africa's monopoly on this crop for antioxidant applications in functional beverages. However, currency volatility and electricity load-shedding are constraining manufacturing capacity, with ingredient suppliers reporting production disruptions that extend lead times by 2-3 weeks. The South African market is mature relative to the broader region, with growth driven by premiumization and clean-label reformulation rather than volume expansion.

Nigeria will surge at 7.11% CAGR through 2031, propelled by a rapidly expanding middle class projected to reach 58 million by 2030 and government mandates for fortification of wheat flour, maize flour, vegetable oil, and sugar. The National Agency for Food and Drug Administration and Control enforces compliance across domestic and imported products, creating predictable demand for vitamin A, iron, and iodine premixes. Cold chain limitations constrain the adoption of probiotic and enzyme ingredients outside Lagos and Abuja, though microencapsulation technology is improving ambient stability. Local production incentives are attracting investment in ingredient manufacturing, with the Nigerian government offering tax holidays and import duty waivers for food processing facilities.

Saudi Arabia and the UAE are driving premiumization trends, with Vision 2030 targeting 85% food self-sufficiency and the UAE's Food Security Strategy 2051 prioritizing local ingredient production. Saudi Arabia's mandatory vitamin D fortification of milk and 50% sugar tax on sweetened beverages are reshaping ingredient demand, with natural sweeteners like date syrup and stevia gaining share. The UAE's Nutri-Mark front-of-pack labeling system, launched in November 2024, is accelerating clean-label reformulation and creating demand for natural preservatives and emulsifiers. Ingredion's Dubai innovation center and Kerry Group's taste and nutrition facility are supporting regional manufacturers with localized formulations that accommodate halal requirements and high-temperature stability needs. The Rest of Middle East and Africa, encompassing Kenya, Tanzania, Ethiopia, and North African countries, exhibits heterogeneous regulatory environments but shares common challenges of infrastructure gaps and cold chain limitations that favor powder formats and ambient-stable ingredients.

Competitive Landscape

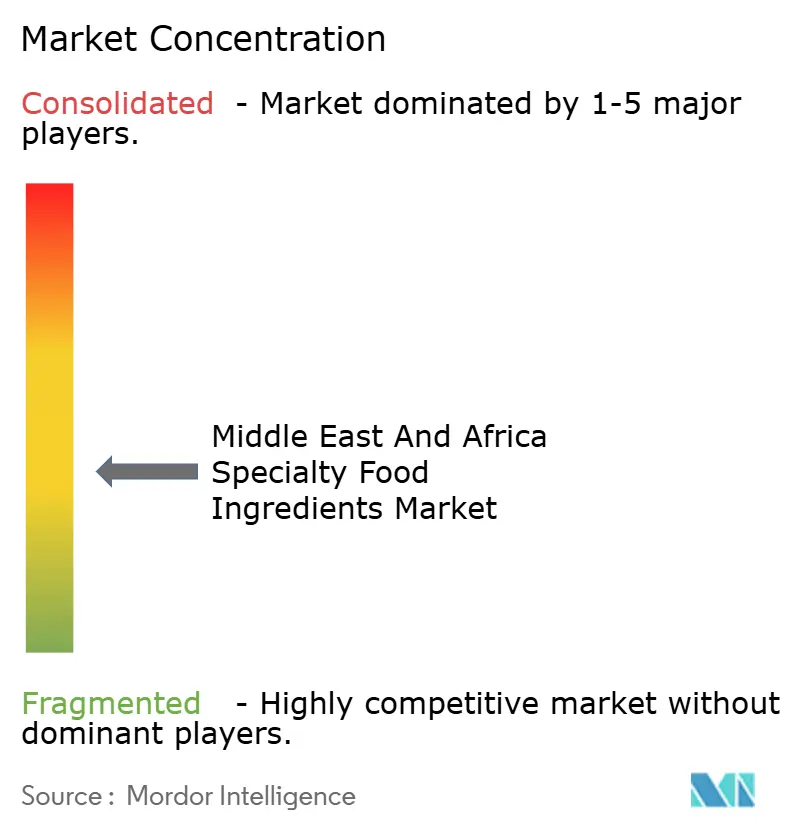

The Middle East and Africa specialty food ingredients market exhibits moderate fragmentation, as global multinationals leverage scale economies and R&D capabilities while regional specialists capture niche segments through halal certification and indigenous ingredient expertise. Cargill, Archer Daniels Midland, and DuPont dominate fortification premixes and commodity sweeteners, but clean-label reformulation is creating openings for agile suppliers offering natural preservatives and functional ingredients. ADM's USD 230 million acquisition of Deerland Probiotics & Enzymes in October 2024 signals a strategic pivot toward high-margin functional ingredients that align with government fortification mandates and consumer health trends.

Novonesis, formed from the January 2024 merger of Chr. Hansen and Novozymes, is leveraging combined enzyme and probiotic portfolios to offer integrated solutions for dairy and bakery applications, reporting 22% growth in African enzyme sales during 2024. Opportunities exist in thermostable probiotic strains for ambient yogurt drinks, natural emulsifiers for industrial bakery, and date-based sweeteners that bridge clean-label and regional flavor preferences. Kerry Group's acquisition of c-LEcta enzyme technology in 2024 targets thermostable variants that maintain activity at elevated temperatures, addressing a critical pain point for MEA manufacturers operating without reliable cold chain infrastructure.

Smaller players are differentiating through halal certification from recognized bodies like JAKIM and ESMA, which requires dedicated production lines and traceability systems that impose barriers to entry. Corbion's Verdad N6 natural mold inhibitor, based on fermented wheat flour, exemplifies how technology-driven innovation can displace synthetic preservatives and capture premium pricing. Regulatory compliance remains a competitive moat, with SFDA registration timelines of 6-9 months in Saudi Arabia and country-specific dossiers across the Gulf Cooperation Council favoring established suppliers with local regulatory expertise.

Middle East And Africa Specialty Food Ingredients Industry Leaders

-

Cargill, Incorporated

-

Tate & Lyle PLC

-

The Archer Daniels Midland Company

-

DSM‑Firmenich

-

Ingredion

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Tate & Lyle introduced a new range of sweetener (Tasteva M) and dietary fiber (Euoligo FOS) solutions tailored for Middle Eastern food & beverage manufacturers, supporting sugar reduction and improved texture in products.

- October 2023: Ingredion, in collaboration with Univar, launched new natural, plant-based, and sugar-reduction ingredient solutions in the Middle East, addressing consumer demand for healthier food formulations (sweeteners/functional).

Middle East And Africa Specialty Food Ingredients Market Report Scope

Specialty food ingredients offer technological and functional benefits and are essential in providing today's consumers with a wide range of tasty, safe, healthy, affordable, qualitative, and sustainably produced food. The Middle East and Africa specialty food ingredients market is segmented by ingredient type, category, application, and geography. By ingredient type, the market is segmented into sweeteners, food flavors and enhancers, emulsifiers, and more. By form, the market is segmented into powder/granular and liquid. By category, the market is segmented into synthetic specialty ingredients and more. By application, the market is segmented into bakery and confectionery, beverages, meat, and more. By geography, the market is segmented into South Africa, Saudi Arabia, And More. The market forecasts are provided in terms of value (USD).

By Ingredient Type

| Functional Food Ingredient | Vitamins |

| Minerals | |

| Amino Acids | |

| Omega‑3 Ingredients | |

| Probiotic Cultures | |

| Other Functional Food Ingredients | |

| Sweetener | |

| Food Flavors and Enhancers | |

| Preservatives | |

| Emulsifiers | |

| Colorants | |

| Enzymes | |

| Other Product Types |

By Form

| Powder/Granular |

| Liquid |

By Category

| Synthetic Specialty Ingredients |

| Natural Specialty Ingredients |

By Application

| Bakery and Confectionery |

| Beverages |

| Meat, Poultry, and Seafood |

| Dairy Products |

| Other Applications |

By Geography

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Rest of Middle East and Africa |

| By Ingredient Type | Functional Food Ingredient | Vitamins |

| Minerals | ||

| Amino Acids | ||

| Omega‑3 Ingredients | ||

| Probiotic Cultures | ||

| Other Functional Food Ingredients | ||

| Sweetener | ||

| Food Flavors and Enhancers | ||

| Preservatives | ||

| Emulsifiers | ||

| Colorants | ||

| Enzymes | ||

| Other Product Types | ||

| By Form | Powder/Granular | |

| Liquid | ||

| By Category | Synthetic Specialty Ingredients | |

| Natural Specialty Ingredients | ||

| By Application | Bakery and Confectionery | |

| Beverages | ||

| Meat, Poultry, and Seafood | ||

| Dairy Products | ||

| Other Applications | ||

| By Geography | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the Middle East and Africa specialty food ingredients market?

The Middle East and Africa specialty food ingredients market is valued at USD 8.2 billion in 2026 and is forecast to reach USD 10.66 billion by 2031.

Which ingredient type leads sales in the region?

Sweeteners remain ahead, accounting for 31.02% of 2025 revenue across the region.

Why are functional ingredients growing faster than other categories?

Government fortification mandates and rising consumer health awareness are driving a 6.48% CAGR for functional ingredients through 2031.

Page last updated on: